Management Accounting Portfolio: Costing & Financial Analysis

VerifiedAdded on 2023/01/11

|8

|1801

|49

Project

AI Summary

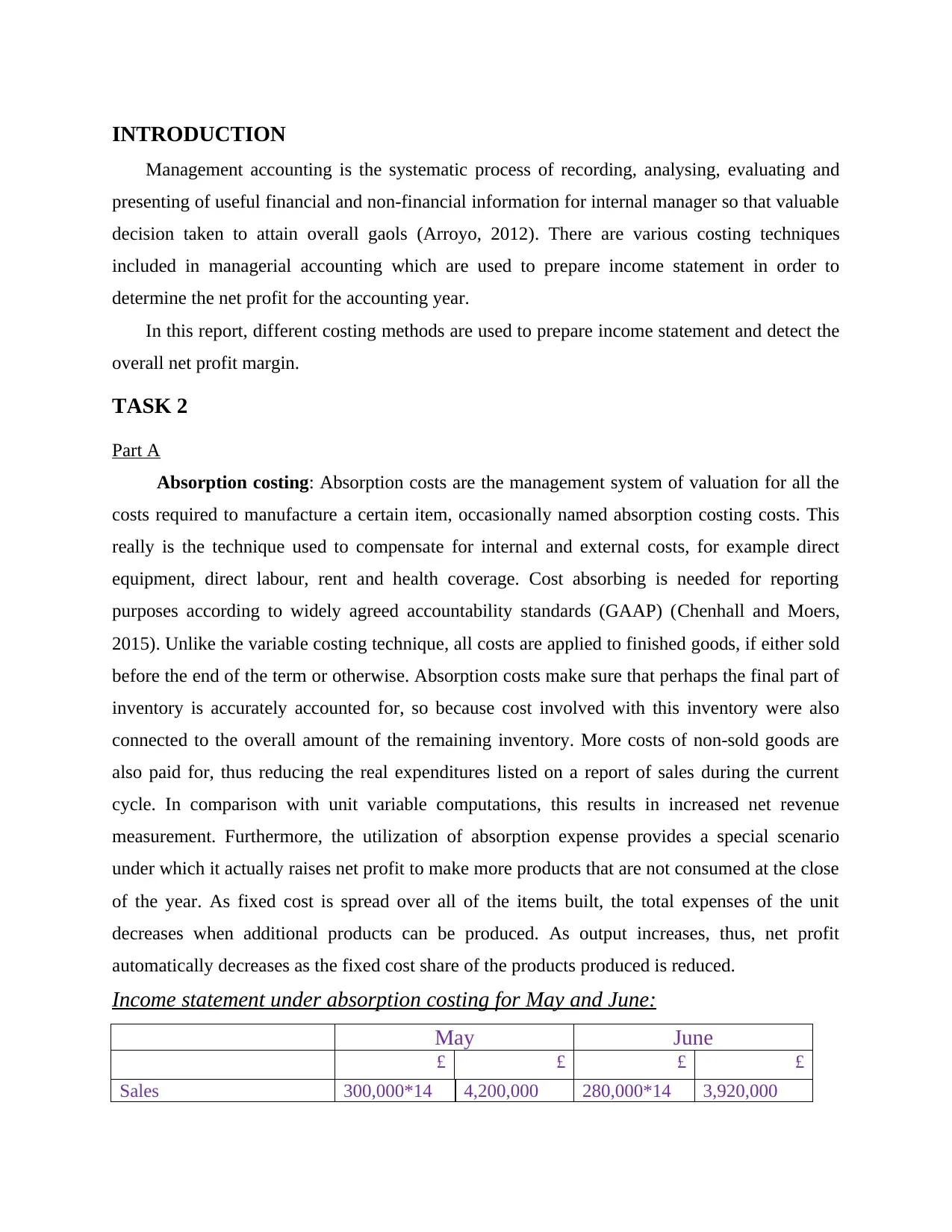

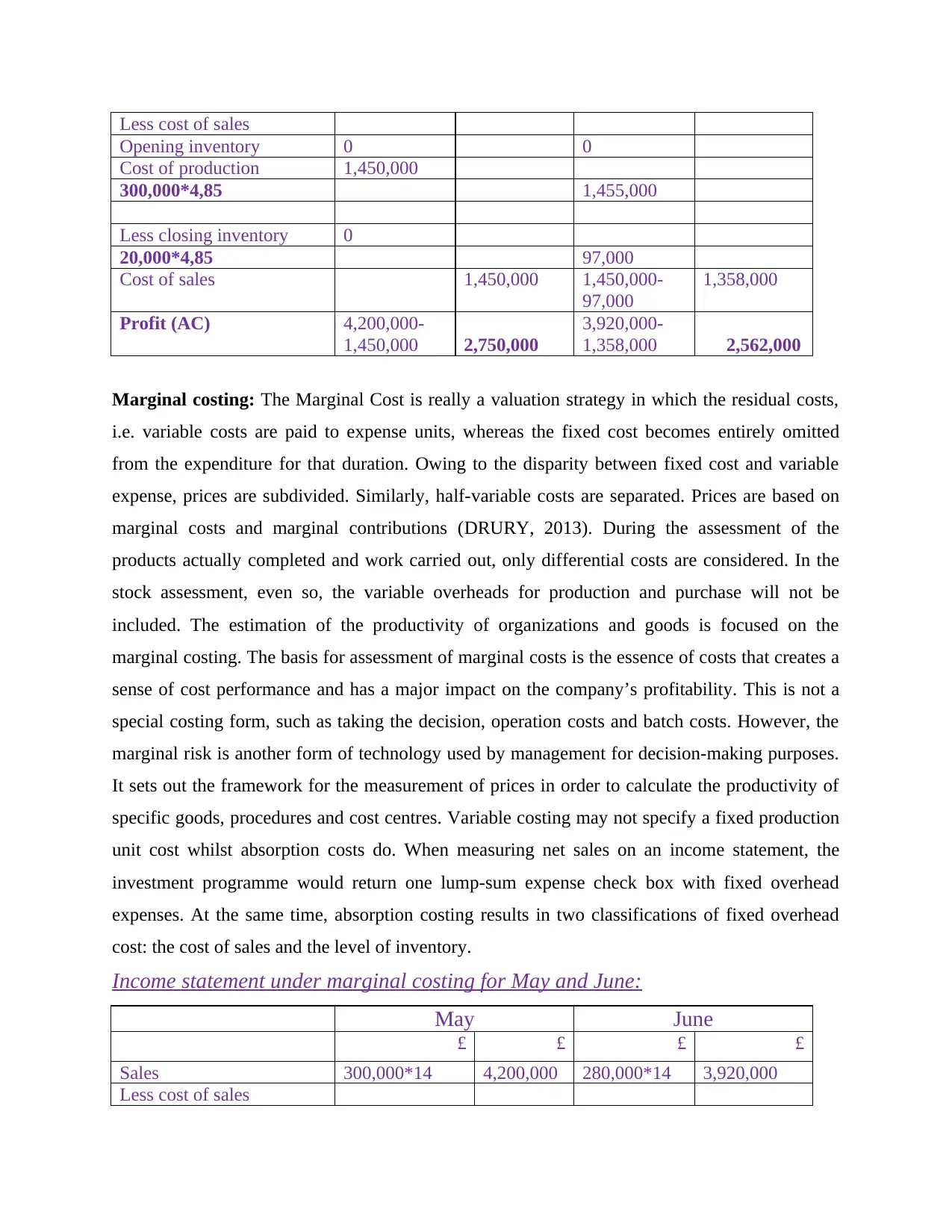

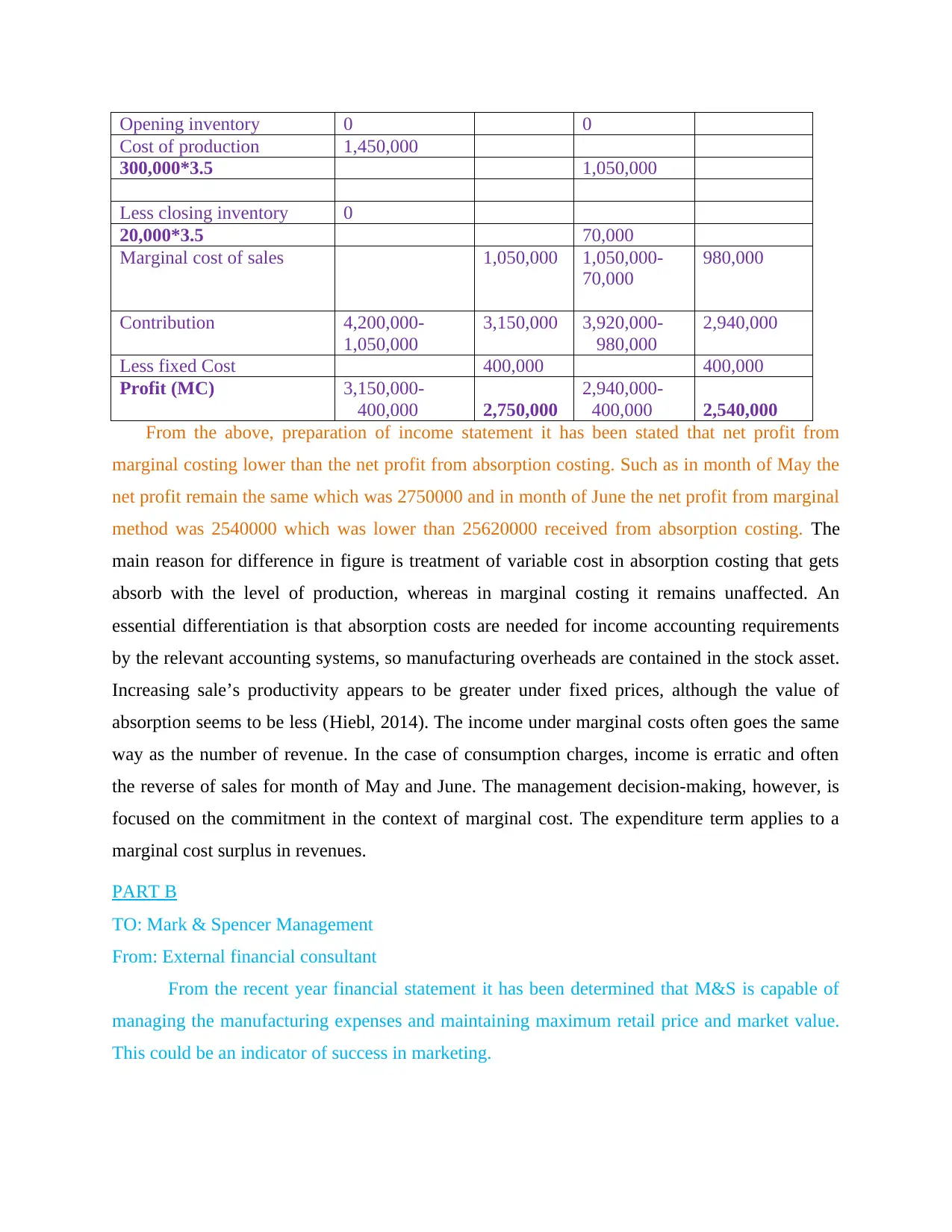

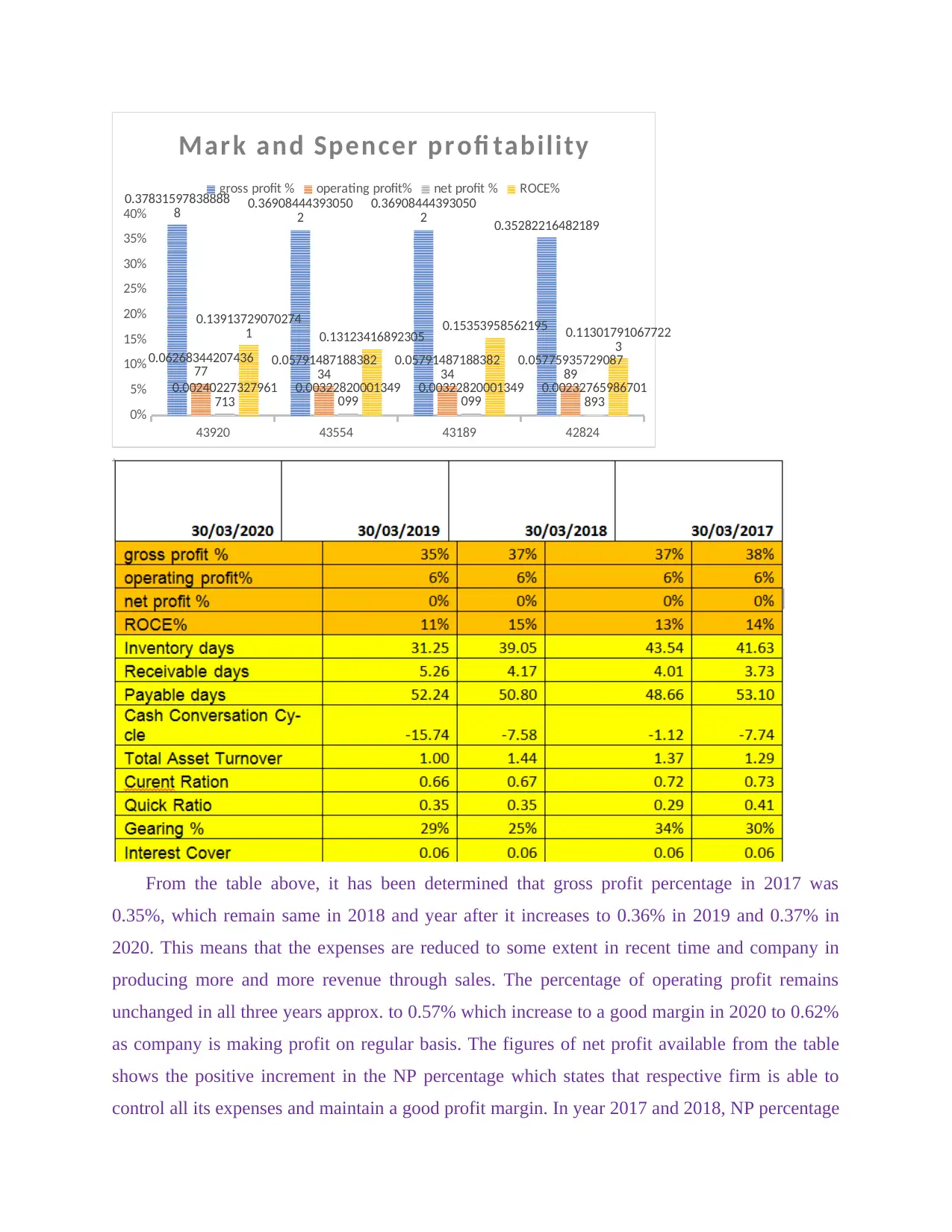

This management accounting portfolio analyzes financial statements and costing methods. The portfolio includes a comparison of absorption and marginal costing methods, with income statements prepared for May and June using both approaches. The analysis highlights the differences in net profit under each method, emphasizing the treatment of fixed and variable costs. Furthermore, the portfolio incorporates a financial analysis of Mark & Spencer (M&S), assessing its profitability, gross profit, operating profit, and return on capital employed (ROCE) over several years. The analysis uses the provided financial data to evaluate M&S's financial performance, including its ability to manage manufacturing expenses, maintain retail prices, and control debt, providing insights into its financial health and performance trends.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.