Management Accounting Report: Cambridge Manufacturing Analysis

VerifiedAdded on 2021/02/20

|19

|5878

|99

Report

AI Summary

This report comprehensively examines management accounting, focusing on its systems, methodologies, and application within a manufacturing context. It begins with an introduction to management accounting, its role in decision-making, and an overview of the Cambridge Manufacturing Company Ltd. The report delves into different types of management accounting systems, including inventory management, price optimization, cost accounting, and job costing. It explores various reporting methodologies like variance analysis, budget reports, and performance reports. Task 2 focuses on cost calculation techniques, including marginal and absorption costing, and the preparation of income statements. The report also evaluates the advantages and disadvantages of planning tools used for budgetary control, comparing organizations' responses to financial problems and assessing how management accounting contributes to sustainable success. The analysis includes detailed calculations and critical evaluations of accounting systems within organizational processes.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

P1 Explanation of management accounting and its different types of system. ..........................3

P2. Different methodologies employed used in Management Accounting Reporting................5

M1 Benefits of management accounting system:.......................................................................6

D1 Critically evaluation of management accounting systems and reports integrated within

organisational processes..............................................................................................................7

TASK 2............................................................................................................................................7

P3 Calculation of costs using appropriate techniques to prepare income statement. .................7

M2. Various Techniques of Management Accounting System..................................................9

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.......................................................................................................................................10

M3 Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................12

P5 Comparison of organisations while adapting management accounting systems to respond

to financial problems.................................................................................................................12

M4 Responding to financial problems, management accounting can lead organisations to

sustainable success....................................................................................................................14

D3 Evaluate how planning tools ..............................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

P1 Explanation of management accounting and its different types of system. ..........................3

P2. Different methodologies employed used in Management Accounting Reporting................5

M1 Benefits of management accounting system:.......................................................................6

D1 Critically evaluation of management accounting systems and reports integrated within

organisational processes..............................................................................................................7

TASK 2............................................................................................................................................7

P3 Calculation of costs using appropriate techniques to prepare income statement. .................7

M2. Various Techniques of Management Accounting System..................................................9

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................9

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.......................................................................................................................................10

M3 Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................12

P5 Comparison of organisations while adapting management accounting systems to respond

to financial problems.................................................................................................................12

M4 Responding to financial problems, management accounting can lead organisations to

sustainable success....................................................................................................................14

D3 Evaluate how planning tools ..............................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

2

INTRODUCTION

Management accounting is a systematic set of activities which includes activities related

to deep analysis of various expenses of business and preparation of internal financial report

which assist managerial personnel’s in decision making activities to achieve objectives of

business organisation (Aksoylu and Aykan, 2013). It simply refers to providing relevant financial

performance to top management for the purpose of strategy formulation and implementation.

This report contains an explanation about management accounting system and its types along

with benefits, various methods of management accounting reporting, use of planning tools and,

advantages and disadvantages of planning tools in the context of Cambridge Manufacturing

Company Ltd., a medium size manufacturing company. It is a manufacturer of weight loss

supplements in UK. This report also exhibits comparison of ways in which organisations could

use management

accounting to respond to financial problems and analysis of how and to what extent, responding

to financial problem help in achievement of sustainable success.

Task 1

P1 Explanation of management accounting and its different types of system.

Management accounting system implies to a set of activities which involves preparation

and reporting of financial and accounting information to managerial personnel’s which assist in

operating organisation's daily activities and functions in effective. It also helps management in

taking short term decisions. Under management accounting system, main motive of different

process is to provide raw information or data to top management for decision-making process.

Management accounting system is adopted by business organisation to assess and evaluate their

actual performance and growth effectively. It simply defied as a systematic process of

preparation of accounts and other management reports that is ultimately used by management to

prepare an action plan for future and to take strategic decisions (Boiral, 2016). In Cambridge

Manufacturing Company Ltd, management accounting is essential aspect of organisation. In

company this system is used for internal analysis of company's activities and functions. In

company, at first divisional and functional managers collect, identify, select and evaluate

information and then communicate or report such information to top level management in

3

Management accounting is a systematic set of activities which includes activities related

to deep analysis of various expenses of business and preparation of internal financial report

which assist managerial personnel’s in decision making activities to achieve objectives of

business organisation (Aksoylu and Aykan, 2013). It simply refers to providing relevant financial

performance to top management for the purpose of strategy formulation and implementation.

This report contains an explanation about management accounting system and its types along

with benefits, various methods of management accounting reporting, use of planning tools and,

advantages and disadvantages of planning tools in the context of Cambridge Manufacturing

Company Ltd., a medium size manufacturing company. It is a manufacturer of weight loss

supplements in UK. This report also exhibits comparison of ways in which organisations could

use management

accounting to respond to financial problems and analysis of how and to what extent, responding

to financial problem help in achievement of sustainable success.

Task 1

P1 Explanation of management accounting and its different types of system.

Management accounting system implies to a set of activities which involves preparation

and reporting of financial and accounting information to managerial personnel’s which assist in

operating organisation's daily activities and functions in effective. It also helps management in

taking short term decisions. Under management accounting system, main motive of different

process is to provide raw information or data to top management for decision-making process.

Management accounting system is adopted by business organisation to assess and evaluate their

actual performance and growth effectively. It simply defied as a systematic process of

preparation of accounts and other management reports that is ultimately used by management to

prepare an action plan for future and to take strategic decisions (Boiral, 2016). In Cambridge

Manufacturing Company Ltd, management accounting is essential aspect of organisation. In

company this system is used for internal analysis of company's activities and functions. In

company, at first divisional and functional managers collect, identify, select and evaluate

information and then communicate or report such information to top level management in

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company to assist them in strategy formulation and implementation. Following are some key

management accounting system that is adopted by Cambridge, as discussed below:

Inventory management system: It is a most significant management accounting system

which is adopted by business organisations for the purpose of effective management of various

inventories like finished goods, raw material, work in progress, closing stock, spare tools etc.

This management accounting system assist in tacking actual and real time movement of various

kind on inventories within a business enterprise. This system also assists in identification of main

cause of increase in abnormal loss or normal loss. As Cambridge Ltd is a manufacture of weight

loss supplements, so inventory management system is essential part company. In company,

various production managers by applying inventory management system monitor the flow of

inventory and minimise additional inventory cost like storage cost, inventory handling costs etc.

In company this system ensures the availability of inventory in manufacturing and production

process.

Price optimisation system: This system is applied by companies to critically analyse the

relationship between demand of product or service and price of product and service. Under this

system business organisation assess a most appropriate price at which demand is maximum. This

system includes a process of analysis of customer's response at different price level of product.

Main motive of this system is to minimise the price of product while maintaining same profit

margin. In Cambridge Ltd, this system is adopted by company to gain competitive advantages by

optimising price of products. Management with help of this system analyse the consumer

response at different price of product to fix a most appropriate price (Bromiley and et.al, 2015).

Cost accounting system: It a kind of management accounting system in which provide

assistance to business organisation in monitor and optimization of various expenses and costs.

This system includes a systematic set of activities like entering, analysing, classifying,

summarizing and evaluation of various expense or costs to develop a frame for controlling these

costs. Main objectives of this system are to enhance the cost efficiency within business

organisation. It assists identification and assessment of excessive costs if any. It also provides

assistance in comparison of actual and budgeted cost. It indicates towards any event which may

incur any additional cost in manufacturing and production cost. In this system is used to analyse

the cost of construction project and any escalation in cost of project. In Cambridge Ltd, this

4

management accounting system that is adopted by Cambridge, as discussed below:

Inventory management system: It is a most significant management accounting system

which is adopted by business organisations for the purpose of effective management of various

inventories like finished goods, raw material, work in progress, closing stock, spare tools etc.

This management accounting system assist in tacking actual and real time movement of various

kind on inventories within a business enterprise. This system also assists in identification of main

cause of increase in abnormal loss or normal loss. As Cambridge Ltd is a manufacture of weight

loss supplements, so inventory management system is essential part company. In company,

various production managers by applying inventory management system monitor the flow of

inventory and minimise additional inventory cost like storage cost, inventory handling costs etc.

In company this system ensures the availability of inventory in manufacturing and production

process.

Price optimisation system: This system is applied by companies to critically analyse the

relationship between demand of product or service and price of product and service. Under this

system business organisation assess a most appropriate price at which demand is maximum. This

system includes a process of analysis of customer's response at different price level of product.

Main motive of this system is to minimise the price of product while maintaining same profit

margin. In Cambridge Ltd, this system is adopted by company to gain competitive advantages by

optimising price of products. Management with help of this system analyse the consumer

response at different price of product to fix a most appropriate price (Bromiley and et.al, 2015).

Cost accounting system: It a kind of management accounting system in which provide

assistance to business organisation in monitor and optimization of various expenses and costs.

This system includes a systematic set of activities like entering, analysing, classifying,

summarizing and evaluation of various expense or costs to develop a frame for controlling these

costs. Main objectives of this system are to enhance the cost efficiency within business

organisation. It assists identification and assessment of excessive costs if any. It also provides

assistance in comparison of actual and budgeted cost. It indicates towards any event which may

incur any additional cost in manufacturing and production cost. In this system is used to analyse

the cost of construction project and any escalation in cost of project. In Cambridge Ltd, this

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system is adopted by company to optimise their product cost to increase profitability. It also

assists company to take out source or produce decision.

Job costing system: This system is mainly used by business organisations in which

various costs and expenses are allocated to particular jobs and tasks. This type of management

accounting system emphasises on systematic classification of cost related to manufacturing and

production costs to a single task or job. Main purpose of this system is to enhance the

accountability within business organisation. In Cambridge Ltd, company is producing various

food and diet supplement some products are totally different in nature thus company is using this

system also to allocate cost in separate product job or task. Following are key information’s that

is needed for job costing system, as follows:

P2. Different methodologies employed used in Management Accounting Reporting.

In an organisation, the management accounting reporting is usually carried out by the

lower level managers who then delivers the same for approval to the higher management

authorities (Malinić and Todorović, 2012). Under Management Accounting Reporting, the main

purpose is to deliver an overall view of the management practices, policies and procedures

undertaken at various organisational levels for a given period. In order to bring uniformity, the

reporting is done using similar formats that are predefined and help in easy identification of the

nature, size, complexity and purpose of the report itself. These may vary from organisation to

organisation. In Cambridge, different reporting formats may be used to communicate

information of varying nature to the top-management. Some of the techniques and

methodologies that are adopted by this company are as follows:

Variance Analysis:

As the name suggest, variance analysis facilitates analysis of deviations found between

the budgeted amounts and their actual occurrence. Thus, helping in the identification of weak

production areas and cost centres present in a manufacturing process. Here, the main aim of the

management is to ascertain any sort of under or over utilisation of resources which may result in

under or over costing on Cambridge's part. A variance reported may be favourable, unfavourable

or adverse in nature. In Cambridge, this method is used to ascertain nature of variance in

construction costs. If any unfavourable variance is found, management strives to strategically

eliminate it. Also, a quantity variance identified in construction project shows that company used

excessive input.

5

assists company to take out source or produce decision.

Job costing system: This system is mainly used by business organisations in which

various costs and expenses are allocated to particular jobs and tasks. This type of management

accounting system emphasises on systematic classification of cost related to manufacturing and

production costs to a single task or job. Main purpose of this system is to enhance the

accountability within business organisation. In Cambridge Ltd, company is producing various

food and diet supplement some products are totally different in nature thus company is using this

system also to allocate cost in separate product job or task. Following are key information’s that

is needed for job costing system, as follows:

P2. Different methodologies employed used in Management Accounting Reporting.

In an organisation, the management accounting reporting is usually carried out by the

lower level managers who then delivers the same for approval to the higher management

authorities (Malinić and Todorović, 2012). Under Management Accounting Reporting, the main

purpose is to deliver an overall view of the management practices, policies and procedures

undertaken at various organisational levels for a given period. In order to bring uniformity, the

reporting is done using similar formats that are predefined and help in easy identification of the

nature, size, complexity and purpose of the report itself. These may vary from organisation to

organisation. In Cambridge, different reporting formats may be used to communicate

information of varying nature to the top-management. Some of the techniques and

methodologies that are adopted by this company are as follows:

Variance Analysis:

As the name suggest, variance analysis facilitates analysis of deviations found between

the budgeted amounts and their actual occurrence. Thus, helping in the identification of weak

production areas and cost centres present in a manufacturing process. Here, the main aim of the

management is to ascertain any sort of under or over utilisation of resources which may result in

under or over costing on Cambridge's part. A variance reported may be favourable, unfavourable

or adverse in nature. In Cambridge, this method is used to ascertain nature of variance in

construction costs. If any unfavourable variance is found, management strives to strategically

eliminate it. Also, a quantity variance identified in construction project shows that company used

excessive input.

5

Budget reports:

This technique helps in planning, controlling and coordinating valuable business

resources so as to generate maximum productivity by incurring minimal costs. For Cambridge,

this is a crucial method so as to ensure liquidity and adequate working capital in the business.

For this purpose, the company prepares various budgets related to cash, sales and purchase

among others. This helps them in being mindful of cost related decisions in the context of both

present as well as future perspectives (McLean, McGovern and Davie, 2015). Also, Management

Accounting Reporting using this technique enables the management in knowing exactly what

needs to be reduced and what needs to be prioritised so as to gain future profitability and value

deliverance on company's part.

Performance Report:

This reporting methodology includes reporting of overall performance of the company to

the higher management authorities. This includes both organisational and employee

performance. Hence, one is able to ascertain and benchmark the level of excellence expected out

of employees as well as the organisation in order to maintain as well as enhance current and

future performance. In Cambridge, this technique is used to control and overlook the

performance of employees of various managers and their subordinates. It also helps in the

determination of those people who are excellent in their work and recognizing their

achievements thereof. Thus, indirectly instilling a sense of motivation and belonging among

them as well as others.

M1 Benefits of management accounting system:

With the help of management accosting system organization enhance their operational

functions such as inventory management system help the organization to regular track their

inventory level. It minimise the carrying cost which automatically increase the profit margin.

Along with this, cost accounting system help the manager to identify their each unit cost and on

the basis of this, manager can build effective strategy which further helps in decision making

process. Management accounting systems are beneficial for organisation that provides

information to ensure organisation goal or objectives. Like in context of Cambridge Ltd is using

management system that helps to decide the goals and objects within organisation and employees

make efforts to complete objectives.

6

This technique helps in planning, controlling and coordinating valuable business

resources so as to generate maximum productivity by incurring minimal costs. For Cambridge,

this is a crucial method so as to ensure liquidity and adequate working capital in the business.

For this purpose, the company prepares various budgets related to cash, sales and purchase

among others. This helps them in being mindful of cost related decisions in the context of both

present as well as future perspectives (McLean, McGovern and Davie, 2015). Also, Management

Accounting Reporting using this technique enables the management in knowing exactly what

needs to be reduced and what needs to be prioritised so as to gain future profitability and value

deliverance on company's part.

Performance Report:

This reporting methodology includes reporting of overall performance of the company to

the higher management authorities. This includes both organisational and employee

performance. Hence, one is able to ascertain and benchmark the level of excellence expected out

of employees as well as the organisation in order to maintain as well as enhance current and

future performance. In Cambridge, this technique is used to control and overlook the

performance of employees of various managers and their subordinates. It also helps in the

determination of those people who are excellent in their work and recognizing their

achievements thereof. Thus, indirectly instilling a sense of motivation and belonging among

them as well as others.

M1 Benefits of management accounting system:

With the help of management accosting system organization enhance their operational

functions such as inventory management system help the organization to regular track their

inventory level. It minimise the carrying cost which automatically increase the profit margin.

Along with this, cost accounting system help the manager to identify their each unit cost and on

the basis of this, manager can build effective strategy which further helps in decision making

process. Management accounting systems are beneficial for organisation that provides

information to ensure organisation goal or objectives. Like in context of Cambridge Ltd is using

management system that helps to decide the goals and objects within organisation and employees

make efforts to complete objectives.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1 Critically evaluation of management accounting systems and reports integrated within

organisational processes

Management accounting system and accounting reports integrated with organisational

process in order to survive business in effective manner. Both are playing important role in the

process and help to increase profitability as well as productivity. All this system helps in proper

analysing of business performance and every essential reports aids company to make proper

plans that support to attain the defined objective in present full manner (Takeda and Boyns,

2014). Management accounting system and report are integrated with each other such as

manager’s uses different management accounting system such as inventory management system,

price optimisation system and cost accounting system that help to maintain the records. The

manager of Cambridge uses this system and prepares accounting reports that help to understand

proper report and transaction. A manager cannot prepare accounting reports without using

management accounting system that provides information within organisation. Such as manager

of Cambridge Ltd uses inventory management system and prepare report that provide

information about raw material and finished good through reports. By using cost accounting

system it prepares cost reports that provide information about costs.

TASK 2

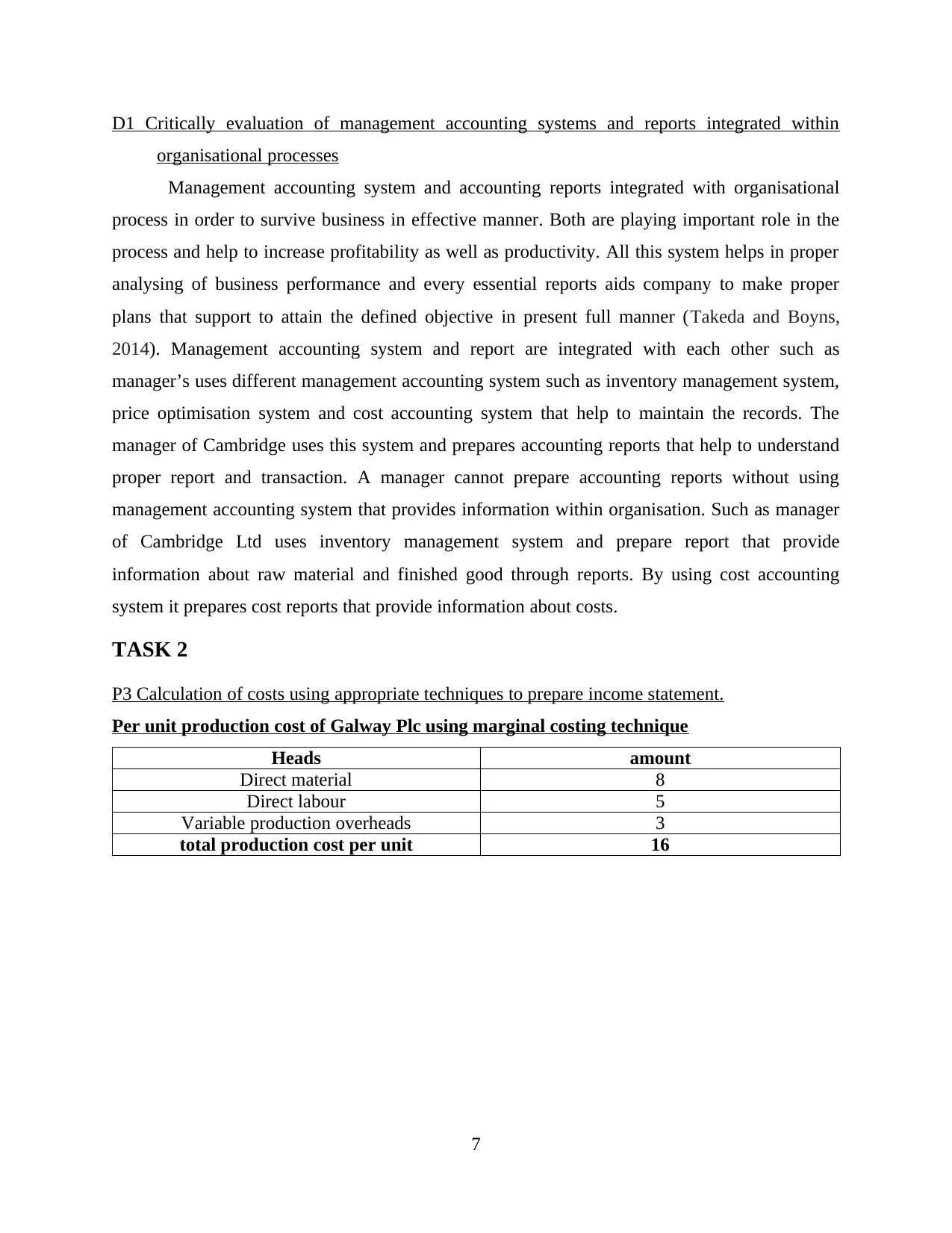

P3 Calculation of costs using appropriate techniques to prepare income statement.

Per unit production cost of Galway Plc using marginal costing technique

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

total production cost per unit 16

7

organisational processes

Management accounting system and accounting reports integrated with organisational

process in order to survive business in effective manner. Both are playing important role in the

process and help to increase profitability as well as productivity. All this system helps in proper

analysing of business performance and every essential reports aids company to make proper

plans that support to attain the defined objective in present full manner (Takeda and Boyns,

2014). Management accounting system and report are integrated with each other such as

manager’s uses different management accounting system such as inventory management system,

price optimisation system and cost accounting system that help to maintain the records. The

manager of Cambridge uses this system and prepares accounting reports that help to understand

proper report and transaction. A manager cannot prepare accounting reports without using

management accounting system that provides information within organisation. Such as manager

of Cambridge Ltd uses inventory management system and prepare report that provide

information about raw material and finished good through reports. By using cost accounting

system it prepares cost reports that provide information about costs.

TASK 2

P3 Calculation of costs using appropriate techniques to prepare income statement.

Per unit production cost of Galway Plc using marginal costing technique

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

total production cost per unit 16

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Per unit production cost of Galway Plc using Absorption costing technique

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

fixed production overheads 13.33

total production cost per unit 29.33

Variance analysis

This method used by company to identify business systemic problems. That could be

identified by matching the real price with the price of the budget. This method yields either

positive or negative outcomes which are advantageous results indicate an enhancement in the

company's effectiveness, while negative results show company inefficiencies.

8

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

fixed production overheads 13.33

total production cost per unit 29.33

Variance analysis

This method used by company to identify business systemic problems. That could be

identified by matching the real price with the price of the budget. This method yields either

positive or negative outcomes which are advantageous results indicate an enhancement in the

company's effectiveness, while negative results show company inefficiencies.

8

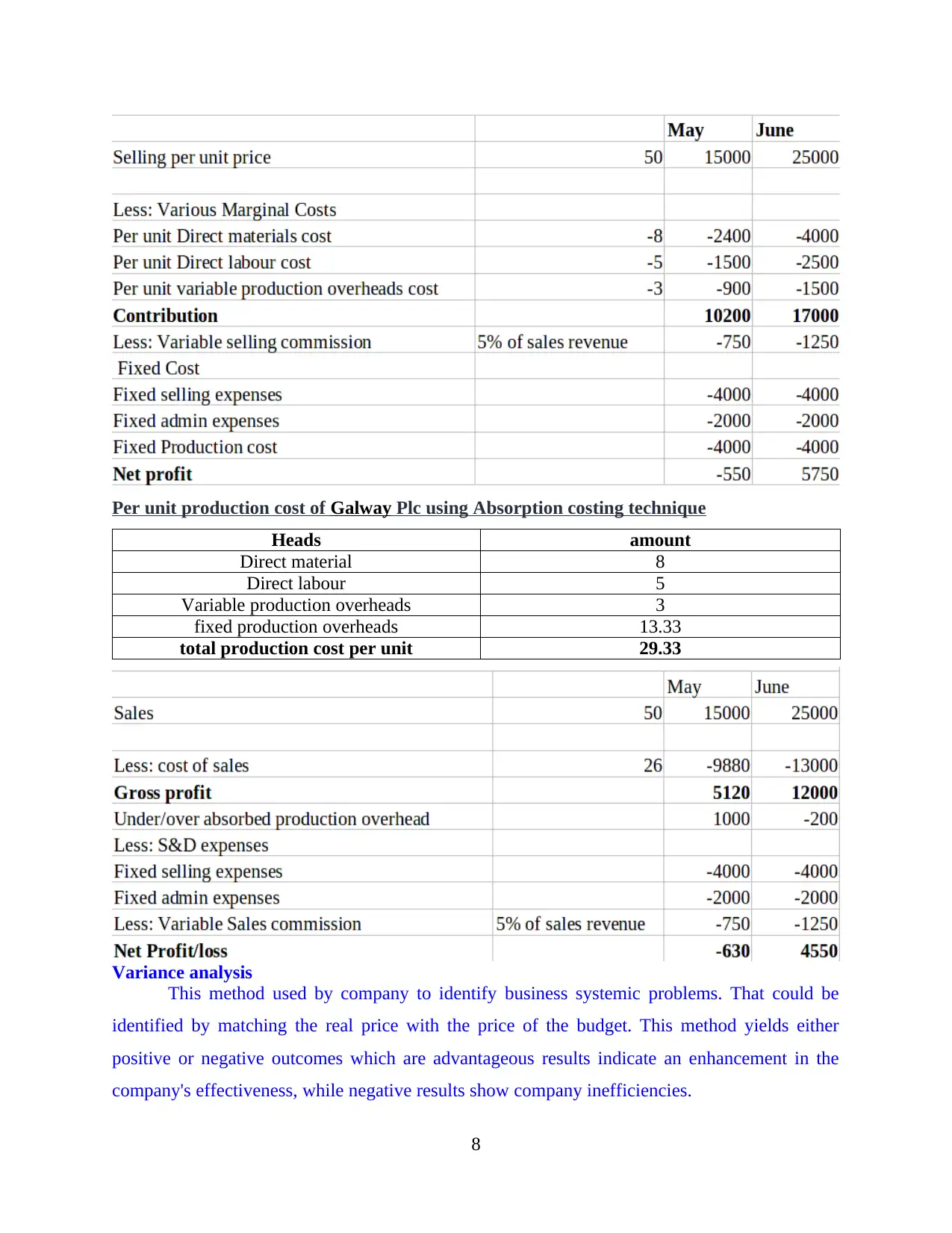

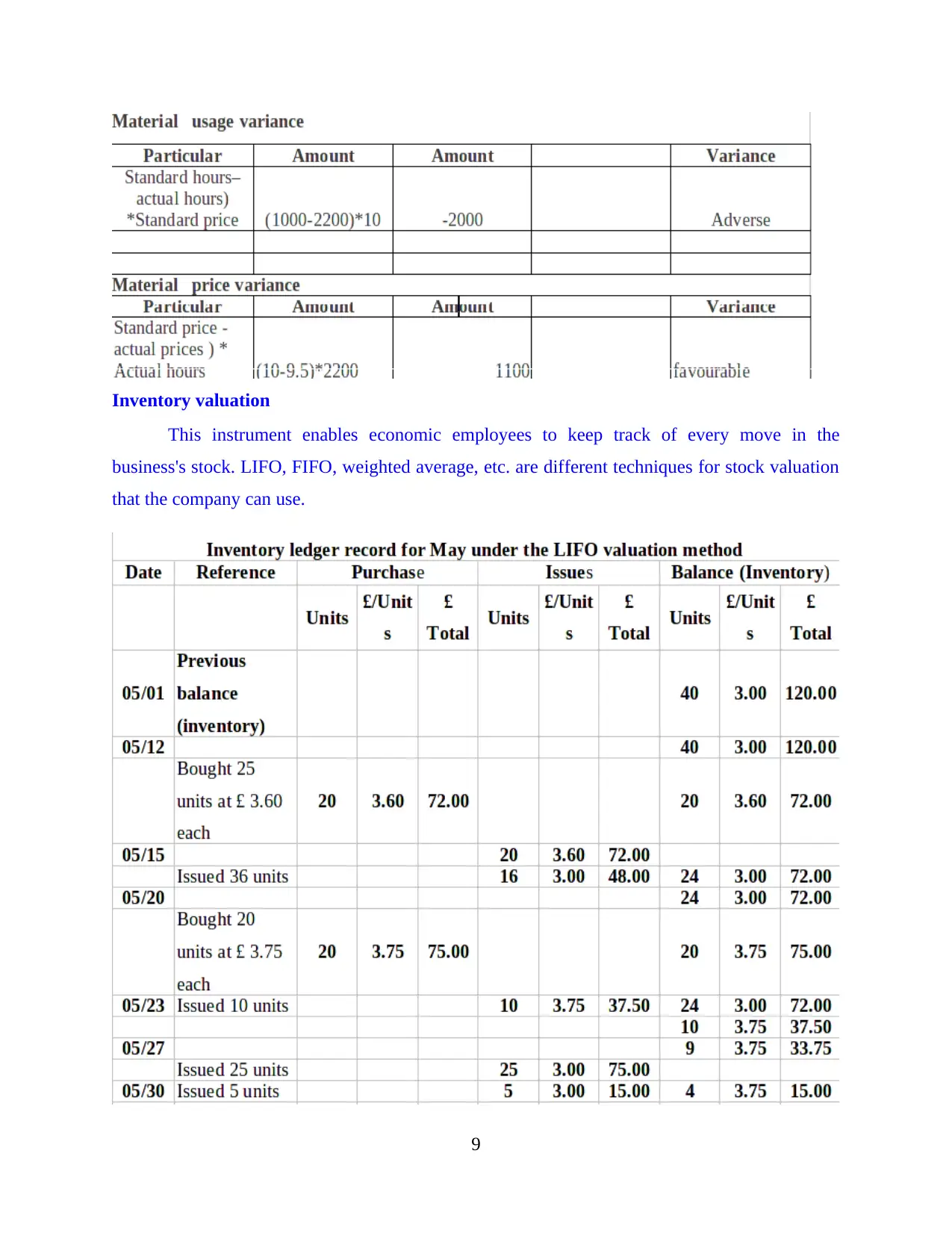

Inventory valuation

This instrument enables economic employees to keep track of every move in the

business's stock. LIFO, FIFO, weighted average, etc. are different techniques for stock valuation

that the company can use.

9

This instrument enables economic employees to keep track of every move in the

business's stock. LIFO, FIFO, weighted average, etc. are different techniques for stock valuation

that the company can use.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2. Various Techniques of Management Accounting System

Techniques of Management Accounting system include Standard and Historical Costing.

Under Standard Costing, variances are identified by benchmarking costs and comparing them

with actual costs incurred. Whereas in Historical costing, the values of assets and liabilities are

reported at their historical or initial costs regardless of their fair market value.

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities

From the above calculation, it has been observed that net profit and gross profit from

marginal costing is because it includes extra cost of producing every extra unit of output.

May June

Net Profit 1050 5750

Gross Profit 11800 17000

On the other side the net profit and gross profit from absorption costing is

Gross Profit

May June

9200 17200

Net Profit

10

Techniques of Management Accounting system include Standard and Historical Costing.

Under Standard Costing, variances are identified by benchmarking costs and comparing them

with actual costs incurred. Whereas in Historical costing, the values of assets and liabilities are

reported at their historical or initial costs regardless of their fair market value.

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities

From the above calculation, it has been observed that net profit and gross profit from

marginal costing is because it includes extra cost of producing every extra unit of output.

May June

Net Profit 1050 5750

Gross Profit 11800 17000

On the other side the net profit and gross profit from absorption costing is

Gross Profit

May June

9200 17200

Net Profit

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

May June

-550 6150

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budget

A budget is approximate structure of income and expenses for a specific time period. It is

basically identifies revenue of an organisation and expenditure for a periodic basis. It can be

made by organisation, family, government and any other person who makes and spends money

for a month and year (Thomas, 2016). Budget is a format which specifies financial gain and

expenses on future estimation or upcoming time period. It forecasts the financial results and

position of an organization for one or more future period of time. A budget is used for provision

and performance measuring purpose.

Cash Budget:

A cash budget is a figuring of the cash inflows and outflows for a business over a specific

period of time. It is used to evaluate whether the organisation has sufficient cash to operate.

Companies use the cash budget to forecast the production and sales.

It is planning of foreseen and cash payment for a specific time period. These cash inflows

and outflows include revenues accumulated, expenses paid, and loans receipts and payments. In

other words, a cash budget is an estimated prediction of the company's cash appearance in the

future.

Advantages:

The major strength of this budget is that it supports to keep detail information about total

cash inflows and outflows of cash during a time period. Maintaining a valid record of

compete expenses year by year help manager of company to remove the same from

consecutive year so that profit margin can be increased.

This budget helps to maintain particular reserves in order to meet the uncertainty of

business and avoid the chances of low productivity. In Cambridge ltd manager maintain a

certain amount as reserve that helps them to deal with contingencies that can happen in

future due to any market circumstances.

Disadvantages:

11

-550 6150

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budget

A budget is approximate structure of income and expenses for a specific time period. It is

basically identifies revenue of an organisation and expenditure for a periodic basis. It can be

made by organisation, family, government and any other person who makes and spends money

for a month and year (Thomas, 2016). Budget is a format which specifies financial gain and

expenses on future estimation or upcoming time period. It forecasts the financial results and

position of an organization for one or more future period of time. A budget is used for provision

and performance measuring purpose.

Cash Budget:

A cash budget is a figuring of the cash inflows and outflows for a business over a specific

period of time. It is used to evaluate whether the organisation has sufficient cash to operate.

Companies use the cash budget to forecast the production and sales.

It is planning of foreseen and cash payment for a specific time period. These cash inflows

and outflows include revenues accumulated, expenses paid, and loans receipts and payments. In

other words, a cash budget is an estimated prediction of the company's cash appearance in the

future.

Advantages:

The major strength of this budget is that it supports to keep detail information about total

cash inflows and outflows of cash during a time period. Maintaining a valid record of

compete expenses year by year help manager of company to remove the same from

consecutive year so that profit margin can be increased.

This budget helps to maintain particular reserves in order to meet the uncertainty of

business and avoid the chances of low productivity. In Cambridge ltd manager maintain a

certain amount as reserve that helps them to deal with contingencies that can happen in

future due to any market circumstances.

Disadvantages:

11

The main drawback of this budgets is that it only disclose the cash position of company

but not able to represent the financial strength of company during an accounting year.

This budget is manipulative sometime as responsible manager make conditional mistake

in figure in order to increase the expenses to avoid taxable income.

Operating budget:

A detailed budget for all figuring income and expense based on foretelling sales during a given

period for a specific time period (Yazdifar and et.al., 2012). It generally comprises of several

sub-budgets, sales budget is prepared first. These all budget are prepared for short-term. The

operational budgets are being prepared annually and based on the functional Category and

included in cost accounts. An operating budget represent a company’s expenses, costs, and

estimated income, considering the annually performance. Accountants make the operating

budget before the accounting period starts in order to include cost and income projections.

Advantages:

Budget is predetermination of goal and objectives: In business world, companies are

focused to attain the desired objective which makes them sustain for long in competitive

market. In respective firm, manager uses particular budgets for each activity that helps to

work accordingly and reached the desired targets. The fix the certain criteria for every

operation and tries to finish these task by considering that criteria that helps to attain the

overall goals and objective.

Defining the strengths and weakness: Budgets are meaningful for companies as they are

able to define the overall performance of each activity. Manager of Cambridge ltd uses

operating budgets that helps to determine the profitable and weak operation for company.

This also helps to check the reason for weaknesses and develop a proper way to remove

these weaknesses that will increase overall profitability of business.

Disadvantages:

It requires more time and cost because failure in operation can lead to decrease in overall

productivity and performance. Sometime, manager makes budgets regarding activities of

company, but due to unexpected circumstances these budgets are not effective which

leads to reduction in overall performance.

Manager in order to prepare operational budgets missed the other crucial function that

leads to mismanagement within Cambridge ltd. Only focusing on operating activities

12

but not able to represent the financial strength of company during an accounting year.

This budget is manipulative sometime as responsible manager make conditional mistake

in figure in order to increase the expenses to avoid taxable income.

Operating budget:

A detailed budget for all figuring income and expense based on foretelling sales during a given

period for a specific time period (Yazdifar and et.al., 2012). It generally comprises of several

sub-budgets, sales budget is prepared first. These all budget are prepared for short-term. The

operational budgets are being prepared annually and based on the functional Category and

included in cost accounts. An operating budget represent a company’s expenses, costs, and

estimated income, considering the annually performance. Accountants make the operating

budget before the accounting period starts in order to include cost and income projections.

Advantages:

Budget is predetermination of goal and objectives: In business world, companies are

focused to attain the desired objective which makes them sustain for long in competitive

market. In respective firm, manager uses particular budgets for each activity that helps to

work accordingly and reached the desired targets. The fix the certain criteria for every

operation and tries to finish these task by considering that criteria that helps to attain the

overall goals and objective.

Defining the strengths and weakness: Budgets are meaningful for companies as they are

able to define the overall performance of each activity. Manager of Cambridge ltd uses

operating budgets that helps to determine the profitable and weak operation for company.

This also helps to check the reason for weaknesses and develop a proper way to remove

these weaknesses that will increase overall profitability of business.

Disadvantages:

It requires more time and cost because failure in operation can lead to decrease in overall

productivity and performance. Sometime, manager makes budgets regarding activities of

company, but due to unexpected circumstances these budgets are not effective which

leads to reduction in overall performance.

Manager in order to prepare operational budgets missed the other crucial function that

leads to mismanagement within Cambridge ltd. Only focusing on operating activities

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.