Critical Evaluation of Management Accounting Systems Report

VerifiedAdded on 2019/12/28

|16

|3681

|113

Report

AI Summary

This report delves into the realm of management accounting, exploring its significance and various systems. It begins by defining management accounting and outlining its essential requirements, contrasting it with financial accounting. The report then examines different methods used in management accounting reporting, including financial planning, cost accounting, and budgetary control. A key focus is on evaluating the benefits of different management accounting systems and their practical applications, particularly within the context of an organization like Dell. The report further analyzes costing methods, specifically comparing absorption and marginal costing, detailing their calculations and the preparation of income statements. It also assesses the advantages and disadvantages of planning tools used for budgetary control, using Dell as a case study. Finally, the report compares Dell with HP, examining how they adapt management accounting systems to address financial challenges and achieve sustainable success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1.......................................................................................................................................1

P1 Management accounting and essential requirement of different types of management

accounting systems......................................................................................................................1

P2 Different methods used for management accounting reporting.............................................2

M1 Evaluation benefits of different management accounting systems and their application.....3

D1 Critical evaluation of management accounting systems ......................................................4

TASK 2............................................................................................................................................5

P3 Calculating cost per unit under both absorption costing and marginal costing by stating the

difference between both of them. Explaining the way in which the income statements are

being prepared from both of these measures...............................................................................5

TASK 3............................................................................................................................................7

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................7

A. Calculation of standard cost of PVC sheet.............................................................................8

B. Calculation of material price variance....................................................................................9

M3 Use of different planning tools and their application for preparing and forecasting budgets

in the context of Dell...................................................................................................................9

D3 Way in which the planning tools respond appropriately to solving problems in the context

of Dell, leading to sustainable business development...............................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of Dell with HP to establish the way in which the organisations are adapting

management accounting systems to respond to financial problems such as lack of view of

what deals had been sold from a budgetary perspective...........................................................10

M4 How responding to financial problems, management accounting can lead an organisation

such as Dell to sustainable success...........................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1.......................................................................................................................................1

P1 Management accounting and essential requirement of different types of management

accounting systems......................................................................................................................1

P2 Different methods used for management accounting reporting.............................................2

M1 Evaluation benefits of different management accounting systems and their application.....3

D1 Critical evaluation of management accounting systems ......................................................4

TASK 2............................................................................................................................................5

P3 Calculating cost per unit under both absorption costing and marginal costing by stating the

difference between both of them. Explaining the way in which the income statements are

being prepared from both of these measures...............................................................................5

TASK 3............................................................................................................................................7

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................7

A. Calculation of standard cost of PVC sheet.............................................................................8

B. Calculation of material price variance....................................................................................9

M3 Use of different planning tools and their application for preparing and forecasting budgets

in the context of Dell...................................................................................................................9

D3 Way in which the planning tools respond appropriately to solving problems in the context

of Dell, leading to sustainable business development...............................................................10

TASK 4..........................................................................................................................................10

P5 Comparison of Dell with HP to establish the way in which the organisations are adapting

management accounting systems to respond to financial problems such as lack of view of

what deals had been sold from a budgetary perspective...........................................................10

M4 How responding to financial problems, management accounting can lead an organisation

such as Dell to sustainable success...........................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is basically preparing accounts and reports which are essential

for the managers to make decisions on the basis of statistics and financial data . This report

defines management accounting and provides different types of management accounting systems

and its requirement. The report focuses on different methods, benefits of various management

accounting systems and integration with organization processes. In this report shows the uses for

preparing income statements using the marginal and absorption costing, its calculation and

differences. This kind of reports producing financial report. It has also discusses different types

of planning tools that are being used for budgetary control.

TASK 1

P1 Management accounting and essential requirement of different types of management

accounting systems

The management accounting is the process for creating and maintaining financial report

in a particular systematic format for providing accurate and statistical data which is essential for

the organization's manager to create decisions on the daily basis (Bebbington, Unerman and

O'Dwyer, 2014). This management accounting consists of making and supplying statistical and

financial information to the enterprises managers for generating daily basis decisions. Financial

accounting is used by organization’s stakeholders for generating financial reports for the

enterprise and it is different from management accounting. Management accounting reports are

like periodical reports that are mostly used by the company’s owner and managers. Report of

management accounting consists of dell and other firms cash and funds which is available in

company like sales revenues, current position of accounts etc. These all things are calculated on

the requirements of an organization requirements . For maintaining growth of Dell firm it is

important for the businesses to calculating the accounts. Report of management accounting is

different from the financial accounting because financial accounting reports are generated on the

basis of historical information and these reports are used to look forward side of business.

For individuals and businesses, various types of management accounting systems are

available. The decision is taken from the account's data and its accounting systems price and

values for selecting an accounting system in the future . The ability of person for accessing

management accounting system is important for the system. Several types of accounting systems

1

Management accounting is basically preparing accounts and reports which are essential

for the managers to make decisions on the basis of statistics and financial data . This report

defines management accounting and provides different types of management accounting systems

and its requirement. The report focuses on different methods, benefits of various management

accounting systems and integration with organization processes. In this report shows the uses for

preparing income statements using the marginal and absorption costing, its calculation and

differences. This kind of reports producing financial report. It has also discusses different types

of planning tools that are being used for budgetary control.

TASK 1

P1 Management accounting and essential requirement of different types of management

accounting systems

The management accounting is the process for creating and maintaining financial report

in a particular systematic format for providing accurate and statistical data which is essential for

the organization's manager to create decisions on the daily basis (Bebbington, Unerman and

O'Dwyer, 2014). This management accounting consists of making and supplying statistical and

financial information to the enterprises managers for generating daily basis decisions. Financial

accounting is used by organization’s stakeholders for generating financial reports for the

enterprise and it is different from management accounting. Management accounting reports are

like periodical reports that are mostly used by the company’s owner and managers. Report of

management accounting consists of dell and other firms cash and funds which is available in

company like sales revenues, current position of accounts etc. These all things are calculated on

the requirements of an organization requirements . For maintaining growth of Dell firm it is

important for the businesses to calculating the accounts. Report of management accounting is

different from the financial accounting because financial accounting reports are generated on the

basis of historical information and these reports are used to look forward side of business.

For individuals and businesses, various types of management accounting systems are

available. The decision is taken from the account's data and its accounting systems price and

values for selecting an accounting system in the future . The ability of person for accessing

management accounting system is important for the system. Several types of accounting systems

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps in making organization decision (Bodie, 2013). Like entry system, computerized and

manual system. Entry system: This is single and double for entry system. In single, this is used by the

small enterprises and it includes some few steps and very easy operations. So this entry

system is not considered any kind of entries for journal (Christopher, 2016). Book and

journal is created for balancing the accounts of business. In double entry system, this is

accurate but at the same time it is difficult and complex. This system consists of debit and

credit and it must be equal. This will help in identifying the errors in an accurate way. Manual: In this system, the accountant keeps records and makes accounts in the journal

and he/she is responsible for records of accounting (Dalton and et.al 2014). Accountants

should create and calculate the statements for financial accounts.

Computer based: In this accounting there is an expert and do accounts internally but for

this firms needs an accountant for operating this kinds of software's who knows

accounts in computer.

P2 Different methods used for management accounting reporting

There various methods used for management accounting reporting and these are under :

Planning for financial: Firm main aim is to increase the profit. So this profit can

be retrieved by a systematic planning of financial data in firms.

Analysis of financial statement: Balance sheet and accounts of loss and profit are

important in the financial statement (DRURY, 2013). Rate of growth can be

known with the help of financial statement analysis .

Account for Cost: This displays the cost of information shows in order of products

value and quality, process, and department.

Analysis of Fund flow: The movements of funds in an organization shows in order

of time period that can be found on the analysis of fund flow.

Analysis of cash flow: The movements of cash in an organization shows in order

of time period that can be found on the analysis of cash flow. Costing: This

involves two things marginal and standard for costing (Fullerton, Kennedy and

Widener, 2014). In standard, Preset or previously planned cost are alike. It

provides stick for yard for identifying the performance of the actual firm. In

2

manual system. Entry system: This is single and double for entry system. In single, this is used by the

small enterprises and it includes some few steps and very easy operations. So this entry

system is not considered any kind of entries for journal (Christopher, 2016). Book and

journal is created for balancing the accounts of business. In double entry system, this is

accurate but at the same time it is difficult and complex. This system consists of debit and

credit and it must be equal. This will help in identifying the errors in an accurate way. Manual: In this system, the accountant keeps records and makes accounts in the journal

and he/she is responsible for records of accounting (Dalton and et.al 2014). Accountants

should create and calculate the statements for financial accounts.

Computer based: In this accounting there is an expert and do accounts internally but for

this firms needs an accountant for operating this kinds of software's who knows

accounts in computer.

P2 Different methods used for management accounting reporting

There various methods used for management accounting reporting and these are under :

Planning for financial: Firm main aim is to increase the profit. So this profit can

be retrieved by a systematic planning of financial data in firms.

Analysis of financial statement: Balance sheet and accounts of loss and profit are

important in the financial statement (DRURY, 2013). Rate of growth can be

known with the help of financial statement analysis .

Account for Cost: This displays the cost of information shows in order of products

value and quality, process, and department.

Analysis of Fund flow: The movements of funds in an organization shows in order

of time period that can be found on the analysis of fund flow.

Analysis of cash flow: The movements of cash in an organization shows in order

of time period that can be found on the analysis of cash flow. Costing: This

involves two things marginal and standard for costing (Fullerton, Kennedy and

Widener, 2014). In standard, Preset or previously planned cost are alike. It

provides stick for yard for identifying the performance of the actual firm. In

2

marginal, it consists of selling fixed prices, use of resources and material in the

best way for making decisions of buying and selling, orders movements, etc.

Control of budgetary: The assumption of financial requirements for future is

figured out (Galliers and Leidner, 2014).

Accounting of revaluation: It helps and used for fairs which are returning on

capitals by the employees.

Accounting for decision making: For business profit, the best profitable decision

is made and taken by comparing the costs and related things.

System of information management: The flow of communication must think free

for firms and this is important for operations of business.

Techniques using statistical: Like regression, control quality and least squares etc

are many techniques in statistics for deducing problems of management.

Cost accounting for historical: This consist of comparing preset plans costs for

evaluating the performance (Ionescu, 2014).

Analysis of ratio: This is used basically for discharging operations like planning,

communication, controlling, and forecasting.

M1 Evaluation benefits of different management accounting systems and their application

Mangers and CEO of the firm s uses management accounting for keeping records and

reports for viewing financial and managerial information. There are many benefits using of

management accounting like expenses reduce, improvements of cash flow, return of financial

increase and decisions of business.

For reducing the expense, this helps and ensures that lower level of firms and operational

expenses must be reduce (Ismail and King, 2014). The CEO and managers of the firm uses this

data and helps in understanding the business expenses and cost of surviving firm.

In improving the cash flow, it helps to know budgets for future expenditures because

budgets plays major role in management accounting.

Increase in returns of financial , this is also used for increasing the financial cash

returns . Management accounts are made for financial calculation regarding client’s requests,

sales or changes in price in the marketplace of economic.

3

best way for making decisions of buying and selling, orders movements, etc.

Control of budgetary: The assumption of financial requirements for future is

figured out (Galliers and Leidner, 2014).

Accounting of revaluation: It helps and used for fairs which are returning on

capitals by the employees.

Accounting for decision making: For business profit, the best profitable decision

is made and taken by comparing the costs and related things.

System of information management: The flow of communication must think free

for firms and this is important for operations of business.

Techniques using statistical: Like regression, control quality and least squares etc

are many techniques in statistics for deducing problems of management.

Cost accounting for historical: This consist of comparing preset plans costs for

evaluating the performance (Ionescu, 2014).

Analysis of ratio: This is used basically for discharging operations like planning,

communication, controlling, and forecasting.

M1 Evaluation benefits of different management accounting systems and their application

Mangers and CEO of the firm s uses management accounting for keeping records and

reports for viewing financial and managerial information. There are many benefits using of

management accounting like expenses reduce, improvements of cash flow, return of financial

increase and decisions of business.

For reducing the expense, this helps and ensures that lower level of firms and operational

expenses must be reduce (Ismail and King, 2014). The CEO and managers of the firm uses this

data and helps in understanding the business expenses and cost of surviving firm.

In improving the cash flow, it helps to know budgets for future expenditures because

budgets plays major role in management accounting.

Increase in returns of financial , this is also used for increasing the financial cash

returns . Management accounts are made for financial calculation regarding client’s requests,

sales or changes in price in the marketplace of economic.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The decisions for business is improving the growth and solutions which is taken by the

CEO and managers. This can be also used like a kit of tool.

D1 Critical evaluation of management accounting systems

Various management accounting systems like for manual system can teach the peoples of

inside and outside for the balancing credits as well as debit. But this also consumes lot time for

accounting. Because in manual there is no computer for summarize and categorize the

information , peoples have to do by their own side. In computerized system it gives benefit for

auto summation and other related things (Kothari, Mizik and Roychowdhury, 2015). This

computerized system the learner can not do by their side of work. In single entry there is big

disadvantage that if any single entry is missed in journal or book so it will be loss that entry and

balance will show the incorrect amount. But double entry has advantage that if any one entry is

missed but there is a another same entry which written on other side but this consume a double

time. In single entry this is saving time from two times entry of record. For the companies and

organizations they use computerized system that gives accurate result of accounting.

Various methods for management accounting helps organizations to know and increase

the growth ,process and productivity and services. Like using planning for financial method

helps to reach their aims by planning the financial things for firm.

Analysis of financial statements helps to know the growth of firm. Analysis of fund flow

helps to know the firms fund movements. Analysis of cash flow useful for the organization to

know the movements of cash. Like investments. So this all methods and systems of management

accounting is majorly integrated with an organization.

4

CEO and managers. This can be also used like a kit of tool.

D1 Critical evaluation of management accounting systems

Various management accounting systems like for manual system can teach the peoples of

inside and outside for the balancing credits as well as debit. But this also consumes lot time for

accounting. Because in manual there is no computer for summarize and categorize the

information , peoples have to do by their own side. In computerized system it gives benefit for

auto summation and other related things (Kothari, Mizik and Roychowdhury, 2015). This

computerized system the learner can not do by their side of work. In single entry there is big

disadvantage that if any single entry is missed in journal or book so it will be loss that entry and

balance will show the incorrect amount. But double entry has advantage that if any one entry is

missed but there is a another same entry which written on other side but this consume a double

time. In single entry this is saving time from two times entry of record. For the companies and

organizations they use computerized system that gives accurate result of accounting.

Various methods for management accounting helps organizations to know and increase

the growth ,process and productivity and services. Like using planning for financial method

helps to reach their aims by planning the financial things for firm.

Analysis of financial statements helps to know the growth of firm. Analysis of fund flow

helps to know the firms fund movements. Analysis of cash flow useful for the organization to

know the movements of cash. Like investments. So this all methods and systems of management

accounting is majorly integrated with an organization.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

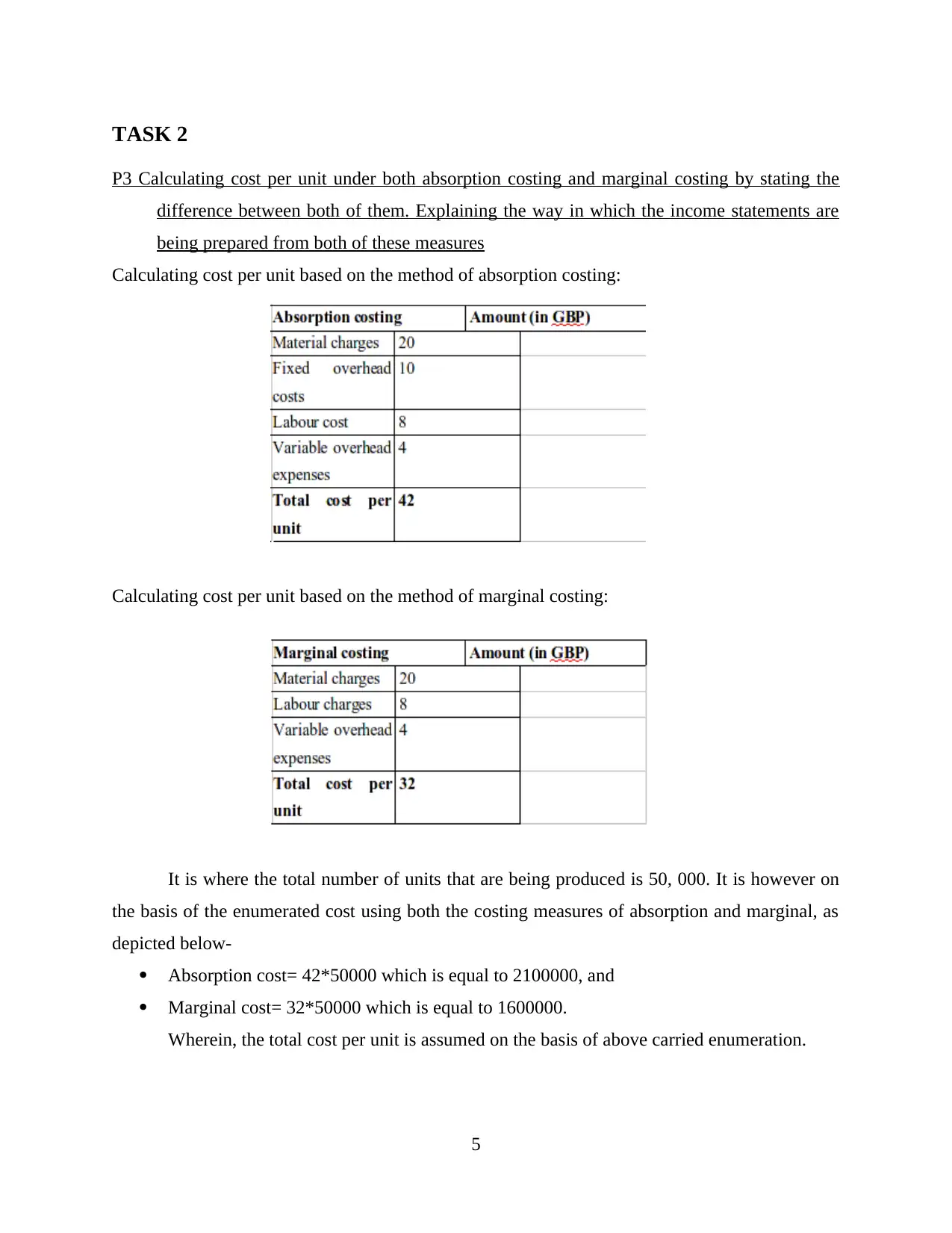

P3 Calculating cost per unit under both absorption costing and marginal costing by stating the

difference between both of them. Explaining the way in which the income statements are

being prepared from both of these measures

Calculating cost per unit based on the method of absorption costing:

Calculating cost per unit based on the method of marginal costing:

It is where the total number of units that are being produced is 50, 000. It is however on

the basis of the enumerated cost using both the costing measures of absorption and marginal, as

depicted below-

Absorption cost= 42*50000 which is equal to 2100000, and

Marginal cost= 32*50000 which is equal to 1600000.

Wherein, the total cost per unit is assumed on the basis of above carried enumeration.

5

P3 Calculating cost per unit under both absorption costing and marginal costing by stating the

difference between both of them. Explaining the way in which the income statements are

being prepared from both of these measures

Calculating cost per unit based on the method of absorption costing:

Calculating cost per unit based on the method of marginal costing:

It is where the total number of units that are being produced is 50, 000. It is however on

the basis of the enumerated cost using both the costing measures of absorption and marginal, as

depicted below-

Absorption cost= 42*50000 which is equal to 2100000, and

Marginal cost= 32*50000 which is equal to 1600000.

Wherein, the total cost per unit is assumed on the basis of above carried enumeration.

5

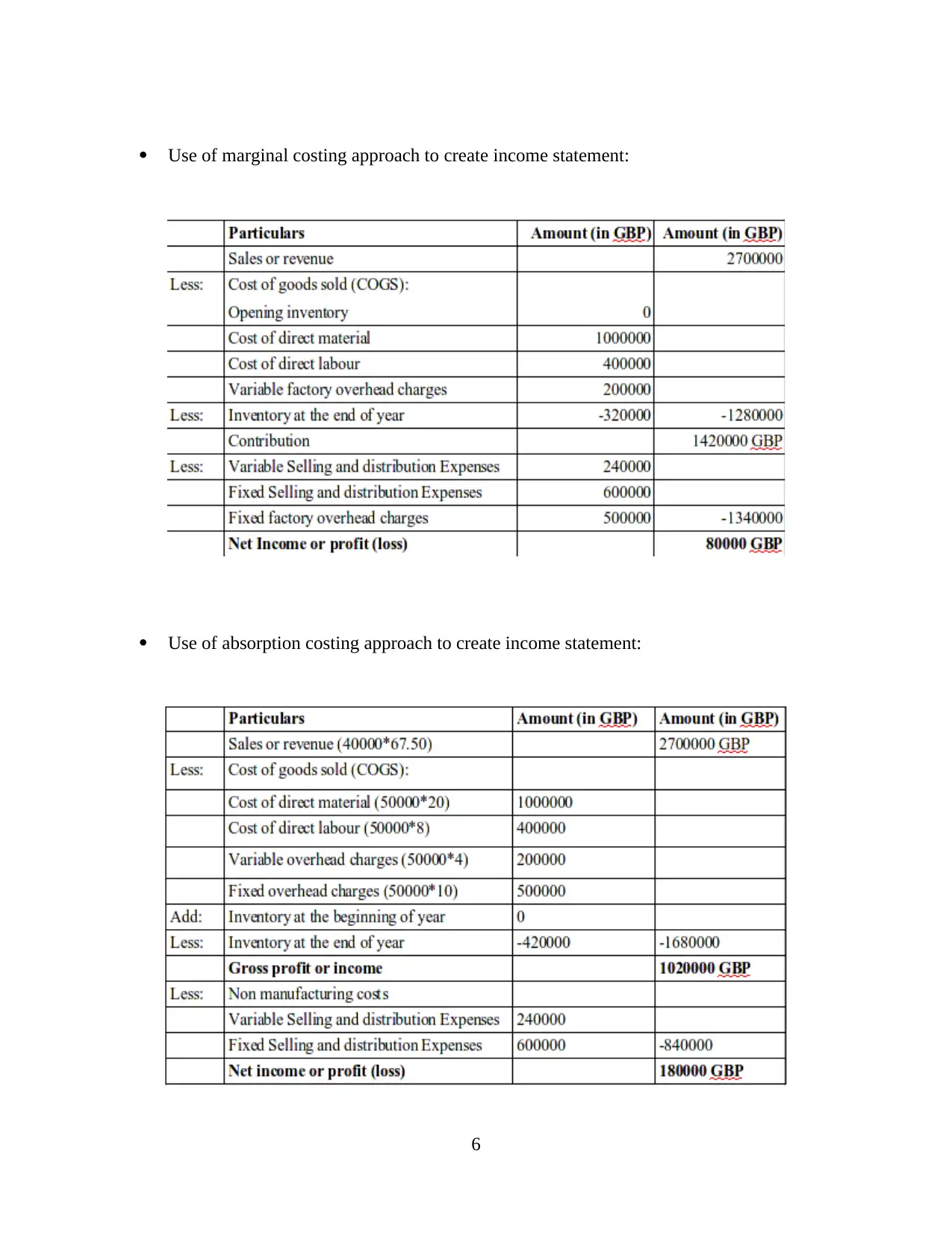

Use of marginal costing approach to create income statement:

Use of absorption costing approach to create income statement:

6

Use of absorption costing approach to create income statement:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is therefore on the basis of above carried computation, the costing approach using

absorption is more assistive for Dell where it has accurately identified the significance of

involving the cost of fixed production. Where it has also made a correct determination of

production cost as per an appropriate policy of pricing (Lind 2017). Also, the costing based upon

the method of absorption pricing together supports in assuring the recovery of all relative costs

where such type of costing is also acceptable in source of variable costs. Although, it is apparent

to necessitate Dell to concentrate upon the preparation of pertinent reporting that is indicating the

involvement of various costs while undertaking this particular approach of costing.

On differentiating both these measures, it is apparent that the cost recognition of both

these methods are distinct from one other. It is where in the marginal cost approach, there exists

total two distinct type of costs namely product and period costs. Herein, the variable costs are

assumed as product costs and the fixed costs are interpreted as period costs. Whereas, the

absorption approach of costing refers to only a single cost where both fixed and variable costs

are considered as product cost.

However, both these methods are useful for the creation of income statements and has a

greater contribution in the decision making procedure of the organisations like Dell (). However,

on referring to the present case of Dell, it has been identified that the approach of absorption

costing is more beneficial for them and will duly support them to take cost related decisions.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control is referred to be a foremost consideration of the organisational bodies

to make an effective utilization of their funds by constantly monitoring their undertaken budget

and making its prompt usage in an undertaken time period of accounting . This process is usually

undertaken using distinct tools of planning with several benefits and drawbacks of each- Incremental budgeting- It is referred to be one of the essential component of accounting

system that duly assists the delegates to make an effective management of their funds

and investments. This type of budgeting is usually done by making small alterations in

the existent budget to create an entirely new budget (Otley and Emmanuel, 2013). A

significant benefit of this method is its easy execution with no complex computation.

However, its incremental nature is a leading drawback where it assumes a prime

7

absorption is more assistive for Dell where it has accurately identified the significance of

involving the cost of fixed production. Where it has also made a correct determination of

production cost as per an appropriate policy of pricing (Lind 2017). Also, the costing based upon

the method of absorption pricing together supports in assuring the recovery of all relative costs

where such type of costing is also acceptable in source of variable costs. Although, it is apparent

to necessitate Dell to concentrate upon the preparation of pertinent reporting that is indicating the

involvement of various costs while undertaking this particular approach of costing.

On differentiating both these measures, it is apparent that the cost recognition of both

these methods are distinct from one other. It is where in the marginal cost approach, there exists

total two distinct type of costs namely product and period costs. Herein, the variable costs are

assumed as product costs and the fixed costs are interpreted as period costs. Whereas, the

absorption approach of costing refers to only a single cost where both fixed and variable costs

are considered as product cost.

However, both these methods are useful for the creation of income statements and has a

greater contribution in the decision making procedure of the organisations like Dell (). However,

on referring to the present case of Dell, it has been identified that the approach of absorption

costing is more beneficial for them and will duly support them to take cost related decisions.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control is referred to be a foremost consideration of the organisational bodies

to make an effective utilization of their funds by constantly monitoring their undertaken budget

and making its prompt usage in an undertaken time period of accounting . This process is usually

undertaken using distinct tools of planning with several benefits and drawbacks of each- Incremental budgeting- It is referred to be one of the essential component of accounting

system that duly assists the delegates to make an effective management of their funds

and investments. This type of budgeting is usually done by making small alterations in

the existent budget to create an entirely new budget (Otley and Emmanuel, 2013). A

significant benefit of this method is its easy execution with no complex computation.

However, its incremental nature is a leading drawback where it assumes a prime

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

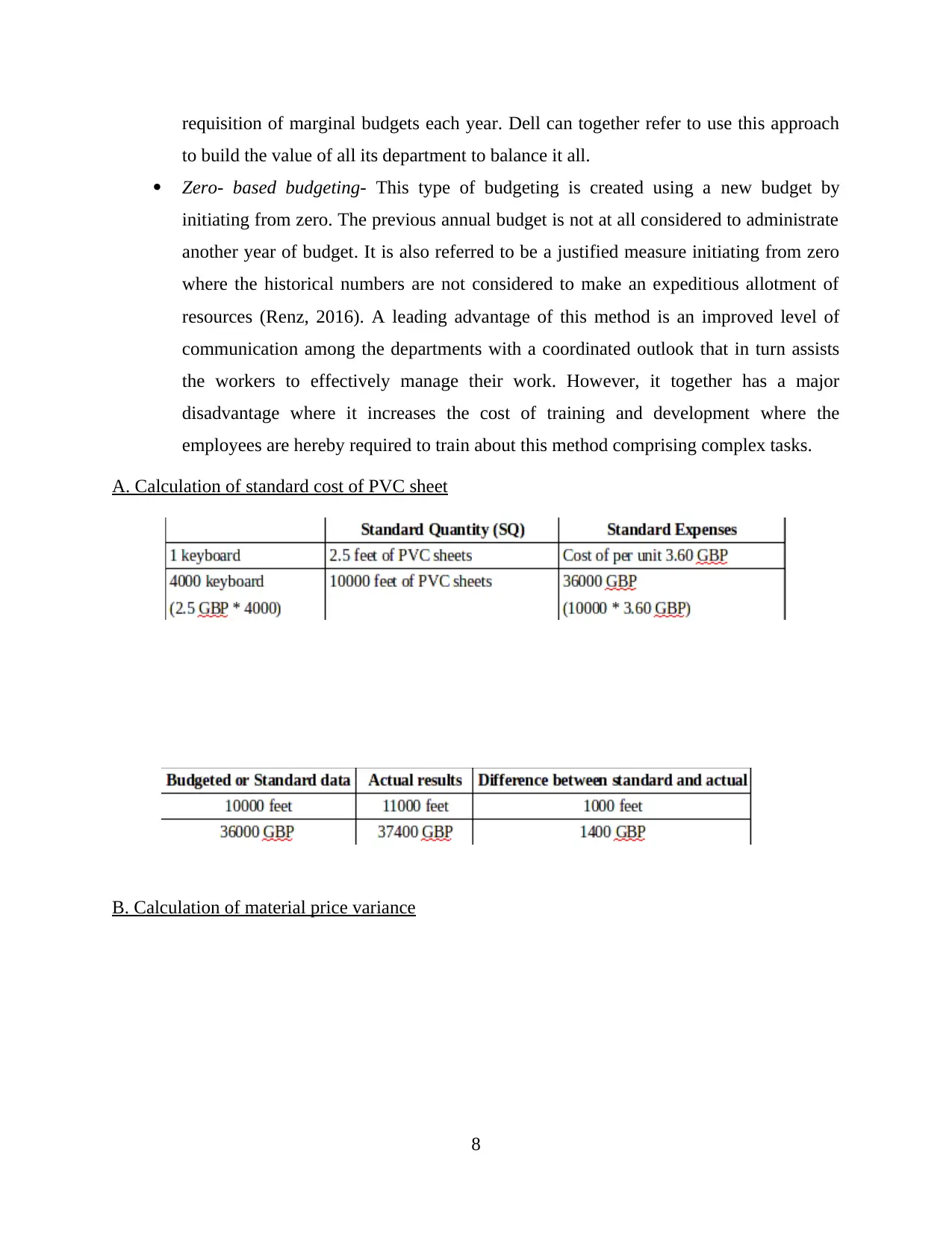

requisition of marginal budgets each year. Dell can together refer to use this approach

to build the value of all its department to balance it all.

Zero- based budgeting- This type of budgeting is created using a new budget by

initiating from zero. The previous annual budget is not at all considered to administrate

another year of budget. It is also referred to be a justified measure initiating from zero

where the historical numbers are not considered to make an expeditious allotment of

resources (Renz, 2016). A leading advantage of this method is an improved level of

communication among the departments with a coordinated outlook that in turn assists

the workers to effectively manage their work. However, it together has a major

disadvantage where it increases the cost of training and development where the

employees are hereby required to train about this method comprising complex tasks.

A. Calculation of standard cost of PVC sheet

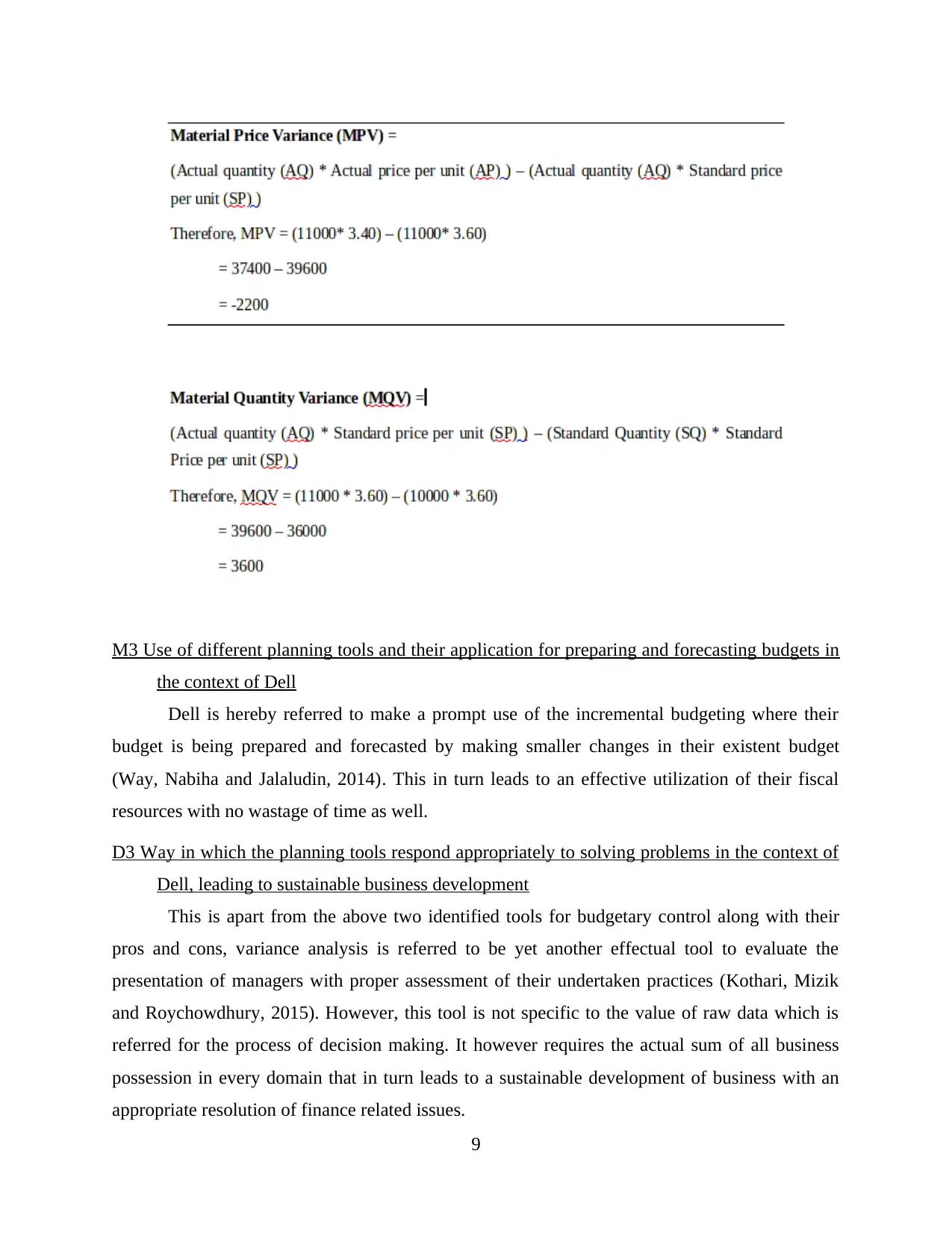

B. Calculation of material price variance

8

to build the value of all its department to balance it all.

Zero- based budgeting- This type of budgeting is created using a new budget by

initiating from zero. The previous annual budget is not at all considered to administrate

another year of budget. It is also referred to be a justified measure initiating from zero

where the historical numbers are not considered to make an expeditious allotment of

resources (Renz, 2016). A leading advantage of this method is an improved level of

communication among the departments with a coordinated outlook that in turn assists

the workers to effectively manage their work. However, it together has a major

disadvantage where it increases the cost of training and development where the

employees are hereby required to train about this method comprising complex tasks.

A. Calculation of standard cost of PVC sheet

B. Calculation of material price variance

8

M3 Use of different planning tools and their application for preparing and forecasting budgets in

the context of Dell

Dell is hereby referred to make a prompt use of the incremental budgeting where their

budget is being prepared and forecasted by making smaller changes in their existent budget

(Way, Nabiha and Jalaludin, 2014). This in turn leads to an effective utilization of their fiscal

resources with no wastage of time as well.

D3 Way in which the planning tools respond appropriately to solving problems in the context of

Dell, leading to sustainable business development

This is apart from the above two identified tools for budgetary control along with their

pros and cons, variance analysis is referred to be yet another effectual tool to evaluate the

presentation of managers with proper assessment of their undertaken practices (Kothari, Mizik

and Roychowdhury, 2015). However, this tool is not specific to the value of raw data which is

referred for the process of decision making. It however requires the actual sum of all business

possession in every domain that in turn leads to a sustainable development of business with an

appropriate resolution of finance related issues.

9

the context of Dell

Dell is hereby referred to make a prompt use of the incremental budgeting where their

budget is being prepared and forecasted by making smaller changes in their existent budget

(Way, Nabiha and Jalaludin, 2014). This in turn leads to an effective utilization of their fiscal

resources with no wastage of time as well.

D3 Way in which the planning tools respond appropriately to solving problems in the context of

Dell, leading to sustainable business development

This is apart from the above two identified tools for budgetary control along with their

pros and cons, variance analysis is referred to be yet another effectual tool to evaluate the

presentation of managers with proper assessment of their undertaken practices (Kothari, Mizik

and Roychowdhury, 2015). However, this tool is not specific to the value of raw data which is

referred for the process of decision making. It however requires the actual sum of all business

possession in every domain that in turn leads to a sustainable development of business with an

appropriate resolution of finance related issues.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.