Project Report: Management Accounting Analysis of US Bright Production

VerifiedAdded on 2020/05/28

|13

|3464

|173

Project

AI Summary

This project report presents a detailed analysis of management accounting principles, focusing on costing systems and budgeting methods within a production company, specifically US Bright Production. The report is divided into two main parts: Part A explores activity-based costing (ABC), evaluating the cost per unit of cakes and preparing a bill of activities to determine product costs, including a specific analysis of Lamington products. The report calculates the cost per unit, considering various activities and cost drivers, and provides detailed calculations for the bill of activities. Part B delves into budgeting, examining the company's current and future cash inflows, and assessing the impact of changes in the fee structure. The report includes calculations and evaluations of the company's financial position, offering insights for decision-making in costing, pricing, and overall financial management. References to relevant literature support the analysis.

Running Head: Management Accounting

1

Project Report: Management Accounting

1

Project Report: Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

2

Executive Summary

This report expresses about 2 cases in which first case express about the costing system

of an organization and other case briefs about the budgeting methods of a production

company. In first case, the total cost per cake has been evaluated and the bill of entire

activities has also been prepared in this report to evaluate the total cost of the cake per unit.

Product cost for Lamington has also been calculated and the extra cost details have been

given accordingly.

In second case, total cash inflows of the company has been measured according to the

present plan of the club and the cash inflows according to the future plan of the club. New

plan explain that the few changes in the fee structure of the club would make a change in the

total cash inflow of the company.

2

Executive Summary

This report expresses about 2 cases in which first case express about the costing system

of an organization and other case briefs about the budgeting methods of a production

company. In first case, the total cost per cake has been evaluated and the bill of entire

activities has also been prepared in this report to evaluate the total cost of the cake per unit.

Product cost for Lamington has also been calculated and the extra cost details have been

given accordingly.

In second case, total cash inflows of the company has been measured according to the

present plan of the club and the cash inflows according to the future plan of the club. New

plan explain that the few changes in the fee structure of the club would make a change in the

total cash inflow of the company.

Management Accounting

3

Contents

Executive Summary..........................................................................................................2

Part A: Activity Based costing.........................................................................................4

Introduction...................................................................................................................4

Cost per unit of the company........................................................................................4

Bill of activities.............................................................................................................6

Product cost for lamington............................................................................................7

Conclusion....................................................................................................................8

Part B: Budgeting.............................................................................................................9

Introduction...................................................................................................................9

Improvement in the fee structure................................................................................10

Assumptions...............................................................................................................11

Evaluation...................................................................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

3

Contents

Executive Summary..........................................................................................................2

Part A: Activity Based costing.........................................................................................4

Introduction...................................................................................................................4

Cost per unit of the company........................................................................................4

Bill of activities.............................................................................................................6

Product cost for lamington............................................................................................7

Conclusion....................................................................................................................8

Part B: Budgeting.............................................................................................................9

Introduction...................................................................................................................9

Improvement in the fee structure................................................................................10

Assumptions...............................................................................................................11

Evaluation...................................................................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

4

Part A: Activity Based costing

Activity based costing is a method of costing which is used by the administration,

companies and the stakeholders of an organization t measure the total cost of a product. In

this method, indirect cost is assigned to the activities and the process of manufacturing of the

product. Basically, under ABC method, an activity could be considered as an event or

transaction which is cost driver (Zimmerman and Yahya-Zadeh, 2011). This is used to

allocate the total indirect cost to products. Cost drivers contain maintenance request, machine

setups, purchase orders, production orders and power consumed.

Introduction:

In this report, a case has been evaluated and the indirect cost has been allocated to the

cost per unit according to their cost drivers. Basically, this case briefs about the US Bright

Production which mainly produces the cakes and the pastries. In this report, the total annual

cost of the company has been dividend according to the cost drivers. Or allocating and

assigning the total cost, activity based costing have been used. The total cost per cake has

been evaluated and the bill of entire activities has also been prepared in this report to evaluate

the total cost of the cake per unit. Product cost for Lamington has also been calculated and

the extra cost details have been given accordingly.

Cost per unit of the company:

It is required for every business to analyze and evaluate the cost per unit of the

product. Cost per unit could be calculated through dividing the activity cost on the basis of

cost drivers. In this case, the cost per unit of cakes has been calculated through assigning the

total cost on the basis of activity driver. Following is the calculations of cost per unit (these

calculations have been done according to the activity based costing):

Calculations of Activity Based Costing

Activity

Activity

cost Activity driver

Annual

quantity

Cost per

unit

Prepare annual cost

$

5,000

Process receivable

$

15,000 No of invoices

$

5,000

$

3.00

Process Payable $ No of purchase orders $ $

4

Part A: Activity Based costing

Activity based costing is a method of costing which is used by the administration,

companies and the stakeholders of an organization t measure the total cost of a product. In

this method, indirect cost is assigned to the activities and the process of manufacturing of the

product. Basically, under ABC method, an activity could be considered as an event or

transaction which is cost driver (Zimmerman and Yahya-Zadeh, 2011). This is used to

allocate the total indirect cost to products. Cost drivers contain maintenance request, machine

setups, purchase orders, production orders and power consumed.

Introduction:

In this report, a case has been evaluated and the indirect cost has been allocated to the

cost per unit according to their cost drivers. Basically, this case briefs about the US Bright

Production which mainly produces the cakes and the pastries. In this report, the total annual

cost of the company has been dividend according to the cost drivers. Or allocating and

assigning the total cost, activity based costing have been used. The total cost per cake has

been evaluated and the bill of entire activities has also been prepared in this report to evaluate

the total cost of the cake per unit. Product cost for Lamington has also been calculated and

the extra cost details have been given accordingly.

Cost per unit of the company:

It is required for every business to analyze and evaluate the cost per unit of the

product. Cost per unit could be calculated through dividing the activity cost on the basis of

cost drivers. In this case, the cost per unit of cakes has been calculated through assigning the

total cost on the basis of activity driver. Following is the calculations of cost per unit (these

calculations have been done according to the activity based costing):

Calculations of Activity Based Costing

Activity

Activity

cost Activity driver

Annual

quantity

Cost per

unit

Prepare annual cost

$

5,000

Process receivable

$

15,000 No of invoices

$

5,000

$

3.00

Process Payable $ No of purchase orders $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

5

25,000 2,500 10.00

Program Production

$

28,000

No of production

schedules

$

1,000

$

28.00

Process sales order

$

40,000 No of sales orders

$

4,000

$

10.00

Dispatch sales order

$

30,000 No of dispatches

$

2,500

$

12.00

Develop and test

products

$

60,000

Assigned directly to

products

Load mixers

$

14,050 No of batches

$

1,000

$

14.05

Operate mixers

$

45,900 No of kg

$

2,00,000

$

0.23

Clean mixers

$

6,900 No of trays

$

1,000

$

6.90

move mixture to filling

$

3,450 No of cake

$

2,00,000

$

0.02

Clean trays

$

20,000 No of trays

$

16,000

$

1.25

Fill trays

$

16,000 No of cake

$

8,00,000

$

0.02

Move to baking

$

8,000 No of trays

$

16,000

$

0.50

Set up ovens

$

50,000 No of batches

$

1,000

$

50.00

Bake cakes/ pastries

$

1,30,000 No of batches

$

1,000

$

130.00

Move to packing

$

40,000 No of trays

$

16,000

$

2.50

Pack cakes/ Pastries

$

80,000 No of cake

$

8,00,000

$

0.10

Inspect pastries

$

2,500 No of pastries

$

50,000

$

0.05

$

268.62

The above calculations explain that the cost per unit of the cake is $ 268.82. This

amount has been calculated through dividing the activity cost on the basis of cost drivers. The

above calculations express that the organization has to pay $ 268.82 to produce a single unit

of cake. The above calculations would assist the management of the company and the

production department to analyze that what is the total cost per unit of the product and how

much the price of the product should be (Weston and Brigham, 2015). More, it would also

5

25,000 2,500 10.00

Program Production

$

28,000

No of production

schedules

$

1,000

$

28.00

Process sales order

$

40,000 No of sales orders

$

4,000

$

10.00

Dispatch sales order

$

30,000 No of dispatches

$

2,500

$

12.00

Develop and test

products

$

60,000

Assigned directly to

products

Load mixers

$

14,050 No of batches

$

1,000

$

14.05

Operate mixers

$

45,900 No of kg

$

2,00,000

$

0.23

Clean mixers

$

6,900 No of trays

$

1,000

$

6.90

move mixture to filling

$

3,450 No of cake

$

2,00,000

$

0.02

Clean trays

$

20,000 No of trays

$

16,000

$

1.25

Fill trays

$

16,000 No of cake

$

8,00,000

$

0.02

Move to baking

$

8,000 No of trays

$

16,000

$

0.50

Set up ovens

$

50,000 No of batches

$

1,000

$

50.00

Bake cakes/ pastries

$

1,30,000 No of batches

$

1,000

$

130.00

Move to packing

$

40,000 No of trays

$

16,000

$

2.50

Pack cakes/ Pastries

$

80,000 No of cake

$

8,00,000

$

0.10

Inspect pastries

$

2,500 No of pastries

$

50,000

$

0.05

$

268.62

The above calculations explain that the cost per unit of the cake is $ 268.82. This

amount has been calculated through dividing the activity cost on the basis of cost drivers. The

above calculations express that the organization has to pay $ 268.82 to produce a single unit

of cake. The above calculations would assist the management of the company and the

production department to analyze that what is the total cost per unit of the product and how

much the price of the product should be (Weston and Brigham, 2015). More, it would also

Management Accounting

6

assist the production manager of the company to make various better decisions about the

position and the performance of the company.

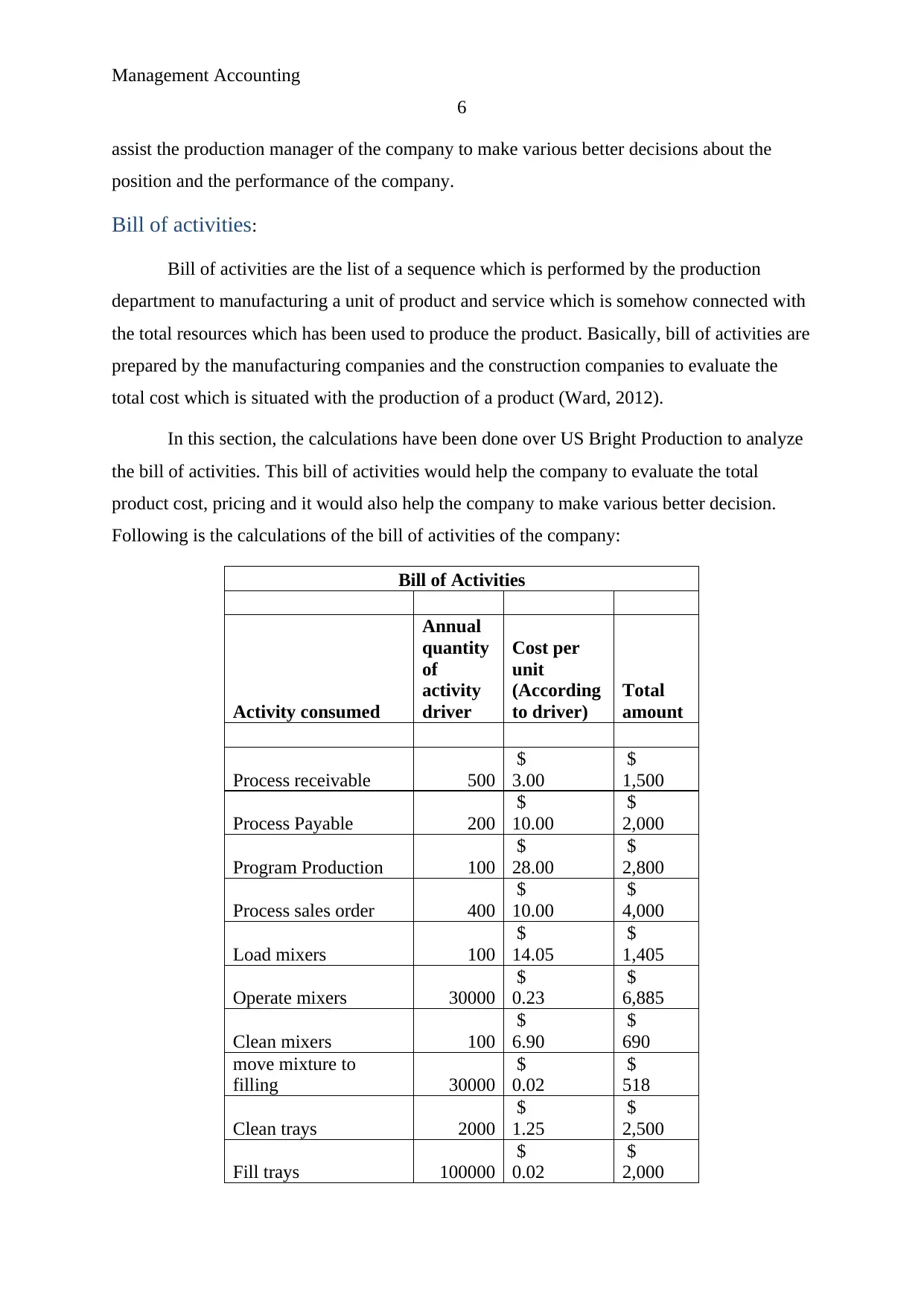

Bill of activities:

Bill of activities are the list of a sequence which is performed by the production

department to manufacturing a unit of product and service which is somehow connected with

the total resources which has been used to produce the product. Basically, bill of activities are

prepared by the manufacturing companies and the construction companies to evaluate the

total cost which is situated with the production of a product (Ward, 2012).

In this section, the calculations have been done over US Bright Production to analyze

the bill of activities. This bill of activities would help the company to evaluate the total

product cost, pricing and it would also help the company to make various better decision.

Following is the calculations of the bill of activities of the company:

Bill of Activities

Activity consumed

Annual

quantity

of

activity

driver

Cost per

unit

(According

to driver)

Total

amount

Process receivable 500

$

3.00

$

1,500

Process Payable 200

$

10.00

$

2,000

Program Production 100

$

28.00

$

2,800

Process sales order 400

$

10.00

$

4,000

Load mixers 100

$

14.05

$

1,405

Operate mixers 30000

$

0.23

$

6,885

Clean mixers 100

$

6.90

$

690

move mixture to

filling 30000

$

0.02

$

518

Clean trays 2000

$

1.25

$

2,500

Fill trays 100000

$

0.02

$

2,000

6

assist the production manager of the company to make various better decisions about the

position and the performance of the company.

Bill of activities:

Bill of activities are the list of a sequence which is performed by the production

department to manufacturing a unit of product and service which is somehow connected with

the total resources which has been used to produce the product. Basically, bill of activities are

prepared by the manufacturing companies and the construction companies to evaluate the

total cost which is situated with the production of a product (Ward, 2012).

In this section, the calculations have been done over US Bright Production to analyze

the bill of activities. This bill of activities would help the company to evaluate the total

product cost, pricing and it would also help the company to make various better decision.

Following is the calculations of the bill of activities of the company:

Bill of Activities

Activity consumed

Annual

quantity

of

activity

driver

Cost per

unit

(According

to driver)

Total

amount

Process receivable 500

$

3.00

$

1,500

Process Payable 200

$

10.00

$

2,000

Program Production 100

$

28.00

$

2,800

Process sales order 400

$

10.00

$

4,000

Load mixers 100

$

14.05

$

1,405

Operate mixers 30000

$

0.23

$

6,885

Clean mixers 100

$

6.90

$

690

move mixture to

filling 30000

$

0.02

$

518

Clean trays 2000

$

1.25

$

2,500

Fill trays 100000

$

0.02

$

2,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

7

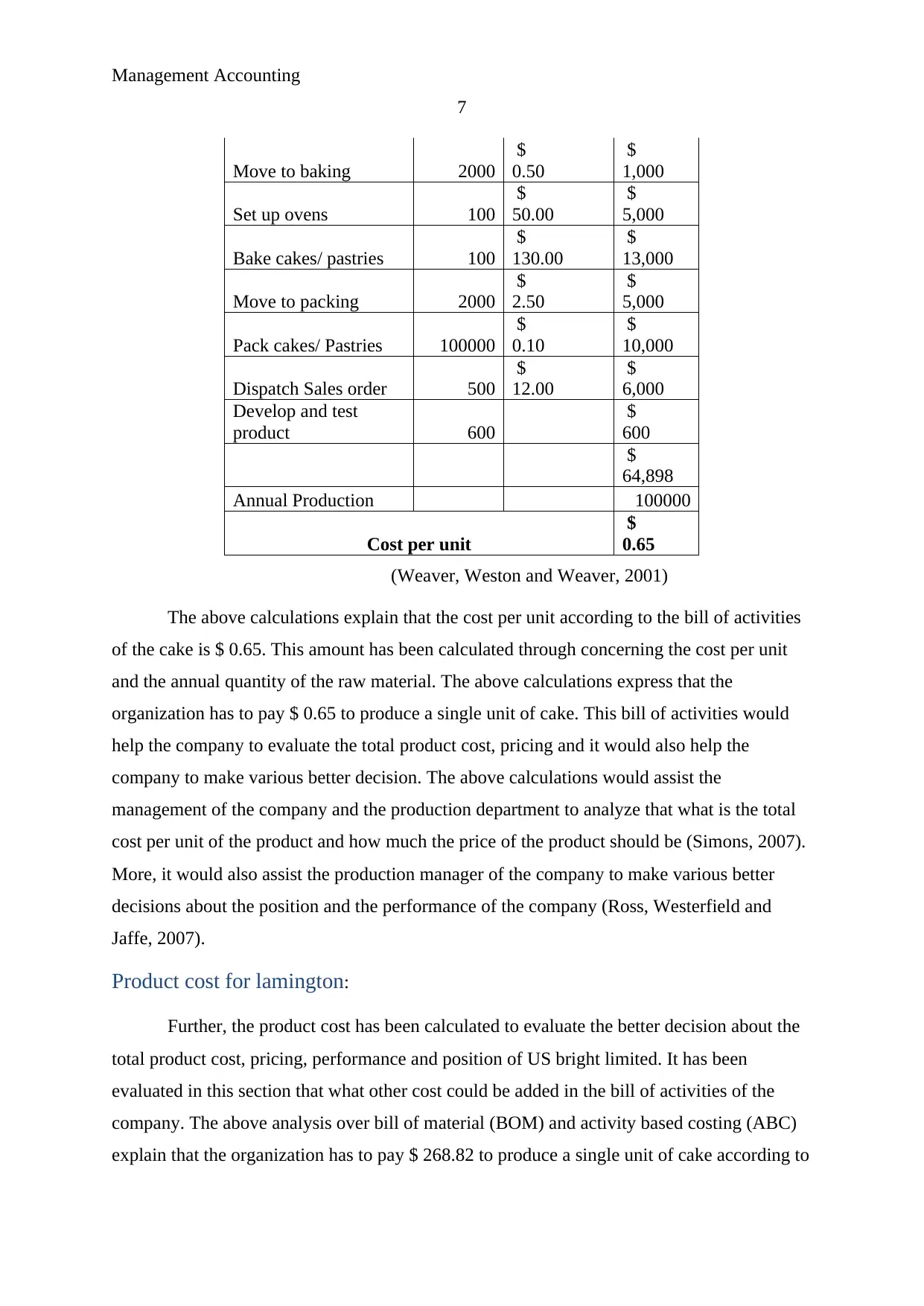

Move to baking 2000

$

0.50

$

1,000

Set up ovens 100

$

50.00

$

5,000

Bake cakes/ pastries 100

$

130.00

$

13,000

Move to packing 2000

$

2.50

$

5,000

Pack cakes/ Pastries 100000

$

0.10

$

10,000

Dispatch Sales order 500

$

12.00

$

6,000

Develop and test

product 600

$

600

$

64,898

Annual Production 100000

Cost per unit

$

0.65

(Weaver, Weston and Weaver, 2001)

The above calculations explain that the cost per unit according to the bill of activities

of the cake is $ 0.65. This amount has been calculated through concerning the cost per unit

and the annual quantity of the raw material. The above calculations express that the

organization has to pay $ 0.65 to produce a single unit of cake. This bill of activities would

help the company to evaluate the total product cost, pricing and it would also help the

company to make various better decision. The above calculations would assist the

management of the company and the production department to analyze that what is the total

cost per unit of the product and how much the price of the product should be (Simons, 2007).

More, it would also assist the production manager of the company to make various better

decisions about the position and the performance of the company (Ross, Westerfield and

Jaffe, 2007).

Product cost for lamington:

Further, the product cost has been calculated to evaluate the better decision about the

total product cost, pricing, performance and position of US bright limited. It has been

evaluated in this section that what other cost could be added in the bill of activities of the

company. The above analysis over bill of material (BOM) and activity based costing (ABC)

explain that the organization has to pay $ 268.82 to produce a single unit of cake according to

7

Move to baking 2000

$

0.50

$

1,000

Set up ovens 100

$

50.00

$

5,000

Bake cakes/ pastries 100

$

130.00

$

13,000

Move to packing 2000

$

2.50

$

5,000

Pack cakes/ Pastries 100000

$

0.10

$

10,000

Dispatch Sales order 500

$

12.00

$

6,000

Develop and test

product 600

$

600

$

64,898

Annual Production 100000

Cost per unit

$

0.65

(Weaver, Weston and Weaver, 2001)

The above calculations explain that the cost per unit according to the bill of activities

of the cake is $ 0.65. This amount has been calculated through concerning the cost per unit

and the annual quantity of the raw material. The above calculations express that the

organization has to pay $ 0.65 to produce a single unit of cake. This bill of activities would

help the company to evaluate the total product cost, pricing and it would also help the

company to make various better decision. The above calculations would assist the

management of the company and the production department to analyze that what is the total

cost per unit of the product and how much the price of the product should be (Simons, 2007).

More, it would also assist the production manager of the company to make various better

decisions about the position and the performance of the company (Ross, Westerfield and

Jaffe, 2007).

Product cost for lamington:

Further, the product cost has been calculated to evaluate the better decision about the

total product cost, pricing, performance and position of US bright limited. It has been

evaluated in this section that what other cost could be added in the bill of activities of the

company. The above analysis over bill of material (BOM) and activity based costing (ABC)

explain that the organization has to pay $ 268.82 to produce a single unit of cake according to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

8

ABC. The above calculations express that the organization has to pay $ 0.65 to produce a

single unit of cake according to BOM (Schlichting, 2013).

The evaluation expresses that the annual cost should be added by the company in bill of

material to evaluate the total cost per unit. The annual cost amount could affect the total

profit and the total cost of the company as it is a huge amount and thus this amount would

enhance the BOM amount a bit. Further, it has been calculated that the Lamington should add

the annual cost in the production cost to measure the company’s cost of capital (Atrill and

McLaney, 2006).

Conclusion:

To conclude, bill of material (BOM) and activity based costing (ABC) explain that the

organization has to pay $ 268.82 to produce a single unit of cake according to ABC. The

above calculations express that the organization has to pay $ 0.65 to produce a single unit of

cake according to BOM. More it has been identified that the Lamington should add the

annual cost in the production cost to measure the company’s cost of capital. The above

calculations and analysis would assist the management of the company and the production

department to analyze that what is the total cost per unit of the product and how much the

price of the product should be. More, it would also assist the production manager of the

company to make various better decisions about the position and the performance of the

company.

8

ABC. The above calculations express that the organization has to pay $ 0.65 to produce a

single unit of cake according to BOM (Schlichting, 2013).

The evaluation expresses that the annual cost should be added by the company in bill of

material to evaluate the total cost per unit. The annual cost amount could affect the total

profit and the total cost of the company as it is a huge amount and thus this amount would

enhance the BOM amount a bit. Further, it has been calculated that the Lamington should add

the annual cost in the production cost to measure the company’s cost of capital (Atrill and

McLaney, 2006).

Conclusion:

To conclude, bill of material (BOM) and activity based costing (ABC) explain that the

organization has to pay $ 268.82 to produce a single unit of cake according to ABC. The

above calculations express that the organization has to pay $ 0.65 to produce a single unit of

cake according to BOM. More it has been identified that the Lamington should add the

annual cost in the production cost to measure the company’s cost of capital. The above

calculations and analysis would assist the management of the company and the production

department to analyze that what is the total cost per unit of the product and how much the

price of the product should be. More, it would also assist the production manager of the

company to make various better decisions about the position and the performance of the

company.

Management Accounting

9

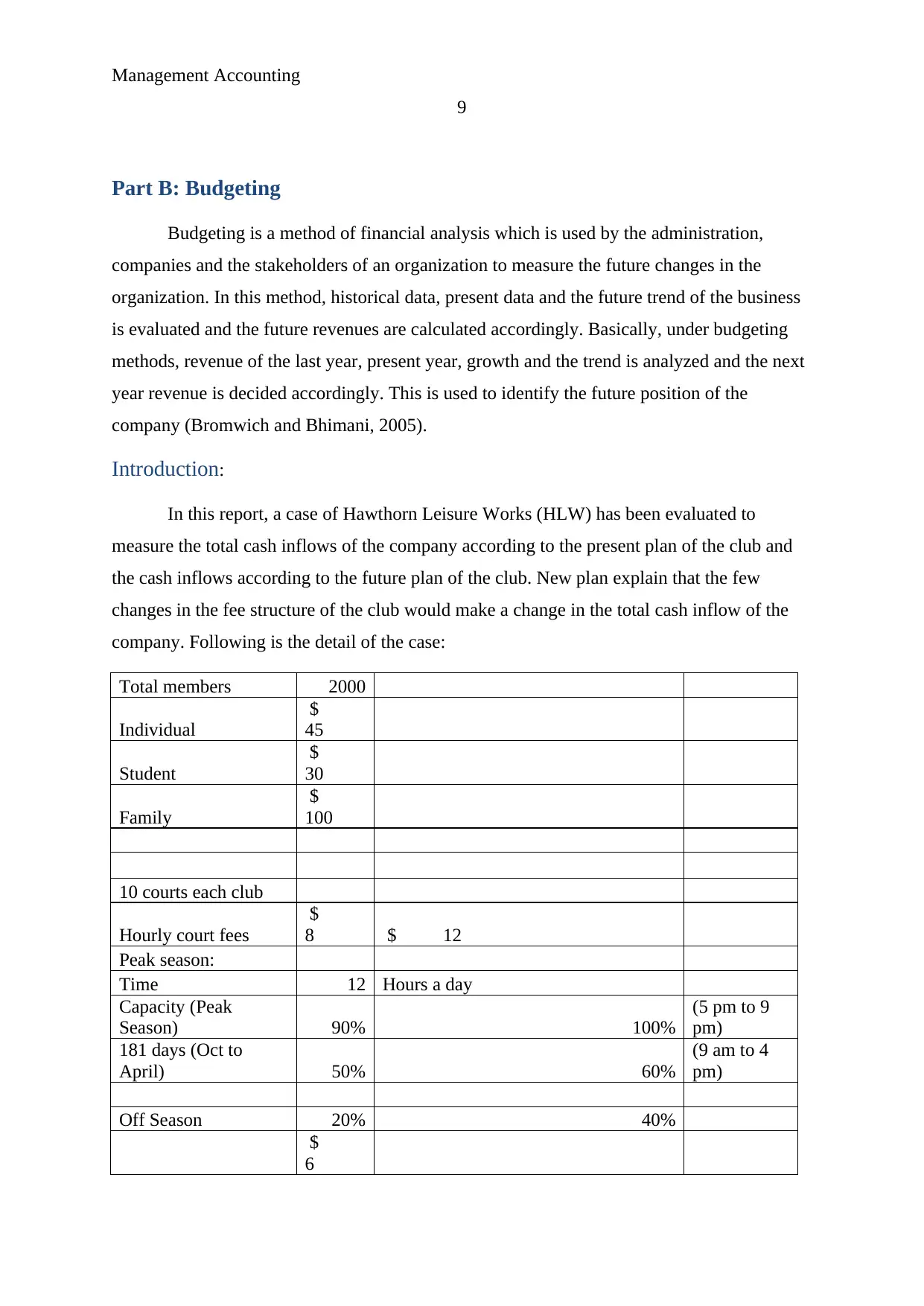

Part B: Budgeting

Budgeting is a method of financial analysis which is used by the administration,

companies and the stakeholders of an organization to measure the future changes in the

organization. In this method, historical data, present data and the future trend of the business

is evaluated and the future revenues are calculated accordingly. Basically, under budgeting

methods, revenue of the last year, present year, growth and the trend is analyzed and the next

year revenue is decided accordingly. This is used to identify the future position of the

company (Bromwich and Bhimani, 2005).

Introduction:

In this report, a case of Hawthorn Leisure Works (HLW) has been evaluated to

measure the total cash inflows of the company according to the present plan of the club and

the cash inflows according to the future plan of the club. New plan explain that the few

changes in the fee structure of the club would make a change in the total cash inflow of the

company. Following is the detail of the case:

Total members 2000

Individual

$

45

Student

$

30

Family

$

100

10 courts each club

Hourly court fees

$

8 $ 12

Peak season:

Time 12 Hours a day

Capacity (Peak

Season) 90% 100%

(5 pm to 9

pm)

181 days (Oct to

April) 50% 60%

(9 am to 4

pm)

Off Season 20% 40%

$

6

9

Part B: Budgeting

Budgeting is a method of financial analysis which is used by the administration,

companies and the stakeholders of an organization to measure the future changes in the

organization. In this method, historical data, present data and the future trend of the business

is evaluated and the future revenues are calculated accordingly. Basically, under budgeting

methods, revenue of the last year, present year, growth and the trend is analyzed and the next

year revenue is decided accordingly. This is used to identify the future position of the

company (Bromwich and Bhimani, 2005).

Introduction:

In this report, a case of Hawthorn Leisure Works (HLW) has been evaluated to

measure the total cash inflows of the company according to the present plan of the club and

the cash inflows according to the future plan of the club. New plan explain that the few

changes in the fee structure of the club would make a change in the total cash inflow of the

company. Following is the detail of the case:

Total members 2000

Individual

$

45

Student

$

30

Family

$

100

10 courts each club

Hourly court fees

$

8 $ 12

Peak season:

Time 12 Hours a day

Capacity (Peak

Season) 90% 100%

(5 pm to 9

pm)

181 days (Oct to

April) 50% 60%

(9 am to 4

pm)

Off Season 20% 40%

$

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting

10

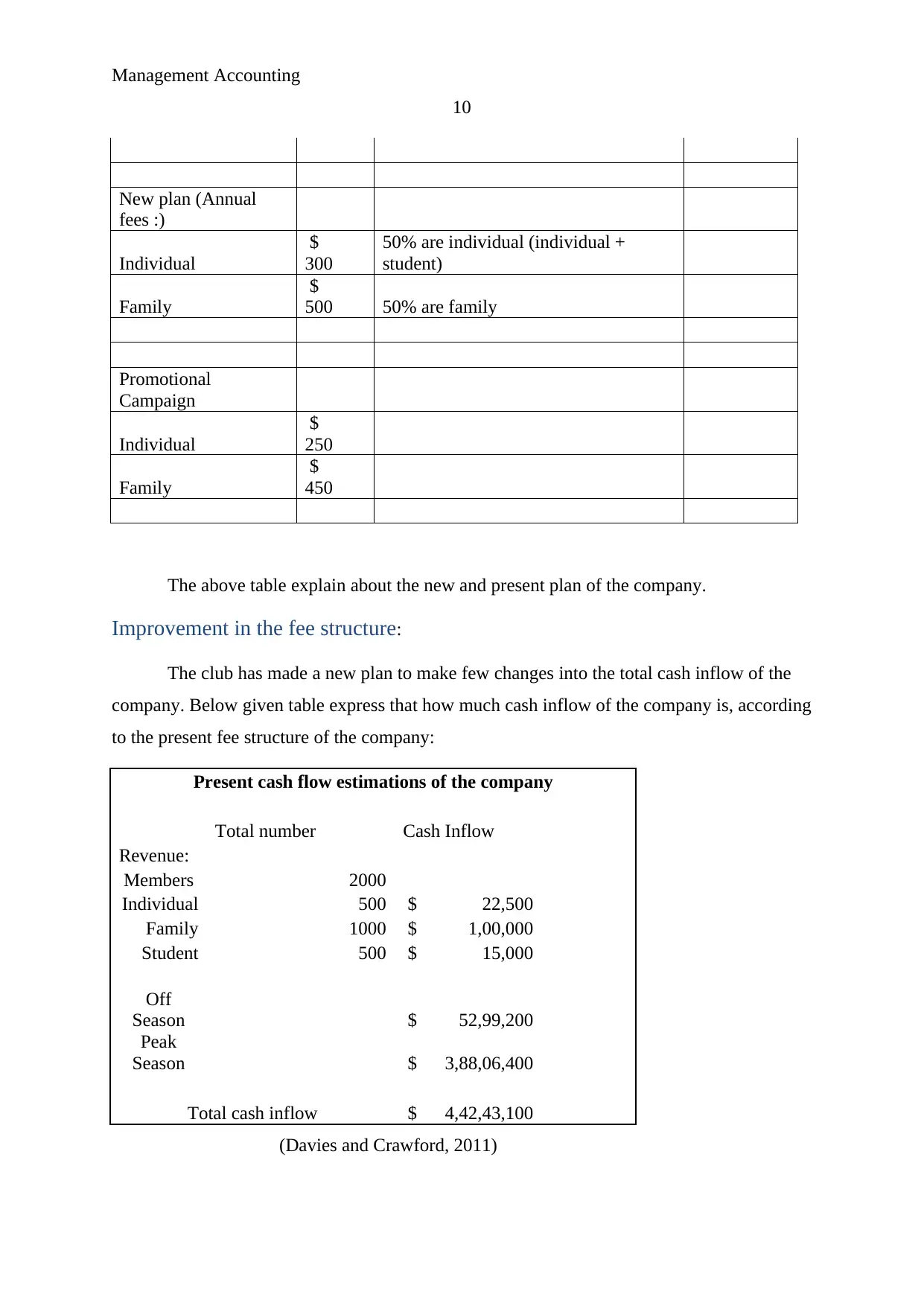

New plan (Annual

fees :)

Individual

$

300

50% are individual (individual +

student)

Family

$

500 50% are family

Promotional

Campaign

Individual

$

250

Family

$

450

The above table explain about the new and present plan of the company.

Improvement in the fee structure:

The club has made a new plan to make few changes into the total cash inflow of the

company. Below given table express that how much cash inflow of the company is, according

to the present fee structure of the company:

Present cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 2000

Individual 500 $ 22,500

Family 1000 $ 1,00,000

Student 500 $ 15,000

Off

Season $ 52,99,200

Peak

Season $ 3,88,06,400

Total cash inflow $ 4,42,43,100

(Davies and Crawford, 2011)

10

New plan (Annual

fees :)

Individual

$

300

50% are individual (individual +

student)

Family

$

500 50% are family

Promotional

Campaign

Individual

$

250

Family

$

450

The above table explain about the new and present plan of the company.

Improvement in the fee structure:

The club has made a new plan to make few changes into the total cash inflow of the

company. Below given table express that how much cash inflow of the company is, according

to the present fee structure of the company:

Present cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 2000

Individual 500 $ 22,500

Family 1000 $ 1,00,000

Student 500 $ 15,000

Off

Season $ 52,99,200

Peak

Season $ 3,88,06,400

Total cash inflow $ 4,42,43,100

(Davies and Crawford, 2011)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

11

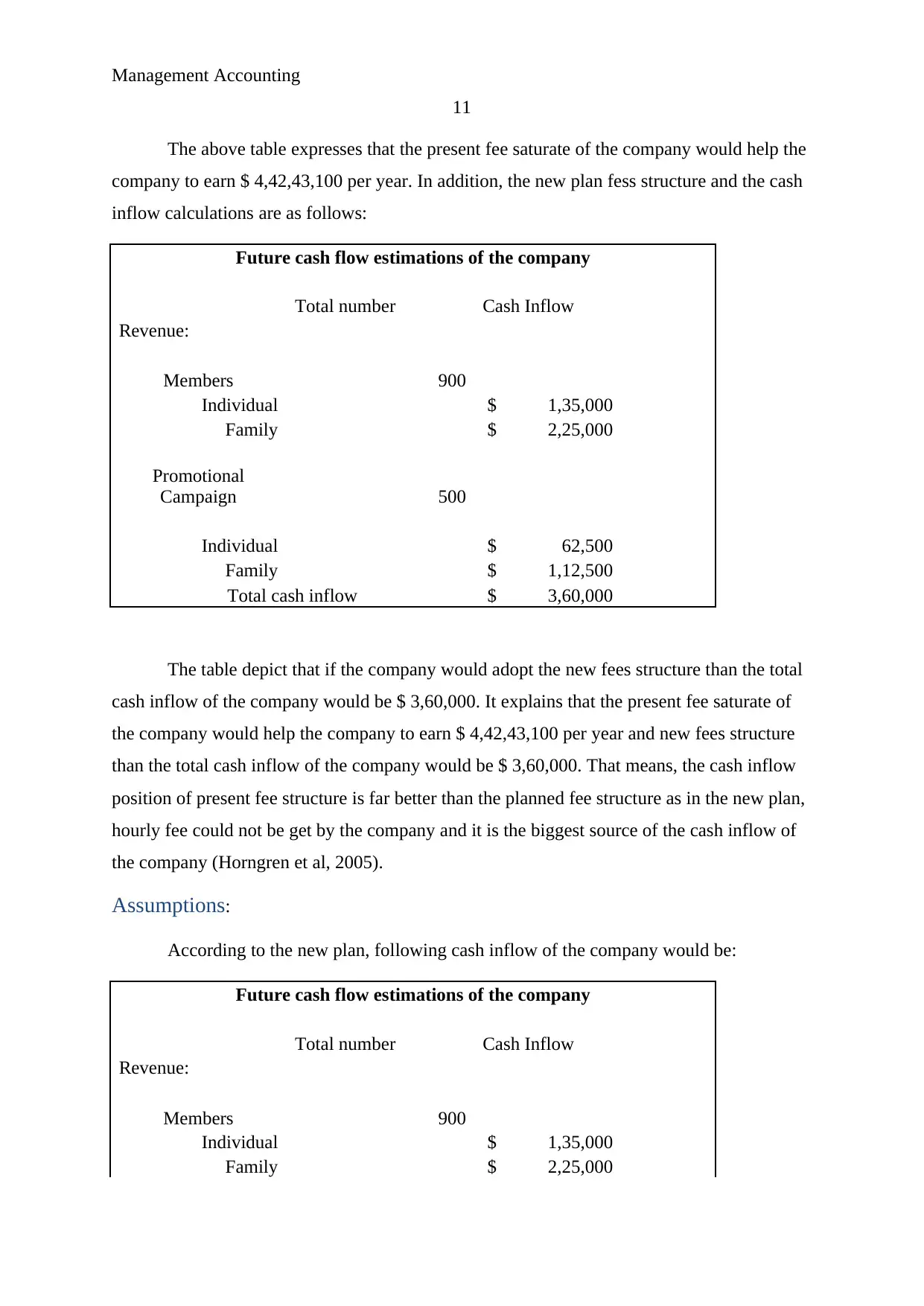

The above table expresses that the present fee saturate of the company would help the

company to earn $ 4,42,43,100 per year. In addition, the new plan fess structure and the cash

inflow calculations are as follows:

Future cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 900

Individual $ 1,35,000

Family $ 2,25,000

Promotional

Campaign 500

Individual $ 62,500

Family $ 1,12,500

Total cash inflow $ 3,60,000

The table depict that if the company would adopt the new fees structure than the total

cash inflow of the company would be $ 3,60,000. It explains that the present fee saturate of

the company would help the company to earn $ 4,42,43,100 per year and new fees structure

than the total cash inflow of the company would be $ 3,60,000. That means, the cash inflow

position of present fee structure is far better than the planned fee structure as in the new plan,

hourly fee could not be get by the company and it is the biggest source of the cash inflow of

the company (Horngren et al, 2005).

Assumptions:

According to the new plan, following cash inflow of the company would be:

Future cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 900

Individual $ 1,35,000

Family $ 2,25,000

11

The above table expresses that the present fee saturate of the company would help the

company to earn $ 4,42,43,100 per year. In addition, the new plan fess structure and the cash

inflow calculations are as follows:

Future cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 900

Individual $ 1,35,000

Family $ 2,25,000

Promotional

Campaign 500

Individual $ 62,500

Family $ 1,12,500

Total cash inflow $ 3,60,000

The table depict that if the company would adopt the new fees structure than the total

cash inflow of the company would be $ 3,60,000. It explains that the present fee saturate of

the company would help the company to earn $ 4,42,43,100 per year and new fees structure

than the total cash inflow of the company would be $ 3,60,000. That means, the cash inflow

position of present fee structure is far better than the planned fee structure as in the new plan,

hourly fee could not be get by the company and it is the biggest source of the cash inflow of

the company (Horngren et al, 2005).

Assumptions:

According to the new plan, following cash inflow of the company would be:

Future cash flow estimations of the company

Total number Cash Inflow

Revenue:

Members 900

Individual $ 1,35,000

Family $ 2,25,000

Management Accounting

12

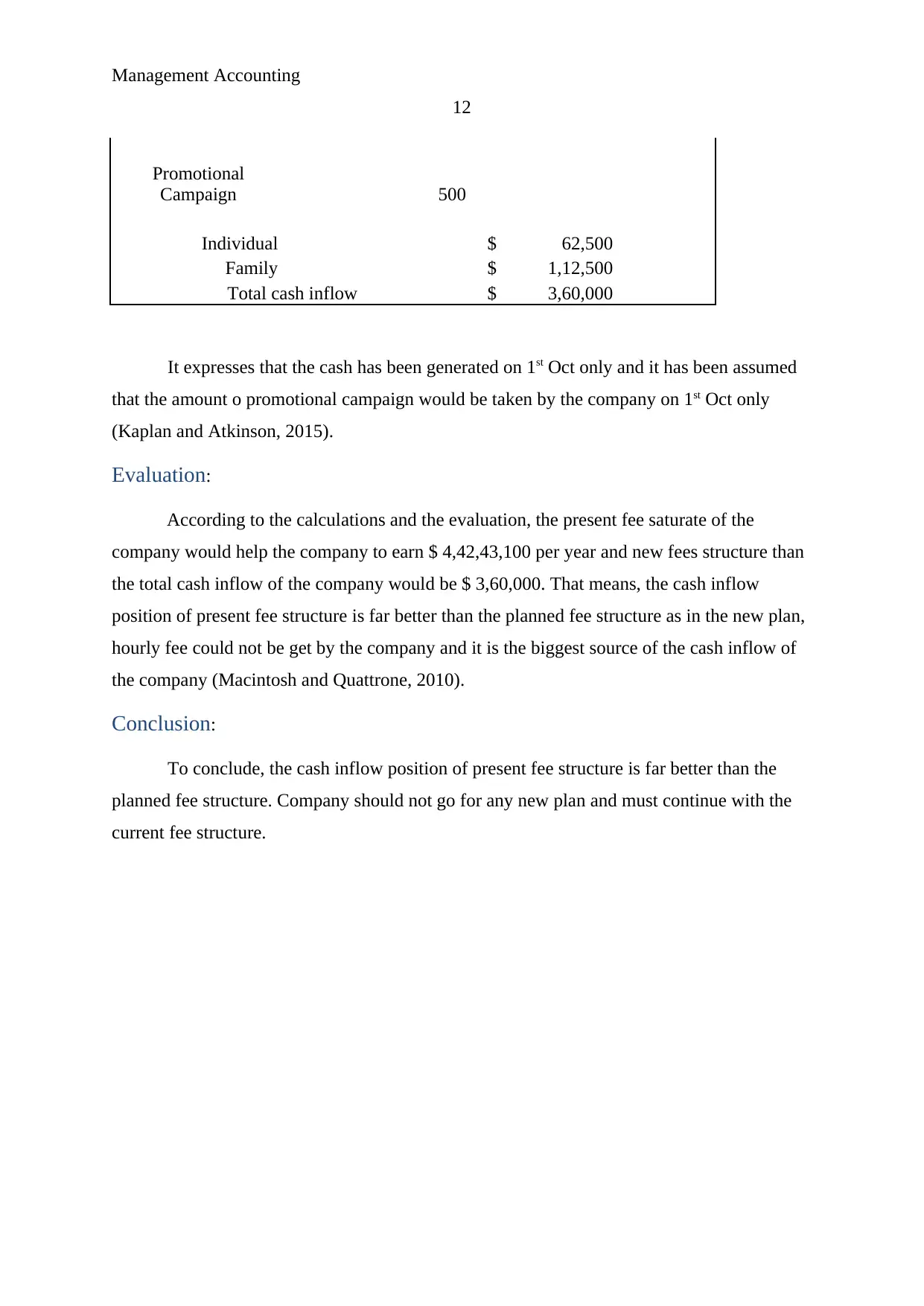

Promotional

Campaign 500

Individual $ 62,500

Family $ 1,12,500

Total cash inflow $ 3,60,000

It expresses that the cash has been generated on 1st Oct only and it has been assumed

that the amount o promotional campaign would be taken by the company on 1st Oct only

(Kaplan and Atkinson, 2015).

Evaluation:

According to the calculations and the evaluation, the present fee saturate of the

company would help the company to earn $ 4,42,43,100 per year and new fees structure than

the total cash inflow of the company would be $ 3,60,000. That means, the cash inflow

position of present fee structure is far better than the planned fee structure as in the new plan,

hourly fee could not be get by the company and it is the biggest source of the cash inflow of

the company (Macintosh and Quattrone, 2010).

Conclusion:

To conclude, the cash inflow position of present fee structure is far better than the

planned fee structure. Company should not go for any new plan and must continue with the

current fee structure.

12

Promotional

Campaign 500

Individual $ 62,500

Family $ 1,12,500

Total cash inflow $ 3,60,000

It expresses that the cash has been generated on 1st Oct only and it has been assumed

that the amount o promotional campaign would be taken by the company on 1st Oct only

(Kaplan and Atkinson, 2015).

Evaluation:

According to the calculations and the evaluation, the present fee saturate of the

company would help the company to earn $ 4,42,43,100 per year and new fees structure than

the total cash inflow of the company would be $ 3,60,000. That means, the cash inflow

position of present fee structure is far better than the planned fee structure as in the new plan,

hourly fee could not be get by the company and it is the biggest source of the cash inflow of

the company (Macintosh and Quattrone, 2010).

Conclusion:

To conclude, the cash inflow position of present fee structure is far better than the

planned fee structure. Company should not go for any new plan and must continue with the

current fee structure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.