Management Accounting Report: Analysis of Imda Tech Limited Operations

VerifiedAdded on 2019/12/04

|16

|4414

|458

Report

AI Summary

This report offers a comprehensive overview of management accounting principles, using Imda Tech Limited as a case study. It delves into key concepts such as management accounting, its types, and its significance in decision-making. The report details the differences between financial and management accounting, emphasizing the role of management accounting information for administrative section managers. It explores various costing methods, including absorption and marginal costing, providing calculations and income statements for each. Additionally, the report covers different types of budgets, their pros and cons, and the relevance of valuation in budget formation, along with the process of budget preparation and pricing strategies. Furthermore, it discusses the importance of scorecards in organizational performance measurement. The analysis includes detailed calculations and comparisons, making it a valuable resource for understanding management accounting practices. The report is available on Desklib, a platform providing AI-based study tools for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Management Accounting.................................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK1........................................................................................................................................3

a)Management accounting..........................................................................................................3

b) Types of management accounting..........................................................................................6

TASK 2............................................................................................................................................7

Calculation of net profit using absorption costing and marginal costing techniques:................7

TASK 3............................................................................................................................................9

(a) various types of budgets and pros and cons and relevance of valuation in budget

formation.....................................................................................................................................9

b)Process of budget preparation:...............................................................................................11

c)Pricing strategies....................................................................................................................11

TASK 4..........................................................................................................................................12

Importance of scorecard in organisation:..................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Management Accounting.................................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK1........................................................................................................................................3

a)Management accounting..........................................................................................................3

b) Types of management accounting..........................................................................................6

TASK 2............................................................................................................................................7

Calculation of net profit using absorption costing and marginal costing techniques:................7

TASK 3............................................................................................................................................9

(a) various types of budgets and pros and cons and relevance of valuation in budget

formation.....................................................................................................................................9

b)Process of budget preparation:...............................................................................................11

c)Pricing strategies....................................................................................................................11

TASK 4..........................................................................................................................................12

Importance of scorecard in organisation:..................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting exercise in the administration of the organisation is not an

elementary job. Nevertheless there are some professional accountants who are particularly

disciplined for assembly the management exercise in command to achieve the main non

subjective and future goals in the firm Imda Tech limited management accountants does the

management accounting exercise for the reporting to the internal management for impressive

operation(Zimmerman, and Yahya-Zadeh,2011). Now, there has been some drastic changes

emerged in the management accounting since this concept was come. Now the management

accounting does not only reports to the internal management but also assist the firm in command

to achieve the property development. efficacious application of management accounting

practices helps the firm to run the operational management smoothly. Imda Tech Limited is

running so efficiently due to expeditious and effectual management accounting practices

attainment of the objectives. Management accounting is more peculiarly known fro the

combining of operations , strategic planning and administrations. Management accounting

practices support the higher level authority for framing the strategical plan for smooth running

the operational process.

TASK1.

a)Management accounting.

Management accounting is a method in which we use judgement applicable fiscal and

non fiscal complacent to domain and create the value of administration by origin, investigating

and communicating. It is a accumulation of finance, accounting and management with the

enterprise skills and methods. It is for addition the value in an organisation(aldvinsdottir,

Mitchell, and Nørreklit,2010). The accountants those who are working in an organisation and

they are suitable to work across the counsel managers on the fiscal express of determination, not

just in finance, activity across the enterprise the observation risk and enterprise strategies is more

crunching than numbers of the data which had given. In this mangers needed data to make daily

bases decision. It is assorted from fiscal accounting because in that we have to make annually

statements for the stakeholders and the weekly statement is done by chief executive officer and

section manager. In this statement we can display the available money and the revenue is

generated, raw material, divergence analysis,The entire sum of debt and obligations on a

Management accounting exercise in the administration of the organisation is not an

elementary job. Nevertheless there are some professional accountants who are particularly

disciplined for assembly the management exercise in command to achieve the main non

subjective and future goals in the firm Imda Tech limited management accountants does the

management accounting exercise for the reporting to the internal management for impressive

operation(Zimmerman, and Yahya-Zadeh,2011). Now, there has been some drastic changes

emerged in the management accounting since this concept was come. Now the management

accounting does not only reports to the internal management but also assist the firm in command

to achieve the property development. efficacious application of management accounting

practices helps the firm to run the operational management smoothly. Imda Tech Limited is

running so efficiently due to expeditious and effectual management accounting practices

attainment of the objectives. Management accounting is more peculiarly known fro the

combining of operations , strategic planning and administrations. Management accounting

practices support the higher level authority for framing the strategical plan for smooth running

the operational process.

TASK1.

a)Management accounting.

Management accounting is a method in which we use judgement applicable fiscal and

non fiscal complacent to domain and create the value of administration by origin, investigating

and communicating. It is a accumulation of finance, accounting and management with the

enterprise skills and methods. It is for addition the value in an organisation(aldvinsdottir,

Mitchell, and Nørreklit,2010). The accountants those who are working in an organisation and

they are suitable to work across the counsel managers on the fiscal express of determination, not

just in finance, activity across the enterprise the observation risk and enterprise strategies is more

crunching than numbers of the data which had given. In this mangers needed data to make daily

bases decision. It is assorted from fiscal accounting because in that we have to make annually

statements for the stakeholders and the weekly statement is done by chief executive officer and

section manager. In this statement we can display the available money and the revenue is

generated, raw material, divergence analysis,The entire sum of debt and obligations on a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation's balance sheet that remains unpaid consider short term expenses, outstanding

payables, and accumulated interest(Lukka,and Modell, 2010).

Scope of Management.

Progression in information technology the client will get the information with the help of

technology before 10 to 20 years client will don't know about the scope of management

accounting. Management accounting is all about better management of companies. In this we can

include amended marketing scheme, feasibleness studies,better valuation of trade good and

services through capable cost management strategies. If we motivate the employees they will

advantage to the organisation(Garrison, and et. al., 2010). By the help of technology we can take

better management risk,leverage on opportunities,protective covering of organisation possession

and investing through crime prevention function of management accounting,Managing

environmental modification we can easily deal with the politics and by the law.

Characteristic of Management accounting system. Cost reduction information processing capacity-Management accounting helps in cost

reduction by the help of information system. We can scrutinize that how to reduce our

cost from the marketplace.

Ability to collecting broad range of information-It has ability to collect the wide range

information through the world.

A explanation instrument is not to be used-It is not necessary to explain the management

accounting by the justification instrument.

Difference between Financial accounting and Management accounting.

Management accounting Financial accounting.

Management Accounting is the procedure of

determination, measuring, accretion, analysis,

formulation, representation and act of data that

utilised by management to plan, measure, and

control inside an entity and to guarantee

befitting use of an accountability for its

resources.

Management accounting is to help

administration by rendering data which

Financial accounting is obsessed with render

data to the stockholders, creditors, and others

who are external structure. management

system render the necessary data with which

companies are really run. Financial accounting

supply the record by which a organisation’s

ago performance is noticed.

Financial accounting is to expose the

last output of the enterprise

payables, and accumulated interest(Lukka,and Modell, 2010).

Scope of Management.

Progression in information technology the client will get the information with the help of

technology before 10 to 20 years client will don't know about the scope of management

accounting. Management accounting is all about better management of companies. In this we can

include amended marketing scheme, feasibleness studies,better valuation of trade good and

services through capable cost management strategies. If we motivate the employees they will

advantage to the organisation(Garrison, and et. al., 2010). By the help of technology we can take

better management risk,leverage on opportunities,protective covering of organisation possession

and investing through crime prevention function of management accounting,Managing

environmental modification we can easily deal with the politics and by the law.

Characteristic of Management accounting system. Cost reduction information processing capacity-Management accounting helps in cost

reduction by the help of information system. We can scrutinize that how to reduce our

cost from the marketplace.

Ability to collecting broad range of information-It has ability to collect the wide range

information through the world.

A explanation instrument is not to be used-It is not necessary to explain the management

accounting by the justification instrument.

Difference between Financial accounting and Management accounting.

Management accounting Financial accounting.

Management Accounting is the procedure of

determination, measuring, accretion, analysis,

formulation, representation and act of data that

utilised by management to plan, measure, and

control inside an entity and to guarantee

befitting use of an accountability for its

resources.

Management accounting is to help

administration by rendering data which

Financial accounting is obsessed with render

data to the stockholders, creditors, and others

who are external structure. management

system render the necessary data with which

companies are really run. Financial accounting

supply the record by which a organisation’s

ago performance is noticed.

Financial accounting is to expose the

last output of the enterprise

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

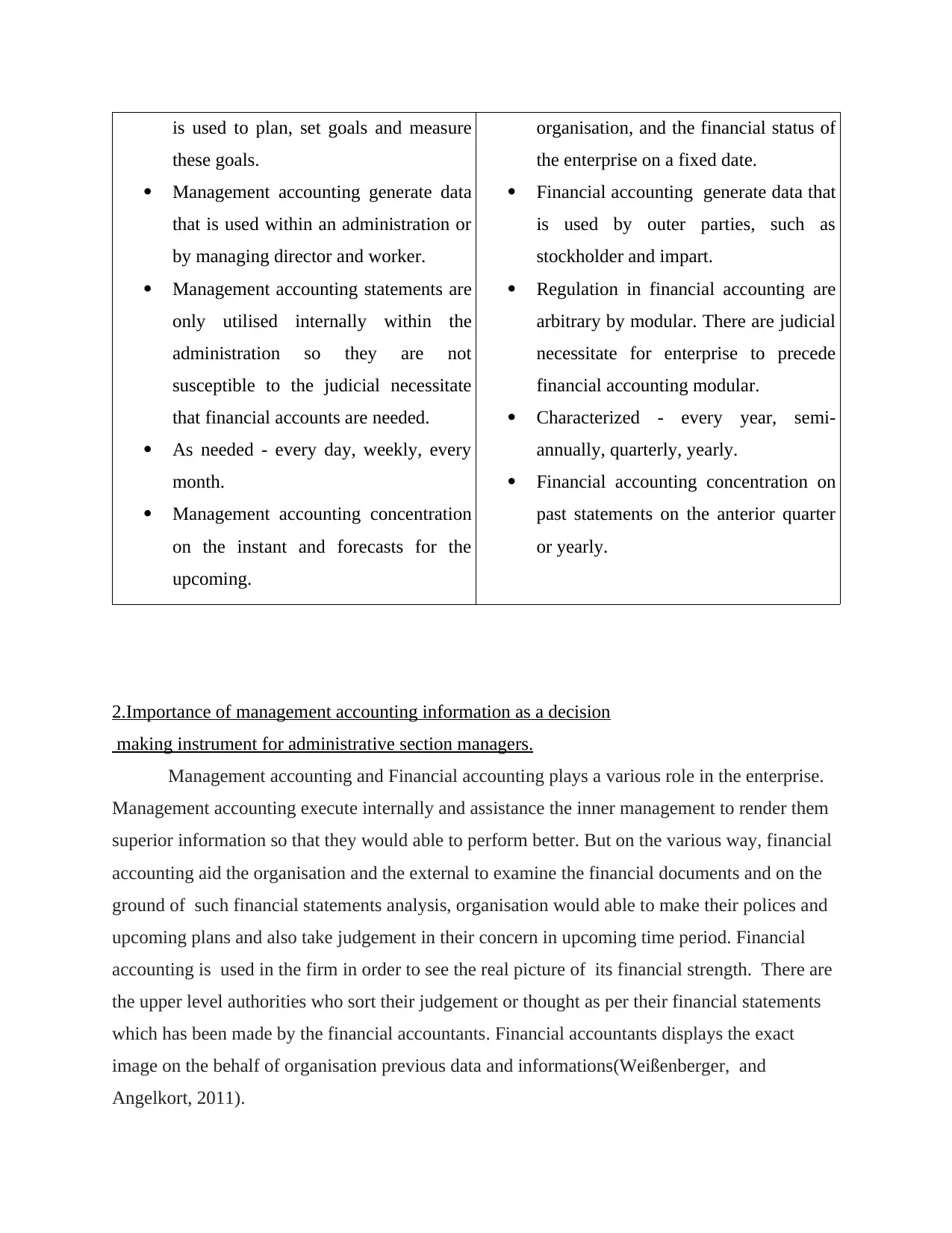

is used to plan, set goals and measure

these goals.

Management accounting generate data

that is used within an administration or

by managing director and worker.

Management accounting statements are

only utilised internally within the

administration so they are not

susceptible to the judicial necessitate

that financial accounts are needed.

As needed - every day, weekly, every

month.

Management accounting concentration

on the instant and forecasts for the

upcoming.

organisation, and the financial status of

the enterprise on a fixed date.

Financial accounting generate data that

is used by outer parties, such as

stockholder and impart.

Regulation in financial accounting are

arbitrary by modular. There are judicial

necessitate for enterprise to precede

financial accounting modular.

Characterized - every year, semi-

annually, quarterly, yearly.

Financial accounting concentration on

past statements on the anterior quarter

or yearly.

2.Importance of management accounting information as a decision

making instrument for administrative section managers.

Management accounting and Financial accounting plays a various role in the enterprise.

Management accounting execute internally and assistance the inner management to render them

superior information so that they would able to perform better. But on the various way, financial

accounting aid the organisation and the external to examine the financial documents and on the

ground of such financial statements analysis, organisation would able to make their polices and

upcoming plans and also take judgement in their concern in upcoming time period. Financial

accounting is used in the firm in order to see the real picture of its financial strength. There are

the upper level authorities who sort their judgement or thought as per their financial statements

which has been made by the financial accountants. Financial accountants displays the exact

image on the behalf of organisation previous data and informations(Weißenberger, and

Angelkort, 2011).

these goals.

Management accounting generate data

that is used within an administration or

by managing director and worker.

Management accounting statements are

only utilised internally within the

administration so they are not

susceptible to the judicial necessitate

that financial accounts are needed.

As needed - every day, weekly, every

month.

Management accounting concentration

on the instant and forecasts for the

upcoming.

organisation, and the financial status of

the enterprise on a fixed date.

Financial accounting generate data that

is used by outer parties, such as

stockholder and impart.

Regulation in financial accounting are

arbitrary by modular. There are judicial

necessitate for enterprise to precede

financial accounting modular.

Characterized - every year, semi-

annually, quarterly, yearly.

Financial accounting concentration on

past statements on the anterior quarter

or yearly.

2.Importance of management accounting information as a decision

making instrument for administrative section managers.

Management accounting and Financial accounting plays a various role in the enterprise.

Management accounting execute internally and assistance the inner management to render them

superior information so that they would able to perform better. But on the various way, financial

accounting aid the organisation and the external to examine the financial documents and on the

ground of such financial statements analysis, organisation would able to make their polices and

upcoming plans and also take judgement in their concern in upcoming time period. Financial

accounting is used in the firm in order to see the real picture of its financial strength. There are

the upper level authorities who sort their judgement or thought as per their financial statements

which has been made by the financial accountants. Financial accountants displays the exact

image on the behalf of organisation previous data and informations(Weißenberger, and

Angelkort, 2011).

b) Types of management accounting.

Management accounting can be categorized below antithetic heads. This system render aid to the

administration by supporting the administrator to take various judgement with the help of various

statements conferred under various accounting system. These statements help in conformation

the precursory year statements which help in doing the process of comparison. It helps in taking

the corrective measures by the managers which gave less results in the previous time period.

various types of accounting systems can be studied under various heads which give long and

short benefit to the organisation(Cinquini, and Tenucci, 2010). Cost accounting: This accounting system is concerned with the various cost of the trade

goods. With the help of this system managers take various decisions regarding the

finance allotment. After analysing the various options available with the managers they

choose the best suitable one by comparing it with the past year statements. Cost

accounting also help in keeping control over the various cost of production by keeping

proper check on the various factor of the production process. With the help of this system

organisation can take the decision of future enlargement also. Inventory Management: inventory refers to the raw material kept in the enterprise which

will be converted into final goods by processing them(Cinquini and Tenucci, 2010). It is

essential to have good inventory management system so that situation of non accessibility

of raw material can be avoided as this will lead to wastage of time and also loss of

potential customers. It is also essential to avoid the situation of excess in the organisation

in order to avoid the cost of storage and maintenance which further is added to the total

cost of the trade good. Job costing system: In an organisation various jobs has there various cost which is

ultimately added to the trade good. As much deviation in the cost of the trade good can

not be done keeping in mind the cost sensitivity in the marketplace. All the customers

before buying any trade good do the comparison of all the trade goods available in the

marketplace. Therefore high cost can not charged from the buyers.

cost optimising system: Earlier fixing the cost of the trade good it is essential to scrutinize

the cost of the other related goods also so that the cost get acceptable by other client in

the marketplace. At first it is essential to keep the cost relatively low so that more

customers get attracted towards it(Luft and Shields, 2010.). Only if the client find the

Management accounting can be categorized below antithetic heads. This system render aid to the

administration by supporting the administrator to take various judgement with the help of various

statements conferred under various accounting system. These statements help in conformation

the precursory year statements which help in doing the process of comparison. It helps in taking

the corrective measures by the managers which gave less results in the previous time period.

various types of accounting systems can be studied under various heads which give long and

short benefit to the organisation(Cinquini, and Tenucci, 2010). Cost accounting: This accounting system is concerned with the various cost of the trade

goods. With the help of this system managers take various decisions regarding the

finance allotment. After analysing the various options available with the managers they

choose the best suitable one by comparing it with the past year statements. Cost

accounting also help in keeping control over the various cost of production by keeping

proper check on the various factor of the production process. With the help of this system

organisation can take the decision of future enlargement also. Inventory Management: inventory refers to the raw material kept in the enterprise which

will be converted into final goods by processing them(Cinquini and Tenucci, 2010). It is

essential to have good inventory management system so that situation of non accessibility

of raw material can be avoided as this will lead to wastage of time and also loss of

potential customers. It is also essential to avoid the situation of excess in the organisation

in order to avoid the cost of storage and maintenance which further is added to the total

cost of the trade good. Job costing system: In an organisation various jobs has there various cost which is

ultimately added to the trade good. As much deviation in the cost of the trade good can

not be done keeping in mind the cost sensitivity in the marketplace. All the customers

before buying any trade good do the comparison of all the trade goods available in the

marketplace. Therefore high cost can not charged from the buyers.

cost optimising system: Earlier fixing the cost of the trade good it is essential to scrutinize

the cost of the other related goods also so that the cost get acceptable by other client in

the marketplace. At first it is essential to keep the cost relatively low so that more

customers get attracted towards it(Luft and Shields, 2010.). Only if the client find the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

trade good worth of the cost they will try the new trade good otherwise it is challenging

to give position to the trade good in the competition external.

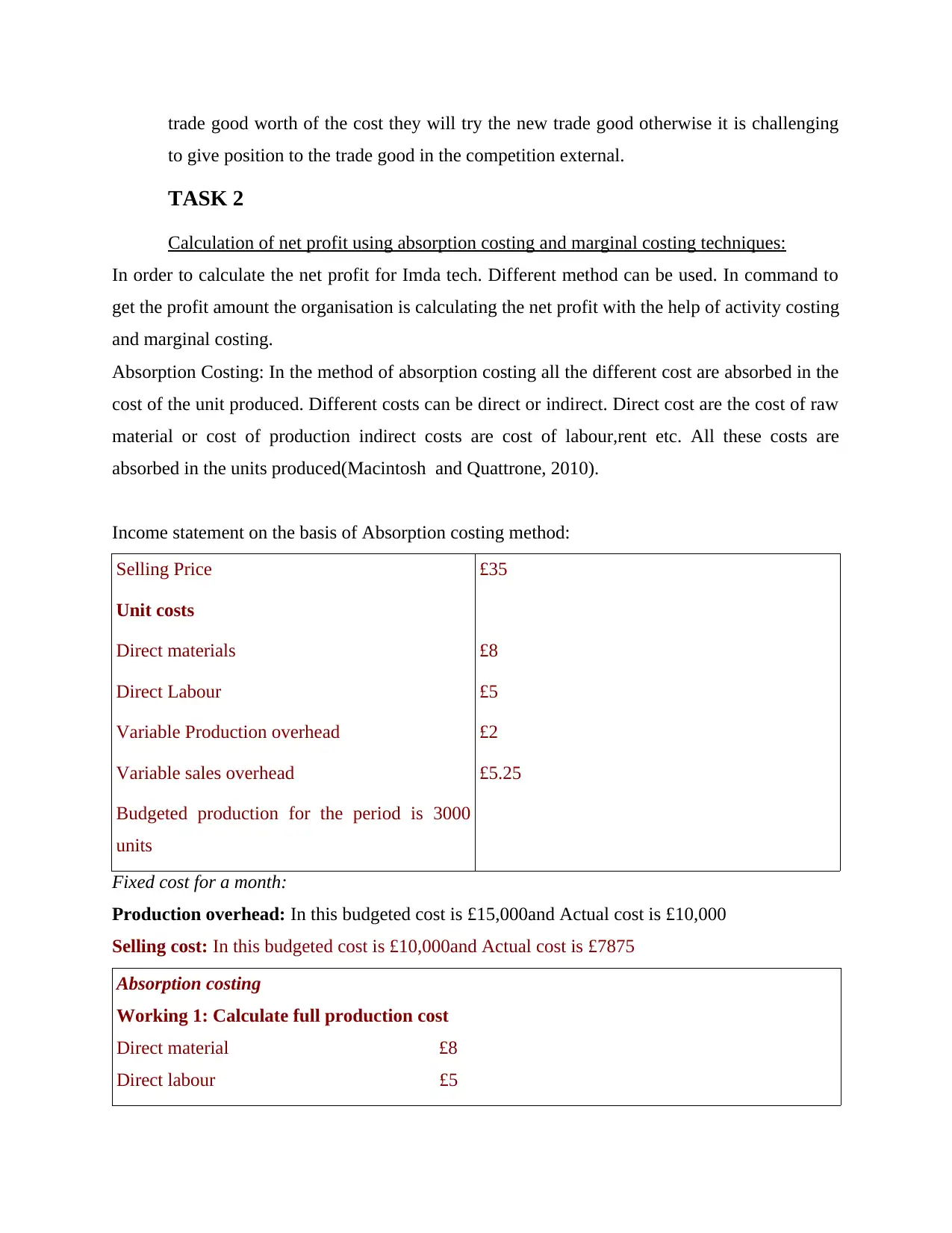

TASK 2

Calculation of net profit using absorption costing and marginal costing techniques:

In order to calculate the net profit for Imda tech. Different method can be used. In command to

get the profit amount the organisation is calculating the net profit with the help of activity costing

and marginal costing.

Absorption Costing: In the method of absorption costing all the different cost are absorbed in the

cost of the unit produced. Different costs can be direct or indirect. Direct cost are the cost of raw

material or cost of production indirect costs are cost of labour,rent etc. All these costs are

absorbed in the units produced(Macintosh and Quattrone, 2010).

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

to give position to the trade good in the competition external.

TASK 2

Calculation of net profit using absorption costing and marginal costing techniques:

In order to calculate the net profit for Imda tech. Different method can be used. In command to

get the profit amount the organisation is calculating the net profit with the help of activity costing

and marginal costing.

Absorption Costing: In the method of absorption costing all the different cost are absorbed in the

cost of the unit produced. Different costs can be direct or indirect. Direct cost are the cost of raw

material or cost of production indirect costs are cost of labour,rent etc. All these costs are

absorbed in the units produced(Macintosh and Quattrone, 2010).

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

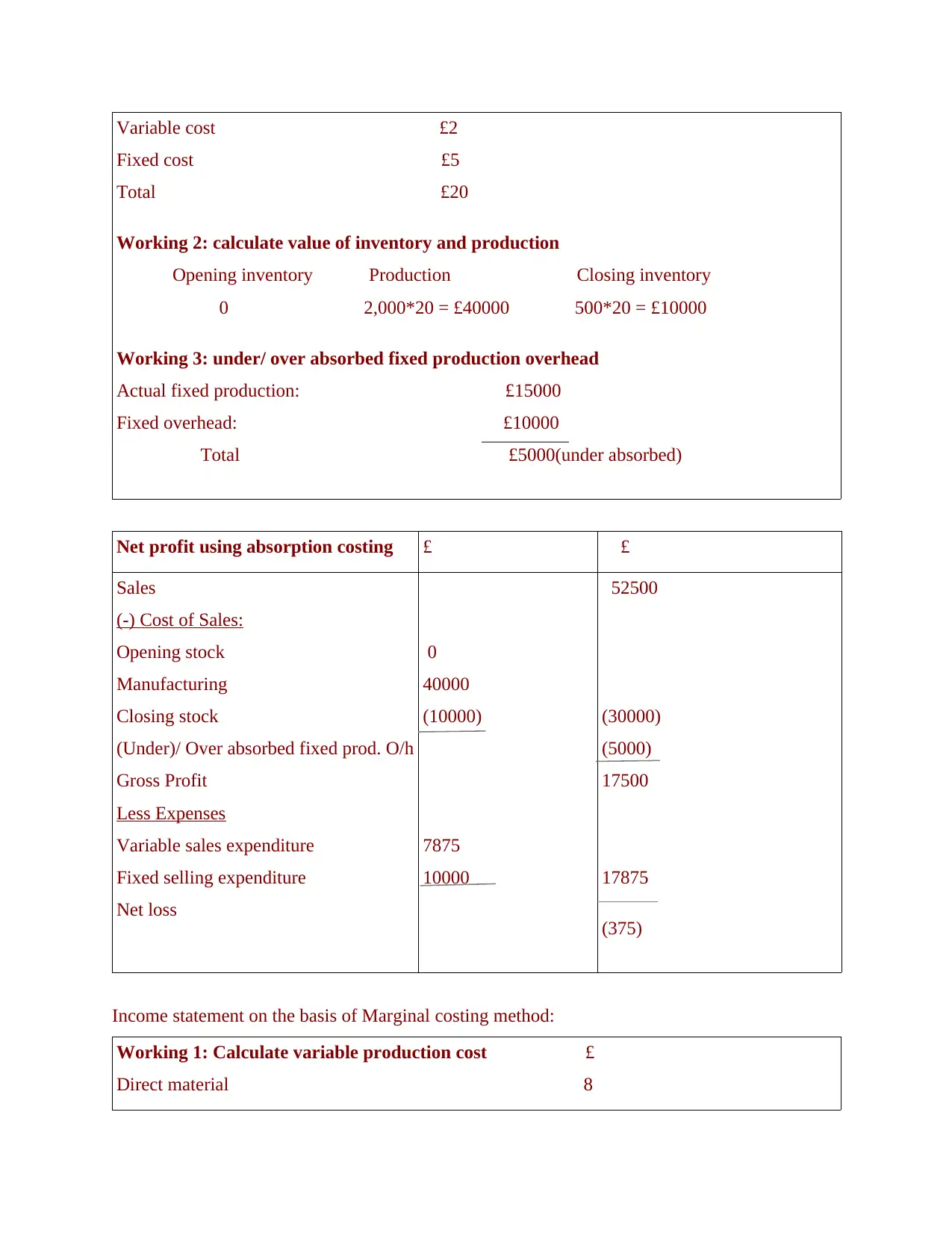

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

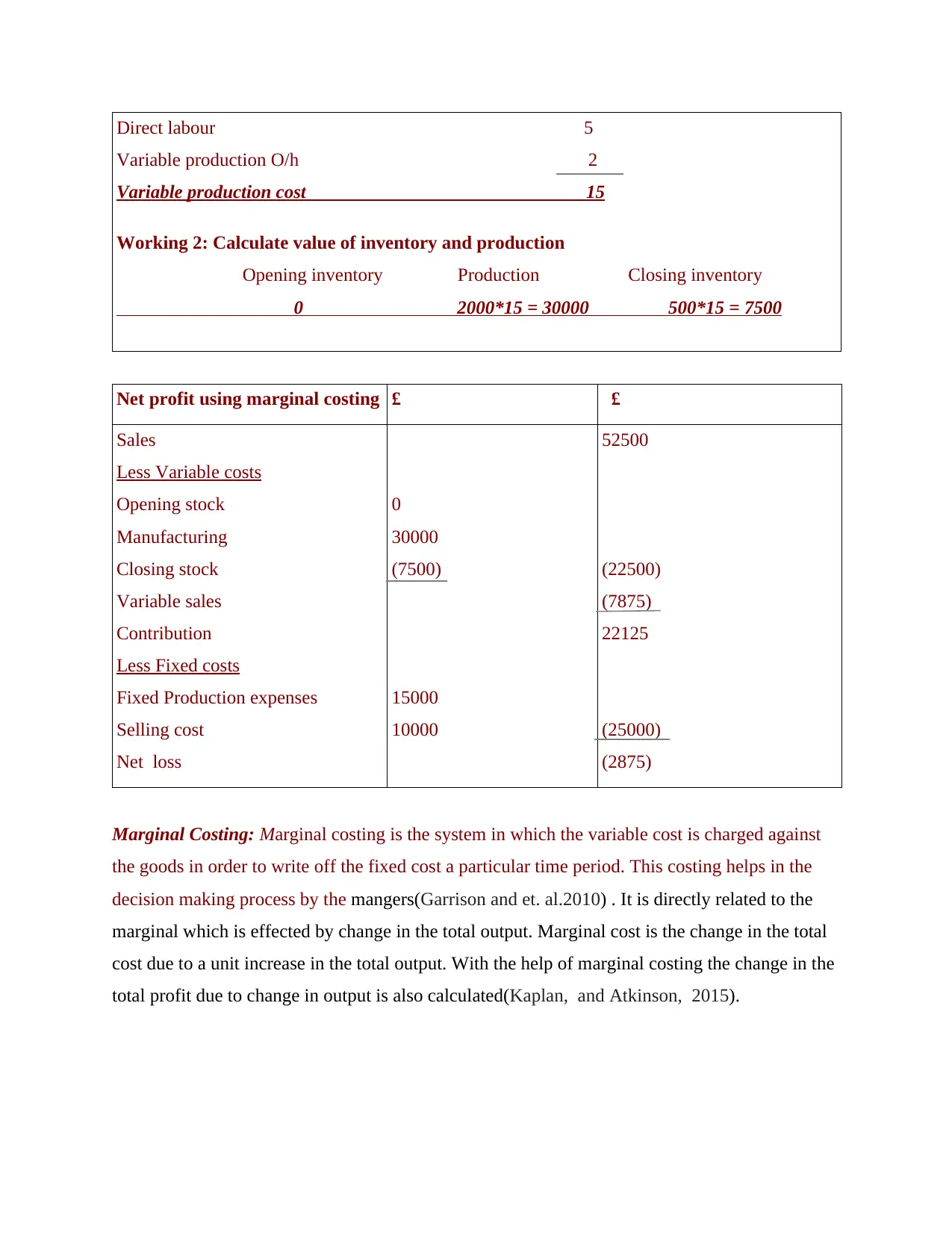

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal Costing: Marginal costing is the system in which the variable cost is charged against

the goods in order to write off the fixed cost a particular time period. This costing helps in the

decision making process by the mangers(Garrison and et. al.2010) . It is directly related to the

marginal which is effected by change in the total output. Marginal cost is the change in the total

cost due to a unit increase in the total output. With the help of marginal costing the change in the

total profit due to change in output is also calculated(Kaplan, and Atkinson, 2015).

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal Costing: Marginal costing is the system in which the variable cost is charged against

the goods in order to write off the fixed cost a particular time period. This costing helps in the

decision making process by the mangers(Garrison and et. al.2010) . It is directly related to the

marginal which is effected by change in the total output. Marginal cost is the change in the total

cost due to a unit increase in the total output. With the help of marginal costing the change in the

total profit due to change in output is also calculated(Kaplan, and Atkinson, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

(a) various types of budgets and pros and cons and relevance of valuation in budget

formation

Budgets play an essential role in any organisation. It helps in efficacious allocation of the

finance of the organisation so that maximum returns can be achieved. Through budgeting process

the mangers keep control on the total cost of the various projects. Each administrative section is

given their budgets and this way they check that they do not transcend the given budget line as

than actions are taken in that case. There are various types of budgets which can be used by the

cited organisation to have efficacious working environment in the organisation. These budgets

can be long term or short term budgets depending upon the need of the project.

Master budget-It is the main budget of the organisation. Under this budget all the

resources are allocated in various administrative sections like the sales administrative section,

administrative section etc. each administrative section is given their goals and resources are also

rendered to them which may be needed during the project working. This budget has its own

positive and negatives(Van Helden. And et. al., 2010).

stockholder of master budget.

1. It gives the summary of all the other small budgets that are prepared. Also the other budgets

are prepared after the master budget is prepared.

2. These budgets helps in getting the estimation of the total profit earned in a particular time

period.

a)Apart from these master budgets have some stockholder also:

As this budgets are a combination of all the other small budgets,it becomes difficult for the top

management to calculate the spending of various administrative section. Therefore it can not be

calculated that in which administrative section maximum expense is done(Cinquini, and Tenucci,

2010).

b) As all the details of each administrative section budgets are given in the same budget report it

becomes difficult to understand and there are also chance of loss of quality information.

2.Operating budget: These budgets are related to the daily operations of the enterprise it helps by

providing budgets for various operations of the enterprise. various operations needs to be budget

variously as operations has their own priority in the organisation.

(a) various types of budgets and pros and cons and relevance of valuation in budget

formation

Budgets play an essential role in any organisation. It helps in efficacious allocation of the

finance of the organisation so that maximum returns can be achieved. Through budgeting process

the mangers keep control on the total cost of the various projects. Each administrative section is

given their budgets and this way they check that they do not transcend the given budget line as

than actions are taken in that case. There are various types of budgets which can be used by the

cited organisation to have efficacious working environment in the organisation. These budgets

can be long term or short term budgets depending upon the need of the project.

Master budget-It is the main budget of the organisation. Under this budget all the

resources are allocated in various administrative sections like the sales administrative section,

administrative section etc. each administrative section is given their goals and resources are also

rendered to them which may be needed during the project working. This budget has its own

positive and negatives(Van Helden. And et. al., 2010).

stockholder of master budget.

1. It gives the summary of all the other small budgets that are prepared. Also the other budgets

are prepared after the master budget is prepared.

2. These budgets helps in getting the estimation of the total profit earned in a particular time

period.

a)Apart from these master budgets have some stockholder also:

As this budgets are a combination of all the other small budgets,it becomes difficult for the top

management to calculate the spending of various administrative section. Therefore it can not be

calculated that in which administrative section maximum expense is done(Cinquini, and Tenucci,

2010).

b) As all the details of each administrative section budgets are given in the same budget report it

becomes difficult to understand and there are also chance of loss of quality information.

2.Operating budget: These budgets are related to the daily operations of the enterprise it helps by

providing budgets for various operations of the enterprise. various operations needs to be budget

variously as operations has their own priority in the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pros of operating budget.

a) Operating budgeting helps in maintaining adequate amount of liquidity for the operations of

the enterprise which can not be avoided by the organisation like buying of raw material, wages to

employees rent etc.

b) It helps the organisation in increasing the total reserves by providing the best alternatives for

the purpose of investment. For making the investment it is essential to have the adequate amount

of reserve with the organisation.

cons of operating budget.

a) It require a separate body to maintain the operation budgets which leads to the increase in the

total cost of the organisation.

3. Financial budget: In this budgets for various functions are prepared under various headings. It

is adopted in all the organisation as it is essential to set the budgets so that if in case finance is

needed in the organisation arrangements can be done in advance.

a)pros and cons of financial budgets.

1. Maintain efficaciousness in various functions of the organisation.

2. Timely availability of the finance is done through the process of financial budgeting.

3. As this budgeting system is involved with finance which is very difficult to manage therefore

it becomes a problem to maintain these budgets and to make the efficacious budget for a specific

function.

b)Process of budget preparation:

1. The first step is to to roll up all the needed data. In this information regarding the need of

budget is discovered. It is an essential part and need to be done by giving full efforts.

Database of various expenses are made so that they can be categorised into various heads

depending upon their urgencies. Planning is done how the total finance of the

organisation can be utilised so that it can full fill the necessitate of each administrative

sections. After the need of each administrative section is recognised budgets are allotted

to them which the administrative section has to follow to complete their given project.

administrative sections are rendered with all the needed resources so that they can

a) Operating budgeting helps in maintaining adequate amount of liquidity for the operations of

the enterprise which can not be avoided by the organisation like buying of raw material, wages to

employees rent etc.

b) It helps the organisation in increasing the total reserves by providing the best alternatives for

the purpose of investment. For making the investment it is essential to have the adequate amount

of reserve with the organisation.

cons of operating budget.

a) It require a separate body to maintain the operation budgets which leads to the increase in the

total cost of the organisation.

3. Financial budget: In this budgets for various functions are prepared under various headings. It

is adopted in all the organisation as it is essential to set the budgets so that if in case finance is

needed in the organisation arrangements can be done in advance.

a)pros and cons of financial budgets.

1. Maintain efficaciousness in various functions of the organisation.

2. Timely availability of the finance is done through the process of financial budgeting.

3. As this budgeting system is involved with finance which is very difficult to manage therefore

it becomes a problem to maintain these budgets and to make the efficacious budget for a specific

function.

b)Process of budget preparation:

1. The first step is to to roll up all the needed data. In this information regarding the need of

budget is discovered. It is an essential part and need to be done by giving full efforts.

Database of various expenses are made so that they can be categorised into various heads

depending upon their urgencies. Planning is done how the total finance of the

organisation can be utilised so that it can full fill the necessitate of each administrative

sections. After the need of each administrative section is recognised budgets are allotted

to them which the administrative section has to follow to complete their given project.

administrative sections are rendered with all the needed resources so that they can

complete their project with the given budget. After this the budget is reviewed before

doing the declaration. At this stage the possibilities of achieving the target with the given

budget is examined again. Lastly, the budget is declared to the concerned administrative

sections(Fullerton, Kennedy, and Widener, 2013).

c)Pricing strategies

Adopting the pricing strategies help the enterprise to keep the efficacious control on the

cost of the enterprise and also to achieve the best price for its good. enterprise can use various

pricing strategies like: Penetration Pricing: This is the process of price taking. Manufacturer has to keep their

price relatively low in comparison to other goods in order to cover more market and than

gradually can increase the price once it is recognised by all. Premium pricing: In this the Manufacturer can set the price according to himself as they

are providing with the good quality(Luft, and Shields, 2010). Customer is also willing to

pay high price due to the difference in the good type and quality.

Skimming pricing strategies: goods for high class society are produced in this pricing.

They charge high price from the customer at the starting and customer find it as a status

symbol to buy expensive goods. Though the price fall after a certain time period.

All these strategies need to be consider while making the budget to make it more efficacious and

approved by all.

TASK 4

Importance of scorecard in organisation:

Scorecard has become a famous instrument nowadays. It helps in maintaining the record

of an individual performance in a particular period of time. Also with the help of this instrument

comparison between various employees over a period of time has become more easy. It is

essential to have the environment of comparison in the organisation so that everyone work

towards giving their best. This help the organisation to get the work done in time and also in the

best manner. Balanced scorecards help the management to overcome the external factors by

doing the efficacious planning in advance. As the organisation is suffering loss it can utilise this

instrument for efficacious planning and take better actions. Balance scorecard is the procedure of

doing the declaration. At this stage the possibilities of achieving the target with the given

budget is examined again. Lastly, the budget is declared to the concerned administrative

sections(Fullerton, Kennedy, and Widener, 2013).

c)Pricing strategies

Adopting the pricing strategies help the enterprise to keep the efficacious control on the

cost of the enterprise and also to achieve the best price for its good. enterprise can use various

pricing strategies like: Penetration Pricing: This is the process of price taking. Manufacturer has to keep their

price relatively low in comparison to other goods in order to cover more market and than

gradually can increase the price once it is recognised by all. Premium pricing: In this the Manufacturer can set the price according to himself as they

are providing with the good quality(Luft, and Shields, 2010). Customer is also willing to

pay high price due to the difference in the good type and quality.

Skimming pricing strategies: goods for high class society are produced in this pricing.

They charge high price from the customer at the starting and customer find it as a status

symbol to buy expensive goods. Though the price fall after a certain time period.

All these strategies need to be consider while making the budget to make it more efficacious and

approved by all.

TASK 4

Importance of scorecard in organisation:

Scorecard has become a famous instrument nowadays. It helps in maintaining the record

of an individual performance in a particular period of time. Also with the help of this instrument

comparison between various employees over a period of time has become more easy. It is

essential to have the environment of comparison in the organisation so that everyone work

towards giving their best. This help the organisation to get the work done in time and also in the

best manner. Balanced scorecards help the management to overcome the external factors by

doing the efficacious planning in advance. As the organisation is suffering loss it can utilise this

instrument for efficacious planning and take better actions. Balance scorecard is the procedure of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.