Report on Management Accounting and Financial Analysis for Imda Tech

VerifiedAdded on 2020/06/04

|13

|4028

|92

Report

AI Summary

This report provides a comprehensive analysis of management and financial accounting for Imda Tech (UK), addressing key aspects such as the functions of management accounting, the importance of accounting information, and the differences between management and financial accounting. It delves into various types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report further explores costing methods, specifically absorption and marginal costing, with detailed calculations and income statements for both methods. Additionally, it covers planning tools, various types of budgets like operating and capital budgets and discusses pricing strategies. The report aims to provide the Finance Director of Imda Tech with crucial insights for decision-making and strategic planning, offering a solid foundation for business growth and financial management.

Management and Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1(a) Report on functions of management of management........................................................2

P2(b) Different types of management accounting......................................................................4

TASK 2............................................................................................................................................5

P3 Calculation of absorption and marginal costing methods......................................................5

P3 (i) Income statement under marginal costing........................................................................6

(ii) Income statement of absorption costing ...............................................................................6

TASK 3............................................................................................................................................7

P4 Report on planning tools........................................................................................................7

TASK 4..........................................................................................................................................10

P5 Balance score card approach................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1(a) Report on functions of management of management........................................................2

P2(b) Different types of management accounting......................................................................4

TASK 2............................................................................................................................................5

P3 Calculation of absorption and marginal costing methods......................................................5

P3 (i) Income statement under marginal costing........................................................................6

(ii) Income statement of absorption costing ...............................................................................6

TASK 3............................................................................................................................................7

P4 Report on planning tools........................................................................................................7

TASK 4..........................................................................................................................................10

P5 Balance score card approach................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION

Accounting and management are two different things but both have a similar and equal

contribution in operating business functions (Hopwood, Unerman and Fries, 2010). Management

accounting is used to maintain and keep records, informations and accounts in a particular

system. Accounting system provides a method to keep these records in such a way that all the

informations could get easily and on time. These information and records helps in making

strategies, forecasting plans and making budgets. There are certain standards, format and rules

are made to maintain these records. These records contains financial statements of companies,

income statements, final accounts, balance sheets, trial balance etc. all these records shows the

financial position of an organisation (Håkansson, Kraus and Lind eds., 2010). This report is

prepared in respect of Imda Tech (UK). Its Finance director wants financial and accounting

reports to make important decisions and strategies for businesses plans and growth model.

TASK 1

P1(a) Report on functions of management of management

There is a report is prepared to explain the meaning of management accounting and the

functions of management accounting. In second phase of report there is importance of

accounting information defined.

From : Management accounting Manager

To : Director of Finance department of Imda Tech

Sub : Management accounting and financial accounting

It is informed to finance department and all sub divisions that this report is formed to explain

meaning of management accounting and its about its functions.

1. Meaning of Management and financial accounting and Difference

Management accounting

This is a tools which is used to maintain records and data in professional manner. An

accounting system contains rules, accounting standards, procedures and specific formats. As per

Institute of Management Accounts (IMA): it is a professional and formal way to present

information regarding figures and data for a specific duration. This tool is used in decision

making, making budgets and in performance management. There are different measures and

certified institutions are established which provide a wide rage of accounting and management

2

Accounting and management are two different things but both have a similar and equal

contribution in operating business functions (Hopwood, Unerman and Fries, 2010). Management

accounting is used to maintain and keep records, informations and accounts in a particular

system. Accounting system provides a method to keep these records in such a way that all the

informations could get easily and on time. These information and records helps in making

strategies, forecasting plans and making budgets. There are certain standards, format and rules

are made to maintain these records. These records contains financial statements of companies,

income statements, final accounts, balance sheets, trial balance etc. all these records shows the

financial position of an organisation (Håkansson, Kraus and Lind eds., 2010). This report is

prepared in respect of Imda Tech (UK). Its Finance director wants financial and accounting

reports to make important decisions and strategies for businesses plans and growth model.

TASK 1

P1(a) Report on functions of management of management

There is a report is prepared to explain the meaning of management accounting and the

functions of management accounting. In second phase of report there is importance of

accounting information defined.

From : Management accounting Manager

To : Director of Finance department of Imda Tech

Sub : Management accounting and financial accounting

It is informed to finance department and all sub divisions that this report is formed to explain

meaning of management accounting and its about its functions.

1. Meaning of Management and financial accounting and Difference

Management accounting

This is a tools which is used to maintain records and data in professional manner. An

accounting system contains rules, accounting standards, procedures and specific formats. As per

Institute of Management Accounts (IMA): it is a professional and formal way to present

information regarding figures and data for a specific duration. This tool is used in decision

making, making budgets and in performance management. There are different measures and

certified institutions are established which provide a wide rage of accounting and management

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

courses and provide expertise in presenting financial and accounting reporting to managers and

directors.

There are different functions of management accounting as

Planning

This is first step to form an management accounting system in organisation. In this

functions an organisation's short term and long term objectives are decided. Best plans and

strategies are sorted out to attain these objectives.

Organising

Business operations remain divide in multiple parts and divisions organising help in

coordinate and manage these departments. This step define roles and responsibilities of

managers and leaders in an organisation.

Controlling

This function helps in monitoring, analysing and evaluating actions and performance of

employees in organisation. It provides path to control and maintain discipline in departments.

Decision making

Decision making is one of the important element which remain responsible in providing

best plans and strategies of growth. this is the function which help in making business plans and

models of business.

Financial accounting

This accounting tool is used in keeping financial information as per set procedures and standard

of management and institutions. Financial accounts as income statements, profit and loss

accounts, final representations and reports. This informations helps both internal department

and outsiders as shareholders, stakeholder, banks, finance institutions, investor groups,

government agencies and business owners. Generally Accepted Accounting Principles (GAAP)

has made standards and rules of maintaining financial records for different type of business and

organisations. Apart from it there are International Financial Reporting Standards (IFRS) are

made which are issued by International Accounting Standards Board (IASB). It provides

guidelines which are used at national and international level in management and accounting.

Difference Between Financial and management accounting .

Management accounting system is useful to managers, directors and departments how ever

financial accounting is useful to external people as shareholders, stakeholders, financiers,

3

directors.

There are different functions of management accounting as

Planning

This is first step to form an management accounting system in organisation. In this

functions an organisation's short term and long term objectives are decided. Best plans and

strategies are sorted out to attain these objectives.

Organising

Business operations remain divide in multiple parts and divisions organising help in

coordinate and manage these departments. This step define roles and responsibilities of

managers and leaders in an organisation.

Controlling

This function helps in monitoring, analysing and evaluating actions and performance of

employees in organisation. It provides path to control and maintain discipline in departments.

Decision making

Decision making is one of the important element which remain responsible in providing

best plans and strategies of growth. this is the function which help in making business plans and

models of business.

Financial accounting

This accounting tool is used in keeping financial information as per set procedures and standard

of management and institutions. Financial accounts as income statements, profit and loss

accounts, final representations and reports. This informations helps both internal department

and outsiders as shareholders, stakeholder, banks, finance institutions, investor groups,

government agencies and business owners. Generally Accepted Accounting Principles (GAAP)

has made standards and rules of maintaining financial records for different type of business and

organisations. Apart from it there are International Financial Reporting Standards (IFRS) are

made which are issued by International Accounting Standards Board (IASB). It provides

guidelines which are used at national and international level in management and accounting.

Difference Between Financial and management accounting .

Management accounting system is useful to managers, directors and departments how ever

financial accounting is useful to external people as shareholders, stakeholders, financiers,

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investors and government.

Financial accounting is known as historical approach whereas management accounting is based

upon present tactics and methods for better operation in future.

Management accounting is designed as per models and accounting formats and financial

accounts are based upon case studies and past scenarios.

Management accounting remain focused upon upcoming incidents and events and financial

accounting helps in making decisions and strategies as per past records.

Financial accounting contains general accounting standards, procedures whereas management

accounting system contains information management system and tools which are used by

managers of organisation in preparing plans and decision making.

2. Importance of management accounting as decision making tool

Scope of business has become vast and business environment has become advanced,

business organisation need a stable and effective management tool which keep business position

strong and confident in competitive environment. Management accounting is one of the

importance tools which is very prominent for an organisation in making impressive decision

making policy. It market is full of uncertainties and competitive business environment creates

more complexity in making policies and strategies. Management accounting support to make

and effective and practical path to deal with changes, interpersonal issues and high-risk

consequences.

P2(b) Different types of management accounting

Management accounting system contains different type of accounting systems which

helps management and departments in making plans, programs and policies for further

operations (DRURY, 2013). Accounting management system are not only helps in making

policies but also help in decision making process. These tools help in smooth formations and

getting best results. It improve the graph of profits and revenues. It helps to make financial

reports and plans which need to present in board meetings and conferences. Below are some

management systems are defined :

Cost accounting system – Cost is one of the factor which define the amount of utilisation of

investment on production process. This system help in analysing the cost which is incurred

during manufacturing and production process (Otley and Emmanuel, 2013). Managers make cost

4

Financial accounting is known as historical approach whereas management accounting is based

upon present tactics and methods for better operation in future.

Management accounting is designed as per models and accounting formats and financial

accounts are based upon case studies and past scenarios.

Management accounting remain focused upon upcoming incidents and events and financial

accounting helps in making decisions and strategies as per past records.

Financial accounting contains general accounting standards, procedures whereas management

accounting system contains information management system and tools which are used by

managers of organisation in preparing plans and decision making.

2. Importance of management accounting as decision making tool

Scope of business has become vast and business environment has become advanced,

business organisation need a stable and effective management tool which keep business position

strong and confident in competitive environment. Management accounting is one of the

importance tools which is very prominent for an organisation in making impressive decision

making policy. It market is full of uncertainties and competitive business environment creates

more complexity in making policies and strategies. Management accounting support to make

and effective and practical path to deal with changes, interpersonal issues and high-risk

consequences.

P2(b) Different types of management accounting

Management accounting system contains different type of accounting systems which

helps management and departments in making plans, programs and policies for further

operations (DRURY, 2013). Accounting management system are not only helps in making

policies but also help in decision making process. These tools help in smooth formations and

getting best results. It improve the graph of profits and revenues. It helps to make financial

reports and plans which need to present in board meetings and conferences. Below are some

management systems are defined :

Cost accounting system – Cost is one of the factor which define the amount of utilisation of

investment on production process. This system help in analysing the cost which is incurred

during manufacturing and production process (Otley and Emmanuel, 2013). Managers make cost

4

budget and plans to analyse future requirement of finance and resources with the help of records

and information provided by this management system. This system remain focused to reduce the

cost and increase profitability. A product cost is very important to control because a customer

attracts towards less price product.

Inventory Management system – Stocks and materials are the factors which are used to

manufacture the product and services (McNeil, Frey and Embrechts, 2015). It is required to

analyse the requirement of stock and manage the quantity of inventories so that production

process could run easily. There is most common system is used in inventory management system

which is ABC system. In this method material and stocks are categories as per their importance

and sensibility. This system prevent over storage and less storage situations n organisation. It

also support different divisions and departments as purchase, sales and manufacturing

department.

Job costing system – In large type of organisations production remain divided in various batches

and jobs. This system helps in analysing the cost at every job and batch. For example in mines

and petroleum refineries job costing are used to bifurcate the cost of particular batch and section.

It also help in deciding the price of joint and by products as diesel, Vaseline, Charcoal, Kerosene

are the joint and by products of petrol.

Price Optimisation system – This management tool helps in identifying and calculating the

factors which affect the price and cost of product (Chenhall, 2012). Product cost remain

distributed in multiple production process and sections. Price optimisation system helps in

consolidate all the cost and optimise job costs in one direction. Managers would get eligible to

decide and optimum price and cost of product by this system. It contains different mathematical

and calculating tools to centralise cost of product as marginal costing, absorption costing, job

costing, batch costing, process costing etc.

TASK 2

P3 Calculation of absorption and marginal costing methods

There are different type of cost approaches are used by business organisation to analyse

the cost of product :

Absorption costing – All the manufacturing and production cost are taken in calculating the cost

of product in this evaluation method. All the variable cost as material, labour and wages are

5

and information provided by this management system. This system remain focused to reduce the

cost and increase profitability. A product cost is very important to control because a customer

attracts towards less price product.

Inventory Management system – Stocks and materials are the factors which are used to

manufacture the product and services (McNeil, Frey and Embrechts, 2015). It is required to

analyse the requirement of stock and manage the quantity of inventories so that production

process could run easily. There is most common system is used in inventory management system

which is ABC system. In this method material and stocks are categories as per their importance

and sensibility. This system prevent over storage and less storage situations n organisation. It

also support different divisions and departments as purchase, sales and manufacturing

department.

Job costing system – In large type of organisations production remain divided in various batches

and jobs. This system helps in analysing the cost at every job and batch. For example in mines

and petroleum refineries job costing are used to bifurcate the cost of particular batch and section.

It also help in deciding the price of joint and by products as diesel, Vaseline, Charcoal, Kerosene

are the joint and by products of petrol.

Price Optimisation system – This management tool helps in identifying and calculating the

factors which affect the price and cost of product (Chenhall, 2012). Product cost remain

distributed in multiple production process and sections. Price optimisation system helps in

consolidate all the cost and optimise job costs in one direction. Managers would get eligible to

decide and optimum price and cost of product by this system. It contains different mathematical

and calculating tools to centralise cost of product as marginal costing, absorption costing, job

costing, batch costing, process costing etc.

TASK 2

P3 Calculation of absorption and marginal costing methods

There are different type of cost approaches are used by business organisation to analyse

the cost of product :

Absorption costing – All the manufacturing and production cost are taken in calculating the cost

of product in this evaluation method. All the variable cost as material, labour and wages are

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

taken in this approach. Rent, bills and depreciations are also considered as fixed cost while

measuring the cost (Lambert and Sponem, 2012). This concept is concentrated on direct cost

which impact the cost of product directly. Variable cost is allocated as labour, material and

wages, it is also known as factory cost of company. It is beneficial in preparing decision making

and pricing strategies for organisation.

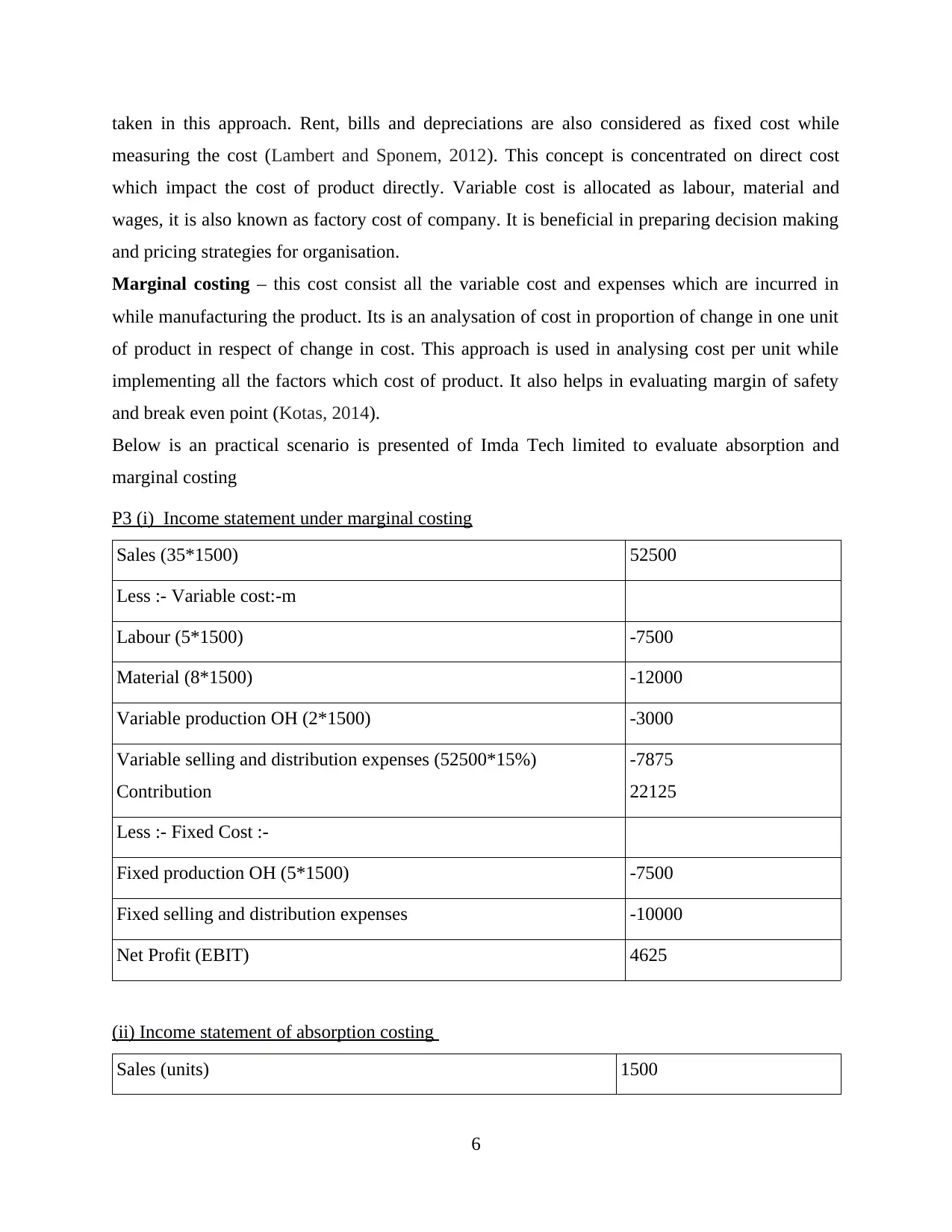

Marginal costing – this cost consist all the variable cost and expenses which are incurred in

while manufacturing the product. Its is an analysation of cost in proportion of change in one unit

of product in respect of change in cost. This approach is used in analysing cost per unit while

implementing all the factors which cost of product. It also helps in evaluating margin of safety

and break even point (Kotas, 2014).

Below is an practical scenario is presented of Imda Tech limited to evaluate absorption and

marginal costing

P3 (i) Income statement under marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%)

Contribution

-7875

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

(ii) Income statement of absorption costing

Sales (units) 1500

6

measuring the cost (Lambert and Sponem, 2012). This concept is concentrated on direct cost

which impact the cost of product directly. Variable cost is allocated as labour, material and

wages, it is also known as factory cost of company. It is beneficial in preparing decision making

and pricing strategies for organisation.

Marginal costing – this cost consist all the variable cost and expenses which are incurred in

while manufacturing the product. Its is an analysation of cost in proportion of change in one unit

of product in respect of change in cost. This approach is used in analysing cost per unit while

implementing all the factors which cost of product. It also helps in evaluating margin of safety

and break even point (Kotas, 2014).

Below is an practical scenario is presented of Imda Tech limited to evaluate absorption and

marginal costing

P3 (i) Income statement under marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%)

Contribution

-7875

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

(ii) Income statement of absorption costing

Sales (units) 1500

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

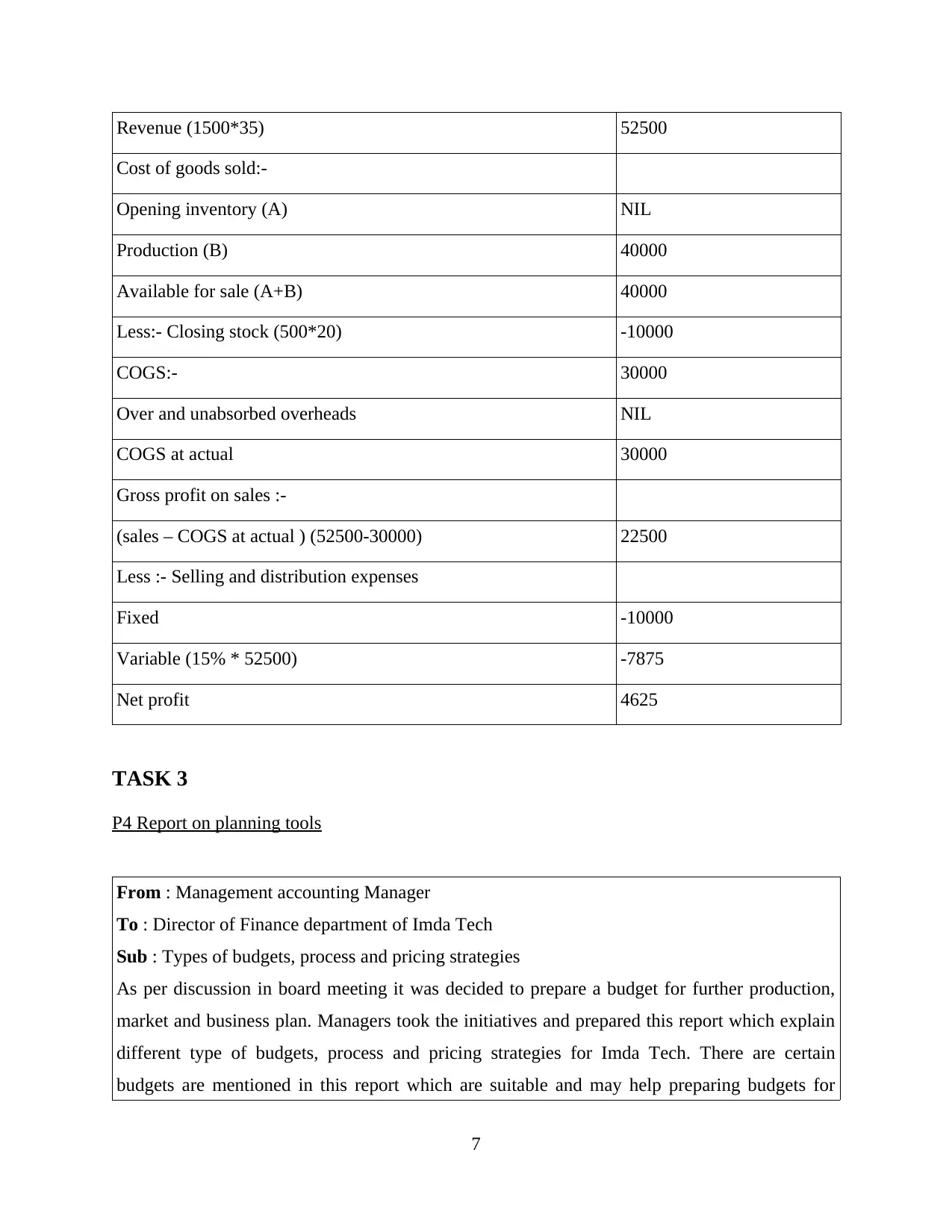

Revenue (1500*35) 52500

Cost of goods sold:-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

TASK 3

P4 Report on planning tools

From : Management accounting Manager

To : Director of Finance department of Imda Tech

Sub : Types of budgets, process and pricing strategies

As per discussion in board meeting it was decided to prepare a budget for further production,

market and business plan. Managers took the initiatives and prepared this report which explain

different type of budgets, process and pricing strategies for Imda Tech. There are certain

budgets are mentioned in this report which are suitable and may help preparing budgets for

7

Cost of goods sold:-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

TASK 3

P4 Report on planning tools

From : Management accounting Manager

To : Director of Finance department of Imda Tech

Sub : Types of budgets, process and pricing strategies

As per discussion in board meeting it was decided to prepare a budget for further production,

market and business plan. Managers took the initiatives and prepared this report which explain

different type of budgets, process and pricing strategies for Imda Tech. There are certain

budgets are mentioned in this report which are suitable and may help preparing budgets for

7

Imda Tech.;

Operating Budget

This budget is prepared to analyse and forecasting the income and expenses for

particular time duration. It contains the cost of operating administration and staff operation.

There are different types of expenditures happen in administrative departments as stationary,

refreshments, maintenance, electricity, telephone bills, petty expenses etc. operating budget

help in managing usual and day to day expenses of administration department of Imda tech.

Capital budget

this budget helps in measuring the amount of investment in upcoming duration. An

organisations capital remain divided in different structure as equity share capital, preference

share capital, reserves and surplus, security premiums. This budget system helps in managing

capital structure of organisation. Managers get eligible to find out best and effective option for

generating finance. Cost of capital, leverages are the method which help in evaluating the cost

of investment which is implemented in organisation.

Sales budget

Organisation which are aligned in providing goods and products businesses, sales

budget helps in analysing optimum level of sales and maintain profitability in organisation.

Margin of safety, profit volume ratio are the methods which helps in calculating break even

point and margin sales. Break even point shows the optimum level of sales where an

organisation not have any loss or profit. Different of actual sales and break even sale is called

margin of safety. This is one of the common approach which is considered very useful in

preparing sales budget.

Cash budget

To operate regular and continuous operations there is cash requirement occurs in

organisation. Cash is considered as liquid and current assets of organisation. It helps in

operating and managing administrative and operating expenses. Cash flow statement, fund flow

statements are major factors which help in preparing cash budget. Cash budget will provide an

idea to analyse cash requirement to operates function in near future. There are certain standards

and guidelines are made to prepare and retain cash flow statements. In financial and banking

industries records are retained in cash flow and fund flow statements.

Financial budget

8

Operating Budget

This budget is prepared to analyse and forecasting the income and expenses for

particular time duration. It contains the cost of operating administration and staff operation.

There are different types of expenditures happen in administrative departments as stationary,

refreshments, maintenance, electricity, telephone bills, petty expenses etc. operating budget

help in managing usual and day to day expenses of administration department of Imda tech.

Capital budget

this budget helps in measuring the amount of investment in upcoming duration. An

organisations capital remain divided in different structure as equity share capital, preference

share capital, reserves and surplus, security premiums. This budget system helps in managing

capital structure of organisation. Managers get eligible to find out best and effective option for

generating finance. Cost of capital, leverages are the method which help in evaluating the cost

of investment which is implemented in organisation.

Sales budget

Organisation which are aligned in providing goods and products businesses, sales

budget helps in analysing optimum level of sales and maintain profitability in organisation.

Margin of safety, profit volume ratio are the methods which helps in calculating break even

point and margin sales. Break even point shows the optimum level of sales where an

organisation not have any loss or profit. Different of actual sales and break even sale is called

margin of safety. This is one of the common approach which is considered very useful in

preparing sales budget.

Cash budget

To operate regular and continuous operations there is cash requirement occurs in

organisation. Cash is considered as liquid and current assets of organisation. It helps in

operating and managing administrative and operating expenses. Cash flow statement, fund flow

statements are major factors which help in preparing cash budget. Cash budget will provide an

idea to analyse cash requirement to operates function in near future. There are certain standards

and guidelines are made to prepare and retain cash flow statements. In financial and banking

industries records are retained in cash flow and fund flow statements.

Financial budget

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This budget contains overall informations and figures which are responsible to

accelerate the functions and operations in effective way. Finance budget access the data and

figures in systematic manner to examine the financial position of organisation in market.

Informations which are provided by finance budget would be very useful and important to

stakeholders, shareholders and owners of Imda tech.

Process of preparing budget

Budget process comprise basically three steps as

Development

this first step in which the improvement criteria is analysed and evaluated. Managers of

Imda tech should analyse the sector and criteria of development. There are certain area are

found in organisation as information technology, communication system are need to establish.

Following plans and strategies must be as per these areas.

Evaluation

This is second step in which proposed plan is analysed and evaluated on the basis of

availability of resources. As above mentions criteria organisation need to find out a strong

communication and information system so that the flow of order and laws in effective manner.

evaluation methods helps in analysing the plan whether its is suitable or not and changes could

be made before implementation.

Implementation

This is the last step of preparing budget process. In this step plans and resources are

implemented on defined criteria and fields. All the resources and informations are utilised in

developing and forming the plan. Roles and responsibilities are decided in this stage.

Pricing strategies

Measurement of cost of product and control the cost are the major criteria of pricing

strategies. Customers get attract towards effective and less price products. These strategies are

made to reduce cost and increase profitability of organisation. There are different factors and

figures need to analysed while preparing and price strategies there are some steps are defined in

respect of forming an effective price strategy as;

Value based pricing

Profit is the only factor which motivates and encourage people of organisation to excel

ahead and keep working for better on regular basis. It is considered as central element of

9

accelerate the functions and operations in effective way. Finance budget access the data and

figures in systematic manner to examine the financial position of organisation in market.

Informations which are provided by finance budget would be very useful and important to

stakeholders, shareholders and owners of Imda tech.

Process of preparing budget

Budget process comprise basically three steps as

Development

this first step in which the improvement criteria is analysed and evaluated. Managers of

Imda tech should analyse the sector and criteria of development. There are certain area are

found in organisation as information technology, communication system are need to establish.

Following plans and strategies must be as per these areas.

Evaluation

This is second step in which proposed plan is analysed and evaluated on the basis of

availability of resources. As above mentions criteria organisation need to find out a strong

communication and information system so that the flow of order and laws in effective manner.

evaluation methods helps in analysing the plan whether its is suitable or not and changes could

be made before implementation.

Implementation

This is the last step of preparing budget process. In this step plans and resources are

implemented on defined criteria and fields. All the resources and informations are utilised in

developing and forming the plan. Roles and responsibilities are decided in this stage.

Pricing strategies

Measurement of cost of product and control the cost are the major criteria of pricing

strategies. Customers get attract towards effective and less price products. These strategies are

made to reduce cost and increase profitability of organisation. There are different factors and

figures need to analysed while preparing and price strategies there are some steps are defined in

respect of forming an effective price strategy as;

Value based pricing

Profit is the only factor which motivates and encourage people of organisation to excel

ahead and keep working for better on regular basis. It is considered as central element of

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. Value based pricing is a techniques which drives the curve of profit in favourable

conditions in respect of business. This strategy is planed and focused towards increasing profits

and revenue. In this technique customer's will power and purchasing power is evaluated, it is

analysed that how much amount a customer wants to spend on product. Base price is considered

to form these strategies.

Implementation

this step help in assigning the project and deciding the roles and responsibilities of

managers and employees for performing the task in effective manner. This step works around

goals, objectives and aims of organisation. In this stage best fit growth model and plan is taken

to lead the idea and deciding the price of product. Analysing customer's nature, purchasing

power, market segmentation, competitive strategies, price of substitute products are the main

factors which are considered in this stage. There is bottom line is created to analyse the least

price for which a customers is willing to pay. Company's motive, competitions also need to

analyse while implementing sources in price strategy.

Analysation

Measurement of strategies whether it is working in desired direction or not is the key

criteria of this step. Communicate value of organisation to attain better understanding and

attributes of employees are considered in this approach. What are the rules and guidelines are

mentioned to giving discount to customers and what are the negotiation and communication

system in organisation is also analysed in this structure.

10

conditions in respect of business. This strategy is planed and focused towards increasing profits

and revenue. In this technique customer's will power and purchasing power is evaluated, it is

analysed that how much amount a customer wants to spend on product. Base price is considered

to form these strategies.

Implementation

this step help in assigning the project and deciding the roles and responsibilities of

managers and employees for performing the task in effective manner. This step works around

goals, objectives and aims of organisation. In this stage best fit growth model and plan is taken

to lead the idea and deciding the price of product. Analysing customer's nature, purchasing

power, market segmentation, competitive strategies, price of substitute products are the main

factors which are considered in this stage. There is bottom line is created to analyse the least

price for which a customers is willing to pay. Company's motive, competitions also need to

analyse while implementing sources in price strategy.

Analysation

Measurement of strategies whether it is working in desired direction or not is the key

criteria of this step. Communicate value of organisation to attain better understanding and

attributes of employees are considered in this approach. What are the rules and guidelines are

mentioned to giving discount to customers and what are the negotiation and communication

system in organisation is also analysed in this structure.

10

TASK 4

P5 Balance score card approach

(Source :Balanced scorecard, 2017)

Balanced score card is an approach which is used to set to trace actions and performance

of employees in organisation. It is a format of semi structured report which helps in executing

the plans and procedure in professional manner. There are plans and strategies are made to attain

goals and objectives of organisation. Balance score card helps in managing, monitoring and

analysing the actions and performance of employees.

Basically this approach is implemented and used to focus on management and operational

activities of organisation (Li and et. al., 2012). As per recent records and figures 60%

respondents are records who implemented balanced scorecard approach to make effective and

approachable management structure and 40% use this approach in managing operating

department of organisation.

Focused criteria

It remain focus in measurement of work and performance of employees and find out

conflicts and causes which effect performance level of employees.

11

P5 Balance score card approach

(Source :Balanced scorecard, 2017)

Balanced score card is an approach which is used to set to trace actions and performance

of employees in organisation. It is a format of semi structured report which helps in executing

the plans and procedure in professional manner. There are plans and strategies are made to attain

goals and objectives of organisation. Balance score card helps in managing, monitoring and

analysing the actions and performance of employees.

Basically this approach is implemented and used to focus on management and operational

activities of organisation (Li and et. al., 2012). As per recent records and figures 60%

respondents are records who implemented balanced scorecard approach to make effective and

approachable management structure and 40% use this approach in managing operating

department of organisation.

Focused criteria

It remain focus in measurement of work and performance of employees and find out

conflicts and causes which effect performance level of employees.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.