Finance Resource Decisions Report: Sainsbury's Analysis

VerifiedAdded on 2020/02/05

|14

|4385

|113

Report

AI Summary

This report delves into the crucial aspects of managing finance resource decisions within a business context, specifically using Sainsbury's as a case study. It begins by identifying and evaluating various internal and external sources of finance available to a company, assessing their implications in terms of costs and benefits. The report then explores how financial information is used by different decision-makers, such as employees, suppliers, investors, and competitors, to make informed choices. It also analyzes the impact of finance on financial statements, including both the income statement and balance sheet. Furthermore, the report examines the use of budgets for financial planning, calculating unit costs for pricing decisions, and applying investment appraisal techniques like net present value and payback period to evaluate investment proposals. Finally, it provides a comprehensive analysis of the company's financial statements, including an examination of different types of businesses and their financial reporting practices.

Managing Finance Resource

Decisions

Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction ...............................................................................................................................1

Task 1.........................................................................................................................................1

AC 1.1 Finance sources available to the business.................................................................1

AC 1.2 Implication of different sources................................................................................1

AC 1.3 Appropriate finance source.......................................................................................2

AC 2.1 Cost of different finance sources..............................................................................2

AC 2.2 Importance of financial planning..............................................................................2

AC 2.3 Information needs of different decision makers.......................................................3

AC 2.4 Impact of finance on the financial statements...........................................................3

Task 2.........................................................................................................................................3

AC 3.1 Analysis of budgets and take decisions.....................................................................3

AC 3.2 Calculation of unit cost and make pricing decisions.................................................4

AC 3.3 Investment appraisal techniques...............................................................................6

Task 3.........................................................................................................................................8

AC 4.1 Financial statements of the company........................................................................8

AC 4.2 Financial statements of different type of businesses.................................................8

AC 4.3 Analysis of financial statements...............................................................................9

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Introduction ...............................................................................................................................1

Task 1.........................................................................................................................................1

AC 1.1 Finance sources available to the business.................................................................1

AC 1.2 Implication of different sources................................................................................1

AC 1.3 Appropriate finance source.......................................................................................2

AC 2.1 Cost of different finance sources..............................................................................2

AC 2.2 Importance of financial planning..............................................................................2

AC 2.3 Information needs of different decision makers.......................................................3

AC 2.4 Impact of finance on the financial statements...........................................................3

Task 2.........................................................................................................................................3

AC 3.1 Analysis of budgets and take decisions.....................................................................3

AC 3.2 Calculation of unit cost and make pricing decisions.................................................4

AC 3.3 Investment appraisal techniques...............................................................................6

Task 3.........................................................................................................................................8

AC 4.1 Financial statements of the company........................................................................8

AC 4.2 Financial statements of different type of businesses.................................................8

AC 4.3 Analysis of financial statements...............................................................................9

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

INTRODUCTION

Every organization has set objectives or targets that the organization needs to achieve.

The success of the business is very much dependent on the availability of finance sources that

the organization requires to run its business. Sainsbury's is the second largest chain of

supermarket in the United Kingdom headquartered in Holborn, London, UK. The company

was established in the year 1869. It operates at international place as it operates in different

countries over the world. The report aims at identifying a range of finance sources for the

company, their implication in terms of cost and benefits. Moreover, the report will explain

that how financial information is used by various decision makers to take important

decisions. Further, Investment appraisal techniques are also identified to evaluate the

alternatives and select the best investment proposal.

TASK 1

AC 1.1 Finance sources available to the business

Sainsbury can fulfil its finance need through distinct type of finance sources that are

described as follows;

Internal sources: These types of sources are available within the organization itself.

The internal sources include retained earnings, other business profits, disposing off the scrap

assets or cash squeezing operations. Retained earnings are the remaining profit balances that

are not distributed among the shareholders. Further, Sainsbury's operates at larger place

hence; it can also use the profits of other businesses. On contrary, through selling the

unusable assets or making delayed payments to the creditors company can avail larger the

cash balances.

External sources: These sources are available outside from the organization includes

bank loans, share capital and overdraft facilities. Sainsbury can take loans from banks for

different time duration. Further, banks also provide overdraft facilities to the company in

order to mitigate the urgent requirement. Moreover, the company can issue shares in the

market to the public to generate the required funds. Another important source is debentures

Sainsbury can issue the debenture to the holders to fulfil the financial needs (Minnis, 2011).

Moreover, venture capital can be provided to the investors for enhancing the funds.

AC 1.2 Implication of different sources

All the finance sources applied different implication to the business. On the share

capital business require to pay return to the shareholders. In case of bank loan and overdraft

businesses require to pay interest charges along with the principal payment. On contrary, in

1 | P a g e

Every organization has set objectives or targets that the organization needs to achieve.

The success of the business is very much dependent on the availability of finance sources that

the organization requires to run its business. Sainsbury's is the second largest chain of

supermarket in the United Kingdom headquartered in Holborn, London, UK. The company

was established in the year 1869. It operates at international place as it operates in different

countries over the world. The report aims at identifying a range of finance sources for the

company, their implication in terms of cost and benefits. Moreover, the report will explain

that how financial information is used by various decision makers to take important

decisions. Further, Investment appraisal techniques are also identified to evaluate the

alternatives and select the best investment proposal.

TASK 1

AC 1.1 Finance sources available to the business

Sainsbury can fulfil its finance need through distinct type of finance sources that are

described as follows;

Internal sources: These types of sources are available within the organization itself.

The internal sources include retained earnings, other business profits, disposing off the scrap

assets or cash squeezing operations. Retained earnings are the remaining profit balances that

are not distributed among the shareholders. Further, Sainsbury's operates at larger place

hence; it can also use the profits of other businesses. On contrary, through selling the

unusable assets or making delayed payments to the creditors company can avail larger the

cash balances.

External sources: These sources are available outside from the organization includes

bank loans, share capital and overdraft facilities. Sainsbury can take loans from banks for

different time duration. Further, banks also provide overdraft facilities to the company in

order to mitigate the urgent requirement. Moreover, the company can issue shares in the

market to the public to generate the required funds. Another important source is debentures

Sainsbury can issue the debenture to the holders to fulfil the financial needs (Minnis, 2011).

Moreover, venture capital can be provided to the investors for enhancing the funds.

AC 1.2 Implication of different sources

All the finance sources applied different implication to the business. On the share

capital business require to pay return to the shareholders. In case of bank loan and overdraft

businesses require to pay interest charges along with the principal payment. On contrary, in

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

case of share capital they have controlling rights as they can manage the operations of the

businesses (Schroeder, Clark and Cathey, 2011). However, banks have not such kind of rights

they can only sell the provided security against the given loan. Furthermore, on the issued

debentures company require to pay fixed rate of interest to the debentures.

AC 1.3 Appropriate finance source

Appropriate finance sources can be select on the basis of their implication. For

fulfilling the urgent or immediate requirement the overdraft and retained earnings will be

appropriate sources. However, for fulfilling the medium term requirement bank loans can be

taken by the company (Managing Financial Resources and Decisions, n.d.). Further, long

term finance requirement can be filled through issuing share capital as the equity

shareholders return are not fixed. Therefore, it does not impose any fixed burden to the

company. Moreover, venture capital also can be provided to the investors for this purpose.

AC 2.1 Cost of different finance sources

The cost of distinct finance sources tends to vary from each other. For instance, on the

issued amount of share capital, the company require to pay dividend to their shareholders.

Further, before adopting any new policy shareholders must be communicate as they are the

owners and having voting rights that give them right to manage the business operations.

However, the cost of bank loans, debentures and overdraft facilities involve interest charges.

The interest rate on bank loans may be of two kinds fixed or fluctuating (Malmi and

Granlund, 2009). However, under the debentures company need to pay a fixed rate of interest

to the holders. Moreover, retained earning does not include any financial burden to the

company. However, it includes opportunities cost as the company can use this retained

earnings in the other sources. For instance, it can invest the profits in other company that

having higher the profits. Further, the cost of cash squeezing operation is that business can

not avail cash discount in case of delayed payments.

AC 2.2 Importance of financial planning

Financial planning helps to manage the business finance sources in an efficient

manner. Moreover, it helps to take better investment and working capital decisions. It

determines the organization fund requirement and determines optimum capital structure. It

helps to attain debt and equity in an appropriate ratio at minimum cost that helps to yield

maximum return. Further, it manages the working capital through administrating the cash

inflows and outflows (Ismail and Mohsin, 2013). Through financial planning business is able

to control income efficiently. Effective financial planning helps to make easier the financial

2 | P a g e

businesses (Schroeder, Clark and Cathey, 2011). However, banks have not such kind of rights

they can only sell the provided security against the given loan. Furthermore, on the issued

debentures company require to pay fixed rate of interest to the debentures.

AC 1.3 Appropriate finance source

Appropriate finance sources can be select on the basis of their implication. For

fulfilling the urgent or immediate requirement the overdraft and retained earnings will be

appropriate sources. However, for fulfilling the medium term requirement bank loans can be

taken by the company (Managing Financial Resources and Decisions, n.d.). Further, long

term finance requirement can be filled through issuing share capital as the equity

shareholders return are not fixed. Therefore, it does not impose any fixed burden to the

company. Moreover, venture capital also can be provided to the investors for this purpose.

AC 2.1 Cost of different finance sources

The cost of distinct finance sources tends to vary from each other. For instance, on the

issued amount of share capital, the company require to pay dividend to their shareholders.

Further, before adopting any new policy shareholders must be communicate as they are the

owners and having voting rights that give them right to manage the business operations.

However, the cost of bank loans, debentures and overdraft facilities involve interest charges.

The interest rate on bank loans may be of two kinds fixed or fluctuating (Malmi and

Granlund, 2009). However, under the debentures company need to pay a fixed rate of interest

to the holders. Moreover, retained earning does not include any financial burden to the

company. However, it includes opportunities cost as the company can use this retained

earnings in the other sources. For instance, it can invest the profits in other company that

having higher the profits. Further, the cost of cash squeezing operation is that business can

not avail cash discount in case of delayed payments.

AC 2.2 Importance of financial planning

Financial planning helps to manage the business finance sources in an efficient

manner. Moreover, it helps to take better investment and working capital decisions. It

determines the organization fund requirement and determines optimum capital structure. It

helps to attain debt and equity in an appropriate ratio at minimum cost that helps to yield

maximum return. Further, it manages the working capital through administrating the cash

inflows and outflows (Ismail and Mohsin, 2013). Through financial planning business is able

to control income efficiently. Effective financial planning helps to make easier the financial

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions in order to achieve the business goals. Moreover, it minimizes the risk factor and

negative impact of market uncertainties to the business. Thus, it can be said that financial

planning is a very important tool for the business.

AC 2.3 Information needs of different decision makers

There are number of decision makers that require financial information regarding the

company's operation to take decisions. Employees require information regarding company's

profits and the growth. It is because all their interest in company is related to the business

success. They are very much interested to get increased salary, better working environment,

working culture and other non monetary benefits. Higher the business performance satisfies

the employees’ needs to a great extent. Supplier analyse the company's creditworthiness to

pay the liabilities on right time. Thus, they wanted to know the business financial

performance. Improved financial performance of the business can avail favourable supplier

terms. Investor invests their money so as to attain greater return. Therefore, they wanted to

know the business return and analyse the risk return factor of alternative businesses in order

to make correct investment decisions (Georgiou, 2010). Further, Government require that all

the business make payment of their taxes on regular basis. It identifies the business

profitability and determines the taxes that business organization is paying tax or not.

Competitor requires information to know their competitors position in the market and

determine their policies and strategies for the purpose of compete effectively.

AC 2.4 Impact of finance on the financial statements

All the finance sources show in the business financial statements of the company.

Financial statements include both income statements and balance sheet. The process in which

business entity records the business transaction is known as financial statements. The amount

of issued share capital shows in both the assets and liability side. However, the dividend

shows in the income statements of the company. Further, the interest payment shows in the

income statement as finance cost. However, the amount of loan shows in the both assets and

liability side. Further, the amount of retained earning that is used by the company for fulfil

the finance requirement shows in the retained earnings statements.

TASK 2

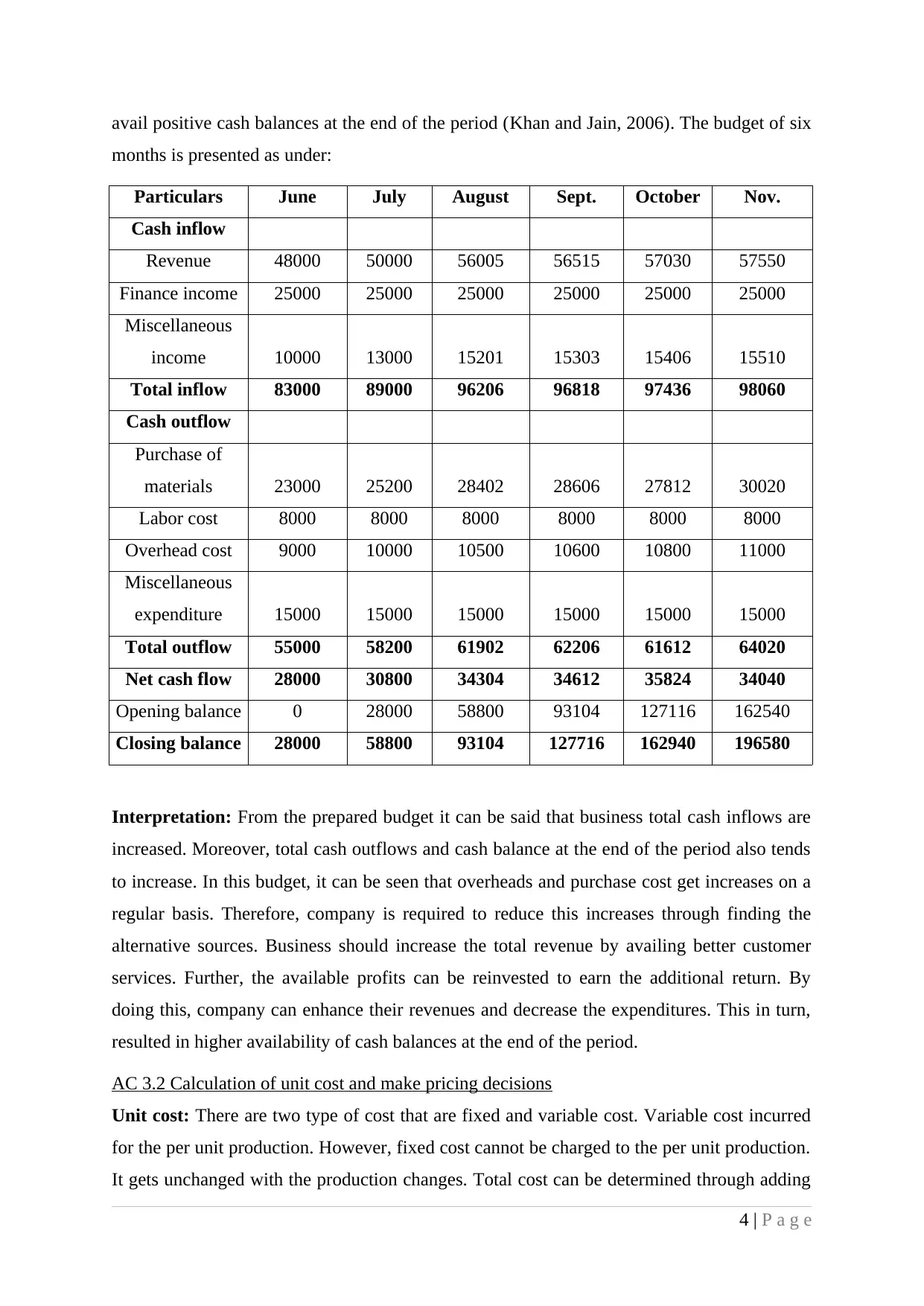

AC 3.1 Analysis of budgets and take decisions

Budgets are prepared through forecasting the future expenditures and incomes for a

specified period. It helps to increase the revenue and reduce the expenditures that help to

3 | P a g e

negative impact of market uncertainties to the business. Thus, it can be said that financial

planning is a very important tool for the business.

AC 2.3 Information needs of different decision makers

There are number of decision makers that require financial information regarding the

company's operation to take decisions. Employees require information regarding company's

profits and the growth. It is because all their interest in company is related to the business

success. They are very much interested to get increased salary, better working environment,

working culture and other non monetary benefits. Higher the business performance satisfies

the employees’ needs to a great extent. Supplier analyse the company's creditworthiness to

pay the liabilities on right time. Thus, they wanted to know the business financial

performance. Improved financial performance of the business can avail favourable supplier

terms. Investor invests their money so as to attain greater return. Therefore, they wanted to

know the business return and analyse the risk return factor of alternative businesses in order

to make correct investment decisions (Georgiou, 2010). Further, Government require that all

the business make payment of their taxes on regular basis. It identifies the business

profitability and determines the taxes that business organization is paying tax or not.

Competitor requires information to know their competitors position in the market and

determine their policies and strategies for the purpose of compete effectively.

AC 2.4 Impact of finance on the financial statements

All the finance sources show in the business financial statements of the company.

Financial statements include both income statements and balance sheet. The process in which

business entity records the business transaction is known as financial statements. The amount

of issued share capital shows in both the assets and liability side. However, the dividend

shows in the income statements of the company. Further, the interest payment shows in the

income statement as finance cost. However, the amount of loan shows in the both assets and

liability side. Further, the amount of retained earning that is used by the company for fulfil

the finance requirement shows in the retained earnings statements.

TASK 2

AC 3.1 Analysis of budgets and take decisions

Budgets are prepared through forecasting the future expenditures and incomes for a

specified period. It helps to increase the revenue and reduce the expenditures that help to

3 | P a g e

avail positive cash balances at the end of the period (Khan and Jain, 2006). The budget of six

months is presented as under:

Particulars June July August Sept. October Nov.

Cash inflow

Revenue 48000 50000 56005 56515 57030 57550

Finance income 25000 25000 25000 25000 25000 25000

Miscellaneous

income 10000 13000 15201 15303 15406 15510

Total inflow 83000 89000 96206 96818 97436 98060

Cash outflow

Purchase of

materials 23000 25200 28402 28606 27812 30020

Labor cost 8000 8000 8000 8000 8000 8000

Overhead cost 9000 10000 10500 10600 10800 11000

Miscellaneous

expenditure 15000 15000 15000 15000 15000 15000

Total outflow 55000 58200 61902 62206 61612 64020

Net cash flow 28000 30800 34304 34612 35824 34040

Opening balance 0 28000 58800 93104 127116 162540

Closing balance 28000 58800 93104 127716 162940 196580

Interpretation: From the prepared budget it can be said that business total cash inflows are

increased. Moreover, total cash outflows and cash balance at the end of the period also tends

to increase. In this budget, it can be seen that overheads and purchase cost get increases on a

regular basis. Therefore, company is required to reduce this increases through finding the

alternative sources. Business should increase the total revenue by availing better customer

services. Further, the available profits can be reinvested to earn the additional return. By

doing this, company can enhance their revenues and decrease the expenditures. This in turn,

resulted in higher availability of cash balances at the end of the period.

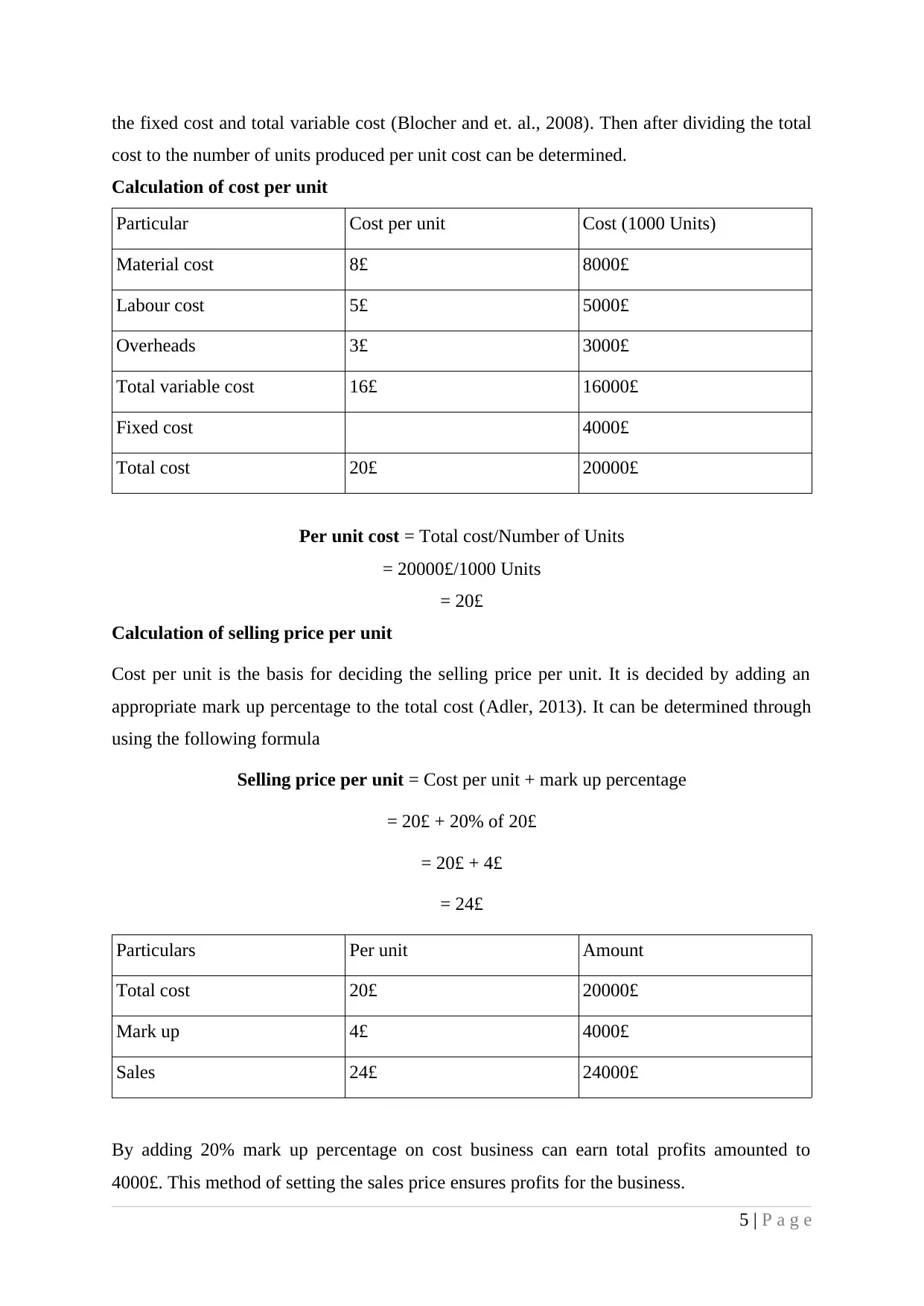

AC 3.2 Calculation of unit cost and make pricing decisions

Unit cost: There are two type of cost that are fixed and variable cost. Variable cost incurred

for the per unit production. However, fixed cost cannot be charged to the per unit production.

It gets unchanged with the production changes. Total cost can be determined through adding

4 | P a g e

months is presented as under:

Particulars June July August Sept. October Nov.

Cash inflow

Revenue 48000 50000 56005 56515 57030 57550

Finance income 25000 25000 25000 25000 25000 25000

Miscellaneous

income 10000 13000 15201 15303 15406 15510

Total inflow 83000 89000 96206 96818 97436 98060

Cash outflow

Purchase of

materials 23000 25200 28402 28606 27812 30020

Labor cost 8000 8000 8000 8000 8000 8000

Overhead cost 9000 10000 10500 10600 10800 11000

Miscellaneous

expenditure 15000 15000 15000 15000 15000 15000

Total outflow 55000 58200 61902 62206 61612 64020

Net cash flow 28000 30800 34304 34612 35824 34040

Opening balance 0 28000 58800 93104 127116 162540

Closing balance 28000 58800 93104 127716 162940 196580

Interpretation: From the prepared budget it can be said that business total cash inflows are

increased. Moreover, total cash outflows and cash balance at the end of the period also tends

to increase. In this budget, it can be seen that overheads and purchase cost get increases on a

regular basis. Therefore, company is required to reduce this increases through finding the

alternative sources. Business should increase the total revenue by availing better customer

services. Further, the available profits can be reinvested to earn the additional return. By

doing this, company can enhance their revenues and decrease the expenditures. This in turn,

resulted in higher availability of cash balances at the end of the period.

AC 3.2 Calculation of unit cost and make pricing decisions

Unit cost: There are two type of cost that are fixed and variable cost. Variable cost incurred

for the per unit production. However, fixed cost cannot be charged to the per unit production.

It gets unchanged with the production changes. Total cost can be determined through adding

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the fixed cost and total variable cost (Blocher and et. al., 2008). Then after dividing the total

cost to the number of units produced per unit cost can be determined.

Calculation of cost per unit

Particular Cost per unit Cost (1000 Units)

Material cost 8£ 8000£

Labour cost 5£ 5000£

Overheads 3£ 3000£

Total variable cost 16£ 16000£

Fixed cost 4000£

Total cost 20£ 20000£

Per unit cost = Total cost/Number of Units

= 20000£/1000 Units

= 20£

Calculation of selling price per unit

Cost per unit is the basis for deciding the selling price per unit. It is decided by adding an

appropriate mark up percentage to the total cost (Adler, 2013). It can be determined through

using the following formula

Selling price per unit = Cost per unit + mark up percentage

= 20£ + 20% of 20£

= 20£ + 4£

= 24£

Particulars Per unit Amount

Total cost 20£ 20000£

Mark up 4£ 4000£

Sales 24£ 24000£

By adding 20% mark up percentage on cost business can earn total profits amounted to

4000£. This method of setting the sales price ensures profits for the business.

5 | P a g e

cost to the number of units produced per unit cost can be determined.

Calculation of cost per unit

Particular Cost per unit Cost (1000 Units)

Material cost 8£ 8000£

Labour cost 5£ 5000£

Overheads 3£ 3000£

Total variable cost 16£ 16000£

Fixed cost 4000£

Total cost 20£ 20000£

Per unit cost = Total cost/Number of Units

= 20000£/1000 Units

= 20£

Calculation of selling price per unit

Cost per unit is the basis for deciding the selling price per unit. It is decided by adding an

appropriate mark up percentage to the total cost (Adler, 2013). It can be determined through

using the following formula

Selling price per unit = Cost per unit + mark up percentage

= 20£ + 20% of 20£

= 20£ + 4£

= 24£

Particulars Per unit Amount

Total cost 20£ 20000£

Mark up 4£ 4000£

Sales 24£ 24000£

By adding 20% mark up percentage on cost business can earn total profits amounted to

4000£. This method of setting the sales price ensures profits for the business.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break-even point = It is the point at which business total expenses are equal to the total

incomes.

Break-even point = Total Fixed cost/Contribution per unit

= 4000£/ (24£-16£)

= 4000£/8£

= 500 Units

Break Even sales = 500 Units*24 = 12000£

AC 3.3 Investment appraisal techniques

A range of investment appraisal techniques are available to the business organization

that helps to take effective investment decisions. It helps to make comparative analysis

through implementing different methods. Net present value method, payback period method,

accounting rate of return method and internal rate of return method can be used for this

purpose.

Payback period: It refers to the time period that the project will take to return the

initial investment of the project. Such project that takes lower the time should be selected by

the business.

Net present value: in this method, all the cash inflows are discounted by a discount

rate that is appropriate for the project. However, net present value shortened to NPV is

calculated by subtracting the initial cash outlay from the total of discounted cash inflows

(Zimmerman and Yahya-Zadeh, 2011). Such project that has higher the net presented value

should be preferred by the company. It is consider as the best method for investment purpose

as it consider the time value of the money.

Accounting rate of return: It is the average accounting rate of return that is

calculated by dividing the average accounting profits to the total initial cash outlay required

for the project. Higher the ARR should be selected by the business organization.

Internal rate of return: It is the rate at which the difference between total discounted

cash inflows and cash outflow will be zero (Chandra, 2011).

For Instance, ABC Ltd. company require to invest funds for 160000£ in project A and

200000£ in project B. Moreover, the cash inflows during the five years are as follows:

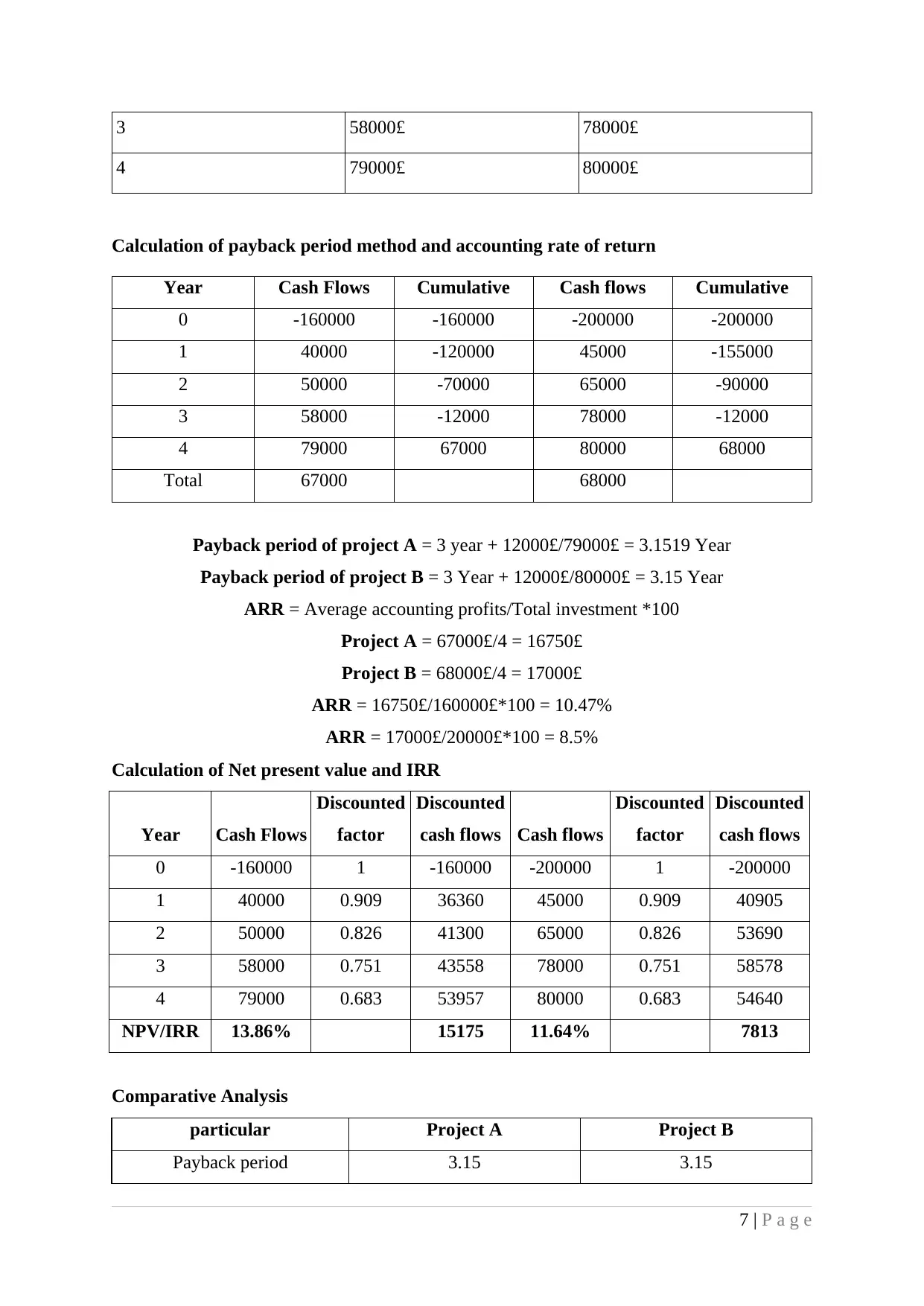

Year Cash Inflows (Project A) Cash Inflows ( Project B)

1 40000£ 45000£

2 50000£ 65000£

6 | P a g e

incomes.

Break-even point = Total Fixed cost/Contribution per unit

= 4000£/ (24£-16£)

= 4000£/8£

= 500 Units

Break Even sales = 500 Units*24 = 12000£

AC 3.3 Investment appraisal techniques

A range of investment appraisal techniques are available to the business organization

that helps to take effective investment decisions. It helps to make comparative analysis

through implementing different methods. Net present value method, payback period method,

accounting rate of return method and internal rate of return method can be used for this

purpose.

Payback period: It refers to the time period that the project will take to return the

initial investment of the project. Such project that takes lower the time should be selected by

the business.

Net present value: in this method, all the cash inflows are discounted by a discount

rate that is appropriate for the project. However, net present value shortened to NPV is

calculated by subtracting the initial cash outlay from the total of discounted cash inflows

(Zimmerman and Yahya-Zadeh, 2011). Such project that has higher the net presented value

should be preferred by the company. It is consider as the best method for investment purpose

as it consider the time value of the money.

Accounting rate of return: It is the average accounting rate of return that is

calculated by dividing the average accounting profits to the total initial cash outlay required

for the project. Higher the ARR should be selected by the business organization.

Internal rate of return: It is the rate at which the difference between total discounted

cash inflows and cash outflow will be zero (Chandra, 2011).

For Instance, ABC Ltd. company require to invest funds for 160000£ in project A and

200000£ in project B. Moreover, the cash inflows during the five years are as follows:

Year Cash Inflows (Project A) Cash Inflows ( Project B)

1 40000£ 45000£

2 50000£ 65000£

6 | P a g e

3 58000£ 78000£

4 79000£ 80000£

Calculation of payback period method and accounting rate of return

Year Cash Flows Cumulative Cash flows Cumulative

0 -160000 -160000 -200000 -200000

1 40000 -120000 45000 -155000

2 50000 -70000 65000 -90000

3 58000 -12000 78000 -12000

4 79000 67000 80000 68000

Total 67000 68000

Payback period of project A = 3 year + 12000£/79000£ = 3.1519 Year

Payback period of project B = 3 Year + 12000£/80000£ = 3.15 Year

ARR = Average accounting profits/Total investment *100

Project A = 67000£/4 = 16750£

Project B = 68000£/4 = 17000£

ARR = 16750£/160000£*100 = 10.47%

ARR = 17000£/20000£*100 = 8.5%

Calculation of Net present value and IRR

Year Cash Flows

Discounted

factor

Discounted

cash flows Cash flows

Discounted

factor

Discounted

cash flows

0 -160000 1 -160000 -200000 1 -200000

1 40000 0.909 36360 45000 0.909 40905

2 50000 0.826 41300 65000 0.826 53690

3 58000 0.751 43558 78000 0.751 58578

4 79000 0.683 53957 80000 0.683 54640

NPV/IRR 13.86% 15175 11.64% 7813

Comparative Analysis

particular Project A Project B

Payback period 3.15 3.15

7 | P a g e

4 79000£ 80000£

Calculation of payback period method and accounting rate of return

Year Cash Flows Cumulative Cash flows Cumulative

0 -160000 -160000 -200000 -200000

1 40000 -120000 45000 -155000

2 50000 -70000 65000 -90000

3 58000 -12000 78000 -12000

4 79000 67000 80000 68000

Total 67000 68000

Payback period of project A = 3 year + 12000£/79000£ = 3.1519 Year

Payback period of project B = 3 Year + 12000£/80000£ = 3.15 Year

ARR = Average accounting profits/Total investment *100

Project A = 67000£/4 = 16750£

Project B = 68000£/4 = 17000£

ARR = 16750£/160000£*100 = 10.47%

ARR = 17000£/20000£*100 = 8.5%

Calculation of Net present value and IRR

Year Cash Flows

Discounted

factor

Discounted

cash flows Cash flows

Discounted

factor

Discounted

cash flows

0 -160000 1 -160000 -200000 1 -200000

1 40000 0.909 36360 45000 0.909 40905

2 50000 0.826 41300 65000 0.826 53690

3 58000 0.751 43558 78000 0.751 58578

4 79000 0.683 53957 80000 0.683 54640

NPV/IRR 13.86% 15175 11.64% 7813

Comparative Analysis

particular Project A Project B

Payback period 3.15 3.15

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

NPV 15175£ 7813£

ARR 10.47% 8.50%

IRR 13.86% 11.64%

Interpretation: On the basis of above calculation it can be concluded that business

should make investment in Project A. The reason behind that is in this project the business

can earn higher amount of return. It is because the net present value of project A and project

B are 15175£ and 7813£. It is higher in case of project A. Further, the ARR and IRR of

project A are 10.47% and 13.86%. However, the project B ARR and IRR are 11.64% and

8.50% respectively. It indicates that project A has greater amount of profitability than

compared to project B. Further, the payback period of both the projects are same to 3.15 year

implies that both the project will take equal time period to get the initial investment of

16000£ and 200000£.

TASK 3

AC 4.1 Financial statements of the company

Financial statements are prepared by every business organization in order to

determine their operational and financial results. There are two statements prepared by every

business that are income statements and balance sheet. Income statements include trading,

profit and loss account.

Trading Account: Trading account is prepared to determine the gross profit and

gross loss from the business trading activities. It includes all the direct income as well as

expenditures (Hayre, 2013).

Profit and loss account: Along with the trading account profit and loss account is

also prepared by every company. It is prepared to find out the net business net results in terms

of net profit or net loss. All the indirect expenses and indirect incomes show in these

statements.

Balance sheet: It is prepared to determine the financial position or the financial status

of the business. Financial growth or weaknesses can be identified through preparing such

statement.

AC 4.2 Financial statements of different type of businesses

There are ranges of financial statements that are prepared by each and every type of

business organization described as under:

8 | P a g e

ARR 10.47% 8.50%

IRR 13.86% 11.64%

Interpretation: On the basis of above calculation it can be concluded that business

should make investment in Project A. The reason behind that is in this project the business

can earn higher amount of return. It is because the net present value of project A and project

B are 15175£ and 7813£. It is higher in case of project A. Further, the ARR and IRR of

project A are 10.47% and 13.86%. However, the project B ARR and IRR are 11.64% and

8.50% respectively. It indicates that project A has greater amount of profitability than

compared to project B. Further, the payback period of both the projects are same to 3.15 year

implies that both the project will take equal time period to get the initial investment of

16000£ and 200000£.

TASK 3

AC 4.1 Financial statements of the company

Financial statements are prepared by every business organization in order to

determine their operational and financial results. There are two statements prepared by every

business that are income statements and balance sheet. Income statements include trading,

profit and loss account.

Trading Account: Trading account is prepared to determine the gross profit and

gross loss from the business trading activities. It includes all the direct income as well as

expenditures (Hayre, 2013).

Profit and loss account: Along with the trading account profit and loss account is

also prepared by every company. It is prepared to find out the net business net results in terms

of net profit or net loss. All the indirect expenses and indirect incomes show in these

statements.

Balance sheet: It is prepared to determine the financial position or the financial status

of the business. Financial growth or weaknesses can be identified through preparing such

statement.

AC 4.2 Financial statements of different type of businesses

There are ranges of financial statements that are prepared by each and every type of

business organization described as under:

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sole proprietorship: Under this type of business organization, an individual person

makes investment in the company. Moreover, all the efforts are made by the entrepreneurs

only so all the profits are available for the entrepreneurs. Further, all the losses are born by

the sole trader. It prepares trading and profit and loss account as the income statements

(Goyal and Goyal 2012). Moreover, balance sheet is prepared in order to determine the

financial position of the business. The sample of trading, profit and loss account and balance

sheet of sole trader are given as under:

Partnership: Under the partnership form of business organization, more than two

partners can make agreement to start the business. Therefore, they all make efforts in the

business and share the business profit and losses. Moreover, the liability of all the partners is

unlimited for the business. It prepares its financial statements according to the partnership act

requirement. It prepares profit and loss account as the income statements and also the balance

sheet.

Company: It is a legal body that came into existence by the companies act. Therefore

all the financial statements are prepared as per the act requirements. It prepares profit and loss

account, balance sheet, statements of retained earnings, cash flow statement and fund flow

statements (O' Bryan, 2010). Moreover, parent company that has any subsidiary company

require preparing consolidated financial statements.

AC 4.3 Analysis of financial statements

Sainsbury's financial statements are analysed by ratio analysis technique (Persons,

2011).

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 1377 1277 1211

Operating profit 1009 887 874

Net profit 716 614 598

Net Sales 23949 23303 22294

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 % 5.43 %

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 4.21 % 3.81% 3.92 %

9 | P a g e

makes investment in the company. Moreover, all the efforts are made by the entrepreneurs

only so all the profits are available for the entrepreneurs. Further, all the losses are born by

the sole trader. It prepares trading and profit and loss account as the income statements

(Goyal and Goyal 2012). Moreover, balance sheet is prepared in order to determine the

financial position of the business. The sample of trading, profit and loss account and balance

sheet of sole trader are given as under:

Partnership: Under the partnership form of business organization, more than two

partners can make agreement to start the business. Therefore, they all make efforts in the

business and share the business profit and losses. Moreover, the liability of all the partners is

unlimited for the business. It prepares its financial statements according to the partnership act

requirement. It prepares profit and loss account as the income statements and also the balance

sheet.

Company: It is a legal body that came into existence by the companies act. Therefore

all the financial statements are prepared as per the act requirements. It prepares profit and loss

account, balance sheet, statements of retained earnings, cash flow statement and fund flow

statements (O' Bryan, 2010). Moreover, parent company that has any subsidiary company

require preparing consolidated financial statements.

AC 4.3 Analysis of financial statements

Sainsbury's financial statements are analysed by ratio analysis technique (Persons,

2011).

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 1377 1277 1211

Operating profit 1009 887 874

Net profit 716 614 598

Net Sales 23949 23303 22294

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 % 5.43 %

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 4.21 % 3.81% 3.92 %

9 | P a g e

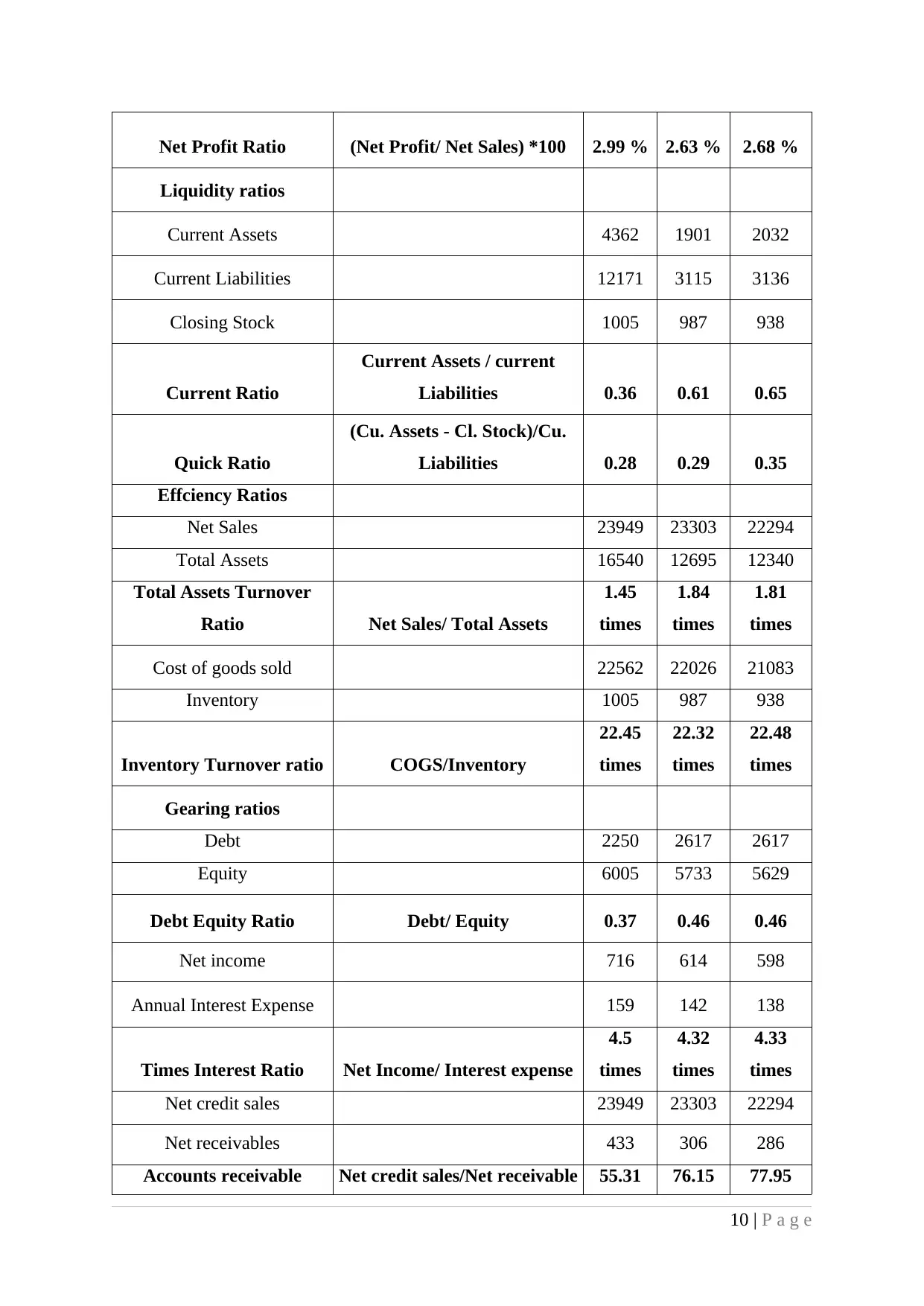

Net Profit Ratio (Net Profit/ Net Sales) *100 2.99 % 2.63 % 2.68 %

Liquidity ratios

Current Assets 4362 1901 2032

Current Liabilities 12171 3115 3136

Closing Stock 1005 987 938

Current Ratio

Current Assets / current

Liabilities 0.36 0.61 0.65

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29 0.35

Effciency Ratios

Net Sales 23949 23303 22294

Total Assets 16540 12695 12340

Total Assets Turnover

Ratio Net Sales/ Total Assets

1.45

times

1.84

times

1.81

times

Cost of goods sold 22562 22026 21083

Inventory 1005 987 938

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

22.48

times

Gearing ratios

Debt 2250 2617 2617

Equity 6005 5733 5629

Debt Equity Ratio Debt/ Equity 0.37 0.46 0.46

Net income 716 614 598

Annual Interest Expense 159 142 138

Times Interest Ratio Net Income/ Interest expense

4.5

times

4.32

times

4.33

times

Net credit sales 23949 23303 22294

Net receivables 433 306 286

Accounts receivable Net credit sales/Net receivable 55.31 76.15 77.95

10 | P a g e

Liquidity ratios

Current Assets 4362 1901 2032

Current Liabilities 12171 3115 3136

Closing Stock 1005 987 938

Current Ratio

Current Assets / current

Liabilities 0.36 0.61 0.65

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29 0.35

Effciency Ratios

Net Sales 23949 23303 22294

Total Assets 16540 12695 12340

Total Assets Turnover

Ratio Net Sales/ Total Assets

1.45

times

1.84

times

1.81

times

Cost of goods sold 22562 22026 21083

Inventory 1005 987 938

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

22.48

times

Gearing ratios

Debt 2250 2617 2617

Equity 6005 5733 5629

Debt Equity Ratio Debt/ Equity 0.37 0.46 0.46

Net income 716 614 598

Annual Interest Expense 159 142 138

Times Interest Ratio Net Income/ Interest expense

4.5

times

4.32

times

4.33

times

Net credit sales 23949 23303 22294

Net receivables 433 306 286

Accounts receivable Net credit sales/Net receivable 55.31 76.15 77.95

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.