University Managerial Accounting Case Study: Analysis and Solution

VerifiedAdded on 2020/04/21

|10

|1237

|93

Case Study

AI Summary

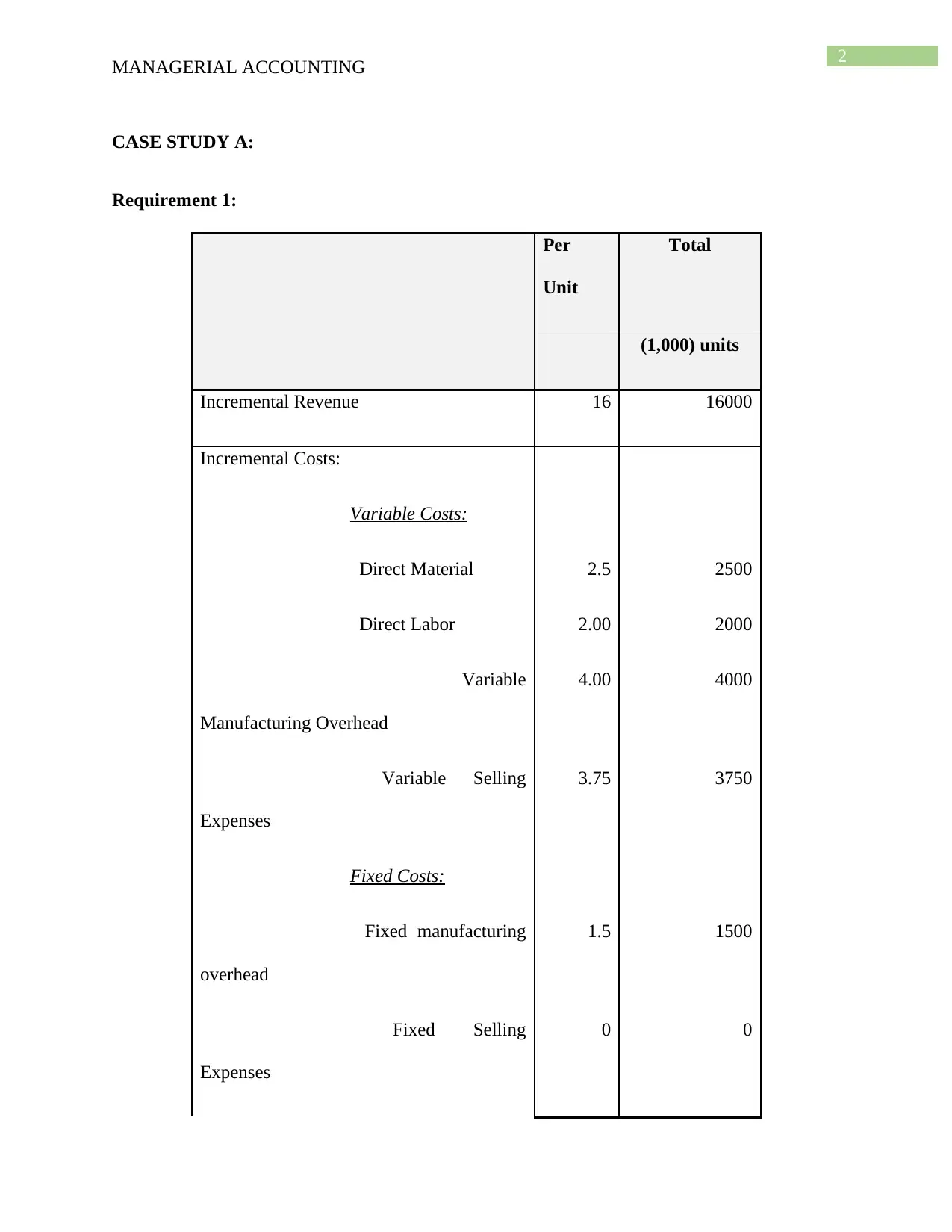

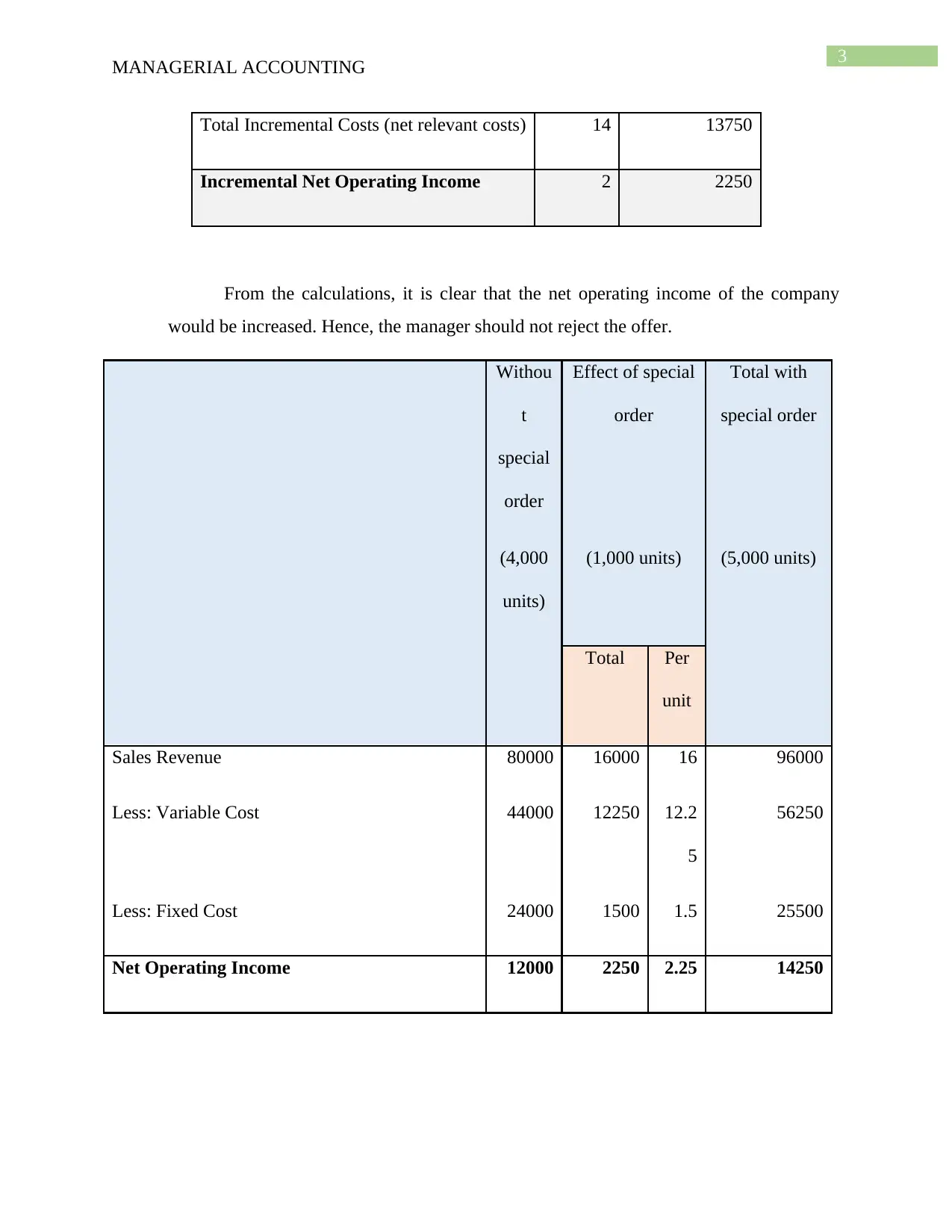

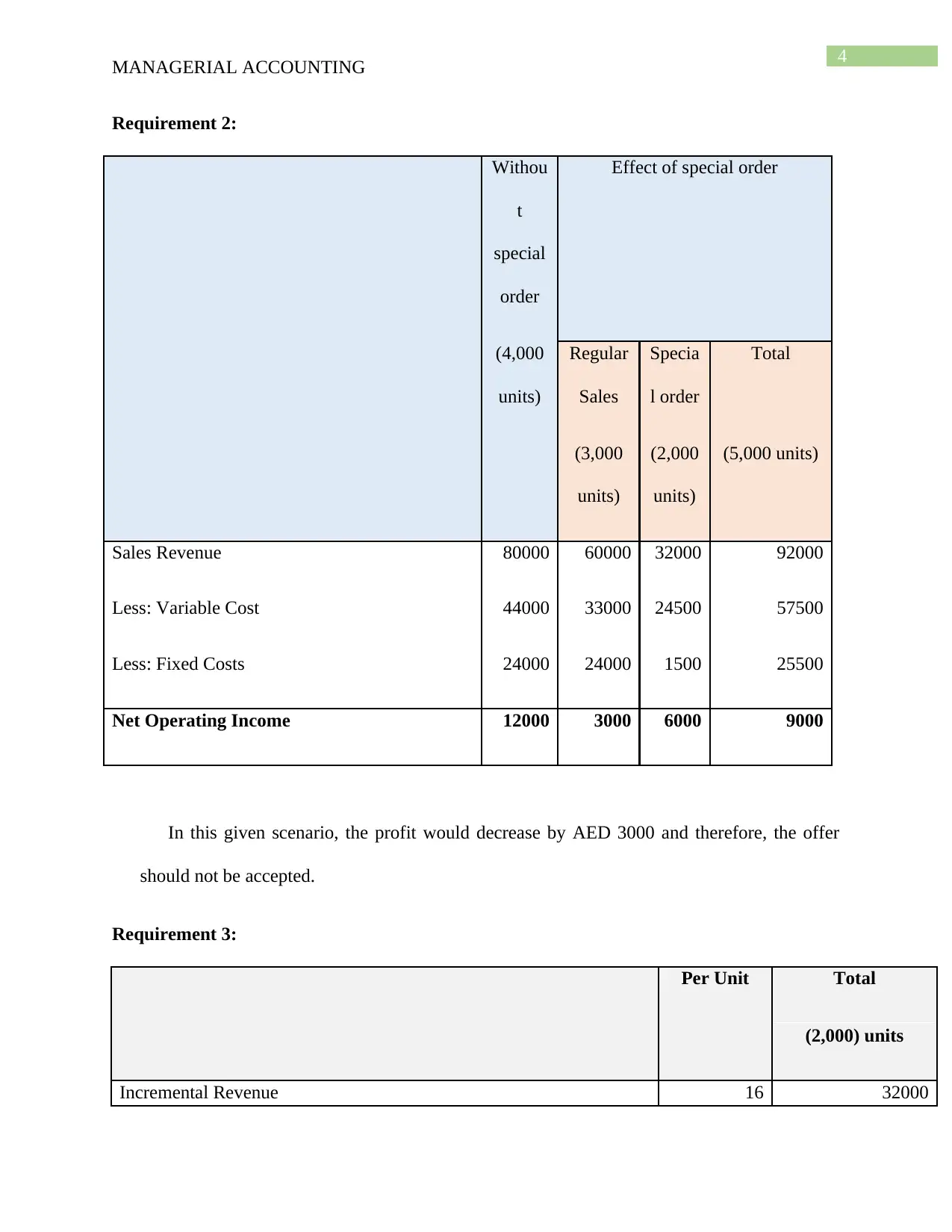

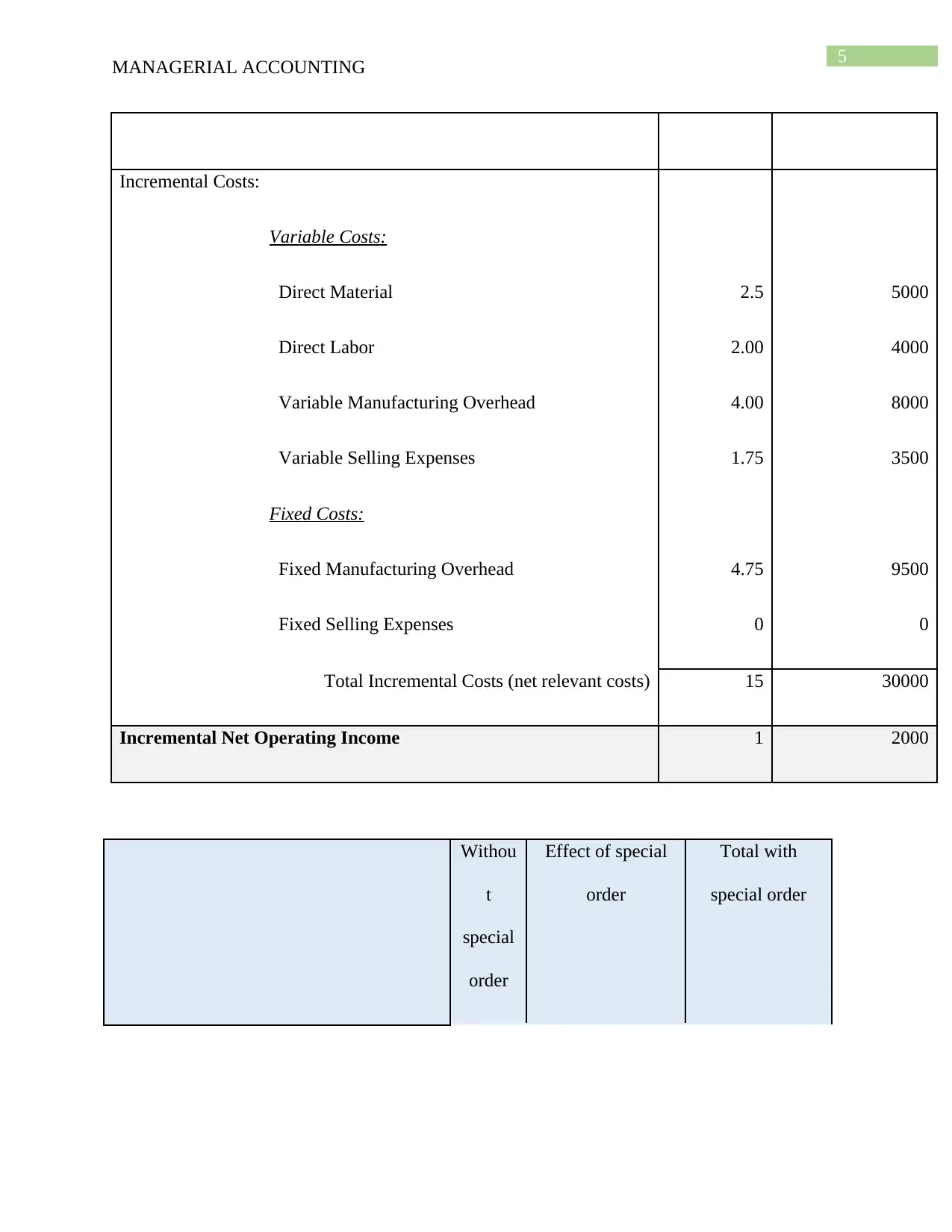

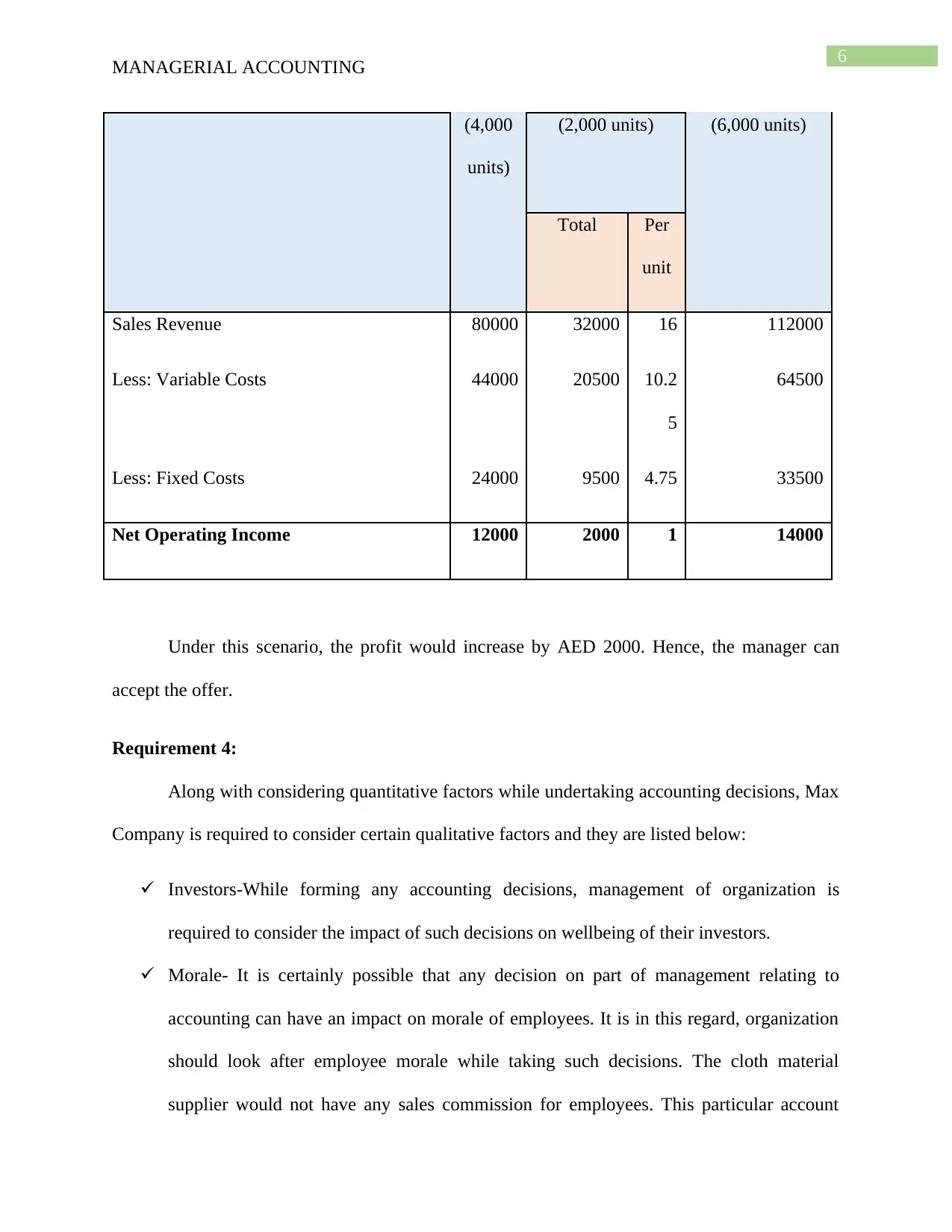

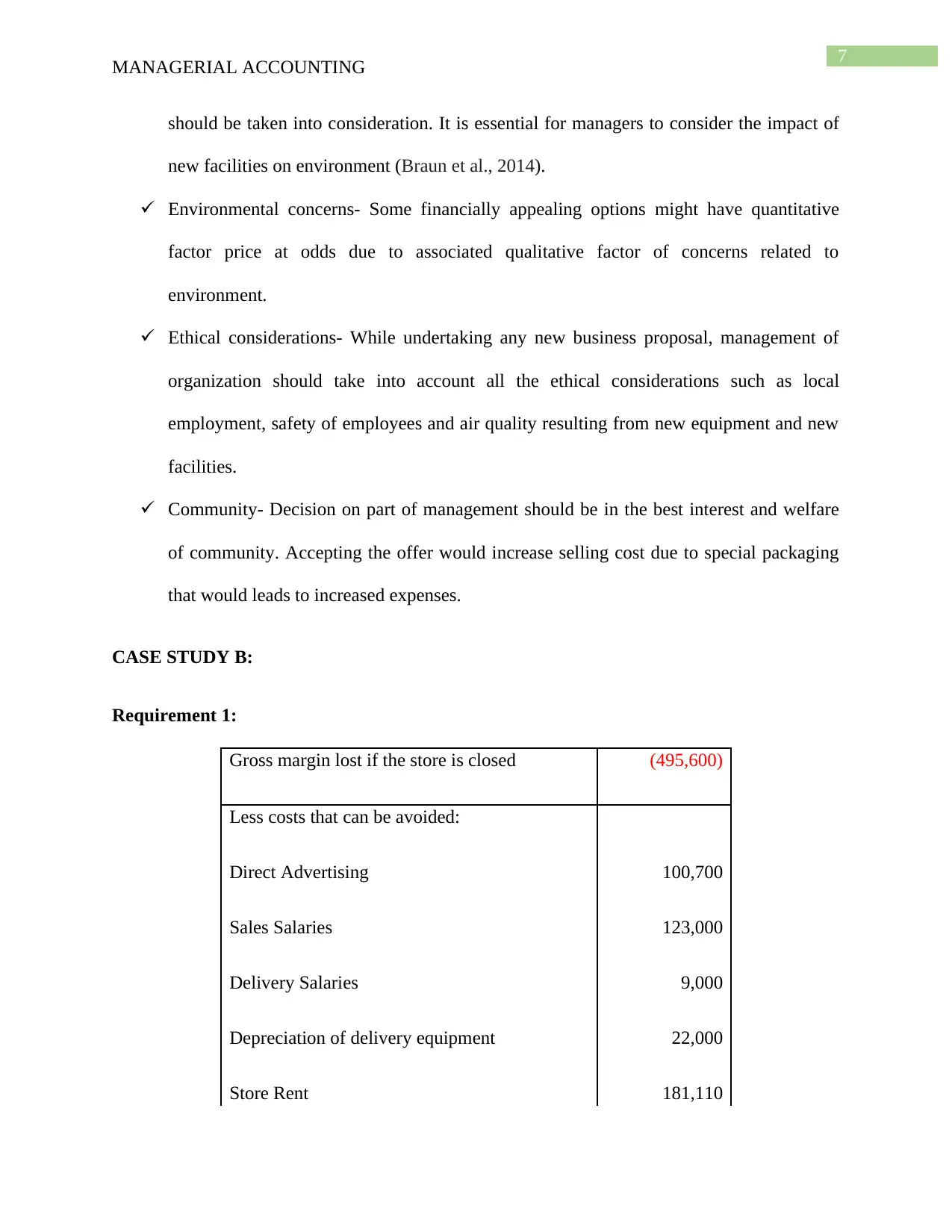

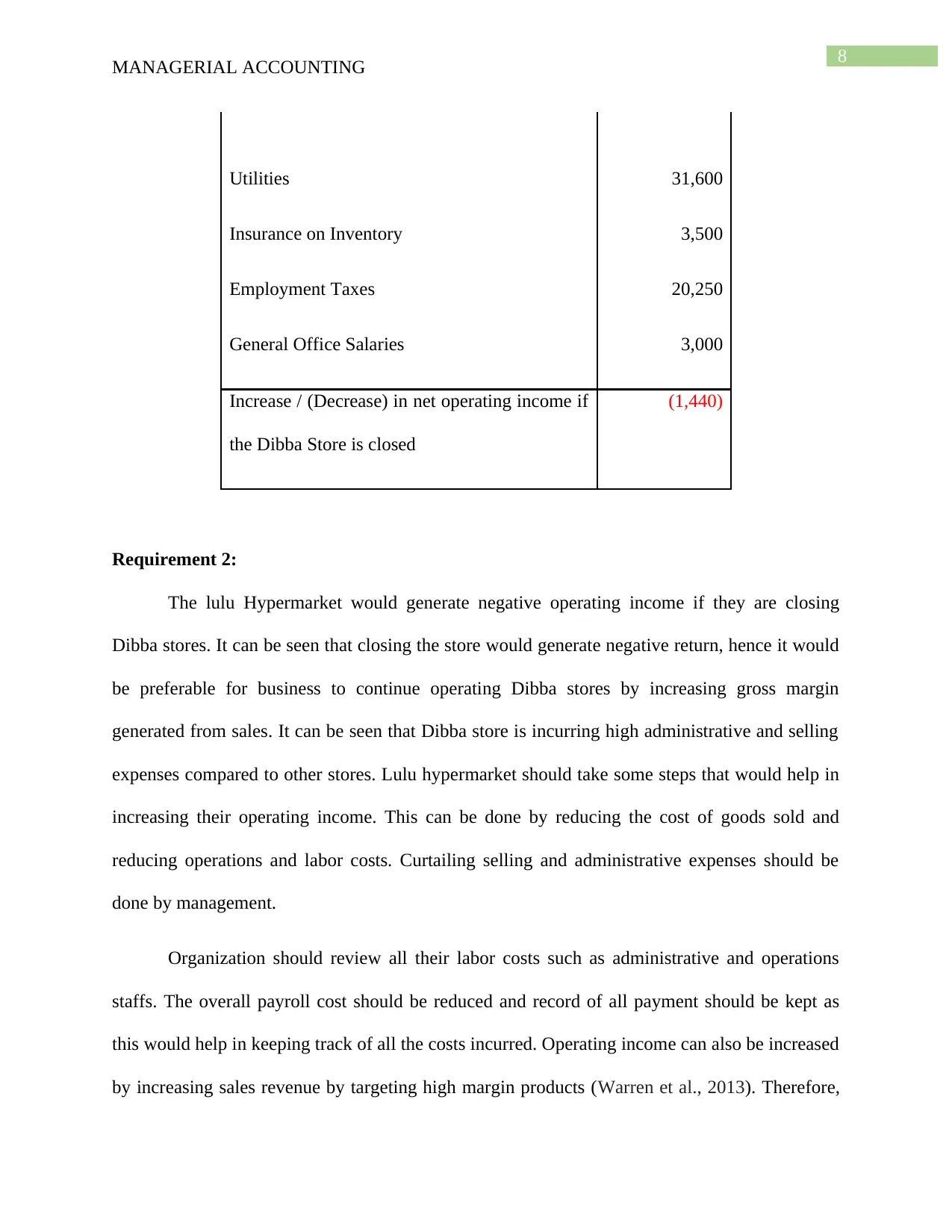

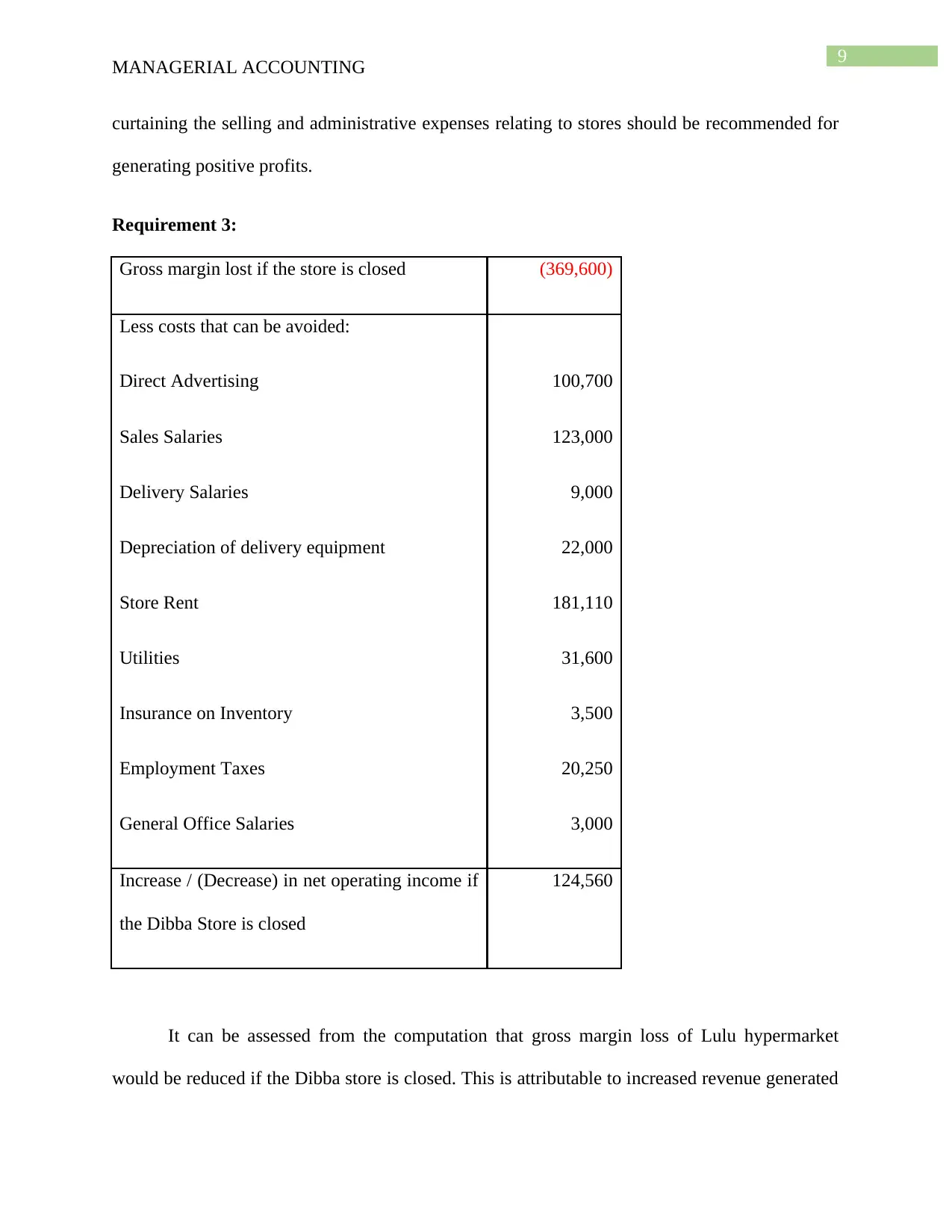

This managerial accounting case study presents two scenarios requiring financial analysis and decision-making. Case Study A examines special order decisions, evaluating incremental revenue, costs, and net operating income under different conditions. It analyzes the impact of accepting or rejecting special orders on profitability, considering both quantitative and qualitative factors like investor impact, employee morale, environmental concerns, ethical considerations, and community welfare. Case Study B focuses on whether to close a store, analyzing the gross margin lost, avoidable costs, and the resulting impact on net operating income. The analysis includes evaluating the potential for increasing operating income by reducing costs and targeting high-margin products. The study considers the effect of closing a store on overall profitability and explores the impact of shifting customers to another store, providing a comprehensive assessment of the financial implications of each decision.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.