Comprehensive Management Accounting Report for Tech (UK) Limited

VerifiedAdded on 2020/07/22

|15

|4675

|37

Report

AI Summary

This management accounting report analyzes the financial strategies of Tech (UK) Ltd. It defines management accounting, its essential requirements, and different managerial accounting reports. The report includes income statements prepared using marginal and absorption costing methods. It also explains the advantages and disadvantages of planning tools for budgetary control and evaluates the Balance Scorecard and other financial approaches. The analysis covers cost accounting systems, inventory management, and various reporting methods like budget reporting, account receivables, and job cost reports, providing a comprehensive overview of financial management within the company.

MANAGEMENT

ACCOUNTING REPORT

FOR

TECH (UK) LIMITED

ACCOUNTING REPORT

FOR

TECH (UK) LIMITED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explanation of management accounting and the essential requirements of management

accounting system.......................................................................................................................1

P.2. Different types of managerial accounting reports................................................................3

TASK 2............................................................................................................................................5

P.3. Income statements of Tech (UK) Ltd organisation using marginal and absorption costing

methods.......................................................................................................................................5

TASK 3............................................................................................................................................7

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control........................................................................................................................7

TASK 4..........................................................................................................................................10

P.5. Evaluation of Balance scorecard and some other financial approaches in terms of proper

address of financial issues in the organisation..........................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explanation of management accounting and the essential requirements of management

accounting system.......................................................................................................................1

P.2. Different types of managerial accounting reports................................................................3

TASK 2............................................................................................................................................5

P.3. Income statements of Tech (UK) Ltd organisation using marginal and absorption costing

methods.......................................................................................................................................5

TASK 3............................................................................................................................................7

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control........................................................................................................................7

TASK 4..........................................................................................................................................10

P.5. Evaluation of Balance scorecard and some other financial approaches in terms of proper

address of financial issues in the organisation..........................................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

In this documentation, it defines about several kinds of management accounting tools and

techniques by which organisational manager of Tech (UK) Ltd company can identify some

factors through which all monetary and non-monetary factor of the organisation is assessed

sufficiently. Moreover, this study also describes about cost accounting system and inventory

management system in the company. This assessment also refers to preparation of income

statements of Tech (UK) Ltd organisation by utilising marginal and absorption costing

approaches within the firm effectively. Apart from it, this investigation also refers to some

management accounting tools and mechanisms by which the firm could resolve their financial

issues in an effective form.

TASK 1

P.1. Explanation of management accounting and the essential requirements of management

accounting system

Management accounting: This is a managerial accounting system in which the manager

of the business needs to make a report which defines about internal management system

effectively. This is a methodology of formation of a report at internal basis which defines about

the internal financial and statistical data required for the manager in order to make appropriate

decision concerning to business goals and objectives (Bennett and James, eds., 2017).

Management accounting is used for making monetary and non-monetary information within the

organisation effectively. Management accounting used to for find out financial rations of the firm

by which performance leverages could be figure out and financial standard performance could be

set up by company's manager.

Financial accounting: This refers to the process by which the business accounting

officer makes recording, summarising and reporting of proper financial transaction within a

given period, in which they need to make development in some areas by which effective decision

can be made by accounting officer of Tech (UK) Ltd. within the industry effectively. This is used

for monetary information within the business effectively (Otley and Emmanuel, 2013). Financial

accounting depends on debit and credit system. In case of debit, it increases of assets and

expenses and the decrease the liabilities and incomes. In the business cash is asset and capital is

liability of the business.

1

In this documentation, it defines about several kinds of management accounting tools and

techniques by which organisational manager of Tech (UK) Ltd company can identify some

factors through which all monetary and non-monetary factor of the organisation is assessed

sufficiently. Moreover, this study also describes about cost accounting system and inventory

management system in the company. This assessment also refers to preparation of income

statements of Tech (UK) Ltd organisation by utilising marginal and absorption costing

approaches within the firm effectively. Apart from it, this investigation also refers to some

management accounting tools and mechanisms by which the firm could resolve their financial

issues in an effective form.

TASK 1

P.1. Explanation of management accounting and the essential requirements of management

accounting system

Management accounting: This is a managerial accounting system in which the manager

of the business needs to make a report which defines about internal management system

effectively. This is a methodology of formation of a report at internal basis which defines about

the internal financial and statistical data required for the manager in order to make appropriate

decision concerning to business goals and objectives (Bennett and James, eds., 2017).

Management accounting is used for making monetary and non-monetary information within the

organisation effectively. Management accounting used to for find out financial rations of the firm

by which performance leverages could be figure out and financial standard performance could be

set up by company's manager.

Financial accounting: This refers to the process by which the business accounting

officer makes recording, summarising and reporting of proper financial transaction within a

given period, in which they need to make development in some areas by which effective decision

can be made by accounting officer of Tech (UK) Ltd. within the industry effectively. This is used

for monetary information within the business effectively (Otley and Emmanuel, 2013). Financial

accounting depends on debit and credit system. In case of debit, it increases of assets and

expenses and the decrease the liabilities and incomes. In the business cash is asset and capital is

liability of the business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance of management accounting as decision-making tools for departmental

manager

Management accounting is the most vital part for each organisation which assists the

management departmental managers in terms of making proper report within the business for

making internal analysis of the business functions and effectively managing them as well. In case

of Tech (UK) Ltd organisational manager, they have also needed to make use of sufficient tools

of management accounting at the workplace for identification of financial issues in the

organisation and making essential decision regarding increment in profitability and productivity

of the business in the industry in more relevant form (McLellan and Moustafa, 2011). With the

assistance of tools of management accounting in the enterprise, the department manager could

make relevant analysis of costing within the business and effectively reduce them as well.

Cost accounting systems:

Cost accounting is a process which has a major goal to capture the organisation's costing

of each production level and assessing them at each level in internal production level which is

capital equipment and depreciation as well. Cost accounting has first step to recording the

costing at individual level and then comparisons of input result figure to output actual report

result in respect to measuring financial performance of the business entity in given period time

within the organisational environment effectively. Cost accounting system helps the manager to

giving prices for each job which is being done in manufacturing plants of the firm. Thus,. It

could be said that, it assists the business manager to making pricing decision for each job in the

manufacturing plant.

Different types of cost accounting systems:

Absorption costing system approach defines that all fixed and variable costs are allotted

to cost unit and overhead in case of computing absorption costing system. Under the marginal

costing system, costa are separated into fixed and variable costs. Variable costs are charged to

unit cost of the company.

Job costing system: This is a costing system in the organisation which defines about the

costing of each manufacturing job which is being done in the business entity effectively. It is one

of major appropriate approach which can assist the manager of the company in order to make

engagement in terms of production of specific products and services within the organisation in an

effective form. In case of Tech (UK) Ltd organisation, the organisational manager requires

2

manager

Management accounting is the most vital part for each organisation which assists the

management departmental managers in terms of making proper report within the business for

making internal analysis of the business functions and effectively managing them as well. In case

of Tech (UK) Ltd organisational manager, they have also needed to make use of sufficient tools

of management accounting at the workplace for identification of financial issues in the

organisation and making essential decision regarding increment in profitability and productivity

of the business in the industry in more relevant form (McLellan and Moustafa, 2011). With the

assistance of tools of management accounting in the enterprise, the department manager could

make relevant analysis of costing within the business and effectively reduce them as well.

Cost accounting systems:

Cost accounting is a process which has a major goal to capture the organisation's costing

of each production level and assessing them at each level in internal production level which is

capital equipment and depreciation as well. Cost accounting has first step to recording the

costing at individual level and then comparisons of input result figure to output actual report

result in respect to measuring financial performance of the business entity in given period time

within the organisational environment effectively. Cost accounting system helps the manager to

giving prices for each job which is being done in manufacturing plants of the firm. Thus,. It

could be said that, it assists the business manager to making pricing decision for each job in the

manufacturing plant.

Different types of cost accounting systems:

Absorption costing system approach defines that all fixed and variable costs are allotted

to cost unit and overhead in case of computing absorption costing system. Under the marginal

costing system, costa are separated into fixed and variable costs. Variable costs are charged to

unit cost of the company.

Job costing system: This is a costing system in the organisation which defines about the

costing of each manufacturing job which is being done in the business entity effectively. It is one

of major appropriate approach which can assist the manager of the company in order to make

engagement in terms of production of specific products and services within the organisation in an

effective form. In case of Tech (UK) Ltd organisation, the organisational manager requires

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

utilisation of job costing system approach at the workplace in order to identify each job costing

of the production level which is being done in the organisational environment in an efficient

form.

Inventory management systems: This is an important system which must be used by

each organisation at the workplace with respect to manage their all works and inventory in

manufacturing plant in an effective form (Nørreklit, 2014). This is an effective process in which

company's parts and inventory is being transported by the company's other locations and manage

inventory at daily basis in the organisation as per the customer re requirements in the business

effectively. The company need to make use of some of effective tools and software of inventory

management at the workplace in context of appropriate management of operational level, raw

material and surplus within the plant in an efficient form. Inventory management approach assist

the business to which products they should buy or not for the company in order to gain sufficient

profit. It also helps Tech (UK) Ltd company's manager in context of making new product

decision for the company which they want to launch in market.

P.2. Different types of managerial accounting reports

Varied of managerial accounting reports presented here by which the managerial

department of the company can formulate effective reports at the workplace effective manner

and identify the key elements of the organisation within the industry in more relevant form

(Hyvönen, 2010). Management accounting reports assist the business manager in order to proper

management of organisation's execution and equipped regularly throughout the accounting

period of the company in relevant form. Moreover, the department manager could utilise of these

accounting system in the organisation in relevant manner as per the needs of reports in business

and this could be prepared by the organisational manager at quarterly, monthly, even daily basis

as well.

Budget reporting: This is also effective approach for preparation of reporting in Tech

(UK) Ltd organisation in effective manner. The manager of the company needs to make use of

some areas by which effective development can be gained in relevant form in sufficient manner.

Budget reporting is also an essential part for the organisation in terms of effectively measuring

the performances of the business in more relevant form and in case of Tech (UK) Ltd

corporation, the business manager requires preparing these kinds of reporting at the workpeople

3

of the production level which is being done in the organisational environment in an efficient

form.

Inventory management systems: This is an important system which must be used by

each organisation at the workplace with respect to manage their all works and inventory in

manufacturing plant in an effective form (Nørreklit, 2014). This is an effective process in which

company's parts and inventory is being transported by the company's other locations and manage

inventory at daily basis in the organisation as per the customer re requirements in the business

effectively. The company need to make use of some of effective tools and software of inventory

management at the workplace in context of appropriate management of operational level, raw

material and surplus within the plant in an efficient form. Inventory management approach assist

the business to which products they should buy or not for the company in order to gain sufficient

profit. It also helps Tech (UK) Ltd company's manager in context of making new product

decision for the company which they want to launch in market.

P.2. Different types of managerial accounting reports

Varied of managerial accounting reports presented here by which the managerial

department of the company can formulate effective reports at the workplace effective manner

and identify the key elements of the organisation within the industry in more relevant form

(Hyvönen, 2010). Management accounting reports assist the business manager in order to proper

management of organisation's execution and equipped regularly throughout the accounting

period of the company in relevant form. Moreover, the department manager could utilise of these

accounting system in the organisation in relevant manner as per the needs of reports in business

and this could be prepared by the organisational manager at quarterly, monthly, even daily basis

as well.

Budget reporting: This is also effective approach for preparation of reporting in Tech

(UK) Ltd organisation in effective manner. The manager of the company needs to make use of

some areas by which effective development can be gained in relevant form in sufficient manner.

Budget reporting is also an essential part for the organisation in terms of effectively measuring

the performances of the business in more relevant form and in case of Tech (UK) Ltd

corporation, the business manager requires preparing these kinds of reporting at the workpeople

3

in order to recognise the performance of the business and effectively control them in the business

environment efficiently (Maheshwari, 2014). Moreover, the estimation of budget reporting is

totally based on the total expenses occurred in the company in previous year in an efficient form.

In case of big organisation, the specific department has been established in the company in order

to prepare budget reporting in the company for cost reduction in the business in relevant form.

This is also used by corporation's manager in respect to provision of appropriate incentives to

employees and workers of the organisation in the industry effectively.

Account receivable: This is also the most appropriate method of reporting at the

workplace for Tech (UK) Ltd organisation effectively by which business manager can effectively

manage cash flows of the organisation and enhance the creditability for their consumers in

relevant form. This report also assist the enterprise manager in terms of breaking down the

customers balances by how long they have been owned in the organisation effectively. This type

of reporting has specific columns in the reporting system in which they need entering invoices

for 30 days, 90 days etc. this report also could assist the business manager in respect to identify

the issues in the organisation's collections methods efficiently. In this way, if some customers are

not paying their required balance in company, then the organisational manager require making

relevant policies in the company in order to paying sufficient credit payments to the company

effectively. This is also helps the business manager on overlooking on overdraft of the company

in the industry in relevant form.

Job cost reports: This type of reporting is specially used for the organisation for separate

projection, which review the expenses for the business in relevant form (Gullkvist, 2013). The

organisational manager generally matched with the approximation of revenue system for the

company so that company can effectively evaluate the work's profitability within the industry in

more relevant form. This is also made major focus on the top earning sections of the business in

the industry so that the manager of the company can make major focus on profit margin on each

job in the company instead of wasting their quality of time on low profit margin functions in the

company efficiently. This is also helpful for the organisation in respect to assessment of

expenses in the specific projection in the company so that each one of them can reduce the

costing of projection by utilising job costing reports tools and mechanisms efficiently.

4

environment efficiently (Maheshwari, 2014). Moreover, the estimation of budget reporting is

totally based on the total expenses occurred in the company in previous year in an efficient form.

In case of big organisation, the specific department has been established in the company in order

to prepare budget reporting in the company for cost reduction in the business in relevant form.

This is also used by corporation's manager in respect to provision of appropriate incentives to

employees and workers of the organisation in the industry effectively.

Account receivable: This is also the most appropriate method of reporting at the

workplace for Tech (UK) Ltd organisation effectively by which business manager can effectively

manage cash flows of the organisation and enhance the creditability for their consumers in

relevant form. This report also assist the enterprise manager in terms of breaking down the

customers balances by how long they have been owned in the organisation effectively. This type

of reporting has specific columns in the reporting system in which they need entering invoices

for 30 days, 90 days etc. this report also could assist the business manager in respect to identify

the issues in the organisation's collections methods efficiently. In this way, if some customers are

not paying their required balance in company, then the organisational manager require making

relevant policies in the company in order to paying sufficient credit payments to the company

effectively. This is also helps the business manager on overlooking on overdraft of the company

in the industry in relevant form.

Job cost reports: This type of reporting is specially used for the organisation for separate

projection, which review the expenses for the business in relevant form (Gullkvist, 2013). The

organisational manager generally matched with the approximation of revenue system for the

company so that company can effectively evaluate the work's profitability within the industry in

more relevant form. This is also made major focus on the top earning sections of the business in

the industry so that the manager of the company can make major focus on profit margin on each

job in the company instead of wasting their quality of time on low profit margin functions in the

company efficiently. This is also helpful for the organisation in respect to assessment of

expenses in the specific projection in the company so that each one of them can reduce the

costing of projection by utilising job costing reports tools and mechanisms efficiently.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

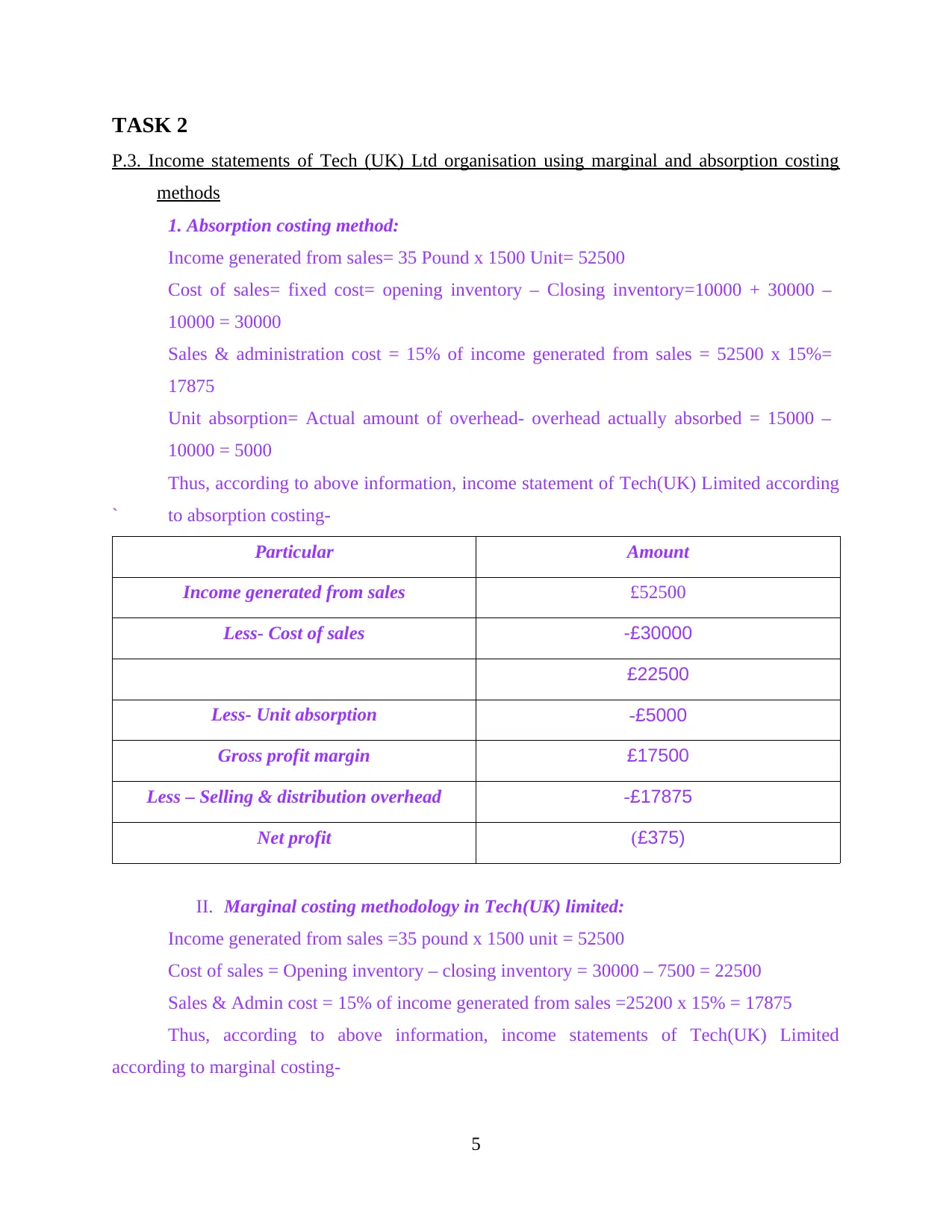

TASK 2

P.3. Income statements of Tech (UK) Ltd organisation using marginal and absorption costing

methods

1. Absorption costing method:

Income generated from sales= 35 Pound x 1500 Unit= 52500

Cost of sales= fixed cost= opening inventory – Closing inventory=10000 + 30000 –

10000 = 30000

Sales & administration cost = 15% of income generated from sales = 52500 x 15%=

17875

Unit absorption= Actual amount of overhead- overhead actually absorbed = 15000 –

10000 = 5000

Thus, according to above information, income statement of Tech(UK) Limited according

` to absorption costing-

Particular Amount

Income generated from sales £52500

Less- Cost of sales -£30000

£22500

Less- Unit absorption -£5000

Gross profit margin £17500

Less – Selling & distribution overhead -£17875

Net profit (£375)

II. Marginal costing methodology in Tech(UK) limited:

Income generated from sales =35 pound x 1500 unit = 52500

Cost of sales = Opening inventory – closing inventory = 30000 – 7500 = 22500

Sales & Admin cost = 15% of income generated from sales =25200 x 15% = 17875

Thus, according to above information, income statements of Tech(UK) Limited

according to marginal costing-

5

P.3. Income statements of Tech (UK) Ltd organisation using marginal and absorption costing

methods

1. Absorption costing method:

Income generated from sales= 35 Pound x 1500 Unit= 52500

Cost of sales= fixed cost= opening inventory – Closing inventory=10000 + 30000 –

10000 = 30000

Sales & administration cost = 15% of income generated from sales = 52500 x 15%=

17875

Unit absorption= Actual amount of overhead- overhead actually absorbed = 15000 –

10000 = 5000

Thus, according to above information, income statement of Tech(UK) Limited according

` to absorption costing-

Particular Amount

Income generated from sales £52500

Less- Cost of sales -£30000

£22500

Less- Unit absorption -£5000

Gross profit margin £17500

Less – Selling & distribution overhead -£17875

Net profit (£375)

II. Marginal costing methodology in Tech(UK) limited:

Income generated from sales =35 pound x 1500 unit = 52500

Cost of sales = Opening inventory – closing inventory = 30000 – 7500 = 22500

Sales & Admin cost = 15% of income generated from sales =25200 x 15% = 17875

Thus, according to above information, income statements of Tech(UK) Limited

according to marginal costing-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

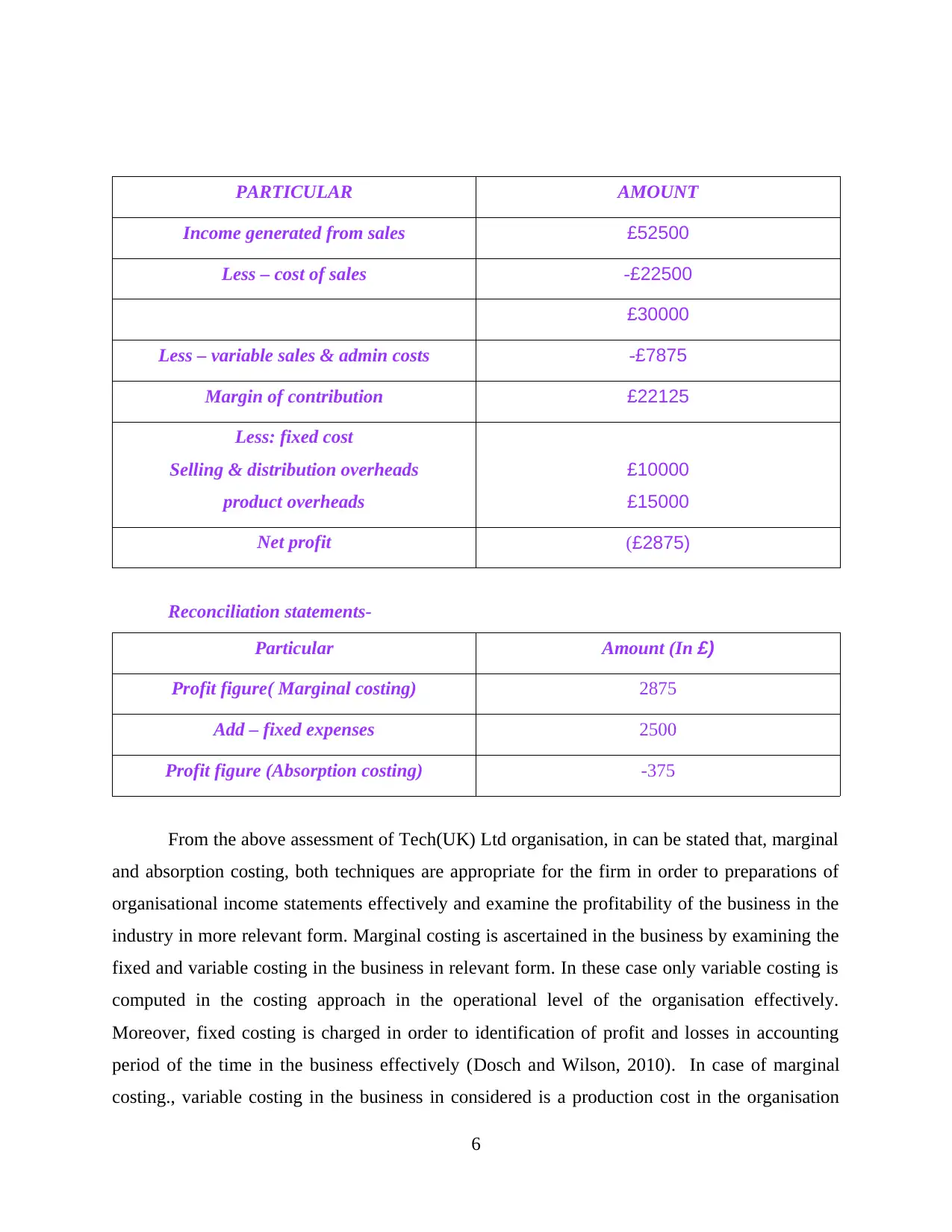

PARTICULAR AMOUNT

Income generated from sales £52500

Less – cost of sales -£22500

£30000

Less – variable sales & admin costs -£7875

Margin of contribution £22125

Less: fixed cost

Selling & distribution overheads

product overheads

£10000

£15000

Net profit (£2875)

Reconciliation statements-

Particular Amount (In £)

Profit figure( Marginal costing) 2875

Add – fixed expenses 2500

Profit figure (Absorption costing) -375

From the above assessment of Tech(UK) Ltd organisation, in can be stated that, marginal

and absorption costing, both techniques are appropriate for the firm in order to preparations of

organisational income statements effectively and examine the profitability of the business in the

industry in more relevant form. Marginal costing is ascertained in the business by examining the

fixed and variable costing in the business in relevant form. In these case only variable costing is

computed in the costing approach in the operational level of the organisation effectively.

Moreover, fixed costing is charged in order to identification of profit and losses in accounting

period of the time in the business effectively (Dosch and Wilson, 2010). In case of marginal

costing., variable costing in the business in considered is a production cost in the organisation

6

Income generated from sales £52500

Less – cost of sales -£22500

£30000

Less – variable sales & admin costs -£7875

Margin of contribution £22125

Less: fixed cost

Selling & distribution overheads

product overheads

£10000

£15000

Net profit (£2875)

Reconciliation statements-

Particular Amount (In £)

Profit figure( Marginal costing) 2875

Add – fixed expenses 2500

Profit figure (Absorption costing) -375

From the above assessment of Tech(UK) Ltd organisation, in can be stated that, marginal

and absorption costing, both techniques are appropriate for the firm in order to preparations of

organisational income statements effectively and examine the profitability of the business in the

industry in more relevant form. Marginal costing is ascertained in the business by examining the

fixed and variable costing in the business in relevant form. In these case only variable costing is

computed in the costing approach in the operational level of the organisation effectively.

Moreover, fixed costing is charged in order to identification of profit and losses in accounting

period of the time in the business effectively (Dosch and Wilson, 2010). In case of marginal

costing., variable costing in the business in considered is a production cost in the organisation

6

and the fixed costing is considered is a period costing in the company in more relevant form.

This can be used by the organisational manager in terms of generation of more profitability in the

industry effectively and in case of absorption costing approach, cost identification of fixed and

variable costing is considered as the product cost of Tech(UK) Ltd. Apart from it, there are some

classification of overhead costing in the business in relevant form in which, in case of marginal

costing the fixed and marginal costing is classified as overhead costing in the company and in

case of absorption costing approach, there some of classification of costing is inclusion which is

production cost, administration costing and selling and distribution costs in the company in more

relevant form.

In case of marginal costing approach, the profitability of the company is measured by the

profit volume ratio in the company in relevant form and in absorption costing, due to the

involvement of fixed costing in the company, organisational profitability gets affected

efficiently. In Tech (UK) Ltd enterprise, there is some of direct material and direct labour fixed

production overhead costing is associated in the company in appropriate form for preparation of

costing in the business (Kokubu and Kitada, 2015). In case of marginal costing approach of the

company, its profitable figure showing value which is, 2875 and moreover, in case of absorption

costing techniques, its net profit is showing the value which is -375 which is more than marginal

costing in the company, because of addition of selling and administration fixed overhead

expenses within the organisation in effective manner. Hence, it could be said that the

organisational manager requires utilisation of absorption costing techniques at the workplace in

more sufficient manner in order to ascertain many things in the business environment in proper

sort. Moreover, it is also concluded that organisation manager can use both techniques in respect

to preparation of income statements and identification of profitability of the business in reliable

ways. So it could be said that marginal costing is one of the approach by which the organisation

can meet to their desired profitability.

TASK 3

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control

Management accounting approach is a system by which company can manage crucial

circumstances of the business in relevant form. By which development could be gained in

appropriate ways, so that budget can be prepared within the organisation (Hopper and Bui,

7

This can be used by the organisational manager in terms of generation of more profitability in the

industry effectively and in case of absorption costing approach, cost identification of fixed and

variable costing is considered as the product cost of Tech(UK) Ltd. Apart from it, there are some

classification of overhead costing in the business in relevant form in which, in case of marginal

costing the fixed and marginal costing is classified as overhead costing in the company and in

case of absorption costing approach, there some of classification of costing is inclusion which is

production cost, administration costing and selling and distribution costs in the company in more

relevant form.

In case of marginal costing approach, the profitability of the company is measured by the

profit volume ratio in the company in relevant form and in absorption costing, due to the

involvement of fixed costing in the company, organisational profitability gets affected

efficiently. In Tech (UK) Ltd enterprise, there is some of direct material and direct labour fixed

production overhead costing is associated in the company in appropriate form for preparation of

costing in the business (Kokubu and Kitada, 2015). In case of marginal costing approach of the

company, its profitable figure showing value which is, 2875 and moreover, in case of absorption

costing techniques, its net profit is showing the value which is -375 which is more than marginal

costing in the company, because of addition of selling and administration fixed overhead

expenses within the organisation in effective manner. Hence, it could be said that the

organisational manager requires utilisation of absorption costing techniques at the workplace in

more sufficient manner in order to ascertain many things in the business environment in proper

sort. Moreover, it is also concluded that organisation manager can use both techniques in respect

to preparation of income statements and identification of profitability of the business in reliable

ways. So it could be said that marginal costing is one of the approach by which the organisation

can meet to their desired profitability.

TASK 3

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control

Management accounting approach is a system by which company can manage crucial

circumstances of the business in relevant form. By which development could be gained in

appropriate ways, so that budget can be prepared within the organisation (Hopper and Bui,

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016). In case of Tech (UK) Ltd organisation, they need to make utilisation of various kind of

budgeting controlling tools at the workplace in more effective manner in order to have proper

management of finance in the company. Proper information regarding budgetary control assists

the business manager in terms of appropriate planning and controlling of budget in the

organisation in effective manner. Several budget formation of management accounting makes

impact on the influences in the forecasting of the departmental exercises and how the manager

can address the growth of the company in the industry in order to meet their desired goals and

objectives in appropriate trems.

Master budget: This is the most appropriate option for Tech (UK) Ltd organisation for

formation of budgeting at the workplace in more effective form. The budget assists' manager to

conduct of all activities of the firm according to master budget period effectively. This is made

for specific projection in the company, in order to formation of cash budget, budgeting income

and budgeted balance sheets effectively (Yalcin, 2012). In case of these budget, all of these are

interrelated to each other in the company in effective manner and several departments are also

associated with them. Manager of the company generally utilises this budgeting process for

completion of plan of projection and meeting objectives in the company effectively.

Advantages:

The major advantage of master budget is that, it furnishes effective company's executives

overview on the specific type of company's budget in more relevant form. It has ability to proper identification of appropriate planning and issues ahead the

business within the business environment efficiently.

Disadvantage:

The major disadvantage of master budgeting is that, it has lower specificity at the

workplace.

This budget is difficult to read and update by the business manager in the company

effectively.

Fixed budget: This is an approach of budgeting at the workplace which never fluctuates

in the company when sales and some of essential exercises increase and decrease in the business

envelopment effectively. The budget has also other name which is statistical budget at the

workplace. Fixed budget is an assumption which is based on particular volume of some good

during some period within the organisation effectively (Ramljak and Rogošić, 2012).

8

budgeting controlling tools at the workplace in more effective manner in order to have proper

management of finance in the company. Proper information regarding budgetary control assists

the business manager in terms of appropriate planning and controlling of budget in the

organisation in effective manner. Several budget formation of management accounting makes

impact on the influences in the forecasting of the departmental exercises and how the manager

can address the growth of the company in the industry in order to meet their desired goals and

objectives in appropriate trems.

Master budget: This is the most appropriate option for Tech (UK) Ltd organisation for

formation of budgeting at the workplace in more effective form. The budget assists' manager to

conduct of all activities of the firm according to master budget period effectively. This is made

for specific projection in the company, in order to formation of cash budget, budgeting income

and budgeted balance sheets effectively (Yalcin, 2012). In case of these budget, all of these are

interrelated to each other in the company in effective manner and several departments are also

associated with them. Manager of the company generally utilises this budgeting process for

completion of plan of projection and meeting objectives in the company effectively.

Advantages:

The major advantage of master budget is that, it furnishes effective company's executives

overview on the specific type of company's budget in more relevant form. It has ability to proper identification of appropriate planning and issues ahead the

business within the business environment efficiently.

Disadvantage:

The major disadvantage of master budgeting is that, it has lower specificity at the

workplace.

This budget is difficult to read and update by the business manager in the company

effectively.

Fixed budget: This is an approach of budgeting at the workplace which never fluctuates

in the company when sales and some of essential exercises increase and decrease in the business

envelopment effectively. The budget has also other name which is statistical budget at the

workplace. Fixed budget is an assumption which is based on particular volume of some good

during some period within the organisation effectively (Ramljak and Rogošić, 2012).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages:

The main advantage of fixed budgeting is that, manager of the organisation can easily

formulate this kind of budget and they do not require to regular modify this in the

organisation.

It assists the business manager in terms of controlling on the costing of production and

services of the company and also assisting in making smart decision within the

organisation effectively.

Disadvantages:

The main disadvantage of fixed budgeting is that it has lower flexibility to change in the

organisation in given time period and sometimes, it gives negative results in the

company.

It is based on previous statistical data of the company so it is difficult to establish and

implement them in the future efficiently.

The budget preparation process:

Obtaining estimates: This is the first step of budget preparation, in which the

computation of sales, production level and expected cost of production etc. the departmental

manager needs to make forecasting about to the future estimation of production expenses and

profitability of the business effectively (Blocher, Stout and Cokins, 2010).

Coordinating estimation: In terms of budget preparation, the organisational manager

needs to make assessment of various plans of action in the company and according to them,

ascertain the potentiality of the company for accomplishment of organisational goals and

objectives.

` Communicating budget: This is also prime responsibility of the manager in terms of

preparation of their plans and actions in more relevant form. They need to communicate plan of

budgeting preparation according to predetermined responsibilities and functions of the company

in efficient form.

Implement the budget plan: this is the final stage of the budget plan, in which manager

of the company need to complete each function requirements in appropriate manner and provides

proper resources to materials, labours, services and human resources in order to implementation

of budgeting in proper format.

Different pricing and costing system:

9

The main advantage of fixed budgeting is that, manager of the organisation can easily

formulate this kind of budget and they do not require to regular modify this in the

organisation.

It assists the business manager in terms of controlling on the costing of production and

services of the company and also assisting in making smart decision within the

organisation effectively.

Disadvantages:

The main disadvantage of fixed budgeting is that it has lower flexibility to change in the

organisation in given time period and sometimes, it gives negative results in the

company.

It is based on previous statistical data of the company so it is difficult to establish and

implement them in the future efficiently.

The budget preparation process:

Obtaining estimates: This is the first step of budget preparation, in which the

computation of sales, production level and expected cost of production etc. the departmental

manager needs to make forecasting about to the future estimation of production expenses and

profitability of the business effectively (Blocher, Stout and Cokins, 2010).

Coordinating estimation: In terms of budget preparation, the organisational manager

needs to make assessment of various plans of action in the company and according to them,

ascertain the potentiality of the company for accomplishment of organisational goals and

objectives.

` Communicating budget: This is also prime responsibility of the manager in terms of

preparation of their plans and actions in more relevant form. They need to communicate plan of

budgeting preparation according to predetermined responsibilities and functions of the company

in efficient form.

Implement the budget plan: this is the final stage of the budget plan, in which manager

of the company need to complete each function requirements in appropriate manner and provides

proper resources to materials, labours, services and human resources in order to implementation

of budgeting in proper format.

Different pricing and costing system:

9

Cost based pricing: Cost based pricing approach would assist the business manager in order to

ascertaining cost of each product and services offering for organisation's customer's in the market

Direct costing and Full costing pricing are two different kinds of budget in the business.

Cost-plus budget:Cost plus pricing occurs in business where its manager compute the costing of

manufacturing process overheads,direct labour and direct materials which will be associated with

the price of products and services of the firm.

Profit pricing: The pricing method is used by its manager to giving proper pricing to each

products by adding various types of manufacturing and other costing which occurred in the

business while manufacturing products. It defines about profitability of the business which has

been earned by the firm while selling its products and services.

TASK 4

P.5. Evaluation of Balance scorecard and some other financial approaches in terms of proper

address of financial issues in the organisation

There are numbers of management accounting tools and techniques are presented by

which Tech(UK) Ltd organisation can improve their financial performance and also identify the

relevant issues in the company in more effective form (Ward, 2012). With the assistance of these

approaches, Tech(UK) Ltd business entity can resolve their financial issues in effective manner.

Balance score card: This is a scorecard of balance performance in the company by which

strategic manager could easily recognise the improvement in several organisational functions in

the company in relevant form. This is mostly used by the organisation in terms of provision of

appropriate suggestion and feedback to proper changes in the strategy of the organisation in

order to make improvement in the business (Hilton and Platt, 2013). As per the approach, the

information is collected and effectively interpreted by the business manager in order to sustain in

the market so that better decision could be made in the organisation effectively. Balance

scorecard is also the most appropriate method for Tech (UK) Ltd organisation in context of

identification of several critical issues in the firm and also make efforts in order to resolve them

in sufficient form. This tool furnishes effective and comprehensive information to the manager of

the company in order to determine the financial measurement and additional metrics that shows

customer satisfaction and production innovation effectiveness within the organisation effectively.

Key performance indicator: This is also one of the vital tools of resolution of financial

issues in the company in effective ways and they need to furnish effective services in proper

10

ascertaining cost of each product and services offering for organisation's customer's in the market

Direct costing and Full costing pricing are two different kinds of budget in the business.

Cost-plus budget:Cost plus pricing occurs in business where its manager compute the costing of

manufacturing process overheads,direct labour and direct materials which will be associated with

the price of products and services of the firm.

Profit pricing: The pricing method is used by its manager to giving proper pricing to each

products by adding various types of manufacturing and other costing which occurred in the

business while manufacturing products. It defines about profitability of the business which has

been earned by the firm while selling its products and services.

TASK 4

P.5. Evaluation of Balance scorecard and some other financial approaches in terms of proper

address of financial issues in the organisation

There are numbers of management accounting tools and techniques are presented by

which Tech(UK) Ltd organisation can improve their financial performance and also identify the

relevant issues in the company in more effective form (Ward, 2012). With the assistance of these

approaches, Tech(UK) Ltd business entity can resolve their financial issues in effective manner.

Balance score card: This is a scorecard of balance performance in the company by which

strategic manager could easily recognise the improvement in several organisational functions in

the company in relevant form. This is mostly used by the organisation in terms of provision of

appropriate suggestion and feedback to proper changes in the strategy of the organisation in

order to make improvement in the business (Hilton and Platt, 2013). As per the approach, the

information is collected and effectively interpreted by the business manager in order to sustain in

the market so that better decision could be made in the organisation effectively. Balance

scorecard is also the most appropriate method for Tech (UK) Ltd organisation in context of

identification of several critical issues in the firm and also make efforts in order to resolve them

in sufficient form. This tool furnishes effective and comprehensive information to the manager of

the company in order to determine the financial measurement and additional metrics that shows

customer satisfaction and production innovation effectiveness within the organisation effectively.

Key performance indicator: This is also one of the vital tools of resolution of financial

issues in the company in effective ways and they need to furnish effective services in proper

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.