Management Accounting Report: Systems, Tools, and Decision Making

VerifiedAdded on 2020/06/04

|25

|7774

|197

Report

AI Summary

This report provides a comprehensive overview of management accounting, covering its functions, different systems, and the tools used for effective decision-making. It begins by defining management accounting and differentiating it from financial accounting, highlighting its role in internal strategic development and decision-making processes within a company like Imda Tech. The report delves into various managerial accounting tools such as margin analysis, constraint analysis, and capital budgeting, explaining their importance in evaluating performance, identifying bottlenecks, and making investment decisions. Furthermore, it explores product costing, various management accounting systems including cost accounting, inventory management, job costing, and price optimizing systems. The report also discusses the use of standard costing as a decision-making tool, emphasizing its role in budgeting and inventory costing. Overall, the report provides a detailed analysis of management accounting principles and practices, offering valuable insights for businesses aiming to improve their financial management and strategic planning.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Management Accounting.................................................................................................................1

TASK-1 ...........................................................................................................................................3

P1 Functions of management accounting...............................................................................3

Margin Analysis.....................................................................................................................5

Constraint Analysis................................................................................................................5

Capital Budgeting...................................................................................................................6

Trend Analysis/Forecasting....................................................................................................6

TASK 2............................................................................................................................................6

Product Costing/Valuation.....................................................................................................6

P2 Explain the different types of Management Accounting Systems ...................................6

P3 Marginal absorption costing..............................................................................................9

..............................................................................................................................................10

TASK 3..........................................................................................................................................11

P4 Budgeting method...........................................................................................................11

TASK- 4 ........................................................................................................................................19

P5 Explain what a Balance Score Card approach is and describe how the implementation19

References......................................................................................................................................24

Management Accounting.................................................................................................................1

TASK-1 ...........................................................................................................................................3

P1 Functions of management accounting...............................................................................3

Margin Analysis.....................................................................................................................5

Constraint Analysis................................................................................................................5

Capital Budgeting...................................................................................................................6

Trend Analysis/Forecasting....................................................................................................6

TASK 2............................................................................................................................................6

Product Costing/Valuation.....................................................................................................6

P2 Explain the different types of Management Accounting Systems ...................................6

P3 Marginal absorption costing..............................................................................................9

..............................................................................................................................................10

TASK 3..........................................................................................................................................11

P4 Budgeting method...........................................................................................................11

TASK- 4 ........................................................................................................................................19

P5 Explain what a Balance Score Card approach is and describe how the implementation19

References......................................................................................................................................24

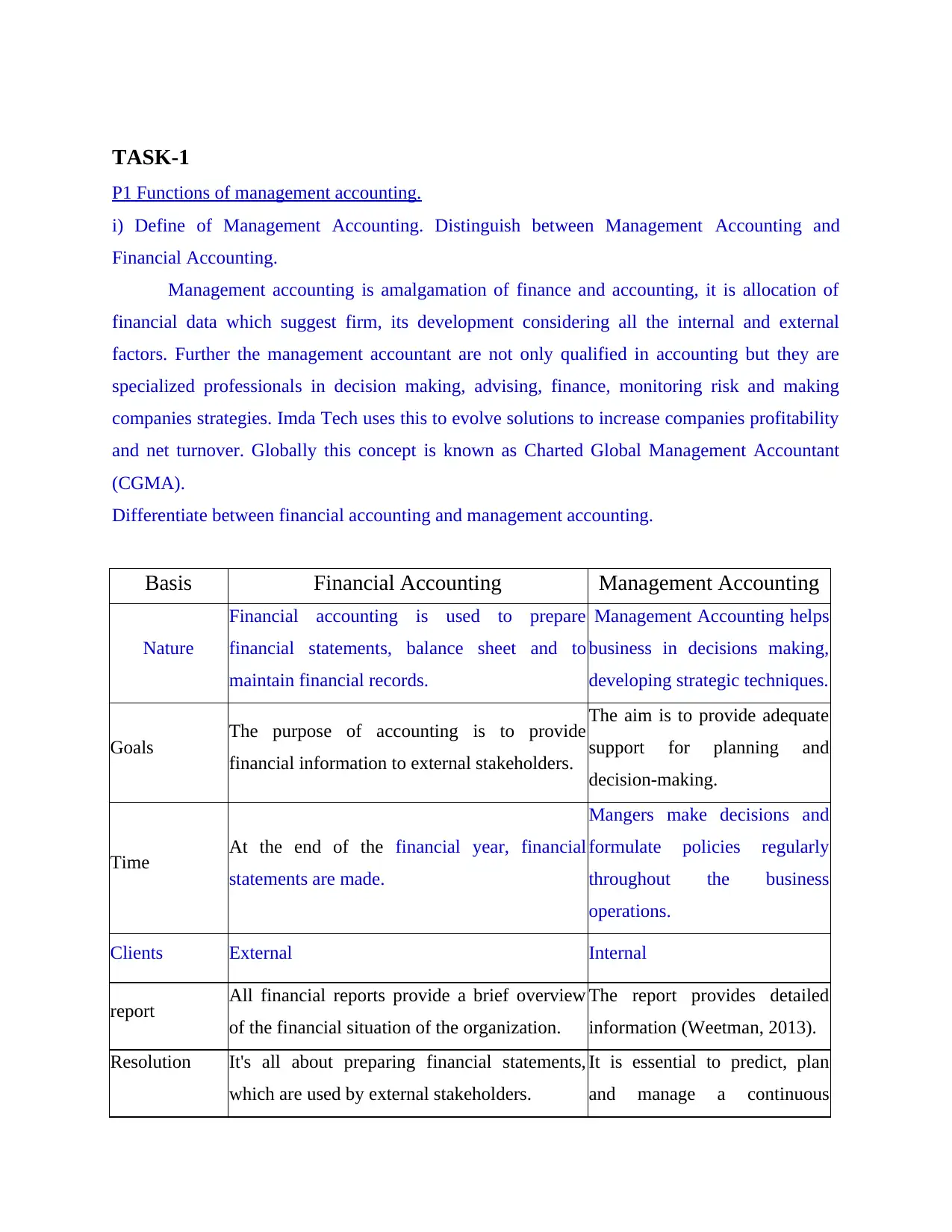

TASK-1

P1 Functions of management accounting.

i) Define of Management Accounting. Distinguish between Management Accounting and

Financial Accounting.

Management accounting is amalgamation of finance and accounting, it is allocation of

financial data which suggest firm, its development considering all the internal and external

factors. Further the management accountant are not only qualified in accounting but they are

specialized professionals in decision making, advising, finance, monitoring risk and making

companies strategies. Imda Tech uses this to evolve solutions to increase companies profitability

and net turnover. Globally this concept is known as Charted Global Management Accountant

(CGMA).

Differentiate between financial accounting and management accounting.

Basis Financial Accounting Management Accounting

Nature

Financial accounting is used to prepare

financial statements, balance sheet and to

maintain financial records.

Management Accounting helps

business in decisions making,

developing strategic techniques.

Goals The purpose of accounting is to provide

financial information to external stakeholders.

The aim is to provide adequate

support for planning and

decision-making.

Time At the end of the financial year, financial

statements are made.

Mangers make decisions and

formulate policies regularly

throughout the business

operations.

Clients External Internal

report All financial reports provide a brief overview

of the financial situation of the organization.

The report provides detailed

information (Weetman, 2013).

Resolution It's all about preparing financial statements,

which are used by external stakeholders.

It is essential to predict, plan

and manage a continuous

P1 Functions of management accounting.

i) Define of Management Accounting. Distinguish between Management Accounting and

Financial Accounting.

Management accounting is amalgamation of finance and accounting, it is allocation of

financial data which suggest firm, its development considering all the internal and external

factors. Further the management accountant are not only qualified in accounting but they are

specialized professionals in decision making, advising, finance, monitoring risk and making

companies strategies. Imda Tech uses this to evolve solutions to increase companies profitability

and net turnover. Globally this concept is known as Charted Global Management Accountant

(CGMA).

Differentiate between financial accounting and management accounting.

Basis Financial Accounting Management Accounting

Nature

Financial accounting is used to prepare

financial statements, balance sheet and to

maintain financial records.

Management Accounting helps

business in decisions making,

developing strategic techniques.

Goals The purpose of accounting is to provide

financial information to external stakeholders.

The aim is to provide adequate

support for planning and

decision-making.

Time At the end of the financial year, financial

statements are made.

Mangers make decisions and

formulate policies regularly

throughout the business

operations.

Clients External Internal

report All financial reports provide a brief overview

of the financial situation of the organization.

The report provides detailed

information (Weetman, 2013).

Resolution It's all about preparing financial statements,

which are used by external stakeholders.

It is essential to predict, plan

and manage a continuous

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

process.

Necessary

information

Financial information is useful to maintain

record of monetary transaction.

Information is helpful in

maintaining quantitative and

qualitative data (Weetman,

2013).

Accounting

branch Financial information is stored.

It tracks all data on financial

and non-financial information,

or collections.

Privacy level It is not a secret, when it is tested and used in

internal and external stakeholders.

Policies and strategies used are

just a set of internal controls

and sufficient to be used. Top

privacy.

Format It has particular form of format for preparation

of financial statements.

This do not have specific

format. (Taipaleenmäki and

Ikäheimo, 2013).

Rules This accounting method is bounded by rules

and regulations like, GAPS and IFRS

In this accounting manager do

not follow any rules just try to

make decisions as per the

business requirement.

Review

The financial statements use it for inspection,

which will help to promote incorrect financial

statements.

No need to check and modify as

a voluntary set of information.

ii) Importance of management accounting information as a decision making tool.

Managerial team of Imda Tech uses different managerial accounting tools and techniques

for the successful decision making process.

The method helps managers in making decisions effective and worth considering for

control and accounting activities. Monitoring control and access over accounting

techniques provides an essential support in regulation with economic activities.

Necessary

information

Financial information is useful to maintain

record of monetary transaction.

Information is helpful in

maintaining quantitative and

qualitative data (Weetman,

2013).

Accounting

branch Financial information is stored.

It tracks all data on financial

and non-financial information,

or collections.

Privacy level It is not a secret, when it is tested and used in

internal and external stakeholders.

Policies and strategies used are

just a set of internal controls

and sufficient to be used. Top

privacy.

Format It has particular form of format for preparation

of financial statements.

This do not have specific

format. (Taipaleenmäki and

Ikäheimo, 2013).

Rules This accounting method is bounded by rules

and regulations like, GAPS and IFRS

In this accounting manager do

not follow any rules just try to

make decisions as per the

business requirement.

Review

The financial statements use it for inspection,

which will help to promote incorrect financial

statements.

No need to check and modify as

a voluntary set of information.

ii) Importance of management accounting information as a decision making tool.

Managerial team of Imda Tech uses different managerial accounting tools and techniques

for the successful decision making process.

The method helps managers in making decisions effective and worth considering for

control and accounting activities. Monitoring control and access over accounting

techniques provides an essential support in regulation with economic activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It helps managers for making comparison between actual and planned activities to

compute variances, which in turn, suitable decisions can be made for the business

success.

It also gives the presentation to administrative department for evaluating overall

performance of the Imda Tech which helps in generating new rules and regulations in the

company to overcome business risk due to adverse change in external environment.

(Taipaleenmäki and Ikäheimo, 20 133).

It also helps the company in making decisions related to products, like whether to buy or

make product, after examining the cost process.

Accounting manager makes decisions which can be changed as per the market

fluctuations.

It also helps in putting better control over the cost through taking rationalized measures

and drive better return to the entity.

Imda Tech manager also keeps the business updated about advancement in technology.

Draft report and account management that provides operational statistics and financial

information timely and accurate decisions by the board on a daily basis and in the short term.

Unlike accounting, the annual report produces, particularly external stakeholders, representing

weekly or monthly reports to organize internal audiences, such as department heads and chief

executive. These reports generally show how much money is available, sales revenue, the

number of orders beads, account status, debtors, creditors, raw materials and inventory, can also

be trend charts, contrast analysis and other statistics.

Margin Analysis

Internal accounting management of marginal analysis, the profit or cash flows from the sale of

the resulting products, customers, or in some stores. The analysis includes border analysis,

further analysis of benefits through increased production and analysis of broken trends. Tie -

account analysis for the promotion and sales mix only now to determine how much when the

sales volume of the total of the same costs. These accounting data have been calculated useful

for determining the prices of products and services.

compute variances, which in turn, suitable decisions can be made for the business

success.

It also gives the presentation to administrative department for evaluating overall

performance of the Imda Tech which helps in generating new rules and regulations in the

company to overcome business risk due to adverse change in external environment.

(Taipaleenmäki and Ikäheimo, 20 133).

It also helps the company in making decisions related to products, like whether to buy or

make product, after examining the cost process.

Accounting manager makes decisions which can be changed as per the market

fluctuations.

It also helps in putting better control over the cost through taking rationalized measures

and drive better return to the entity.

Imda Tech manager also keeps the business updated about advancement in technology.

Draft report and account management that provides operational statistics and financial

information timely and accurate decisions by the board on a daily basis and in the short term.

Unlike accounting, the annual report produces, particularly external stakeholders, representing

weekly or monthly reports to organize internal audiences, such as department heads and chief

executive. These reports generally show how much money is available, sales revenue, the

number of orders beads, account status, debtors, creditors, raw materials and inventory, can also

be trend charts, contrast analysis and other statistics.

Margin Analysis

Internal accounting management of marginal analysis, the profit or cash flows from the sale of

the resulting products, customers, or in some stores. The analysis includes border analysis,

further analysis of benefits through increased production and analysis of broken trends. Tie -

account analysis for the promotion and sales mix only now to determine how much when the

sales volume of the total of the same costs. These accounting data have been calculated useful

for determining the prices of products and services.

Constraint Analysis

The restrictions on production or sales, management accountants to determine where bottlenecks

occur and calculate the impact on the restrictions on income, profits and cash flows.

Capital Budgeting

t includes the recognition of the use of information management, and making investment

decisions. Management Accountants with the standard budget for capital ratios , as in the present

value and internal rate of return for supporting the resolution , which does not leave the capital -

intensive projects or study includes proposals for products or services required and to find an

appropriate way to finance the purchase made. This also explains the repayment period can be

controlled and cannot predict future economic benefits, and when it happens.

Trend Analysis/Forecasting

Finance and exploring some cost trend line to investigate irregularities or inconsistencies. The

region also makes use of the financial statements for the prior period to calculate and provide

future financial information. These can include historical prices, sales volume, geographical

location, customer trends, or account information.

TASK 2

Product Costing/Valuation

Accounting requires determining the actual cost of a product or service. Accountants calculate

and allocate appropriate costs around the actual cost of product production. It can be applied to

the expenses of the goods produced on the basis of a number of charges or the other driver, such

as box with top accountants use of direct costs to assess the appropriate cost of goods sold and

grains have different stages of the production process

P2 Explain the different types of Management Accounting Systems

i) Cost accounting systems

It is a process of used by companies like Imda Tech to estimate the cost of their product

in order to maintain net profitability, cost and annual turnover. Cost accounting system of the

business evaluate its actual cost, normal cost and standard cost. These cost involves material and

labour which are assigned. These costing method are used to value products and their actual cost

The restrictions on production or sales, management accountants to determine where bottlenecks

occur and calculate the impact on the restrictions on income, profits and cash flows.

Capital Budgeting

t includes the recognition of the use of information management, and making investment

decisions. Management Accountants with the standard budget for capital ratios , as in the present

value and internal rate of return for supporting the resolution , which does not leave the capital -

intensive projects or study includes proposals for products or services required and to find an

appropriate way to finance the purchase made. This also explains the repayment period can be

controlled and cannot predict future economic benefits, and when it happens.

Trend Analysis/Forecasting

Finance and exploring some cost trend line to investigate irregularities or inconsistencies. The

region also makes use of the financial statements for the prior period to calculate and provide

future financial information. These can include historical prices, sales volume, geographical

location, customer trends, or account information.

TASK 2

Product Costing/Valuation

Accounting requires determining the actual cost of a product or service. Accountants calculate

and allocate appropriate costs around the actual cost of product production. It can be applied to

the expenses of the goods produced on the basis of a number of charges or the other driver, such

as box with top accountants use of direct costs to assess the appropriate cost of goods sold and

grains have different stages of the production process

P2 Explain the different types of Management Accounting Systems

i) Cost accounting systems

It is a process of used by companies like Imda Tech to estimate the cost of their product

in order to maintain net profitability, cost and annual turnover. Cost accounting system of the

business evaluate its actual cost, normal cost and standard cost. These cost involves material and

labour which are assigned. These costing method are used to value products and their actual cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of production. Standard cost method is provides the values to manufactured goods and their

estimated material costs.

Estimating the actual cost of goods sold (COGS) is necessary to evaluate companies

profits. Hence, with the help of these methods firm can know products profitability.

ii) Inventory management system

It is a continuous process used by Imda Tech, this helps in maintaining daily incoming

and outgoings of the products and services from the firm. This system consists of receiving

inbound merchandise, transferring outbound merchandise, inquiry, sales, returns. It helps

company in maintaining enough stock for production on daily basis. It helps firm to keep a check

over daily inventory in order to regulate the demands of the customers. Companies also uses

machines to track all orders, vendors, etc.

iii) Job costing systems:

This system is used by Imda Tech manager to identify that its products are different from

each product because identical products and affects the sales and profitability. Measuring job

cost helps in reducing wastage of time and resources. Imda tech uses this to assign

manufacturing cost according to batches of products as per their functioning. This system

involves documentation of Costs of goods sold, finished inventory and work in progress.

iv) Price optimising system

It is an assumption process of the company, system which is used by Imda Tech to evaluate how

the buyers will react to its products and offered prices. The manager involves some important

factors to determine price which are, past prices, inventory cost, and operating cost of the

products. The system gives mathematical analysis of prices which includes the cost which firm is

planning to offer and which will be beneficial.

Lots of business management costs. These costs are separated into different types, such as:

job Costing:

Cost function: - based on the cost function with 8 types, such as: -

Production costs: - part of the costs incurred directly in the manufacturing process for

the production of goods or services are the so - called production costs. Where the cost of

direct materials, direct labor and other direct costs (Mastilak, 2011).

estimated material costs.

Estimating the actual cost of goods sold (COGS) is necessary to evaluate companies

profits. Hence, with the help of these methods firm can know products profitability.

ii) Inventory management system

It is a continuous process used by Imda Tech, this helps in maintaining daily incoming

and outgoings of the products and services from the firm. This system consists of receiving

inbound merchandise, transferring outbound merchandise, inquiry, sales, returns. It helps

company in maintaining enough stock for production on daily basis. It helps firm to keep a check

over daily inventory in order to regulate the demands of the customers. Companies also uses

machines to track all orders, vendors, etc.

iii) Job costing systems:

This system is used by Imda Tech manager to identify that its products are different from

each product because identical products and affects the sales and profitability. Measuring job

cost helps in reducing wastage of time and resources. Imda tech uses this to assign

manufacturing cost according to batches of products as per their functioning. This system

involves documentation of Costs of goods sold, finished inventory and work in progress.

iv) Price optimising system

It is an assumption process of the company, system which is used by Imda Tech to evaluate how

the buyers will react to its products and offered prices. The manager involves some important

factors to determine price which are, past prices, inventory cost, and operating cost of the

products. The system gives mathematical analysis of prices which includes the cost which firm is

planning to offer and which will be beneficial.

Lots of business management costs. These costs are separated into different types, such as:

job Costing:

Cost function: - based on the cost function with 8 types, such as: -

Production costs: - part of the costs incurred directly in the manufacturing process for

the production of goods or services are the so - called production costs. Where the cost of

direct materials, direct labor and other direct costs (Mastilak, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administration costs: part of the cost of the public sector in general is considered

indirect costs and are called administrative costs. As salaries, office expenses and so on.

Selling costs: the costs of making the sale of the sale of goods and services, called the

cost. These commissions, discounts, etc. (Mastilak, 2011).

It is encouraged to share production costs of their products in the market that are

recognized Distribution costs - distribution costs. Since transportation costs, warehouse

rental, etc.

Research and Development cost (Ahmad, et al., 2014), the costs of executives to

develop new products or services or to make an adequate improvement of the product or

service is available and is known as the cost of research development.

Conversion cost: direct costs in the form of salaries, overhead, which was created to

convert raw materials into finished products. There are different stages of production to

intervene for.

Analyse the use of standard costing as decision making tool.

Standard costing: This is the expected replacement cost of the actual costs of their accounts

to record the spread refers to the difference between the difference and the proposed costs of the

actual costs. It contains a collection of useful information that managers use to make effective

decisions (Farkas et al. 2016).

In fact the standard price is used as a decision-making tool, such as using different features as

follows:

Budgeting: - Budget reporting prepared using standard costs, because it can not be used in the

actual cost figures are not final, because the budget is always ready to begin treatment, and

underwent surgery after a period of entry into force of standard cost accounting is used

effectively . The use of standard modules is expected to cost different costs such as costs and

sales. The difference between a standard billing system and a standard cost-standard budget for

each product is an intelligent sharing of the degree that the system offers to accept the existence

of a partition wise. The standard cost used in budget preparation is estimated as the total cost,

because it is used less (VARCAS et al., 20166).

Inventory costing: cost accounting method is used to receive the rest of the unit costs lager

hankerings closed distribution devices. There is a big difference in stock to cover the closure and

indirect costs and are called administrative costs. As salaries, office expenses and so on.

Selling costs: the costs of making the sale of the sale of goods and services, called the

cost. These commissions, discounts, etc. (Mastilak, 2011).

It is encouraged to share production costs of their products in the market that are

recognized Distribution costs - distribution costs. Since transportation costs, warehouse

rental, etc.

Research and Development cost (Ahmad, et al., 2014), the costs of executives to

develop new products or services or to make an adequate improvement of the product or

service is available and is known as the cost of research development.

Conversion cost: direct costs in the form of salaries, overhead, which was created to

convert raw materials into finished products. There are different stages of production to

intervene for.

Analyse the use of standard costing as decision making tool.

Standard costing: This is the expected replacement cost of the actual costs of their accounts

to record the spread refers to the difference between the difference and the proposed costs of the

actual costs. It contains a collection of useful information that managers use to make effective

decisions (Farkas et al. 2016).

In fact the standard price is used as a decision-making tool, such as using different features as

follows:

Budgeting: - Budget reporting prepared using standard costs, because it can not be used in the

actual cost figures are not final, because the budget is always ready to begin treatment, and

underwent surgery after a period of entry into force of standard cost accounting is used

effectively . The use of standard modules is expected to cost different costs such as costs and

sales. The difference between a standard billing system and a standard cost-standard budget for

each product is an intelligent sharing of the degree that the system offers to accept the existence

of a partition wise. The standard cost used in budget preparation is estimated as the total cost,

because it is used less (VARCAS et al., 20166).

Inventory costing: cost accounting method is used to receive the rest of the unit costs lager

hankerings closed distribution devices. There is a big difference in stock to cover the closure and

the actual cost of the traditional normal expected to be effective for each part separately from the

different stages of the production process control of economic (Farkas et al. , 20166).

Controlling: - Administrators can use this tool in the management of their activities and make

adequate improvement in their institutions. They are used to reduce the total cost of increasing

the level of income at the highest level. Using shared spreadsheet software performance and

contrast analysis help you determine the difference between the unit cost and the actual standard

cost per unit (Martin, 20 155).

Performance evaluation:with the standard cost managers can assess the overall performance

they actual performance to take responsibility for basic needs to install evaluation. By

recognizing their achievements, employees are truly motivated to achieve specific goals (Martin,

2015).

Price setting: Use of standard administrative value to determine the price determines the price

accordingly, in order to assess the total cost of survival. They increase the appropriate margins

for their expenses, so they went out at reasonable prices to attract customers to their products

(Martin, 2015).

recognition

TASK-2

P3 Marginal absorption costing

The value of work - work values refers to the way the cost of this method because of cost

calculation. This is mainly used for industrial or corporate purposes that ensure a variety of

contracts and jobs. This is due to a number of rules that will help the technology used in different

situations according to different tasks to these specific customer requirements. Labor costs help

keep accounts straight and indirect. Set of contract method of labor cost.

Precious process - the cost of the additional costs or preparation of the production process steps.

This is the unit cost of the product to ensure that each unit production costs produced by the

standard process division. London CIMA describes the process of value "as a form of influence

on the price, which can be used for the production where standardize goods". These methods can

be used in industries such as chemicals, oil, textile, rubber, sugar, coal, etc.

different stages of the production process control of economic (Farkas et al. , 20166).

Controlling: - Administrators can use this tool in the management of their activities and make

adequate improvement in their institutions. They are used to reduce the total cost of increasing

the level of income at the highest level. Using shared spreadsheet software performance and

contrast analysis help you determine the difference between the unit cost and the actual standard

cost per unit (Martin, 20 155).

Performance evaluation:with the standard cost managers can assess the overall performance

they actual performance to take responsibility for basic needs to install evaluation. By

recognizing their achievements, employees are truly motivated to achieve specific goals (Martin,

2015).

Price setting: Use of standard administrative value to determine the price determines the price

accordingly, in order to assess the total cost of survival. They increase the appropriate margins

for their expenses, so they went out at reasonable prices to attract customers to their products

(Martin, 2015).

recognition

TASK-2

P3 Marginal absorption costing

The value of work - work values refers to the way the cost of this method because of cost

calculation. This is mainly used for industrial or corporate purposes that ensure a variety of

contracts and jobs. This is due to a number of rules that will help the technology used in different

situations according to different tasks to these specific customer requirements. Labor costs help

keep accounts straight and indirect. Set of contract method of labor cost.

Precious process - the cost of the additional costs or preparation of the production process steps.

This is the unit cost of the product to ensure that each unit production costs produced by the

standard process division. London CIMA describes the process of value "as a form of influence

on the price, which can be used for the production where standardize goods". These methods can

be used in industries such as chemicals, oil, textile, rubber, sugar, coal, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

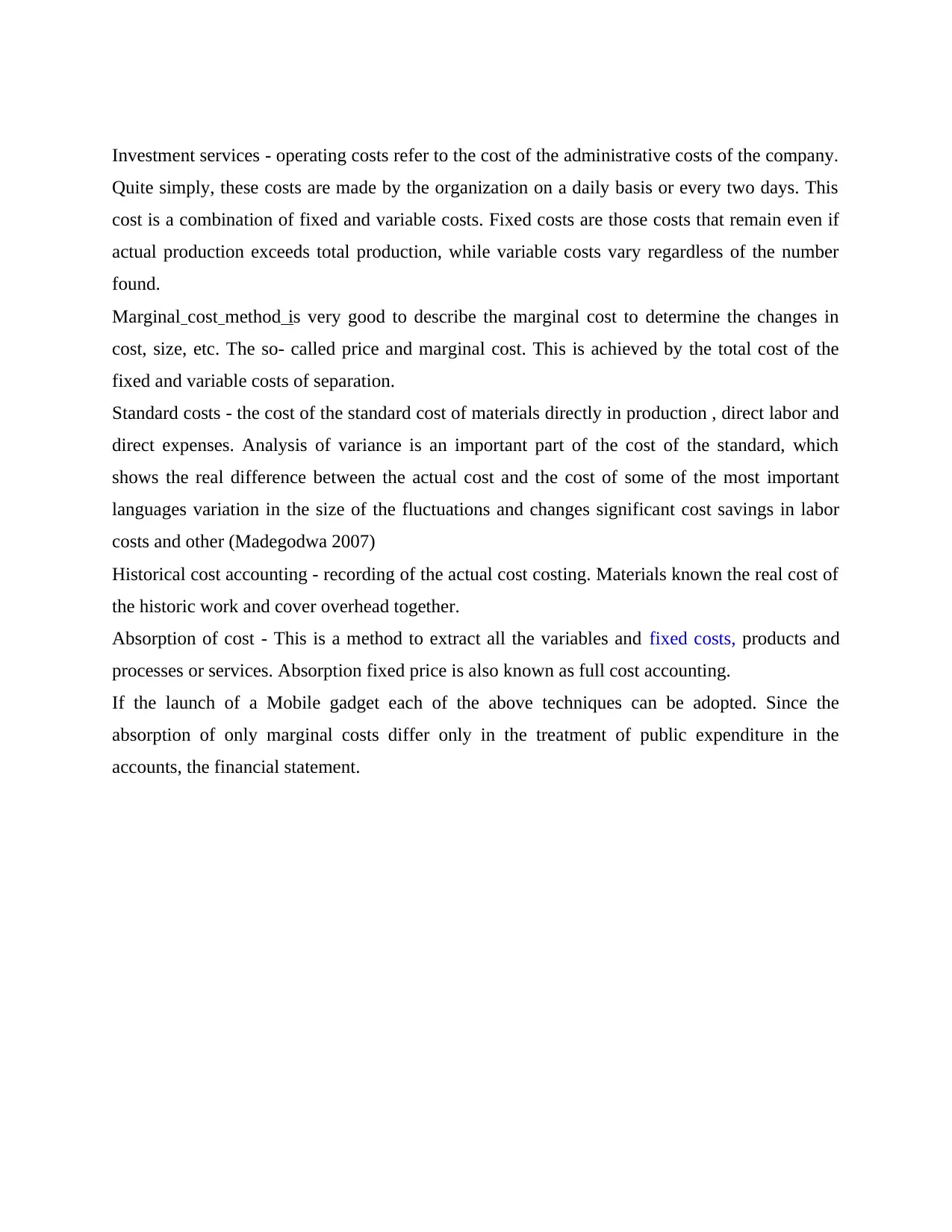

Investment services - operating costs refer to the cost of the administrative costs of the company.

Quite simply, these costs are made by the organization on a daily basis or every two days. This

cost is a combination of fixed and variable costs. Fixed costs are those costs that remain even if

actual production exceeds total production, while variable costs vary regardless of the number

found.

Marginal cost method is very good to describe the marginal cost to determine the changes in

cost, size, etc. The so- called price and marginal cost. This is achieved by the total cost of the

fixed and variable costs of separation.

Standard costs - the cost of the standard cost of materials directly in production , direct labor and

direct expenses. Analysis of variance is an important part of the cost of the standard, which

shows the real difference between the actual cost and the cost of some of the most important

languages variation in the size of the fluctuations and changes significant cost savings in labor

costs and other (Madegodwa 2007)

Historical cost accounting - recording of the actual cost costing. Materials known the real cost of

the historic work and cover overhead together.

Absorption of cost - This is a method to extract all the variables and fixed costs, products and

processes or services. Absorption fixed price is also known as full cost accounting.

If the launch of a Mobile gadget each of the above techniques can be adopted. Since the

absorption of only marginal costs differ only in the treatment of public expenditure in the

accounts, the financial statement.

Quite simply, these costs are made by the organization on a daily basis or every two days. This

cost is a combination of fixed and variable costs. Fixed costs are those costs that remain even if

actual production exceeds total production, while variable costs vary regardless of the number

found.

Marginal cost method is very good to describe the marginal cost to determine the changes in

cost, size, etc. The so- called price and marginal cost. This is achieved by the total cost of the

fixed and variable costs of separation.

Standard costs - the cost of the standard cost of materials directly in production , direct labor and

direct expenses. Analysis of variance is an important part of the cost of the standard, which

shows the real difference between the actual cost and the cost of some of the most important

languages variation in the size of the fluctuations and changes significant cost savings in labor

costs and other (Madegodwa 2007)

Historical cost accounting - recording of the actual cost costing. Materials known the real cost of

the historic work and cover overhead together.

Absorption of cost - This is a method to extract all the variables and fixed costs, products and

processes or services. Absorption fixed price is also known as full cost accounting.

If the launch of a Mobile gadget each of the above techniques can be adopted. Since the

absorption of only marginal costs differ only in the treatment of public expenditure in the

accounts, the financial statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

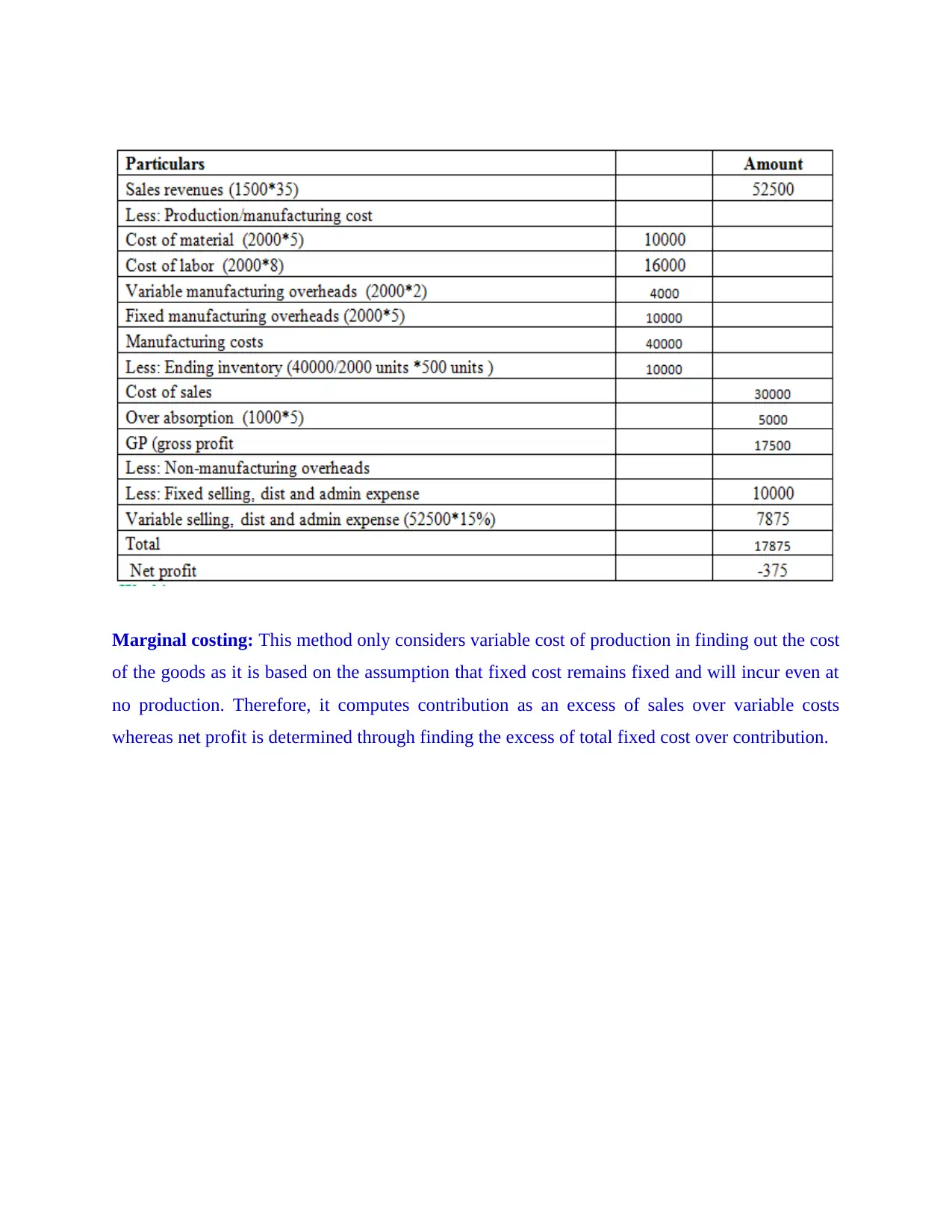

Marginal costing: This method only considers variable cost of production in finding out the cost

of the goods as it is based on the assumption that fixed cost remains fixed and will incur even at

no production. Therefore, it computes contribution as an excess of sales over variable costs

whereas net profit is determined through finding the excess of total fixed cost over contribution.

of the goods as it is based on the assumption that fixed cost remains fixed and will incur even at

no production. Therefore, it computes contribution as an excess of sales over variable costs

whereas net profit is determined through finding the excess of total fixed cost over contribution.

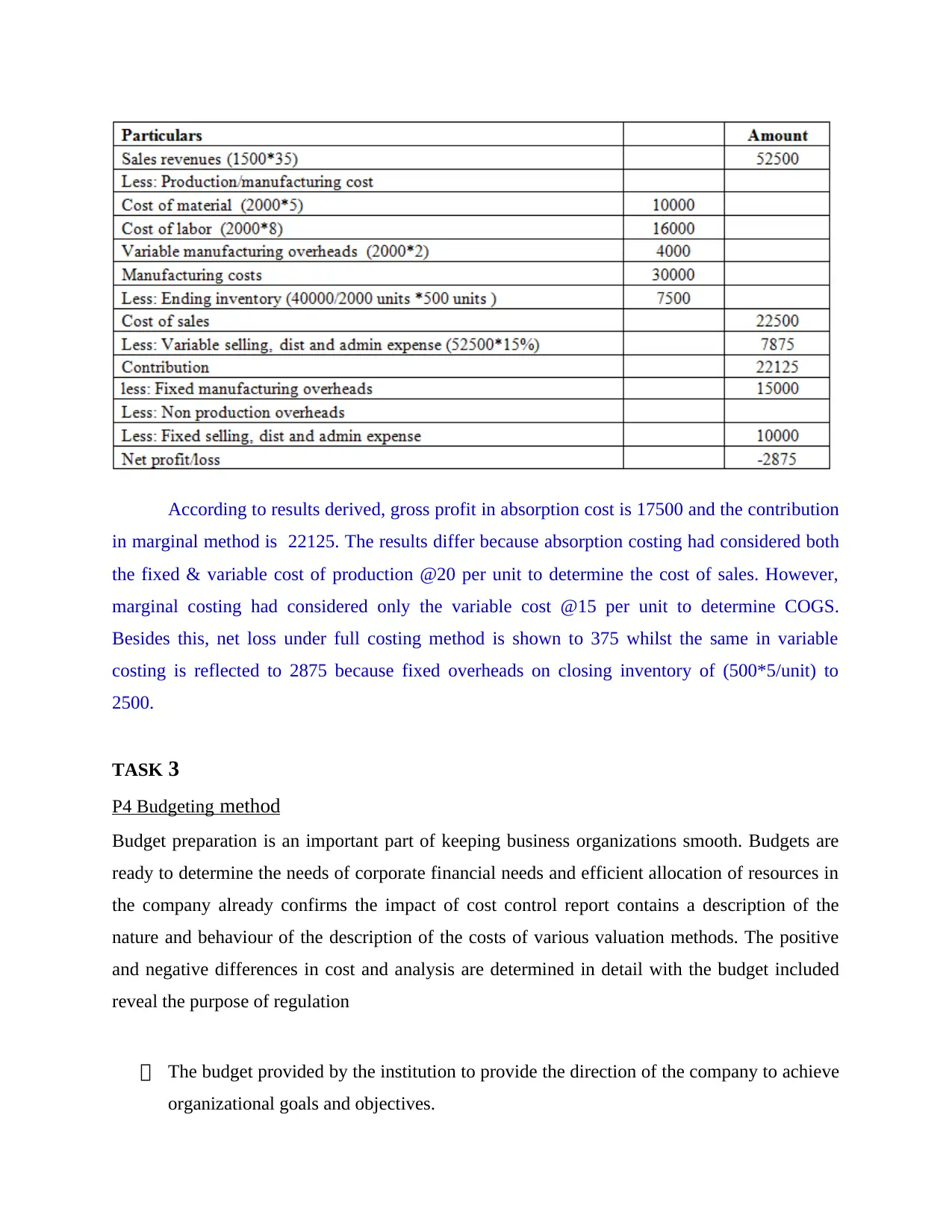

According to results derived, gross profit in absorption cost is 17500 and the contribution

in marginal method is 22125. The results differ because absorption costing had considered both

the fixed & variable cost of production @20 per unit to determine the cost of sales. However,

marginal costing had considered only the variable cost @15 per unit to determine COGS.

Besides this, net loss under full costing method is shown to 375 whilst the same in variable

costing is reflected to 2875 because fixed overheads on closing inventory of (500*5/unit) to

2500.

TASK 3

P4 Budgeting method

Budget preparation is an important part of keeping business organizations smooth. Budgets are

ready to determine the needs of corporate financial needs and efficient allocation of resources in

the company already confirms the impact of cost control report contains a description of the

nature and behaviour of the description of the costs of various valuation methods. The positive

and negative differences in cost and analysis are determined in detail with the budget included

reveal the purpose of regulation

The budget provided by the institution to provide the direction of the company to achieve

organizational goals and objectives.

in marginal method is 22125. The results differ because absorption costing had considered both

the fixed & variable cost of production @20 per unit to determine the cost of sales. However,

marginal costing had considered only the variable cost @15 per unit to determine COGS.

Besides this, net loss under full costing method is shown to 375 whilst the same in variable

costing is reflected to 2875 because fixed overheads on closing inventory of (500*5/unit) to

2500.

TASK 3

P4 Budgeting method

Budget preparation is an important part of keeping business organizations smooth. Budgets are

ready to determine the needs of corporate financial needs and efficient allocation of resources in

the company already confirms the impact of cost control report contains a description of the

nature and behaviour of the description of the costs of various valuation methods. The positive

and negative differences in cost and analysis are determined in detail with the budget included

reveal the purpose of regulation

The budget provided by the institution to provide the direction of the company to achieve

organizational goals and objectives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.