Management Accounting and Financial Analysis Report: TECH (UK) LTD

VerifiedAdded on 2021/01/01

|20

|4600

|179

Report

AI Summary

This report provides an overview of management accounting practices within an organization, focusing on TECH (UK) LTD. It details the essential requirements of management accounting systems, contrasting them with financial accounting, and emphasizes their importance as decision-making tools for department managers. Various cost accounting and inventory management systems are explored, alongside different types of managerial accounting reports such as budgeting, job cost, inventory, and performance reports. The report also discusses costing methods for calculating net profit, the effective use of management accounting tools and techniques, and the role of budgeting in planning and control. It concludes by examining how management accounting contributes to addressing financial issues within the organization. The student-contributed document is available on Desklib, a platform offering a range of study tools for students.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A) Management Accounting:......................................................................................................3

b). Presenting Financial Information:..........................................................................................6

TASK 2............................................................................................................................................8

Various types of costing methods which are use for calculating net profit.................................8

Effective use of management accounting tools and techniques................................................14

Evaluation on the basis of data collected from business activities............................................14

TASK 3.........................................................................................................................................15

a).Different kinds of budgets and their advantages and disadvantages:....................................15

b). Budget preparation process including identifying of pricing and diverse costing systems

which can be used:.....................................................................................................................16

c). Importance of budget as a tool for planning and control purpose:.......................................18

TASK 4..........................................................................................................................................18

Contribution of management accounting tools to respond financial issues..............................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A) Management Accounting:......................................................................................................3

b). Presenting Financial Information:..........................................................................................6

TASK 2............................................................................................................................................8

Various types of costing methods which are use for calculating net profit.................................8

Effective use of management accounting tools and techniques................................................14

Evaluation on the basis of data collected from business activities............................................14

TASK 3.........................................................................................................................................15

a).Different kinds of budgets and their advantages and disadvantages:....................................15

b). Budget preparation process including identifying of pricing and diverse costing systems

which can be used:.....................................................................................................................16

c). Importance of budget as a tool for planning and control purpose:.......................................18

TASK 4..........................................................................................................................................18

Contribution of management accounting tools to respond financial issues..............................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

2

INTRODUCTION

This report tells about the management accounting is very useful in

the organization which helps the manager to take appropriate decision which

is related to the organization. The tools and techniques of the management

accounting help the manager to prepare the plans from where the

organization can get the more sales from which market and also tells that

the what the consumer needs and desire in the selected market. This report

also includes various management accounting systems and their useful

requirements in the business activities which are integrated with the

management accounting reporting. The organization can measure the

performance of their business activities with the help of management

accounting methods. Further in this report includes the income statement on

the basis of marginal and absorption costing which helps the manager to

make profits by applying these methods of the costing (Bennett, Schaltegger and

Zvezdov, 2013). The report also describes the essential uses of different

planning tools which are used for budgetary control as a performance

measure for the organization. The comparison in this report is also made

which show that how the management accounting can use in organization in

responding the financial problems. TECH (UK) LTD. used the management

accounting to sort out the problems of the department managers, who give

the complained about the lack of financial information. If the flow of

information is in appropriate way, the department managers can make

decisions for their respective departments.

TASK 1

A) Management Accounting:

Management accounting involves providing and preparing timely and useful

statistical and financial information to the business managers so that they

can prepare day- to- day and useful managerial decisions. It is also known as

cost and managerial accounting. It produces reports for organization’s

internal stakeholders. The result of management accounting is regular

3

This report tells about the management accounting is very useful in

the organization which helps the manager to take appropriate decision which

is related to the organization. The tools and techniques of the management

accounting help the manager to prepare the plans from where the

organization can get the more sales from which market and also tells that

the what the consumer needs and desire in the selected market. This report

also includes various management accounting systems and their useful

requirements in the business activities which are integrated with the

management accounting reporting. The organization can measure the

performance of their business activities with the help of management

accounting methods. Further in this report includes the income statement on

the basis of marginal and absorption costing which helps the manager to

make profits by applying these methods of the costing (Bennett, Schaltegger and

Zvezdov, 2013). The report also describes the essential uses of different

planning tools which are used for budgetary control as a performance

measure for the organization. The comparison in this report is also made

which show that how the management accounting can use in organization in

responding the financial problems. TECH (UK) LTD. used the management

accounting to sort out the problems of the department managers, who give

the complained about the lack of financial information. If the flow of

information is in appropriate way, the department managers can make

decisions for their respective departments.

TASK 1

A) Management Accounting:

Management accounting involves providing and preparing timely and useful

statistical and financial information to the business managers so that they

can prepare day- to- day and useful managerial decisions. It is also known as

cost and managerial accounting. It produces reports for organization’s

internal stakeholders. The result of management accounting is regular

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

intervals reports for the department managers and directors. The reports

include the details of the organization available cash, current sales revenue,

and recent state of accounts receivable and payable.

Essential requirements of management accounting systems:

1. Measures the performance of whole organization including employees’ efficiency and

working in effectiveness.

2. Another advantage of the use management accounting is that finding out the risk factors

within the organization which can be reduced by the management of each and every

department.

3. The management accounting gives the accurate and suitable presentation of financial

position of the organization with essential data and information to every department.

4. This is also helpful to manager to prepare the management accounting reports in good

and precise manner which is helpful to the each division of an organization.

I. Management accounting Vs. Financial accounting

1. Management accounting is concerned with the accounting information that is helpful to

the management of an organization whereas financial accounting covers the preparation

of final accounts, financial statements, and communication of accounting information to

the users for the interpretation (Bennett, Schaltegger and Zvezdov, 2013).

2. Management accounting emphasizes the preparation of reports of an organization for

external users whereas financial accounting emphasizes the preparation of reports for its

internal users.

3. Management accounting objectivity is flexibility whereas financial accounting objectivity

is verifiability.

4. Management accounting emphasis on the future whereas financial accounting records of

financial history.

5. Management accounting focuses on segments of a company whereas financial accounting

focuses on company as a whole.

II. The importance of management accounting information as a

decision making tool for department managers are:

1. It helps in finding out the major important performance metrics

for each division within the organization.

4

include the details of the organization available cash, current sales revenue,

and recent state of accounts receivable and payable.

Essential requirements of management accounting systems:

1. Measures the performance of whole organization including employees’ efficiency and

working in effectiveness.

2. Another advantage of the use management accounting is that finding out the risk factors

within the organization which can be reduced by the management of each and every

department.

3. The management accounting gives the accurate and suitable presentation of financial

position of the organization with essential data and information to every department.

4. This is also helpful to manager to prepare the management accounting reports in good

and precise manner which is helpful to the each division of an organization.

I. Management accounting Vs. Financial accounting

1. Management accounting is concerned with the accounting information that is helpful to

the management of an organization whereas financial accounting covers the preparation

of final accounts, financial statements, and communication of accounting information to

the users for the interpretation (Bennett, Schaltegger and Zvezdov, 2013).

2. Management accounting emphasizes the preparation of reports of an organization for

external users whereas financial accounting emphasizes the preparation of reports for its

internal users.

3. Management accounting objectivity is flexibility whereas financial accounting objectivity

is verifiability.

4. Management accounting emphasis on the future whereas financial accounting records of

financial history.

5. Management accounting focuses on segments of a company whereas financial accounting

focuses on company as a whole.

II. The importance of management accounting information as a

decision making tool for department managers are:

1. It helps in finding out the major important performance metrics

for each division within the organization.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. It gathers the data and comparing it and reports the current

performance as compared to the expectations which helps the

mangers for decision making for an organization.

3. It uses some many useful High-Tec tools and techniques such as

balanced scorecard, key performance indicators and

management information system etc. for analyzing working of

the department and also employees working efficiency are

evaluated.

4. With the help of management accounting information, the

managers analysis the reasons behind such deviations which is

incurred in the operations and suggest the department manager

to take the corrective measures to solve out the problems.

III. Cost accounting systems

- It collects information to determine the production cost per unit.

- It assist the managers in set the selling price that will lead to profits,

compute cost of goods sold for the income statement and compute

the cost of inventory for the organization business activities.

- It also involves recording, measuring, reporting the product costs.

- It guides the organization in such a way that to make or buy,

introduction of new product etc.

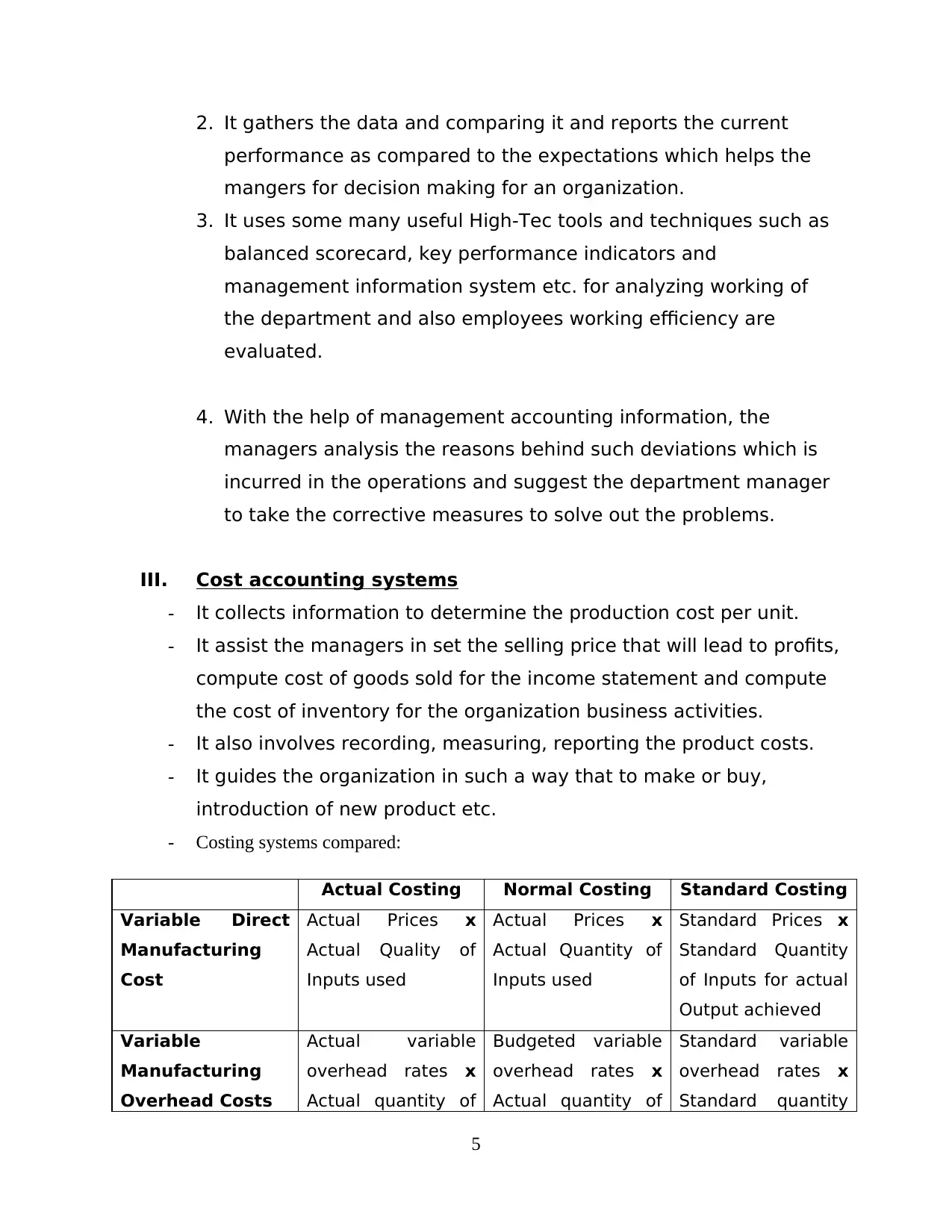

- Costing systems compared:

Actual Costing Normal Costing Standard Costing

Variable Direct

Manufacturing

Cost

Actual Prices x

Actual Quality of

Inputs used

Actual Prices x

Actual Quantity of

Inputs used

Standard Prices x

Standard Quantity

of Inputs for actual

Output achieved

Variable

Manufacturing

Overhead Costs

Actual variable

overhead rates x

Actual quantity of

Budgeted variable

overhead rates x

Actual quantity of

Standard variable

overhead rates x

Standard quantity

5

performance as compared to the expectations which helps the

mangers for decision making for an organization.

3. It uses some many useful High-Tec tools and techniques such as

balanced scorecard, key performance indicators and

management information system etc. for analyzing working of

the department and also employees working efficiency are

evaluated.

4. With the help of management accounting information, the

managers analysis the reasons behind such deviations which is

incurred in the operations and suggest the department manager

to take the corrective measures to solve out the problems.

III. Cost accounting systems

- It collects information to determine the production cost per unit.

- It assist the managers in set the selling price that will lead to profits,

compute cost of goods sold for the income statement and compute

the cost of inventory for the organization business activities.

- It also involves recording, measuring, reporting the product costs.

- It guides the organization in such a way that to make or buy,

introduction of new product etc.

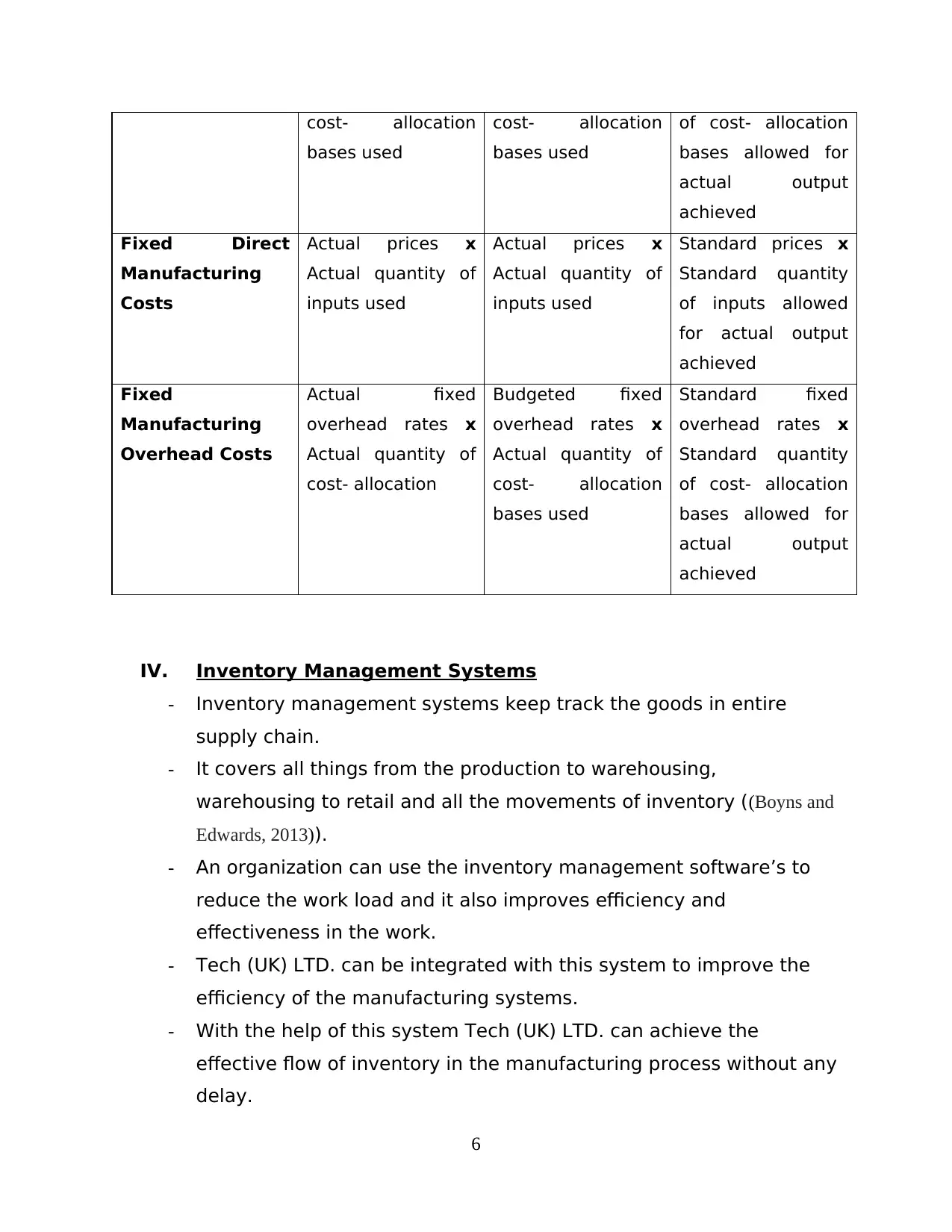

- Costing systems compared:

Actual Costing Normal Costing Standard Costing

Variable Direct

Manufacturing

Cost

Actual Prices x

Actual Quality of

Inputs used

Actual Prices x

Actual Quantity of

Inputs used

Standard Prices x

Standard Quantity

of Inputs for actual

Output achieved

Variable

Manufacturing

Overhead Costs

Actual variable

overhead rates x

Actual quantity of

Budgeted variable

overhead rates x

Actual quantity of

Standard variable

overhead rates x

Standard quantity

5

cost- allocation

bases used

cost- allocation

bases used

of cost- allocation

bases allowed for

actual output

achieved

Fixed Direct

Manufacturing

Costs

Actual prices x

Actual quantity of

inputs used

Actual prices x

Actual quantity of

inputs used

Standard prices x

Standard quantity

of inputs allowed

for actual output

achieved

Fixed

Manufacturing

Overhead Costs

Actual fixed

overhead rates x

Actual quantity of

cost- allocation

Budgeted fixed

overhead rates x

Actual quantity of

cost- allocation

bases used

Standard fixed

overhead rates x

Standard quantity

of cost- allocation

bases allowed for

actual output

achieved

IV. Inventory Management Systems

- Inventory management systems keep track the goods in entire

supply chain.

- It covers all things from the production to warehousing,

warehousing to retail and all the movements of inventory ((Boyns and

Edwards, 2013)).

- An organization can use the inventory management software’s to

reduce the work load and it also improves efficiency and

effectiveness in the work.

- Tech (UK) LTD. can be integrated with this system to improve the

efficiency of the manufacturing systems.

- With the help of this system Tech (UK) LTD. can achieve the

effective flow of inventory in the manufacturing process without any

delay.

6

bases used

cost- allocation

bases used

of cost- allocation

bases allowed for

actual output

achieved

Fixed Direct

Manufacturing

Costs

Actual prices x

Actual quantity of

inputs used

Actual prices x

Actual quantity of

inputs used

Standard prices x

Standard quantity

of inputs allowed

for actual output

achieved

Fixed

Manufacturing

Overhead Costs

Actual fixed

overhead rates x

Actual quantity of

cost- allocation

Budgeted fixed

overhead rates x

Actual quantity of

cost- allocation

bases used

Standard fixed

overhead rates x

Standard quantity

of cost- allocation

bases allowed for

actual output

achieved

IV. Inventory Management Systems

- Inventory management systems keep track the goods in entire

supply chain.

- It covers all things from the production to warehousing,

warehousing to retail and all the movements of inventory ((Boyns and

Edwards, 2013)).

- An organization can use the inventory management software’s to

reduce the work load and it also improves efficiency and

effectiveness in the work.

- Tech (UK) LTD. can be integrated with this system to improve the

efficiency of the manufacturing systems.

- With the help of this system Tech (UK) LTD. can achieve the

effective flow of inventory in the manufacturing process without any

delay.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

V. Job Costing Systems

- In a job costing system, the cost object is an individual unit, batch

or lot of distinct product or service called as job.

- A job costing system includes the process of gathering useful

information about the costs of particular job. This information is

useful to the customer while placing the order and investigates the

each job order cost.

- Tech (UK) Ltd. can use this system to allocate the production cost to

each and particular product while keep tracking on expenses.

- The organization can use this system when the jobs are similar and

keep track all the order expenses of the jobs.

b). Presenting Financial Information:

I. Different types of managerial accounting reports

The following reports are prepared by the management of the

organization to take the appropriate decisions for achievement of

future goals. While preparing these reports following benefits

which are discuss below:

1. Budgeting Reports: This report is include all the

performance and evaluation of the departments working in a

particular projects. The budgeting reports are utilized to

prepare the budgets for the upcoming years. All the past data

are a stored in these reports; the managers use these reports

for estimation the expenditure and income in the past budget.

The future budgets are based on these reports which help the

organization to prepare the budgets for the each department

to achieve the goals.

2. Job Cost Reports: Job cost reports are used to find out the

cost, expenses, and profits of each and different jobs. These

reports are used by the customer for the evaluation. The

7

- In a job costing system, the cost object is an individual unit, batch

or lot of distinct product or service called as job.

- A job costing system includes the process of gathering useful

information about the costs of particular job. This information is

useful to the customer while placing the order and investigates the

each job order cost.

- Tech (UK) Ltd. can use this system to allocate the production cost to

each and particular product while keep tracking on expenses.

- The organization can use this system when the jobs are similar and

keep track all the order expenses of the jobs.

b). Presenting Financial Information:

I. Different types of managerial accounting reports

The following reports are prepared by the management of the

organization to take the appropriate decisions for achievement of

future goals. While preparing these reports following benefits

which are discuss below:

1. Budgeting Reports: This report is include all the

performance and evaluation of the departments working in a

particular projects. The budgeting reports are utilized to

prepare the budgets for the upcoming years. All the past data

are a stored in these reports; the managers use these reports

for estimation the expenditure and income in the past budget.

The future budgets are based on these reports which help the

organization to prepare the budgets for the each department

to achieve the goals.

2. Job Cost Reports: Job cost reports are used to find out the

cost, expenses, and profits of each and different jobs. These

reports are used by the customer for the evaluation. The

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manager can use these reports for evaluation the earning

aspect of the particular job and reducing their efforts on less

profitable jobs. The past jobs are recorded in these reports

which show the achievement of the organization in each job.

3. Inventory and Manufacturing Reports: The organization

business activities involved in the manufacturing process,

prepare these kinds of reports so that the entire supply chain

works in more efficient manner without any delay. The

managers use these kinds of reports for the comparison in

between the various dissimilar assembly lines and search out

the opportunity in it. The inventory and manufacturing reports

assists the manager to prepare the effective plan for the

inventory and manufacturing process so that the each division

can attain their targets on the time.

4. Performance Reports: Under these reports, the manager

assess the overall performance of the organization by

gathering all the data which financial and non-financial. With

the help of performance reports the manager is able to

prepare the effective useful strategies in an appropriate

manner. By using these reports, the investors and other

stakeholders investigate the organization performance and

achievement in the entire markets and afterwards take

decision of the investment in the company.

II. It is necessary to present the information which is important for

the entire organization in an appropriate manner which is easily

to understandable to each department of the organization. The

information is useful to prepare the strategies for the

organization to achieve their goals and targets on the time. The

management information system used by the department for

fulfills the targets without any delay. The user of the

8

aspect of the particular job and reducing their efforts on less

profitable jobs. The past jobs are recorded in these reports

which show the achievement of the organization in each job.

3. Inventory and Manufacturing Reports: The organization

business activities involved in the manufacturing process,

prepare these kinds of reports so that the entire supply chain

works in more efficient manner without any delay. The

managers use these kinds of reports for the comparison in

between the various dissimilar assembly lines and search out

the opportunity in it. The inventory and manufacturing reports

assists the manager to prepare the effective plan for the

inventory and manufacturing process so that the each division

can attain their targets on the time.

4. Performance Reports: Under these reports, the manager

assess the overall performance of the organization by

gathering all the data which financial and non-financial. With

the help of performance reports the manager is able to

prepare the effective useful strategies in an appropriate

manner. By using these reports, the investors and other

stakeholders investigate the organization performance and

achievement in the entire markets and afterwards take

decision of the investment in the company.

II. It is necessary to present the information which is important for

the entire organization in an appropriate manner which is easily

to understandable to each department of the organization. The

information is useful to prepare the strategies for the

organization to achieve their goals and targets on the time. The

management information system used by the department for

fulfills the targets without any delay. The user of the

8

management information system utilized the information to

prepare the records and these records are also submitted in

these systems. The information which is available should be in

the understandable form which can be easily utilized in the

organization whether it is used in internal and external purposes.

TASK 2

Various types of costing methods which are use for calculating net profit

In each and every business organisation, there is paramount role of cost in numerous

procedure of organisation including manufacture of services and products. This is fundamental

for a business enterprise to create and undertake proper optimisation of assigned cost in more

adequate manner in order to reduce the amount of expense of organisation (Quattrone, 2016). It

is fundamental for the service manager to ascertain the utilise of microeconomic components on

regular basis in context of generating more authentic and reliable results. It is an efficient part

that can help in setting whether the company resource are used effectively or not. In regard of

getting more efficient results within certain period of time, firm may need to monitor their weed

expenses and cost those which are incurring on consist production cost.

Cost can be termed as the value or amount which is charged in regard of achieving or

getting certain service or product. These are indirectly and directly associated with the service es

and foods produced by company, It can emphasise the productivity of worker to deliver their best

services that tend to increase the profitability of enterprise within genuine period of time. This

has been noticed that without carrying out proper funds management and flow of cash,

administration cannot enable valuable decision in order to execute further projects. It can make

certain major role or influence used through UK Tech Ltd in their activities of business to set

whole organisation's profitability. Here are discussed few of them as beneath:

Cost volume profit (CVP): This is one of the fundamental techniques that is being

utilised in order to measure numerous modification or changes in regard of whole volume and

cost which can influence organisation's overall earnings along with net flexible components or

aspects.

9

prepare the records and these records are also submitted in

these systems. The information which is available should be in

the understandable form which can be easily utilized in the

organization whether it is used in internal and external purposes.

TASK 2

Various types of costing methods which are use for calculating net profit

In each and every business organisation, there is paramount role of cost in numerous

procedure of organisation including manufacture of services and products. This is fundamental

for a business enterprise to create and undertake proper optimisation of assigned cost in more

adequate manner in order to reduce the amount of expense of organisation (Quattrone, 2016). It

is fundamental for the service manager to ascertain the utilise of microeconomic components on

regular basis in context of generating more authentic and reliable results. It is an efficient part

that can help in setting whether the company resource are used effectively or not. In regard of

getting more efficient results within certain period of time, firm may need to monitor their weed

expenses and cost those which are incurring on consist production cost.

Cost can be termed as the value or amount which is charged in regard of achieving or

getting certain service or product. These are indirectly and directly associated with the service es

and foods produced by company, It can emphasise the productivity of worker to deliver their best

services that tend to increase the profitability of enterprise within genuine period of time. This

has been noticed that without carrying out proper funds management and flow of cash,

administration cannot enable valuable decision in order to execute further projects. It can make

certain major role or influence used through UK Tech Ltd in their activities of business to set

whole organisation's profitability. Here are discussed few of them as beneath:

Cost volume profit (CVP): This is one of the fundamental techniques that is being

utilised in order to measure numerous modification or changes in regard of whole volume and

cost which can influence organisation's overall earnings along with net flexible components or

aspects.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Flexible budgeting: It can affirm as more adjustable tools or methods which change in

more dependable way and ascertain static budget utilisation. This can alter with the modification

in output which are flexible.

Cost variance: This is paramount, effective and simple techniques to create a relevant

comparison between the budgeted amount as well as actual value of cost. It will assist

organisation to develop an evaluation of entire those alternations which incur during the process

of production.

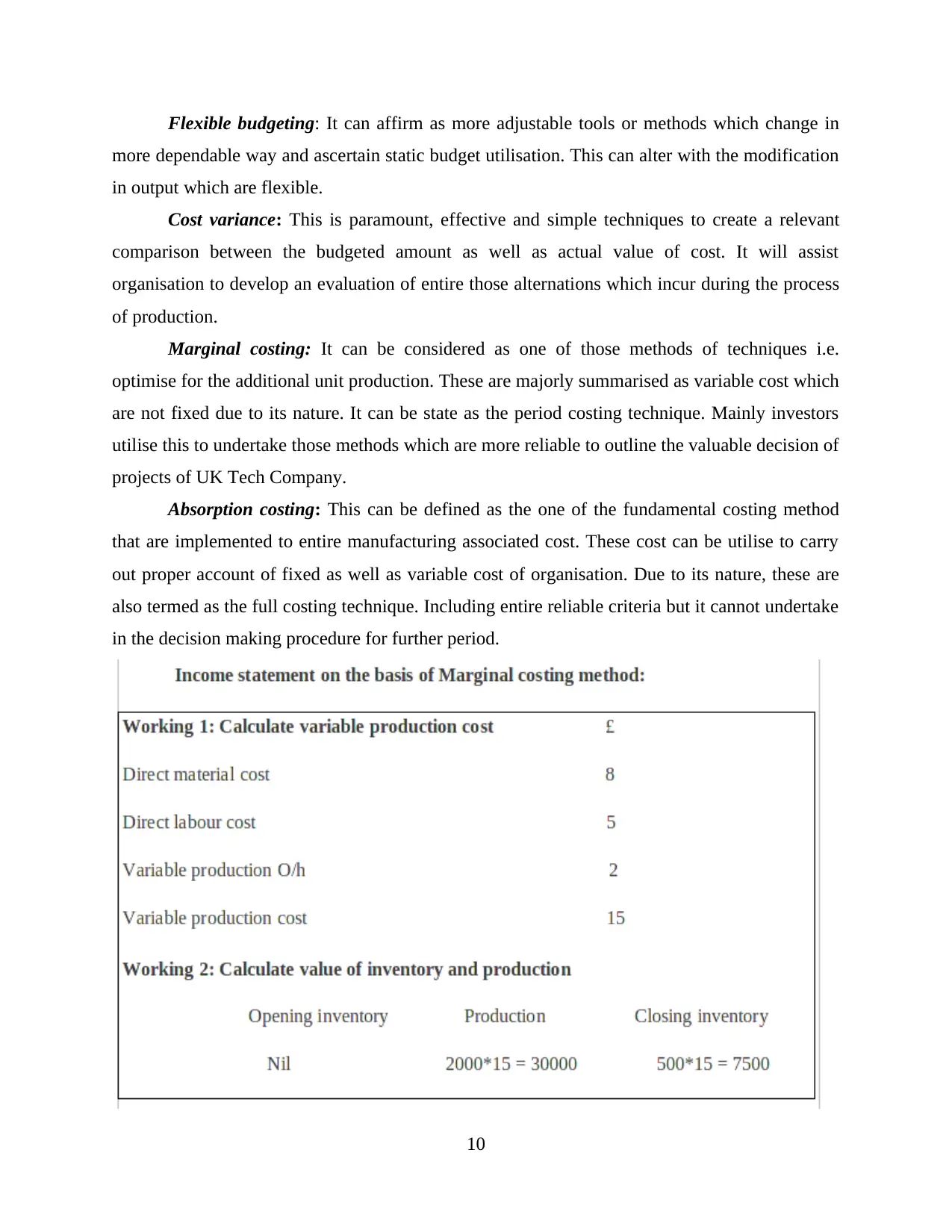

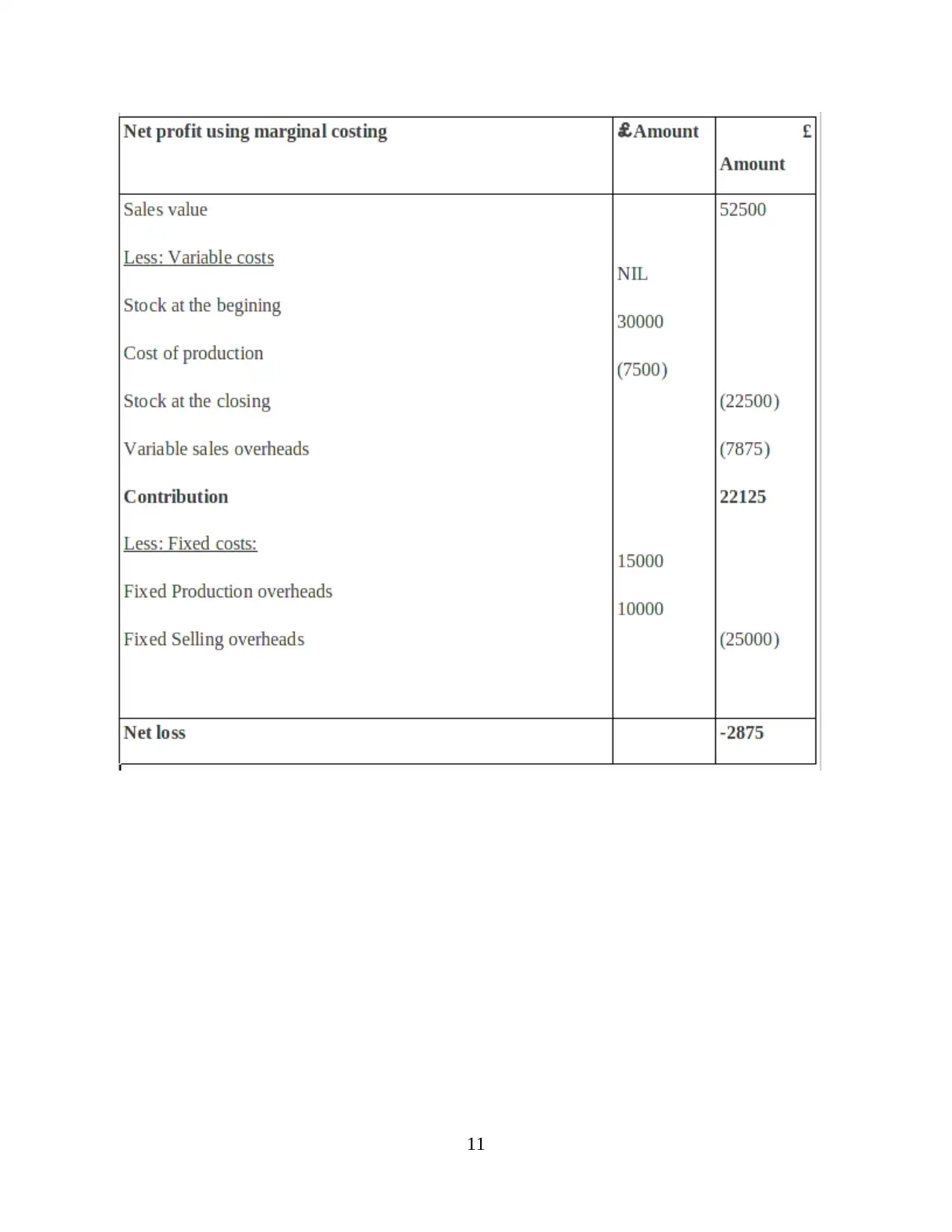

Marginal costing: It can be considered as one of those methods of techniques i.e.

optimise for the additional unit production. These are majorly summarised as variable cost which

are not fixed due to its nature. It can be state as the period costing technique. Mainly investors

utilise this to undertake those methods which are more reliable to outline the valuable decision of

projects of UK Tech Company.

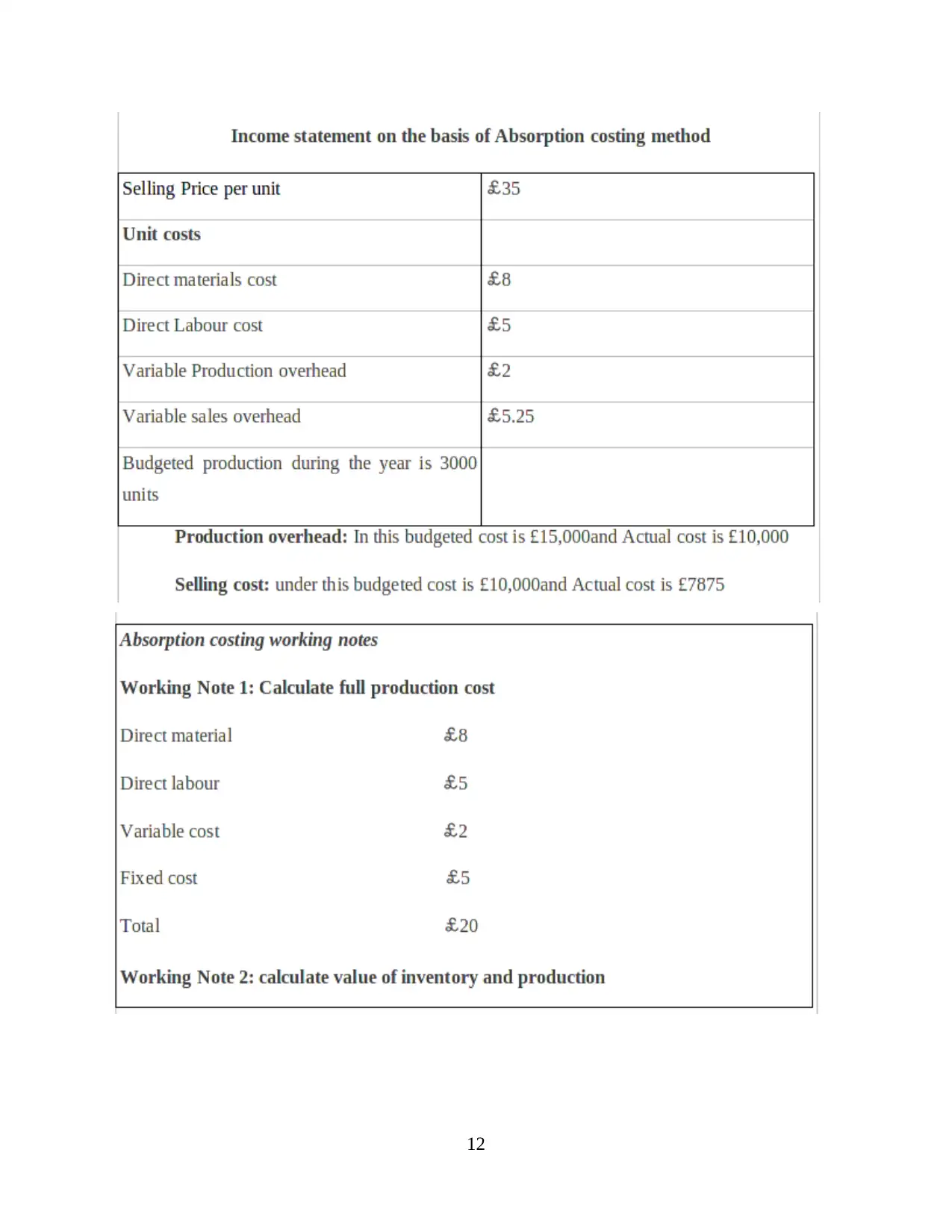

Absorption costing: This can be defined as the one of the fundamental costing method

that are implemented to entire manufacturing associated cost. These cost can be utilise to carry

out proper account of fixed as well as variable cost of organisation. Due to its nature, these are

also termed as the full costing technique. Including entire reliable criteria but it cannot undertake

in the decision making procedure for further period.

10

more dependable way and ascertain static budget utilisation. This can alter with the modification

in output which are flexible.

Cost variance: This is paramount, effective and simple techniques to create a relevant

comparison between the budgeted amount as well as actual value of cost. It will assist

organisation to develop an evaluation of entire those alternations which incur during the process

of production.

Marginal costing: It can be considered as one of those methods of techniques i.e.

optimise for the additional unit production. These are majorly summarised as variable cost which

are not fixed due to its nature. It can be state as the period costing technique. Mainly investors

utilise this to undertake those methods which are more reliable to outline the valuable decision of

projects of UK Tech Company.

Absorption costing: This can be defined as the one of the fundamental costing method

that are implemented to entire manufacturing associated cost. These cost can be utilise to carry

out proper account of fixed as well as variable cost of organisation. Due to its nature, these are

also termed as the full costing technique. Including entire reliable criteria but it cannot undertake

in the decision making procedure for further period.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.