Management Accounting Report: Systems, Reporting, and Costing Analysis

VerifiedAdded on 2020/06/05

|18

|5512

|35

Report

AI Summary

This report, prepared for Taj Stores, a London-based grocery shop, provides a comprehensive overview of management accounting systems and reporting methods. It explores various aspects, including the differences between financial and management accounting, and the application of systems such as price optimization, cost accounting, inventory management, and job costing. The report delves into different management accounting reporting methods, such as account receivable, accounts payable, inventory control, performance, and budget reporting. It also highlights the advantages and disadvantages of planning tools used for budgetary control and addresses the application of management accounting systems in responding to financial troubles. The analysis includes a comparison between marginal and absorption costing, offering valuable insights into their applications. Overall, the report aims to equip the organization with the knowledge necessary to effectively implement management accounting practices for improved financial management and decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting system and essential requirements of its different types..............1

P2 Methods of management accounting reporting......................................................................4

TASK 2............................................................................................................................................7

P3 Difference between income statement made through marginal and absorption costing........7

TASK 3 ........................................................................................................................................10

P4 Advantages and disadvantages of planning tools which are used for budgetary control....10

P5 Adopting management accounting systems for responding financial troubles .................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting system and essential requirements of its different types..............1

P2 Methods of management accounting reporting......................................................................4

TASK 2............................................................................................................................................7

P3 Difference between income statement made through marginal and absorption costing........7

TASK 3 ........................................................................................................................................10

P4 Advantages and disadvantages of planning tools which are used for budgetary control....10

P5 Adopting management accounting systems for responding financial troubles .................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

Report

From: Management Accounting Officer

To: General Manager

Subject: Report covering management accounting system and reporting along with different

costing techniques for enabling organization to implement them.

From: Management Accounting Officer

To: General Manager

Subject: Report covering management accounting system and reporting along with different

costing techniques for enabling organization to implement them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The system of recoding, analysing and using financial data and non-financial information

is known as management accounting. In the modern business era, companies are facing different

kinds of problems relating to managing their resources (Ahmad and Mohamed Zabri, 2012).

Managerial accounting focuses on expertise and assists an organisation in increasing their profit

by lower down the overall cost of operations and other activities. It also helps managers in

expanding enterprises by finding new ways of enhancing sales. There is a big difference between

management and financial accounting where first one is for growth of business while other is for

external stakeholders. Taj stores is situated in London. They are running a grocery shop which

started in the year 1936. Their employee’s strength is less than 50 and turnover is below 500000

pounds. This project will give complete explanation about different management accounting

systems. Some reporting methods will also become an important part of this assignment. Major

difference between marginal and absorption costing will get covered in the mid part of this

report. There are various planning tools which manager can use for controlling the budget and all

will be explained in this file (Aminbakhsh, Gunduz and Sonmez, 2013). At the end, this project

will talk about financial problems and their solution by management accounting tools and

techniques.

TASK 1

P1. Management accounting system and essential requirements of its different types

Making profit in this business world is not a difficult task if an organisation knows all

correct manner of managing all available resources. There was an era when companies try to

focus only on their financial activities because they think that if they will manage monetary fund

properly then they can find out solution of most of their troubles. But, with time, new business

issues have raised because of various reasons like globalisation and swift changes in rules made

by government, high competition, etc. Management accounting has many perks that assist in

forecasting and playing a crucial role at the time of making decisions relating to buying or sale of

investments. Cash is an important asset of company and tools of managerial accounts predict

need of this liquid asset at a particular time period. Financial accounting is mainly used for

showing stakeholders that firm has successfully achieved mentioned goals and if they fail to

reach these targets (Chen, Weikart and Williams, 2014). There are many differences between

managerial and financial accounts that are shown as below:

1

The system of recoding, analysing and using financial data and non-financial information

is known as management accounting. In the modern business era, companies are facing different

kinds of problems relating to managing their resources (Ahmad and Mohamed Zabri, 2012).

Managerial accounting focuses on expertise and assists an organisation in increasing their profit

by lower down the overall cost of operations and other activities. It also helps managers in

expanding enterprises by finding new ways of enhancing sales. There is a big difference between

management and financial accounting where first one is for growth of business while other is for

external stakeholders. Taj stores is situated in London. They are running a grocery shop which

started in the year 1936. Their employee’s strength is less than 50 and turnover is below 500000

pounds. This project will give complete explanation about different management accounting

systems. Some reporting methods will also become an important part of this assignment. Major

difference between marginal and absorption costing will get covered in the mid part of this

report. There are various planning tools which manager can use for controlling the budget and all

will be explained in this file (Aminbakhsh, Gunduz and Sonmez, 2013). At the end, this project

will talk about financial problems and their solution by management accounting tools and

techniques.

TASK 1

P1. Management accounting system and essential requirements of its different types

Making profit in this business world is not a difficult task if an organisation knows all

correct manner of managing all available resources. There was an era when companies try to

focus only on their financial activities because they think that if they will manage monetary fund

properly then they can find out solution of most of their troubles. But, with time, new business

issues have raised because of various reasons like globalisation and swift changes in rules made

by government, high competition, etc. Management accounting has many perks that assist in

forecasting and playing a crucial role at the time of making decisions relating to buying or sale of

investments. Cash is an important asset of company and tools of managerial accounts predict

need of this liquid asset at a particular time period. Financial accounting is mainly used for

showing stakeholders that firm has successfully achieved mentioned goals and if they fail to

reach these targets (Chen, Weikart and Williams, 2014). There are many differences between

managerial and financial accounts that are shown as below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting Management accounting

Its main aim is to convey the performance of

company to stakeholders.

It is made by managers of the firm so that they

can analyse different kinds of data and make

right decisions.

Principles of GAAP are applied for making

various reports.

There are known principles and organisation

can make it in any possible way which they

want.

Only quantitative data is used in financial

accounting.

Both qualitative and quantitative data are

utilised in managerial accounts.

All the departments are covered in this section. Specific division, which is relevant to

profitability, are taken in account in this

process.

Complete information or data in these accounts

is highly accurate.

Sometimes, information is present in

approximate figures.

Small enterprises always face problems relating to funding. As they know that they

cannot get much funds so, manager of these firms Taj stores focuses on different management

accounting systems which can assist them in different areas of business. They are as follows:

Price optimisation – Production cost of every item is different. Their market rate is also

dependent on manufacturing expenses. This system plays the key role on decision price of

various products which prove to be the best for customers as well as company. Buyers never buy

a good, rate of which is high for them. This ultimately results in low sales as well as profits also.

Other option for enterprise is that they can sell it at low value but, in this case, organisation

would not earn a decent amount of revenue and they will miss their short and long term targets.

Cost accounting system – Significance of costing has grown in the past two decades as

many multi-national corporation like Toyota earned benefit of competitive advantage by working

on different methods for reducing cost of production. This management accounting system is

capable of increasing the profit by identifying and removing wastage of resources. It also

2

Its main aim is to convey the performance of

company to stakeholders.

It is made by managers of the firm so that they

can analyse different kinds of data and make

right decisions.

Principles of GAAP are applied for making

various reports.

There are known principles and organisation

can make it in any possible way which they

want.

Only quantitative data is used in financial

accounting.

Both qualitative and quantitative data are

utilised in managerial accounts.

All the departments are covered in this section. Specific division, which is relevant to

profitability, are taken in account in this

process.

Complete information or data in these accounts

is highly accurate.

Sometimes, information is present in

approximate figures.

Small enterprises always face problems relating to funding. As they know that they

cannot get much funds so, manager of these firms Taj stores focuses on different management

accounting systems which can assist them in different areas of business. They are as follows:

Price optimisation – Production cost of every item is different. Their market rate is also

dependent on manufacturing expenses. This system plays the key role on decision price of

various products which prove to be the best for customers as well as company. Buyers never buy

a good, rate of which is high for them. This ultimately results in low sales as well as profits also.

Other option for enterprise is that they can sell it at low value but, in this case, organisation

would not earn a decent amount of revenue and they will miss their short and long term targets.

Cost accounting system – Significance of costing has grown in the past two decades as

many multi-national corporation like Toyota earned benefit of competitive advantage by working

on different methods for reducing cost of production. This management accounting system is

capable of increasing the profit by identifying and removing wastage of resources. It also

2

provides information about profitability by analysing various factors which are unnecessarily

enhancing the total cost (Cokins, 2013).

Inventory management system – Taj stores is a small firm; they do not have much

employees. If they will use inventory management software then they can keep all the records

relating to goods that have entered in stores and that are present in warehouses. This system

delivers information about the right quantity of goods that an organisation should keep in the

store. Tracking of all commodities can be done by using this technique. If manager of Taj stores

will buy this software then they will get an exact idea about the profitability of every product

which they are selling in their shop. All the problems regarding supply chain can get resolved if

an organisation adopts this system (Zoni, Dossi and Morelli, 2012). Latest technology can be

considered as an essential requirement for this management accounting procedure but small

enterprise can also use old software as their area of operations is limited.

Job costing – This system gained popularity in the last few years because it directly

makes a positive impact on the profitability of business. In job costing, contribution in profit of

every 'job' is checked so that manager can identify all work which is increasing revenue and

decreasing 'Jobs' which are not important for company and putting burden of additional cost on

organisation.

3

Management

Accounting

system

Inventory

management

System

Cost

Accounting System

Job Costing Price

Optimisation

enhancing the total cost (Cokins, 2013).

Inventory management system – Taj stores is a small firm; they do not have much

employees. If they will use inventory management software then they can keep all the records

relating to goods that have entered in stores and that are present in warehouses. This system

delivers information about the right quantity of goods that an organisation should keep in the

store. Tracking of all commodities can be done by using this technique. If manager of Taj stores

will buy this software then they will get an exact idea about the profitability of every product

which they are selling in their shop. All the problems regarding supply chain can get resolved if

an organisation adopts this system (Zoni, Dossi and Morelli, 2012). Latest technology can be

considered as an essential requirement for this management accounting procedure but small

enterprise can also use old software as their area of operations is limited.

Job costing – This system gained popularity in the last few years because it directly

makes a positive impact on the profitability of business. In job costing, contribution in profit of

every 'job' is checked so that manager can identify all work which is increasing revenue and

decreasing 'Jobs' which are not important for company and putting burden of additional cost on

organisation.

3

Management

Accounting

system

Inventory

management

System

Cost

Accounting System

Job Costing Price

Optimisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application of management accounting system to the chosen company:

Price optimisation - Taj stores are selling many items in their shop and by using this

system, they can decide the right price of every product. This will positive affect their profit can

their number of customer will also increase because they will find goods at a price which they

can happily pay (Renz, 2016).

Cost accounting system – Taj stores can apply this system for identifying various areas

where they can decrease wastage of resources. If they will adopt it then their total cost of doing

business will go down and profit will go up.

Inventory management system – For a grocery store, managing stock is very important

because it is directly connected to their sales. By using this system, they can keep right good and

their proper quantity in the stores.

Job costing – Some ''jobs'' at Taj stores may not have any major role in earning profit.

This report can identify these jobs and increase those ''jobs'' who have ability to enhance more

profit of the company.

P2 Methods of management accounting reporting

Management accounting reporting is the process of presenting different kind of reports to

the manager so they can analyse them and, in future, make effective plans by using it (Delafrooz

and Paim, 2011). Report shows all the activities which is done by the company in past period but

for a particular time. Below is the importance of management accounting reporting:

It assist managers in finding various kind of mistakes which company is committing

regarding managing inventory, debtors and creditors.

These reports can be used for making future strategies so strong plans can be made for

achieving long term goals.

These reports support all the divisions and they assist in forming a systematic procedure

so all the work can be done in best way possible.

Following are some popular type of management accounting reports along with their importance:

4

Price optimisation - Taj stores are selling many items in their shop and by using this

system, they can decide the right price of every product. This will positive affect their profit can

their number of customer will also increase because they will find goods at a price which they

can happily pay (Renz, 2016).

Cost accounting system – Taj stores can apply this system for identifying various areas

where they can decrease wastage of resources. If they will adopt it then their total cost of doing

business will go down and profit will go up.

Inventory management system – For a grocery store, managing stock is very important

because it is directly connected to their sales. By using this system, they can keep right good and

their proper quantity in the stores.

Job costing – Some ''jobs'' at Taj stores may not have any major role in earning profit.

This report can identify these jobs and increase those ''jobs'' who have ability to enhance more

profit of the company.

P2 Methods of management accounting reporting

Management accounting reporting is the process of presenting different kind of reports to

the manager so they can analyse them and, in future, make effective plans by using it (Delafrooz

and Paim, 2011). Report shows all the activities which is done by the company in past period but

for a particular time. Below is the importance of management accounting reporting:

It assist managers in finding various kind of mistakes which company is committing

regarding managing inventory, debtors and creditors.

These reports can be used for making future strategies so strong plans can be made for

achieving long term goals.

These reports support all the divisions and they assist in forming a systematic procedure

so all the work can be done in best way possible.

Following are some popular type of management accounting reports along with their importance:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Account receivable reporting – This report is made for finding the amount which

debtors will give to the company. It contain whole details about how much money organisation

has receivable up-to a particular date and what are source of these funds. Making this report is

essential for enterprises because it assist them in managing the monetary resources is right

manner. The prime important of this report is that it can reduce the amount of bad debt by

finding and making hard rules for debtors who are not paying the money which they have have

to pay for purchased good to the firm. This report can be used at the time of calculating the need

of cash in business.

Accounting payable reporting – Every company have some suppliers. These are

stakeholders who play crucial role in success or failure of enterprise because the raw material or

goods supplied by them are sold to the customer. Under this report, information about amount

which company has paid to creditors is mentioned and it also shows data of the sum which

company have to pay to their supplier in upcoming time. Major significant of this report is that it

can assist in making a procedure where company pay due amount to their creditor is promised

time. This make a huge positive impact on relationship between organisation and their suppliers

(Ekbatani and Sangeladji, 2011). Having good relationship with vendors help in forming strong

supply chain management. A/C payable has high significance in finding right supplier for

company i.e. who provide good quality of goods at low price.

Inventory control reporting – Inventory is the unsold goods which is company want to

sell to their customers. This report reveal data regarding stock which was sold in a period of time

and unsold inventory which is present in warehouse. Performance of some important techniques

of managing stock like EOQ is checked under this report. Main advantage and use of this report

is that it can resolve most of the major troubles relating to overstocking and under-stocking of

goods. By utilising this document, company can analyse the demand of particular good which

they should should keep and sale in their stores. They will also get information about right time

and exact quantity of goods which should be ordered by enterprise.

Performance reporting – Analysing performance of every department and employees is

main target of this form of reporting. Making it is important because company can use it at the

time of deciding incentives and promotion of workers. Every division has some target, this report

depict whether they have reached it or not and how close or far they were to the aim. If

5

debtors will give to the company. It contain whole details about how much money organisation

has receivable up-to a particular date and what are source of these funds. Making this report is

essential for enterprises because it assist them in managing the monetary resources is right

manner. The prime important of this report is that it can reduce the amount of bad debt by

finding and making hard rules for debtors who are not paying the money which they have have

to pay for purchased good to the firm. This report can be used at the time of calculating the need

of cash in business.

Accounting payable reporting – Every company have some suppliers. These are

stakeholders who play crucial role in success or failure of enterprise because the raw material or

goods supplied by them are sold to the customer. Under this report, information about amount

which company has paid to creditors is mentioned and it also shows data of the sum which

company have to pay to their supplier in upcoming time. Major significant of this report is that it

can assist in making a procedure where company pay due amount to their creditor is promised

time. This make a huge positive impact on relationship between organisation and their suppliers

(Ekbatani and Sangeladji, 2011). Having good relationship with vendors help in forming strong

supply chain management. A/C payable has high significance in finding right supplier for

company i.e. who provide good quality of goods at low price.

Inventory control reporting – Inventory is the unsold goods which is company want to

sell to their customers. This report reveal data regarding stock which was sold in a period of time

and unsold inventory which is present in warehouse. Performance of some important techniques

of managing stock like EOQ is checked under this report. Main advantage and use of this report

is that it can resolve most of the major troubles relating to overstocking and under-stocking of

goods. By utilising this document, company can analyse the demand of particular good which

they should should keep and sale in their stores. They will also get information about right time

and exact quantity of goods which should be ordered by enterprise.

Performance reporting – Analysing performance of every department and employees is

main target of this form of reporting. Making it is important because company can use it at the

time of deciding incentives and promotion of workers. Every division has some target, this report

depict whether they have reached it or not and how close or far they were to the aim. If

5

organisation will not make this document then they will never know how their employees

performed and what blunder they have committed in particular time period.

Budget reporting – Budget is most common from of report. It is important to make this

report as it provide all the information about company's work and performance and it also reveal

income and expenditure both expected and actual. Prime use of this report is done in finding

deviation. This report is important because it assist in making future strategies. It company

would not make this document then their whole operation can go off the right track.

Applying management accounting reporting to chosen firm

Account receivable report – Taj stores can decrease the amount of their bad debts by

constructing this report. If they make it, then they can find debtor who are regular defaulter and

they may take decision to not sell good to them on credit (Foster, Hart and Lewis, 2011).

Account payable report – Formation of A/C payable report show details about supplier

who can be trusted. It will also provide all the information about payable and paid sum to

vendors. By using this report, Taj stores can make payment to their vendor on decided day and

this will result in fine relationship with them.

Performance report – Taj stores do not have more than 50 employees. Performance

report will assist them in analysing employees and other division work so their promotion can be

done accordingly and their incentives can be decided for upcoming time.

Budget report – Taj stores may have some problem for making budget report because it

is bit expensive and time consuming but they should make it as it will show them right path to

6

Methods of Management Accounting Report

Budget Report

Accounts receivable

Report

Inventory

control report

Account payable

report

Performance report

performed and what blunder they have committed in particular time period.

Budget reporting – Budget is most common from of report. It is important to make this

report as it provide all the information about company's work and performance and it also reveal

income and expenditure both expected and actual. Prime use of this report is done in finding

deviation. This report is important because it assist in making future strategies. It company

would not make this document then their whole operation can go off the right track.

Applying management accounting reporting to chosen firm

Account receivable report – Taj stores can decrease the amount of their bad debts by

constructing this report. If they make it, then they can find debtor who are regular defaulter and

they may take decision to not sell good to them on credit (Foster, Hart and Lewis, 2011).

Account payable report – Formation of A/C payable report show details about supplier

who can be trusted. It will also provide all the information about payable and paid sum to

vendors. By using this report, Taj stores can make payment to their vendor on decided day and

this will result in fine relationship with them.

Performance report – Taj stores do not have more than 50 employees. Performance

report will assist them in analysing employees and other division work so their promotion can be

done accordingly and their incentives can be decided for upcoming time.

Budget report – Taj stores may have some problem for making budget report because it

is bit expensive and time consuming but they should make it as it will show them right path to

6

Methods of Management Accounting Report

Budget Report

Accounts receivable

Report

Inventory

control report

Account payable

report

Performance report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

follow and work of all the employees can be synchronised by removing confusing and conflict.

Separate funds are allotted to every wing or worker in under this budget.

Inventory control report – All the issues of Taj stores regarding extra stock or scarcity

of inventory can get resolve by taking use of inventory report.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

In today's business environment, income statement can be made by adopt different

management accounting techniques like marginal and absorption costing. Prior one is modern

concept and it concentration on assisting in making managerial decisions while later one only

deal with production activity (Fullerton, Kennedy and Widener, 2014).

Marginal costing – In this technique of management accounting expenditure incurred on

manufacturing of additional goods is taken in account. Variable cost is treated according to the

cost unit but fixed expenses fully written off from total contribution.

Absorption costing – It does not matter whether an expenditure is fixed or variable, under

this management account technique, all the expenses is considered for product cost. Allocation

of cost per produced unit is the main concept behind absorption costing.

Marginal costing Absorption costing

Inventory is valued by considering only

variable cost.

For inventory valuation, total cost is taken in

account under this technique.

Accounting standards do not allow this

technique for valuation of stock if, it is to be

submitted to government authority.

This approach can be adopted by a company

for valuation of inventory because it is

permitted under accounting standards.

It is formed for internal use i.e. for making

right decisions.

Absorption costing is for external users.

Fixed cost is taken as period cost. Fixed cost is part of product cost of each unit.

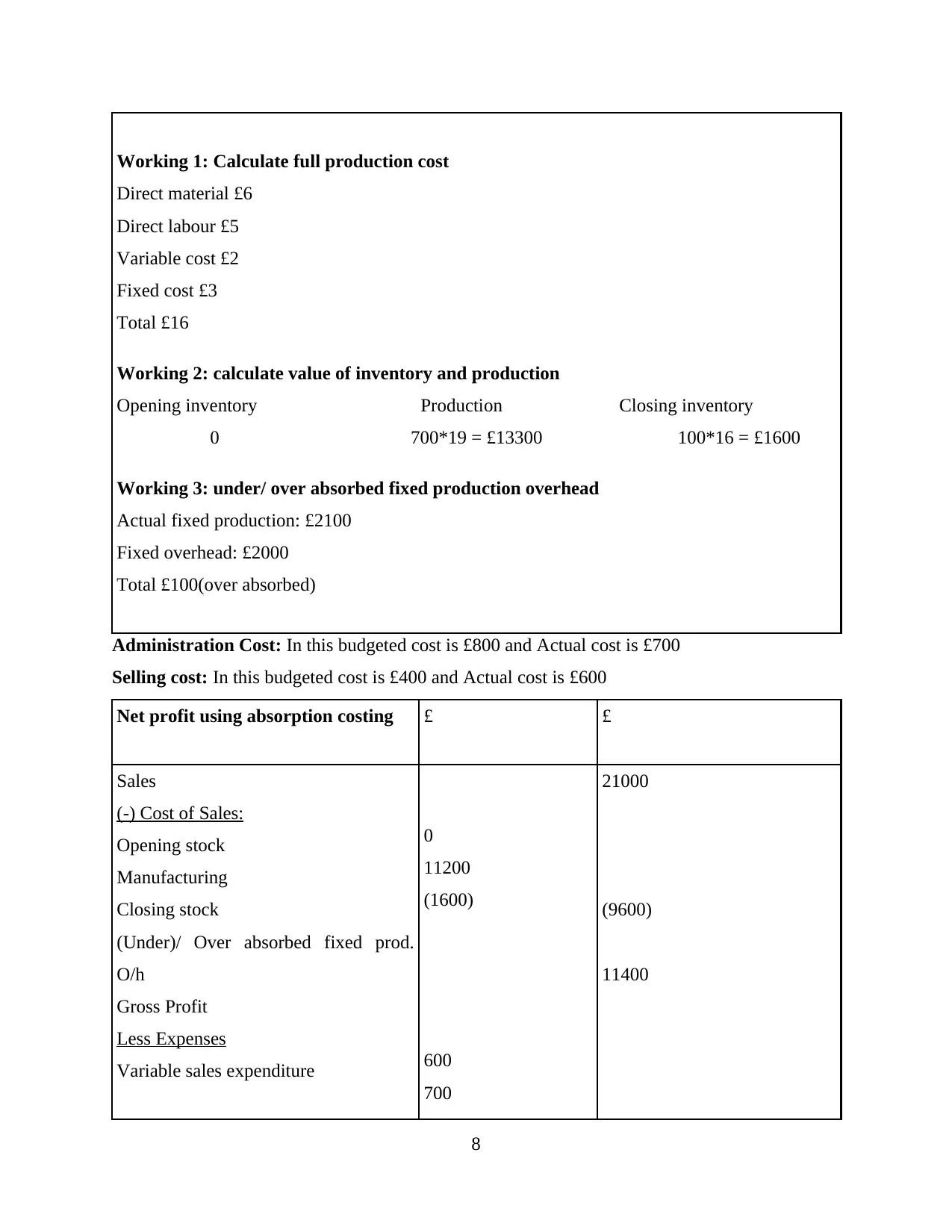

Calculation as per Absorption costing.

Working notes:

Absorption costing

7

Separate funds are allotted to every wing or worker in under this budget.

Inventory control report – All the issues of Taj stores regarding extra stock or scarcity

of inventory can get resolve by taking use of inventory report.

TASK 2

P3 Difference between income statement made through marginal and absorption costing

In today's business environment, income statement can be made by adopt different

management accounting techniques like marginal and absorption costing. Prior one is modern

concept and it concentration on assisting in making managerial decisions while later one only

deal with production activity (Fullerton, Kennedy and Widener, 2014).

Marginal costing – In this technique of management accounting expenditure incurred on

manufacturing of additional goods is taken in account. Variable cost is treated according to the

cost unit but fixed expenses fully written off from total contribution.

Absorption costing – It does not matter whether an expenditure is fixed or variable, under

this management account technique, all the expenses is considered for product cost. Allocation

of cost per produced unit is the main concept behind absorption costing.

Marginal costing Absorption costing

Inventory is valued by considering only

variable cost.

For inventory valuation, total cost is taken in

account under this technique.

Accounting standards do not allow this

technique for valuation of stock if, it is to be

submitted to government authority.

This approach can be adopted by a company

for valuation of inventory because it is

permitted under accounting standards.

It is formed for internal use i.e. for making

right decisions.

Absorption costing is for external users.

Fixed cost is taken as period cost. Fixed cost is part of product cost of each unit.

Calculation as per Absorption costing.

Working notes:

Absorption costing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

0

11200

(1600)

600

700

21000

(9600)

11400

8

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

0

11200

(1600)

600

700

21000

(9600)

11400

8

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

(100)

(1800)

9600

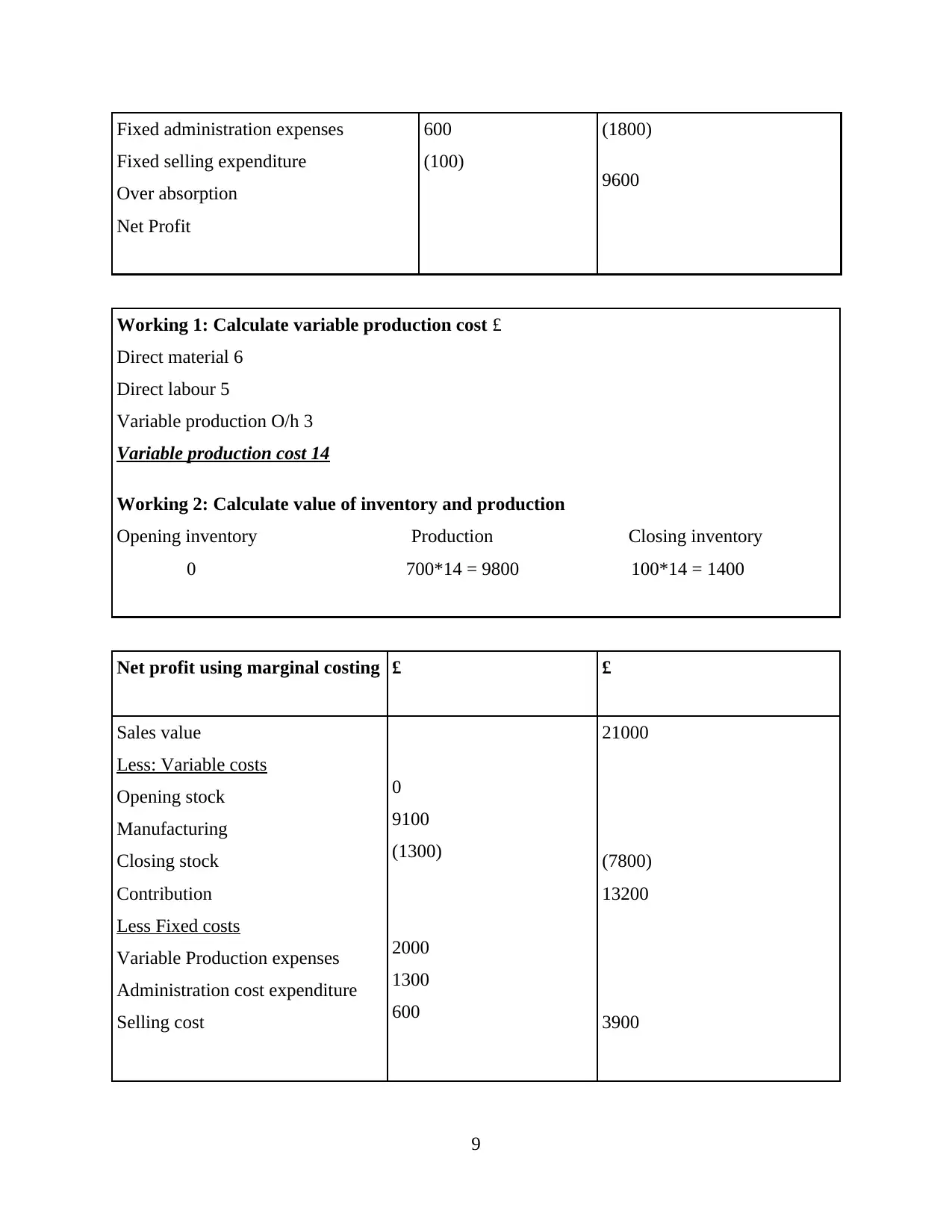

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9

Fixed selling expenditure

Over absorption

Net Profit

600

(100)

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.