Costing Analysis Report: Traditional vs ABC in Management Accounting

VerifiedAdded on 2019/10/30

|5

|1066

|326

Report

AI Summary

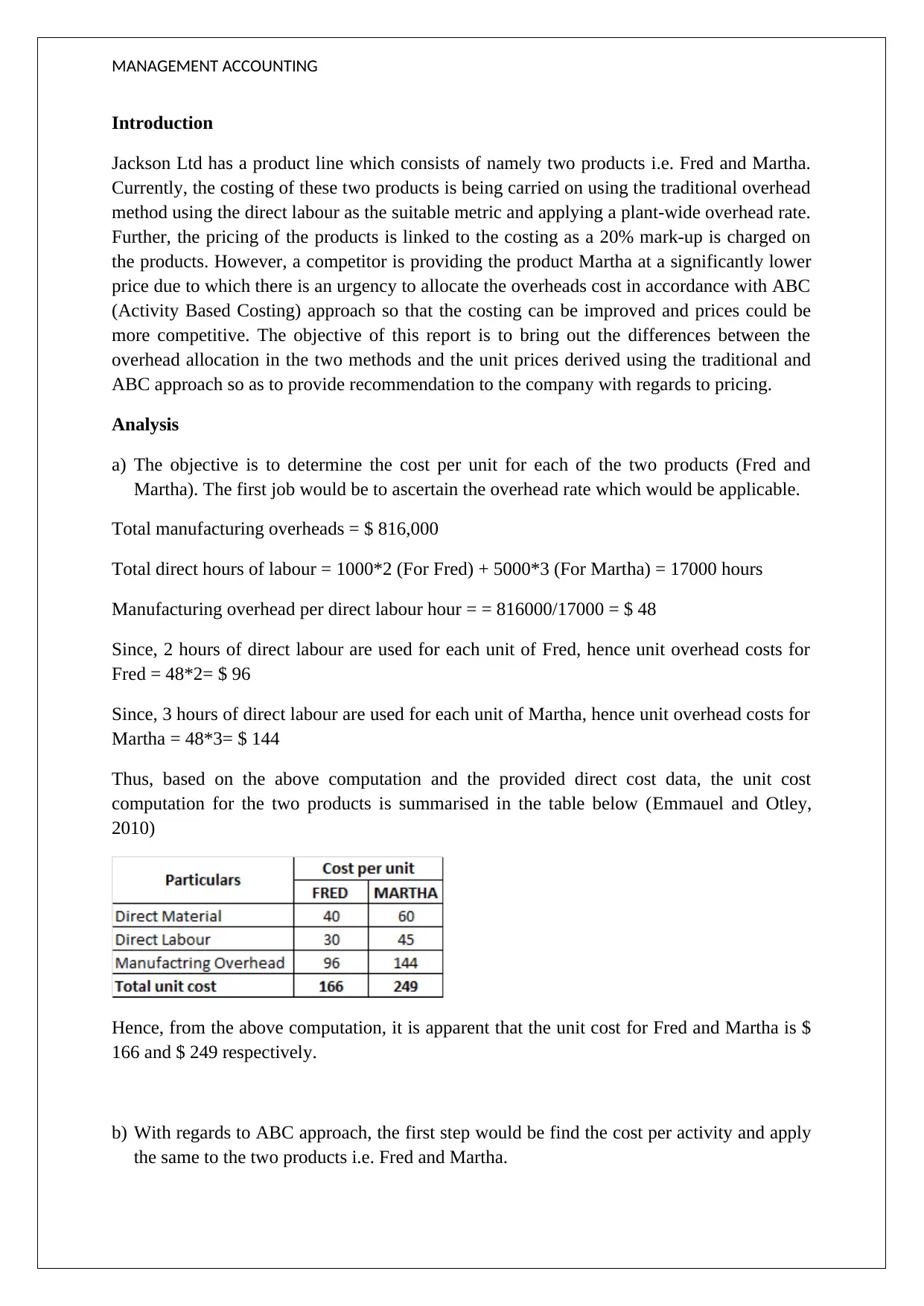

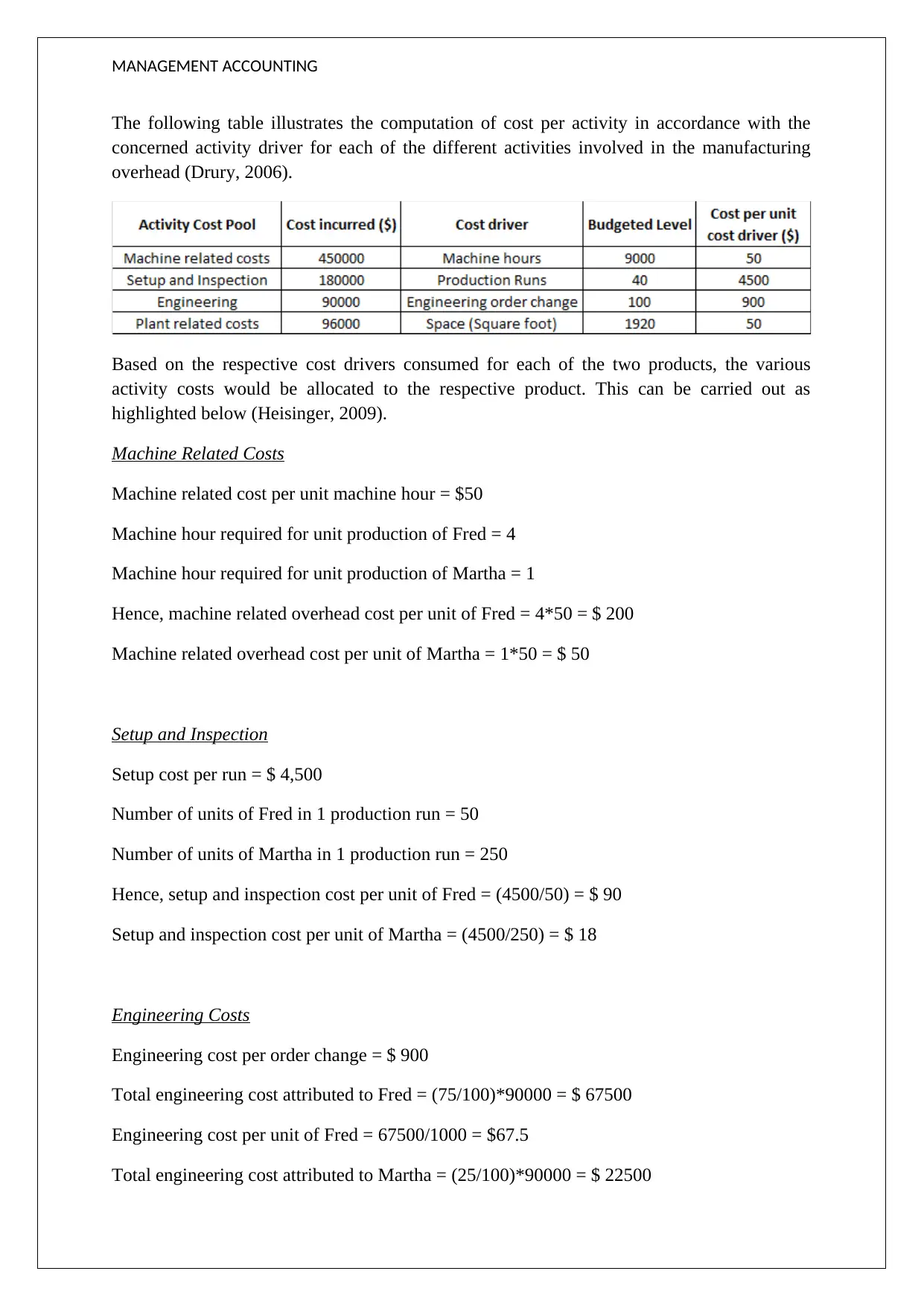

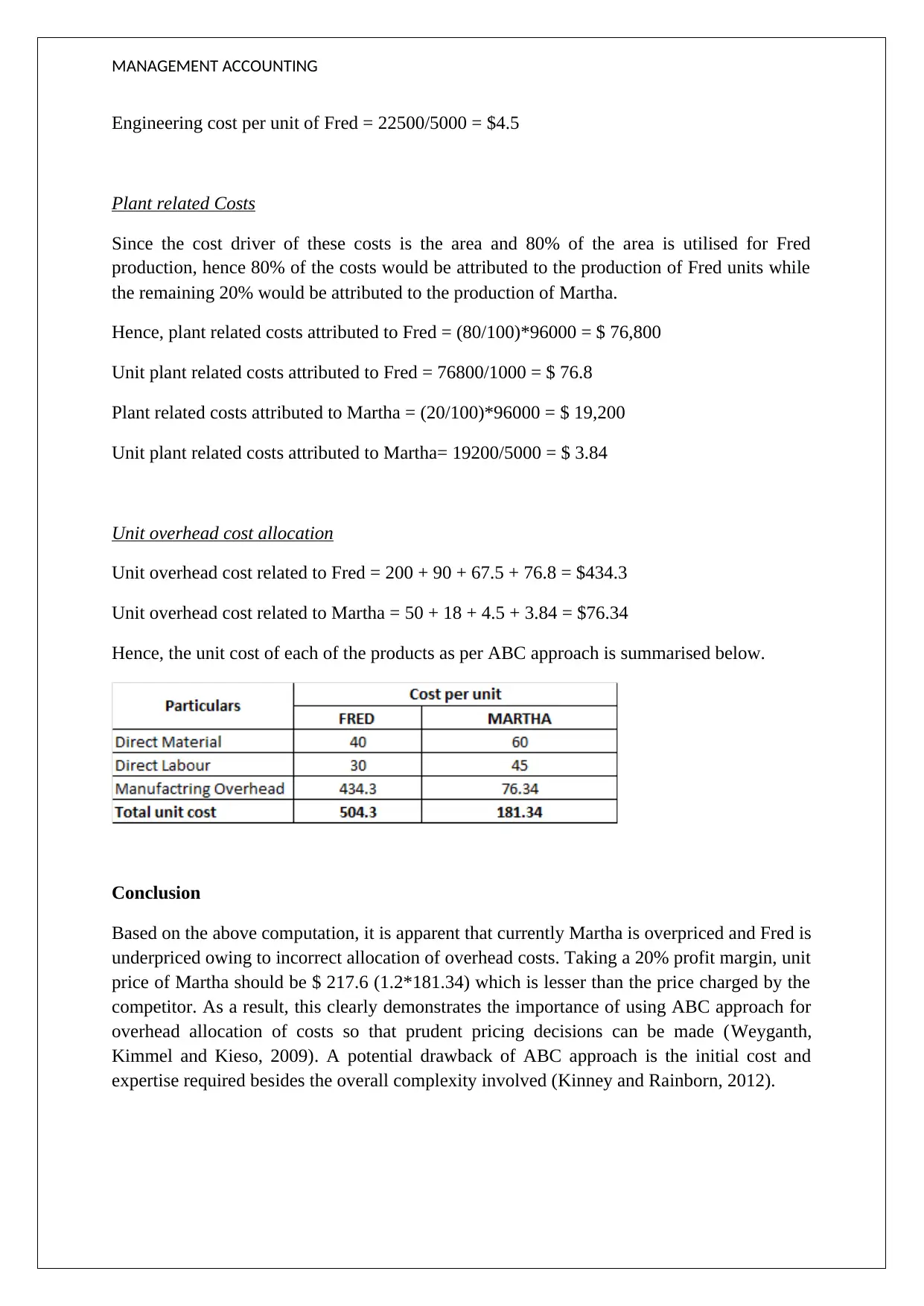

This report evaluates the differences between traditional and Activity-Based Costing (ABC) methods in management accounting, using a case study of Jackson Ltd. The analysis compares overhead allocation and unit prices for two products, Fred and Martha. The traditional method uses direct labor hours to allocate overhead, while ABC identifies various activities and cost drivers. The report calculates unit costs under both methods, revealing that Martha is overpriced and Fred is underpriced under the traditional approach. The ABC method provides a more accurate allocation, leading to a recommended price adjustment for Martha to remain competitive. The report concludes by emphasizing the importance of ABC for informed pricing decisions while acknowledging its potential drawbacks, such as initial costs and complexity. References to key accounting texts are included to support the analysis.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.