Management Accounting Report: Systems and Decision Making at Tech (UK)

VerifiedAdded on 2024/05/21

|21

|5099

|243

Report

AI Summary

This report provides an overview of management accounting systems at Tech (UK) Limited, differentiating it from financial accounting and highlighting its importance in decision-making. It delves into cost accounting systems (actual, normal, and standard), inventory management, and job costing systems. The report also explores various managerial accounting reports, including financial reports, pro forma cash flow statements, and sales reports, emphasizing their roles in improving productivity and profitability. It examines how these systems and reports aid department managers in forecasting, analyzing rates of return, understanding performance variances, making buy-make decisions, and analyzing cash flows, ultimately contributing to sustainable revenue growth.

Management Accounting report for Tech

(UK) Limited

1

(UK) Limited

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................4

Task 1(M1, D1)...........................................................................................................................................5

TASK 2 (M2, D2).....................................................................................................................................11

TASK 3 (M3, D3).....................................................................................................................................14

TASK 4(M4, D4)......................................................................................................................................18

Conclusion.................................................................................................................................................20

References.................................................................................................................................................21

2

Introduction.................................................................................................................................................4

Task 1(M1, D1)...........................................................................................................................................5

TASK 2 (M2, D2).....................................................................................................................................11

TASK 3 (M3, D3).....................................................................................................................................14

TASK 4(M4, D4)......................................................................................................................................18

Conclusion.................................................................................................................................................20

References.................................................................................................................................................21

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Management accounting helps in managing the income and expenses of the organisations. The

concepts of management accounting help management in taking overview of the sources of

income and centres of cost within the organisation from various streams. The report

differentiates the concepts of management accounting and financial accounting. The report also

presents the various techniques which can employ by the management within the organisation.

Balance score card approach helps in dealing financial problem within the organisation, which

helps in getting sustainable success for a long time period.

4

Management accounting helps in managing the income and expenses of the organisations. The

concepts of management accounting help management in taking overview of the sources of

income and centres of cost within the organisation from various streams. The report

differentiates the concepts of management accounting and financial accounting. The report also

presents the various techniques which can employ by the management within the organisation.

Balance score card approach helps in dealing financial problem within the organisation, which

helps in getting sustainable success for a long time period.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As a trainee management accountant at TECH (UK) Limited a report on the functions of

Management Accounting systems are hereby presented.

Task 1(M1, D1)

a. Explanation of management accounting and the essential requirements of management

accounting system which entails:

I. Distinguishing Management Accounting from Financial Accounting

1.Management accounting provides operational reports to the end users within the concerned

entity that means to the people working or connected within the business entity such as

employees, stakeholders etc. The purpose of management accounting is to provide the fair

position of the company to the internal team so that they operate the company more efficiently

and effectively and also helps in decision making, controlling and planning.

Financial accounting provides reports which are complied with the relevant accounting standards

that gives true and fair position of the company to the various users and is meant for the people

belonging outside the entity such as shareholders.

Financial accounting is required by the law and every year a report of the financial statements

has to be filed as per the required law to the government

II. The importance of management accounting information as a decision making tool for

department managers

2. The importance of management accounting information as a decision making tool for

department managers can be explained as

Helps in Forecasting the Future – Management accounting helps in forecasting future related

to decision making as whether to go for the decision or not. (Drury, 2013).

As decision making is dependent on the operational reports derived through management

accounting are used by the department managers in decision making. Forecasting the future

trends in business helps to acknowledge the past problems and provides appropriate remedies to

5

Management Accounting systems are hereby presented.

Task 1(M1, D1)

a. Explanation of management accounting and the essential requirements of management

accounting system which entails:

I. Distinguishing Management Accounting from Financial Accounting

1.Management accounting provides operational reports to the end users within the concerned

entity that means to the people working or connected within the business entity such as

employees, stakeholders etc. The purpose of management accounting is to provide the fair

position of the company to the internal team so that they operate the company more efficiently

and effectively and also helps in decision making, controlling and planning.

Financial accounting provides reports which are complied with the relevant accounting standards

that gives true and fair position of the company to the various users and is meant for the people

belonging outside the entity such as shareholders.

Financial accounting is required by the law and every year a report of the financial statements

has to be filed as per the required law to the government

II. The importance of management accounting information as a decision making tool for

department managers

2. The importance of management accounting information as a decision making tool for

department managers can be explained as

Helps in Forecasting the Future – Management accounting helps in forecasting future related

to decision making as whether to go for the decision or not. (Drury, 2013).

As decision making is dependent on the operational reports derived through management

accounting are used by the department managers in decision making. Forecasting the future

trends in business helps to acknowledge the past problems and provides appropriate remedies to

5

resolve such issues. In a long run management accounting information is very important decision

making tool. Future business is somewhat similar to what the business has shown results in past

in anticipating such business one has to understand management Accounting system.

Helps in analyzing rate of return- Rate of return is the amount of return that is obtained against

the capital invested for running the business.

Through management accounting reports can be generated easily and through these reports it is

very easy for the department managers to analyze the rate of return. When rate of return is

calculated and analyzed then it helps the department managers in decision making. The return

from a business is to be calculated at every moment as one has to have records where the uses of

the business can easily identify and understand what returns is the business providing to them.

The purpose of the business is to earn and knowing whether the business is providing the

expected rate of return one has to calculate them for this purpose management Accounting

systems are made which helps in decision making so as to continue the business if the rate of

return is as expected or above expectation.

Helps in understanding various performance variances- When the expected future growth is

compared with the actual growth then the difference that arises is the performance variance and

such variances can only be calculated through the Management accounting reports that provides

the managers the actual position the entity and also helps the managers to make future decisions

where the managers can reduce such variances to happen. Business no set of blueprint, there are

variances from whatever we expect from it and whatever we get from it so as to understand such

variances one has to go into the depths of the business. Management accounting system provides

information that helps identify search variances and helps the user to analyse whether such

variances are tolerable. As resolving an issue identified during the course of the business is very

crucial.

Helps in buy –make decision-Introducing a product the manufacturer need to understand that

whether buying a product from a third party is cheaper then manufacturing it. Managerial

accounting system provides information through which it can be calculated. Both the cost are

calculated and then analysed before reaching towards the final decision of making it or buying it

from outside.

6

making tool. Future business is somewhat similar to what the business has shown results in past

in anticipating such business one has to understand management Accounting system.

Helps in analyzing rate of return- Rate of return is the amount of return that is obtained against

the capital invested for running the business.

Through management accounting reports can be generated easily and through these reports it is

very easy for the department managers to analyze the rate of return. When rate of return is

calculated and analyzed then it helps the department managers in decision making. The return

from a business is to be calculated at every moment as one has to have records where the uses of

the business can easily identify and understand what returns is the business providing to them.

The purpose of the business is to earn and knowing whether the business is providing the

expected rate of return one has to calculate them for this purpose management Accounting

systems are made which helps in decision making so as to continue the business if the rate of

return is as expected or above expectation.

Helps in understanding various performance variances- When the expected future growth is

compared with the actual growth then the difference that arises is the performance variance and

such variances can only be calculated through the Management accounting reports that provides

the managers the actual position the entity and also helps the managers to make future decisions

where the managers can reduce such variances to happen. Business no set of blueprint, there are

variances from whatever we expect from it and whatever we get from it so as to understand such

variances one has to go into the depths of the business. Management accounting system provides

information that helps identify search variances and helps the user to analyse whether such

variances are tolerable. As resolving an issue identified during the course of the business is very

crucial.

Helps in buy –make decision-Introducing a product the manufacturer need to understand that

whether buying a product from a third party is cheaper then manufacturing it. Managerial

accounting system provides information through which it can be calculated. Both the cost are

calculated and then analysed before reaching towards the final decision of making it or buying it

from outside.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Helps in analyzing Cash Flows - Cash flow statement are made every year through which cash

position of the company can be ascertained. Analysing such cash flow statements provides the

user the detailed cash inflow outflow within the company. It helps in identifying the impact of

the cash flow on the business and how essential is it. It also provides because that the company

will incur in the future forecasting cash flows helps in identifying from where the revenues will

come whether the revenues will increase or decrease in the upcoming future. Management

Accounting information that is provided by the system helps in designing various budgets,

trends, charts and helps in allocating money and resources so that a sustainable future revenue

growth can be expected from the business.

To improve productivity and profitability: A Company will always try to improve its

productivity and profitability and to improve the same the company needs to work on certain

factors. Management Accounting systems provides information and health the company to

increase its productivity and and profitability through understanding the entity and its nature. It

also helps in enhancing the productivity and the quality of the product. Such reports are prepared

to enhance the productivity of the organization through planning and controlling organizational

activities. Such activities also aid in improving the profitability of the organisation as well. (Van

Dooren, et. al., 2016).

III. Cost accounting systems (actual, normal and standard costing)

3. Cost accounting system can be defined as the system through which the cost of a product that

the entity is producing can be calculated and also the profits arising from such products can be

ascertained. It can be further divided into following segments:

a. Normal costing – Where the manufactured product is measured through actual material costs

involved, actual labour and variable overhead cost occurred. (Drury, 2013).

b. Actual costing – In calculating the product cost it includes the actual value of materials and

labour and variable overheads used to manufacture such product.

c. Standard costing- Where an estimate of the various material, labour and overheads is taken into

consideration for producing a good are standard cost occurred in manufacturing such product.

And such an approach is called as standard costing.

7

position of the company can be ascertained. Analysing such cash flow statements provides the

user the detailed cash inflow outflow within the company. It helps in identifying the impact of

the cash flow on the business and how essential is it. It also provides because that the company

will incur in the future forecasting cash flows helps in identifying from where the revenues will

come whether the revenues will increase or decrease in the upcoming future. Management

Accounting information that is provided by the system helps in designing various budgets,

trends, charts and helps in allocating money and resources so that a sustainable future revenue

growth can be expected from the business.

To improve productivity and profitability: A Company will always try to improve its

productivity and profitability and to improve the same the company needs to work on certain

factors. Management Accounting systems provides information and health the company to

increase its productivity and and profitability through understanding the entity and its nature. It

also helps in enhancing the productivity and the quality of the product. Such reports are prepared

to enhance the productivity of the organization through planning and controlling organizational

activities. Such activities also aid in improving the profitability of the organisation as well. (Van

Dooren, et. al., 2016).

III. Cost accounting systems (actual, normal and standard costing)

3. Cost accounting system can be defined as the system through which the cost of a product that

the entity is producing can be calculated and also the profits arising from such products can be

ascertained. It can be further divided into following segments:

a. Normal costing – Where the manufactured product is measured through actual material costs

involved, actual labour and variable overhead cost occurred. (Drury, 2013).

b. Actual costing – In calculating the product cost it includes the actual value of materials and

labour and variable overheads used to manufacture such product.

c. Standard costing- Where an estimate of the various material, labour and overheads is taken into

consideration for producing a good are standard cost occurred in manufacturing such product.

And such an approach is called as standard costing.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IV. Inventory management systems

4. Inventory management systems-

Inventory management system tracks good and identifies where the goods are kept in the

business and from where the goods are to be transferred wherever there is a shortage of goods in

any one of the warehouse it helps the goods to transfer from one warehouse to another and thus

is helpful in determining the stock levels and helps in maintaining the minimum stock level for a

company.

The coverage of the inventory management system is very vast as it covers every single aspect of

a company's business which begins from production to the retail warehousing to where the goods

are being shipped and it also considers every movement of stocks is necessary and so that it

helps in in avoiding repetition.

The inventory management system nowadays helps the department managers as it reduces their

effort and time and is very helpful for them to devote their time in the other aspect of the

company and also they can easily give time towards other important aspects of the supply chain.

V. Job costing systems

5. Job costing systems

Job costing system helps in tracking the work done by a labour for a particular specific job and it

accumulates information for various jobs done by various labour and the estimated time to do a

service job is then compared with the actual time taken on a particular job by a labour and this

process of governing all these things is called as job costing system.

Job costing helps in accumulating various cost undertaken to complete various service jobs done

by various labour such a process is followed where a company needs to submit the cost analysis

to a customer where a contract is being made for that such information also helps to company to

quote a particular price to the customer also it helps in determining the accuracy of companies

estimation of various cost and which results in a reasonable profit.

8

4. Inventory management systems-

Inventory management system tracks good and identifies where the goods are kept in the

business and from where the goods are to be transferred wherever there is a shortage of goods in

any one of the warehouse it helps the goods to transfer from one warehouse to another and thus

is helpful in determining the stock levels and helps in maintaining the minimum stock level for a

company.

The coverage of the inventory management system is very vast as it covers every single aspect of

a company's business which begins from production to the retail warehousing to where the goods

are being shipped and it also considers every movement of stocks is necessary and so that it

helps in in avoiding repetition.

The inventory management system nowadays helps the department managers as it reduces their

effort and time and is very helpful for them to devote their time in the other aspect of the

company and also they can easily give time towards other important aspects of the supply chain.

V. Job costing systems

5. Job costing systems

Job costing system helps in tracking the work done by a labour for a particular specific job and it

accumulates information for various jobs done by various labour and the estimated time to do a

service job is then compared with the actual time taken on a particular job by a labour and this

process of governing all these things is called as job costing system.

Job costing helps in accumulating various cost undertaken to complete various service jobs done

by various labour such a process is followed where a company needs to submit the cost analysis

to a customer where a contract is being made for that such information also helps to company to

quote a particular price to the customer also it helps in determining the accuracy of companies

estimation of various cost and which results in a reasonable profit.

8

Job costing system accumulates three types of cost which includes direct material, direct labour

and overheads in a particular service job. The amount of direct material, direct labour and

overheads are to be calculated for estimating the cost of a particular service job such 3 costs are

then combined together and the cost of a job is calculated and such calculation of all the jobs

together is being done by the job costing system through through which the cost of the job can be

calculated easily.

Job costing system can be tailor made as per the requirement of a customer because there are

many customers who do not like to include all such kinds of cost in the job they want to get

done. Such customers only want to add the cost which they wanted in their job so they get their

job costing system customised as per their requirement. (Drury, 2013).

b)

I. Different types of managerial accounting reports

1. Managerial accounting reports-

Management Accounting reports are various tools which helps in decision making and helps the

department managers to understand what is going in the business and is the business running

smoothly. Mangerial Accounting reporting also includes collecting various data from various

other operations and combining them and working according to the Generally Accepted

Accounting Principles where during managerial accounting report are very helpful in providing

data to the internal team. (Drury, 2013).

Types of Managerial accounting reports-

a. Financial reports- Financial report is the type of managerial accounting reports where the user's

of the report can find the profit and loss statement which tells about the company and the amount

the company has spent, the amount the company has earned .It Breaks the numbers into various

categories and also provides the detailed profit that the company is being earning everyday,

every week and every year. The balance sheet that the financial report provides to the company

summarizes the data and provides how much the company is earning how much the company

owes to the outsiders. Managerial accounting is very useful and these financial reports make

9

and overheads in a particular service job. The amount of direct material, direct labour and

overheads are to be calculated for estimating the cost of a particular service job such 3 costs are

then combined together and the cost of a job is calculated and such calculation of all the jobs

together is being done by the job costing system through through which the cost of the job can be

calculated easily.

Job costing system can be tailor made as per the requirement of a customer because there are

many customers who do not like to include all such kinds of cost in the job they want to get

done. Such customers only want to add the cost which they wanted in their job so they get their

job costing system customised as per their requirement. (Drury, 2013).

b)

I. Different types of managerial accounting reports

1. Managerial accounting reports-

Management Accounting reports are various tools which helps in decision making and helps the

department managers to understand what is going in the business and is the business running

smoothly. Mangerial Accounting reporting also includes collecting various data from various

other operations and combining them and working according to the Generally Accepted

Accounting Principles where during managerial accounting report are very helpful in providing

data to the internal team. (Drury, 2013).

Types of Managerial accounting reports-

a. Financial reports- Financial report is the type of managerial accounting reports where the user's

of the report can find the profit and loss statement which tells about the company and the amount

the company has spent, the amount the company has earned .It Breaks the numbers into various

categories and also provides the detailed profit that the company is being earning everyday,

every week and every year. The balance sheet that the financial report provides to the company

summarizes the data and provides how much the company is earning how much the company

owes to the outsiders. Managerial accounting is very useful and these financial reports make

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them more useful as they determine how the profits and the losses of the company have played

out over time and what is the company's current net worth and how much the company is

carrying the liquid cash for their available operations. (Drury, 2013).

b. Pro forma cash flow-

Cash flow statement is a type of managerial accounting report which gives week by week

summary of incoming and outgoing cash flows which provides the company to anticipate the

shortfalls and the gains that the company has .Proforma cash flow can also be subdivided into a

short term proforma cash flow report and long term cash flow report considering both together

short term proforma cash flow report is found more useful than a long-term pro forma cash flow

report.

c. Sales report-Sales reports are highly useful for the company’s Management Accounting as they

help and identify sources of the company's revenue and also guides the company as to which

aspects of the business are most and least successful .Sales report basically focuses on the

business activities which provides the user with the activities that earn the most revenue for the

company and also it provides which salesperson are generating more revenue for the company by

taking the least income from the company.

II. Why it is important for the information to be presented in manner that must be

understandable.

2. Nowadays presentation is what matters if the data provided in the report to the management

accounting is not understandable is not presentable it cannot be understood. The user will not be

able to understand what the data provider has provided in the reports if such data is not arranged

is not presented properly. Such reports will be of no use for the users. So that the users can easily

understand the data in the reports shall be presentable (Weygandt, et. al., 2015).

10

out over time and what is the company's current net worth and how much the company is

carrying the liquid cash for their available operations. (Drury, 2013).

b. Pro forma cash flow-

Cash flow statement is a type of managerial accounting report which gives week by week

summary of incoming and outgoing cash flows which provides the company to anticipate the

shortfalls and the gains that the company has .Proforma cash flow can also be subdivided into a

short term proforma cash flow report and long term cash flow report considering both together

short term proforma cash flow report is found more useful than a long-term pro forma cash flow

report.

c. Sales report-Sales reports are highly useful for the company’s Management Accounting as they

help and identify sources of the company's revenue and also guides the company as to which

aspects of the business are most and least successful .Sales report basically focuses on the

business activities which provides the user with the activities that earn the most revenue for the

company and also it provides which salesperson are generating more revenue for the company by

taking the least income from the company.

II. Why it is important for the information to be presented in manner that must be

understandable.

2. Nowadays presentation is what matters if the data provided in the report to the management

accounting is not understandable is not presentable it cannot be understood. The user will not be

able to understand what the data provider has provided in the reports if such data is not arranged

is not presented properly. Such reports will be of no use for the users. So that the users can easily

understand the data in the reports shall be presentable (Weygandt, et. al., 2015).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

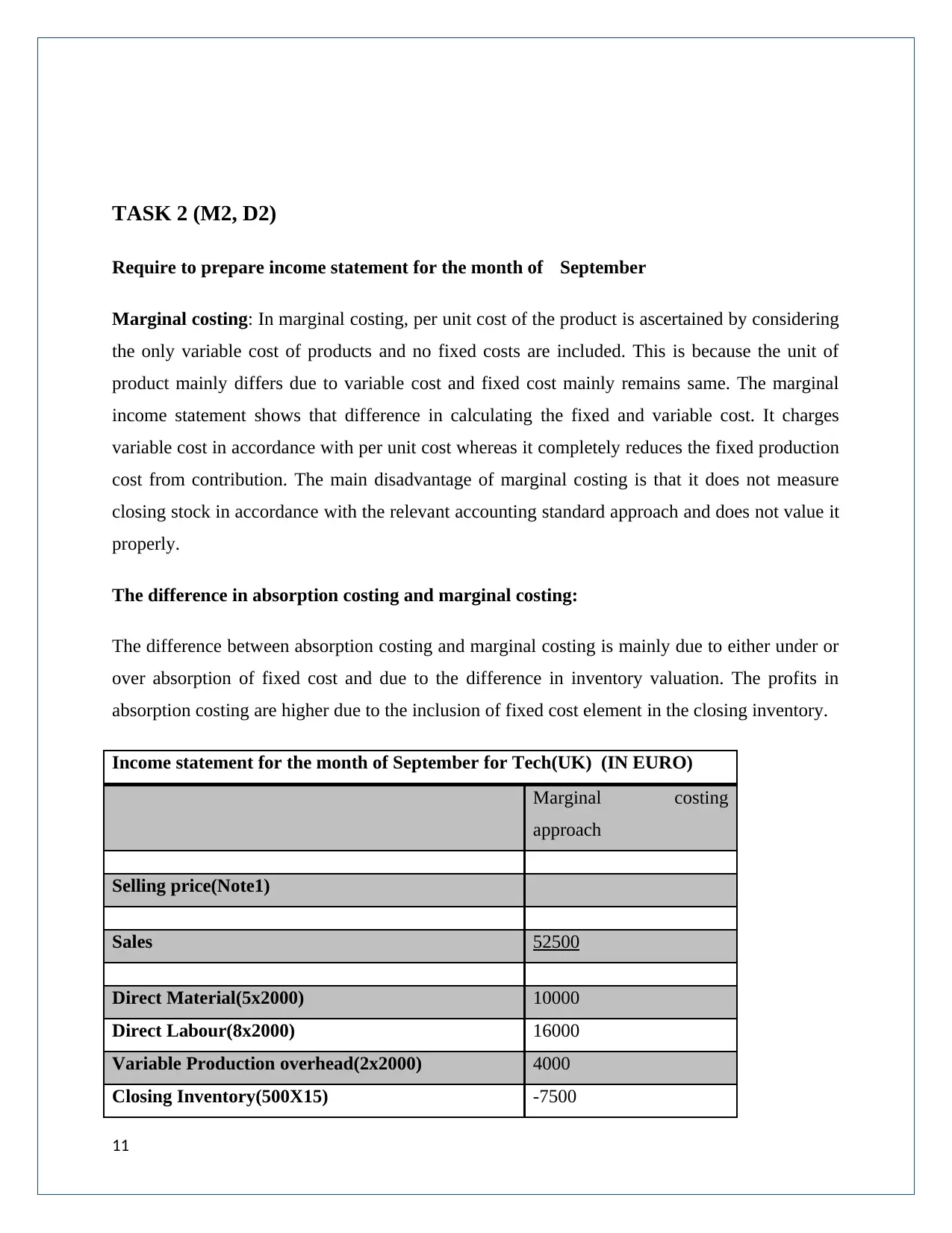

TASK 2 (M2, D2)

Require to prepare income statement for the month of September

Marginal costing: In marginal costing, per unit cost of the product is ascertained by considering

the only variable cost of products and no fixed costs are included. This is because the unit of

product mainly differs due to variable cost and fixed cost mainly remains same. The marginal

income statement shows that difference in calculating the fixed and variable cost. It charges

variable cost in accordance with per unit cost whereas it completely reduces the fixed production

cost from contribution. The main disadvantage of marginal costing is that it does not measure

closing stock in accordance with the relevant accounting standard approach and does not value it

properly.

The difference in absorption costing and marginal costing:

The difference between absorption costing and marginal costing is mainly due to either under or

over absorption of fixed cost and due to the difference in inventory valuation. The profits in

absorption costing are higher due to the inclusion of fixed cost element in the closing inventory.

Income statement for the month of September for Tech(UK) (IN EURO)

Marginal costing

approach

Selling price(Note1)

Sales 52500

Direct Material(5x2000) 10000

Direct Labour(8x2000) 16000

Variable Production overhead(2x2000) 4000

Closing Inventory(500X15) -7500

11

Require to prepare income statement for the month of September

Marginal costing: In marginal costing, per unit cost of the product is ascertained by considering

the only variable cost of products and no fixed costs are included. This is because the unit of

product mainly differs due to variable cost and fixed cost mainly remains same. The marginal

income statement shows that difference in calculating the fixed and variable cost. It charges

variable cost in accordance with per unit cost whereas it completely reduces the fixed production

cost from contribution. The main disadvantage of marginal costing is that it does not measure

closing stock in accordance with the relevant accounting standard approach and does not value it

properly.

The difference in absorption costing and marginal costing:

The difference between absorption costing and marginal costing is mainly due to either under or

over absorption of fixed cost and due to the difference in inventory valuation. The profits in

absorption costing are higher due to the inclusion of fixed cost element in the closing inventory.

Income statement for the month of September for Tech(UK) (IN EURO)

Marginal costing

approach

Selling price(Note1)

Sales 52500

Direct Material(5x2000) 10000

Direct Labour(8x2000) 16000

Variable Production overhead(2x2000) 4000

Closing Inventory(500X15) -7500

11

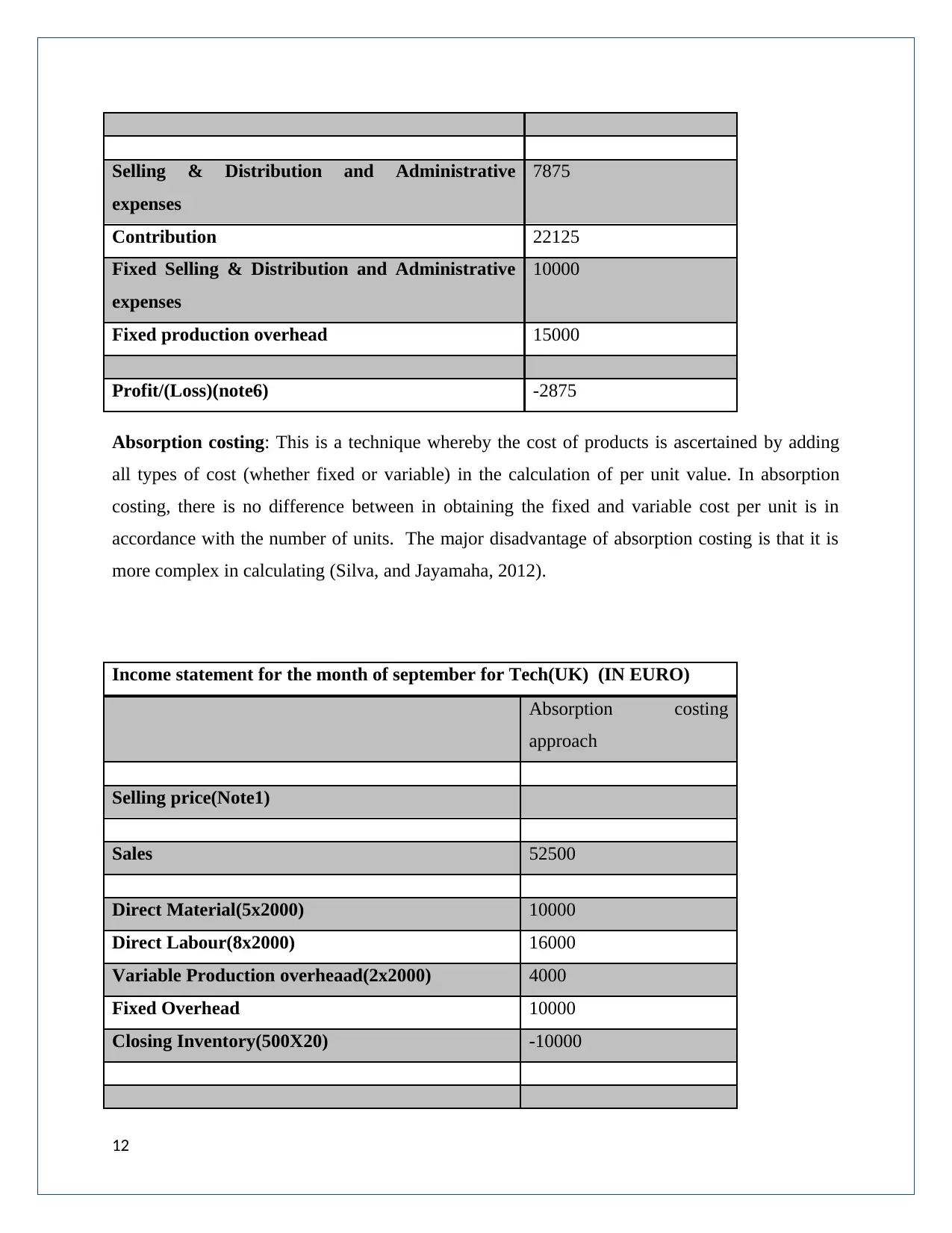

Selling & Distribution and Administrative

expenses

7875

Contribution 22125

Fixed Selling & Distribution and Administrative

expenses

10000

Fixed production overhead 15000

Profit/(Loss)(note6) -2875

Absorption costing: This is a technique whereby the cost of products is ascertained by adding

all types of cost (whether fixed or variable) in the calculation of per unit value. In absorption

costing, there is no difference between in obtaining the fixed and variable cost per unit is in

accordance with the number of units. The major disadvantage of absorption costing is that it is

more complex in calculating (Silva, and Jayamaha, 2012).

Income statement for the month of september for Tech(UK) (IN EURO)

Absorption costing

approach

Selling price(Note1)

Sales 52500

Direct Material(5x2000) 10000

Direct Labour(8x2000) 16000

Variable Production overheaad(2x2000) 4000

Fixed Overhead 10000

Closing Inventory(500X20) -10000

12

expenses

7875

Contribution 22125

Fixed Selling & Distribution and Administrative

expenses

10000

Fixed production overhead 15000

Profit/(Loss)(note6) -2875

Absorption costing: This is a technique whereby the cost of products is ascertained by adding

all types of cost (whether fixed or variable) in the calculation of per unit value. In absorption

costing, there is no difference between in obtaining the fixed and variable cost per unit is in

accordance with the number of units. The major disadvantage of absorption costing is that it is

more complex in calculating (Silva, and Jayamaha, 2012).

Income statement for the month of september for Tech(UK) (IN EURO)

Absorption costing

approach

Selling price(Note1)

Sales 52500

Direct Material(5x2000) 10000

Direct Labour(8x2000) 16000

Variable Production overheaad(2x2000) 4000

Fixed Overhead 10000

Closing Inventory(500X20) -10000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.