Management Accounting Report: Modern Ltd. Analysis & Solutions

VerifiedAdded on 2020/12/29

|14

|3719

|417

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on their application within Modern Ltd. It begins with an introduction to management accounting, its core concepts, and essential requirements, along with various techniques and methods used in reporting. The report then delves into the application of absorption and marginal costing methods to prepare income statements, showcasing their impact on financial reporting. Furthermore, it explores the advantages and disadvantages of different budgeting methods and their significance in financial planning and control. Finally, the report examines how management accounting systems can be utilized to address and overcome financial issues. The report includes detailed calculations, analyses, and comparisons to illustrate the practical implications of each concept. This comprehensive analysis provides valuable insights into effective financial management and decision-making within an organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting and its essential requirement.......................................3

P2 Different techniques and methods used in management accounting reporting.....................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different kind of budgets and their importance..............9

TASK 4..........................................................................................................................................11

P5 Application of management accounting system to overcome from financial issues...........11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting and its essential requirement.......................................3

P2 Different techniques and methods used in management accounting reporting.....................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different kind of budgets and their importance..............9

TASK 4..........................................................................................................................................11

P5 Application of management accounting system to overcome from financial issues...........11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting refers as the process of formulating reports and accounts which

provides financial and non financial data timely in accurate manner which enables the manager

of organisation is to make day to day decisions effectively. These accounts and reports are

generally produced for the aid of internal parties of organisation which contributes in

improvement of their understanding. The information which is provided by these reports

includes cash, sales revenue, amount of orders in hand, outstanding debts, raw materials and

inventory. Modern Ltd. Is medium sized organisation which deals in diversified products

(Arroyo, 2012).

In the present report explain about different types of management accounting systems

along with benefits derived by organisation, various types of management accounting reports and

application of cost analysis techniques to prepare income statements. Also, advantages and

disadvantages of various planning tools used for controlling budget and application of

management accounting principles to respond financial issues.

TASK 1

P1 Concept of management accounting and its essential requirement

Management accounting: It is refers as the process which includes formulation of

accounts and reports which enables the manager of organisation to collect financial and

statistical information to make their day to day decisions. The different type of informations

which are included under this report is related to availability of cash, sales revenue, current value

of accounts payable and receivable.

According to CMA, management accounting is the concept which includes preparation of

accounts and reports by accountant through application of their knowledge and skills to assist the

manager of organisation in formulation of policies and controlling of operations of undertaking.

Management accounting systems

It is refers as internal system which is mainly used by the organisation to measure and

assess their different processes for the purpose of bring effective management within the

Management Accounting refers as the process of formulating reports and accounts which

provides financial and non financial data timely in accurate manner which enables the manager

of organisation is to make day to day decisions effectively. These accounts and reports are

generally produced for the aid of internal parties of organisation which contributes in

improvement of their understanding. The information which is provided by these reports

includes cash, sales revenue, amount of orders in hand, outstanding debts, raw materials and

inventory. Modern Ltd. Is medium sized organisation which deals in diversified products

(Arroyo, 2012).

In the present report explain about different types of management accounting systems

along with benefits derived by organisation, various types of management accounting reports and

application of cost analysis techniques to prepare income statements. Also, advantages and

disadvantages of various planning tools used for controlling budget and application of

management accounting principles to respond financial issues.

TASK 1

P1 Concept of management accounting and its essential requirement

Management accounting: It is refers as the process which includes formulation of

accounts and reports which enables the manager of organisation to collect financial and

statistical information to make their day to day decisions. The different type of informations

which are included under this report is related to availability of cash, sales revenue, current value

of accounts payable and receivable.

According to CMA, management accounting is the concept which includes preparation of

accounts and reports by accountant through application of their knowledge and skills to assist the

manager of organisation in formulation of policies and controlling of operations of undertaking.

Management accounting systems

It is refers as internal system which is mainly used by the organisation to measure and

assess their different processes for the purpose of bring effective management within the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. Different type of accounts are prepared which helps to gather valuable data to

control the business activities better. The different type of accounts along with their functioning

in Modern Ltd is defined below:

Job costing system: This system incluIdes the activities related to assigning of

manufacturing cost each individuals product produced by organisation. It also provides the

function regarding monitoring of expense which is incurred in production process.

Cost accounting system: Application of the provision of this system enables the

manager of organisation regarding approximation of the cost of product in regards to

determination of profitability, inventory and cost control.

Inventory management system: This system enables the manager regarding supervision

of their stocks and assets lies with the organisation. This will improves the understanding of

manager regarding effective flow of their inventories to optimally utilise them is accomplishment

of their desired targets (Boyns and Edwards, 2013 ).

Functions of management accounting

The four major functions which are performed after application of management

accounting concepts by the management of Modern Ltd are defined below:

Planning: Collected information through application of management accounting systems

helps in formulation of short and long term plans in attainment of particular end results.

Organising: Management accounting system helps to determine the tasks which are

required to carry to achieve targets. This will enables in process of assigning responsibility to

employees.

Controlling: It also assist the manager of organisation in process of monitoring,

evaluating and correcting the actual performance to attain the results as per predetermined

standards.

Decision-making: Different accounts provides various information which improves

decision making as they can make able to make infoIrmation based decisions.

Advantages of management accounting

The different type of benefits received by Modern Ltd. From use of management

accounting are defined below:

Maximisation of profit: Management accounting system is used by the manager in

regards to setting of standards and appraisal of actual performance. This will enables the

control the business activities better. The different type of accounts along with their functioning

in Modern Ltd is defined below:

Job costing system: This system incluIdes the activities related to assigning of

manufacturing cost each individuals product produced by organisation. It also provides the

function regarding monitoring of expense which is incurred in production process.

Cost accounting system: Application of the provision of this system enables the

manager of organisation regarding approximation of the cost of product in regards to

determination of profitability, inventory and cost control.

Inventory management system: This system enables the manager regarding supervision

of their stocks and assets lies with the organisation. This will improves the understanding of

manager regarding effective flow of their inventories to optimally utilise them is accomplishment

of their desired targets (Boyns and Edwards, 2013 ).

Functions of management accounting

The four major functions which are performed after application of management

accounting concepts by the management of Modern Ltd are defined below:

Planning: Collected information through application of management accounting systems

helps in formulation of short and long term plans in attainment of particular end results.

Organising: Management accounting system helps to determine the tasks which are

required to carry to achieve targets. This will enables in process of assigning responsibility to

employees.

Controlling: It also assist the manager of organisation in process of monitoring,

evaluating and correcting the actual performance to attain the results as per predetermined

standards.

Decision-making: Different accounts provides various information which improves

decision making as they can make able to make infoIrmation based decisions.

Advantages of management accounting

The different type of benefits received by Modern Ltd. From use of management

accounting are defined below:

Maximisation of profit: Management accounting system is used by the manager in

regards to setting of standards and appraisal of actual performance. This will enables the

manager to identify deviations and provide corrective measures to improve their performances.

It results in maximisation of profit of organisation in future.

Regulation of business activities: Management accounting systems helps in

performance of four basic functions effectively such as planning, organising, controlling and

decision-making which enables in effective regulation of day to day operations.

Better Communication: Application of management accounting concept within the

organisation helps in creation of two way communication through responsibilities and duties are

effectively disbursed in accomplishment of desired outcomes within given frame of time.

P2 Different techniques and methods used in management accounting reporting

Management accounting reports: It is refers as the process of preparation of different type

of reports on the basis of information gathered from various accounts. These reports have huge

importance within the organisation regarding determination of the actual performance of departs

and setting of the budgets and standards for their guidance. The different kind of reports which

are majorly prepared within the organisation are related to inventory, accounts receivable, job

cost etc. All these reports having their own advantages and disadvantages in organisation in

regulation of their daily operations. There are many techniques and methods are used in the

process of preparing these reports. Such different type of techniques along with their functioning

is defined below:

Variance analysis: It is an accounting tool which is mainly used regarding evaluation of

the difference between actual and planned behaviour. This tool has huge importance in

controlling of the business functions in appropriate manner. Here, differences should be reduced

through assessment of actual reasons and effective guidance (Herzig and et. al. 2012).

Target costing: It is refers as the approach which includes determination of product life

cycle cost. It is important to determine to perform according to standards and with good quality

to earn desired amount of profit. The target cost is set within the organisation after subtraction of

desired profit from market price.

Marginal costing: It is effective tool which is used regarding determination of the cost

which is incurred in production of product. According to the principle of this method, only

variable costs are charged to the units and fixed cost is totally write off against contribution. This

will improves the understanding of manager regarding determination of change in cost due to

increase and decrease of one unit of cost of production.

It results in maximisation of profit of organisation in future.

Regulation of business activities: Management accounting systems helps in

performance of four basic functions effectively such as planning, organising, controlling and

decision-making which enables in effective regulation of day to day operations.

Better Communication: Application of management accounting concept within the

organisation helps in creation of two way communication through responsibilities and duties are

effectively disbursed in accomplishment of desired outcomes within given frame of time.

P2 Different techniques and methods used in management accounting reporting

Management accounting reports: It is refers as the process of preparation of different type

of reports on the basis of information gathered from various accounts. These reports have huge

importance within the organisation regarding determination of the actual performance of departs

and setting of the budgets and standards for their guidance. The different kind of reports which

are majorly prepared within the organisation are related to inventory, accounts receivable, job

cost etc. All these reports having their own advantages and disadvantages in organisation in

regulation of their daily operations. There are many techniques and methods are used in the

process of preparing these reports. Such different type of techniques along with their functioning

is defined below:

Variance analysis: It is an accounting tool which is mainly used regarding evaluation of

the difference between actual and planned behaviour. This tool has huge importance in

controlling of the business functions in appropriate manner. Here, differences should be reduced

through assessment of actual reasons and effective guidance (Herzig and et. al. 2012).

Target costing: It is refers as the approach which includes determination of product life

cycle cost. It is important to determine to perform according to standards and with good quality

to earn desired amount of profit. The target cost is set within the organisation after subtraction of

desired profit from market price.

Marginal costing: It is effective tool which is used regarding determination of the cost

which is incurred in production of product. According to the principle of this method, only

variable costs are charged to the units and fixed cost is totally write off against contribution. This

will improves the understanding of manager regarding determination of change in cost due to

increase and decrease of one unit of cost of production.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard costing: It is referred as estimated and predetermined cost which is incurred in

the process of producing goods and services. This will also be known as targeted cost which is

further used by the management for its comparison with actual costs. The deviations are

determined to build new and effective strategies which provides opportunity to attain their target

of costs and improve their profit margin. Such targeted cost is determined on the basis of

analysis of historical data and motion studies. The basic reasons which are identified for

deviation in actual costs from standards includes presence of many unpredictable factors.

Absorption costing: This method of costing is also known as full costing. As per this

method, all the costs whether fixed or variable in nature are apportioned to the units which are

produced by organisation.

Activity based costing: It is refers as such accounting method which includes the

process of identification and assignment of costs to different overhead activities and after that its

application on the products which are manufactured by organisation. This method used by the

manager generally for the purpose of determining relationship between different aspects.

Application of the principles of ABC system provides the information regarding relation between

costs, overhead activities and manufactured products. This relationship is further used to assign

the indirect cost to products (Otley and Emmanuel, 2013).

TASK 2

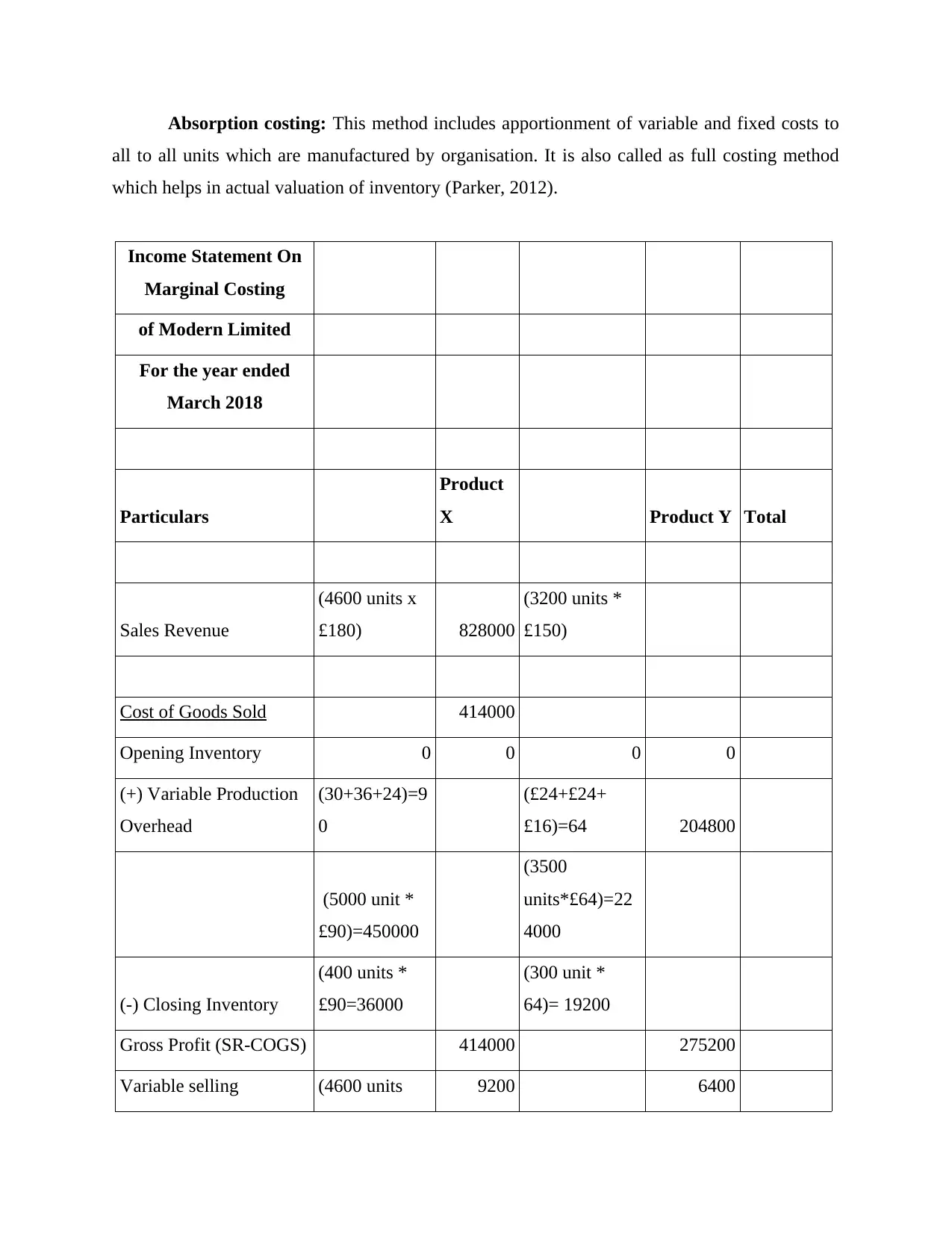

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It is refers as the amount which is incurred by the organisation in process of

producing and manufacturing of their products. The different aspects which are included while

calculating overall cost are efforts, raw materials, opportunity cost, labour, time and risk.

Marginal costing: It is variable costing method where only such costs are considered

which are variable in nature. It is mainly used to determine the change in cost due to production

of one extra unit.

the process of producing goods and services. This will also be known as targeted cost which is

further used by the management for its comparison with actual costs. The deviations are

determined to build new and effective strategies which provides opportunity to attain their target

of costs and improve their profit margin. Such targeted cost is determined on the basis of

analysis of historical data and motion studies. The basic reasons which are identified for

deviation in actual costs from standards includes presence of many unpredictable factors.

Absorption costing: This method of costing is also known as full costing. As per this

method, all the costs whether fixed or variable in nature are apportioned to the units which are

produced by organisation.

Activity based costing: It is refers as such accounting method which includes the

process of identification and assignment of costs to different overhead activities and after that its

application on the products which are manufactured by organisation. This method used by the

manager generally for the purpose of determining relationship between different aspects.

Application of the principles of ABC system provides the information regarding relation between

costs, overhead activities and manufactured products. This relationship is further used to assign

the indirect cost to products (Otley and Emmanuel, 2013).

TASK 2

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It is refers as the amount which is incurred by the organisation in process of

producing and manufacturing of their products. The different aspects which are included while

calculating overall cost are efforts, raw materials, opportunity cost, labour, time and risk.

Marginal costing: It is variable costing method where only such costs are considered

which are variable in nature. It is mainly used to determine the change in cost due to production

of one extra unit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing: This method includes apportionment of variable and fixed costs to

all to all units which are manufactured by organisation. It is also called as full costing method

which helps in actual valuation of inventory (Parker, 2012).

Income Statement On

Marginal Costing

of Modern Limited

For the year ended

March 2018

Particulars

Product

X Product Y Total

Sales Revenue

(4600 units x

£180) 828000

(3200 units *

£150)

Cost of Goods Sold 414000

Opening Inventory 0 0 0 0

(+) Variable Production

Overhead

(30+36+24)=9

0

(£24+£24+

£16)=64 204800

(5000 unit *

£90)=450000

(3500

units*£64)=22

4000

(-) Closing Inventory

(400 units *

£90=36000

(300 unit *

64)= 19200

Gross Profit (SR-COGS) 414000 275200

Variable selling (4600 units 9200 6400

all to all units which are manufactured by organisation. It is also called as full costing method

which helps in actual valuation of inventory (Parker, 2012).

Income Statement On

Marginal Costing

of Modern Limited

For the year ended

March 2018

Particulars

Product

X Product Y Total

Sales Revenue

(4600 units x

£180) 828000

(3200 units *

£150)

Cost of Goods Sold 414000

Opening Inventory 0 0 0 0

(+) Variable Production

Overhead

(30+36+24)=9

0

(£24+£24+

£16)=64 204800

(5000 unit *

£90)=450000

(3500

units*£64)=22

4000

(-) Closing Inventory

(400 units *

£90=36000

(300 unit *

64)= 19200

Gross Profit (SR-COGS) 414000 275200

Variable selling (4600 units 9200 6400

overheads *£2)

Contribution (GP-VSO) 404800 268800

(-) Fix Production

Overheads 210000

(-) Fixed Administration

Overheads 54000

Profits 409600

Income Statement On absorption Costing

of Modern Limited

For the year ended March 2018

Product X Product X Product Y Product Y Total

Sales Revenue

(4600 unit *

£180 per unit) 828000 480000

Cost of Goods Sold 690000 332800

Opening Inventory 0 0 0 0

(+) Full Production

Overhead

(£30+£36+

£24+£60)

=30+36+24+6

0

(24+24+16

+40)

=24+24+16

+40

(5000 unit *

150)

=5000*150

(3500 units

*

104)=3500*

104

(-) Closing

Inventory

(400 unit *

150)

(300 units

*104)

Contribution (GP-VSO) 404800 268800

(-) Fix Production

Overheads 210000

(-) Fixed Administration

Overheads 54000

Profits 409600

Income Statement On absorption Costing

of Modern Limited

For the year ended March 2018

Product X Product X Product Y Product Y Total

Sales Revenue

(4600 unit *

£180 per unit) 828000 480000

Cost of Goods Sold 690000 332800

Opening Inventory 0 0 0 0

(+) Full Production

Overhead

(£30+£36+

£24+£60)

=30+36+24+6

0

(24+24+16

+40)

=24+24+16

+40

(5000 unit *

150)

=5000*150

(3500 units

*

104)=3500*

104

(-) Closing

Inventory

(400 unit *

150)

(300 units

*104)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

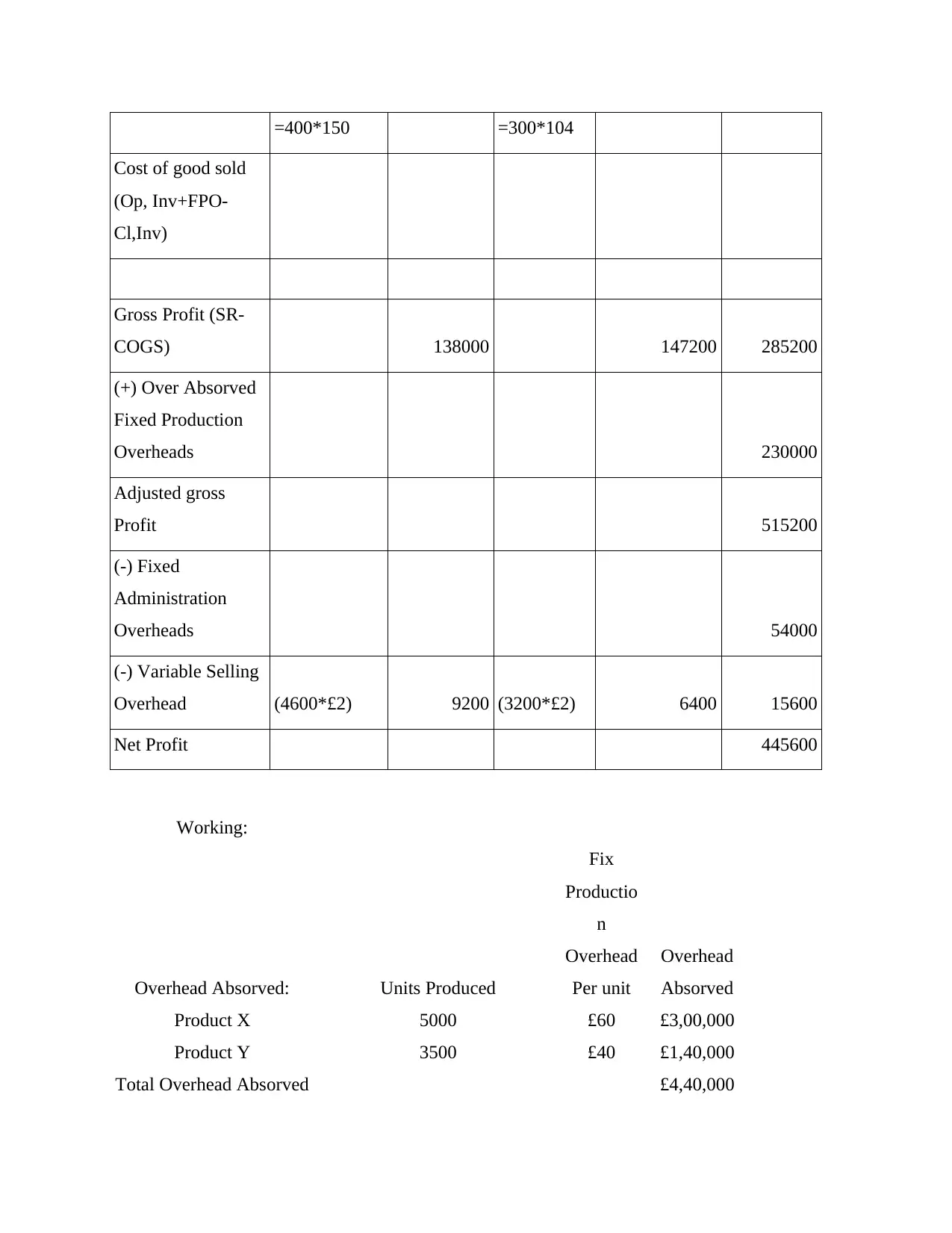

=400*150 =300*104

Cost of good sold

(Op, Inv+FPO-

Cl,Inv)

Gross Profit (SR-

COGS) 138000 147200 285200

(+) Over Absorved

Fixed Production

Overheads 230000

Adjusted gross

Profit 515200

(-) Fixed

Administration

Overheads 54000

(-) Variable Selling

Overhead (4600*£2) 9200 (3200*£2) 6400 15600

Net Profit 445600

Working:

Overhead Absorved: Units Produced

Fix

Productio

n

Overhead

Per unit

Overhead

Absorved

Product X 5000 £60 £3,00,000

Product Y 3500 £40 £1,40,000

Total Overhead Absorved £4,40,000

Cost of good sold

(Op, Inv+FPO-

Cl,Inv)

Gross Profit (SR-

COGS) 138000 147200 285200

(+) Over Absorved

Fixed Production

Overheads 230000

Adjusted gross

Profit 515200

(-) Fixed

Administration

Overheads 54000

(-) Variable Selling

Overhead (4600*£2) 9200 (3200*£2) 6400 15600

Net Profit 445600

Working:

Overhead Absorved: Units Produced

Fix

Productio

n

Overhead

Per unit

Overhead

Absorved

Product X 5000 £60 £3,00,000

Product Y 3500 £40 £1,40,000

Total Overhead Absorved £4,40,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

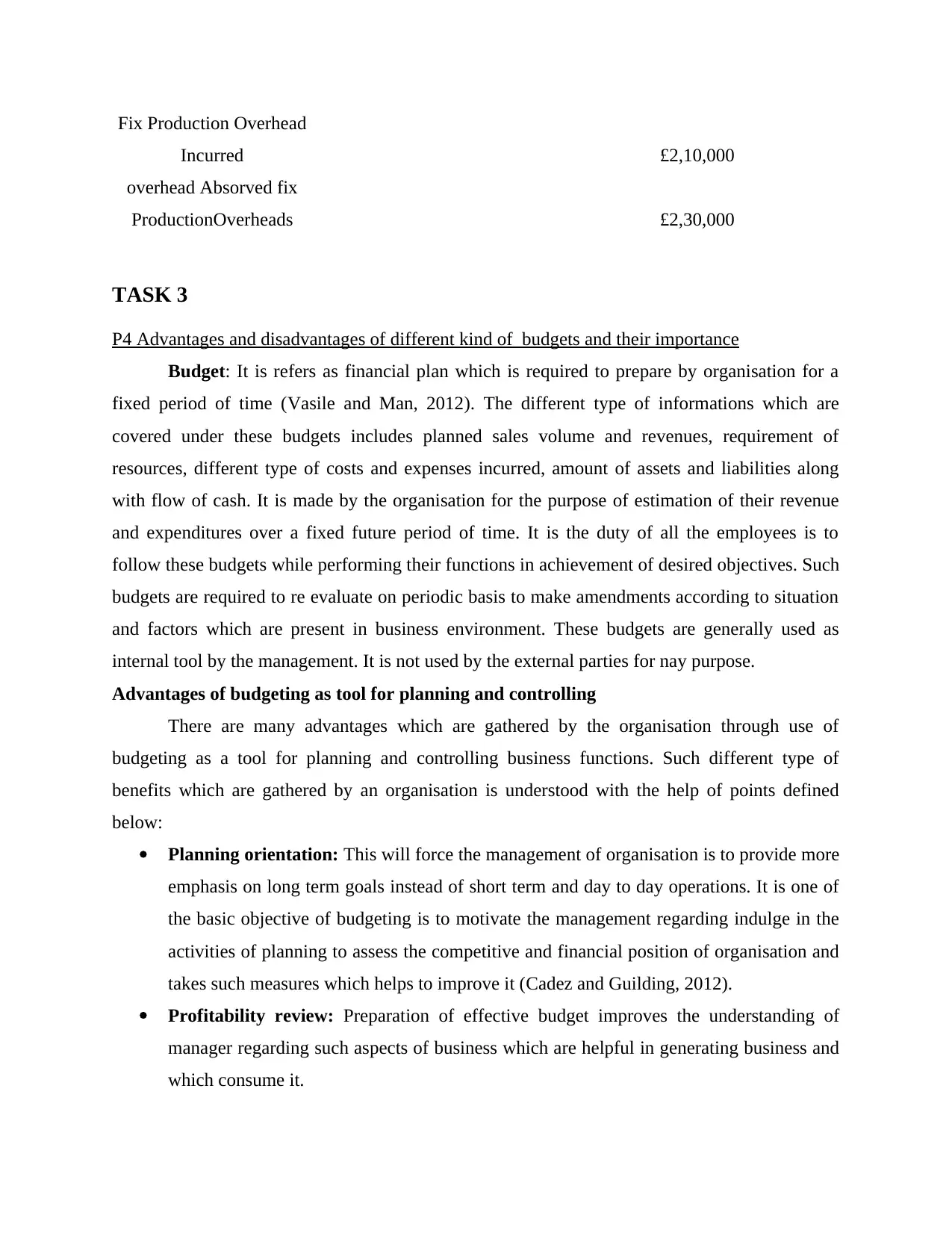

Fix Production Overhead

Incurred £2,10,000

overhead Absorved fix

ProductionOverheads £2,30,000

TASK 3

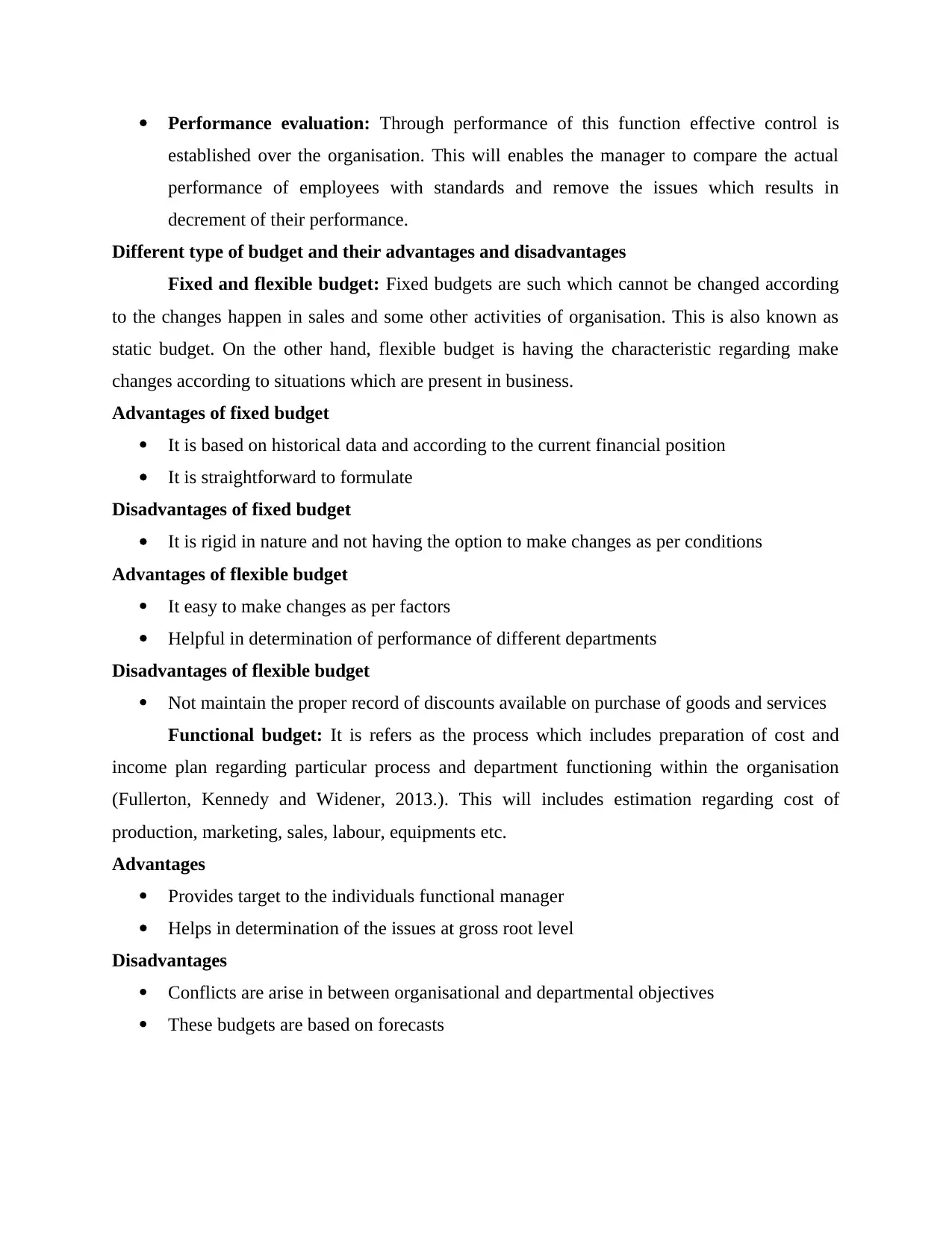

P4 Advantages and disadvantages of different kind of budgets and their importance

Budget: It is refers as financial plan which is required to prepare by organisation for a

fixed period of time (Vasile and Man, 2012). The different type of informations which are

covered under these budgets includes planned sales volume and revenues, requirement of

resources, different type of costs and expenses incurred, amount of assets and liabilities along

with flow of cash. It is made by the organisation for the purpose of estimation of their revenue

and expenditures over a fixed future period of time. It is the duty of all the employees is to

follow these budgets while performing their functions in achievement of desired objectives. Such

budgets are required to re evaluate on periodic basis to make amendments according to situation

and factors which are present in business environment. These budgets are generally used as

internal tool by the management. It is not used by the external parties for nay purpose.

Advantages of budgeting as tool for planning and controlling

There are many advantages which are gathered by the organisation through use of

budgeting as a tool for planning and controlling business functions. Such different type of

benefits which are gathered by an organisation is understood with the help of points defined

below:

Planning orientation: This will force the management of organisation is to provide more

emphasis on long term goals instead of short term and day to day operations. It is one of

the basic objective of budgeting is to motivate the management regarding indulge in the

activities of planning to assess the competitive and financial position of organisation and

takes such measures which helps to improve it (Cadez and Guilding, 2012).

Profitability review: Preparation of effective budget improves the understanding of

manager regarding such aspects of business which are helpful in generating business and

which consume it.

Incurred £2,10,000

overhead Absorved fix

ProductionOverheads £2,30,000

TASK 3

P4 Advantages and disadvantages of different kind of budgets and their importance

Budget: It is refers as financial plan which is required to prepare by organisation for a

fixed period of time (Vasile and Man, 2012). The different type of informations which are

covered under these budgets includes planned sales volume and revenues, requirement of

resources, different type of costs and expenses incurred, amount of assets and liabilities along

with flow of cash. It is made by the organisation for the purpose of estimation of their revenue

and expenditures over a fixed future period of time. It is the duty of all the employees is to

follow these budgets while performing their functions in achievement of desired objectives. Such

budgets are required to re evaluate on periodic basis to make amendments according to situation

and factors which are present in business environment. These budgets are generally used as

internal tool by the management. It is not used by the external parties for nay purpose.

Advantages of budgeting as tool for planning and controlling

There are many advantages which are gathered by the organisation through use of

budgeting as a tool for planning and controlling business functions. Such different type of

benefits which are gathered by an organisation is understood with the help of points defined

below:

Planning orientation: This will force the management of organisation is to provide more

emphasis on long term goals instead of short term and day to day operations. It is one of

the basic objective of budgeting is to motivate the management regarding indulge in the

activities of planning to assess the competitive and financial position of organisation and

takes such measures which helps to improve it (Cadez and Guilding, 2012).

Profitability review: Preparation of effective budget improves the understanding of

manager regarding such aspects of business which are helpful in generating business and

which consume it.

Performance evaluation: Through performance of this function effective control is

established over the organisation. This will enables the manager to compare the actual

performance of employees with standards and remove the issues which results in

decrement of their performance.

Different type of budget and their advantages and disadvantages

Fixed and flexible budget: Fixed budgets are such which cannot be changed according

to the changes happen in sales and some other activities of organisation. This is also known as

static budget. On the other hand, flexible budget is having the characteristic regarding make

changes according to situations which are present in business.

Advantages of fixed budget

It is based on historical data and according to the current financial position

It is straightforward to formulate

Disadvantages of fixed budget

It is rigid in nature and not having the option to make changes as per conditions

Advantages of flexible budget

It easy to make changes as per factors

Helpful in determination of performance of different departments

Disadvantages of flexible budget

Not maintain the proper record of discounts available on purchase of goods and services

Functional budget: It is refers as the process which includes preparation of cost and

income plan regarding particular process and department functioning within the organisation

(Fullerton, Kennedy and Widener, 2013.). This will includes estimation regarding cost of

production, marketing, sales, labour, equipments etc.

Advantages

Provides target to the individuals functional manager

Helps in determination of the issues at gross root level

Disadvantages

Conflicts are arise in between organisational and departmental objectives

These budgets are based on forecasts

established over the organisation. This will enables the manager to compare the actual

performance of employees with standards and remove the issues which results in

decrement of their performance.

Different type of budget and their advantages and disadvantages

Fixed and flexible budget: Fixed budgets are such which cannot be changed according

to the changes happen in sales and some other activities of organisation. This is also known as

static budget. On the other hand, flexible budget is having the characteristic regarding make

changes according to situations which are present in business.

Advantages of fixed budget

It is based on historical data and according to the current financial position

It is straightforward to formulate

Disadvantages of fixed budget

It is rigid in nature and not having the option to make changes as per conditions

Advantages of flexible budget

It easy to make changes as per factors

Helpful in determination of performance of different departments

Disadvantages of flexible budget

Not maintain the proper record of discounts available on purchase of goods and services

Functional budget: It is refers as the process which includes preparation of cost and

income plan regarding particular process and department functioning within the organisation

(Fullerton, Kennedy and Widener, 2013.). This will includes estimation regarding cost of

production, marketing, sales, labour, equipments etc.

Advantages

Provides target to the individuals functional manager

Helps in determination of the issues at gross root level

Disadvantages

Conflicts are arise in between organisational and departmental objectives

These budgets are based on forecasts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.