Management Accounting Report: Tech (UK) Limited, HND Business Module

VerifiedAdded on 2020/06/05

|18

|4718

|183

Report

AI Summary

This report examines management accounting practices within Tech (UK) Limited, addressing the need for improved financial information to aid departmental decision-making. The report begins by differentiating management accounting from financial accounting, highlighting their respective purposes and formats. It then explores various management accounting systems, including ABC costing and relevant costing analysis, and emphasizes the importance of effective information dissemination. The report delves into different types of accounting systems, such as cost accounting, inventory management, and job costing systems. Furthermore, the report discusses management reporting systems like schedule reports, exception reports, and performance reports. It covers costing methods used to calculate net profit, the advantages and disadvantages of budgeting, and the use of planning tools. The report analyzes financial problems, emphasizing the effective use of accounting systems to resolve them. Overall, the report provides a comprehensive overview of management accounting's role in enhancing financial performance and strategic decision-making within the organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various types of management accounting system and their importance..............................1

P2: (1): Different types of management reporting system..........................................................4

M1: Benefits of using management accounting system..............................................................6

D1: Critical evaluation of accounting reporting systems............................................................6

TASK 2............................................................................................................................................6

P3: Various types of costing methods which are use for calculating net profit..........................6

M2: Effective use of management accounting tools and techniques........................................12

D2: Evaluation on the basis of data collected from business activities....................................12

TASK 3..........................................................................................................................................12

P4: Advantage and disadvantage of budget..............................................................................12

M3: use of various planning tools.............................................................................................14

D3: Critical analysis to overcome financial issues........................................................................14

TASK 4..........................................................................................................................................14

P5: Effective use of accounting systems to resolve financial issues.........................................14

M4: Analysis of financial problems..........................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various types of management accounting system and their importance..............................1

P2: (1): Different types of management reporting system..........................................................4

M1: Benefits of using management accounting system..............................................................6

D1: Critical evaluation of accounting reporting systems............................................................6

TASK 2............................................................................................................................................6

P3: Various types of costing methods which are use for calculating net profit..........................6

M2: Effective use of management accounting tools and techniques........................................12

D2: Evaluation on the basis of data collected from business activities....................................12

TASK 3..........................................................................................................................................12

P4: Advantage and disadvantage of budget..............................................................................12

M3: use of various planning tools.............................................................................................14

D3: Critical analysis to overcome financial issues........................................................................14

TASK 4..........................................................................................................................................14

P5: Effective use of accounting systems to resolve financial issues.........................................14

M4: Analysis of financial problems..........................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Nowadays, it has been seen that plenty of organisations are looking for an effective

system that can assists them to record various accounting transaction in their respective format.

The primary aims and objective of an organisation is to attain their long and short term goals that

are being set by company for betterment of future. The main role of managers is to record their

financial transactions in more effective manner so that goodwill of the company can be attain in

more quick time (Wickramasinghe and Alawattage, 2012).

The project report provide various information about different types of accounting

systems and reporting that are helpful in recording of the data in more reliable manner. Further,

this report would use various costing methods that are effectively responsible for evaluating net

profit of Tech Imda ltd. Merits and demerits of planning tools for controlling budgets are explain

under this. Examination of certain types of financial issues and their effective measures to

overcome those issues is discussed under this project.

TASK 1

P1: Various types of management accounting system and their importance

In accordance to increase profitability, it is necessary to make use of effective accounting

tools that are responsible for garneting more valuable results to the company. In every business

whether small or large they need to collect, summarise and evaluate financial transactions

through using effective accounting systems. Administration is always in research for all those

matters which are necessary for increasing productivity of Imda tech Ltd. It is necessary

operation of management to make use of appropriate accounting information for the purpose of

making effective decision making near future.

The management need to make proper planning, organising and communicating every

department works to analyse whether they are operating in right manner for the growth of the

company. While accounting is said to be a systematic recording of financial data that is being use

for the purpose of analysing future profitability of the company. Management accounting is one

of the most important aspects as a profession which include manager for partnering in effective

company to make future decision making. This is an effective technique of business performance

1

Nowadays, it has been seen that plenty of organisations are looking for an effective

system that can assists them to record various accounting transaction in their respective format.

The primary aims and objective of an organisation is to attain their long and short term goals that

are being set by company for betterment of future. The main role of managers is to record their

financial transactions in more effective manner so that goodwill of the company can be attain in

more quick time (Wickramasinghe and Alawattage, 2012).

The project report provide various information about different types of accounting

systems and reporting that are helpful in recording of the data in more reliable manner. Further,

this report would use various costing methods that are effectively responsible for evaluating net

profit of Tech Imda ltd. Merits and demerits of planning tools for controlling budgets are explain

under this. Examination of certain types of financial issues and their effective measures to

overcome those issues is discussed under this project.

TASK 1

P1: Various types of management accounting system and their importance

In accordance to increase profitability, it is necessary to make use of effective accounting

tools that are responsible for garneting more valuable results to the company. In every business

whether small or large they need to collect, summarise and evaluate financial transactions

through using effective accounting systems. Administration is always in research for all those

matters which are necessary for increasing productivity of Imda tech Ltd. It is necessary

operation of management to make use of appropriate accounting information for the purpose of

making effective decision making near future.

The management need to make proper planning, organising and communicating every

department works to analyse whether they are operating in right manner for the growth of the

company. While accounting is said to be a systematic recording of financial data that is being use

for the purpose of analysing future profitability of the company. Management accounting is one

of the most important aspects as a profession which include manager for partnering in effective

company to make future decision making. This is an effective technique of business performance

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

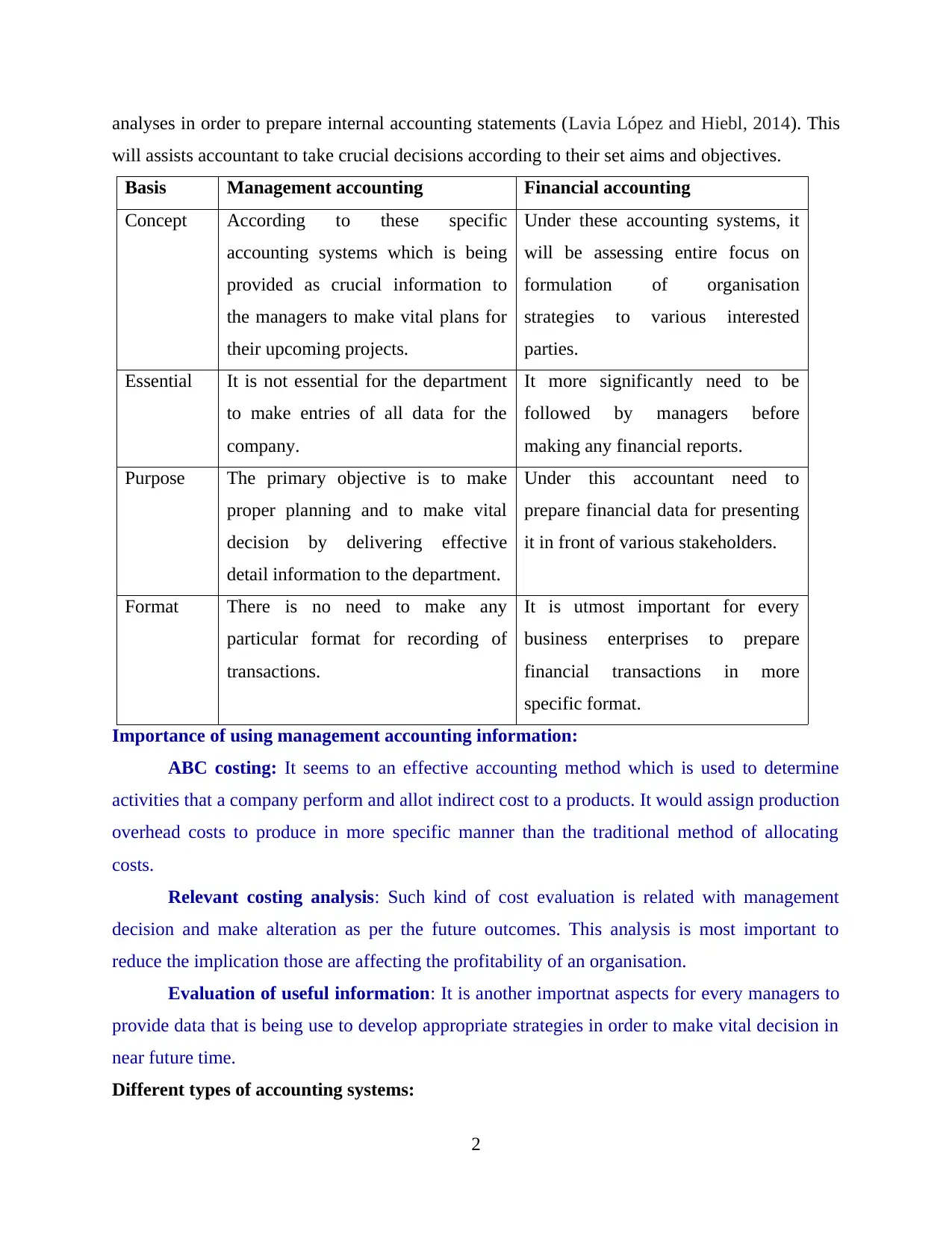

analyses in order to prepare internal accounting statements (Lavia López and Hiebl, 2014). This

will assists accountant to take crucial decisions according to their set aims and objectives.

Basis Management accounting Financial accounting

Concept According to these specific

accounting systems which is being

provided as crucial information to

the managers to make vital plans for

their upcoming projects.

Under these accounting systems, it

will be assessing entire focus on

formulation of organisation

strategies to various interested

parties.

Essential It is not essential for the department

to make entries of all data for the

company.

It more significantly need to be

followed by managers before

making any financial reports.

Purpose The primary objective is to make

proper planning and to make vital

decision by delivering effective

detail information to the department.

Under this accountant need to

prepare financial data for presenting

it in front of various stakeholders.

Format There is no need to make any

particular format for recording of

transactions.

It is utmost important for every

business enterprises to prepare

financial transactions in more

specific format.

Importance of using management accounting information:

ABC costing: It seems to an effective accounting method which is used to determine

activities that a company perform and allot indirect cost to a products. It would assign production

overhead costs to produce in more specific manner than the traditional method of allocating

costs.

Relevant costing analysis: Such kind of cost evaluation is related with management

decision and make alteration as per the future outcomes. This analysis is most important to

reduce the implication those are affecting the profitability of an organisation.

Evaluation of useful information: It is another importnat aspects for every managers to

provide data that is being use to develop appropriate strategies in order to make vital decision in

near future time.

Different types of accounting systems:

2

will assists accountant to take crucial decisions according to their set aims and objectives.

Basis Management accounting Financial accounting

Concept According to these specific

accounting systems which is being

provided as crucial information to

the managers to make vital plans for

their upcoming projects.

Under these accounting systems, it

will be assessing entire focus on

formulation of organisation

strategies to various interested

parties.

Essential It is not essential for the department

to make entries of all data for the

company.

It more significantly need to be

followed by managers before

making any financial reports.

Purpose The primary objective is to make

proper planning and to make vital

decision by delivering effective

detail information to the department.

Under this accountant need to

prepare financial data for presenting

it in front of various stakeholders.

Format There is no need to make any

particular format for recording of

transactions.

It is utmost important for every

business enterprises to prepare

financial transactions in more

specific format.

Importance of using management accounting information:

ABC costing: It seems to an effective accounting method which is used to determine

activities that a company perform and allot indirect cost to a products. It would assign production

overhead costs to produce in more specific manner than the traditional method of allocating

costs.

Relevant costing analysis: Such kind of cost evaluation is related with management

decision and make alteration as per the future outcomes. This analysis is most important to

reduce the implication those are affecting the profitability of an organisation.

Evaluation of useful information: It is another importnat aspects for every managers to

provide data that is being use to develop appropriate strategies in order to make vital decision in

near future time.

Different types of accounting systems:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are several accounting systems that can be helpful for an organisation to evaluate

their regular financial transactions that are done during the period of time. Few of them are

elaborated underneath:

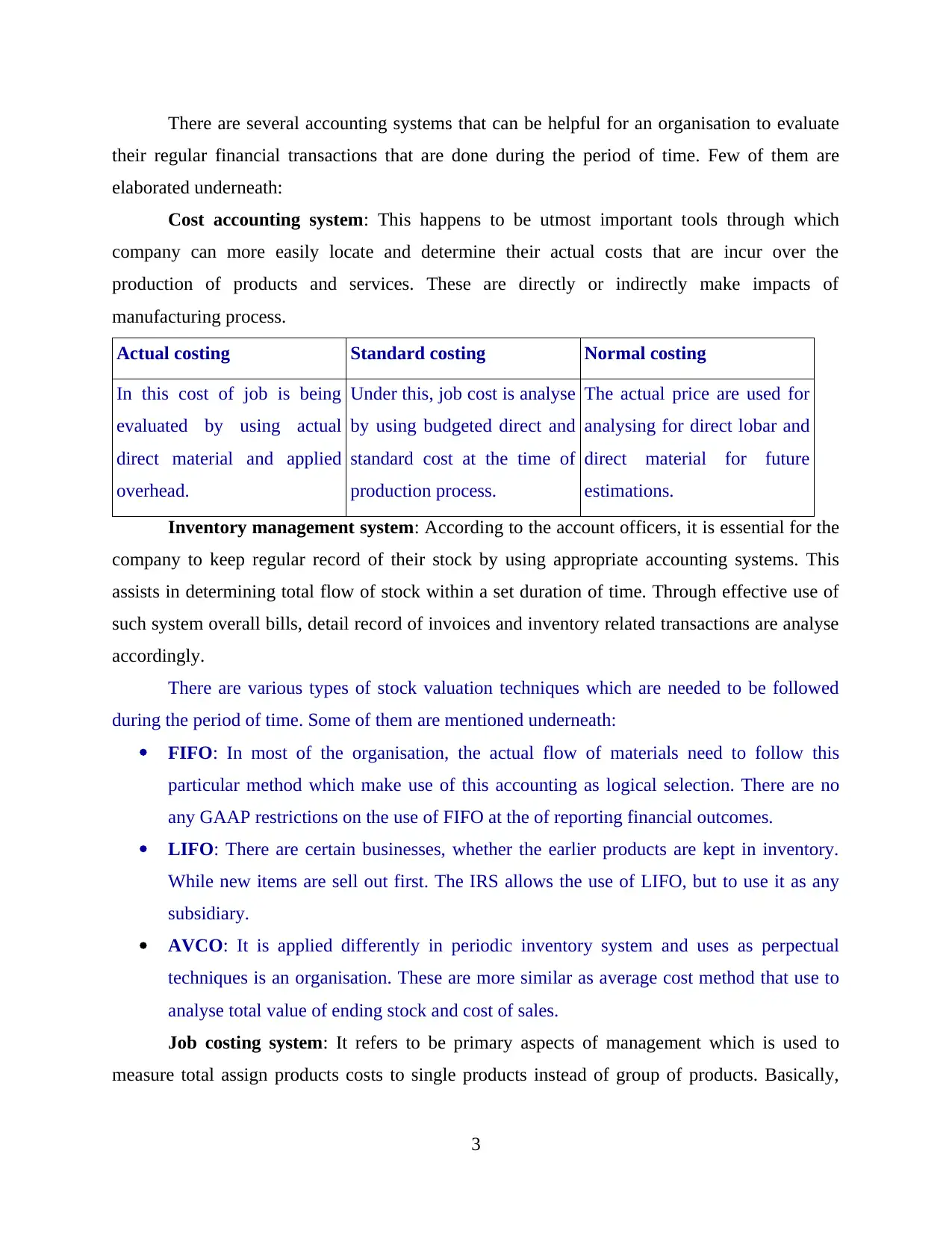

Cost accounting system: This happens to be utmost important tools through which

company can more easily locate and determine their actual costs that are incur over the

production of products and services. These are directly or indirectly make impacts of

manufacturing process.

Actual costing Standard costing Normal costing

In this cost of job is being

evaluated by using actual

direct material and applied

overhead.

Under this, job cost is analyse

by using budgeted direct and

standard cost at the time of

production process.

The actual price are used for

analysing for direct lobar and

direct material for future

estimations.

Inventory management system: According to the account officers, it is essential for the

company to keep regular record of their stock by using appropriate accounting systems. This

assists in determining total flow of stock within a set duration of time. Through effective use of

such system overall bills, detail record of invoices and inventory related transactions are analyse

accordingly.

There are various types of stock valuation techniques which are needed to be followed

during the period of time. Some of them are mentioned underneath:

FIFO: In most of the organisation, the actual flow of materials need to follow this

particular method which make use of this accounting as logical selection. There are no

any GAAP restrictions on the use of FIFO at the of reporting financial outcomes.

LIFO: There are certain businesses, whether the earlier products are kept in inventory.

While new items are sell out first. The IRS allows the use of LIFO, but to use it as any

subsidiary.

AVCO: It is applied differently in periodic inventory system and uses as perpectual

techniques is an organisation. These are more similar as average cost method that use to

analyse total value of ending stock and cost of sales.

Job costing system: It refers to be primary aspects of management which is used to

measure total assign products costs to single products instead of group of products. Basically,

3

their regular financial transactions that are done during the period of time. Few of them are

elaborated underneath:

Cost accounting system: This happens to be utmost important tools through which

company can more easily locate and determine their actual costs that are incur over the

production of products and services. These are directly or indirectly make impacts of

manufacturing process.

Actual costing Standard costing Normal costing

In this cost of job is being

evaluated by using actual

direct material and applied

overhead.

Under this, job cost is analyse

by using budgeted direct and

standard cost at the time of

production process.

The actual price are used for

analysing for direct lobar and

direct material for future

estimations.

Inventory management system: According to the account officers, it is essential for the

company to keep regular record of their stock by using appropriate accounting systems. This

assists in determining total flow of stock within a set duration of time. Through effective use of

such system overall bills, detail record of invoices and inventory related transactions are analyse

accordingly.

There are various types of stock valuation techniques which are needed to be followed

during the period of time. Some of them are mentioned underneath:

FIFO: In most of the organisation, the actual flow of materials need to follow this

particular method which make use of this accounting as logical selection. There are no

any GAAP restrictions on the use of FIFO at the of reporting financial outcomes.

LIFO: There are certain businesses, whether the earlier products are kept in inventory.

While new items are sell out first. The IRS allows the use of LIFO, but to use it as any

subsidiary.

AVCO: It is applied differently in periodic inventory system and uses as perpectual

techniques is an organisation. These are more similar as average cost method that use to

analyse total value of ending stock and cost of sales.

Job costing system: It refers to be primary aspects of management which is used to

measure total assign products costs to single products instead of group of products. Basically,

3

such types of accounting system would always provide information about produced products

which is relatively different from each other (Christ, 2014). Some of them are:

Batch costing: It is an effective form of particular order costing. In this each batch are

marked as number of identical units but every batch will be separate from one another.

Contract costing: It is use to track flow of cost those are asscoaited with a particular

conract with an individual. Like for example a company bids for a wide contruction projects

related to prospective customers.

Process costing: It is mostly use as significant aspects for project management. It is an

essential techniques of allotting costs to units of production in various companies.

Service costing: It is a ncessary metod of operation costing that is used in an organisation

that provide services in accordance of producing products during the time.

P2: (1): Different types of management reporting system

It is the primary motive of every profit generating business is to make use of best

suitable reporting system that can provide them more reliable and healthy outcomes in very less

time period. This would be primary responsibility of managers to look for effective system for

the future development and to control extra costs of TECH UKLtd. They need to record every

financial data that are being incurred during the time and which has been collected from various

department of an organization (Moser, 2012).

By doing so, all these reports are being presented in front of all investors and external

stakeholders those are held liable to make analyses of current financial position of the company.

On that basis, a valuable decision would be made so that further capital investment decisions will

be made in advance by the investors. The data would be recorded by collecting information from

various department or sources. The primary sources of data collection would be taken from

internal department. Some crucial information would be collected from financial or non financial

modes.

There are various types of accounting reporting system which are effectively useful the

company. Some of them are discuss underneath:

Schedule report: It is an important activities that lets company's data from one or more

dashboards on regular or recurring basis. It is more systematic manner of reporting data. It is a

typical report that consists of all assessment of data in order to attain long term aims and

objectives.

4

which is relatively different from each other (Christ, 2014). Some of them are:

Batch costing: It is an effective form of particular order costing. In this each batch are

marked as number of identical units but every batch will be separate from one another.

Contract costing: It is use to track flow of cost those are asscoaited with a particular

conract with an individual. Like for example a company bids for a wide contruction projects

related to prospective customers.

Process costing: It is mostly use as significant aspects for project management. It is an

essential techniques of allotting costs to units of production in various companies.

Service costing: It is a ncessary metod of operation costing that is used in an organisation

that provide services in accordance of producing products during the time.

P2: (1): Different types of management reporting system

It is the primary motive of every profit generating business is to make use of best

suitable reporting system that can provide them more reliable and healthy outcomes in very less

time period. This would be primary responsibility of managers to look for effective system for

the future development and to control extra costs of TECH UKLtd. They need to record every

financial data that are being incurred during the time and which has been collected from various

department of an organization (Moser, 2012).

By doing so, all these reports are being presented in front of all investors and external

stakeholders those are held liable to make analyses of current financial position of the company.

On that basis, a valuable decision would be made so that further capital investment decisions will

be made in advance by the investors. The data would be recorded by collecting information from

various department or sources. The primary sources of data collection would be taken from

internal department. Some crucial information would be collected from financial or non financial

modes.

There are various types of accounting reporting system which are effectively useful the

company. Some of them are discuss underneath:

Schedule report: It is an important activities that lets company's data from one or more

dashboards on regular or recurring basis. It is more systematic manner of reporting data. It is a

typical report that consists of all assessment of data in order to attain long term aims and

objectives.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Exception report: It is a list of abnormal products or items that included outside of

particular range. This kind of reports are strictly prohibited without permission from the owners.

Demand report: It is a kind of report that is not pre planned, but formulated on the

requirement of interested parties. This seems that demand for course at the concluding of the

scheduler are pre-recorded under this report.

Performance report: It is one of the most essential report that are use for the purpose of

making comparison among actual outcomes with the standard one. In order to do so, managers

need to be making use of past data and make evaluation with present one. This will determine

real position of the company. All those issues that are arises in an organisation can be resolve

before making posting of the data into this statements.

Inventory management report: This kind of accounting reports consists of all vital

information about inventory position of the company. Such as opening and closing record of

stock that a company has kept in their warehouse are posted as per their data of occurrence. As it

has been observed that inventory is primary part of any manufacturing business that leads to

increase of overall growth and efficiency at the same point of time. There are various techniques

are being used by the accountant to record detail information about stocks such as inventory

turnover ratios, ABC costing and LIFO and FIFO method.

Account receivable report: According to this particular report every information which

is related with total lists of unpaid customers those are due for payment are determine under this

report. Through using this reporting system, a company can easily be able to analyse exact

timing of amount recovery which are being overdue for the payment.

Job cost report: Such kind of reports assist for evaluating vital records of product

manufacturing related information’s. This will be used to identify overall costs which they are

going to incur for producing one unit of products of group of products. Through this company

can easily be able to analyse their every day job costs and operations expenses.

Operational budget report: As per this report, every data regarding their total costs and

expenses that are invested during the manufacturing of goods are recorded properly. Such kind

of reports would be summarised by collected information about sales, production purchase, raw

material consumed and allocation of resources during that time (Hilton and Platt, 2013).

II): Importance of reporting methods

5

particular range. This kind of reports are strictly prohibited without permission from the owners.

Demand report: It is a kind of report that is not pre planned, but formulated on the

requirement of interested parties. This seems that demand for course at the concluding of the

scheduler are pre-recorded under this report.

Performance report: It is one of the most essential report that are use for the purpose of

making comparison among actual outcomes with the standard one. In order to do so, managers

need to be making use of past data and make evaluation with present one. This will determine

real position of the company. All those issues that are arises in an organisation can be resolve

before making posting of the data into this statements.

Inventory management report: This kind of accounting reports consists of all vital

information about inventory position of the company. Such as opening and closing record of

stock that a company has kept in their warehouse are posted as per their data of occurrence. As it

has been observed that inventory is primary part of any manufacturing business that leads to

increase of overall growth and efficiency at the same point of time. There are various techniques

are being used by the accountant to record detail information about stocks such as inventory

turnover ratios, ABC costing and LIFO and FIFO method.

Account receivable report: According to this particular report every information which

is related with total lists of unpaid customers those are due for payment are determine under this

report. Through using this reporting system, a company can easily be able to analyse exact

timing of amount recovery which are being overdue for the payment.

Job cost report: Such kind of reports assist for evaluating vital records of product

manufacturing related information’s. This will be used to identify overall costs which they are

going to incur for producing one unit of products of group of products. Through this company

can easily be able to analyse their every day job costs and operations expenses.

Operational budget report: As per this report, every data regarding their total costs and

expenses that are invested during the manufacturing of goods are recorded properly. Such kind

of reports would be summarised by collected information about sales, production purchase, raw

material consumed and allocation of resources during that time (Hilton and Platt, 2013).

II): Importance of reporting methods

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per the above mentioned significant reports, it has been seen that organisation

required to record all essential financial data in their respective statements. Through preformance

report, managers would be able to analyse overall performance by comparising actual data with

the past one. Whereas accounting receivable report should lead to determine exact time to gather

overdue payments from various persons. Inventory management reprort would be liable to

manage and control overall stock positions kept by the company.

M1: Benefits of using management accounting system

It has been seen that wide organisation are mainly using more reliable systems that can

assists in summating data as per their data of transactions. By doing this, chances of mistakes

would be minimise up to a extent. There are various crucial advantages of using those above

mentioned accounting systems. By the use of cost accounting systems, total flow of cash in the

business can easily be analysed. Whereas with having inventory management tools managers can

easily be able to record and maintain balance in their stock level. All of them are held

responsible for increase overall productivity of the company.

D1: Critical evaluation of accounting reporting systems

As per the above mentioned various types of accounting reports, it has been examine that

all of them are held responsible for generating maximum return for the company. If managers

use to record financial information in accurate and reliable manner they are in very less period of

time can attain their set aims and objectives. In respect to this, performance report would be

analysing in more effectively so that exact detail information about company’s financial position

would easily be determine. Whereas by the use of account receivable report company can

identify exact time and date of total overdue payments. It has been analyse that managers do

have two options such as accounting system which is liable to evalaute financial information

during the time. While reportingis basic system that is held responsible for recording of all

financial data in theri respective format. This seems to be more favourble techniques for the

company.

6

required to record all essential financial data in their respective statements. Through preformance

report, managers would be able to analyse overall performance by comparising actual data with

the past one. Whereas accounting receivable report should lead to determine exact time to gather

overdue payments from various persons. Inventory management reprort would be liable to

manage and control overall stock positions kept by the company.

M1: Benefits of using management accounting system

It has been seen that wide organisation are mainly using more reliable systems that can

assists in summating data as per their data of transactions. By doing this, chances of mistakes

would be minimise up to a extent. There are various crucial advantages of using those above

mentioned accounting systems. By the use of cost accounting systems, total flow of cash in the

business can easily be analysed. Whereas with having inventory management tools managers can

easily be able to record and maintain balance in their stock level. All of them are held

responsible for increase overall productivity of the company.

D1: Critical evaluation of accounting reporting systems

As per the above mentioned various types of accounting reports, it has been examine that

all of them are held responsible for generating maximum return for the company. If managers

use to record financial information in accurate and reliable manner they are in very less period of

time can attain their set aims and objectives. In respect to this, performance report would be

analysing in more effectively so that exact detail information about company’s financial position

would easily be determine. Whereas by the use of account receivable report company can

identify exact time and date of total overdue payments. It has been analyse that managers do

have two options such as accounting system which is liable to evalaute financial information

during the time. While reportingis basic system that is held responsible for recording of all

financial data in theri respective format. This seems to be more favourble techniques for the

company.

6

TASK 2

P3: Various types of costing methods which are use for calculating net profit

In every business, costs play an eminent role during production of products and services.

It is an essential part of an organisation to make use to their total costs in right manner so that it

would not increase extra expense for the company. This is necessary for managers to make use

of microeconomic factors in their daily business to generate more reliable outcomes. This is an

effective part which would assist in determining whether resources of the company are utilised in

proper manner. This will help entire operational department to make desirable and economic

reputation within an organisation. In respect to get more effective outcomes within a definite set

of time the company may require to control their unnecessary cost and expenses those are incur

in their regular cost of productions (Becker, Ulrich and Staffel, 2011).

Cost is said to be amount of value charged in respect to get something. These are directly

or indirectly related with production of goods and services. This will enhance maximum burden

over employees to give their best efforts to increase profitability for the company in very least

time. It has been observed that without having proper flow of funds management cannot be able

to take valuable decision for their upcoming projects. The will make huge impacts on their desire

aims and objectives. There are various costing methods which could effectively utilised by

TECH Ltd in their business to determine total net profitability of the company. Few of them are

discuss below:

Cost volume profit (CVP): It is an essential techniques which is being use to measure

various modification in respect to total cost and volume that can affect companies overall

operating earnings as well as net flexible aspects.

Flexible budgeting: This is said to be an adjusted techniques which alter in more reliable

manner and make use as static budgets. It can varies with the changes in output those are flexible

in nature.

Cost variance: It is an essential or more simple for making comparison between actual

cost value and their budgeted amount. This would assist to make analysis of all those changes

those are incur during production process.

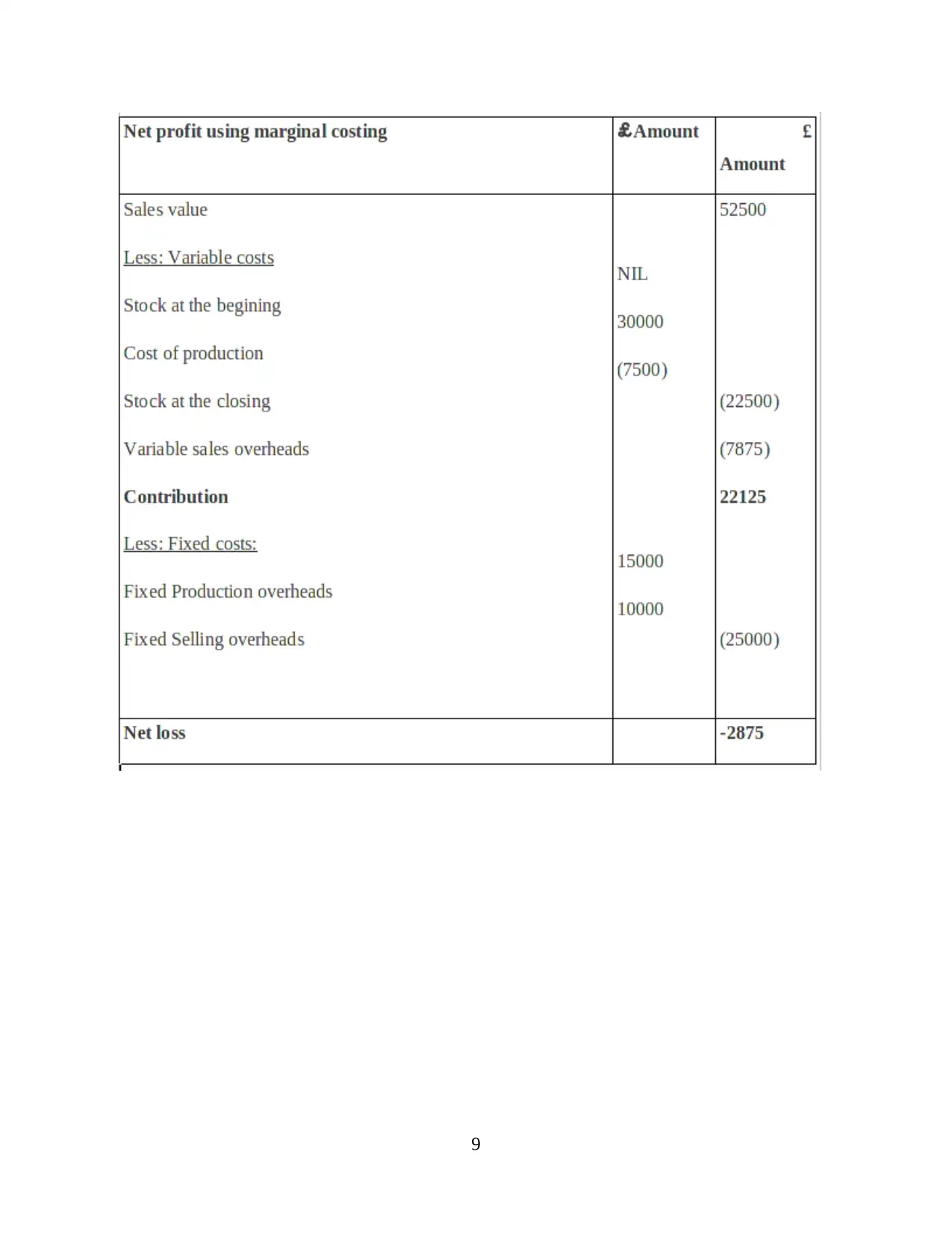

Marginal costing: It is known as those costing techniques which is use for production of

one additional unit. These are mainly conclude variable costs not fixed because of this nature, it

7

P3: Various types of costing methods which are use for calculating net profit

In every business, costs play an eminent role during production of products and services.

It is an essential part of an organisation to make use to their total costs in right manner so that it

would not increase extra expense for the company. This is necessary for managers to make use

of microeconomic factors in their daily business to generate more reliable outcomes. This is an

effective part which would assist in determining whether resources of the company are utilised in

proper manner. This will help entire operational department to make desirable and economic

reputation within an organisation. In respect to get more effective outcomes within a definite set

of time the company may require to control their unnecessary cost and expenses those are incur

in their regular cost of productions (Becker, Ulrich and Staffel, 2011).

Cost is said to be amount of value charged in respect to get something. These are directly

or indirectly related with production of goods and services. This will enhance maximum burden

over employees to give their best efforts to increase profitability for the company in very least

time. It has been observed that without having proper flow of funds management cannot be able

to take valuable decision for their upcoming projects. The will make huge impacts on their desire

aims and objectives. There are various costing methods which could effectively utilised by

TECH Ltd in their business to determine total net profitability of the company. Few of them are

discuss below:

Cost volume profit (CVP): It is an essential techniques which is being use to measure

various modification in respect to total cost and volume that can affect companies overall

operating earnings as well as net flexible aspects.

Flexible budgeting: This is said to be an adjusted techniques which alter in more reliable

manner and make use as static budgets. It can varies with the changes in output those are flexible

in nature.

Cost variance: It is an essential or more simple for making comparison between actual

cost value and their budgeted amount. This would assist to make analysis of all those changes

those are incur during production process.

Marginal costing: It is known as those costing techniques which is use for production of

one additional unit. These are mainly conclude variable costs not fixed because of this nature, it

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is said be period costing method. Most of the investors use to take these techniques more reliable

for making valuable decision for their business projects.

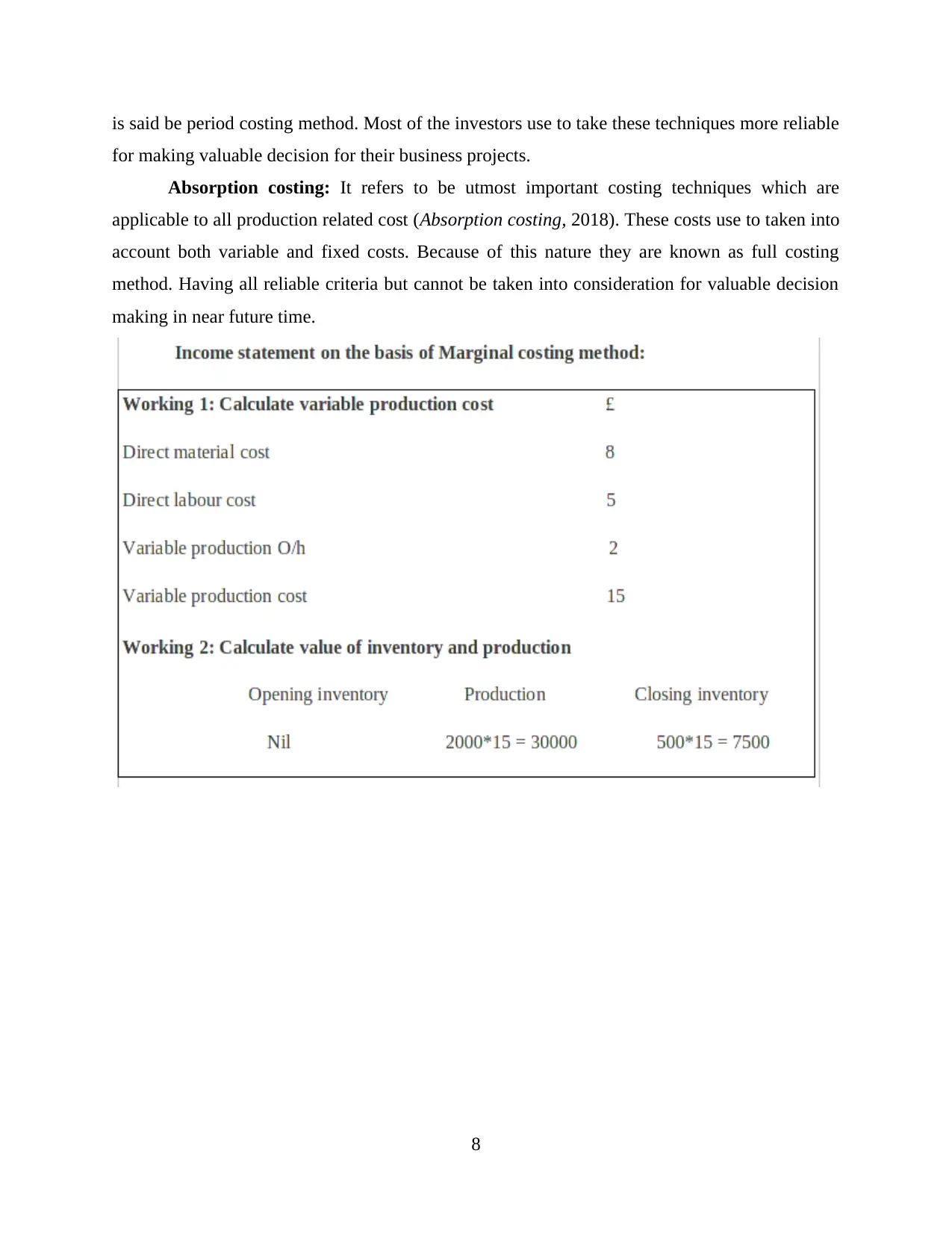

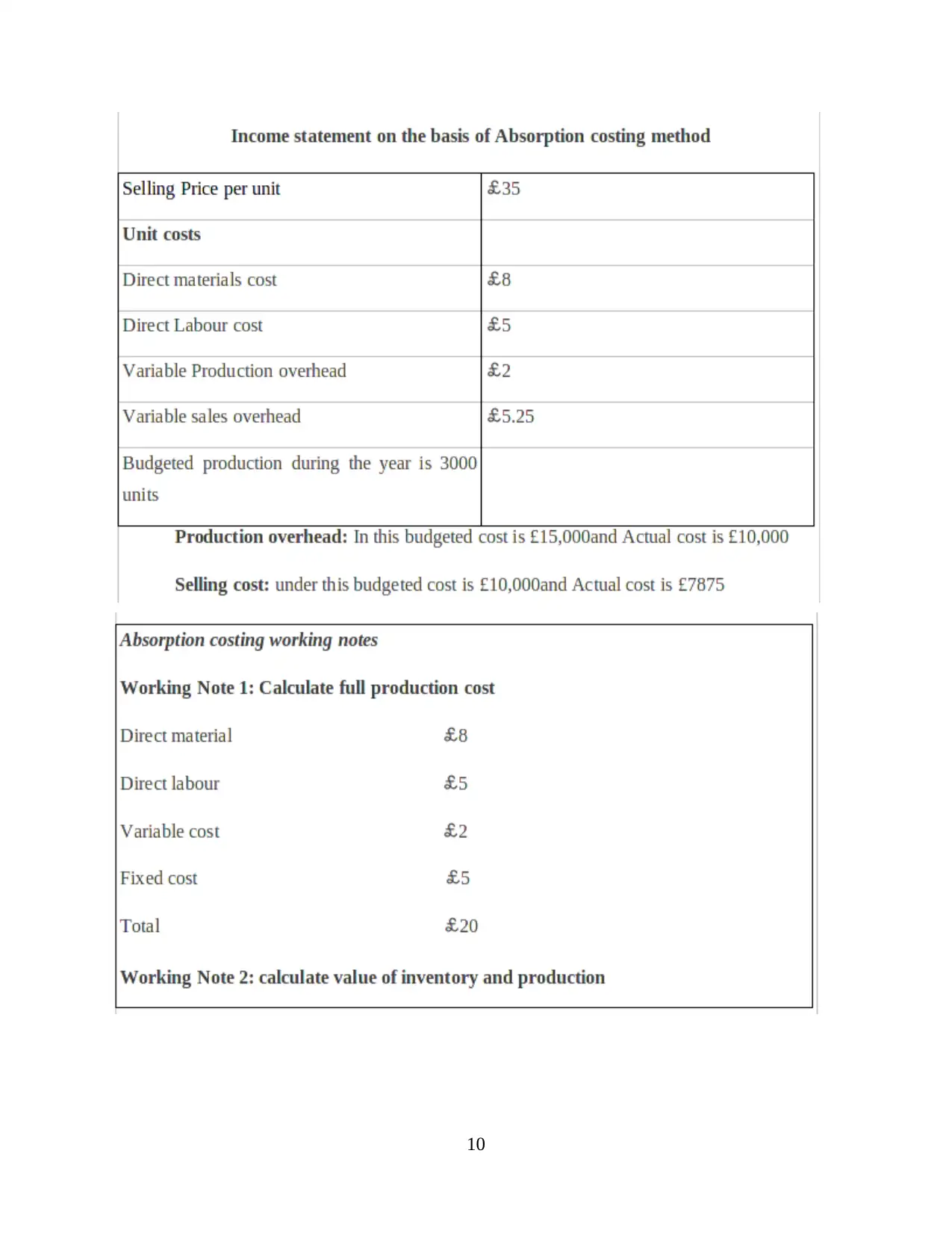

Absorption costing: It refers to be utmost important costing techniques which are

applicable to all production related cost (Absorption costing, 2018). These costs use to taken into

account both variable and fixed costs. Because of this nature they are known as full costing

method. Having all reliable criteria but cannot be taken into consideration for valuable decision

making in near future time.

8

for making valuable decision for their business projects.

Absorption costing: It refers to be utmost important costing techniques which are

applicable to all production related cost (Absorption costing, 2018). These costs use to taken into

account both variable and fixed costs. Because of this nature they are known as full costing

method. Having all reliable criteria but cannot be taken into consideration for valuable decision

making in near future time.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.