Management Accounting Report: Financial Decision Making Tools

VerifiedAdded on 2020/06/04

|13

|3519

|41

Report

AI Summary

This report delves into the core principles of management accounting, exploring its role in providing financial and non-financial information to facilitate effective decision-making within organizations. It distinguishes management accounting from financial accounting, highlighting the former's focus on internal use and forward-looking perspectives. The report examines key management accounting tools such as relevant cost analysis, make-or-buy analysis, activity-based costing, inventory management, and job costing. Furthermore, it presents various types of managerial accounting reports, including budget reports and performance reports, emphasizing their importance in conveying information understandably. The report then compares marginal costing and absorption costing methods, illustrating their application through financial statements and reconciliation, and evaluates their impact on profit calculation. Finally, it discusses the advantages and disadvantages of planning tools like budgets and the balance scorecard approach, providing a comprehensive overview of management accounting practices and their influence on financial performance and strategic decision-making within a company, specifically focusing on the context of Tech Ltd.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A). Explanation of management accounting and its essential requirements:.........................1

B). Presenting financial information:.....................................................................................3

M1...........................................................................................................................................4

D1...........................................................................................................................................4

TASK 2............................................................................................................................................4

M2...........................................................................................................................................6

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4: Advantages and disadvantages of planning tools............................................................7

M3...........................................................................................................................................8

D3...........................................................................................................................................8

TASK 4............................................................................................................................................9

P5. Balance score card approach:...........................................................................................9

M4.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A). Explanation of management accounting and its essential requirements:.........................1

B). Presenting financial information:.....................................................................................3

M1...........................................................................................................................................4

D1...........................................................................................................................................4

TASK 2............................................................................................................................................4

M2...........................................................................................................................................6

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4: Advantages and disadvantages of planning tools............................................................7

M3...........................................................................................................................................8

D3...........................................................................................................................................8

TASK 4............................................................................................................................................9

P5. Balance score card approach:...........................................................................................9

M4.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management is the major branch in any organisation as this helps the firm to make their

process sustainable so that the firm can attain their pre-set targets effectively. Management

accounting is the major task which is used by the finance in tech company in order to make their

operations so smooth and transparent (Parker, 2012). Under this report, various management

accounting tools are discussed, reporting methods are also determined, various types of

budgetary tools are used within the firm so that the management can get the competitive

advantages.

TASK 1

A). Explanation of management accounting and its essential requirements:

1. Distinguishing Management accounting from Financial Accounting:

Management accounting is the tool that are used by the finance in tech in order to

provides the financial and non-financial information to the managers so that they can make

decisions accordingly. Various business decisions enables the firm to be better equipped in their

management and control functions. Management accounting system is mainly forward looking

rather than based on the historical and this is framed after keeping in mind the managers of the

firm. This system is confidential and applied by the management, rather than publicly reported.

Financial accounting and management accounting is the part of accounting process as these are

the two different branches. Financial accounting emphasis on providing the fair view of the

financial position on the firm to various stakeholders so that the they can make their investment

related strategies. While on the other hand, management accounting is the one which main

purpose to provides qualitative and quantitative information to the managers of the firm which

would assist the firm to take various strategies and also able to maximize the profits.

2. Importance of management accounting information as a decision making tools for

department managers:

There are so many decisions needed to take by the managers in a day. MA information

renders the data driven input to these decisions, that could enhance decision making over the

long term. Management accounting is used by the company's manager in order to have various

under-mentioned analysis:

1

Management is the major branch in any organisation as this helps the firm to make their

process sustainable so that the firm can attain their pre-set targets effectively. Management

accounting is the major task which is used by the finance in tech company in order to make their

operations so smooth and transparent (Parker, 2012). Under this report, various management

accounting tools are discussed, reporting methods are also determined, various types of

budgetary tools are used within the firm so that the management can get the competitive

advantages.

TASK 1

A). Explanation of management accounting and its essential requirements:

1. Distinguishing Management accounting from Financial Accounting:

Management accounting is the tool that are used by the finance in tech in order to

provides the financial and non-financial information to the managers so that they can make

decisions accordingly. Various business decisions enables the firm to be better equipped in their

management and control functions. Management accounting system is mainly forward looking

rather than based on the historical and this is framed after keeping in mind the managers of the

firm. This system is confidential and applied by the management, rather than publicly reported.

Financial accounting and management accounting is the part of accounting process as these are

the two different branches. Financial accounting emphasis on providing the fair view of the

financial position on the firm to various stakeholders so that the they can make their investment

related strategies. While on the other hand, management accounting is the one which main

purpose to provides qualitative and quantitative information to the managers of the firm which

would assist the firm to take various strategies and also able to maximize the profits.

2. Importance of management accounting information as a decision making tools for

department managers:

There are so many decisions needed to take by the managers in a day. MA information

renders the data driven input to these decisions, that could enhance decision making over the

long term. Management accounting is used by the company's manager in order to have various

under-mentioned analysis:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relevant cost analysis: MA reports are implemented by the firm to identify the selling

process (Qian, Burritt and Monroe, 2011). To evaluate such decisions, management accountant

assess the costs which differentiate between advertising alternatives for each product, avoiding

common costs. Such process is known as relevant cost analysis and is taught in basic managerial

accounting courses.

Make or Buy Analysis: The main aim of such MA information is to renders information

implemented in the production. With the help of this analysis, manager will get to know about

whether they need to produce the product or to buy form the outsiders. By analysing,

management can identify the choice that are more profitable for the firm.

Activity- based costing method: This is the method that company has identified about

the goods that are required to sell, business requires to identify about whom they can sell the

products. With the help of ABC techniques, management could identify the activities which are

needed to be produced and service a product line.

These are the above-mentioned things that are required to be done by the management in

order to get the sustainability.

3. Cost accounting system:

It is the accounting system which is used by the firm in order to identify the cost of

production and also makes efforts in order to lower the price of the products by eliminating

waste from the cost of production. There are basically three methods that are used by the firm I.e

Actual costing, Normal costing and the Standard costing.

Actual costing is recording of products costs after considering following factors:Actual

cost of materials, actual cost of labour, actual overhead costs incurred. Henceforth, the

main point under an actual costing system is that this only implement actual costs

covered and allocation bases experienced. This does not form any kind of budgeted

amount. This is the most convenient method which does not require pre-plan of the

standard cost.

Normal costing: It is the one which is used by the manager to identify the cost of a

product. This covers: Actual cost of materials, labour and standard overheads. But there

is difference in the actual and standard overheads cost. By this, firm can either charge the

difference to cost of sales or prorate difference between COGS and inventory.

2

process (Qian, Burritt and Monroe, 2011). To evaluate such decisions, management accountant

assess the costs which differentiate between advertising alternatives for each product, avoiding

common costs. Such process is known as relevant cost analysis and is taught in basic managerial

accounting courses.

Make or Buy Analysis: The main aim of such MA information is to renders information

implemented in the production. With the help of this analysis, manager will get to know about

whether they need to produce the product or to buy form the outsiders. By analysing,

management can identify the choice that are more profitable for the firm.

Activity- based costing method: This is the method that company has identified about

the goods that are required to sell, business requires to identify about whom they can sell the

products. With the help of ABC techniques, management could identify the activities which are

needed to be produced and service a product line.

These are the above-mentioned things that are required to be done by the management in

order to get the sustainability.

3. Cost accounting system:

It is the accounting system which is used by the firm in order to identify the cost of

production and also makes efforts in order to lower the price of the products by eliminating

waste from the cost of production. There are basically three methods that are used by the firm I.e

Actual costing, Normal costing and the Standard costing.

Actual costing is recording of products costs after considering following factors:Actual

cost of materials, actual cost of labour, actual overhead costs incurred. Henceforth, the

main point under an actual costing system is that this only implement actual costs

covered and allocation bases experienced. This does not form any kind of budgeted

amount. This is the most convenient method which does not require pre-plan of the

standard cost.

Normal costing: It is the one which is used by the manager to identify the cost of a

product. This covers: Actual cost of materials, labour and standard overheads. But there

is difference in the actual and standard overheads cost. By this, firm can either charge the

difference to cost of sales or prorate difference between COGS and inventory.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing: This is the practice of substituting an estimated cost for an actual one in

an accounting year, and then periodically recording variances which are diverse between

the estimated and the actual one.

4. Inventory management system: The management accounting officer is the main person who

inherently controls and regulate the inventory in an effective manner (Otley and Emmanuel,

2013). Inventory management is used by the manager in order to track the inventory levels,

orders, sales and deliveries. This can also be utilized in the production industry to form a work

order, bill of materials and other manufacturing related documents.

5. Job costing system: this is the system that are used by the manager in order to assign the

manufacturing costs to an each product or batches of product. Normally, this technique is used

by the manger at the time when the products produced are adequately diverse from each other.

B). Presenting financial information:

1. Various types of managerial accounting reports: There are various kinds of reports that are

required to be made by the MA officer in an effective manner so that the business can run

effectively. These includes product costs reports, budget reports, performance reports and others.

Budget report: one of the key factor in the management accounting is to make budget.

These are made by applying past records and then make the future budgeted figures. With the

help of budget report, this also been cited that the company on the basis of such assumption can

compare their budgeted results with the actual one which will help out to take certain strategies

in a better manner.

Performance report: With the help of this report, company could get to know the

performance and then react accordingly. As there are certain tools which are required to know

about the performance of the company. The variation occurred after comparing budgeted and

actual figure, are minimised and tries to eliminate them. These reports helps the firm to make

better strategies in order to assess the performance.

2. Their importance for information to be presented in understandable manner:

These reports assist the firm to have the better strategies in order to get the sustainability. By

applying these tools, per unit cost is determined and that can be compared to the competitors

product prices so that they could make the strategies accordingly so that they could attain the

3

an accounting year, and then periodically recording variances which are diverse between

the estimated and the actual one.

4. Inventory management system: The management accounting officer is the main person who

inherently controls and regulate the inventory in an effective manner (Otley and Emmanuel,

2013). Inventory management is used by the manager in order to track the inventory levels,

orders, sales and deliveries. This can also be utilized in the production industry to form a work

order, bill of materials and other manufacturing related documents.

5. Job costing system: this is the system that are used by the manager in order to assign the

manufacturing costs to an each product or batches of product. Normally, this technique is used

by the manger at the time when the products produced are adequately diverse from each other.

B). Presenting financial information:

1. Various types of managerial accounting reports: There are various kinds of reports that are

required to be made by the MA officer in an effective manner so that the business can run

effectively. These includes product costs reports, budget reports, performance reports and others.

Budget report: one of the key factor in the management accounting is to make budget.

These are made by applying past records and then make the future budgeted figures. With the

help of budget report, this also been cited that the company on the basis of such assumption can

compare their budgeted results with the actual one which will help out to take certain strategies

in a better manner.

Performance report: With the help of this report, company could get to know the

performance and then react accordingly. As there are certain tools which are required to know

about the performance of the company. The variation occurred after comparing budgeted and

actual figure, are minimised and tries to eliminate them. These reports helps the firm to make

better strategies in order to assess the performance.

2. Their importance for information to be presented in understandable manner:

These reports assist the firm to have the better strategies in order to get the sustainability. By

applying these tools, per unit cost is determined and that can be compared to the competitors

product prices so that they could make the strategies accordingly so that they could attain the

3

targets of the firm. The wastage cost can be eliminated after applying cost related strategy in an

effective manner.

M1.

The cited company needs to make certain strategies in order to implement the

management accounting tools. With the help of management accounting, company is able to get

the sustainability in an effective manner. There are so many tools that are needed in order to

provides effective outcome. There are so many tools of management accounting that are used by

the firm in order to get the product done in an effective manner. The tech Ltd company apply

management accounting tools in order to get the competitive advantages over the other

competitors.

D1

Management accounting tools are used by the firm for achieving sustainability but on the

other way, these accounting tools are integrated with the management accounting reporting in

order to get the sustainability over the other rivals. There is a need to provide effective outcome

for getting sustainability.

TASK 2

The net profits of finance in tech company is assessed by using marginal costing and

absorption costing methods, and then compare about which method is useful so that maximum

profits can be earned.

Marginal costing: this is the costing method under which extra cost is determined for

making an additional units in the firm (Østergren and Stensaker, 2011). This is normally a tool or

approach that helps the firm for making decisions. This is the change in the total cost which

emerge from producing an additional unit. This is the cost which categories the variable and

fixed costs. Marginal cost is known as he cost of additional or one less unit produced apart from

the current level of production.

Absorption costing: This is the costing tool which is used for collecting cost related

information from the manufacturing process and apportioned them in an individual goods. Such

types of costing is required as per the accounting standards in order to make the stock valuation

under a company. Under this, the cost which are related to manufacturing of goods are covered

irrespective of fixed or variable costs.

4

effective manner.

M1.

The cited company needs to make certain strategies in order to implement the

management accounting tools. With the help of management accounting, company is able to get

the sustainability in an effective manner. There are so many tools that are needed in order to

provides effective outcome. There are so many tools of management accounting that are used by

the firm in order to get the product done in an effective manner. The tech Ltd company apply

management accounting tools in order to get the competitive advantages over the other

competitors.

D1

Management accounting tools are used by the firm for achieving sustainability but on the

other way, these accounting tools are integrated with the management accounting reporting in

order to get the sustainability over the other rivals. There is a need to provide effective outcome

for getting sustainability.

TASK 2

The net profits of finance in tech company is assessed by using marginal costing and

absorption costing methods, and then compare about which method is useful so that maximum

profits can be earned.

Marginal costing: this is the costing method under which extra cost is determined for

making an additional units in the firm (Østergren and Stensaker, 2011). This is normally a tool or

approach that helps the firm for making decisions. This is the change in the total cost which

emerge from producing an additional unit. This is the cost which categories the variable and

fixed costs. Marginal cost is known as he cost of additional or one less unit produced apart from

the current level of production.

Absorption costing: This is the costing tool which is used for collecting cost related

information from the manufacturing process and apportioned them in an individual goods. Such

types of costing is required as per the accounting standards in order to make the stock valuation

under a company. Under this, the cost which are related to manufacturing of goods are covered

irrespective of fixed or variable costs.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

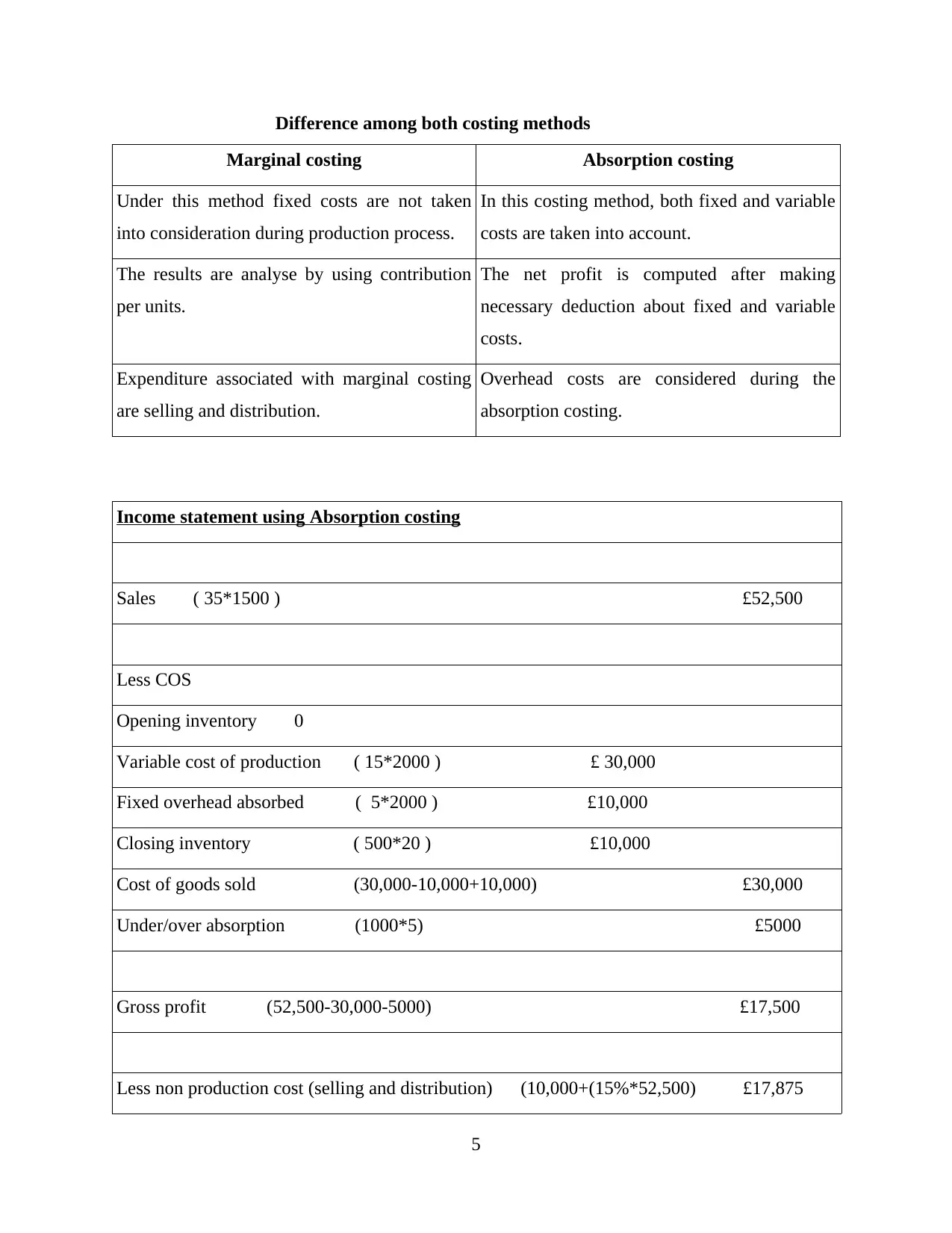

Difference among both costing methods

Marginal costing Absorption costing

Under this method fixed costs are not taken

into consideration during production process.

In this costing method, both fixed and variable

costs are taken into account.

The results are analyse by using contribution

per units.

The net profit is computed after making

necessary deduction about fixed and variable

costs.

Expenditure associated with marginal costing

are selling and distribution.

Overhead costs are considered during the

absorption costing.

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

5

Marginal costing Absorption costing

Under this method fixed costs are not taken

into consideration during production process.

In this costing method, both fixed and variable

costs are taken into account.

The results are analyse by using contribution

per units.

The net profit is computed after making

necessary deduction about fixed and variable

costs.

Expenditure associated with marginal costing

are selling and distribution.

Overhead costs are considered during the

absorption costing.

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit/loss (17,500-17,875) -£375

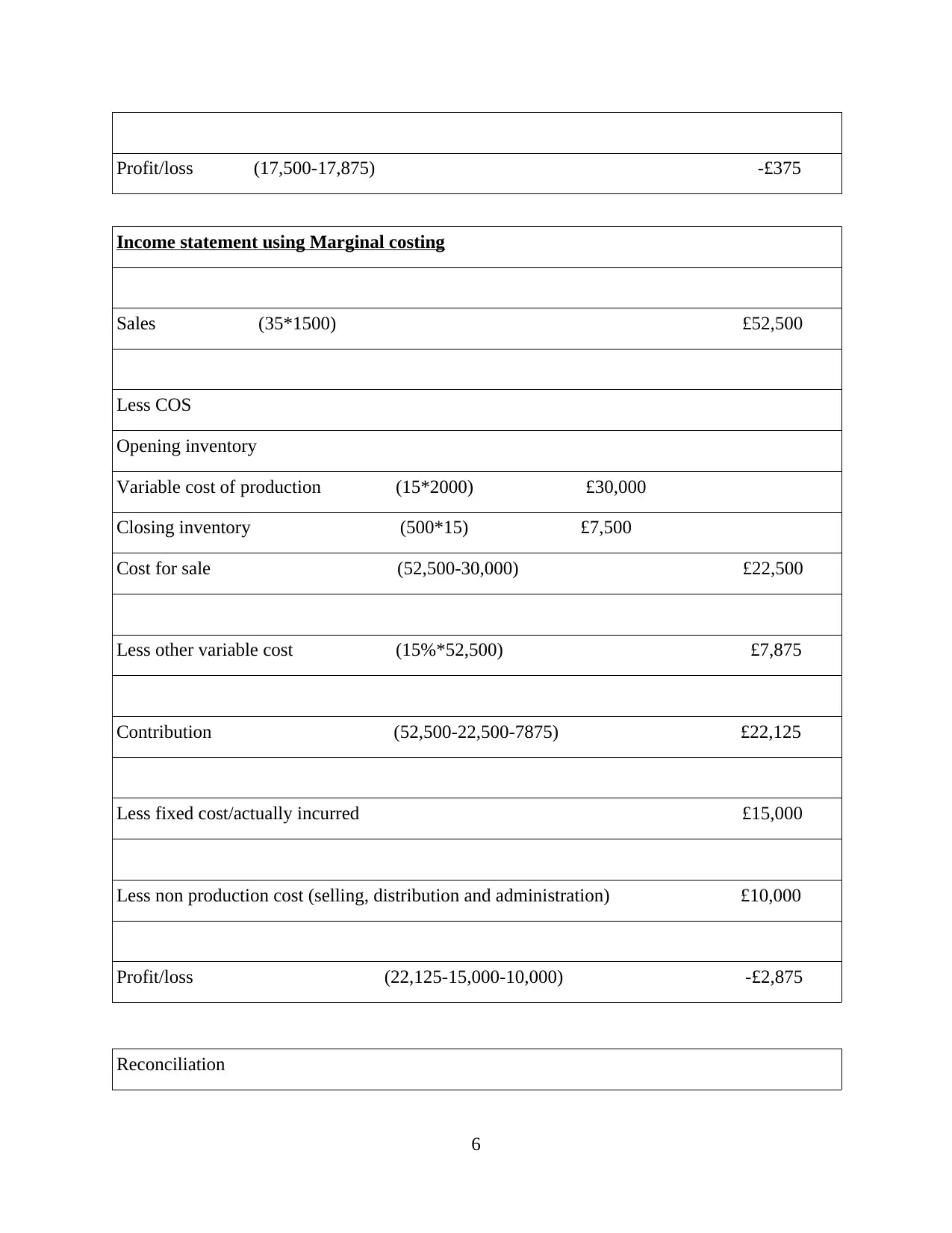

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

6

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

6

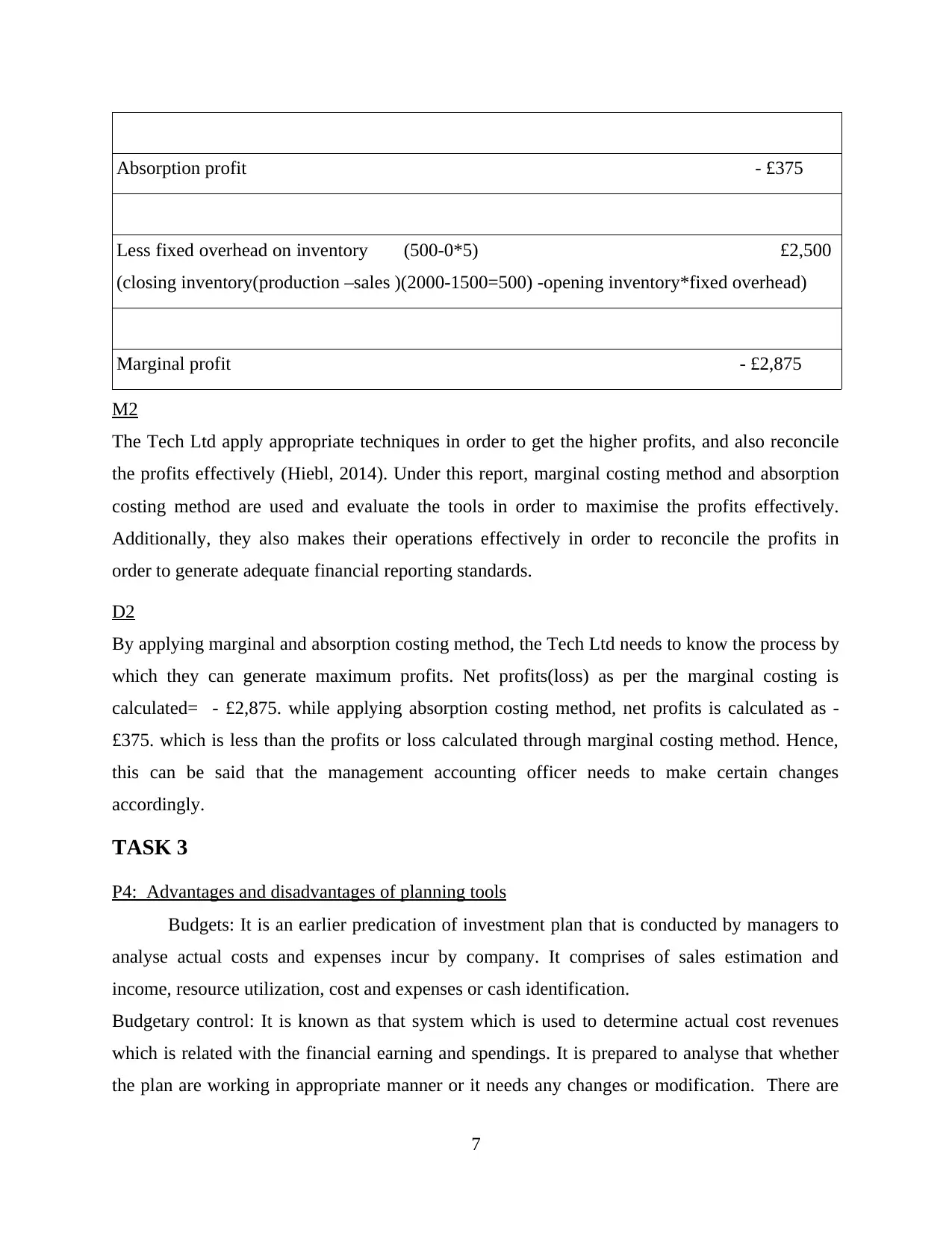

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales )(2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

M2

The Tech Ltd apply appropriate techniques in order to get the higher profits, and also reconcile

the profits effectively (Hiebl, 2014). Under this report, marginal costing method and absorption

costing method are used and evaluate the tools in order to maximise the profits effectively.

Additionally, they also makes their operations effectively in order to reconcile the profits in

order to generate adequate financial reporting standards.

D2

By applying marginal and absorption costing method, the Tech Ltd needs to know the process by

which they can generate maximum profits. Net profits(loss) as per the marginal costing is

calculated= - £2,875. while applying absorption costing method, net profits is calculated as -

£375. which is less than the profits or loss calculated through marginal costing method. Hence,

this can be said that the management accounting officer needs to make certain changes

accordingly.

TASK 3

P4: Advantages and disadvantages of planning tools

Budgets: It is an earlier predication of investment plan that is conducted by managers to

analyse actual costs and expenses incur by company. It comprises of sales estimation and

income, resource utilization, cost and expenses or cash identification.

Budgetary control: It is known as that system which is used to determine actual cost revenues

which is related with the financial earning and spendings. It is prepared to analyse that whether

the plan are working in appropriate manner or it needs any changes or modification. There are

7

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales )(2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

M2

The Tech Ltd apply appropriate techniques in order to get the higher profits, and also reconcile

the profits effectively (Hiebl, 2014). Under this report, marginal costing method and absorption

costing method are used and evaluate the tools in order to maximise the profits effectively.

Additionally, they also makes their operations effectively in order to reconcile the profits in

order to generate adequate financial reporting standards.

D2

By applying marginal and absorption costing method, the Tech Ltd needs to know the process by

which they can generate maximum profits. Net profits(loss) as per the marginal costing is

calculated= - £2,875. while applying absorption costing method, net profits is calculated as -

£375. which is less than the profits or loss calculated through marginal costing method. Hence,

this can be said that the management accounting officer needs to make certain changes

accordingly.

TASK 3

P4: Advantages and disadvantages of planning tools

Budgets: It is an earlier predication of investment plan that is conducted by managers to

analyse actual costs and expenses incur by company. It comprises of sales estimation and

income, resource utilization, cost and expenses or cash identification.

Budgetary control: It is known as that system which is used to determine actual cost revenues

which is related with the financial earning and spendings. It is prepared to analyse that whether

the plan are working in appropriate manner or it needs any changes or modification. There are

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

various precess by which budgets can be controlled (Grabner and Moers, 2013). Some of them

are as followed:

Consult with the managers: The requirement of budgets is prior need perfect consultation

from every department. It will help them to manage and control there costs and extra

expenses. If there is need of any budget it will be directly transfer to higher authorities for

further approvals.

Make assumption and declaration: It is very true that budget are always made on an

assumption basis. Because it is very difficult to analyse total revenue and sale incur by

company during the next few year.

Fixed information about budgets to achieve future goals: Under this stages, a specific lists

of budgets are prepared by taking guidance from superior persons. It can be operational,

cash other other budgets that are included in it.

Measuring actual performance with other budgets.

Review stage.

8

are as followed:

Consult with the managers: The requirement of budgets is prior need perfect consultation

from every department. It will help them to manage and control there costs and extra

expenses. If there is need of any budget it will be directly transfer to higher authorities for

further approvals.

Make assumption and declaration: It is very true that budget are always made on an

assumption basis. Because it is very difficult to analyse total revenue and sale incur by

company during the next few year.

Fixed information about budgets to achieve future goals: Under this stages, a specific lists

of budgets are prepared by taking guidance from superior persons. It can be operational,

cash other other budgets that are included in it.

Measuring actual performance with other budgets.

Review stage.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Planning tools: These tools includes the use of various budgets information to measure the

performance of company.

Operating budget: This budget includes the information related to the cost and and

expenses incurred during particular period of time. It has to be said that it includes the data

related to the operation of business activities (The Advantages and Disadvantages of Budgeting,

2017).

Advantages: The main advantage of this budget is that it is prepared by company in

advance.

Disadvantage: The preparation of this budget is costly because it is difficult to estimate

the budget in advance without any proper information.

Cash budgets: This budgets helps in determination of inflow and outflow of cash in one

accounting year. The preparation of cash budget includes the involvement of three activities

which are: operating, investing and financing.

Advantages: It provides the information related to cash to company.

Disadvantage: One of the disadvantage is that the present cash flow is ignored, when the

recovery time of cash is completed (Davies and Crawford, 2011).

Static budget: It is prepared at very first stage. It is prepared by the company at the time

of designing of the activities. All the data included in the budget are on the basis of the facts

which is different from actual outcomes.

Advantages: Information cannot be changed because it is based on assumption.

Disadvantage: It is not much effective because it includes only few information.

M3.

There are so many planning tools that are used by the firm in order to get the desired results. For

this, diverse aim of the planning tools are considered like- operating budget, cash and master

budgets. These all are used by the company in order to have the various plans. There are so many

tools that can be used by the Tech Ltd in order to make sustainability.

D3.

For aiming the performance analysis, various factors are required to analyse that affects

the performance of the firm. This is connected with the management for doing their routine

work. Which ultimately affects their routine work. This is connected to the management of their

9

performance of company.

Operating budget: This budget includes the information related to the cost and and

expenses incurred during particular period of time. It has to be said that it includes the data

related to the operation of business activities (The Advantages and Disadvantages of Budgeting,

2017).

Advantages: The main advantage of this budget is that it is prepared by company in

advance.

Disadvantage: The preparation of this budget is costly because it is difficult to estimate

the budget in advance without any proper information.

Cash budgets: This budgets helps in determination of inflow and outflow of cash in one

accounting year. The preparation of cash budget includes the involvement of three activities

which are: operating, investing and financing.

Advantages: It provides the information related to cash to company.

Disadvantage: One of the disadvantage is that the present cash flow is ignored, when the

recovery time of cash is completed (Davies and Crawford, 2011).

Static budget: It is prepared at very first stage. It is prepared by the company at the time

of designing of the activities. All the data included in the budget are on the basis of the facts

which is different from actual outcomes.

Advantages: Information cannot be changed because it is based on assumption.

Disadvantage: It is not much effective because it includes only few information.

M3.

There are so many planning tools that are used by the firm in order to get the desired results. For

this, diverse aim of the planning tools are considered like- operating budget, cash and master

budgets. These all are used by the company in order to have the various plans. There are so many

tools that can be used by the Tech Ltd in order to make sustainability.

D3.

For aiming the performance analysis, various factors are required to analyse that affects

the performance of the firm. This is connected with the management for doing their routine

work. Which ultimately affects their routine work. This is connected to the management of their

9

day to day routine work. Such could be assisted by the financial and non-financial factors. This is

the main accountability of the mangers to assess such finance related problems or issues in such

a way by which firm's profits can not be affected. But, for resolving these issues, firm can use

balance score card approach.

TASK 4

P5. Balance score card approach:

In any company, this is mandatory to implement those tools that helps for solving finance related

problems effectively (Caglio and Ditillo, 2012). Earlier, there were no techniques that could be

used in order to solve the financial problems effectively. Balance score card is the main tool that

permits the managers to oversee the business performance and also support the firm to improve

their performance. BSC connects with the performance measures and this can be used as:

How do consumers view the firm? (Consumer perspective)

What must be excel at? (Internal Perspective) ?

Could managers regularly to enhance and incorporate values? (Innovation and learning

perspectives)

How do we express to shareholders? (Financial perspective)

by providing senior manager information from above mentioned four diverse perspectives, the

balance score card limit the information overload by reducing the number of uses. Various firms'

have already uses scorecard approach (Cadez and Guilding, 2012). Their early experience

implementing the score card reflected that it satiate various managerial needs.

Customer Perspective: In this competitive world, everyone is focusing on the

customers. To be the leader in the market, company would need to focus on the

customers and tries to satiate their demand effectively. So that they could think about

their customers and provides them service into particular measures which show the

factors which concerned to the customers. However, customer concerns are categories

into four categories: these are time, quality, performance, and the last one is cost.

Internal business perspective: Customer based measures are essential, but they are

required to translate into the measures of what the firm are required to do internally so

that the customer expectations can be achieved. Tech Ltd needs to concentrates on the

internal operations which helps to assist the firm to satisfy their customers needs.

10

the main accountability of the mangers to assess such finance related problems or issues in such

a way by which firm's profits can not be affected. But, for resolving these issues, firm can use

balance score card approach.

TASK 4

P5. Balance score card approach:

In any company, this is mandatory to implement those tools that helps for solving finance related

problems effectively (Caglio and Ditillo, 2012). Earlier, there were no techniques that could be

used in order to solve the financial problems effectively. Balance score card is the main tool that

permits the managers to oversee the business performance and also support the firm to improve

their performance. BSC connects with the performance measures and this can be used as:

How do consumers view the firm? (Consumer perspective)

What must be excel at? (Internal Perspective) ?

Could managers regularly to enhance and incorporate values? (Innovation and learning

perspectives)

How do we express to shareholders? (Financial perspective)

by providing senior manager information from above mentioned four diverse perspectives, the

balance score card limit the information overload by reducing the number of uses. Various firms'

have already uses scorecard approach (Cadez and Guilding, 2012). Their early experience

implementing the score card reflected that it satiate various managerial needs.

Customer Perspective: In this competitive world, everyone is focusing on the

customers. To be the leader in the market, company would need to focus on the

customers and tries to satiate their demand effectively. So that they could think about

their customers and provides them service into particular measures which show the

factors which concerned to the customers. However, customer concerns are categories

into four categories: these are time, quality, performance, and the last one is cost.

Internal business perspective: Customer based measures are essential, but they are

required to translate into the measures of what the firm are required to do internally so

that the customer expectations can be achieved. Tech Ltd needs to concentrates on the

internal operations which helps to assist the firm to satisfy their customers needs.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.