Analysis of Management Accounting Techniques: Cost Measurement Methods

VerifiedAdded on 2020/06/04

|6

|769

|98

Homework Assignment

AI Summary

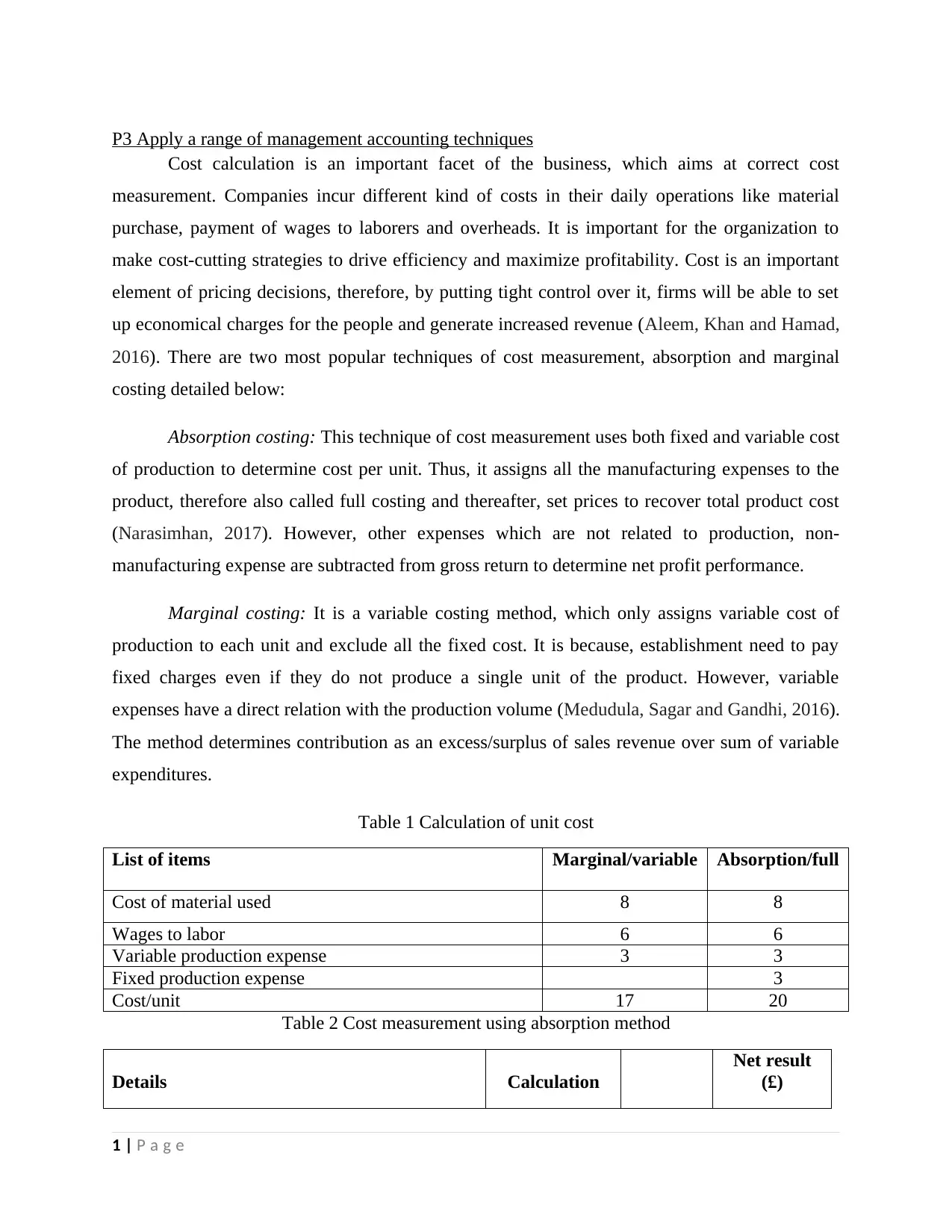

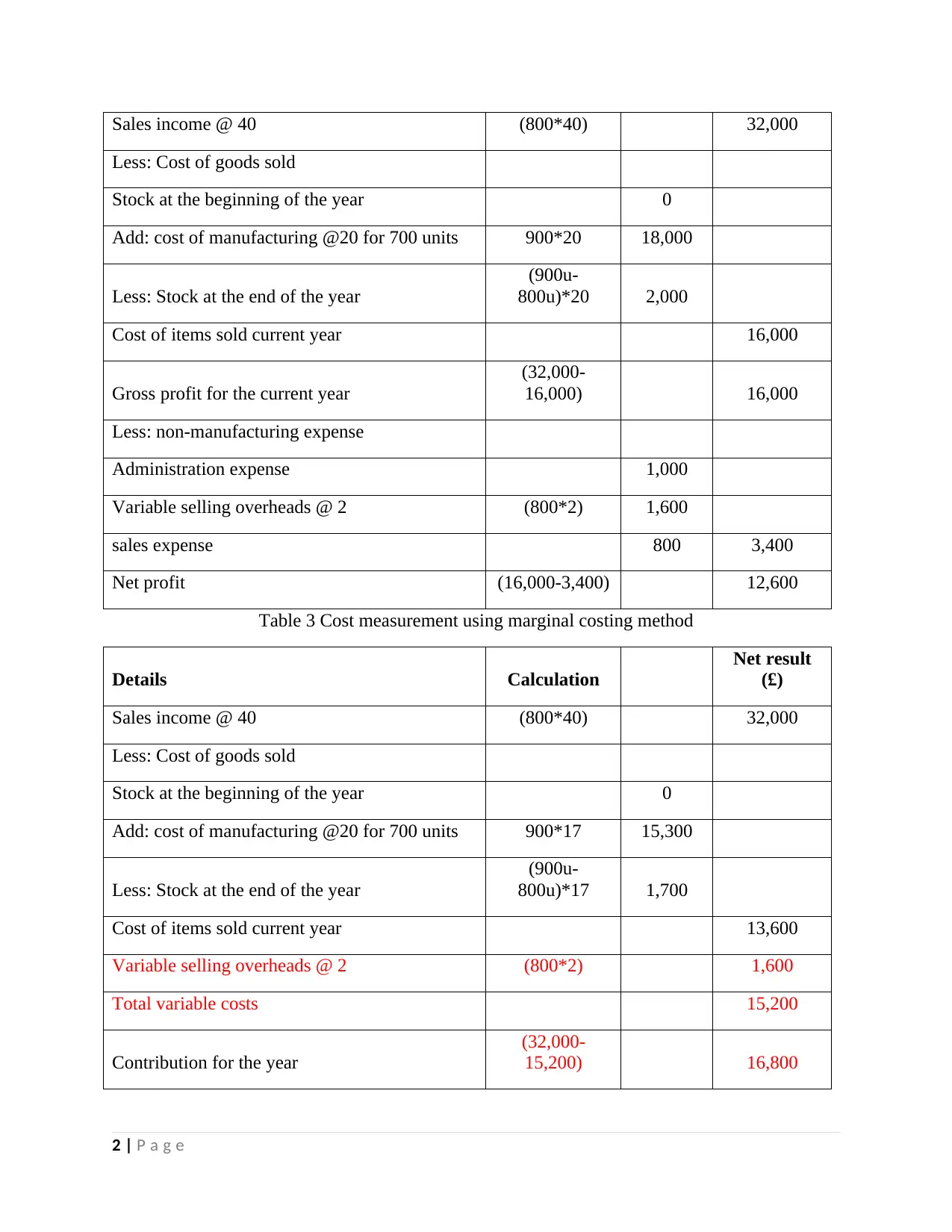

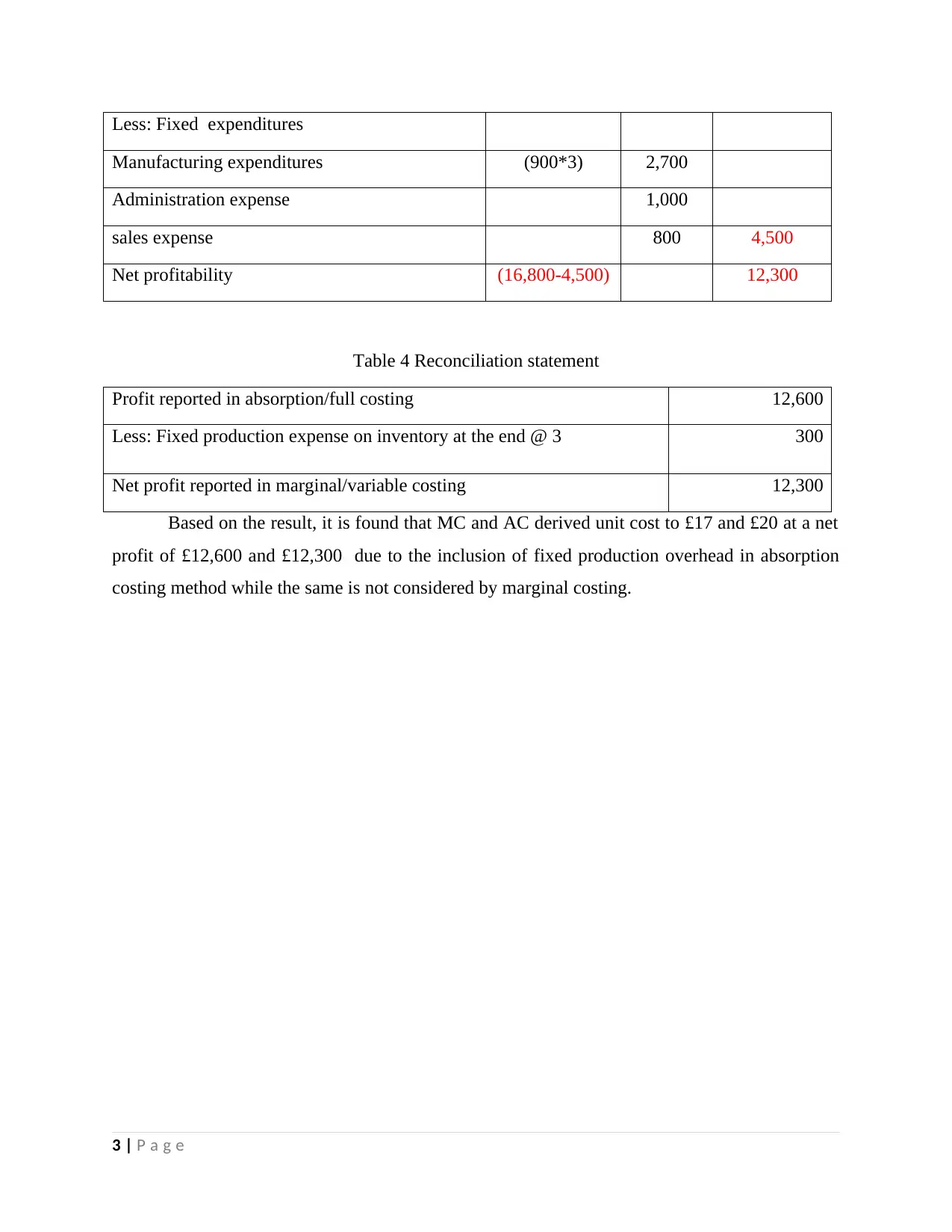

This assignment delves into the core concepts of management accounting, focusing on two primary costing techniques: absorption costing and marginal costing. It elucidates the methods for calculating unit costs, considering both fixed and variable production expenses. The document presents detailed calculations through tables, illustrating the application of each costing method and their impact on profit determination. Absorption costing, also known as full costing, allocates all manufacturing expenses to the product, while marginal costing only assigns variable costs. The assignment includes a reconciliation statement to compare the net profits derived from both methods. The analysis highlights how these techniques influence cost measurement, pricing decisions, and overall financial performance, supported by references to relevant literature.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.