Management Accounting Report: Costing, Budgeting, and Reporting

VerifiedAdded on 2020/09/17

|13

|4315

|69

Report

AI Summary

This management accounting report analyzes the application of various accounting systems and techniques within the context of Zylla Company, a multinational corporation. The report explores different management accounting systems like inventory management, job costing, price optimization, and cost accounting, highlighting their essential requirements. It then delves into different reporting methods such as accounts payable, accounts receivable, job cost, inventory control, and budgetary reporting. The core of the report compares and contrasts marginal and absorption costing methods, illustrating the key differences through a practical example. Furthermore, it examines the advantages and disadvantages of planning tools used in budgetary control and proposes ways to respond to financial problems using management techniques. The report provides a comprehensive overview of management accounting principles, making it a valuable resource for students and professionals alike.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM involving management accounting and its different system

together with various costing techniques and reporting to enable the company to execute it.

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM involving management accounting and its different system

together with various costing techniques and reporting to enable the company to execute it.

Table of Contents

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Different management accounting systems and their essential requirements..................2

P2. Different methods which can be taken into account for management accounting reporting3

TASK 2............................................................................................................................................5

P3. Key differences between income statement developed through marginal and absorption

costing.....................................................................................................................................5

TASK 3............................................................................................................................................6

P4. Advantages and disadvantages of planning tools used in budgetary control...................6

TASK 4............................................................................................................................................9

P5. Ways for responding to financial problems.....................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

P1. Different management accounting systems and their essential requirements..................2

P2. Different methods which can be taken into account for management accounting reporting3

TASK 2............................................................................................................................................5

P3. Key differences between income statement developed through marginal and absorption

costing.....................................................................................................................................5

TASK 3............................................................................................................................................6

P4. Advantages and disadvantages of planning tools used in budgetary control...................6

TASK 4............................................................................................................................................9

P5. Ways for responding to financial problems.....................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

It has been analysed that every day, there are number of challenges which are faced by

organisation and due to these they have to adopt new and different approaches of accounts.

Management accounting can be defined as the process of developing different financial and non-

financial documents which help managers in making right decisions. This report will be

highlighting different requirements of various kinds of management accounting and for this

same, Zylla Company will be chosen which a multinational company with reference to which all

concepts will be explained. It also briefs about various methods of reporting along with

advantages and disadvantages of planning tools which are used in budgetary control. This covers

the major part of assignment and there will an income statement framed by using marginal and

absorption costing methods as well. Also, ways to overcome various problems faced by

organisation by using different management techniques are highlighted as well.

TASK 1

P1. Different management accounting systems and their essential requirements

Organisations whose business is expanded all over the world in different countries cannot

much rely on old techniques of financial accounting. With the variation in business environment,

the needs of managerial accounts is rising and the reason behind this is that it emphasises on

developing future plans and policies of organisation. Its various systems are used for the

interpretation of financial data. When an enterprise initiates their business, they come up with

various problems which firm has to deal with and acts as a barrier in achieving more profits. The

tools which are part of current modern accounting has objectives of framing strategies which can

resolve the troubles of organisation.

In earlier scenario, finance area was restricted to taxation, costing, etc. But, in the current

era, they have to look at the factors like plans of rivals and trends in industry, etc. Through

reducing the process cost the profits margins can be increased. It is an important part of

management accounting and is an internal process. The other way to increase profits is to hike

sales of products and services. For this, it is required that there should be large investment

decision thus knowing the areas where investment can be done or where it is difficult to do.

Thus, it can be said that for such decisions managerial accounting is required.

Following are some of the management accounting systems:

2

It has been analysed that every day, there are number of challenges which are faced by

organisation and due to these they have to adopt new and different approaches of accounts.

Management accounting can be defined as the process of developing different financial and non-

financial documents which help managers in making right decisions. This report will be

highlighting different requirements of various kinds of management accounting and for this

same, Zylla Company will be chosen which a multinational company with reference to which all

concepts will be explained. It also briefs about various methods of reporting along with

advantages and disadvantages of planning tools which are used in budgetary control. This covers

the major part of assignment and there will an income statement framed by using marginal and

absorption costing methods as well. Also, ways to overcome various problems faced by

organisation by using different management techniques are highlighted as well.

TASK 1

P1. Different management accounting systems and their essential requirements

Organisations whose business is expanded all over the world in different countries cannot

much rely on old techniques of financial accounting. With the variation in business environment,

the needs of managerial accounts is rising and the reason behind this is that it emphasises on

developing future plans and policies of organisation. Its various systems are used for the

interpretation of financial data. When an enterprise initiates their business, they come up with

various problems which firm has to deal with and acts as a barrier in achieving more profits. The

tools which are part of current modern accounting has objectives of framing strategies which can

resolve the troubles of organisation.

In earlier scenario, finance area was restricted to taxation, costing, etc. But, in the current

era, they have to look at the factors like plans of rivals and trends in industry, etc. Through

reducing the process cost the profits margins can be increased. It is an important part of

management accounting and is an internal process. The other way to increase profits is to hike

sales of products and services. For this, it is required that there should be large investment

decision thus knowing the areas where investment can be done or where it is difficult to do.

Thus, it can be said that for such decisions managerial accounting is required.

Following are some of the management accounting systems:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory Management System: - The business of Zylla is complex as they are

operating their business in different nations. So, it becomes a little challenging task for them.

This area of management accounting is concerned with the issues of keeping more or less needed

inventory which should be available in warehouse of an organisation. In back time, companies

used to keep and maintain record through manually recording but now they utilise current

technology like EOQ, determining carrying and ordering cost. It is observed that in scenario if

an organisation stocks a large in warehouses then it will directly increase process cost and

chances of wastage of resources increases. On the other hand, if stocks are less in store, this will

also affect the organisation in a negative way and supply chain management of firm as well.

Job Costing: - This gives them an idea that which activity is hampering their profits in

negative way or becoming burden on organisation. Through this, they can eliminate that activity

which is increasing process cost and thus, helping them in achieving the goals of organisation.

Price Optimisation: - It is required that a product should be sold on suitable price so that

price set will be favourable for both sellers and buyers. The management use this technique in

identifying that what will be the right cost at which they can sell the product and on the other

hand, it also gives profit to organisation. This is required because most of the consumers avoid

buying any product if it is expensive and thus, decreasing its demand in market.

Cost Accounting System: - Costing is most crucial factor for business and if they

decrease cost then it will directly increase the profit. Cost accounting reduces chances of

wastage of resources and it can be achieved through decreasing the unnecessary expenses. Its

scope is large and affect almost all areas of company.

P2. Different methods which can be taken into account for management accounting reporting

Developing report is quite an important task as this is a summary of the work which has

been carried out in past and thus it can be said that it can be used for analysing the business

profits and losses etc. Through referring to such reports they can make certain decision through

looking at their future plans. With this they get an idea that what are the areas where they are

lagging behind and making mistakes. Working on the mistakes for their growth in future is quite

necessary for expansion in business market. Following are some of the forms of reporting that

are as follows:-

Account Payable Reporting:- This kind of report is used to know the amount which has

to be paid to their creditors along with the due amounts. Suppliers are the key aspects of business

3

operating their business in different nations. So, it becomes a little challenging task for them.

This area of management accounting is concerned with the issues of keeping more or less needed

inventory which should be available in warehouse of an organisation. In back time, companies

used to keep and maintain record through manually recording but now they utilise current

technology like EOQ, determining carrying and ordering cost. It is observed that in scenario if

an organisation stocks a large in warehouses then it will directly increase process cost and

chances of wastage of resources increases. On the other hand, if stocks are less in store, this will

also affect the organisation in a negative way and supply chain management of firm as well.

Job Costing: - This gives them an idea that which activity is hampering their profits in

negative way or becoming burden on organisation. Through this, they can eliminate that activity

which is increasing process cost and thus, helping them in achieving the goals of organisation.

Price Optimisation: - It is required that a product should be sold on suitable price so that

price set will be favourable for both sellers and buyers. The management use this technique in

identifying that what will be the right cost at which they can sell the product and on the other

hand, it also gives profit to organisation. This is required because most of the consumers avoid

buying any product if it is expensive and thus, decreasing its demand in market.

Cost Accounting System: - Costing is most crucial factor for business and if they

decrease cost then it will directly increase the profit. Cost accounting reduces chances of

wastage of resources and it can be achieved through decreasing the unnecessary expenses. Its

scope is large and affect almost all areas of company.

P2. Different methods which can be taken into account for management accounting reporting

Developing report is quite an important task as this is a summary of the work which has

been carried out in past and thus it can be said that it can be used for analysing the business

profits and losses etc. Through referring to such reports they can make certain decision through

looking at their future plans. With this they get an idea that what are the areas where they are

lagging behind and making mistakes. Working on the mistakes for their growth in future is quite

necessary for expansion in business market. Following are some of the forms of reporting that

are as follows:-

Account Payable Reporting:- This kind of report is used to know the amount which has

to be paid to their creditors along with the due amounts. Suppliers are the key aspects of business

3

and are considered as stakeholders for organisation like Zylla as they provide them raw materials

and other resources used in their process. It is necessary that they should be given their payments

on time so that they can improve their services and Zylla credibility will increase. There are

some of the firms who develop such reports by considering the amount which others prefers

duration of credit. There are no certain standards and regulations which has to be followed to

adopt this into business model. This can be used to ensure that there is proper relation with the

suppliers of organisation and on the other hand account payable reporting can be also used for

making future policies and plans concerned with creditors.

Account Receivable Reporting:- Debtors can be called as individuals or companies who

own money to organisation. This kind of reporting is useful in getting information about debtors

who has purchased goods from the company on credit thus it also includes the time period which

is given to them to repay the amount. The two ways which can be considered in this is time and

the other one is amount. The objective of such kind of reporting is to reduce the chances of bad

debts. Manager at Zylla ensures that they regularly frame this kind of report so that an insight

about the debtors who are not paying due amount in time and as a result they can blacklist them.

This way they can save lots of money of company and will regularly get the details of debtors

who should not get the products on credit from firm.

Job Cost Reporting:- Profits attained through the business activities can be analysed

through developing such report and it is the duty of manager to make this. It can be said that the

usefulness of activities can be find out and those who are not giving them good profit and there is

usage of more resources in it they can they can eliminate such activity. Most of these operations

are part of manufacturing process thus they have the aim of minimising expenditure of resources.

Inventory Control Reporting:- Due to lots of production MNC's find it challenging to

maintain their stock. To overcome such situation inventory control report is framed with the aim

of finding right quality of goods which should be ordered on one time. Overstocking and under-

stocking are two issues which can hamper multinational organisation profits. The solution for

this problem lies in with inventory control reporting and in this they have option of using

economic order quality (EOQ). With this kind of tool they can reduce carrying and ordering

costs which are part of managing inventory. It briefs or gives details about the time period when

the organisation did not have required good or certain raw materials which are required for the

production process. It has been seen that organisation store lots of good in warehouses more than

4

and other resources used in their process. It is necessary that they should be given their payments

on time so that they can improve their services and Zylla credibility will increase. There are

some of the firms who develop such reports by considering the amount which others prefers

duration of credit. There are no certain standards and regulations which has to be followed to

adopt this into business model. This can be used to ensure that there is proper relation with the

suppliers of organisation and on the other hand account payable reporting can be also used for

making future policies and plans concerned with creditors.

Account Receivable Reporting:- Debtors can be called as individuals or companies who

own money to organisation. This kind of reporting is useful in getting information about debtors

who has purchased goods from the company on credit thus it also includes the time period which

is given to them to repay the amount. The two ways which can be considered in this is time and

the other one is amount. The objective of such kind of reporting is to reduce the chances of bad

debts. Manager at Zylla ensures that they regularly frame this kind of report so that an insight

about the debtors who are not paying due amount in time and as a result they can blacklist them.

This way they can save lots of money of company and will regularly get the details of debtors

who should not get the products on credit from firm.

Job Cost Reporting:- Profits attained through the business activities can be analysed

through developing such report and it is the duty of manager to make this. It can be said that the

usefulness of activities can be find out and those who are not giving them good profit and there is

usage of more resources in it they can they can eliminate such activity. Most of these operations

are part of manufacturing process thus they have the aim of minimising expenditure of resources.

Inventory Control Reporting:- Due to lots of production MNC's find it challenging to

maintain their stock. To overcome such situation inventory control report is framed with the aim

of finding right quality of goods which should be ordered on one time. Overstocking and under-

stocking are two issues which can hamper multinational organisation profits. The solution for

this problem lies in with inventory control reporting and in this they have option of using

economic order quality (EOQ). With this kind of tool they can reduce carrying and ordering

costs which are part of managing inventory. It briefs or gives details about the time period when

the organisation did not have required good or certain raw materials which are required for the

production process. It has been seen that organisation store lots of good in warehouses more than

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

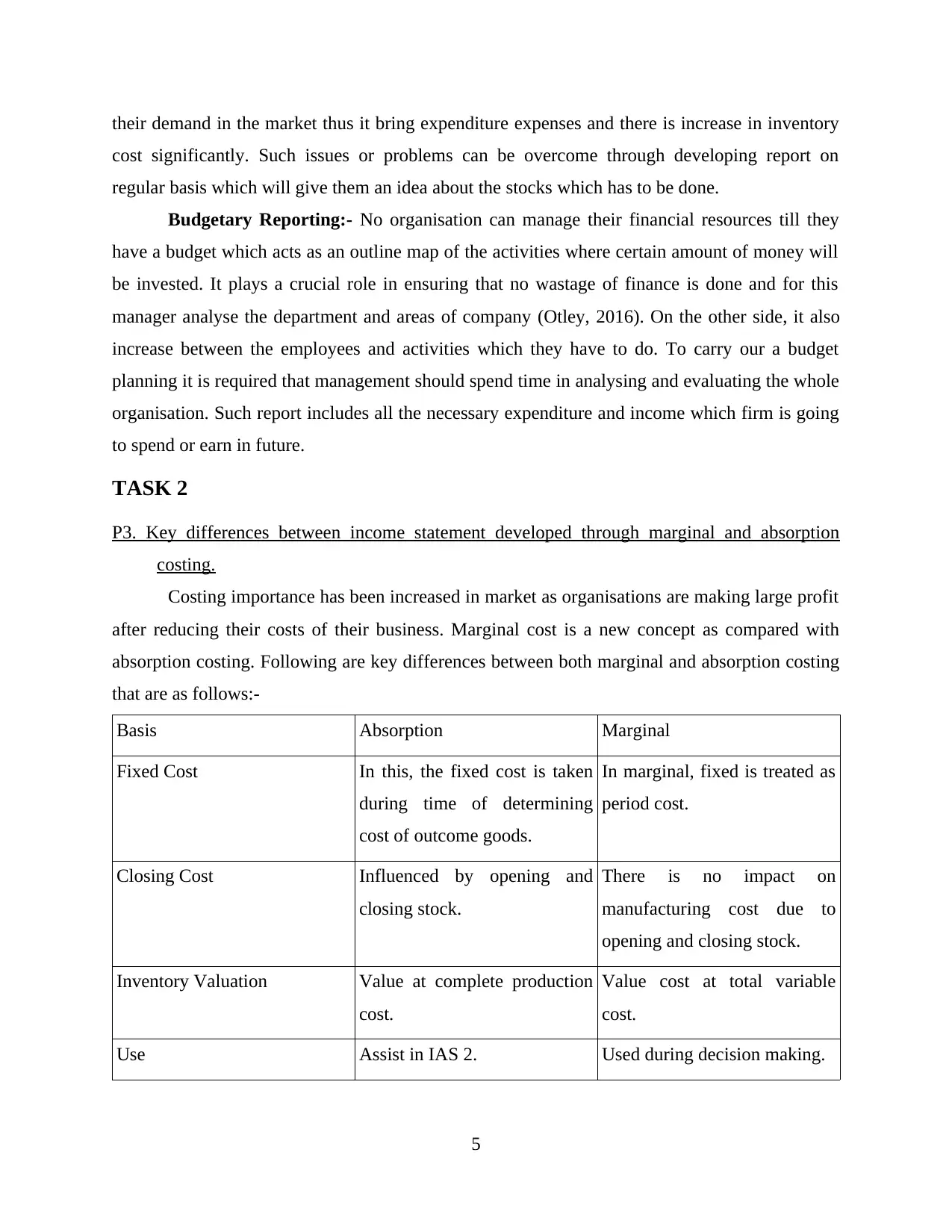

their demand in the market thus it bring expenditure expenses and there is increase in inventory

cost significantly. Such issues or problems can be overcome through developing report on

regular basis which will give them an idea about the stocks which has to be done.

Budgetary Reporting:- No organisation can manage their financial resources till they

have a budget which acts as an outline map of the activities where certain amount of money will

be invested. It plays a crucial role in ensuring that no wastage of finance is done and for this

manager analyse the department and areas of company (Otley, 2016). On the other side, it also

increase between the employees and activities which they have to do. To carry our a budget

planning it is required that management should spend time in analysing and evaluating the whole

organisation. Such report includes all the necessary expenditure and income which firm is going

to spend or earn in future.

TASK 2

P3. Key differences between income statement developed through marginal and absorption

costing.

Costing importance has been increased in market as organisations are making large profit

after reducing their costs of their business. Marginal cost is a new concept as compared with

absorption costing. Following are key differences between both marginal and absorption costing

that are as follows:-

Basis Absorption Marginal

Fixed Cost In this, the fixed cost is taken

during time of determining

cost of outcome goods.

In marginal, fixed is treated as

period cost.

Closing Cost Influenced by opening and

closing stock.

There is no impact on

manufacturing cost due to

opening and closing stock.

Inventory Valuation Value at complete production

cost.

Value cost at total variable

cost.

Use Assist in IAS 2. Used during decision making.

5

cost significantly. Such issues or problems can be overcome through developing report on

regular basis which will give them an idea about the stocks which has to be done.

Budgetary Reporting:- No organisation can manage their financial resources till they

have a budget which acts as an outline map of the activities where certain amount of money will

be invested. It plays a crucial role in ensuring that no wastage of finance is done and for this

manager analyse the department and areas of company (Otley, 2016). On the other side, it also

increase between the employees and activities which they have to do. To carry our a budget

planning it is required that management should spend time in analysing and evaluating the whole

organisation. Such report includes all the necessary expenditure and income which firm is going

to spend or earn in future.

TASK 2

P3. Key differences between income statement developed through marginal and absorption

costing.

Costing importance has been increased in market as organisations are making large profit

after reducing their costs of their business. Marginal cost is a new concept as compared with

absorption costing. Following are key differences between both marginal and absorption costing

that are as follows:-

Basis Absorption Marginal

Fixed Cost In this, the fixed cost is taken

during time of determining

cost of outcome goods.

In marginal, fixed is treated as

period cost.

Closing Cost Influenced by opening and

closing stock.

There is no impact on

manufacturing cost due to

opening and closing stock.

Inventory Valuation Value at complete production

cost.

Value cost at total variable

cost.

Use Assist in IAS 2. Used during decision making.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

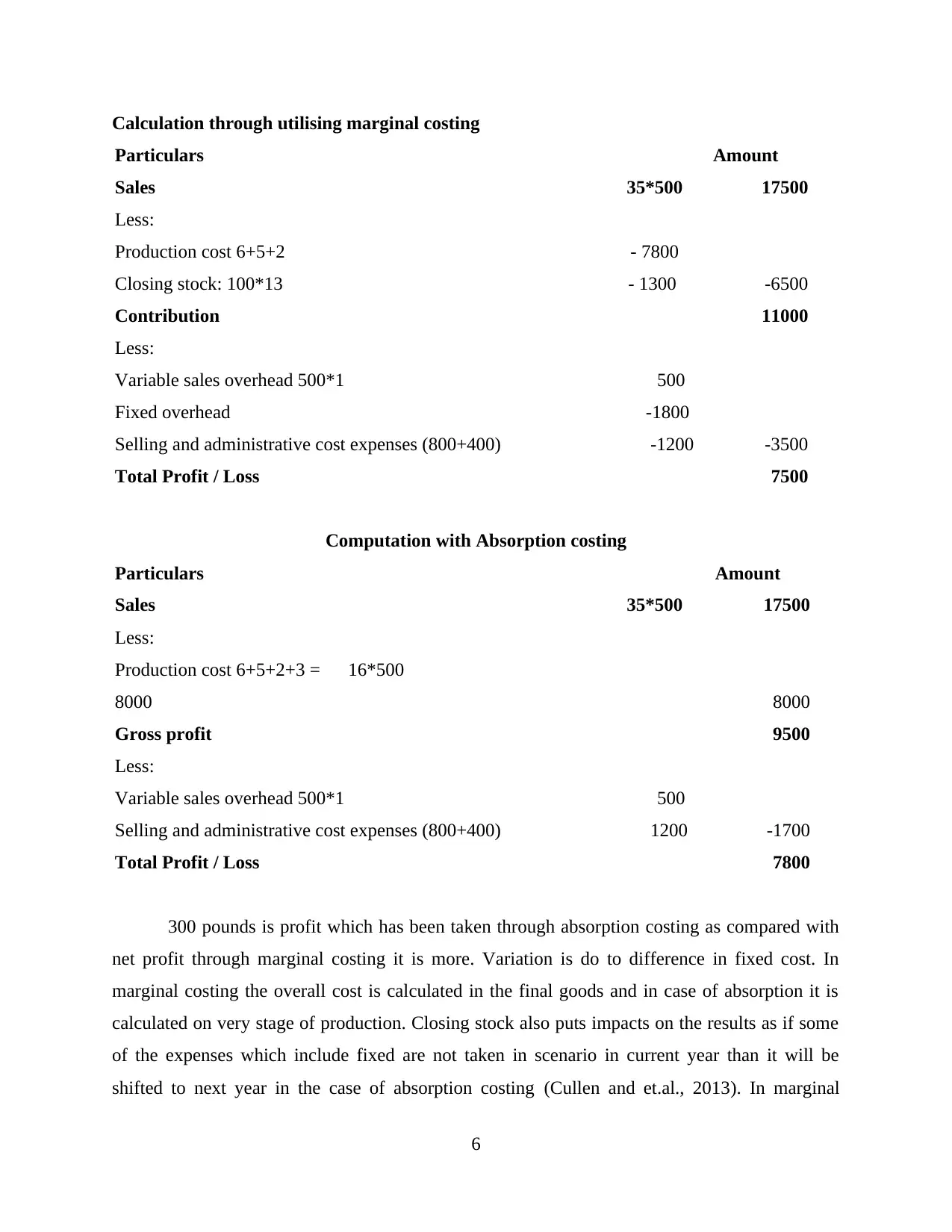

Calculation through utilising marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation with Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

300 pounds is profit which has been taken through absorption costing as compared with

net profit through marginal costing it is more. Variation is do to difference in fixed cost. In

marginal costing the overall cost is calculated in the final goods and in case of absorption it is

calculated on very stage of production. Closing stock also puts impacts on the results as if some

of the expenses which include fixed are not taken in scenario in current year than it will be

shifted to next year in the case of absorption costing (Cullen and et.al., 2013). In marginal

6

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation with Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

300 pounds is profit which has been taken through absorption costing as compared with

net profit through marginal costing it is more. Variation is do to difference in fixed cost. In

marginal costing the overall cost is calculated in the final goods and in case of absorption it is

calculated on very stage of production. Closing stock also puts impacts on the results as if some

of the expenses which include fixed are not taken in scenario in current year than it will be

shifted to next year in the case of absorption costing (Cullen and et.al., 2013). In marginal

6

costing if expenditure like fixed cost is acquired in current year but the closing stock remain at

the end of year the burden of fixed cost will be taken in this year. This includes a unnecessary

cost in the case.

TASK 3

P4. Advantages and disadvantages of planning tools used in budgetary control.

Budgetary control is a long process that make sure that organisation takes proper decision

related to their finance so that they can easily attain the targets which has been set for a particular

time period. This is not a monitoring activity but instead it is more over related to proper

planning. Different companies who are part of business environment use various tools of

planning as they are aware that it is necessary to be prepared themselves for future situations.

This will bring a positive impact on the organisation as the confidence level of staff will go high.

If they have planning then they will find it easier to make their stable position at crisis time

(Parker, 2012). Following are some of crucial planning with their advantages and disadvantage:-

Case Budget:- Due to high liquidity, managing cash is becomes a challenging tasks so it

is required that there should be proper planning for this. This is one of the tool through which

they can know the requirements of finance at difference time and situation. Through cash budget

they can reduce the chances of bad debts and can overcome the hurdles which are coming in

supply chain management and etc (Delafrooz and Paim, 2011). In includes the information about

funds which organisation have to pay to various business bodies in coming time and also states

that how the company will be earning the finance from different platforms like selling of product

or through loan interest which they have provided to certain debtors.

Advantages:- Having the money in sufficient amount will allow them to pay to creditor in

the promised time period. This will improve their image and they will win the trust of suppliers

which will result in some kind of discounts from suppliers. Suppliers are aware that if they will

be giving right materials they will get timely payments. In emergency situation they can easily

buy the materials required for production through case they have instead of credit facility.

Disadvantages:- Some of the companies does not develop cash budget as they think that

ascertaining the needs of liquid assets is not possible. As their continuous change in business

environment has to incorporate in their business and they have to decided what amount will be

enough for particular situation. It is tough to decide the right amount and the other demerit of this

7

the end of year the burden of fixed cost will be taken in this year. This includes a unnecessary

cost in the case.

TASK 3

P4. Advantages and disadvantages of planning tools used in budgetary control.

Budgetary control is a long process that make sure that organisation takes proper decision

related to their finance so that they can easily attain the targets which has been set for a particular

time period. This is not a monitoring activity but instead it is more over related to proper

planning. Different companies who are part of business environment use various tools of

planning as they are aware that it is necessary to be prepared themselves for future situations.

This will bring a positive impact on the organisation as the confidence level of staff will go high.

If they have planning then they will find it easier to make their stable position at crisis time

(Parker, 2012). Following are some of crucial planning with their advantages and disadvantage:-

Case Budget:- Due to high liquidity, managing cash is becomes a challenging tasks so it

is required that there should be proper planning for this. This is one of the tool through which

they can know the requirements of finance at difference time and situation. Through cash budget

they can reduce the chances of bad debts and can overcome the hurdles which are coming in

supply chain management and etc (Delafrooz and Paim, 2011). In includes the information about

funds which organisation have to pay to various business bodies in coming time and also states

that how the company will be earning the finance from different platforms like selling of product

or through loan interest which they have provided to certain debtors.

Advantages:- Having the money in sufficient amount will allow them to pay to creditor in

the promised time period. This will improve their image and they will win the trust of suppliers

which will result in some kind of discounts from suppliers. Suppliers are aware that if they will

be giving right materials they will get timely payments. In emergency situation they can easily

buy the materials required for production through case they have instead of credit facility.

Disadvantages:- Some of the companies does not develop cash budget as they think that

ascertaining the needs of liquid assets is not possible. As their continuous change in business

environment has to incorporate in their business and they have to decided what amount will be

enough for particular situation. It is tough to decide the right amount and the other demerit of this

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is that it is totally based on the previous years budget. As in this the previous years clinging

balance is taken for developing the budget for current year. It is a little risky as there can be large

variations.

Master Budget:- Zylla can incorporated this tool in their business so that they can attain

the goals. It includes sales, marketing, marketing budgets and etc. It has been observed that the

department which are part of the organisation has their own budget but there is a master budget

for the company. It ascertain the income which they may can take out and the expenditure which

are done in the productive organisation (Renz, 2016).

Advantages:- If firm has master budget the chances of conflict reduces and has

information that which department needs to be given how much funds. It might happen that

production department requires more budget than the marketing department and through they

have to use it so that they can attain the goals which has been set. It provides that all demands of

areas in company are met.

Disadvantage:- Small organisation does not believes in the concept of master budget due

to high cost which is required to develop it. There is requirement of a large workforce as it

includes analysing the sales, storage etc. and not only workforce there is requirement of different

resources (Hansen, 2011). Many managers thinks that developing master budget needs a lot of

time and can be considered as a lengthy process and they prefer to frame short budgets thus

giving them better outcomes.

Operating Budget:- Operational planning includes the income and expenses which are

concerned to core revenue generating operations of organisation. Production and administration

are two areas which are emphasised through this planning technique. These are the key areas

where most of the expenditure are done by any company so through this budgeting planning is

also done (Schaltegger and Zvezdov, 2015)

Advantages:- To ensure that more investors should invest in their business it is required

that they should show better operating costs of an investment to the industry. Doing so will

attract a lot of people and they will able to increase their market share along with income of

company. Modifying any budget is a quite complicated task and but in the case of operating

modes the changes can be made easily. Bringing any amendments ensure that every body has

been altered about the changes.

8

balance is taken for developing the budget for current year. It is a little risky as there can be large

variations.

Master Budget:- Zylla can incorporated this tool in their business so that they can attain

the goals. It includes sales, marketing, marketing budgets and etc. It has been observed that the

department which are part of the organisation has their own budget but there is a master budget

for the company. It ascertain the income which they may can take out and the expenditure which

are done in the productive organisation (Renz, 2016).

Advantages:- If firm has master budget the chances of conflict reduces and has

information that which department needs to be given how much funds. It might happen that

production department requires more budget than the marketing department and through they

have to use it so that they can attain the goals which has been set. It provides that all demands of

areas in company are met.

Disadvantage:- Small organisation does not believes in the concept of master budget due

to high cost which is required to develop it. There is requirement of a large workforce as it

includes analysing the sales, storage etc. and not only workforce there is requirement of different

resources (Hansen, 2011). Many managers thinks that developing master budget needs a lot of

time and can be considered as a lengthy process and they prefer to frame short budgets thus

giving them better outcomes.

Operating Budget:- Operational planning includes the income and expenses which are

concerned to core revenue generating operations of organisation. Production and administration

are two areas which are emphasised through this planning technique. These are the key areas

where most of the expenditure are done by any company so through this budgeting planning is

also done (Schaltegger and Zvezdov, 2015)

Advantages:- To ensure that more investors should invest in their business it is required

that they should show better operating costs of an investment to the industry. Doing so will

attract a lot of people and they will able to increase their market share along with income of

company. Modifying any budget is a quite complicated task and but in the case of operating

modes the changes can be made easily. Bringing any amendments ensure that every body has

been altered about the changes.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantage:- Operational budget is restricted to some areas of organisation and can be

called as risky. They have key feature that it is easy to amend and in case if manager regularly

puts some sort of changes it will look that the manager is not at all confident about the plans

thus they are in state of confusion among staff.

Zero Based Budgeting (ZBB):- It is method of budgeting in which all expenditure

should be justified for different new period. It initiates from zero base and each of the

organisation is analysed for their requirements and costs (Hopper and Bui, 2016). Then budgets

are formed around what is required for the upcoming period, whether the budget as compare with

the previous one is higher or lower.

Advantages:- They are flexible budgets, has focused on certain activities and includers

low costs. The implementation of such budgets takes in disciplined way without and unwanted

activity.

Disadvantage:- The blender which comes with this is that there are chances of being

manipulated by different manager thus also showing a bias approach towards short term

planning.

Activity Based Budgeting:- It is a budgeting method in which budgets are developed

through activity based costing after taking into the account for overhead costs. In this the past

year budget is not taken to frame the current year budget. Those activities which are incurred are

analysed and evaluated (Wagenhofer, 2016).

Advantages:- Through this each and every factor can be analysed which are cost driver

thus taking all the levels in consideration which are involved in. Those activities which are not

yielding good results are obstructed out as it helps in viewing the business as a single unit and

not in any division in departments.

Disadvantage:- To use this technique it is required that there should be deep knowledge

of various areas of business and if the manager finds it difficult to understand that the budget

preparation can go in vein. This budgeting planning tool consumes a lot of resources of an

organisation.

9

called as risky. They have key feature that it is easy to amend and in case if manager regularly

puts some sort of changes it will look that the manager is not at all confident about the plans

thus they are in state of confusion among staff.

Zero Based Budgeting (ZBB):- It is method of budgeting in which all expenditure

should be justified for different new period. It initiates from zero base and each of the

organisation is analysed for their requirements and costs (Hopper and Bui, 2016). Then budgets

are formed around what is required for the upcoming period, whether the budget as compare with

the previous one is higher or lower.

Advantages:- They are flexible budgets, has focused on certain activities and includers

low costs. The implementation of such budgets takes in disciplined way without and unwanted

activity.

Disadvantage:- The blender which comes with this is that there are chances of being

manipulated by different manager thus also showing a bias approach towards short term

planning.

Activity Based Budgeting:- It is a budgeting method in which budgets are developed

through activity based costing after taking into the account for overhead costs. In this the past

year budget is not taken to frame the current year budget. Those activities which are incurred are

analysed and evaluated (Wagenhofer, 2016).

Advantages:- Through this each and every factor can be analysed which are cost driver

thus taking all the levels in consideration which are involved in. Those activities which are not

yielding good results are obstructed out as it helps in viewing the business as a single unit and

not in any division in departments.

Disadvantage:- To use this technique it is required that there should be deep knowledge

of various areas of business and if the manager finds it difficult to understand that the budget

preparation can go in vein. This budgeting planning tool consumes a lot of resources of an

organisation.

9

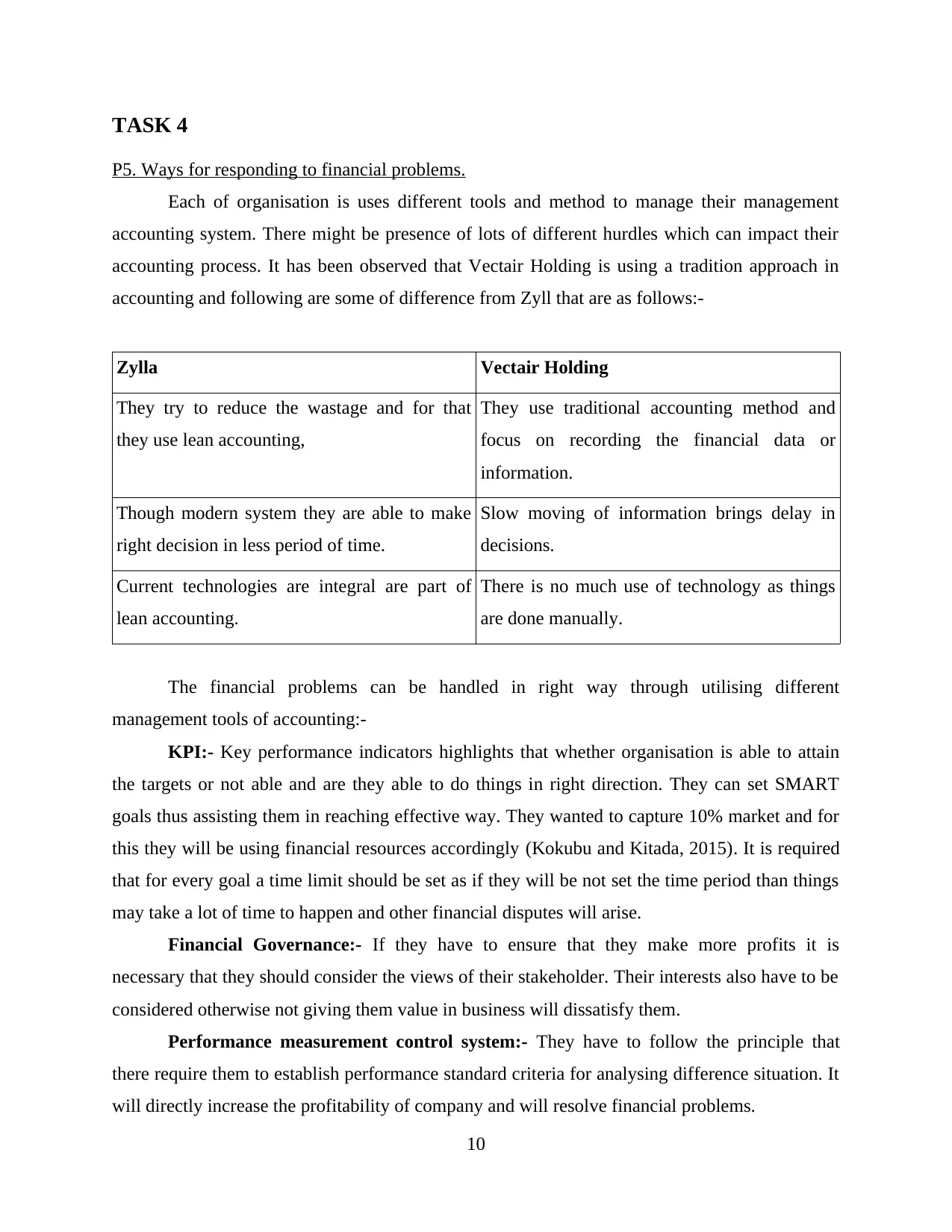

TASK 4

P5. Ways for responding to financial problems.

Each of organisation is uses different tools and method to manage their management

accounting system. There might be presence of lots of different hurdles which can impact their

accounting process. It has been observed that Vectair Holding is using a tradition approach in

accounting and following are some of difference from Zyll that are as follows:-

Zylla Vectair Holding

They try to reduce the wastage and for that

they use lean accounting,

They use traditional accounting method and

focus on recording the financial data or

information.

Though modern system they are able to make

right decision in less period of time.

Slow moving of information brings delay in

decisions.

Current technologies are integral are part of

lean accounting.

There is no much use of technology as things

are done manually.

The financial problems can be handled in right way through utilising different

management tools of accounting:-

KPI:- Key performance indicators highlights that whether organisation is able to attain

the targets or not able and are they able to do things in right direction. They can set SMART

goals thus assisting them in reaching effective way. They wanted to capture 10% market and for

this they will be using financial resources accordingly (Kokubu and Kitada, 2015). It is required

that for every goal a time limit should be set as if they will be not set the time period than things

may take a lot of time to happen and other financial disputes will arise.

Financial Governance:- If they have to ensure that they make more profits it is

necessary that they should consider the views of their stakeholder. Their interests also have to be

considered otherwise not giving them value in business will dissatisfy them.

Performance measurement control system:- They have to follow the principle that

there require them to establish performance standard criteria for analysing difference situation. It

will directly increase the profitability of company and will resolve financial problems.

10

P5. Ways for responding to financial problems.

Each of organisation is uses different tools and method to manage their management

accounting system. There might be presence of lots of different hurdles which can impact their

accounting process. It has been observed that Vectair Holding is using a tradition approach in

accounting and following are some of difference from Zyll that are as follows:-

Zylla Vectair Holding

They try to reduce the wastage and for that

they use lean accounting,

They use traditional accounting method and

focus on recording the financial data or

information.

Though modern system they are able to make

right decision in less period of time.

Slow moving of information brings delay in

decisions.

Current technologies are integral are part of

lean accounting.

There is no much use of technology as things

are done manually.

The financial problems can be handled in right way through utilising different

management tools of accounting:-

KPI:- Key performance indicators highlights that whether organisation is able to attain

the targets or not able and are they able to do things in right direction. They can set SMART

goals thus assisting them in reaching effective way. They wanted to capture 10% market and for

this they will be using financial resources accordingly (Kokubu and Kitada, 2015). It is required

that for every goal a time limit should be set as if they will be not set the time period than things

may take a lot of time to happen and other financial disputes will arise.

Financial Governance:- If they have to ensure that they make more profits it is

necessary that they should consider the views of their stakeholder. Their interests also have to be

considered otherwise not giving them value in business will dissatisfy them.

Performance measurement control system:- They have to follow the principle that

there require them to establish performance standard criteria for analysing difference situation. It

will directly increase the profitability of company and will resolve financial problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.