Management Accounting Report: Systems, Reports, and Techniques

VerifiedAdded on 2023/01/12

|11

|638

|66

Report

AI Summary

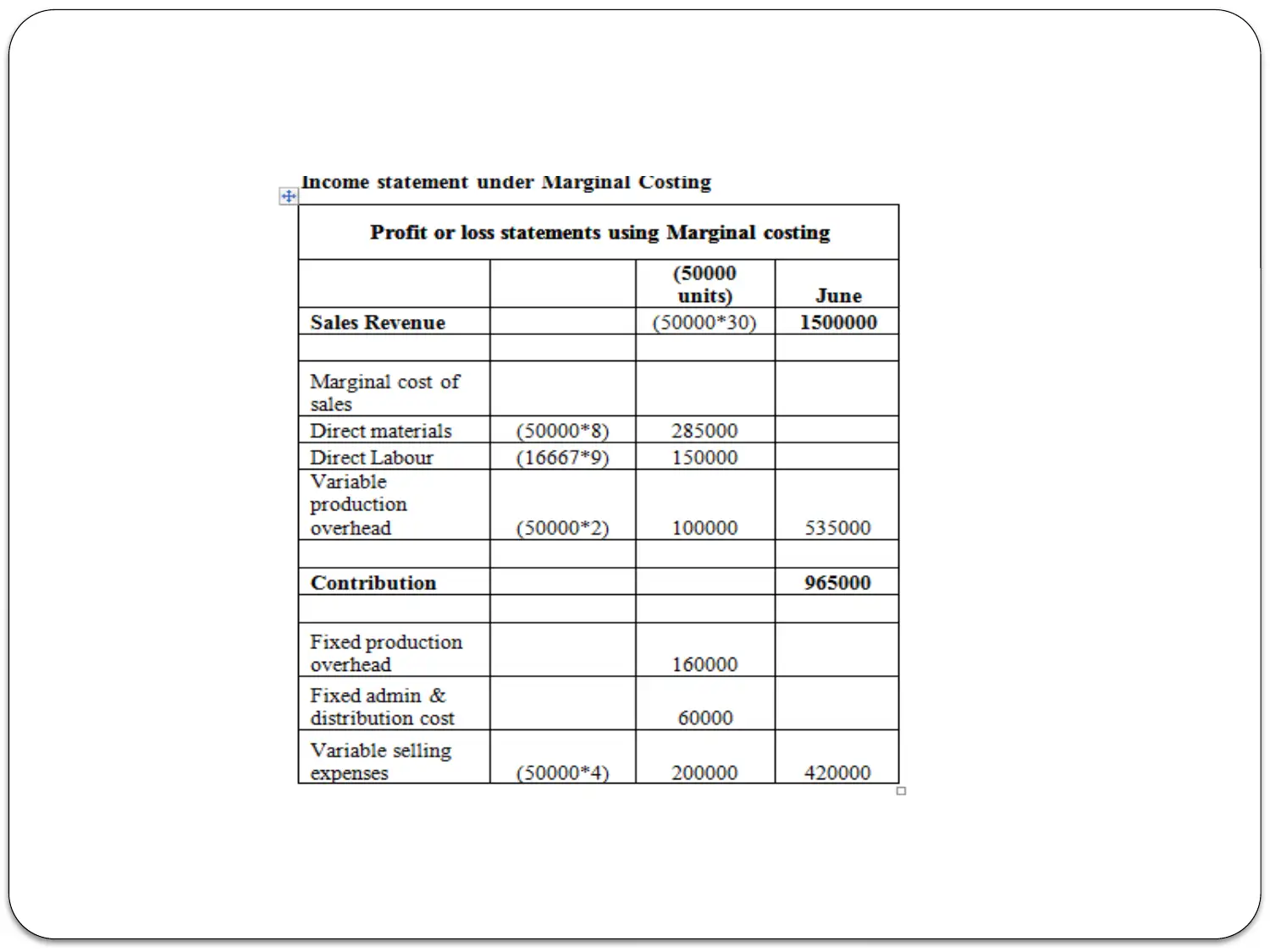

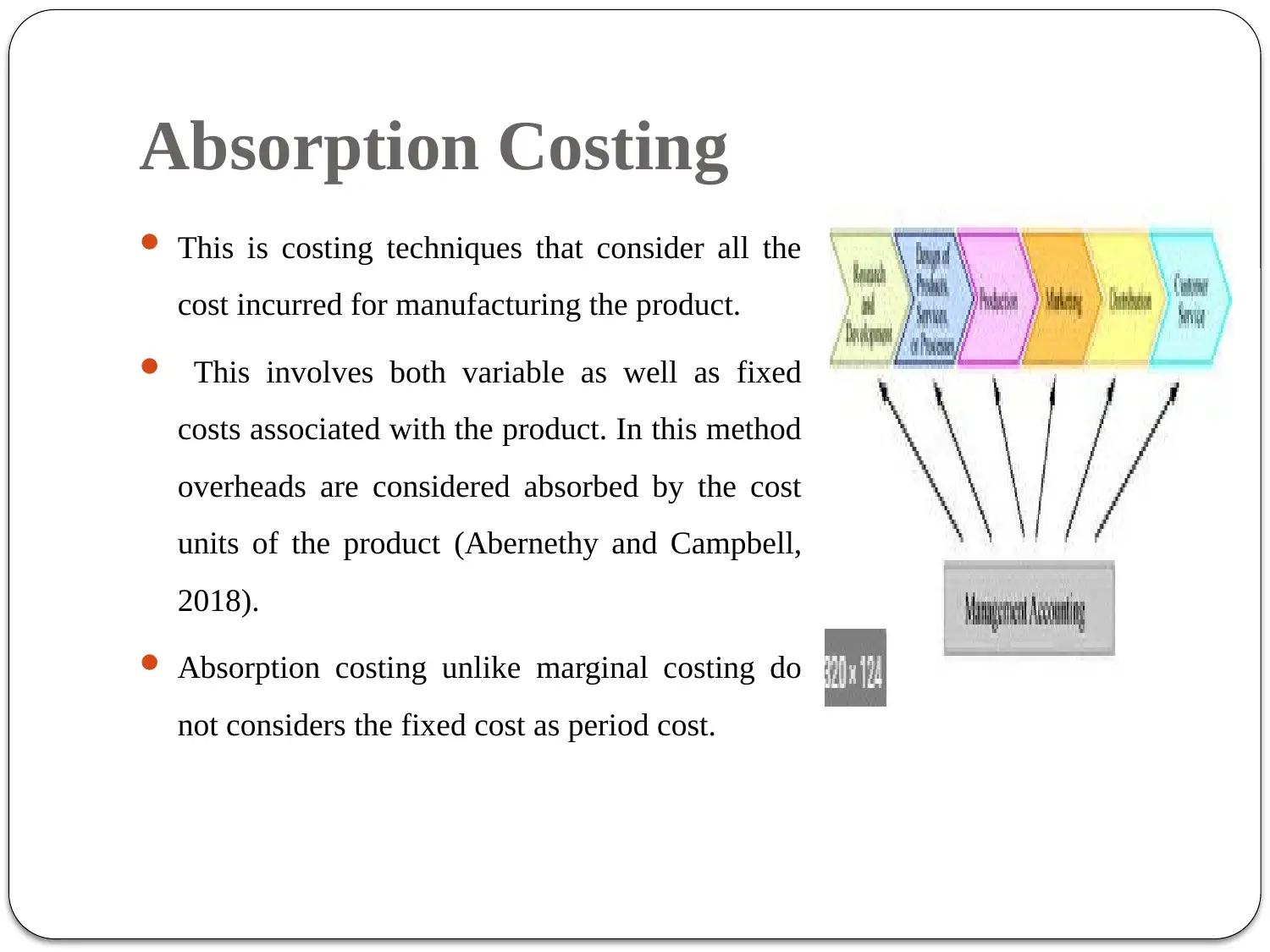

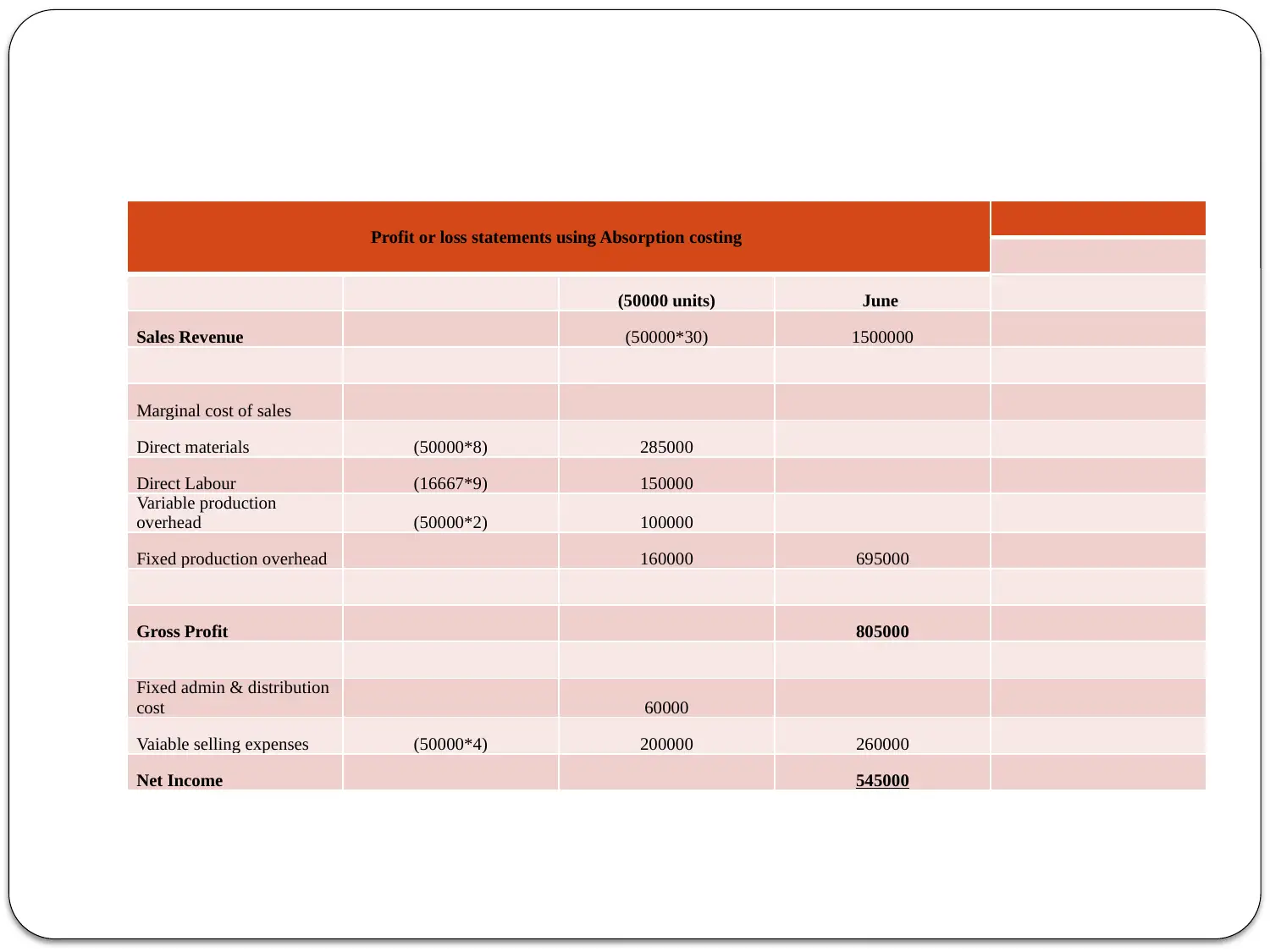

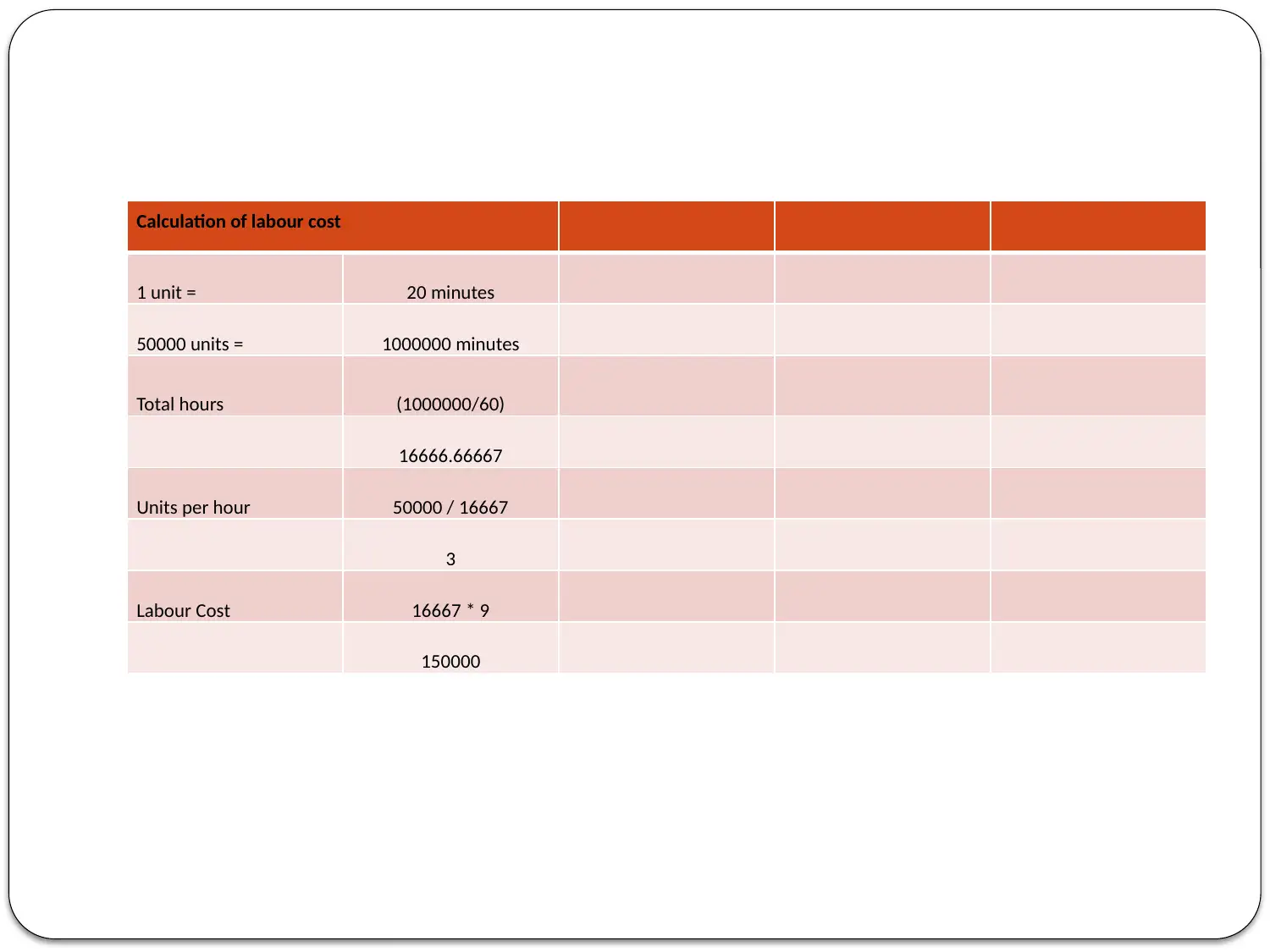

This report provides an overview of management accounting, focusing on its role in decision-making within organizations. It defines management accounting as the process of gathering, analyzing, and interpreting financial information for internal use. The report uses GSQ Limited as a case study, covering management accounting systems, reports, and costing techniques. It explains marginal and absorption costing methods, including their application in profit or loss statements. The report includes calculations for labor costs and concludes by highlighting the importance of management accounting systems and reports in strategic and operational decision-making. It emphasizes the role of cost accounting techniques in profit analysis and planning tools for cost control. References to relevant academic sources are also included.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.