Management Accounting Report: Analysis for Imda Tech (UK)

VerifiedAdded on 2020/06/06

|17

|5712

|26

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of Imda Tech. It begins by highlighting the importance of management accounting, detailing its various functions such as planning, organizing, decision-making, and controlling, and differentiating it from financial accounting. The report then delves into different types of management accounting systems, including traditional, lean, and throughput accounting, and their specific applications. The core of the report explores costing methods, contrasting marginal and absorption costing, and explaining their implications through the income statement. Budgeting is another key area, with an examination of various budget types and the budget preparation process, along with pricing strategies. Finally, the report concludes by discussing the use of the balance scorecard approach in addressing financial problems and improving financial governance within an organization. The report offers insights into the practical application of accounting methods to enhance business operations and decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Importance of management accounting and its various functions....................................1

B2. Various kinds of management accounting systems and their use in Imda Tech.............3

TASK 2............................................................................................................................................5

A & B. Income statement and explanation of marginal and absorption costing....................5

TASK 3............................................................................................................................................8

A. Various types of budget and process of budget preparation..............................................8

B. Budget preparation process..............................................................................................10

C. Pricing Strategies.............................................................................................................11

TASK 4..........................................................................................................................................11

A. Use of balance scorecard approach in solving financial problems..................................11

Use of balance card approach in improving financial governance.......................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Importance of management accounting and its various functions....................................1

B2. Various kinds of management accounting systems and their use in Imda Tech.............3

TASK 2............................................................................................................................................5

A & B. Income statement and explanation of marginal and absorption costing....................5

TASK 3............................................................................................................................................8

A. Various types of budget and process of budget preparation..............................................8

B. Budget preparation process..............................................................................................10

C. Pricing Strategies.............................................................................................................11

TASK 4..........................................................................................................................................11

A. Use of balance scorecard approach in solving financial problems..................................11

Use of balance card approach in improving financial governance.......................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

With time, complexity in conducting a business is increasing. Companies want to expand

their area of operation so they can attain more profit and achieve their short and long term goals.

Globalisation made a huge impact on most of the organisations that are working in different

industries. Enterprises face various kinds of financial problems in the business environment.

Management accounting system helps a firm in resolving critical issues like correct field of

investment, proper sources of borrowings, etc. Some people think that it only assists the finance

department but this is a myth because other wings of a company also take their support. They ask

them for significant data which can be related to availability of cash or strategy of competitors.

Imda Tech (UK) is an enterprise that makes and sells extraordinary kind of mobile chargers and

different types of other gadgets for retail shop (HammadJusoh and Ghozali, 2013). This

assignment will focus on difference between management and financial accounting. It will also

discuss important method of costing like marginal and absorption. Types of budget and its

various merit and demerit will also become part of this report. Use of modern method of

accounting for solving financial problems will be explained at the end of this file.

TASK 1

A. Importance of management accounting and its various functions

Management accounting is a process which help an organisation in conducting their

business in an efficient manner. The process of decision making is getting complicated every day

because of involvement of various factors like government policies, change in taxations system

etc. Most of the companies are trying to find a way by which they can reduce their cost of

business operation as it is essential for getting some extra edge over their competitors.

Management accounting play crucial role in minimising wastage and enhancing sale of an

organisation. Its modern tool provide great assistance to the managers, it assist them in making

fast and accurate decision which is important for long term growth of a company (Agbejule,

2011). Below are some major function of management accounting:

Planning and forecasting – A firm cannot attaining their goals if they do not have an

effective plan. Decisions taken by manager decide whether a company will move forward or they

are going to face huge loss in upcoming time. Systems of management accounting play crucial

role in forecasting various activities like growth rate of enterprise and other competitors etc.

1

With time, complexity in conducting a business is increasing. Companies want to expand

their area of operation so they can attain more profit and achieve their short and long term goals.

Globalisation made a huge impact on most of the organisations that are working in different

industries. Enterprises face various kinds of financial problems in the business environment.

Management accounting system helps a firm in resolving critical issues like correct field of

investment, proper sources of borrowings, etc. Some people think that it only assists the finance

department but this is a myth because other wings of a company also take their support. They ask

them for significant data which can be related to availability of cash or strategy of competitors.

Imda Tech (UK) is an enterprise that makes and sells extraordinary kind of mobile chargers and

different types of other gadgets for retail shop (HammadJusoh and Ghozali, 2013). This

assignment will focus on difference between management and financial accounting. It will also

discuss important method of costing like marginal and absorption. Types of budget and its

various merit and demerit will also become part of this report. Use of modern method of

accounting for solving financial problems will be explained at the end of this file.

TASK 1

A. Importance of management accounting and its various functions

Management accounting is a process which help an organisation in conducting their

business in an efficient manner. The process of decision making is getting complicated every day

because of involvement of various factors like government policies, change in taxations system

etc. Most of the companies are trying to find a way by which they can reduce their cost of

business operation as it is essential for getting some extra edge over their competitors.

Management accounting play crucial role in minimising wastage and enhancing sale of an

organisation. Its modern tool provide great assistance to the managers, it assist them in making

fast and accurate decision which is important for long term growth of a company (Agbejule,

2011). Below are some major function of management accounting:

Planning and forecasting – A firm cannot attaining their goals if they do not have an

effective plan. Decisions taken by manager decide whether a company will move forward or they

are going to face huge loss in upcoming time. Systems of management accounting play crucial

role in forecasting various activities like growth rate of enterprise and other competitors etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

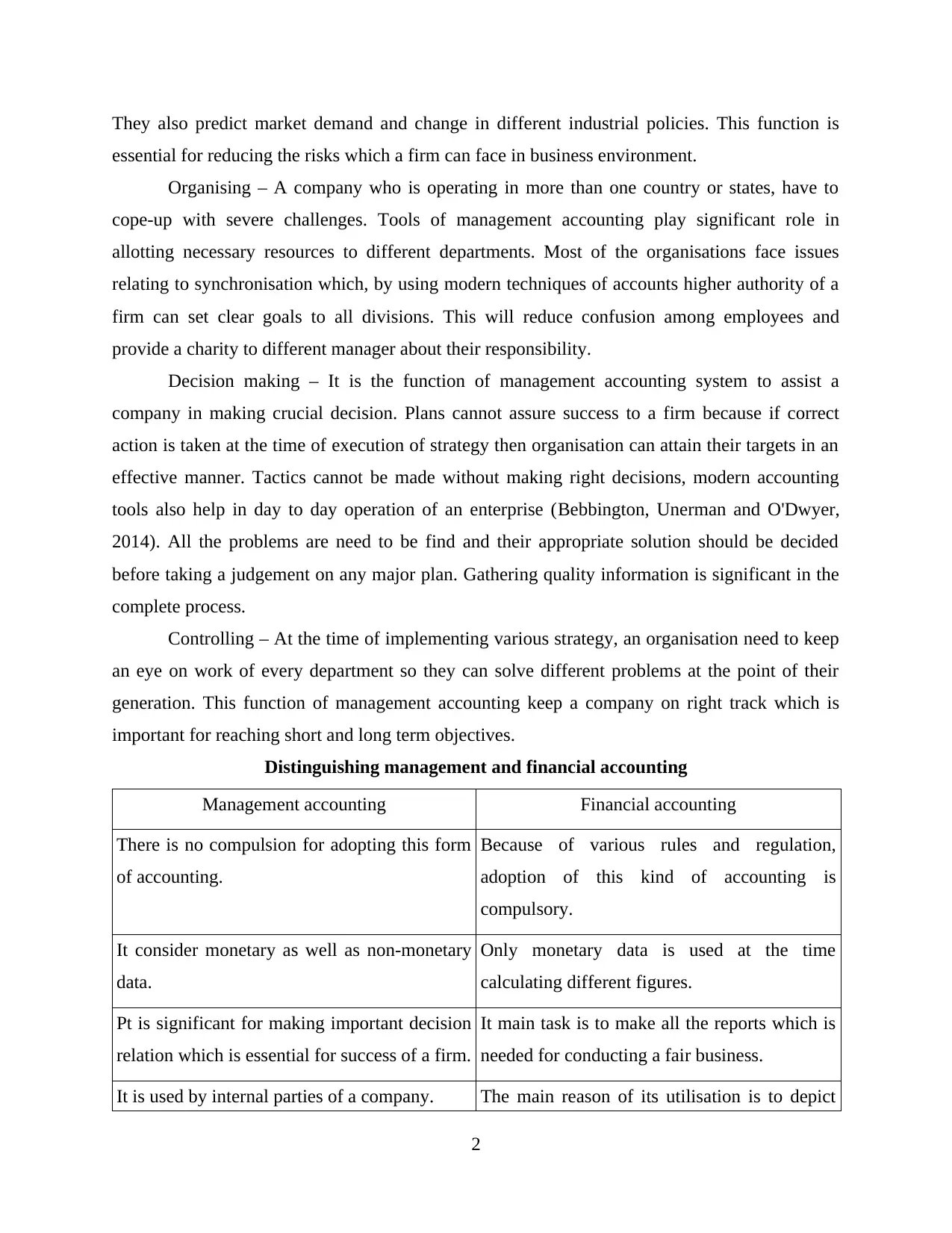

They also predict market demand and change in different industrial policies. This function is

essential for reducing the risks which a firm can face in business environment.

Organising – A company who is operating in more than one country or states, have to

cope-up with severe challenges. Tools of management accounting play significant role in

allotting necessary resources to different departments. Most of the organisations face issues

relating to synchronisation which, by using modern techniques of accounts higher authority of a

firm can set clear goals to all divisions. This will reduce confusion among employees and

provide a charity to different manager about their responsibility.

Decision making – It is the function of management accounting system to assist a

company in making crucial decision. Plans cannot assure success to a firm because if correct

action is taken at the time of execution of strategy then organisation can attain their targets in an

effective manner. Tactics cannot be made without making right decisions, modern accounting

tools also help in day to day operation of an enterprise (Bebbington, Unerman and O'Dwyer,

2014). All the problems are need to be find and their appropriate solution should be decided

before taking a judgement on any major plan. Gathering quality information is significant in the

complete process.

Controlling – At the time of implementing various strategy, an organisation need to keep

an eye on work of every department so they can solve different problems at the point of their

generation. This function of management accounting keep a company on right track which is

important for reaching short and long term objectives.

Distinguishing management and financial accounting

Management accounting Financial accounting

There is no compulsion for adopting this form

of accounting.

Because of various rules and regulation,

adoption of this kind of accounting is

compulsory.

It consider monetary as well as non-monetary

data.

Only monetary data is used at the time

calculating different figures.

Pt is significant for making important decision

relation which is essential for success of a firm.

It main task is to make all the reports which is

needed for conducting a fair business.

It is used by internal parties of a company. The main reason of its utilisation is to depict

2

essential for reducing the risks which a firm can face in business environment.

Organising – A company who is operating in more than one country or states, have to

cope-up with severe challenges. Tools of management accounting play significant role in

allotting necessary resources to different departments. Most of the organisations face issues

relating to synchronisation which, by using modern techniques of accounts higher authority of a

firm can set clear goals to all divisions. This will reduce confusion among employees and

provide a charity to different manager about their responsibility.

Decision making – It is the function of management accounting system to assist a

company in making crucial decision. Plans cannot assure success to a firm because if correct

action is taken at the time of execution of strategy then organisation can attain their targets in an

effective manner. Tactics cannot be made without making right decisions, modern accounting

tools also help in day to day operation of an enterprise (Bebbington, Unerman and O'Dwyer,

2014). All the problems are need to be find and their appropriate solution should be decided

before taking a judgement on any major plan. Gathering quality information is significant in the

complete process.

Controlling – At the time of implementing various strategy, an organisation need to keep

an eye on work of every department so they can solve different problems at the point of their

generation. This function of management accounting keep a company on right track which is

important for reaching short and long term objectives.

Distinguishing management and financial accounting

Management accounting Financial accounting

There is no compulsion for adopting this form

of accounting.

Because of various rules and regulation,

adoption of this kind of accounting is

compulsory.

It consider monetary as well as non-monetary

data.

Only monetary data is used at the time

calculating different figures.

Pt is significant for making important decision

relation which is essential for success of a firm.

It main task is to make all the reports which is

needed for conducting a fair business.

It is used by internal parties of a company. The main reason of its utilisation is to depict

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

present position of the enterprise to the

external parties.

Significance of management accounting in the process of decision making by managers of

different departments

Every firm face a situation where they get distracted by goals and success of other

players who are operating in same industry. Management accounting stop a company in moving

towards wrong direction by reminding them their strategies and set targets. It an enterprise get

assistance in forecasting then managers of various departments can make appropriate plans. It

can improve efficiency of workers which will result in better product and service (QianBurritt

and Monroe, 2011). Management accounting solve significant issues relating to investment and

proper source of borrowings, it provide correct direction to a division as well as to whole

organisation. Financial accounting only help finance department but this managerial accounts

help all the wings of an enterprise by giving necessary data and information.

Back up plans are sometime considered as the backbone of a firm, tool of management

accounting pour confidence in employees because at the time of execution of different thoughts,

they know that managers do not have to make any major call because they already made have a

program for coping up with these kind of issues. If various department of an organisation use

management accounting information then they can make quick and accurate decision. This is

essential for getting some extra edge over other players of the company.

B2. Various kinds of management accounting systems and their use in Imda Tech

Management accounting has mainly has three types, first is traditional, second is lean and

third is throughput. By utilising tools of these methods, Imda Tech can attain their objectives in

an effective manner:

Traditional accounting – It is an old approach which mainly focus on allocating direct as

well as indirect cost to the each unit of a product. It various tools assist in predicting profits but

its significant in present era is diminishing. It do not concentrate on various important

department of a firm which can be considered as the main reason of its reducing popularity. Job

order and process costing are its key methods, earlier one try to ascertain cost of each job while

later one focuses on the determining the expenses by analysing production process.

3

external parties.

Significance of management accounting in the process of decision making by managers of

different departments

Every firm face a situation where they get distracted by goals and success of other

players who are operating in same industry. Management accounting stop a company in moving

towards wrong direction by reminding them their strategies and set targets. It an enterprise get

assistance in forecasting then managers of various departments can make appropriate plans. It

can improve efficiency of workers which will result in better product and service (QianBurritt

and Monroe, 2011). Management accounting solve significant issues relating to investment and

proper source of borrowings, it provide correct direction to a division as well as to whole

organisation. Financial accounting only help finance department but this managerial accounts

help all the wings of an enterprise by giving necessary data and information.

Back up plans are sometime considered as the backbone of a firm, tool of management

accounting pour confidence in employees because at the time of execution of different thoughts,

they know that managers do not have to make any major call because they already made have a

program for coping up with these kind of issues. If various department of an organisation use

management accounting information then they can make quick and accurate decision. This is

essential for getting some extra edge over other players of the company.

B2. Various kinds of management accounting systems and their use in Imda Tech

Management accounting has mainly has three types, first is traditional, second is lean and

third is throughput. By utilising tools of these methods, Imda Tech can attain their objectives in

an effective manner:

Traditional accounting – It is an old approach which mainly focus on allocating direct as

well as indirect cost to the each unit of a product. It various tools assist in predicting profits but

its significant in present era is diminishing. It do not concentrate on various important

department of a firm which can be considered as the main reason of its reducing popularity. Job

order and process costing are its key methods, earlier one try to ascertain cost of each job while

later one focuses on the determining the expenses by analysing production process.

3

Lean accounting – Its main area of focus is on reducing wastage in production process

which will ultimately make a positive impact on the profit earned by a firm (Weißenberger and

Angelkort, 2011). This method is significant in delivering various information in short period of

which is essential for making correct and fast decisions by managers of different department.

This form of accounting reveal the areas where company need to make necessary changes, it can

be related to monitoring or measuring.

Throughput accounting – Most of the modern methods focus on minimising cost but this

system concentrate of enhancing sale by increasing production capacity. It a company

manufacture more goods then they can meet demand of customers in less time, it play significant

role in increasing the wealth of an enterprise. Its benefits are not limited to only manufacturing

unit, other wings of an organisation like marketing, finance also get assistance from this type of

management accounting (Zoni, Dossi and Morelli, 2012).

Below are some other systems which can be adopted by various department in order to

improve their reports:

Cost accounting system – It mainly concentrate on reducing production cost by using

different tools. Cited company can increase their profit by either minimising operation

expenses of business or enhance total sale of the firm. This system focuses on three type

of cost, first is actual costing. It can be ascertained by calculating the real expenses that

has incurred on production process. Expenditure on labour, material and other overheads

are significant part of this method. In normal costing, actual cost of material and labour is

taken but overheads are applied at a standard rate. Standard costing works on expected

expenditure, instead of reporting actual expenditure incurred on manufacturing process,

companies like to use standards rates (Tsamenyi, Sahadev and Qiao, 2011).

Inventory management system – Managing stock in an effective manner can provide

extra edge to cited organisation on their competitors. Tool of this kind of accounting play

significant role in maintaining proper balance between demand and supply of goods. If

this system in used in Imda Tech by storage department then they can reduce their

carrying and ordering cost which will assist company in increasing their total revenue.

There are various software relating to inventory management that can tell exact amount

of stock that enterprise should keep in their storage units. It help in solving two crucial

problems, first is overstocking which raise carrying cost and other is fulfil demand of

4

which will ultimately make a positive impact on the profit earned by a firm (Weißenberger and

Angelkort, 2011). This method is significant in delivering various information in short period of

which is essential for making correct and fast decisions by managers of different department.

This form of accounting reveal the areas where company need to make necessary changes, it can

be related to monitoring or measuring.

Throughput accounting – Most of the modern methods focus on minimising cost but this

system concentrate of enhancing sale by increasing production capacity. It a company

manufacture more goods then they can meet demand of customers in less time, it play significant

role in increasing the wealth of an enterprise. Its benefits are not limited to only manufacturing

unit, other wings of an organisation like marketing, finance also get assistance from this type of

management accounting (Zoni, Dossi and Morelli, 2012).

Below are some other systems which can be adopted by various department in order to

improve their reports:

Cost accounting system – It mainly concentrate on reducing production cost by using

different tools. Cited company can increase their profit by either minimising operation

expenses of business or enhance total sale of the firm. This system focuses on three type

of cost, first is actual costing. It can be ascertained by calculating the real expenses that

has incurred on production process. Expenditure on labour, material and other overheads

are significant part of this method. In normal costing, actual cost of material and labour is

taken but overheads are applied at a standard rate. Standard costing works on expected

expenditure, instead of reporting actual expenditure incurred on manufacturing process,

companies like to use standards rates (Tsamenyi, Sahadev and Qiao, 2011).

Inventory management system – Managing stock in an effective manner can provide

extra edge to cited organisation on their competitors. Tool of this kind of accounting play

significant role in maintaining proper balance between demand and supply of goods. If

this system in used in Imda Tech by storage department then they can reduce their

carrying and ordering cost which will assist company in increasing their total revenue.

There are various software relating to inventory management that can tell exact amount

of stock that enterprise should keep in their storage units. It help in solving two crucial

problems, first is overstocking which raise carrying cost and other is fulfil demand of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

customers on right time. Sometime permanent buyer of a product switch to other brand

because they do not get their commodities in needed period.

Job costing – This method focuses on each job that is performed in the production

process. The basic idea behind this concept is to shut the jobs which do not have

considerable amount of contribution in earning money (Uluyol and Akçi, 2014).

Profitability is ascertained according to each task that is performed at the time of

manufacturing a single unit. A job which is generating more revenue can be given more

support in order to increase the total profit of the company. Normally costing system

concentrate of processes but this form of costing deals with jobs performed by every

worker.

Price optimisation system – Most of the enterprise face problems relating to deciding

price of a product which is acceptable by significant number of consumers (Ezzamel and

et.al., 2003). If marketing and production department of cited company use this system

then they can decide a value is not more, in the view of customers, and not less,

according to the management of organisation.

If Imda Tech adopt use these accounting system then they can minimise wastage of

resources and increase total sale by an impressive rate (Ward, 2012). They should select correct

approach according to their size and long term targets.

TASK 2

A & B. Income statement and explanation of marginal and absorption costing

An organisation can adopt any method of costing according to their suitable. Marginal

and absorption has their own advantages, below is explanation of both terms:

Marginal costing – It is the extra cost which is incurred in the production of an additional

unit. It is basically a technique which assist in the process of decision making, two type of cost in

considered in this process first is fixed and second is variable. Closing stock is considered at the

time of using this method which is the prime reason for getting less profit if the volume of sale is

low. Whether volume of production go up or down, fixed cost remain same in this approach.

Marginal costing help manager in selecting correct choices, it only deals with various cost which

is a right method because involving fixed expenditure in decision making process will show

wrong results (Naidu and Chand, 2013).

5

because they do not get their commodities in needed period.

Job costing – This method focuses on each job that is performed in the production

process. The basic idea behind this concept is to shut the jobs which do not have

considerable amount of contribution in earning money (Uluyol and Akçi, 2014).

Profitability is ascertained according to each task that is performed at the time of

manufacturing a single unit. A job which is generating more revenue can be given more

support in order to increase the total profit of the company. Normally costing system

concentrate of processes but this form of costing deals with jobs performed by every

worker.

Price optimisation system – Most of the enterprise face problems relating to deciding

price of a product which is acceptable by significant number of consumers (Ezzamel and

et.al., 2003). If marketing and production department of cited company use this system

then they can decide a value is not more, in the view of customers, and not less,

according to the management of organisation.

If Imda Tech adopt use these accounting system then they can minimise wastage of

resources and increase total sale by an impressive rate (Ward, 2012). They should select correct

approach according to their size and long term targets.

TASK 2

A & B. Income statement and explanation of marginal and absorption costing

An organisation can adopt any method of costing according to their suitable. Marginal

and absorption has their own advantages, below is explanation of both terms:

Marginal costing – It is the extra cost which is incurred in the production of an additional

unit. It is basically a technique which assist in the process of decision making, two type of cost in

considered in this process first is fixed and second is variable. Closing stock is considered at the

time of using this method which is the prime reason for getting less profit if the volume of sale is

low. Whether volume of production go up or down, fixed cost remain same in this approach.

Marginal costing help manager in selecting correct choices, it only deals with various cost which

is a right method because involving fixed expenditure in decision making process will show

wrong results (Naidu and Chand, 2013).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

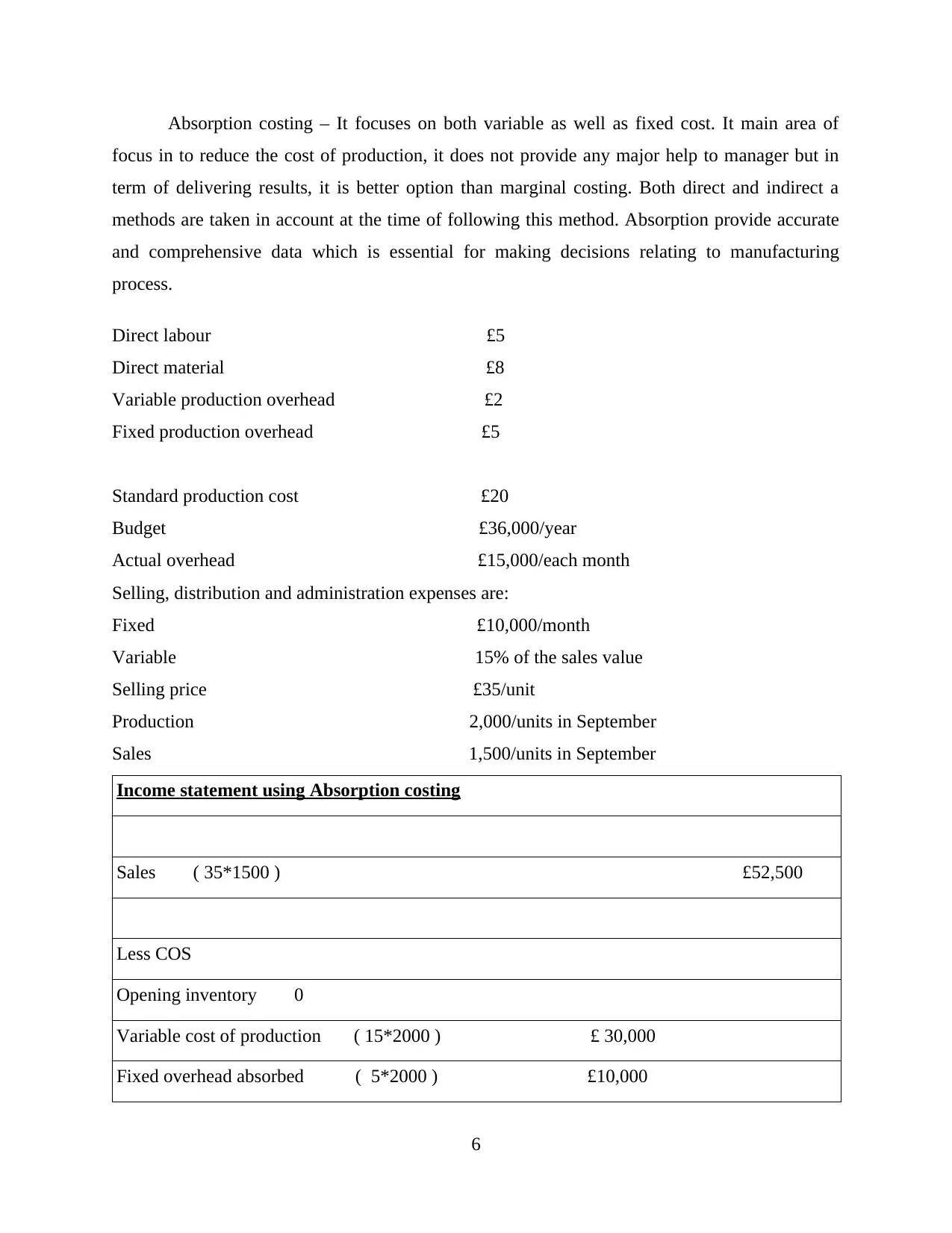

Absorption costing – It focuses on both variable as well as fixed cost. It main area of

focus in to reduce the cost of production, it does not provide any major help to manager but in

term of delivering results, it is better option than marginal costing. Both direct and indirect a

methods are taken in account at the time of following this method. Absorption provide accurate

and comprehensive data which is essential for making decisions relating to manufacturing

process.

Direct labour £5

Direct material £8

Variable production overhead £2

Fixed production overhead £5

Standard production cost £20

Budget £36,000/year

Actual overhead £15,000/each month

Selling, distribution and administration expenses are:

Fixed £10,000/month

Variable 15% of the sales value

Selling price £35/unit

Production 2,000/units in September

Sales 1,500/units in September

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

6

focus in to reduce the cost of production, it does not provide any major help to manager but in

term of delivering results, it is better option than marginal costing. Both direct and indirect a

methods are taken in account at the time of following this method. Absorption provide accurate

and comprehensive data which is essential for making decisions relating to manufacturing

process.

Direct labour £5

Direct material £8

Variable production overhead £2

Fixed production overhead £5

Standard production cost £20

Budget £36,000/year

Actual overhead £15,000/each month

Selling, distribution and administration expenses are:

Fixed £10,000/month

Variable 15% of the sales value

Selling price £35/unit

Production 2,000/units in September

Sales 1,500/units in September

Income statement using Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

6

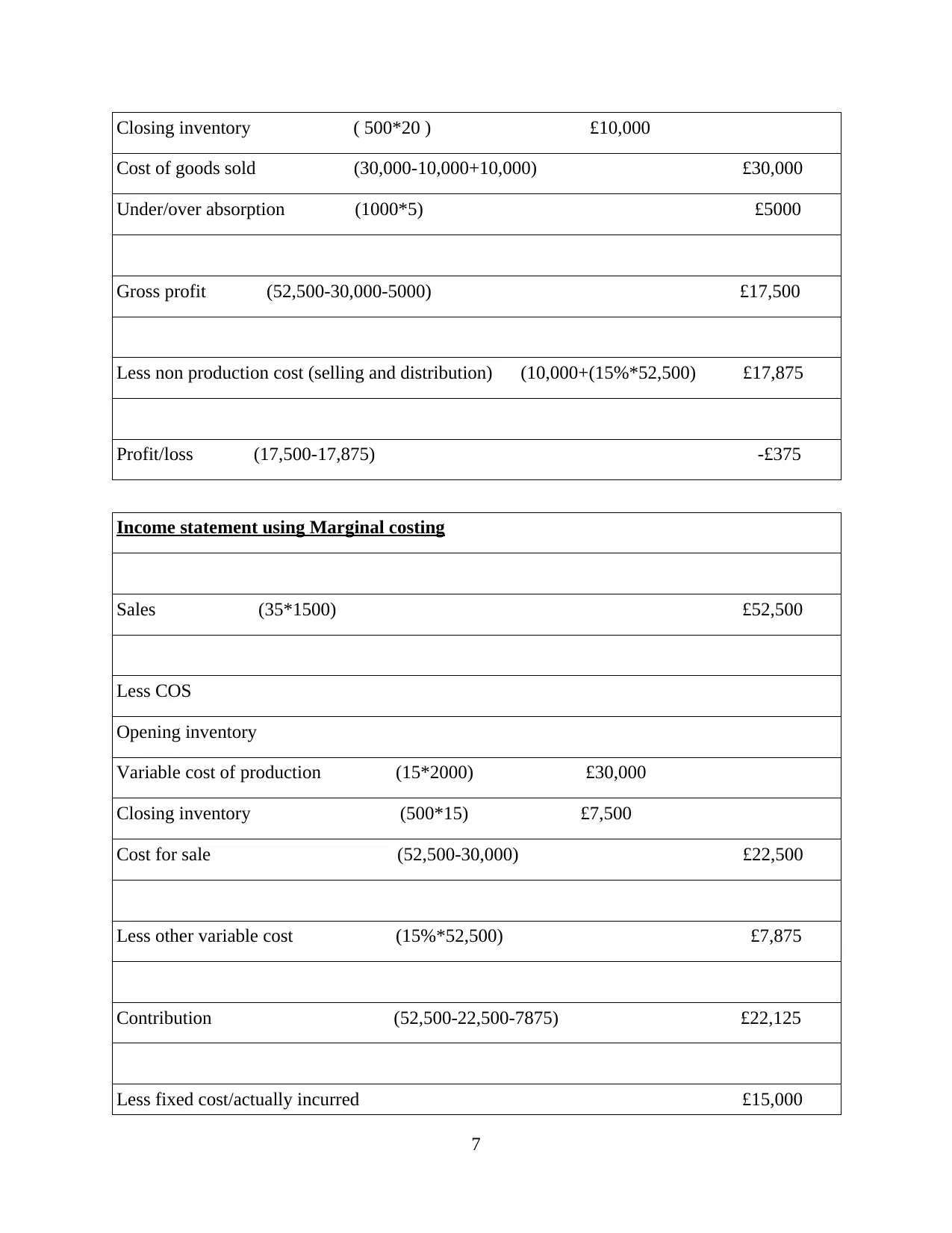

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

7

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Income statement using Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less non production cost (selling, distribution and administration) £10,000

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

By analysing above income statement it can be concluded that absorption costing would

be appropriate method for cited company because they will face a loss of £375 which is less than

the figure determined by marginal approach. This difference in amount occur due to different

treatment of closing stock. Fixed cost is considered in both methods but in marginal costing, it is

subtracted in one shot which put a heavy burden on profit. The variation between both

approaches could be less it this figure is treated in same way (Ngoc Phi Anh Nguyen and Mia,

2011). In absorption costing, fixed cost is allotted with the production of each unit which reduces

the overall burden on net profit. Marginal approach focuses on variable expenses in starting but

in the end, fixed expenditure is included which is the main reason behind the major difference.

£2,875 is the loss which is ascertained by using this method. At the time of reporting, absorption

costing would be perfect option but marginal is considered as a more realistic concept as there is

no point of including fixed cost in each unit that is produced by the production department.

8

Profit/loss (22,125-15,000-10,000) -£2,875

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

By analysing above income statement it can be concluded that absorption costing would

be appropriate method for cited company because they will face a loss of £375 which is less than

the figure determined by marginal approach. This difference in amount occur due to different

treatment of closing stock. Fixed cost is considered in both methods but in marginal costing, it is

subtracted in one shot which put a heavy burden on profit. The variation between both

approaches could be less it this figure is treated in same way (Ngoc Phi Anh Nguyen and Mia,

2011). In absorption costing, fixed cost is allotted with the production of each unit which reduces

the overall burden on net profit. Marginal approach focuses on variable expenses in starting but

in the end, fixed expenditure is included which is the main reason behind the major difference.

£2,875 is the loss which is ascertained by using this method. At the time of reporting, absorption

costing would be perfect option but marginal is considered as a more realistic concept as there is

no point of including fixed cost in each unit that is produced by the production department.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing basically focus on additional expenses, but absorption deals with all the

expenses that has happened in production process.

TASK 3

A. Various types of budget and process of budget preparation

Budget is basically a record of planned expenditure and expect income. It provide a

pathway to various department of an organisation which save them for facing different kind of

confusions. It also reduce conflict between two divisions that can derail all the major business

operation of cited organisation. An effective plan give confidence to the managers because they

have basic idea activity next step which they have to follow for completing a task (Otley and

Emmanuel, 2013). Some people raise question on accuracy of budget but in reality every

organisation has to do some planning as it is essential for moving on a same path. Following are

some popular kind of budgets:

Master budget – Normally plans are made for one of two department of an enterprise

but this type of budget is made for all the divisions of a company. It include all the operational

area which has direct or indirect role in attaining set objectives. Every wing of the firm get their

targets and essential funds.

Advantages – One of the most important merit of this budget it that it synchronise all the

task that would be performed in the organisation (Kotas, 2014). This will help cited company in

advancing on correct path. It also reduce the number of conflicts which can happen between two

divisions of an enterprise. Sometime plans made by various department work against each other,

this create major confusion in the firm and it has many negative impact on the image of

company. By making a master budget, cited organisation can remove these kind of major

problems. Most of the managers get distracted by strategy of their competitors, they forget their

actual plan which can assure them success in long run (Hoque, 2012). This type of planning will

help them in focusing on their own goals and reduce different type of noises which they hear

from outer world.

Disadvantages – Master budget cannot be made by small firms because it is one of the

most expensive planning which is currently present in business environment. Most of the

manager raise question regarding its accuracy (Macintosh. and Quattrone, 2010). One this budget

is made by company, they cannot do any major changes in set program because if one part get

9

expenses that has happened in production process.

TASK 3

A. Various types of budget and process of budget preparation

Budget is basically a record of planned expenditure and expect income. It provide a

pathway to various department of an organisation which save them for facing different kind of

confusions. It also reduce conflict between two divisions that can derail all the major business

operation of cited organisation. An effective plan give confidence to the managers because they

have basic idea activity next step which they have to follow for completing a task (Otley and

Emmanuel, 2013). Some people raise question on accuracy of budget but in reality every

organisation has to do some planning as it is essential for moving on a same path. Following are

some popular kind of budgets:

Master budget – Normally plans are made for one of two department of an enterprise

but this type of budget is made for all the divisions of a company. It include all the operational

area which has direct or indirect role in attaining set objectives. Every wing of the firm get their

targets and essential funds.

Advantages – One of the most important merit of this budget it that it synchronise all the

task that would be performed in the organisation (Kotas, 2014). This will help cited company in

advancing on correct path. It also reduce the number of conflicts which can happen between two

divisions of an enterprise. Sometime plans made by various department work against each other,

this create major confusion in the firm and it has many negative impact on the image of

company. By making a master budget, cited organisation can remove these kind of major

problems. Most of the managers get distracted by strategy of their competitors, they forget their

actual plan which can assure them success in long run (Hoque, 2012). This type of planning will

help them in focusing on their own goals and reduce different type of noises which they hear

from outer world.

Disadvantages – Master budget cannot be made by small firms because it is one of the

most expensive planning which is currently present in business environment. Most of the

manager raise question regarding its accuracy (Macintosh. and Quattrone, 2010). One this budget

is made by company, they cannot do any major changes in set program because if one part get

9

affected then other will also face its heat. Process of this kind of planning is very lengthy,

managers do not like spend hours of efforts on formation of plans as their main focus is on

execution of various tactics. Companies do not like to make this budget because they believe in

making short term plans because they can easily execute them.

Cash budget – Liquid asset are considered as backbone of an organisation. This budget

is prepared for determining the amount of cash that should be kept in business. Estimation is

done relating to expected cash inflow and outflow. Collection of revenue, payment of expenses

are some of the major areas which are focused at the time of forming this budget.

Advantages – It help in ascertaining the right amount of cash that should be kept by

accountant. It support time payment to different creditors and suppliers who are significant part

of stakeholders (Horngren. and et.al., 2005). Firm can make a record of various debtors who are

not paying their dues on right time. This will reduce the amount of bad debts by figuring out

defaulters.

Disadvantages – There is a big question make on its accuracy, managers often argue that

company can never determine the exact amount of cash that they should keep in their

organisation. It is do not have direct relation to profit so its formation is considered as wastage of

time by many accountants.

Operating budget – This type of planning is done for manufacturing and administrative

work. All the income from operational activities is estimated along with the expenditure that

company is going to do in upcoming time.

Advantages – This budget play crucial role in minimising the wastage of resources. If

manager know the actual amount which they can spend then they use it in an effective manner

(Baldvinsdottir, Mitchell and Nørreklit, 2010). It play crucial role in expansion of business

because planning for new area of operation can reduce various risks that an organisation can face

at the time of entering new market.

Disadvantages – Formation of this budget put an extra pressure on financial position of a

firm. This type of planning is done for short time period, changes can be done in these plans on

continuous basis. It create confusion among manager because they fail to decide correct program

which they have to follow. This type of budget focuses on a single year, long term plans ar3e

generally ignored at the of its formation.

10

managers do not like spend hours of efforts on formation of plans as their main focus is on

execution of various tactics. Companies do not like to make this budget because they believe in

making short term plans because they can easily execute them.

Cash budget – Liquid asset are considered as backbone of an organisation. This budget

is prepared for determining the amount of cash that should be kept in business. Estimation is

done relating to expected cash inflow and outflow. Collection of revenue, payment of expenses

are some of the major areas which are focused at the time of forming this budget.

Advantages – It help in ascertaining the right amount of cash that should be kept by

accountant. It support time payment to different creditors and suppliers who are significant part

of stakeholders (Horngren. and et.al., 2005). Firm can make a record of various debtors who are

not paying their dues on right time. This will reduce the amount of bad debts by figuring out

defaulters.

Disadvantages – There is a big question make on its accuracy, managers often argue that

company can never determine the exact amount of cash that they should keep in their

organisation. It is do not have direct relation to profit so its formation is considered as wastage of

time by many accountants.

Operating budget – This type of planning is done for manufacturing and administrative

work. All the income from operational activities is estimated along with the expenditure that

company is going to do in upcoming time.

Advantages – This budget play crucial role in minimising the wastage of resources. If

manager know the actual amount which they can spend then they use it in an effective manner

(Baldvinsdottir, Mitchell and Nørreklit, 2010). It play crucial role in expansion of business

because planning for new area of operation can reduce various risks that an organisation can face

at the time of entering new market.

Disadvantages – Formation of this budget put an extra pressure on financial position of a

firm. This type of planning is done for short time period, changes can be done in these plans on

continuous basis. It create confusion among manager because they fail to decide correct program

which they have to follow. This type of budget focuses on a single year, long term plans ar3e

generally ignored at the of its formation.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.