Comprehensive Report: Management Accounting for Agmet Chemical Company

VerifiedAdded on 2020/01/28

|18

|5953

|164

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Agmet, a chemical producing company. It begins with an introduction to management accounting, its importance, and the different types of systems, including cost accounting and inventory management. The report then delves into various reporting methods, such as ratio analysis and cash flow analysis, and highlights the benefits of a management accounting system, including improved cash flow and decision-making. A critical evaluation of the management accounting system is presented, focusing on relevant cost analysis, activity-based costing, and make-or-buy decisions. The report further explores cost calculation techniques like absorption costing and marginal costing, along with interpretation of data using distinct techniques. It also discusses the advantages and disadvantages of different planning tools used for budgetary control, such as variance analysis and flexible budgeting. The report concludes with a comparison of how different organizations adapt management accounting to address financial problems and an analysis of management accounting's role in achieving sustainable success. The report uses a variety of sources to support its findings.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting system and different type of system which is related to

management accounting..............................................................................................................4

P2 Different method which is used in management accounting reporting.................................5

M1 Benefits of management accounting system and their application.......................................7

D1 Critically evaluate the management accounting system.......................................................7

TASK 2............................................................................................................................................8

P3 & M2 Calculation of costs using different techniques...........................................................8

D2 Interpretation of data by using distinct techniques..............................................................11

TASK 3..........................................................................................................................................12

P4 Advantage and disadvantage of different planning tools which is used for budgetary

control.......................................................................................................................................12

M3 Use of different planning tools...........................................................................................13

D3 Evaluation of planning methods..........................................................................................14

P5 Comparison on different organisation that they adapt the management accounting system

to respond financial problems...................................................................................................14

M4 Analysis of management accounting for the sustainable success.......................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting system and different type of system which is related to

management accounting..............................................................................................................4

P2 Different method which is used in management accounting reporting.................................5

M1 Benefits of management accounting system and their application.......................................7

D1 Critically evaluate the management accounting system.......................................................7

TASK 2............................................................................................................................................8

P3 & M2 Calculation of costs using different techniques...........................................................8

D2 Interpretation of data by using distinct techniques..............................................................11

TASK 3..........................................................................................................................................12

P4 Advantage and disadvantage of different planning tools which is used for budgetary

control.......................................................................................................................................12

M3 Use of different planning tools...........................................................................................13

D3 Evaluation of planning methods..........................................................................................14

P5 Comparison on different organisation that they adapt the management accounting system

to respond financial problems...................................................................................................14

M4 Analysis of management accounting for the sustainable success.......................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting helps every company in managing all the business activities so

that they can not face any issues and by that they can attain the goals and objectives. In each and

every business whether it is large or small having managers who use the management accounting

system. For improving the business appropriate plans should be made. Along with this they have

to organise the resources and control the operations (Baldvinsdottir Mitchell and Nørreklit,

2010). Managers of the firm have to carry out the different activities which includes planning,

directing, motivating as well as controlling. Management accounting is the branch of accounting

which assist in focuses on providing the information or data and this can be used by the internal

users. Managerial accounting along with the financial accounting having the most prominent the

branches of accounting and both deal with processing by using the information which aid in

making the correct decisions (Significance of Management Accounting Techniques in Decision-

making: An Empirical Study on Manufacturing Organizations in Bangladesh. 2011). The present

report is based on Agmet which is a chemical producing company and this business entity having

50 employees. In the below mentioned assignment, different planning tools should be used along

with the advantages and disadvantages of distinct budgetary control has to be discussed.

TASK 1

P1 Concept of management accounting system and different type of system which is related to

management accounting

Management accounting is a system which is concerned with the different accounting

information and that data is useful to the management. Management accounting is a application

of the appropriate tools so that they can make projected and historical economic data of the entity

so that they can assist the administration by establishing or making plans for the reasonable

economic objectives in making the rational decisions as that they can accomplish the goals.

Management accounting may be defined as a aspect of accounting which is concerned with the

efficient management of a business so that they can facilitate having the efficient and opportune

the planning and control (Bennett, Schaltegger and Zvezdov, 2013). Management accounting

satisfies the requirements of the managerial activities so that they can make appropriate business

Managerial accounting helps every company in managing all the business activities so

that they can not face any issues and by that they can attain the goals and objectives. In each and

every business whether it is large or small having managers who use the management accounting

system. For improving the business appropriate plans should be made. Along with this they have

to organise the resources and control the operations (Baldvinsdottir Mitchell and Nørreklit,

2010). Managers of the firm have to carry out the different activities which includes planning,

directing, motivating as well as controlling. Management accounting is the branch of accounting

which assist in focuses on providing the information or data and this can be used by the internal

users. Managerial accounting along with the financial accounting having the most prominent the

branches of accounting and both deal with processing by using the information which aid in

making the correct decisions (Significance of Management Accounting Techniques in Decision-

making: An Empirical Study on Manufacturing Organizations in Bangladesh. 2011). The present

report is based on Agmet which is a chemical producing company and this business entity having

50 employees. In the below mentioned assignment, different planning tools should be used along

with the advantages and disadvantages of distinct budgetary control has to be discussed.

TASK 1

P1 Concept of management accounting system and different type of system which is related to

management accounting

Management accounting is a system which is concerned with the different accounting

information and that data is useful to the management. Management accounting is a application

of the appropriate tools so that they can make projected and historical economic data of the entity

so that they can assist the administration by establishing or making plans for the reasonable

economic objectives in making the rational decisions as that they can accomplish the goals.

Management accounting may be defined as a aspect of accounting which is concerned with the

efficient management of a business so that they can facilitate having the efficient and opportune

the planning and control (Bennett, Schaltegger and Zvezdov, 2013). Management accounting

satisfies the requirements of the managerial activities so that they can make appropriate business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

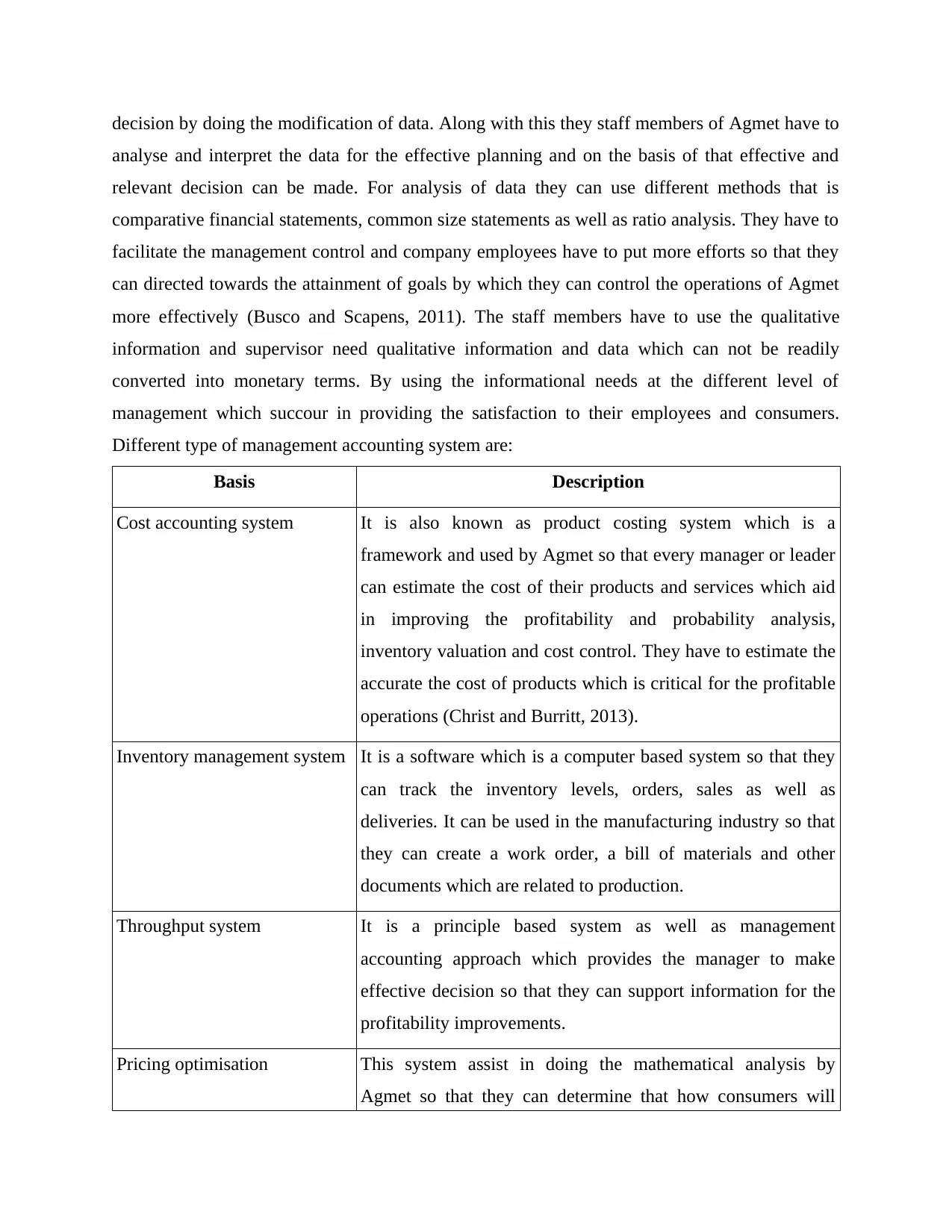

decision by doing the modification of data. Along with this they staff members of Agmet have to

analyse and interpret the data for the effective planning and on the basis of that effective and

relevant decision can be made. For analysis of data they can use different methods that is

comparative financial statements, common size statements as well as ratio analysis. They have to

facilitate the management control and company employees have to put more efforts so that they

can directed towards the attainment of goals by which they can control the operations of Agmet

more effectively (Busco and Scapens, 2011). The staff members have to use the qualitative

information and supervisor need qualitative information and data which can not be readily

converted into monetary terms. By using the informational needs at the different level of

management which succour in providing the satisfaction to their employees and consumers.

Different type of management accounting system are:

Basis Description

Cost accounting system It is also known as product costing system which is a

framework and used by Agmet so that every manager or leader

can estimate the cost of their products and services which aid

in improving the profitability and probability analysis,

inventory valuation and cost control. They have to estimate the

accurate the cost of products which is critical for the profitable

operations (Christ and Burritt, 2013).

Inventory management system It is a software which is a computer based system so that they

can track the inventory levels, orders, sales as well as

deliveries. It can be used in the manufacturing industry so that

they can create a work order, a bill of materials and other

documents which are related to production.

Throughput system It is a principle based system as well as management

accounting approach which provides the manager to make

effective decision so that they can support information for the

profitability improvements.

Pricing optimisation This system assist in doing the mathematical analysis by

Agmet so that they can determine that how consumers will

analyse and interpret the data for the effective planning and on the basis of that effective and

relevant decision can be made. For analysis of data they can use different methods that is

comparative financial statements, common size statements as well as ratio analysis. They have to

facilitate the management control and company employees have to put more efforts so that they

can directed towards the attainment of goals by which they can control the operations of Agmet

more effectively (Busco and Scapens, 2011). The staff members have to use the qualitative

information and supervisor need qualitative information and data which can not be readily

converted into monetary terms. By using the informational needs at the different level of

management which succour in providing the satisfaction to their employees and consumers.

Different type of management accounting system are:

Basis Description

Cost accounting system It is also known as product costing system which is a

framework and used by Agmet so that every manager or leader

can estimate the cost of their products and services which aid

in improving the profitability and probability analysis,

inventory valuation and cost control. They have to estimate the

accurate the cost of products which is critical for the profitable

operations (Christ and Burritt, 2013).

Inventory management system It is a software which is a computer based system so that they

can track the inventory levels, orders, sales as well as

deliveries. It can be used in the manufacturing industry so that

they can create a work order, a bill of materials and other

documents which are related to production.

Throughput system It is a principle based system as well as management

accounting approach which provides the manager to make

effective decision so that they can support information for the

profitability improvements.

Pricing optimisation This system assist in doing the mathematical analysis by

Agmet so that they can determine that how consumers will

respond to the distinctive price of the different products which

help the employees in meeting the objectives and maximising

the operating profit (Cinquini and Tenucci, 2010).

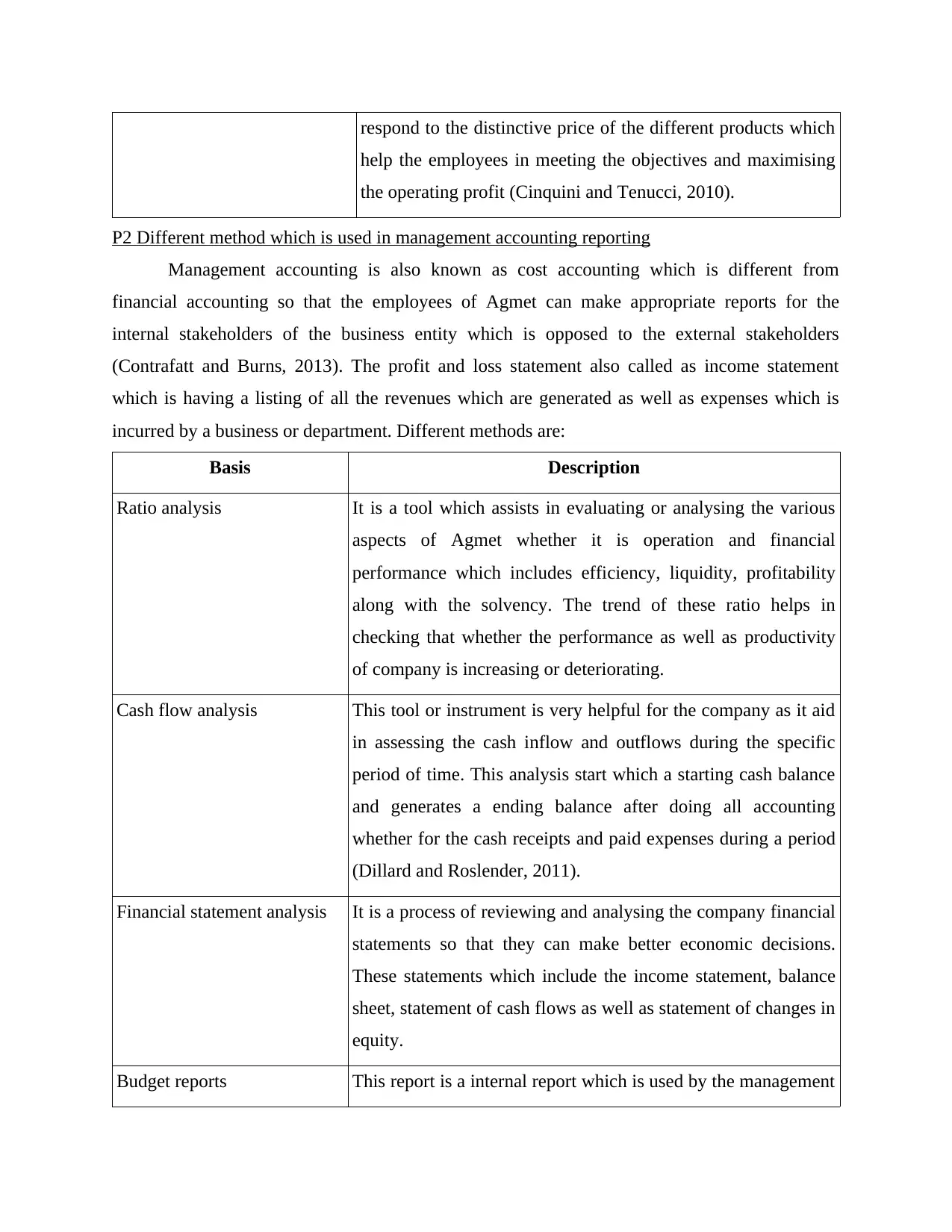

P2 Different method which is used in management accounting reporting

Management accounting is also known as cost accounting which is different from

financial accounting so that the employees of Agmet can make appropriate reports for the

internal stakeholders of the business entity which is opposed to the external stakeholders

(Contrafatt and Burns, 2013). The profit and loss statement also called as income statement

which is having a listing of all the revenues which are generated as well as expenses which is

incurred by a business or department. Different methods are:

Basis Description

Ratio analysis It is a tool which assists in evaluating or analysing the various

aspects of Agmet whether it is operation and financial

performance which includes efficiency, liquidity, profitability

along with the solvency. The trend of these ratio helps in

checking that whether the performance as well as productivity

of company is increasing or deteriorating.

Cash flow analysis This tool or instrument is very helpful for the company as it aid

in assessing the cash inflow and outflows during the specific

period of time. This analysis start which a starting cash balance

and generates a ending balance after doing all accounting

whether for the cash receipts and paid expenses during a period

(Dillard and Roslender, 2011).

Financial statement analysis It is a process of reviewing and analysing the company financial

statements so that they can make better economic decisions.

These statements which include the income statement, balance

sheet, statement of cash flows as well as statement of changes in

equity.

Budget reports This report is a internal report which is used by the management

help the employees in meeting the objectives and maximising

the operating profit (Cinquini and Tenucci, 2010).

P2 Different method which is used in management accounting reporting

Management accounting is also known as cost accounting which is different from

financial accounting so that the employees of Agmet can make appropriate reports for the

internal stakeholders of the business entity which is opposed to the external stakeholders

(Contrafatt and Burns, 2013). The profit and loss statement also called as income statement

which is having a listing of all the revenues which are generated as well as expenses which is

incurred by a business or department. Different methods are:

Basis Description

Ratio analysis It is a tool which assists in evaluating or analysing the various

aspects of Agmet whether it is operation and financial

performance which includes efficiency, liquidity, profitability

along with the solvency. The trend of these ratio helps in

checking that whether the performance as well as productivity

of company is increasing or deteriorating.

Cash flow analysis This tool or instrument is very helpful for the company as it aid

in assessing the cash inflow and outflows during the specific

period of time. This analysis start which a starting cash balance

and generates a ending balance after doing all accounting

whether for the cash receipts and paid expenses during a period

(Dillard and Roslender, 2011).

Financial statement analysis It is a process of reviewing and analysing the company financial

statements so that they can make better economic decisions.

These statements which include the income statement, balance

sheet, statement of cash flows as well as statement of changes in

equity.

Budget reports This report is a internal report which is used by the management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of Agmet so that they can compare the estimated, budgeted

projections with the actual performance so that they can achieve

the targets within a specified time. A budget report is to be

designed so that they can close the budgeted performance on the

basis of actual performance during an accounting period

(Weißenberger and Angelkort,2011).

M1 Benefits of management accounting system and their application

Management accounting system should be used by the business entity which helps in

attaining maximum benefits that includes the improvement in cash flow so that they can manage

the cash of firm. Another is reduction in operating and non operating expenses which helps in

making the good expenditure by making appropriate budgets. In addition to this, business

decision-making means the employees or managers have to make appropriate decisions for the

business entity so that they can meet their objectives (Fullerton, Kennedy and Widener, 2014).

Next is financial planning and in this manager have to do relevant and proper planning which is

related to finance so that they can make budgets and on the basis of that budget they can make

the spendings along with the earning as these factors helps in improving the performance and

productivity. Moreover, they can use management reporting which aid in preparing and

maintaining the specific accounting report of the distinctive contents that is profit and loss

statement and balance sheet. Along with this they can use different tools and techniques that is

ratio analysis, cost accounting along with the marginal costing and according to that they can

attain success when the employees facing high competition. By using the management functions

they can allot the resources as well as have to use proper process so that they can attain the goals.

The use of management accounting system succour in identifying the needs and on the basis of

that decisions to be made to fulfil that by the involvement of the employees which assist in

maintaining the standards and leading position in the market place (Håkansson, Kraus and Lind

eds., 2010).

D1 Critically evaluate the management accounting system

By using the process of management accounting system employees of Agmet have to do

proper leader and transformation. There are different methods which helps in management

accounting and reporting system in the different areas that is:

projections with the actual performance so that they can achieve

the targets within a specified time. A budget report is to be

designed so that they can close the budgeted performance on the

basis of actual performance during an accounting period

(Weißenberger and Angelkort,2011).

M1 Benefits of management accounting system and their application

Management accounting system should be used by the business entity which helps in

attaining maximum benefits that includes the improvement in cash flow so that they can manage

the cash of firm. Another is reduction in operating and non operating expenses which helps in

making the good expenditure by making appropriate budgets. In addition to this, business

decision-making means the employees or managers have to make appropriate decisions for the

business entity so that they can meet their objectives (Fullerton, Kennedy and Widener, 2014).

Next is financial planning and in this manager have to do relevant and proper planning which is

related to finance so that they can make budgets and on the basis of that budget they can make

the spendings along with the earning as these factors helps in improving the performance and

productivity. Moreover, they can use management reporting which aid in preparing and

maintaining the specific accounting report of the distinctive contents that is profit and loss

statement and balance sheet. Along with this they can use different tools and techniques that is

ratio analysis, cost accounting along with the marginal costing and according to that they can

attain success when the employees facing high competition. By using the management functions

they can allot the resources as well as have to use proper process so that they can attain the goals.

The use of management accounting system succour in identifying the needs and on the basis of

that decisions to be made to fulfil that by the involvement of the employees which assist in

maintaining the standards and leading position in the market place (Håkansson, Kraus and Lind

eds., 2010).

D1 Critically evaluate the management accounting system

By using the process of management accounting system employees of Agmet have to do

proper leader and transformation. There are different methods which helps in management

accounting and reporting system in the different areas that is:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Relevant cost analysis: This can be used for evaluating the relevant cost. Here relevant

cost refers to the cost which having a impact on the process of decision making of Agmet and its

administration. Management Accounting as well as reporting which aid in providing the relevant

information related to cost to the employees of Agmet (Herbert and Seal, 2012). Along with this,

it helps the management in making more efficient decision for business enterprise. Variable cost

of the product can be considered as the relevant cost as changes on the basis of change in

quantity and volume of production. Where as fixed cost of merchandise does not change in the

production level as it is not related with the relevant cost.

Activity based costing methods: This method helps Agmet in ascertaining that who will

be the consumers of the company and it also aid in identifying the wants and desires of them.

Activity based costing method helps in making the changes in the activities. Once service user

get known by Agmet or when company is able to identify its more beneficial to end users the

company will than focus the advertising efforts on that customers (Hiebl, 2014).

Make or buy analysis: The supervising of cited enterprise can analyse that what they want

to purchase from outsiders as well as what they can produce in the business entity. If making a

merchandise will proof more costly to the employees of Agmet than in this situation it will be

better for business enterprise to buy it from the outside. While if equipments which are using in

the enterprise is very cheap than the corporation should produce qualitative products.

Utilising the data: The employees as well as managers of Agmet have to use or utilise the

appropriate data so that they can manage all the operational activities. The management

accounting along with the reporting provide the manager necessary and essential information.

Further, by using this information or data they can attain success in future (Ward, 2012).

TASK 2

P3 & M2 Calculation of costs using different techniques

Absorption costing: It is a method which assist in doing the inventory valuation on the

basis of all the manufacturing expenses which are allocated to the cost centres so that they

recognise the total cost of production. It is a traditional method for the ascertainment of cost and

in this both fixed as well as variable cost are related to product cost (Jansen, 2011). There are

different type of absorption costing which includes activity based costing, job costing as well as

process costing.

cost refers to the cost which having a impact on the process of decision making of Agmet and its

administration. Management Accounting as well as reporting which aid in providing the relevant

information related to cost to the employees of Agmet (Herbert and Seal, 2012). Along with this,

it helps the management in making more efficient decision for business enterprise. Variable cost

of the product can be considered as the relevant cost as changes on the basis of change in

quantity and volume of production. Where as fixed cost of merchandise does not change in the

production level as it is not related with the relevant cost.

Activity based costing methods: This method helps Agmet in ascertaining that who will

be the consumers of the company and it also aid in identifying the wants and desires of them.

Activity based costing method helps in making the changes in the activities. Once service user

get known by Agmet or when company is able to identify its more beneficial to end users the

company will than focus the advertising efforts on that customers (Hiebl, 2014).

Make or buy analysis: The supervising of cited enterprise can analyse that what they want

to purchase from outsiders as well as what they can produce in the business entity. If making a

merchandise will proof more costly to the employees of Agmet than in this situation it will be

better for business enterprise to buy it from the outside. While if equipments which are using in

the enterprise is very cheap than the corporation should produce qualitative products.

Utilising the data: The employees as well as managers of Agmet have to use or utilise the

appropriate data so that they can manage all the operational activities. The management

accounting along with the reporting provide the manager necessary and essential information.

Further, by using this information or data they can attain success in future (Ward, 2012).

TASK 2

P3 & M2 Calculation of costs using different techniques

Absorption costing: It is a method which assist in doing the inventory valuation on the

basis of all the manufacturing expenses which are allocated to the cost centres so that they

recognise the total cost of production. It is a traditional method for the ascertainment of cost and

in this both fixed as well as variable cost are related to product cost (Jansen, 2011). There are

different type of absorption costing which includes activity based costing, job costing as well as

process costing.

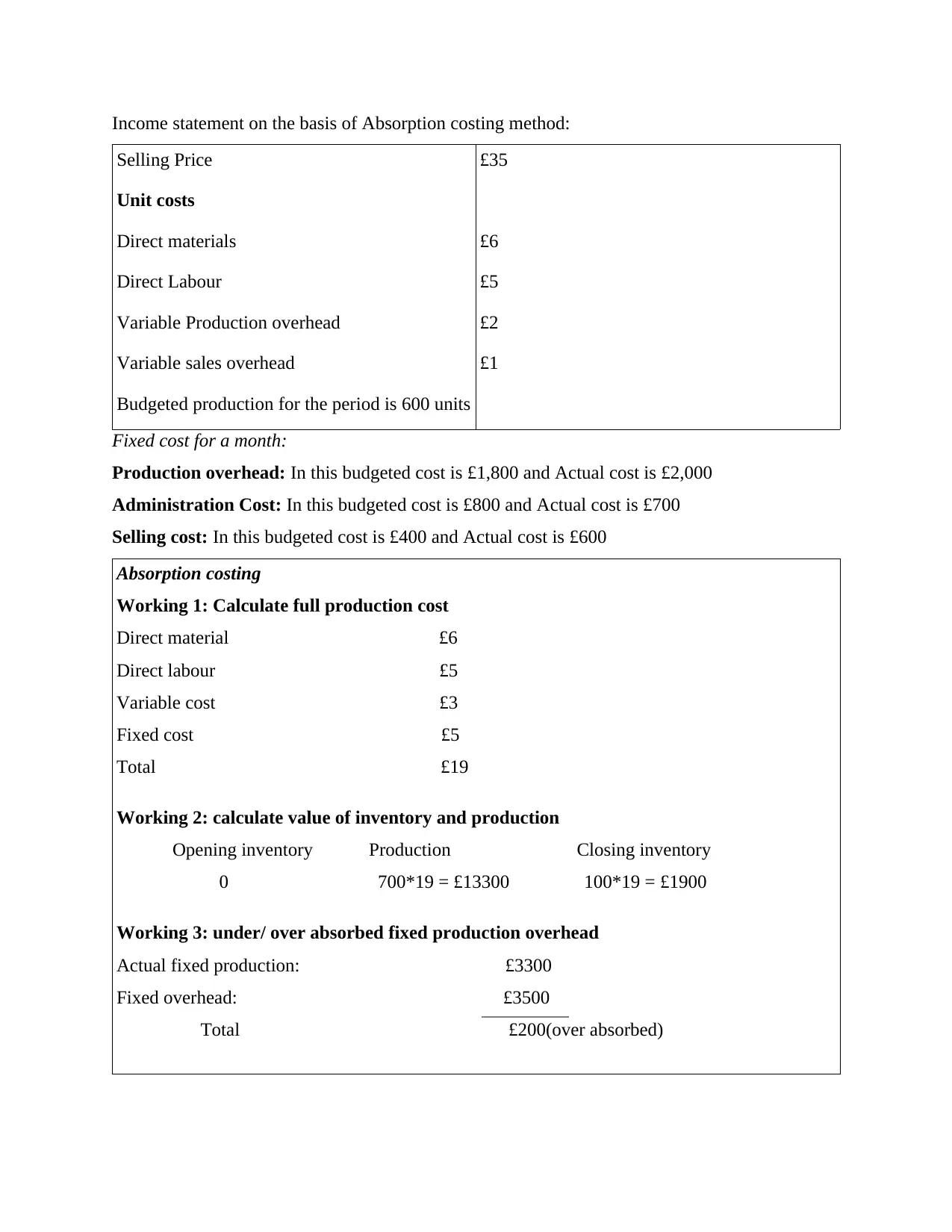

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

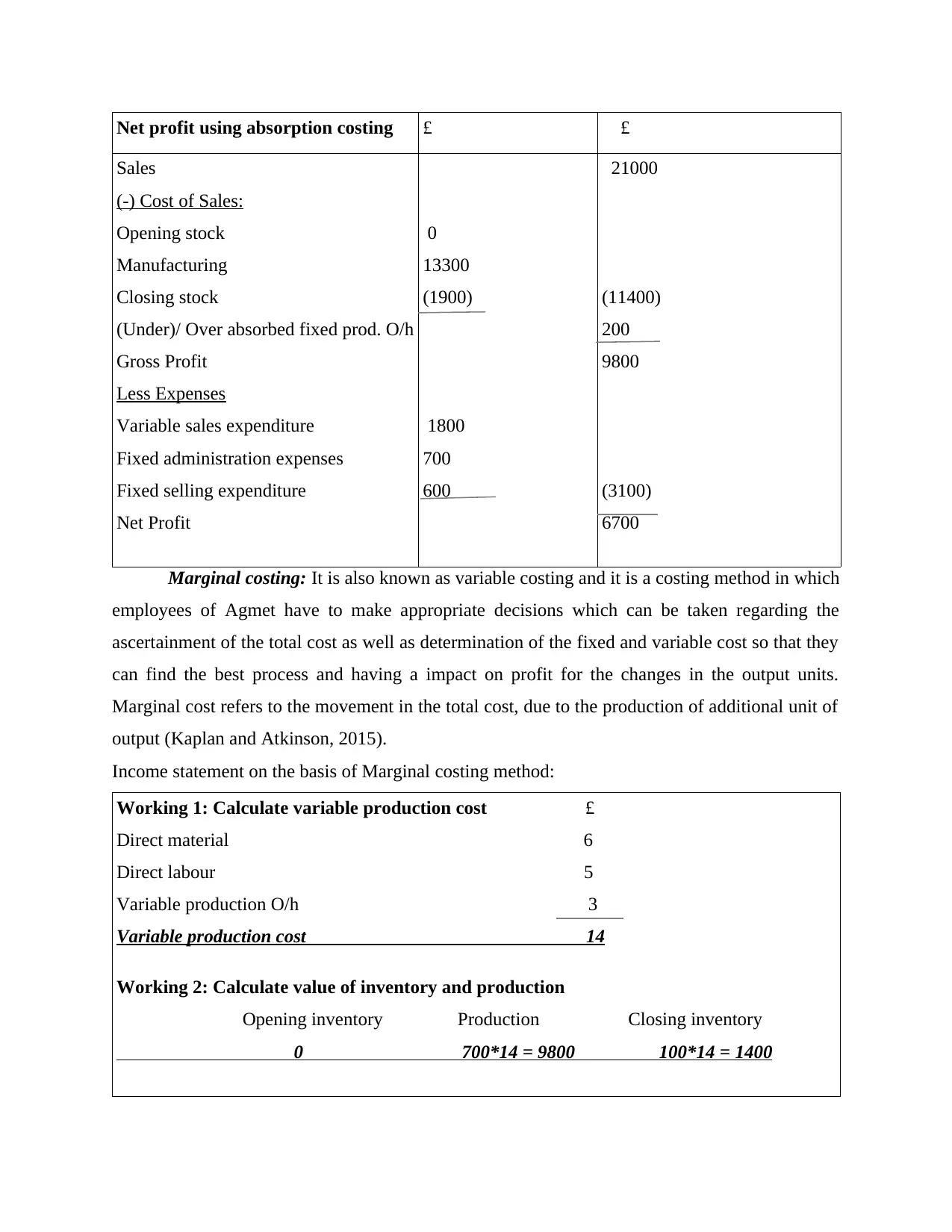

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Net Profit

0

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Marginal costing: It is also known as variable costing and it is a costing method in which

employees of Agmet have to make appropriate decisions which can be taken regarding the

ascertainment of the total cost as well as determination of the fixed and variable cost so that they

can find the best process and having a impact on profit for the changes in the output units.

Marginal cost refers to the movement in the total cost, due to the production of additional unit of

output (Kaplan and Atkinson, 2015).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Net Profit

0

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Marginal costing: It is also known as variable costing and it is a costing method in which

employees of Agmet have to make appropriate decisions which can be taken regarding the

ascertainment of the total cost as well as determination of the fixed and variable cost so that they

can find the best process and having a impact on profit for the changes in the output units.

Marginal cost refers to the movement in the total cost, due to the production of additional unit of

output (Kaplan and Atkinson, 2015).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

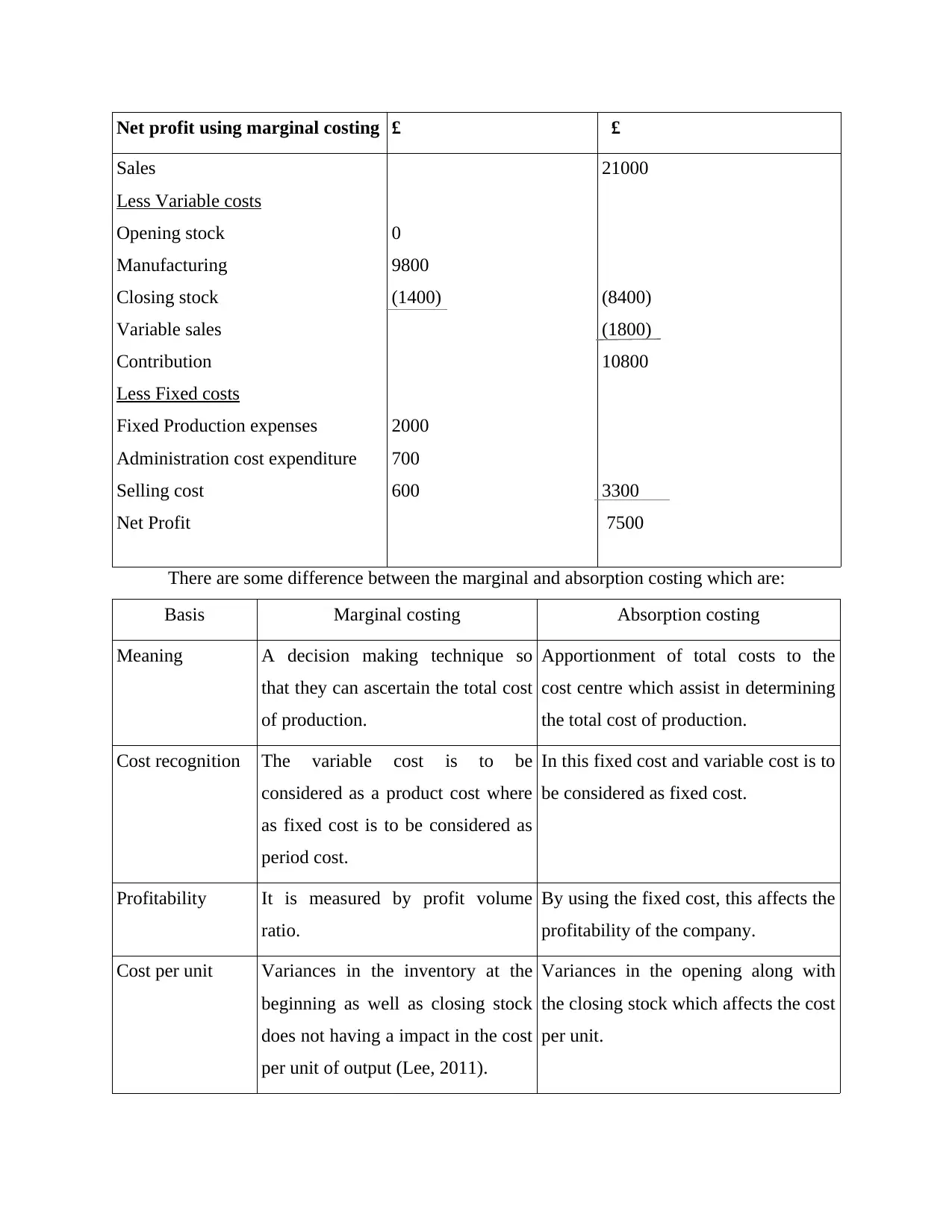

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

3300

7500

There are some difference between the marginal and absorption costing which are:

Basis Marginal costing Absorption costing

Meaning A decision making technique so

that they can ascertain the total cost

of production.

Apportionment of total costs to the

cost centre which assist in determining

the total cost of production.

Cost recognition The variable cost is to be

considered as a product cost where

as fixed cost is to be considered as

period cost.

In this fixed cost and variable cost is to

be considered as fixed cost.

Profitability It is measured by profit volume

ratio.

By using the fixed cost, this affects the

profitability of the company.

Cost per unit Variances in the inventory at the

beginning as well as closing stock

does not having a impact in the cost

per unit of output (Lee, 2011).

Variances in the opening along with

the closing stock which affects the cost

per unit.

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

3300

7500

There are some difference between the marginal and absorption costing which are:

Basis Marginal costing Absorption costing

Meaning A decision making technique so

that they can ascertain the total cost

of production.

Apportionment of total costs to the

cost centre which assist in determining

the total cost of production.

Cost recognition The variable cost is to be

considered as a product cost where

as fixed cost is to be considered as

period cost.

In this fixed cost and variable cost is to

be considered as fixed cost.

Profitability It is measured by profit volume

ratio.

By using the fixed cost, this affects the

profitability of the company.

Cost per unit Variances in the inventory at the

beginning as well as closing stock

does not having a impact in the cost

per unit of output (Lee, 2011).

Variances in the opening along with

the closing stock which affects the cost

per unit.

Classification of

overheads

Fixed and variable Production, administration as well as

selling and distribution.

D2 Interpretation of data by using distinct techniques

The staff members as well as manager of Agmet have to make appropriate financial

reports in a attractive way which assist in making decisions for doing the investments which

accomplish the goals and objectives. Along with this to identify the net profit for doing the

investments on company they can use different tools and techniques that is absorption or

marginal costing which provides the overview of the financial position of the corporation (Van

Helden and et. al., 2010). Moreover, investors having to find the capability of Agmet that they

can do then investment or not in this firm. By doing the calculation of marginal cost by using

appropriate formula net profit is 7500 and contribution is 10800. Further, by using the absorption

costing method net profit is 6700. Along with this by using different instruments net profit is

different from each other.

TASK 3

P4 Advantage and disadvantage of different planning tools which is used for budgetary control

There are different type of planning tools are there so that they can do proper budgetary

control for Agmet. Advantages of budgetary tools which is used for planning:

Coordination: The employees of the company have to make proper budgets so that they

can coordinate the activities across the distinct departments and which assist in maintaining the

link between the activities as well as flow of activities which has to be maintained in Agmet

(Luft and Shields, 2010).

Strategic plans: Budget helps in translating the strategic plans into action. They have to

use specific resources so that they can generate the maximum revenue as well as activities so that

they are required to carry out specific plans.

Records keeping: Budget provides the excellent indicator so that they can maintain the

records of all different activities which assist in attaining the goals and objectives.

Communication: Budgetary instrument aids to communicate with staff members so that

they can make proper budget and communicate in advance with the workers of Agmet and this

assist in future planning of budget.

overheads

Fixed and variable Production, administration as well as

selling and distribution.

D2 Interpretation of data by using distinct techniques

The staff members as well as manager of Agmet have to make appropriate financial

reports in a attractive way which assist in making decisions for doing the investments which

accomplish the goals and objectives. Along with this to identify the net profit for doing the

investments on company they can use different tools and techniques that is absorption or

marginal costing which provides the overview of the financial position of the corporation (Van

Helden and et. al., 2010). Moreover, investors having to find the capability of Agmet that they

can do then investment or not in this firm. By doing the calculation of marginal cost by using

appropriate formula net profit is 7500 and contribution is 10800. Further, by using the absorption

costing method net profit is 6700. Along with this by using different instruments net profit is

different from each other.

TASK 3

P4 Advantage and disadvantage of different planning tools which is used for budgetary control

There are different type of planning tools are there so that they can do proper budgetary

control for Agmet. Advantages of budgetary tools which is used for planning:

Coordination: The employees of the company have to make proper budgets so that they

can coordinate the activities across the distinct departments and which assist in maintaining the

link between the activities as well as flow of activities which has to be maintained in Agmet

(Luft and Shields, 2010).

Strategic plans: Budget helps in translating the strategic plans into action. They have to

use specific resources so that they can generate the maximum revenue as well as activities so that

they are required to carry out specific plans.

Records keeping: Budget provides the excellent indicator so that they can maintain the

records of all different activities which assist in attaining the goals and objectives.

Communication: Budgetary instrument aids to communicate with staff members so that

they can make proper budget and communicate in advance with the workers of Agmet and this

assist in future planning of budget.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.