Management Accounting Report Analysis for Tech(UK) Ltd. (Semester 1)

VerifiedAdded on 2020/10/05

|18

|5370

|87

Report

AI Summary

This report delves into the core concepts of management accounting, differentiating it from financial accounting and highlighting its importance in organizational decision-making. It explores various management accounting systems, including cost accounting and inventory management, and examines different types of managerial reports, such as accounts receivable and budgeting reports, emphasizing their significance in enhancing financial returns and reducing losses. The report further applies absorption and marginal costing methods for income statement preparation, outlining the merits and demerits of different budgeting techniques. It also addresses the use of planning tools, financial issue analysis, and the application of management accounting principles to resolve financial problems. The analysis is contextualized within the framework of Tech(UK) Ltd., providing practical insights into real-world applications of management accounting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting and its essential requirement.......................................1

P2 Different types of managerial reports and its importance......................................................4

M1...............................................................................................................................................5

D1................................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................6

M2...............................................................................................................................................8

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of using various types of budgets and their significant.......................9

M3: Evaluation of planning tools..............................................................................................12

D3: Critical analysis of financial issues....................................................................................12

TASK 4..........................................................................................................................................12

P5: Balance scorecard approach................................................................................................12

M4: Analysis of financial issues arises in an organisation.......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting and its essential requirement.......................................1

P2 Different types of managerial reports and its importance......................................................4

M1...............................................................................................................................................5

D1................................................................................................................................................5

TASK 2............................................................................................................................................6

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................6

M2...............................................................................................................................................8

D2................................................................................................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of using various types of budgets and their significant.......................9

M3: Evaluation of planning tools..............................................................................................12

D3: Critical analysis of financial issues....................................................................................12

TASK 4..........................................................................................................................................12

P5: Balance scorecard approach................................................................................................12

M4: Analysis of financial issues arises in an organisation.......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Every kind of organisation whether small or large in nature required to record their

transactions to analyse the current performance of their employees. This will provides the

opportunity in development of new strategies which directs the employees for accomplishment

of desired objectives. Management accounting is important concept which helps in formulation

of different kind of accounts and reports for improvement of understanding between the different

departments. It refers to the process of measuring, analysing, interpreting and communication of

information in achievement of organisational goals. Such different kind of reports provides

financial and statistical information which enhance decision making power of management for

operation of day to day functions (Arroyo, 2012). It assists the manager of organisation in

planning, organising, monitoring and controlling. Tech(UK) Ltd. Producing special charger for

mobile telephone and other gadgets for retail outlets in UK.

In the present report explain about, concept of management accounting, distinguish

between management and financial accounting, importance ascertained by manager from

management accounting information as decision making tool, different types of management

accounting systems, various kind of managerial accounting reports and their importance and

application of the costing techniques like marginal and absorption for the purpose of preparation

of income statement. Also, define about different kind of budgets and its advantages and

disadvantages, budget preparation process along with different pricing and costing system,

importance of such budgets to manager and application of the principles of management

accounting to respond financial problems.

TASK 1

P1 Concept of management accounting and its essential requirement

Difference between management and financial accounting

Management Accounting Financial Accounting

Broad concept contains the provisions of

managerial and cost accounting

Narrow concept in comparison to

management accounting and only includes the

provisions which helps in preparation of

financial statements

The different kind of accounts and reports are These accounts are used by the external

1

Every kind of organisation whether small or large in nature required to record their

transactions to analyse the current performance of their employees. This will provides the

opportunity in development of new strategies which directs the employees for accomplishment

of desired objectives. Management accounting is important concept which helps in formulation

of different kind of accounts and reports for improvement of understanding between the different

departments. It refers to the process of measuring, analysing, interpreting and communication of

information in achievement of organisational goals. Such different kind of reports provides

financial and statistical information which enhance decision making power of management for

operation of day to day functions (Arroyo, 2012). It assists the manager of organisation in

planning, organising, monitoring and controlling. Tech(UK) Ltd. Producing special charger for

mobile telephone and other gadgets for retail outlets in UK.

In the present report explain about, concept of management accounting, distinguish

between management and financial accounting, importance ascertained by manager from

management accounting information as decision making tool, different types of management

accounting systems, various kind of managerial accounting reports and their importance and

application of the costing techniques like marginal and absorption for the purpose of preparation

of income statement. Also, define about different kind of budgets and its advantages and

disadvantages, budget preparation process along with different pricing and costing system,

importance of such budgets to manager and application of the principles of management

accounting to respond financial problems.

TASK 1

P1 Concept of management accounting and its essential requirement

Difference between management and financial accounting

Management Accounting Financial Accounting

Broad concept contains the provisions of

managerial and cost accounting

Narrow concept in comparison to

management accounting and only includes the

provisions which helps in preparation of

financial statements

The different kind of accounts and reports are These accounts are used by the external

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

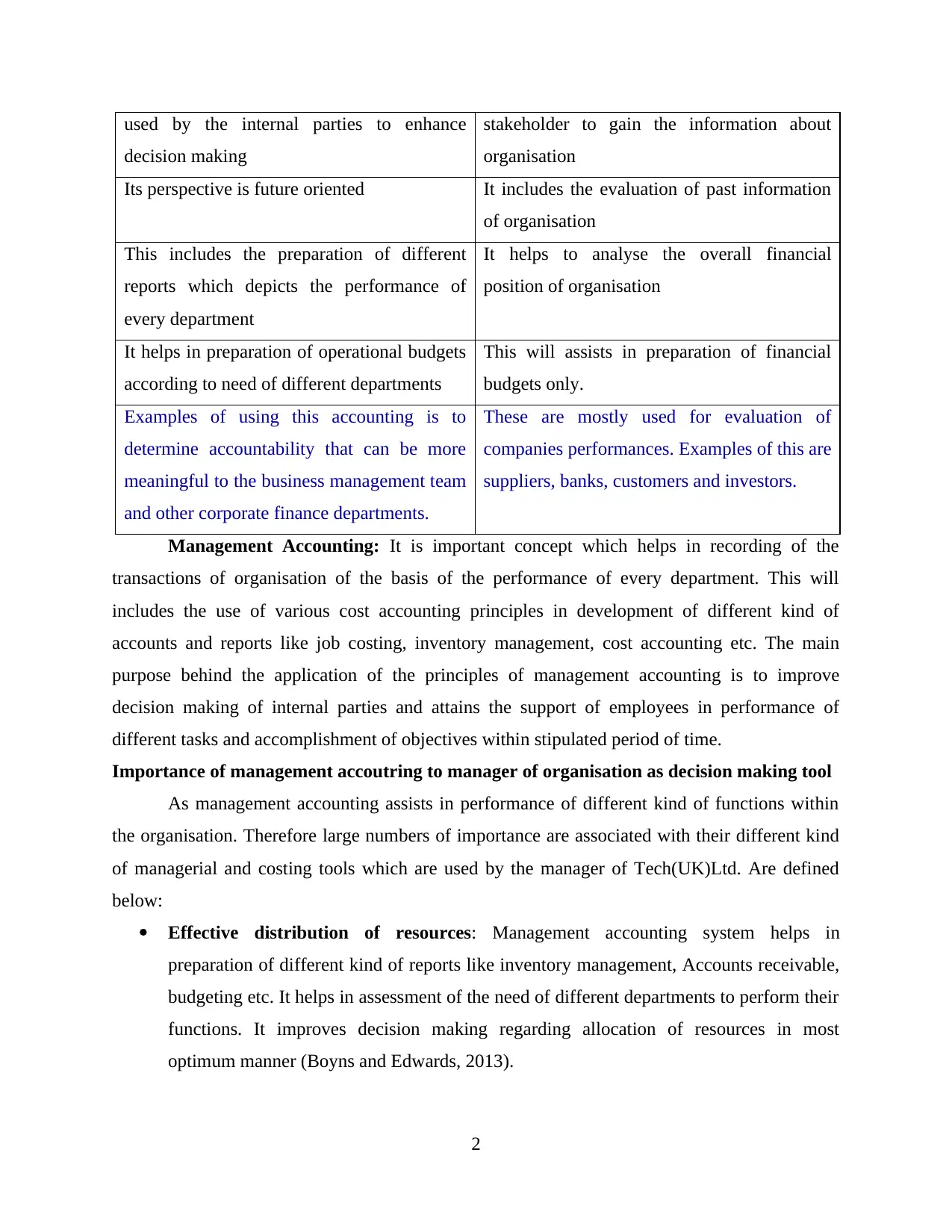

used by the internal parties to enhance

decision making

stakeholder to gain the information about

organisation

Its perspective is future oriented It includes the evaluation of past information

of organisation

This includes the preparation of different

reports which depicts the performance of

every department

It helps to analyse the overall financial

position of organisation

It helps in preparation of operational budgets

according to need of different departments

This will assists in preparation of financial

budgets only.

Examples of using this accounting is to

determine accountability that can be more

meaningful to the business management team

and other corporate finance departments.

These are mostly used for evaluation of

companies performances. Examples of this are

suppliers, banks, customers and investors.

Management Accounting: It is important concept which helps in recording of the

transactions of organisation of the basis of the performance of every department. This will

includes the use of various cost accounting principles in development of different kind of

accounts and reports like job costing, inventory management, cost accounting etc. The main

purpose behind the application of the principles of management accounting is to improve

decision making of internal parties and attains the support of employees in performance of

different tasks and accomplishment of objectives within stipulated period of time.

Importance of management accoutring to manager of organisation as decision making tool

As management accounting assists in performance of different kind of functions within

the organisation. Therefore large numbers of importance are associated with their different kind

of managerial and costing tools which are used by the manager of Tech(UK)Ltd. Are defined

below:

Effective distribution of resources: Management accounting system helps in

preparation of different kind of reports like inventory management, Accounts receivable,

budgeting etc. It helps in assessment of the need of different departments to perform their

functions. It improves decision making regarding allocation of resources in most

optimum manner (Boyns and Edwards, 2013).

2

decision making

stakeholder to gain the information about

organisation

Its perspective is future oriented It includes the evaluation of past information

of organisation

This includes the preparation of different

reports which depicts the performance of

every department

It helps to analyse the overall financial

position of organisation

It helps in preparation of operational budgets

according to need of different departments

This will assists in preparation of financial

budgets only.

Examples of using this accounting is to

determine accountability that can be more

meaningful to the business management team

and other corporate finance departments.

These are mostly used for evaluation of

companies performances. Examples of this are

suppliers, banks, customers and investors.

Management Accounting: It is important concept which helps in recording of the

transactions of organisation of the basis of the performance of every department. This will

includes the use of various cost accounting principles in development of different kind of

accounts and reports like job costing, inventory management, cost accounting etc. The main

purpose behind the application of the principles of management accounting is to improve

decision making of internal parties and attains the support of employees in performance of

different tasks and accomplishment of objectives within stipulated period of time.

Importance of management accoutring to manager of organisation as decision making tool

As management accounting assists in performance of different kind of functions within

the organisation. Therefore large numbers of importance are associated with their different kind

of managerial and costing tools which are used by the manager of Tech(UK)Ltd. Are defined

below:

Effective distribution of resources: Management accounting system helps in

preparation of different kind of reports like inventory management, Accounts receivable,

budgeting etc. It helps in assessment of the need of different departments to perform their

functions. It improves decision making regarding allocation of resources in most

optimum manner (Boyns and Edwards, 2013).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment of risk: The main perspective behind the application of the management

accounting principles within the organisation is formulation of future strategies on the

basis of the evaluation of their past performance. It improves the insight of manager to

effectively identify the risks and make solutions for its removal.

Appraisal of the actual performance: Formulation of different kind of reports

according to the performance of various departments helps in preparation of budgets

which contains the standards which are need to adhere by the employees in performance

of their functions. One the basis of the deviations which are arise in actual results

performance of employees are measures and effective actions are taken to overcome from

such issues and attains their standards.

Presentation of financial position: There are many accounts which provide the

opportunity to understand about the financial performance and position of organisation in

market. This will contributes in improvement of their brand image which has direct

impact upon their profit earning capacity (Herzig and et. al. 2012).

Various kind management accounting systems

The three different kind of accounting systems are adopted in Tech(UK)Ltd. All these

systems have their different roles and importance o for organisation. This can be understood

from the points which describe their provisions and roles mentioned below:

Cost accounting system: It is important of organisation to estimate their costs in future

for ascertaining the information regarding their profitability, inventory cost and controlling of

expenses. It assists the manager of organisation as per such approaches which help in

maximisation of their profits. It includes the process of costing of product in different styles

defined below:

Actual costing: Here all the ingredients which are used in production process at actual

cost.

Standard costing: This will provide the targeted cost which is needed to achieve.

Normal costing: Here the costs are assorted on the basis of predetermined manufacturing

overhead rate.

Examples: it is more appropriate for an activities management companies, a niche

furniture producers of manufacture of very high cost air surveillances system. Coffee roaster

which after retaining at wider order of material.

3

accounting principles within the organisation is formulation of future strategies on the

basis of the evaluation of their past performance. It improves the insight of manager to

effectively identify the risks and make solutions for its removal.

Appraisal of the actual performance: Formulation of different kind of reports

according to the performance of various departments helps in preparation of budgets

which contains the standards which are need to adhere by the employees in performance

of their functions. One the basis of the deviations which are arise in actual results

performance of employees are measures and effective actions are taken to overcome from

such issues and attains their standards.

Presentation of financial position: There are many accounts which provide the

opportunity to understand about the financial performance and position of organisation in

market. This will contributes in improvement of their brand image which has direct

impact upon their profit earning capacity (Herzig and et. al. 2012).

Various kind management accounting systems

The three different kind of accounting systems are adopted in Tech(UK)Ltd. All these

systems have their different roles and importance o for organisation. This can be understood

from the points which describe their provisions and roles mentioned below:

Cost accounting system: It is important of organisation to estimate their costs in future

for ascertaining the information regarding their profitability, inventory cost and controlling of

expenses. It assists the manager of organisation as per such approaches which help in

maximisation of their profits. It includes the process of costing of product in different styles

defined below:

Actual costing: Here all the ingredients which are used in production process at actual

cost.

Standard costing: This will provide the targeted cost which is needed to achieve.

Normal costing: Here the costs are assorted on the basis of predetermined manufacturing

overhead rate.

Examples: it is more appropriate for an activities management companies, a niche

furniture producers of manufacture of very high cost air surveillances system. Coffee roaster

which after retaining at wider order of material.

3

Job costing: One of the important system need to implement all manufacturing units to

track the expenses. This will be useful in providence of cost to each individual product which is

manufactured by organisation. So, the provisions of this system are more important for

organisation which produces multi products. The costs are charges upon two different aspects

which are named as direct material and fixed and variable overheads.

Example: It must track cost of material that are mainly helpful for Scrapped during the

course of job. It is mostly useful for construction companies.

Inventory management system: The main role of this system is that it helps to organise

the assets and stock of organisation in effective manner. As it provides opportunity to attain

maximum results for utilisation of their resources at full capacity. The different kind of tools

which provides their supporting in such management work is defined below:

FIFO: Here inventories are record as they used in organisation. It helps in valuation of

closing stock.

LIFO: Here, such inventory is recognised which is oldest in organisation whether used

later.

AVCO: It provides the opportunity regarding ascertaining the average cost to take better

decisions.

Examples: Raw material such as wood to make various products. Unfinished cake in a

product producing business. Tangible items that a business holds and ultimately available for

sales.

P2 Different types of managerial reports and its importance

Different management accounting reports

There are different kind of reports prepared by the management of Tech(UK)Ltd. To

interpret the results and performance of their different departments(Otley and Emmanuel, 2013).

The main purpose of these supports improves the coordination and communication which helps

bring understanding among employees. The function of such different report is defined below:

Accounts Receivable report: The main function of this report is to provide the

information regarding outstanding amounts from their debtors along with their time

period. It is the duty of the management is to segmentation of invoices on the basis of

time period they are unpaid. It helps to assess the effectiveness of their exist credit

4

track the expenses. This will be useful in providence of cost to each individual product which is

manufactured by organisation. So, the provisions of this system are more important for

organisation which produces multi products. The costs are charges upon two different aspects

which are named as direct material and fixed and variable overheads.

Example: It must track cost of material that are mainly helpful for Scrapped during the

course of job. It is mostly useful for construction companies.

Inventory management system: The main role of this system is that it helps to organise

the assets and stock of organisation in effective manner. As it provides opportunity to attain

maximum results for utilisation of their resources at full capacity. The different kind of tools

which provides their supporting in such management work is defined below:

FIFO: Here inventories are record as they used in organisation. It helps in valuation of

closing stock.

LIFO: Here, such inventory is recognised which is oldest in organisation whether used

later.

AVCO: It provides the opportunity regarding ascertaining the average cost to take better

decisions.

Examples: Raw material such as wood to make various products. Unfinished cake in a

product producing business. Tangible items that a business holds and ultimately available for

sales.

P2 Different types of managerial reports and its importance

Different management accounting reports

There are different kind of reports prepared by the management of Tech(UK)Ltd. To

interpret the results and performance of their different departments(Otley and Emmanuel, 2013).

The main purpose of these supports improves the coordination and communication which helps

bring understanding among employees. The function of such different report is defined below:

Accounts Receivable report: The main function of this report is to provide the

information regarding outstanding amounts from their debtors along with their time

period. It is the duty of the management is to segmentation of invoices on the basis of

time period they are unpaid. It helps to assess the effectiveness of their exist credit

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

policies and if there is need to tighten their policies then bring changes according to

requirements. It helps to recover their outstanding amounts.

Budgeting reports: One of the effective report which is used regarding appraisal of

performance of departments in comparison to standards which are set while preparing

such budgets. It provides the opportunity regarding determination of issues and

application of innovative technique which to improve their performances. It also helps in

designing of incentive reports according to such appraisal of performance.

Job cost report: This report is used to assess the profits which are going to earn in future

after deduction of estimated cost and expenses. This will provides the information

regarding which part of project which consist higher amount of profits. So, it helps to

frame the strategies according to that and provide more efforts to such activities.

Importance of management accounting reports

Increased financial returns: Budgeting report provides direction through providence of

standards to employees that accomplish their targets and earn large number of income.

This will prove as motivating factor which improves their passion towards their work.

Reduction in loss: Analysis of the past information on the basis of such reports helps to

identify the mistakes and provides opportunity to reduce their future risks through

application of appropriate solution (Parker, 2012).

M1

Benefits of management accounting systems:

Cost accounting system

To ascertain the amount of profitability

Helps in reduction in amount of expenses

Makes better future plans

Measurement of the efficiency of actual processes

Job costing system

It helps to track their expenses

Helps in reduction in the amount of repetition of work

D1

Type of reporting Integration with organisational process

5

requirements. It helps to recover their outstanding amounts.

Budgeting reports: One of the effective report which is used regarding appraisal of

performance of departments in comparison to standards which are set while preparing

such budgets. It provides the opportunity regarding determination of issues and

application of innovative technique which to improve their performances. It also helps in

designing of incentive reports according to such appraisal of performance.

Job cost report: This report is used to assess the profits which are going to earn in future

after deduction of estimated cost and expenses. This will provides the information

regarding which part of project which consist higher amount of profits. So, it helps to

frame the strategies according to that and provide more efforts to such activities.

Importance of management accounting reports

Increased financial returns: Budgeting report provides direction through providence of

standards to employees that accomplish their targets and earn large number of income.

This will prove as motivating factor which improves their passion towards their work.

Reduction in loss: Analysis of the past information on the basis of such reports helps to

identify the mistakes and provides opportunity to reduce their future risks through

application of appropriate solution (Parker, 2012).

M1

Benefits of management accounting systems:

Cost accounting system

To ascertain the amount of profitability

Helps in reduction in amount of expenses

Makes better future plans

Measurement of the efficiency of actual processes

Job costing system

It helps to track their expenses

Helps in reduction in the amount of repetition of work

D1

Type of reporting Integration with organisational process

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivable report It helps in collection of their outstanding

amounts from debtors and maintenance of

liquidity

Job cost report Provides opportunity in identification of most

profitable projects and reduction of cost to

reduction in amount of efforts from such

wasteful processes

TASK 2

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It is the amount which is paid by organisation in manufacturing of the product. There

are many which also takes the part of total cost of products which includes material, labour,

opportunity foregone, risk and time.

Marginal costing: This method of costing considered only variable cost. It helps in

assessing the change in cost if there is change in production of units.

Absorption costing: It contributes to build effective long term decisions. This method

includes both fixed and variable costs (Vasile and Man, 2012).

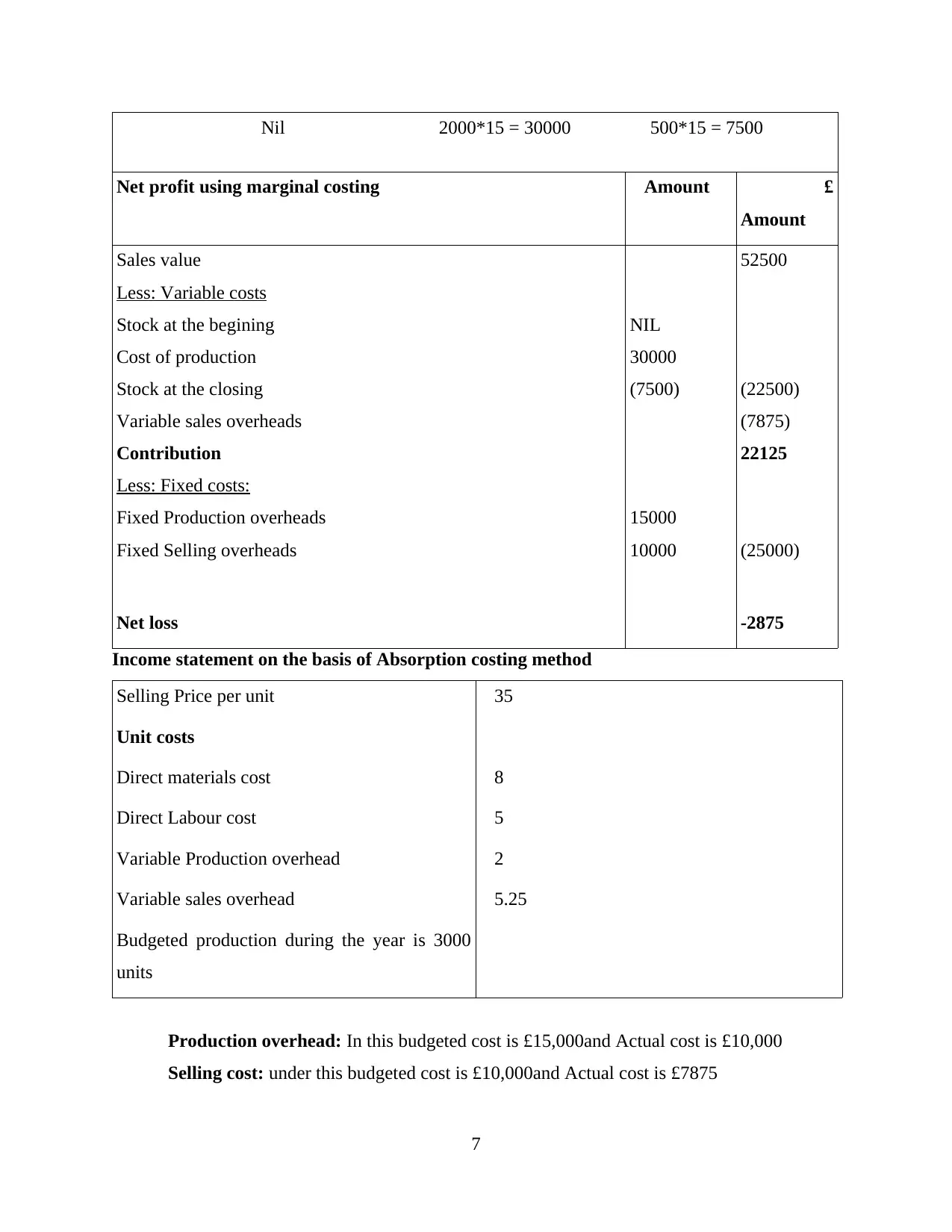

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

6

amounts from debtors and maintenance of

liquidity

Job cost report Provides opportunity in identification of most

profitable projects and reduction of cost to

reduction in amount of efforts from such

wasteful processes

TASK 2

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It is the amount which is paid by organisation in manufacturing of the product. There

are many which also takes the part of total cost of products which includes material, labour,

opportunity foregone, risk and time.

Marginal costing: This method of costing considered only variable cost. It helps in

assessing the change in cost if there is change in production of units.

Absorption costing: It contributes to build effective long term decisions. This method

includes both fixed and variable costs (Vasile and Man, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

6

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £

Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

7

Net profit using marginal costing £Amount £

Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

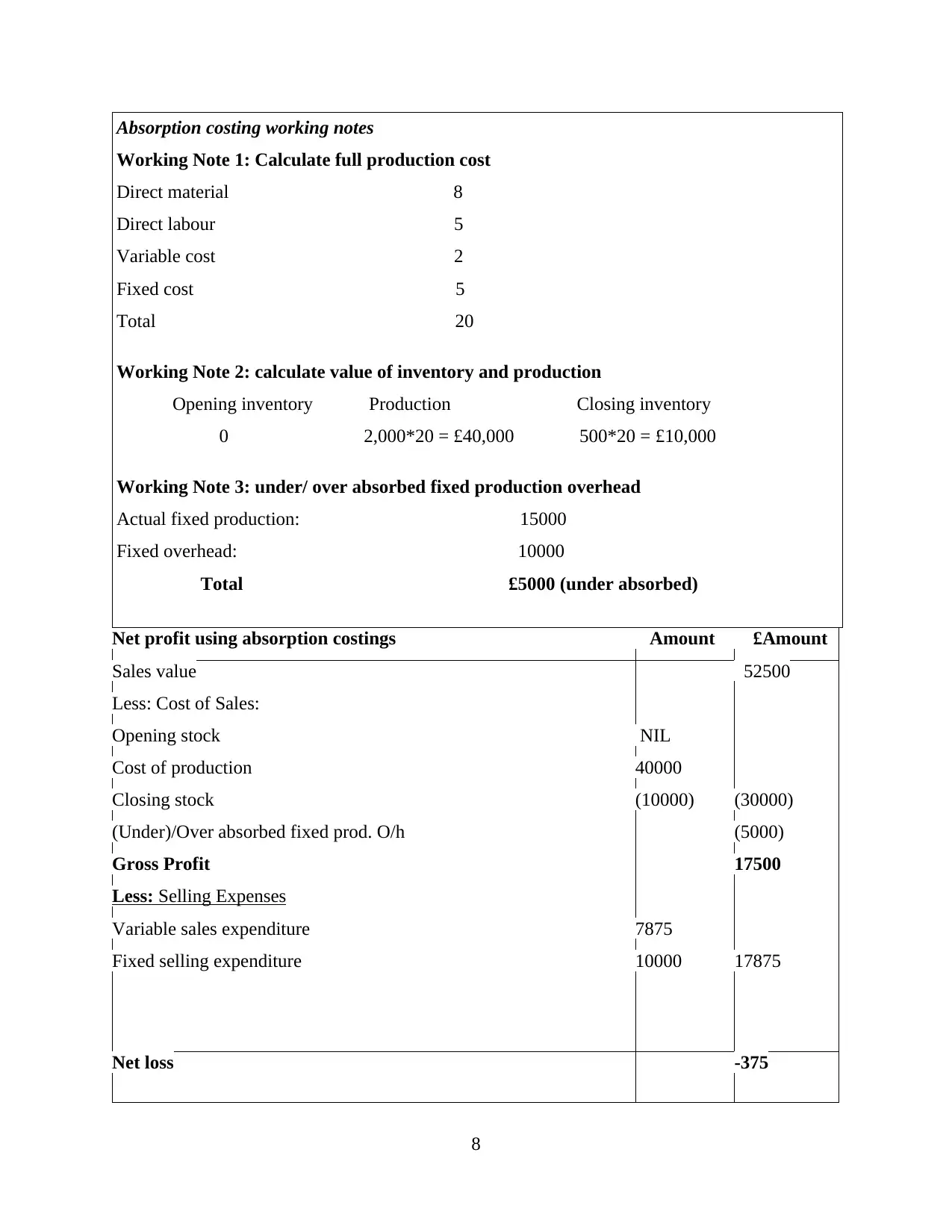

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2

It is the obligation upon the manager is to adopt approach which helps in improvement of

their profitability. Such approaches also help in attainment of sustainability in their business

operations. The two techniques are used improve their business performances. Conservatism

technique helps in reduction of their unnecessary expenses and on the other hand materiality

technique helps to manage their available resources in more optimum manner.

D2

Through use of marginal costing method loss of 2875 is observed whether from the use of

absorption costing method loss is attained of the amount of 375. This difference occur because

involvement of fixed cost in absorption costing method.

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

According to the above calculation, it has been found that profit generated from marginal

costing is 2125 from their total sales. This differences are arises because of fixed cost

adjustments.

TASK 3

P4: Merits and demerits of using various types of budgets and their significant

Planning is an important part for every business, they need to make use of data in order to

manage and control resources of an organisation in effective manner. This will assists TECH UK

to attain their set objectives by using appropriate budgets. Budgets is known as future estimation

of total costs and expenditure they are going to invested on the production of specific products

and services are recorded effectively. The primary motive of every project managers is to make

use data in accordance to attain future aims and objectives. It has been seen that there are various

types of budgets that are essential for an organisation to record their important data during the

period of time. Some of them are discussed underneath:

Master budget: According to this particular budget which is known as combination of all

types of budgets those are prepared by an organisation at the time of manufacturing process.

9

It is the obligation upon the manager is to adopt approach which helps in improvement of

their profitability. Such approaches also help in attainment of sustainability in their business

operations. The two techniques are used improve their business performances. Conservatism

technique helps in reduction of their unnecessary expenses and on the other hand materiality

technique helps to manage their available resources in more optimum manner.

D2

Through use of marginal costing method loss of 2875 is observed whether from the use of

absorption costing method loss is attained of the amount of 375. This difference occur because

involvement of fixed cost in absorption costing method.

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

According to the above calculation, it has been found that profit generated from marginal

costing is 2125 from their total sales. This differences are arises because of fixed cost

adjustments.

TASK 3

P4: Merits and demerits of using various types of budgets and their significant

Planning is an important part for every business, they need to make use of data in order to

manage and control resources of an organisation in effective manner. This will assists TECH UK

to attain their set objectives by using appropriate budgets. Budgets is known as future estimation

of total costs and expenditure they are going to invested on the production of specific products

and services are recorded effectively. The primary motive of every project managers is to make

use data in accordance to attain future aims and objectives. It has been seen that there are various

types of budgets that are essential for an organisation to record their important data during the

period of time. Some of them are discussed underneath:

Master budget: According to this particular budget which is known as combination of all

types of budgets those are prepared by an organisation at the time of manufacturing process.

9

This budget is consists of essential financial statements such as income statement, balance sheet,

cash forecast and financial planning. This help and organisation to perform all kinds of internal

or external activities in accurate manner (Cadez and Guilding, 2012).

Advantage: The main benefits of using this budget are to assist manager to prepare only

one report that consists of all data regarding growth and financial performance of Tech UK.

Disadvantage: The main limitation of using these types of budgets is that it is more costly

and time consuming of the company.

Cash flow budget: According to this types of budget which is prepared by an organisation

to analyse total cash flow incurred by the company during an accounting period of time. The

main sources of data collection are taken from various activities such as investing, operating and

financing.

Advantage: Total cash goes out of the business can easily be determine by managers

during the period of time. It will make simple to account managers to make use of data in

systematic manner so that they can determine total cash inflows during the time.

Disadvantage: In case of total recovery time get completed it is more difficult to calculate

total cash generate by the company during the time.

Operating budget: It is known as total all those report which is being prepared by using

all essential data regarding total costs and expenditure Tech UK at the time of production

process. It can be prepared on regular or continuous basis (What is Budgetary control? 2017).

This will assist and organisation to control necessary implications that are affecting overall

profitability at the same point of time.

Advantage: It assists company to analyse their total sales, operation and raw material

budgets which is being prepared during the period of time. It is more reliable in case they are

preparing for longer terms.

Disadvantage: It is more time consumer as regular data is needed to be collected in

continuous basis which is tougher task for production managers (Fullerton, Kennedy and

Widener, 2013).

Rolling budget: It is continually updated to include a new budget period as the most

budget period as the most recent completion of time frame. This involves the incremental growth

of current budgets.

10

cash forecast and financial planning. This help and organisation to perform all kinds of internal

or external activities in accurate manner (Cadez and Guilding, 2012).

Advantage: The main benefits of using this budget are to assist manager to prepare only

one report that consists of all data regarding growth and financial performance of Tech UK.

Disadvantage: The main limitation of using these types of budgets is that it is more costly

and time consuming of the company.

Cash flow budget: According to this types of budget which is prepared by an organisation

to analyse total cash flow incurred by the company during an accounting period of time. The

main sources of data collection are taken from various activities such as investing, operating and

financing.

Advantage: Total cash goes out of the business can easily be determine by managers

during the period of time. It will make simple to account managers to make use of data in

systematic manner so that they can determine total cash inflows during the time.

Disadvantage: In case of total recovery time get completed it is more difficult to calculate

total cash generate by the company during the time.

Operating budget: It is known as total all those report which is being prepared by using

all essential data regarding total costs and expenditure Tech UK at the time of production

process. It can be prepared on regular or continuous basis (What is Budgetary control? 2017).

This will assist and organisation to control necessary implications that are affecting overall

profitability at the same point of time.

Advantage: It assists company to analyse their total sales, operation and raw material

budgets which is being prepared during the period of time. It is more reliable in case they are

preparing for longer terms.

Disadvantage: It is more time consumer as regular data is needed to be collected in

continuous basis which is tougher task for production managers (Fullerton, Kennedy and

Widener, 2013).

Rolling budget: It is continually updated to include a new budget period as the most

budget period as the most recent completion of time frame. This involves the incremental growth

of current budgets.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.