Management Accounting Report: Holder Construction Analysis and Systems

VerifiedAdded on 2020/07/22

|20

|4975

|29

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their practical application within a business context, specifically using Holder Construction as a case study. The report begins by highlighting the significance of management accounting in various decision-making processes, emphasizing its role in forecasting, performance evaluation, and make-or-buy decisions. It then assesses different management accounting systems, including job costing, cost accounting, inventory management, and price optimization, evaluating their respective advantages and disadvantages. The core of the report involves a detailed comparison of absorption and marginal costing systems, including the preparation of income statements and a reconciliation analysis to explain the differences in profit figures. Furthermore, the report explores various planning tools used in management accounting and presents how these systems aid in addressing financial challenges. The conclusion summarizes the key findings, reinforcing the value of management accounting for effective financial planning, cost control, and strategic decision-making. The report utilizes financial statements and calculations to illustrate the practical application of the concepts discussed.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

SECTION 1................................................................................................................................1

1. Explaining the importance of management accounting in the decision making aspects...1

2. Assessing different types of management accounting systems that can be used within the

firm.........................................................................................................................................2

3. Critically evaluate management accounting systems that are assessed above..................3

4..............................................................................................................................................5

a. Preparing statements by using absorption and marginal costing system...........................5

b. Stating reasons due to which profit as per each technique is different..............................9

c. Reconciliation statement....................................................................................................9

SECTION 2..............................................................................................................................10

Comparing and contrasting planning tools that can be undertaken in accordance with

management accounting.......................................................................................................10

Presenting the manner in which management accounting systems help in responding

monetary problems...............................................................................................................14

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION......................................................................................................................1

SECTION 1................................................................................................................................1

1. Explaining the importance of management accounting in the decision making aspects...1

2. Assessing different types of management accounting systems that can be used within the

firm.........................................................................................................................................2

3. Critically evaluate management accounting systems that are assessed above..................3

4..............................................................................................................................................5

a. Preparing statements by using absorption and marginal costing system...........................5

b. Stating reasons due to which profit as per each technique is different..............................9

c. Reconciliation statement....................................................................................................9

SECTION 2..............................................................................................................................10

Comparing and contrasting planning tools that can be undertaken in accordance with

management accounting.......................................................................................................10

Presenting the manner in which management accounting systems help in responding

monetary problems...............................................................................................................14

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION

Management accounting field of finance deals with the aspects of performance

evaluation and management. For the purpose of making effective day to day and short term

business decisions manager requires timely and accurate statistical or financial information.

In this regard, MA tools and techniques help in preparing reports that furnishes information

regarding the monetary aspects of the firm. Managerial accounting reports give input for

decision making and thereby make contribution in the attainment of organizational goals and

objectives. The present report is based on Holder Construction, a manufacturing medium

sized business unit, which will provide deepe insight about the different types of MA

systems. Further, report depicts the manner in which MA aid in suitable decision making.

Besides this, it also shed light on the tools that ensure suitable financial planning. It also

presents how MA tools help in preventing and dealing with monetary issues.

SECTION 1

1. Explaining the importance of management accounting in the decision making aspects

Management accounting is the process of preparing accounts and reports that provides

manager with suitable inputs for decision making. In the business organization, managers are

usually faced with countless problems. In this regard, role and significance of management

accounting in decision making aspects are as follows:

Provides assistance in making forecast about future:

MA tools such as activity & zero base budgeting helps in preparing suitable financial

plan and thereby helps in making prediction about the future (Ionescu, 2016). Hence, using

such techniques manager of Holder Construction can assess the revenue or profit margin will

be generated over the expenses.

Facilitates performance evaluation

Management accounting field of finance deals with the aspects of performance

evaluation and management. For the purpose of making effective day to day and short term

business decisions manager requires timely and accurate statistical or financial information.

In this regard, MA tools and techniques help in preparing reports that furnishes information

regarding the monetary aspects of the firm. Managerial accounting reports give input for

decision making and thereby make contribution in the attainment of organizational goals and

objectives. The present report is based on Holder Construction, a manufacturing medium

sized business unit, which will provide deepe insight about the different types of MA

systems. Further, report depicts the manner in which MA aid in suitable decision making.

Besides this, it also shed light on the tools that ensure suitable financial planning. It also

presents how MA tools help in preventing and dealing with monetary issues.

SECTION 1

1. Explaining the importance of management accounting in the decision making aspects

Management accounting is the process of preparing accounts and reports that provides

manager with suitable inputs for decision making. In the business organization, managers are

usually faced with countless problems. In this regard, role and significance of management

accounting in decision making aspects are as follows:

Provides assistance in making forecast about future:

MA tools such as activity & zero base budgeting helps in preparing suitable financial

plan and thereby helps in making prediction about the future (Ionescu, 2016). Hence, using

such techniques manager of Holder Construction can assess the revenue or profit margin will

be generated over the expenses.

Facilitates performance evaluation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variance analysis technique of MA enables manager to do comparison of actual

performance with the standards. Hence, by assessing deviations and associated causes

manager of Holder Construction can take appropriate decision for further improvement.

Assists in taking decision (make or buy):

In the context of manufacturing firms, managers face issue in deciding whether they

need to make or buy component of products from outside. Hence, such issue can be resolved

by the manager more effectually through conducting make or buy analysis (Fullerton,

Kennedy and Widener, 2013). Thus, comparing profit associated with both the options

manager of Holder Construction can select the profitable one.

Helps in taking decision about sales and profit

MA helps manager in assessing the number of units which they need to sell for

recovering the expenses incurred. Further, marginal costing assessment also assists manager

in determining the level of sales that need to be made for the generation of desired profit

margin.

2. Assessing different types of management accounting systems that can be used within the

firm

Management accounting refers to the process of analyzing cost and operations which

in turn helps in preparing financial reports. Hence, report that is prepared as per MA

significantly aid in managers decision making and thereby helps in achieving goals. There are

several types of management accounting systems that can be used by Holder Construction

for managing internal operations, cost control and profit maximization.

Job costing: This system helps in accumulating information about the costs associated

with specific production or services. By undertaking job costing systems, manager of

Holder Construction can assess or trace cost related to specific jobs. Job costing

system also helps in assessing whether cost or expenses can be reduced in further

production or not (Job Costing, 2018).

Cost accounting: For manufacturing products or services, business unit incurs several

expenses such as direct and indirect. Hence, using the system of cost accounting

Holder Construction can accumulate all the expenses such as material, labour and

overhead. Hence, by dividing total expenses from the number of units manufactured

unit cost can be identified. Along with this, cost accounting system also helps in

performance with the standards. Hence, by assessing deviations and associated causes

manager of Holder Construction can take appropriate decision for further improvement.

Assists in taking decision (make or buy):

In the context of manufacturing firms, managers face issue in deciding whether they

need to make or buy component of products from outside. Hence, such issue can be resolved

by the manager more effectually through conducting make or buy analysis (Fullerton,

Kennedy and Widener, 2013). Thus, comparing profit associated with both the options

manager of Holder Construction can select the profitable one.

Helps in taking decision about sales and profit

MA helps manager in assessing the number of units which they need to sell for

recovering the expenses incurred. Further, marginal costing assessment also assists manager

in determining the level of sales that need to be made for the generation of desired profit

margin.

2. Assessing different types of management accounting systems that can be used within the

firm

Management accounting refers to the process of analyzing cost and operations which

in turn helps in preparing financial reports. Hence, report that is prepared as per MA

significantly aid in managers decision making and thereby helps in achieving goals. There are

several types of management accounting systems that can be used by Holder Construction

for managing internal operations, cost control and profit maximization.

Job costing: This system helps in accumulating information about the costs associated

with specific production or services. By undertaking job costing systems, manager of

Holder Construction can assess or trace cost related to specific jobs. Job costing

system also helps in assessing whether cost or expenses can be reduced in further

production or not (Job Costing, 2018).

Cost accounting: For manufacturing products or services, business unit incurs several

expenses such as direct and indirect. Hence, using the system of cost accounting

Holder Construction can accumulate all the expenses such as material, labour and

overhead. Hence, by dividing total expenses from the number of units manufactured

unit cost can be identified. Along with this, cost accounting system also helps in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

setting suitable price of the offerings. By adding desired margin % in unit cost, firm

can determine or set price of the offerings.

Inventory management: In the context of Holder Construction, stock management is

highly significant because it imposes cost in front of the firm such as holding,

ordering etc. Hence, using tools such as economic order quantity, just in time (JIT) etc

concerned manufacturing firm can manage stock more effectually and thereby exerts

control cost level (Macintosh and Quattrone, 2010). Thus, MA tools ensure

effective inventory management as well as smooth functioning of the business

operations and functions.

Price optimization: Such MA system helps in assessing and evaluating the

willingness of customers pertaining to pricing aspects. Hence, by getting information

about the money that customers are ready to pay Holder Construction can set suitable

prices of the products or services.

3. Critically evaluate management accounting systems that are assessed above

Benefits and drawbacks that associated with the different types of management

accounting systems are enumerated below:

Job costing

Advantages Disadvantages

Furnishes information about the profit

margin generated from each job.

Past record of job costing helps in

making estimation about cost or

expenses (Advantages and

Disadvantages of Job Costing, 2018).

It is highly suitable for cost plus

contracts and give input for taking

pricing decisions.

Time consuming process

Requires more clerical work for

getting information about the

expenses

Cost accounting:

Advantages Disadvantages

Facilitates cost reduction and aid in Sometimes, such accounting system

can determine or set price of the offerings.

Inventory management: In the context of Holder Construction, stock management is

highly significant because it imposes cost in front of the firm such as holding,

ordering etc. Hence, using tools such as economic order quantity, just in time (JIT) etc

concerned manufacturing firm can manage stock more effectually and thereby exerts

control cost level (Macintosh and Quattrone, 2010). Thus, MA tools ensure

effective inventory management as well as smooth functioning of the business

operations and functions.

Price optimization: Such MA system helps in assessing and evaluating the

willingness of customers pertaining to pricing aspects. Hence, by getting information

about the money that customers are ready to pay Holder Construction can set suitable

prices of the products or services.

3. Critically evaluate management accounting systems that are assessed above

Benefits and drawbacks that associated with the different types of management

accounting systems are enumerated below:

Job costing

Advantages Disadvantages

Furnishes information about the profit

margin generated from each job.

Past record of job costing helps in

making estimation about cost or

expenses (Advantages and

Disadvantages of Job Costing, 2018).

It is highly suitable for cost plus

contracts and give input for taking

pricing decisions.

Time consuming process

Requires more clerical work for

getting information about the

expenses

Cost accounting:

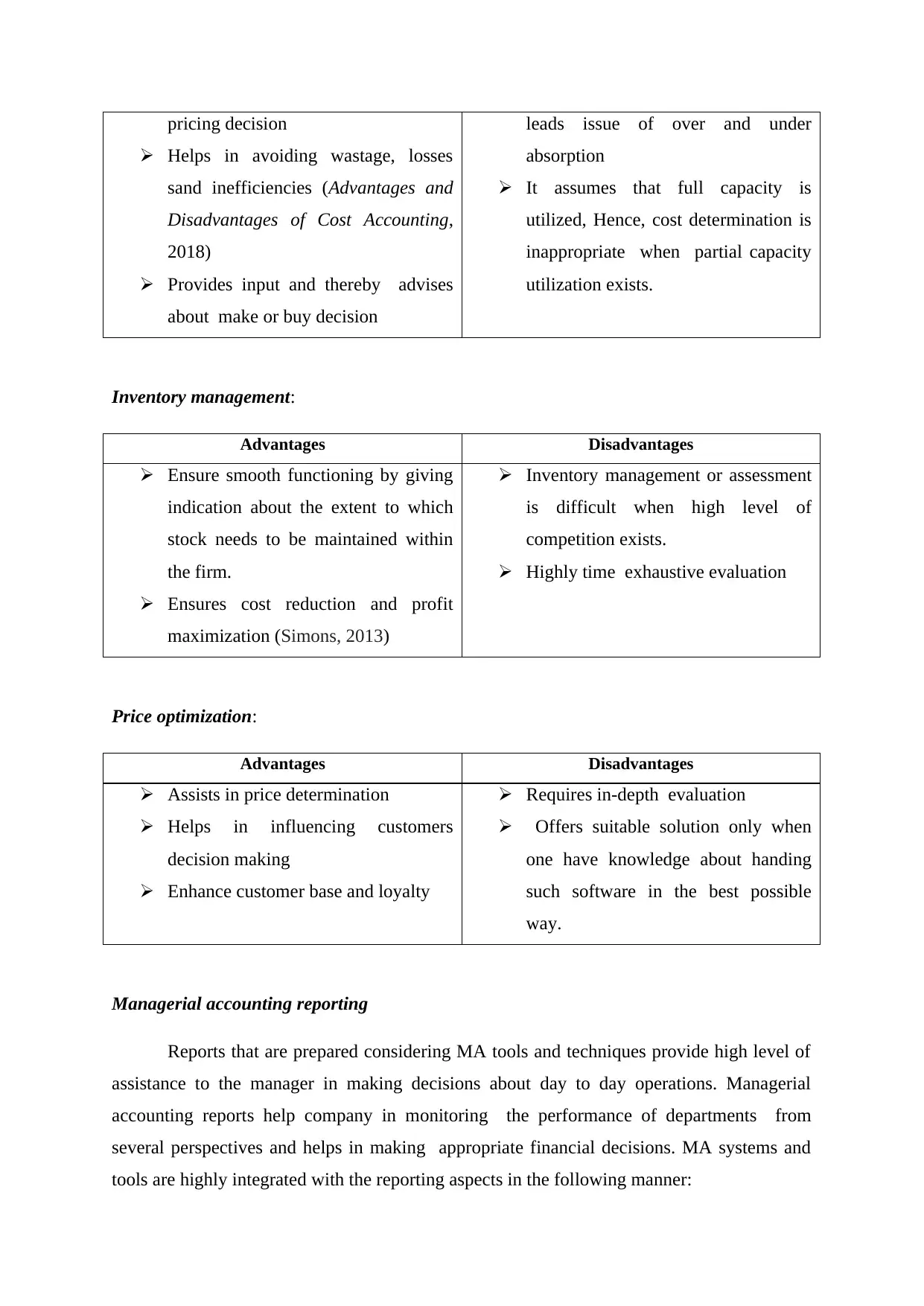

Advantages Disadvantages

Facilitates cost reduction and aid in Sometimes, such accounting system

pricing decision

Helps in avoiding wastage, losses

sand inefficiencies (Advantages and

Disadvantages of Cost Accounting,

2018)

Provides input and thereby advises

about make or buy decision

leads issue of over and under

absorption

It assumes that full capacity is

utilized, Hence, cost determination is

inappropriate when partial capacity

utilization exists.

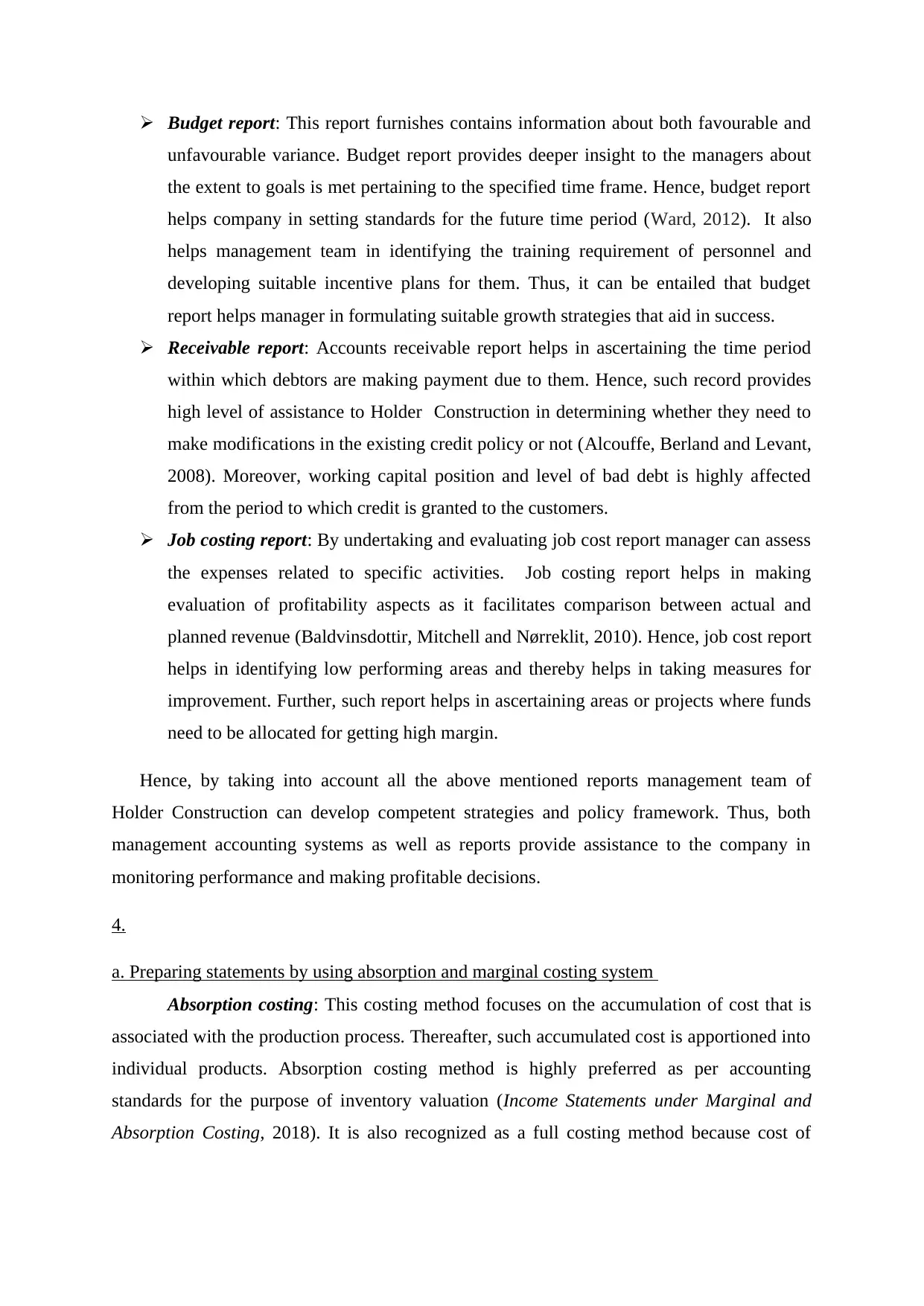

Inventory management:

Advantages Disadvantages

Ensure smooth functioning by giving

indication about the extent to which

stock needs to be maintained within

the firm.

Ensures cost reduction and profit

maximization (Simons, 2013)

Inventory management or assessment

is difficult when high level of

competition exists.

Highly time exhaustive evaluation

Price optimization:

Advantages Disadvantages

Assists in price determination

Helps in influencing customers

decision making

Enhance customer base and loyalty

Requires in-depth evaluation

Offers suitable solution only when

one have knowledge about handing

such software in the best possible

way.

Managerial accounting reporting

Reports that are prepared considering MA tools and techniques provide high level of

assistance to the manager in making decisions about day to day operations. Managerial

accounting reports help company in monitoring the performance of departments from

several perspectives and helps in making appropriate financial decisions. MA systems and

tools are highly integrated with the reporting aspects in the following manner:

Helps in avoiding wastage, losses

sand inefficiencies (Advantages and

Disadvantages of Cost Accounting,

2018)

Provides input and thereby advises

about make or buy decision

leads issue of over and under

absorption

It assumes that full capacity is

utilized, Hence, cost determination is

inappropriate when partial capacity

utilization exists.

Inventory management:

Advantages Disadvantages

Ensure smooth functioning by giving

indication about the extent to which

stock needs to be maintained within

the firm.

Ensures cost reduction and profit

maximization (Simons, 2013)

Inventory management or assessment

is difficult when high level of

competition exists.

Highly time exhaustive evaluation

Price optimization:

Advantages Disadvantages

Assists in price determination

Helps in influencing customers

decision making

Enhance customer base and loyalty

Requires in-depth evaluation

Offers suitable solution only when

one have knowledge about handing

such software in the best possible

way.

Managerial accounting reporting

Reports that are prepared considering MA tools and techniques provide high level of

assistance to the manager in making decisions about day to day operations. Managerial

accounting reports help company in monitoring the performance of departments from

several perspectives and helps in making appropriate financial decisions. MA systems and

tools are highly integrated with the reporting aspects in the following manner:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: This report furnishes contains information about both favourable and

unfavourable variance. Budget report provides deeper insight to the managers about

the extent to goals is met pertaining to the specified time frame. Hence, budget report

helps company in setting standards for the future time period (Ward, 2012). It also

helps management team in identifying the training requirement of personnel and

developing suitable incentive plans for them. Thus, it can be entailed that budget

report helps manager in formulating suitable growth strategies that aid in success.

Receivable report: Accounts receivable report helps in ascertaining the time period

within which debtors are making payment due to them. Hence, such record provides

high level of assistance to Holder Construction in determining whether they need to

make modifications in the existing credit policy or not (Alcouffe, Berland and Levant,

2008). Moreover, working capital position and level of bad debt is highly affected

from the period to which credit is granted to the customers.

Job costing report: By undertaking and evaluating job cost report manager can assess

the expenses related to specific activities. Job costing report helps in making

evaluation of profitability aspects as it facilitates comparison between actual and

planned revenue (Baldvinsdottir, Mitchell and Nørreklit, 2010). Hence, job cost report

helps in identifying low performing areas and thereby helps in taking measures for

improvement. Further, such report helps in ascertaining areas or projects where funds

need to be allocated for getting high margin.

Hence, by taking into account all the above mentioned reports management team of

Holder Construction can develop competent strategies and policy framework. Thus, both

management accounting systems as well as reports provide assistance to the company in

monitoring performance and making profitable decisions.

4.

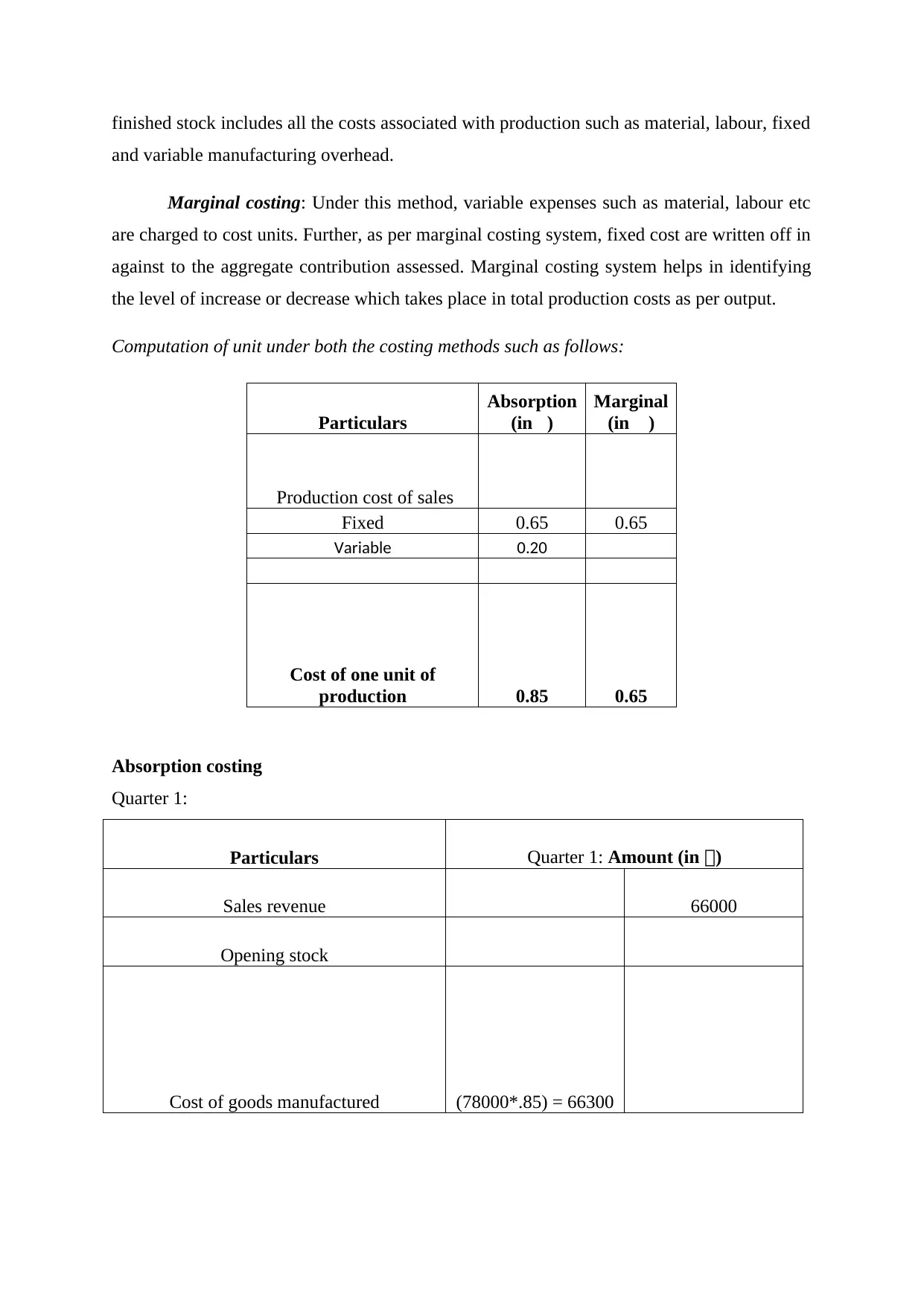

a. Preparing statements by using absorption and marginal costing system

Absorption costing: This costing method focuses on the accumulation of cost that is

associated with the production process. Thereafter, such accumulated cost is apportioned into

individual products. Absorption costing method is highly preferred as per accounting

standards for the purpose of inventory valuation (Income Statements under Marginal and

Absorption Costing, 2018). It is also recognized as a full costing method because cost of

unfavourable variance. Budget report provides deeper insight to the managers about

the extent to goals is met pertaining to the specified time frame. Hence, budget report

helps company in setting standards for the future time period (Ward, 2012). It also

helps management team in identifying the training requirement of personnel and

developing suitable incentive plans for them. Thus, it can be entailed that budget

report helps manager in formulating suitable growth strategies that aid in success.

Receivable report: Accounts receivable report helps in ascertaining the time period

within which debtors are making payment due to them. Hence, such record provides

high level of assistance to Holder Construction in determining whether they need to

make modifications in the existing credit policy or not (Alcouffe, Berland and Levant,

2008). Moreover, working capital position and level of bad debt is highly affected

from the period to which credit is granted to the customers.

Job costing report: By undertaking and evaluating job cost report manager can assess

the expenses related to specific activities. Job costing report helps in making

evaluation of profitability aspects as it facilitates comparison between actual and

planned revenue (Baldvinsdottir, Mitchell and Nørreklit, 2010). Hence, job cost report

helps in identifying low performing areas and thereby helps in taking measures for

improvement. Further, such report helps in ascertaining areas or projects where funds

need to be allocated for getting high margin.

Hence, by taking into account all the above mentioned reports management team of

Holder Construction can develop competent strategies and policy framework. Thus, both

management accounting systems as well as reports provide assistance to the company in

monitoring performance and making profitable decisions.

4.

a. Preparing statements by using absorption and marginal costing system

Absorption costing: This costing method focuses on the accumulation of cost that is

associated with the production process. Thereafter, such accumulated cost is apportioned into

individual products. Absorption costing method is highly preferred as per accounting

standards for the purpose of inventory valuation (Income Statements under Marginal and

Absorption Costing, 2018). It is also recognized as a full costing method because cost of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

finished stock includes all the costs associated with production such as material, labour, fixed

and variable manufacturing overhead.

Marginal costing: Under this method, variable expenses such as material, labour etc

are charged to cost units. Further, as per marginal costing system, fixed cost are written off in

against to the aggregate contribution assessed. Marginal costing system helps in identifying

the level of increase or decrease which takes place in total production costs as per output.

Computation of unit under both the costing methods such as follows:

Particulars

Absorption

(in£)

Marginal

(in £)

Production cost of sales

Fixed 0.65 0.65

Variable 0.20

Cost of one unit of

production 0.85 0.65

Absorption costing

Quarter 1:

Particulars Quarter 1: Amount (in £)

Sales revenue 66000

Opening stock

Cost of goods manufactured (78000*.85) = 66300

and variable manufacturing overhead.

Marginal costing: Under this method, variable expenses such as material, labour etc

are charged to cost units. Further, as per marginal costing system, fixed cost are written off in

against to the aggregate contribution assessed. Marginal costing system helps in identifying

the level of increase or decrease which takes place in total production costs as per output.

Computation of unit under both the costing methods such as follows:

Particulars

Absorption

(in£)

Marginal

(in £)

Production cost of sales

Fixed 0.65 0.65

Variable 0.20

Cost of one unit of

production 0.85 0.65

Absorption costing

Quarter 1:

Particulars Quarter 1: Amount (in £)

Sales revenue 66000

Opening stock

Cost of goods manufactured (78000*.85) = 66300

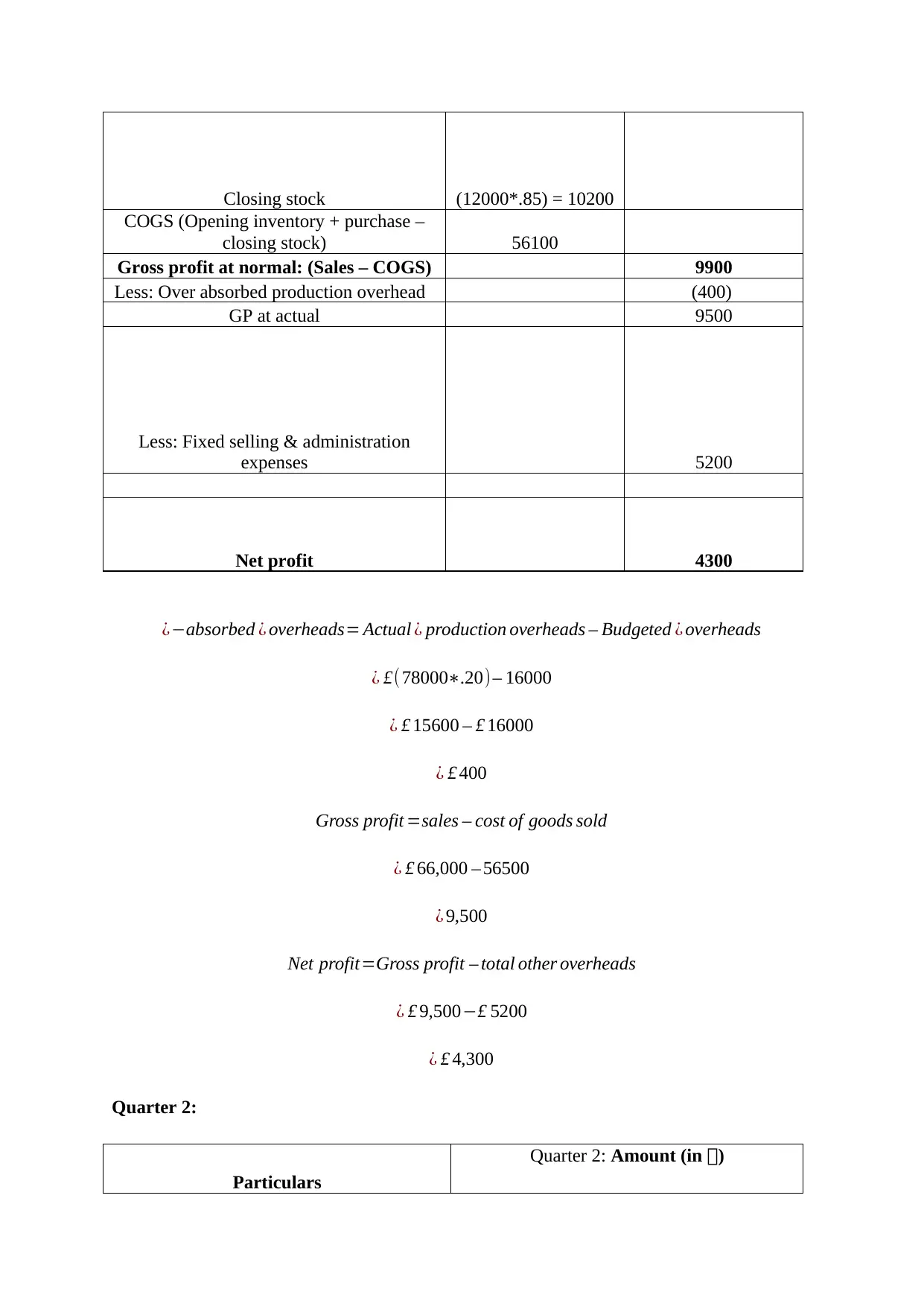

Closing stock (12000*.85) = 10200

COGS (Opening inventory + purchase –

closing stock) 56100

Gross profit at normal: (Sales – COGS) 9900

Less: Over absorbed production overhead (400)

GP at actual 9500

Less: Fixed selling & administration

expenses 5200

Net profit 4300

¿−absorbed ¿ overheads= Actual ¿ production overheads – Budgeted ¿ overheads

¿ £(78000∗.20) – 16000

¿ £ 15600 – £ 16000

¿ £ 400

Gross profit =sales – cost of goods sold

¿ £ 66,000 – 56500

¿ 9,500

Net profit=Gross profit – total other overheads

¿ £ 9,500−£ 5200

¿ £ 4,300

Quarter 2:

Particulars

Quarter 2: Amount (in £)

COGS (Opening inventory + purchase –

closing stock) 56100

Gross profit at normal: (Sales – COGS) 9900

Less: Over absorbed production overhead (400)

GP at actual 9500

Less: Fixed selling & administration

expenses 5200

Net profit 4300

¿−absorbed ¿ overheads= Actual ¿ production overheads – Budgeted ¿ overheads

¿ £(78000∗.20) – 16000

¿ £ 15600 – £ 16000

¿ £ 400

Gross profit =sales – cost of goods sold

¿ £ 66,000 – 56500

¿ 9,500

Net profit=Gross profit – total other overheads

¿ £ 9,500−£ 5200

¿ £ 4,300

Quarter 2:

Particulars

Quarter 2: Amount (in £)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

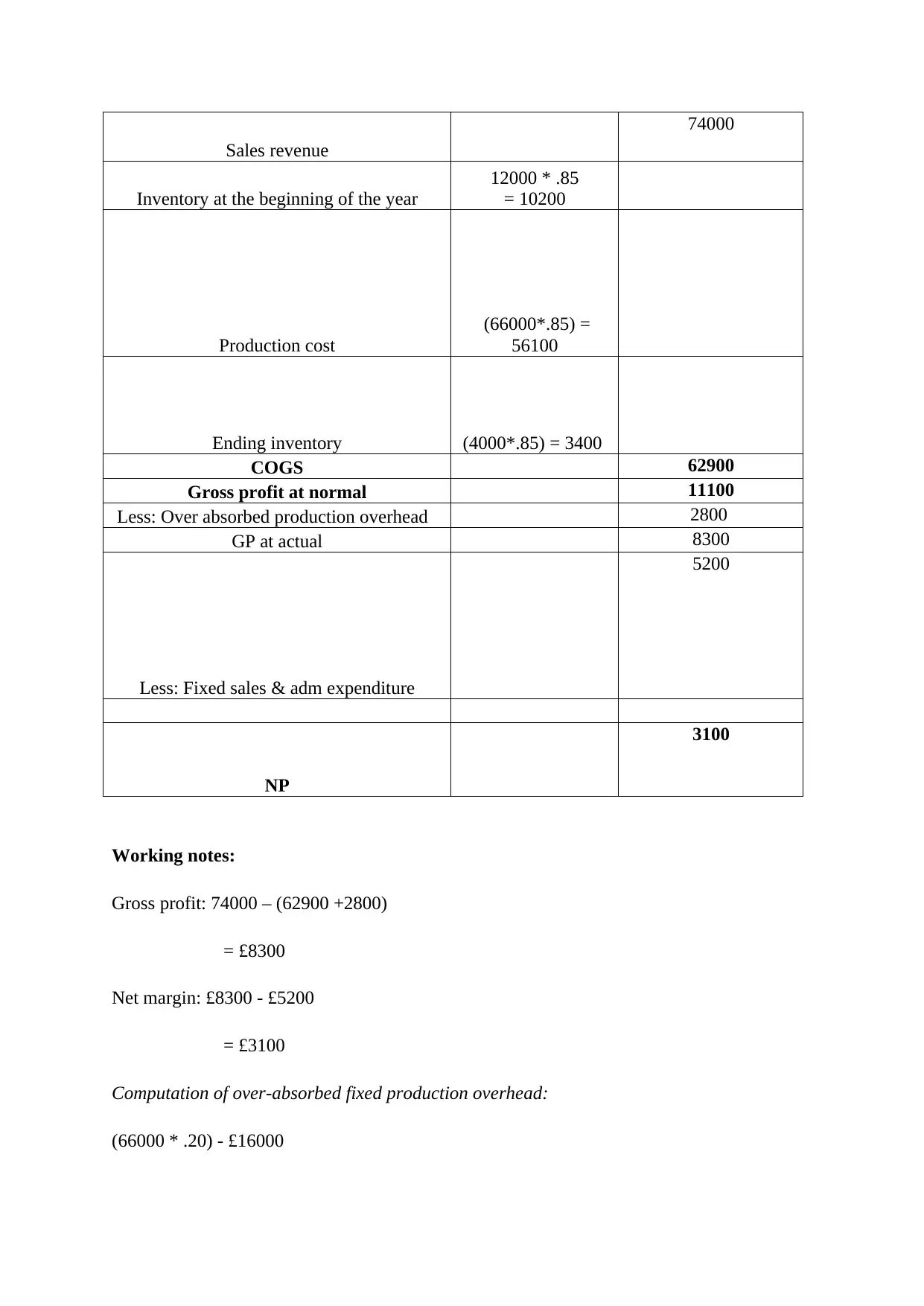

Sales revenue

74000

Inventory at the beginning of the year

12000 * .85

= 10200

Production cost

(66000*.85) =

56100

Ending inventory (4000*.85) = 3400

COGS 62900

Gross profit at normal 11100

Less: Over absorbed production overhead 2800

GP at actual 8300

Less: Fixed sales & adm expenditure

5200

NP

3100

Working notes:

Gross profit: 74000 – (62900 +2800)

= £8300

Net margin: £8300 - £5200

= £3100

Computation of over-absorbed fixed production overhead:

(66000 * .20) - £16000

74000

Inventory at the beginning of the year

12000 * .85

= 10200

Production cost

(66000*.85) =

56100

Ending inventory (4000*.85) = 3400

COGS 62900

Gross profit at normal 11100

Less: Over absorbed production overhead 2800

GP at actual 8300

Less: Fixed sales & adm expenditure

5200

NP

3100

Working notes:

Gross profit: 74000 – (62900 +2800)

= £8300

Net margin: £8300 - £5200

= £3100

Computation of over-absorbed fixed production overhead:

(66000 * .20) - £16000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £13200 - £16000

= £2800

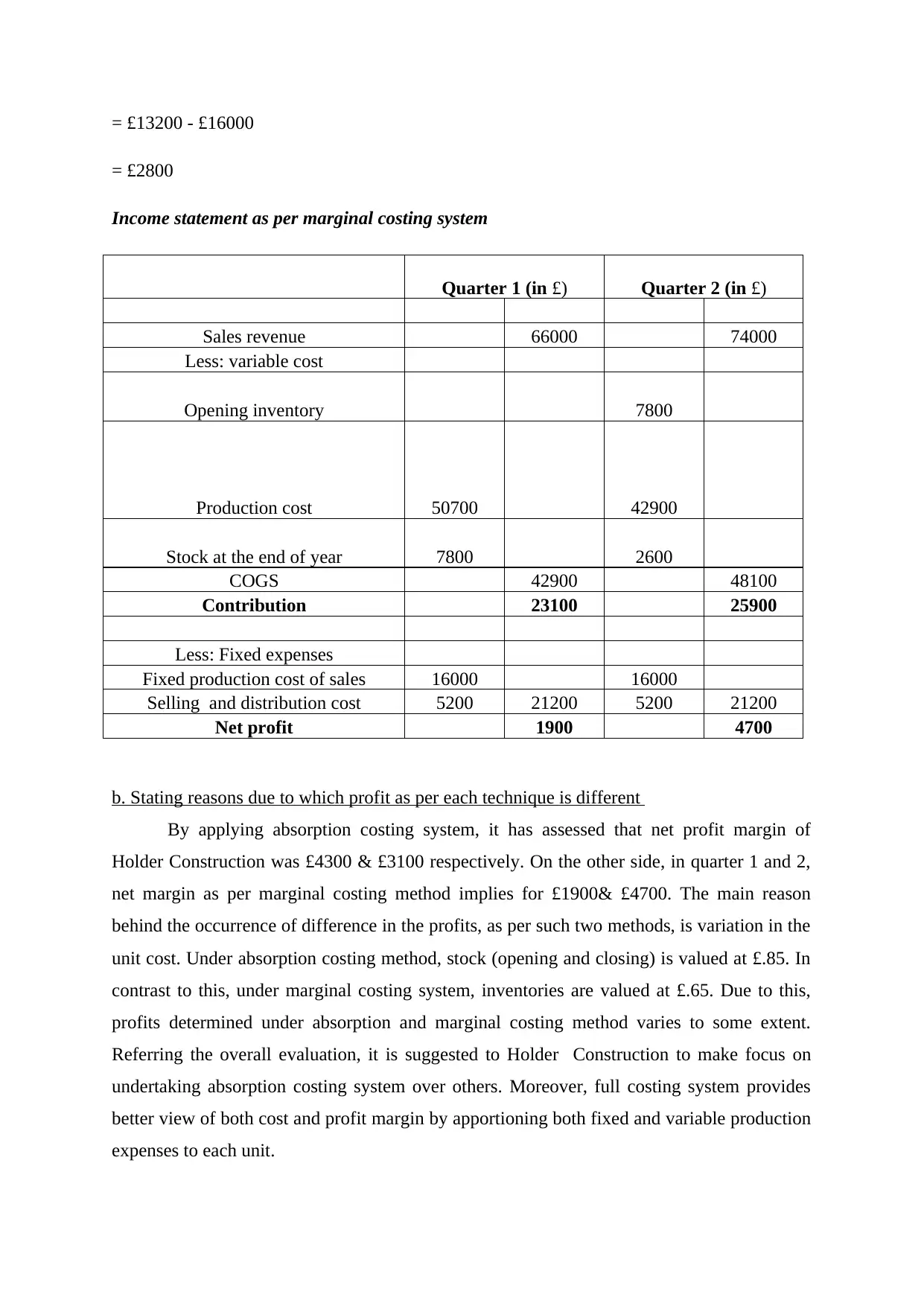

Income statement as per marginal costing system

Quarter 1 (in £) Quarter 2 (in £)

Sales revenue 66000 74000

Less: variable cost

Opening inventory 7800

Production cost 50700 42900

Stock at the end of year 7800 2600

COGS 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost of sales 16000 16000

Selling and distribution cost 5200 21200 5200 21200

Net profit 1900 4700

b. Stating reasons due to which profit as per each technique is different

By applying absorption costing system, it has assessed that net profit margin of

Holder Construction was £4300 & £3100 respectively. On the other side, in quarter 1 and 2,

net margin as per marginal costing method implies for £1900& £4700. The main reason

behind the occurrence of difference in the profits, as per such two methods, is variation in the

unit cost. Under absorption costing method, stock (opening and closing) is valued at £.85. In

contrast to this, under marginal costing system, inventories are valued at £.65. Due to this,

profits determined under absorption and marginal costing method varies to some extent.

Referring the overall evaluation, it is suggested to Holder Construction to make focus on

undertaking absorption costing system over others. Moreover, full costing system provides

better view of both cost and profit margin by apportioning both fixed and variable production

expenses to each unit.

= £2800

Income statement as per marginal costing system

Quarter 1 (in £) Quarter 2 (in £)

Sales revenue 66000 74000

Less: variable cost

Opening inventory 7800

Production cost 50700 42900

Stock at the end of year 7800 2600

COGS 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost of sales 16000 16000

Selling and distribution cost 5200 21200 5200 21200

Net profit 1900 4700

b. Stating reasons due to which profit as per each technique is different

By applying absorption costing system, it has assessed that net profit margin of

Holder Construction was £4300 & £3100 respectively. On the other side, in quarter 1 and 2,

net margin as per marginal costing method implies for £1900& £4700. The main reason

behind the occurrence of difference in the profits, as per such two methods, is variation in the

unit cost. Under absorption costing method, stock (opening and closing) is valued at £.85. In

contrast to this, under marginal costing system, inventories are valued at £.65. Due to this,

profits determined under absorption and marginal costing method varies to some extent.

Referring the overall evaluation, it is suggested to Holder Construction to make focus on

undertaking absorption costing system over others. Moreover, full costing system provides

better view of both cost and profit margin by apportioning both fixed and variable production

expenses to each unit.

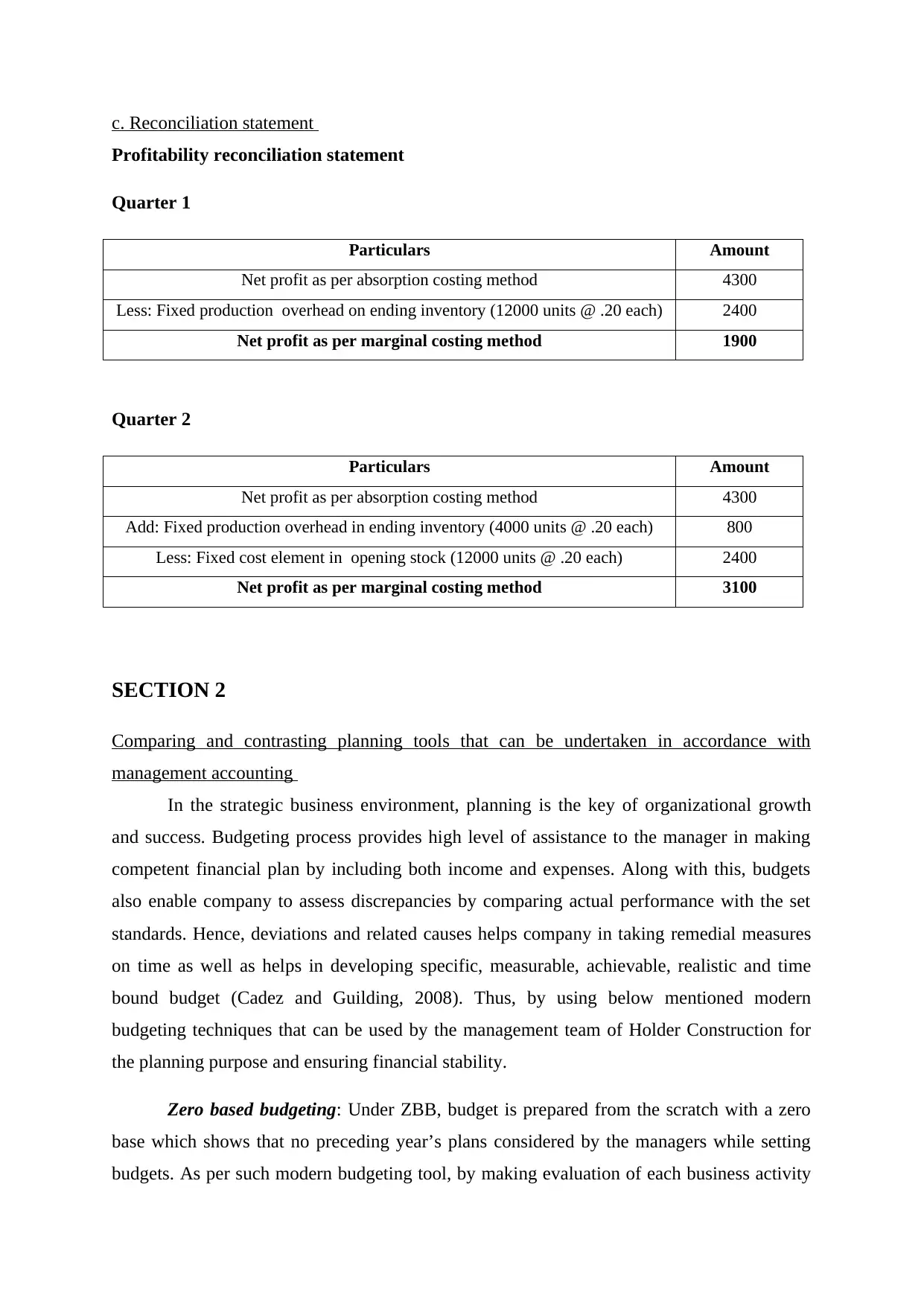

c. Reconciliation statement

Profitability reconciliation statement

Quarter 1

Particulars Amount

Net profit as per absorption costing method 4300

Less: Fixed production overhead on ending inventory (12000 units @ .20 each) 2400

Net profit as per marginal costing method 1900

Quarter 2

Particulars Amount

Net profit as per absorption costing method 4300

Add: Fixed production overhead in ending inventory (4000 units @ .20 each) 800

Less: Fixed cost element in opening stock (12000 units @ .20 each) 2400

Net profit as per marginal costing method 3100

SECTION 2

Comparing and contrasting planning tools that can be undertaken in accordance with

management accounting

In the strategic business environment, planning is the key of organizational growth

and success. Budgeting process provides high level of assistance to the manager in making

competent financial plan by including both income and expenses. Along with this, budgets

also enable company to assess discrepancies by comparing actual performance with the set

standards. Hence, deviations and related causes helps company in taking remedial measures

on time as well as helps in developing specific, measurable, achievable, realistic and time

bound budget (Cadez and Guilding, 2008). Thus, by using below mentioned modern

budgeting techniques that can be used by the management team of Holder Construction for

the planning purpose and ensuring financial stability.

Zero based budgeting: Under ZBB, budget is prepared from the scratch with a zero

base which shows that no preceding year’s plans considered by the managers while setting

budgets. As per such modern budgeting tool, by making evaluation of each business activity

Profitability reconciliation statement

Quarter 1

Particulars Amount

Net profit as per absorption costing method 4300

Less: Fixed production overhead on ending inventory (12000 units @ .20 each) 2400

Net profit as per marginal costing method 1900

Quarter 2

Particulars Amount

Net profit as per absorption costing method 4300

Add: Fixed production overhead in ending inventory (4000 units @ .20 each) 800

Less: Fixed cost element in opening stock (12000 units @ .20 each) 2400

Net profit as per marginal costing method 3100

SECTION 2

Comparing and contrasting planning tools that can be undertaken in accordance with

management accounting

In the strategic business environment, planning is the key of organizational growth

and success. Budgeting process provides high level of assistance to the manager in making

competent financial plan by including both income and expenses. Along with this, budgets

also enable company to assess discrepancies by comparing actual performance with the set

standards. Hence, deviations and related causes helps company in taking remedial measures

on time as well as helps in developing specific, measurable, achievable, realistic and time

bound budget (Cadez and Guilding, 2008). Thus, by using below mentioned modern

budgeting techniques that can be used by the management team of Holder Construction for

the planning purpose and ensuring financial stability.

Zero based budgeting: Under ZBB, budget is prepared from the scratch with a zero

base which shows that no preceding year’s plans considered by the managers while setting

budgets. As per such modern budgeting tool, by making evaluation of each business activity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.