Management Accounting Homework: Costing Analysis and Interpretation

VerifiedAdded on 2023/01/12

|8

|1151

|24

Homework Assignment

AI Summary

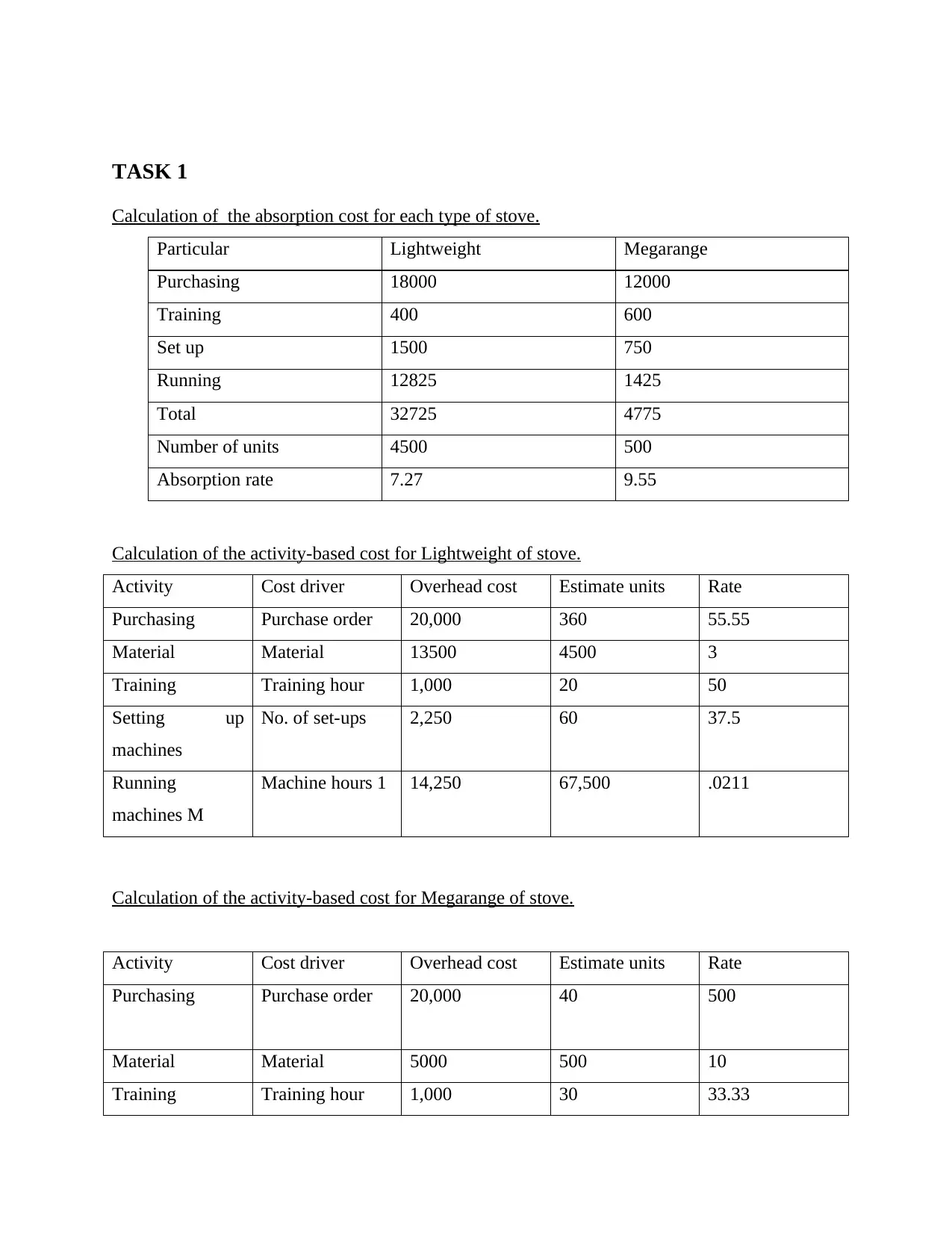

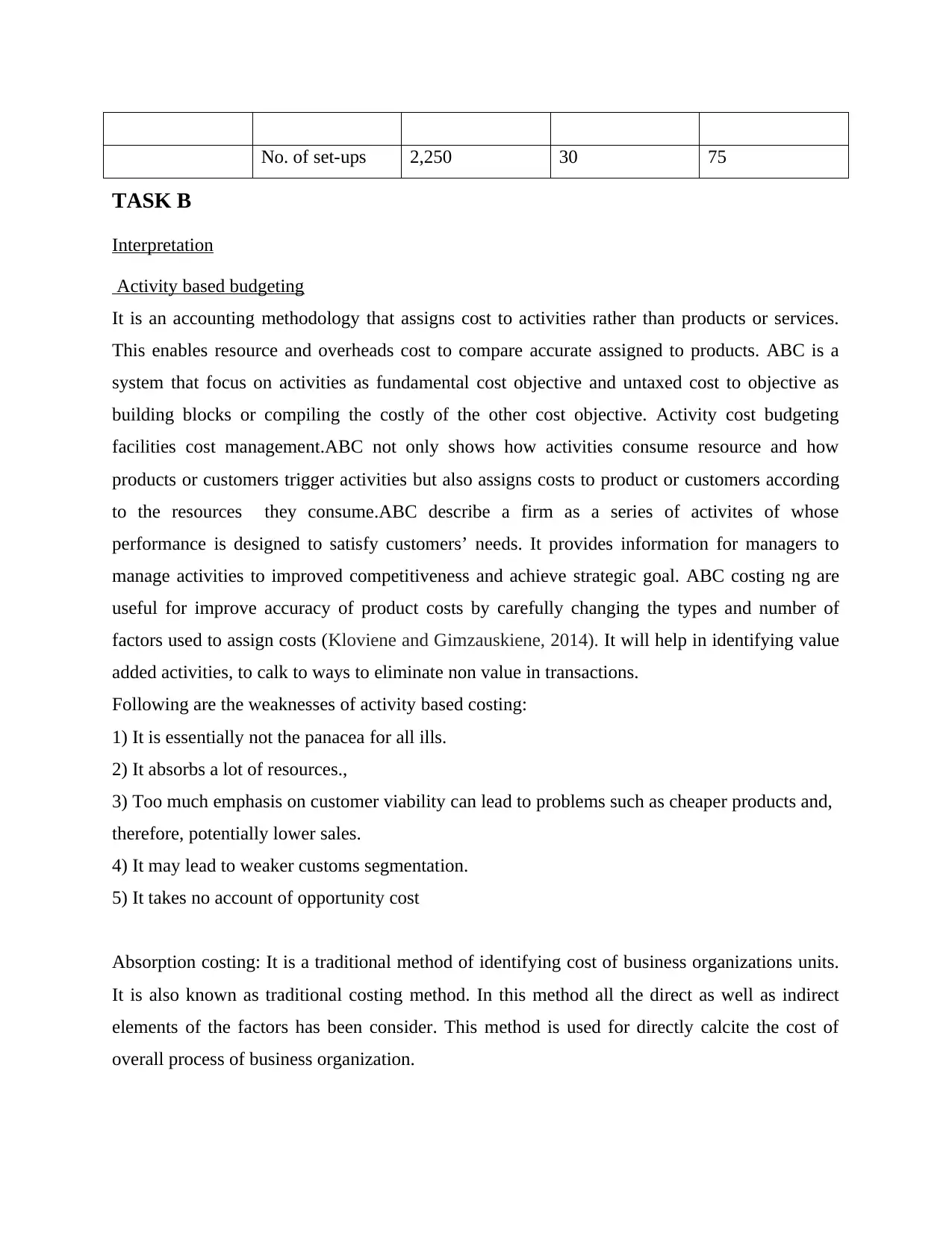

This document presents a comprehensive solution to a management accounting homework assignment, focusing on the calculation and interpretation of absorption and activity-based costing methods. The solution includes detailed calculations for both Lightweight and Megarange stoves, comparing absorption rates and activity-based costs across various activities such as purchasing, material handling, training, and setup. It also provides an interpretation of the results, discussing the advantages and disadvantages of each costing method, particularly highlighting the benefits of activity-based budgeting and its role in cost management. Furthermore, the document explains the differences between absorption costing and activity-based costing, emphasizing how ABC provides a more realistic picture of cost behavior by utilizing activities instead of functional departments. The solution also references relevant literature to support the analysis and findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.