Financial Management: Resources and Decision-Making Report, Semester 1

VerifiedAdded on 2019/12/03

|20

|7147

|28

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decision-making within Taste PLC. It begins by exploring various sources of finance, including equity and debt, and evaluates their suitability for the company's expansion plans. The report compares and contrasts right issues of shares and loan notes, ultimately recommending equity financing. It then delves into financial statements, including the profit and loss statement, balance sheet, and cash flow statement, offering financial planning advice to the board of directors and calculating the company's earnings per share. The report also covers investment appraisal methods like net present value and payback period, recommending investment opportunities. Furthermore, it addresses cash flow versus profit, highlighting key trends and the importance of financial planning. The report concludes with an interpretation of financial statements using ratio analysis and a discussion of the differences in financial statements across different business structures. The report provides a detailed examination of Taste PLC's financial performance and strategic financial decisions.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. Introduction............................................................................................................................................3

2. Sources of finance for business..............................................................................................................3

2.1. Type of business..............................................................................................................................3

2.2. Sources of Funds.............................................................................................................................3

2.3. Comparing and contrasting right issue of shares and loan notes....................................................6

2.4. Source which proves to be more suitable for raising finance.........................................................7

2.5. Advising source of finance for working capital to the board of directors ......................................7

3. Financial statements...............................................................................................................................8

3.1 Statement of profit and loss.............................................................................................................8

3.2 Statement of balance sheet...............................................................................................................8

3.3 Statement of cash flow statement.....................................................................................................9

3.4 Advising board of director in relation to the financial planning which proves to be more

beneficial for Taste PLC.........................................................................................................................9

3.5 Calculation of company's current earnings per share.......................................................................9

4. Investment appriasal............................................................................................................................10

4.1 Benefits of net present value method of investment appraisal.......................................................10

4.3 Calculation of the payback period and net present value for European investment opportunity. .10

4.4 Recommending the board of directors by evaluating investment opportunities............................11

4.5 Defining the concept of unit cost ..................................................................................................12

4.6 Factors needs to be considered while setting prices for their output.............................................12

5. Cash flow vs profit...............................................................................................................................13

5.1 Main trends which are in the cash flow of organization................................................................13

5.2 Importance of the financial planning.............................................................................................13

5.3 Reason due to which company faces the liquidity issues or problems..........................................13

5.4 Users of financial statements and their needs...............................................................................14

6. Interpretation of the financial statements.............................................................................................15

6. Ratio analysis of Taste PLC.............................................................................................................15

Interpretation of ratios..........................................................................................................................15

6.2 Overall opinion on the company's current performance................................................................16

7. Differences in financial statements of sole traders, partnership and limited companies.................16

CONCLUSION........................................................................................................................................17

REFERENCES.........................................................................................................................................18

1. Introduction............................................................................................................................................3

2. Sources of finance for business..............................................................................................................3

2.1. Type of business..............................................................................................................................3

2.2. Sources of Funds.............................................................................................................................3

2.3. Comparing and contrasting right issue of shares and loan notes....................................................6

2.4. Source which proves to be more suitable for raising finance.........................................................7

2.5. Advising source of finance for working capital to the board of directors ......................................7

3. Financial statements...............................................................................................................................8

3.1 Statement of profit and loss.............................................................................................................8

3.2 Statement of balance sheet...............................................................................................................8

3.3 Statement of cash flow statement.....................................................................................................9

3.4 Advising board of director in relation to the financial planning which proves to be more

beneficial for Taste PLC.........................................................................................................................9

3.5 Calculation of company's current earnings per share.......................................................................9

4. Investment appriasal............................................................................................................................10

4.1 Benefits of net present value method of investment appraisal.......................................................10

4.3 Calculation of the payback period and net present value for European investment opportunity. .10

4.4 Recommending the board of directors by evaluating investment opportunities............................11

4.5 Defining the concept of unit cost ..................................................................................................12

4.6 Factors needs to be considered while setting prices for their output.............................................12

5. Cash flow vs profit...............................................................................................................................13

5.1 Main trends which are in the cash flow of organization................................................................13

5.2 Importance of the financial planning.............................................................................................13

5.3 Reason due to which company faces the liquidity issues or problems..........................................13

5.4 Users of financial statements and their needs...............................................................................14

6. Interpretation of the financial statements.............................................................................................15

6. Ratio analysis of Taste PLC.............................................................................................................15

Interpretation of ratios..........................................................................................................................15

6.2 Overall opinion on the company's current performance................................................................16

7. Differences in financial statements of sole traders, partnership and limited companies.................16

CONCLUSION........................................................................................................................................17

REFERENCES.........................................................................................................................................18

1. INTRODUCTION

Successful run of a business enterprise depends upon the level of financial stability that

company maintains. However, looking at the present corporate environment in UK, it is important for

companies to manage their financial position in order to maintain competitive edge. Present report

focuses on evaluating and analysing the financial aspects of various PLC's such as Taste and Drink.

Hence, sources of finance required by the firm to carry out its business and its implications to select the

appropriate source for the investment are discussed in the report (Herman, 2011). Thereafter, researcher

suggests three different financial plans for the benefit of shareholders by using WACC. Along with this,

investigator calculates the current earnings per share of Taste PLC so that shareholders can make smart

and effective judgement regarding future contingency.

Thereafter, report focuses on different appraisal methods to evaluate and analyse the reliability

and validity of investment. Concept of unit costs has been considered and the factors that management

should consider while setting the prices of their products and services are focussed here. Further,

research illustrates the reason by which company can be profitable but run into problems with its

liquidity in terms of financial planning. Lastly, by using four financial ratios, researcher will analyse

the profitability and liquidity performance of Taste plc and differences in the financial statements

between sole traders, partnerships and limited companies.

2. SOURCES OF FINANCE FOR BUSINESS

2.1. Type of business

There are various types of business organizations such as sole proprietorship firm, partnership

firm as well as public and private limited organization. As per the case scenario, Taste plc is the public

limited organization whose main objective is to maximize the benefit by satisfying the needs of

customers.

2.2. Sources of Funds

In order to expand the business, it is essential for the firm to raise funds so that effective

expansion can be carried out. By operating in catering business, constantly increasing competition is

enforcing the firm to enhance their business operations for maintaining their competitive edge. There

are several sources of finance available to the top level management of Taste PLC through the help of

which they can easily carry out expansion strategy in an effective and efficient manner. However,

management is intended to invest $1000000 in buildings and non-current assets. Thus, various

available sources are as follows:

Successful run of a business enterprise depends upon the level of financial stability that

company maintains. However, looking at the present corporate environment in UK, it is important for

companies to manage their financial position in order to maintain competitive edge. Present report

focuses on evaluating and analysing the financial aspects of various PLC's such as Taste and Drink.

Hence, sources of finance required by the firm to carry out its business and its implications to select the

appropriate source for the investment are discussed in the report (Herman, 2011). Thereafter, researcher

suggests three different financial plans for the benefit of shareholders by using WACC. Along with this,

investigator calculates the current earnings per share of Taste PLC so that shareholders can make smart

and effective judgement regarding future contingency.

Thereafter, report focuses on different appraisal methods to evaluate and analyse the reliability

and validity of investment. Concept of unit costs has been considered and the factors that management

should consider while setting the prices of their products and services are focussed here. Further,

research illustrates the reason by which company can be profitable but run into problems with its

liquidity in terms of financial planning. Lastly, by using four financial ratios, researcher will analyse

the profitability and liquidity performance of Taste plc and differences in the financial statements

between sole traders, partnerships and limited companies.

2. SOURCES OF FINANCE FOR BUSINESS

2.1. Type of business

There are various types of business organizations such as sole proprietorship firm, partnership

firm as well as public and private limited organization. As per the case scenario, Taste plc is the public

limited organization whose main objective is to maximize the benefit by satisfying the needs of

customers.

2.2. Sources of Funds

In order to expand the business, it is essential for the firm to raise funds so that effective

expansion can be carried out. By operating in catering business, constantly increasing competition is

enforcing the firm to enhance their business operations for maintaining their competitive edge. There

are several sources of finance available to the top level management of Taste PLC through the help of

which they can easily carry out expansion strategy in an effective and efficient manner. However,

management is intended to invest $1000000 in buildings and non-current assets. Thus, various

available sources are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

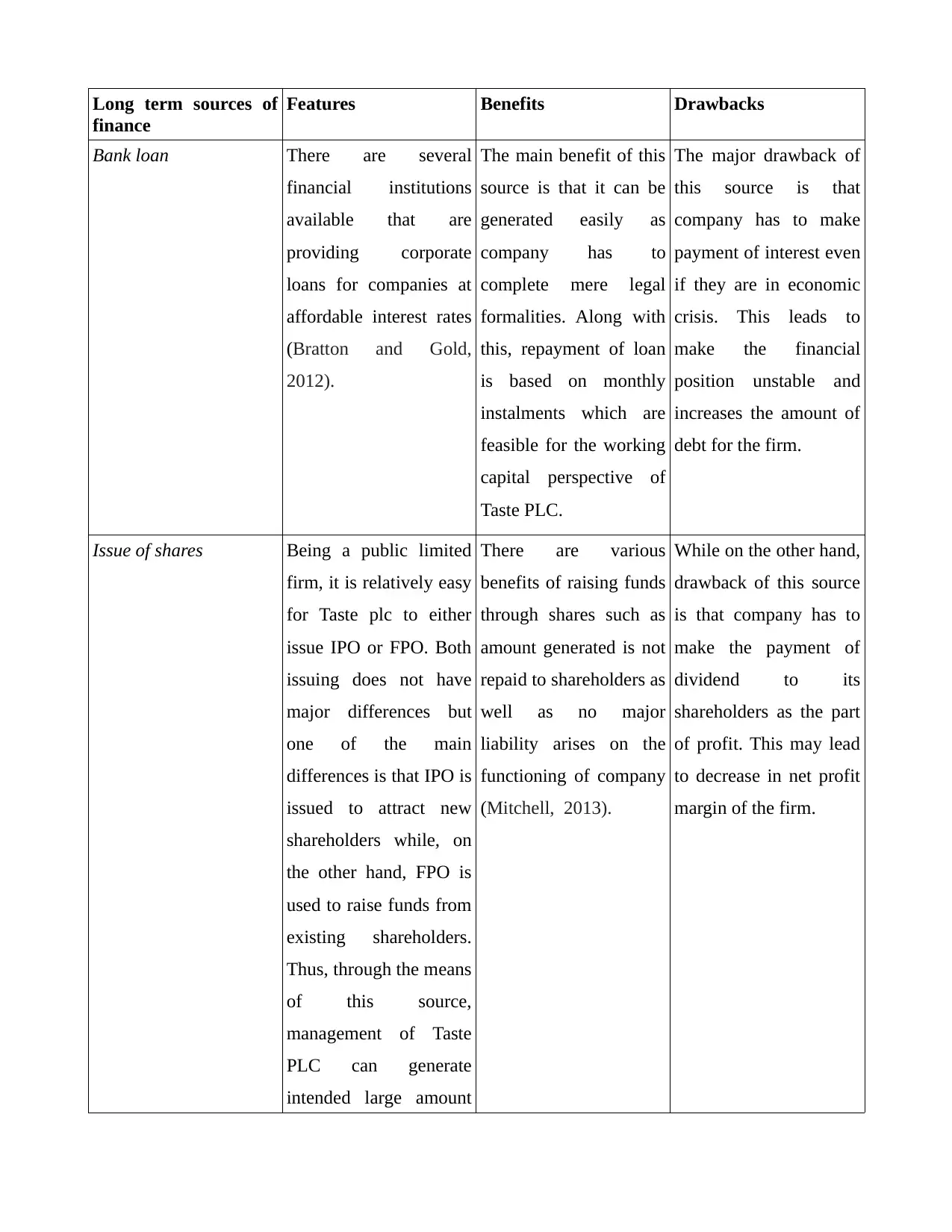

Long term sources of

finance

Features Benefits Drawbacks

Bank loan There are several

financial institutions

available that are

providing corporate

loans for companies at

affordable interest rates

(Bratton and Gold,

2012).

The main benefit of this

source is that it can be

generated easily as

company has to

complete mere legal

formalities. Along with

this, repayment of loan

is based on monthly

instalments which are

feasible for the working

capital perspective of

Taste PLC.

The major drawback of

this source is that

company has to make

payment of interest even

if they are in economic

crisis. This leads to

make the financial

position unstable and

increases the amount of

debt for the firm.

Issue of shares Being a public limited

firm, it is relatively easy

for Taste plc to either

issue IPO or FPO. Both

issuing does not have

major differences but

one of the main

differences is that IPO is

issued to attract new

shareholders while, on

the other hand, FPO is

used to raise funds from

existing shareholders.

Thus, through the means

of this source,

management of Taste

PLC can generate

intended large amount

There are various

benefits of raising funds

through shares such as

amount generated is not

repaid to shareholders as

well as no major

liability arises on the

functioning of company

(Mitchell, 2013).

While on the other hand,

drawback of this source

is that company has to

make the payment of

dividend to its

shareholders as the part

of profit. This may lead

to decrease in net profit

margin of the firm.

finance

Features Benefits Drawbacks

Bank loan There are several

financial institutions

available that are

providing corporate

loans for companies at

affordable interest rates

(Bratton and Gold,

2012).

The main benefit of this

source is that it can be

generated easily as

company has to

complete mere legal

formalities. Along with

this, repayment of loan

is based on monthly

instalments which are

feasible for the working

capital perspective of

Taste PLC.

The major drawback of

this source is that

company has to make

payment of interest even

if they are in economic

crisis. This leads to

make the financial

position unstable and

increases the amount of

debt for the firm.

Issue of shares Being a public limited

firm, it is relatively easy

for Taste plc to either

issue IPO or FPO. Both

issuing does not have

major differences but

one of the main

differences is that IPO is

issued to attract new

shareholders while, on

the other hand, FPO is

used to raise funds from

existing shareholders.

Thus, through the means

of this source,

management of Taste

PLC can generate

intended large amount

There are various

benefits of raising funds

through shares such as

amount generated is not

repaid to shareholders as

well as no major

liability arises on the

functioning of company

(Mitchell, 2013).

While on the other hand,

drawback of this source

is that company has to

make the payment of

dividend to its

shareholders as the part

of profit. This may lead

to decrease in net profit

margin of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that will help in the

expansion strategy.

Long term leasing Leasing is another

important source of

finance. It provides

opportunity to the

company to make use of

fixed asset for the

predetermined period

without making huge

investment on it with

the intention for

purchase.

The main benefit of

leasing is that company

does not have need to

make large investment

of the fixed assets.

Through this, company

can use this money in

the other productive

activities.

Leasing organization

charge periodical

amount for the use of

the assets which impose

high financial cost in

front of the company.

Short term sources of

finance

Features Benefits Drawbacks

Bank overdraft It is also the main short

term source of finance

which can provide

financial assistance to

Taste PLC for the

limited period of time.

In this, company can use

money in excess which

is available in their bank

account up to a certain

limit.

One of the main benefit

of bank overdraft is

interest is charged only

on the fund which is

utilized by an

organization. Besides

this, if credit rating of

customer is good then

bank is ready to give

overdraft facility to their

customers.

In bank overdraft,

organization has to pay

high rate of interest as

compared to other credit

sources which impose

financial cost in front of

the company.

Letter of credit Financial institution

issues letter of the credit

to the seller of goods

and services. In this,

One of the main benefits

is that on the basis of

the financial security

financial institution are

For this facility,

financial institution

charges high interest

rate which creates

expansion strategy.

Long term leasing Leasing is another

important source of

finance. It provides

opportunity to the

company to make use of

fixed asset for the

predetermined period

without making huge

investment on it with

the intention for

purchase.

The main benefit of

leasing is that company

does not have need to

make large investment

of the fixed assets.

Through this, company

can use this money in

the other productive

activities.

Leasing organization

charge periodical

amount for the use of

the assets which impose

high financial cost in

front of the company.

Short term sources of

finance

Features Benefits Drawbacks

Bank overdraft It is also the main short

term source of finance

which can provide

financial assistance to

Taste PLC for the

limited period of time.

In this, company can use

money in excess which

is available in their bank

account up to a certain

limit.

One of the main benefit

of bank overdraft is

interest is charged only

on the fund which is

utilized by an

organization. Besides

this, if credit rating of

customer is good then

bank is ready to give

overdraft facility to their

customers.

In bank overdraft,

organization has to pay

high rate of interest as

compared to other credit

sources which impose

financial cost in front of

the company.

Letter of credit Financial institution

issues letter of the credit

to the seller of goods

and services. In this,

One of the main benefits

is that on the basis of

the financial security

financial institution are

For this facility,

financial institution

charges high interest

rate which creates

financial institution

takes responsibility to

give payment on the

behalf of the company.

ready to give credit to

the organization.

financial burden in front

of the company.

Leasing In leasing, Taste plc has

the opportunity to take

benefit from the assets

without making huge

investment on it.

Tax deduction is one of

the main benefits which

compel organization to

make use of the asset

without purchasing it.

Taste plc requires

paying periodical rent to

the real owner of assets

which imposing high

financial cost in front of

the organization.

2.3. Comparing and contrasting right issue of shares and loan notes Right issue: It can be defined as a form of dividend in which organization provides right to its

existing shareholders to purchase the shares of company. In this, firm initially offers the shares

to its existing investors instead of others. Right issues are usually undertaken by PLC because

they prefer to raise finance through issuing of equity shares rather than issuing of debt. Taste is

also the PLC which prefers to raise fund from the equity sources. Whereas, loan notes are the

financial instruments in which borrower provides a written form to the lender which contains

interest rate that borrower has to pay (Mitchell, 2013). It also consists of the time in which

Taste PLC needs to repay the whole amount of debt. Loan stock: Company also issues the loan note which can be easily convertible into equity

shares after a predetermined time period. Raising fund from right issues proves to be more

beneficial for Taste PLC as compared to debt issues. When company fulfils its financial needs

through its existing shareholders then it does not have need to incur extra expenses to attract

them. Besides this, financial position of Taste PLC is sound so, organization is able to attract its

existing shareholders. In contrary to this, corporation can meet its financial requirements

through debt issues. For this, company has to pay interest to the holders of loan notes after a

regular interval. As compared to equity sources, raising finance through loan notes imposes

high cost in front of the organization.

Implications of the right issue of shares: There are several implications of right issue of shares

upon the organization, invests and financial statement of an organization. In right issue

company issue shares to their existing shareholders. Thus, corporation does not have need to

takes responsibility to

give payment on the

behalf of the company.

ready to give credit to

the organization.

financial burden in front

of the company.

Leasing In leasing, Taste plc has

the opportunity to take

benefit from the assets

without making huge

investment on it.

Tax deduction is one of

the main benefits which

compel organization to

make use of the asset

without purchasing it.

Taste plc requires

paying periodical rent to

the real owner of assets

which imposing high

financial cost in front of

the organization.

2.3. Comparing and contrasting right issue of shares and loan notes Right issue: It can be defined as a form of dividend in which organization provides right to its

existing shareholders to purchase the shares of company. In this, firm initially offers the shares

to its existing investors instead of others. Right issues are usually undertaken by PLC because

they prefer to raise finance through issuing of equity shares rather than issuing of debt. Taste is

also the PLC which prefers to raise fund from the equity sources. Whereas, loan notes are the

financial instruments in which borrower provides a written form to the lender which contains

interest rate that borrower has to pay (Mitchell, 2013). It also consists of the time in which

Taste PLC needs to repay the whole amount of debt. Loan stock: Company also issues the loan note which can be easily convertible into equity

shares after a predetermined time period. Raising fund from right issues proves to be more

beneficial for Taste PLC as compared to debt issues. When company fulfils its financial needs

through its existing shareholders then it does not have need to incur extra expenses to attract

them. Besides this, financial position of Taste PLC is sound so, organization is able to attract its

existing shareholders. In contrary to this, corporation can meet its financial requirements

through debt issues. For this, company has to pay interest to the holders of loan notes after a

regular interval. As compared to equity sources, raising finance through loan notes imposes

high cost in front of the organization.

Implications of the right issue of shares: There are several implications of right issue of shares

upon the organization, invests and financial statement of an organization. In right issue

company issue shares to their existing shareholders. Thus, corporation does not have need to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

make expenses of prospects and other floating cost. Besides this, when company issue right

share then it place positive impact upon the existing and potential shareholders. Along with it,

voting rights of the investors are also increases when company offers right share to the

investors. In addition to this, amount of share capital is increases in balance sheet when

company issue right shares. Thus, liability side of the organization is also increases which

imposes financial obligation in front of the company.

2.4. Source which proves to be more suitable for raising finance

On the basis of above sources, Taste PLC needs to meet its financial requirements through an

issuance of equity shares. It proves to be more beneficial for meeting the needs such as building and

non-current assets. It does not create financial burden in front of company as compared to debt

instrument. By raising finance through equity sources, Taste PLC is able to take use of money which

ensures smooth functioning of business activities and functions. In this, company requires to pay

dividend to its shareholders whenever it generates profit (Mathis and Jackson, 2011). Through this,

corporation is able to build and maintain faith in the minds of investors. Thus, it proves to be more

suitable source for an organization which helps company in achieving the organizational aim and

objectives.

Further, Taste also approaches bank for the loan to meet their financial needs and requirements.

In this, bank provides credit on the basis of the financial security. The building in which organization

wants to invest is in the under of the bank until the whole amount of loan is not repaid by the company

to the bank. In addition to this, where as if Taste issue loan notes to meet their financial requirement

then it saves time and cost of the organization. Moreover, it is the debt source of finance which is

offered to existing stakeholders of an organization. Thus, company does not have need to incur extra

expenses in order to attract the investors which proves to be more beneficial for an organization.

2.5. Advising source of finance for working capital to the board of directors

There are various sources of finance for working capital that is available to Taste PLC and

which it can use to meet its financial needs and requirements. Sources of working capital include

retained earnings, bank loan as well as loan from the other financial institutions. It is advised to the

board of director of Taste PLC that they should undertake bank loan and retained earnings to fulfil the

need of working capital. It proves to be more beneficial for an organization in terms of high level of

productivity and profitability.

It enables Taste PLC to carry out its business operations and activities more effectively and

share then it place positive impact upon the existing and potential shareholders. Along with it,

voting rights of the investors are also increases when company offers right share to the

investors. In addition to this, amount of share capital is increases in balance sheet when

company issue right shares. Thus, liability side of the organization is also increases which

imposes financial obligation in front of the company.

2.4. Source which proves to be more suitable for raising finance

On the basis of above sources, Taste PLC needs to meet its financial requirements through an

issuance of equity shares. It proves to be more beneficial for meeting the needs such as building and

non-current assets. It does not create financial burden in front of company as compared to debt

instrument. By raising finance through equity sources, Taste PLC is able to take use of money which

ensures smooth functioning of business activities and functions. In this, company requires to pay

dividend to its shareholders whenever it generates profit (Mathis and Jackson, 2011). Through this,

corporation is able to build and maintain faith in the minds of investors. Thus, it proves to be more

suitable source for an organization which helps company in achieving the organizational aim and

objectives.

Further, Taste also approaches bank for the loan to meet their financial needs and requirements.

In this, bank provides credit on the basis of the financial security. The building in which organization

wants to invest is in the under of the bank until the whole amount of loan is not repaid by the company

to the bank. In addition to this, where as if Taste issue loan notes to meet their financial requirement

then it saves time and cost of the organization. Moreover, it is the debt source of finance which is

offered to existing stakeholders of an organization. Thus, company does not have need to incur extra

expenses in order to attract the investors which proves to be more beneficial for an organization.

2.5. Advising source of finance for working capital to the board of directors

There are various sources of finance for working capital that is available to Taste PLC and

which it can use to meet its financial needs and requirements. Sources of working capital include

retained earnings, bank loan as well as loan from the other financial institutions. It is advised to the

board of director of Taste PLC that they should undertake bank loan and retained earnings to fulfil the

need of working capital. It proves to be more beneficial for an organization in terms of high level of

productivity and profitability.

It enables Taste PLC to carry out its business operations and activities more effectively and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

efficiently. Retained earnings are the best source which enables the organization to fulfil its financial

needs. Nevertheless, if firm retains high level of profit then it is unable to pay dividend to the

shareholders which make negative impact upon them. On the other hand, if company undertakes only

bank loan then it has to pay high interest amount which imposes difficulty in front of the firm ( Brealey,

2012). Thus, Taste PLC needs to use both the sources of finance to meet the financial requirement.

Sources of finance include trade credit, factoring, lines of credit and bank loan are the major sources of

working capital.

3. FINANCIAL STATEMENTS

3.1 Statement of profit and loss

It is one of the main part of financial statement which provides deeper insight about the profit

generated by the firm during the accounting year. Besides this, it also provides information about the

expenditure which are incurred by the business organization. One of the main purpose behind the

preparation of profit and loss a/c is make analysis of the profit upon which dividend, investment and

other business decisions are highly dependent. In addition to this, business entity can also make review

of their expenditure on which company needs to exert control.

Debit side Credit side

Particulars Amount Particulars Amount

To salaries and wages xxx By gross profit xxx

To electricity expenses xxx By interest receive xxx

To office expenses xxx By dividend receive xxx

3.2 Statement of balance sheet

This statement summarizes company's assets, liabilities and shareholders equity which is highly

associated with the particular time period. Every organization prepares balance sheet at the end of the

financial year to evaluate its financial strength and weaknesses. Through this, manager of the firm is

able to employ competent strategies which helps them in converting their weaknesses into strengths.

Liabilities Amount Assets Amount

Shareholders equity xxx Fixed assets:

Furnitures &

xxx

needs. Nevertheless, if firm retains high level of profit then it is unable to pay dividend to the

shareholders which make negative impact upon them. On the other hand, if company undertakes only

bank loan then it has to pay high interest amount which imposes difficulty in front of the firm ( Brealey,

2012). Thus, Taste PLC needs to use both the sources of finance to meet the financial requirement.

Sources of finance include trade credit, factoring, lines of credit and bank loan are the major sources of

working capital.

3. FINANCIAL STATEMENTS

3.1 Statement of profit and loss

It is one of the main part of financial statement which provides deeper insight about the profit

generated by the firm during the accounting year. Besides this, it also provides information about the

expenditure which are incurred by the business organization. One of the main purpose behind the

preparation of profit and loss a/c is make analysis of the profit upon which dividend, investment and

other business decisions are highly dependent. In addition to this, business entity can also make review

of their expenditure on which company needs to exert control.

Debit side Credit side

Particulars Amount Particulars Amount

To salaries and wages xxx By gross profit xxx

To electricity expenses xxx By interest receive xxx

To office expenses xxx By dividend receive xxx

3.2 Statement of balance sheet

This statement summarizes company's assets, liabilities and shareholders equity which is highly

associated with the particular time period. Every organization prepares balance sheet at the end of the

financial year to evaluate its financial strength and weaknesses. Through this, manager of the firm is

able to employ competent strategies which helps them in converting their weaknesses into strengths.

Liabilities Amount Assets Amount

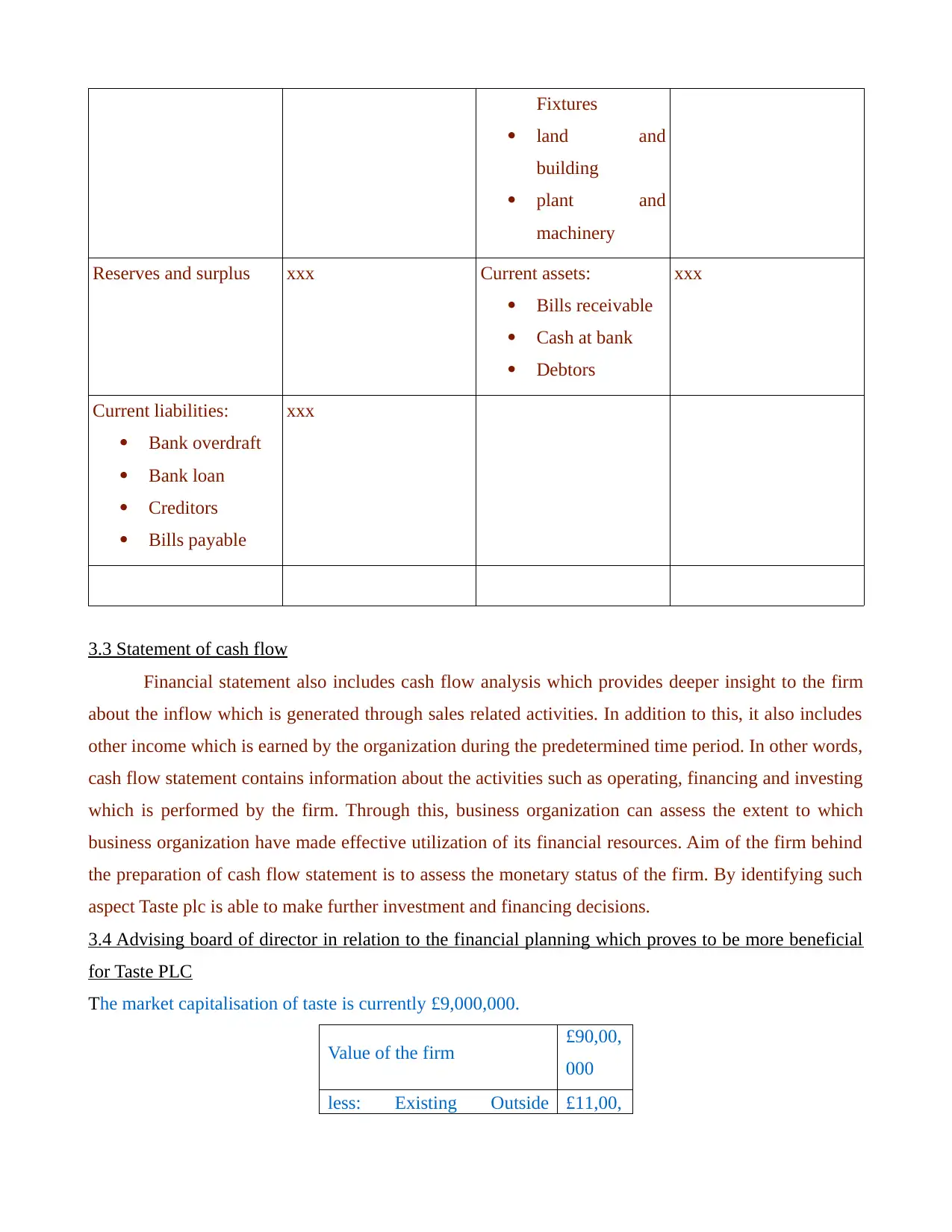

Shareholders equity xxx Fixed assets:

Furnitures &

xxx

Fixtures

land and

building

plant and

machinery

Reserves and surplus xxx Current assets:

Bills receivable

Cash at bank

Debtors

xxx

Current liabilities:

Bank overdraft

Bank loan

Creditors

Bills payable

xxx

3.3 Statement of cash flow

Financial statement also includes cash flow analysis which provides deeper insight to the firm

about the inflow which is generated through sales related activities. In addition to this, it also includes

other income which is earned by the organization during the predetermined time period. In other words,

cash flow statement contains information about the activities such as operating, financing and investing

which is performed by the firm. Through this, business organization can assess the extent to which

business organization have made effective utilization of its financial resources. Aim of the firm behind

the preparation of cash flow statement is to assess the monetary status of the firm. By identifying such

aspect Taste plc is able to make further investment and financing decisions.

3.4 Advising board of director in relation to the financial planning which proves to be more beneficial

for Taste PLC

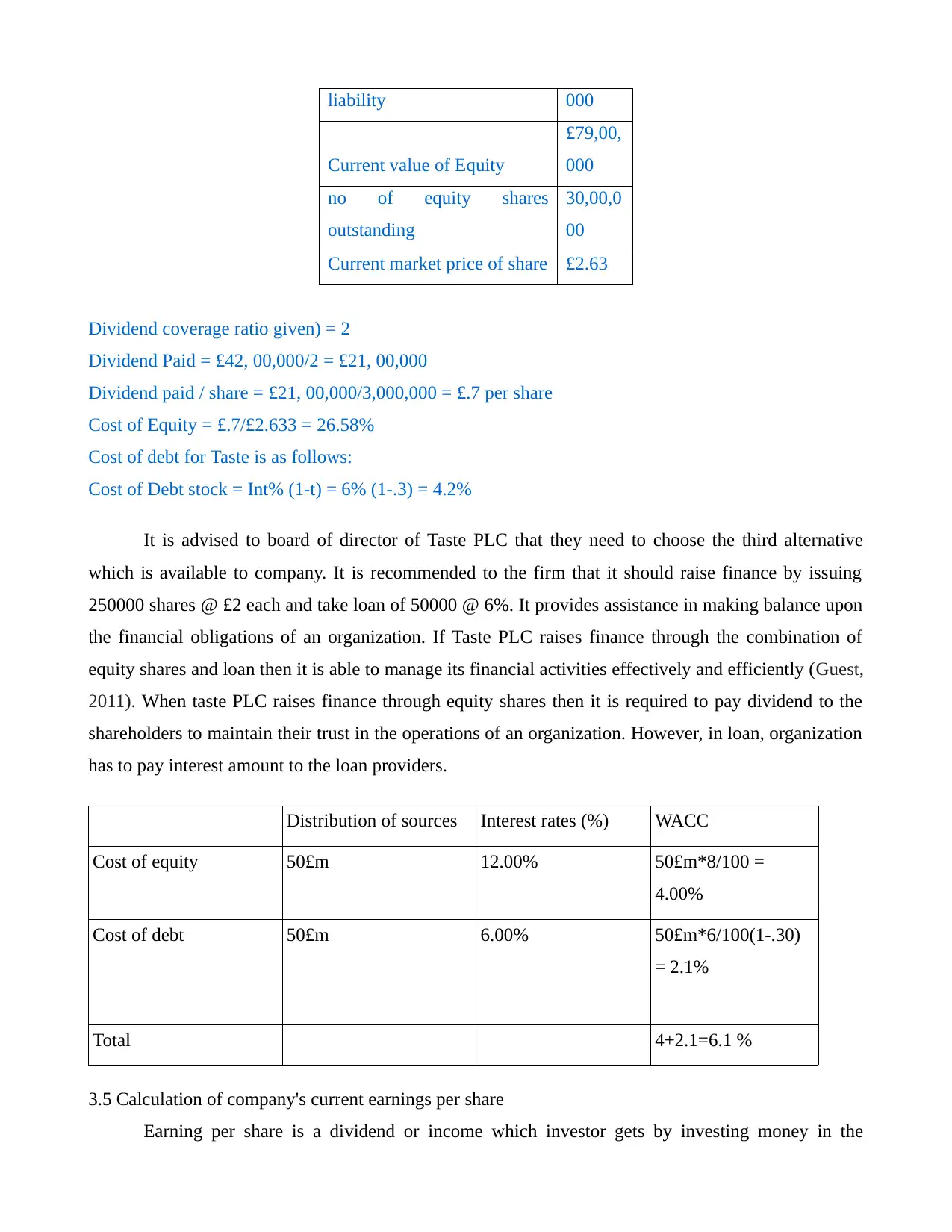

The market capitalisation of taste is currently £9,000,000.

Value of the firm £90,00,

000

less: Existing Outside £11,00,

land and

building

plant and

machinery

Reserves and surplus xxx Current assets:

Bills receivable

Cash at bank

Debtors

xxx

Current liabilities:

Bank overdraft

Bank loan

Creditors

Bills payable

xxx

3.3 Statement of cash flow

Financial statement also includes cash flow analysis which provides deeper insight to the firm

about the inflow which is generated through sales related activities. In addition to this, it also includes

other income which is earned by the organization during the predetermined time period. In other words,

cash flow statement contains information about the activities such as operating, financing and investing

which is performed by the firm. Through this, business organization can assess the extent to which

business organization have made effective utilization of its financial resources. Aim of the firm behind

the preparation of cash flow statement is to assess the monetary status of the firm. By identifying such

aspect Taste plc is able to make further investment and financing decisions.

3.4 Advising board of director in relation to the financial planning which proves to be more beneficial

for Taste PLC

The market capitalisation of taste is currently £9,000,000.

Value of the firm £90,00,

000

less: Existing Outside £11,00,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liability 000

Current value of Equity

£79,00,

000

no of equity shares

outstanding

30,00,0

00

Current market price of share £2.63

Dividend coverage ratio given) = 2

Dividend Paid = £42, 00,000/2 = £21, 00,000

Dividend paid / share = £21, 00,000/3,000,000 = £.7 per share

Cost of Equity = £.7/£2.633 = 26.58%

Cost of debt for Taste is as follows:

Cost of Debt stock = Int% (1-t) = 6% (1-.3) = 4.2%

It is advised to board of director of Taste PLC that they need to choose the third alternative

which is available to company. It is recommended to the firm that it should raise finance by issuing

250000 shares @ £2 each and take loan of 50000 @ 6%. It provides assistance in making balance upon

the financial obligations of an organization. If Taste PLC raises finance through the combination of

equity shares and loan then it is able to manage its financial activities effectively and efficiently (Guest,

2011). When taste PLC raises finance through equity shares then it is required to pay dividend to the

shareholders to maintain their trust in the operations of an organization. However, in loan, organization

has to pay interest amount to the loan providers.

Distribution of sources Interest rates (%) WACC

Cost of equity 50£m 12.00% 50£m*8/100 =

4.00%

Cost of debt 50£m 6.00% 50£m*6/100(1-.30)

= 2.1%

Total 4+2.1=6.1 %

3.5 Calculation of company's current earnings per share

Earning per share is a dividend or income which investor gets by investing money in the

Current value of Equity

£79,00,

000

no of equity shares

outstanding

30,00,0

00

Current market price of share £2.63

Dividend coverage ratio given) = 2

Dividend Paid = £42, 00,000/2 = £21, 00,000

Dividend paid / share = £21, 00,000/3,000,000 = £.7 per share

Cost of Equity = £.7/£2.633 = 26.58%

Cost of debt for Taste is as follows:

Cost of Debt stock = Int% (1-t) = 6% (1-.3) = 4.2%

It is advised to board of director of Taste PLC that they need to choose the third alternative

which is available to company. It is recommended to the firm that it should raise finance by issuing

250000 shares @ £2 each and take loan of 50000 @ 6%. It provides assistance in making balance upon

the financial obligations of an organization. If Taste PLC raises finance through the combination of

equity shares and loan then it is able to manage its financial activities effectively and efficiently (Guest,

2011). When taste PLC raises finance through equity shares then it is required to pay dividend to the

shareholders to maintain their trust in the operations of an organization. However, in loan, organization

has to pay interest amount to the loan providers.

Distribution of sources Interest rates (%) WACC

Cost of equity 50£m 12.00% 50£m*8/100 =

4.00%

Cost of debt 50£m 6.00% 50£m*6/100(1-.30)

= 2.1%

Total 4+2.1=6.1 %

3.5 Calculation of company's current earnings per share

Earning per share is a dividend or income which investor gets by investing money in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business activities of Taste PLC. Shareholders or investors are highly concerned with the income which

they generate from making investment in Taste PLC. Investment decisions of shareholders are highly

dependent upon the growth and development aspects of corporation. By dividing profit after tax to the

number of shares, investor can assess the return which they get from an organization.

Profit before interest and tax = £720000

Number of shares = 3000

Earnings per share = Profit before interest and tax/number of shares

EPS = 720000/3000

EPS = £240 each

4. INVESTMENT APPRIASAL

4.1 Benefits of net present value method of investment appraisal

NPV can be defined as an investment appraisal technique through which organization is able to

assess the inflow and outflow of cash through the discounting factors. This method considers time

value of money concept which provides deeper insight to Taste PLC about the investment which proves

to be more profitable for the firm. Besides this, it also facilitates the comparison between two potential

investments. Through this, organization is able to select the investment which gives higher return to an

organization (Guerrero, Maas and Hogland, 2013). It is one of the important investment appraisal

methods which help in assessing the return which organization gets over the period of time. If it is

positive then, firm should select the investment; otherwise, it should reject it.

4.3 Calculation of the payback period and net present value for European investment opportunity

Investment appraisal techniques can be defined as a tool through which organization is able to

assess the suitability of investment (Maditinos and et.al, 2011). It provides assistance to an organization

in making appropriate investment decisions which makes contribution in the achievement of

organizational goals and objectives.

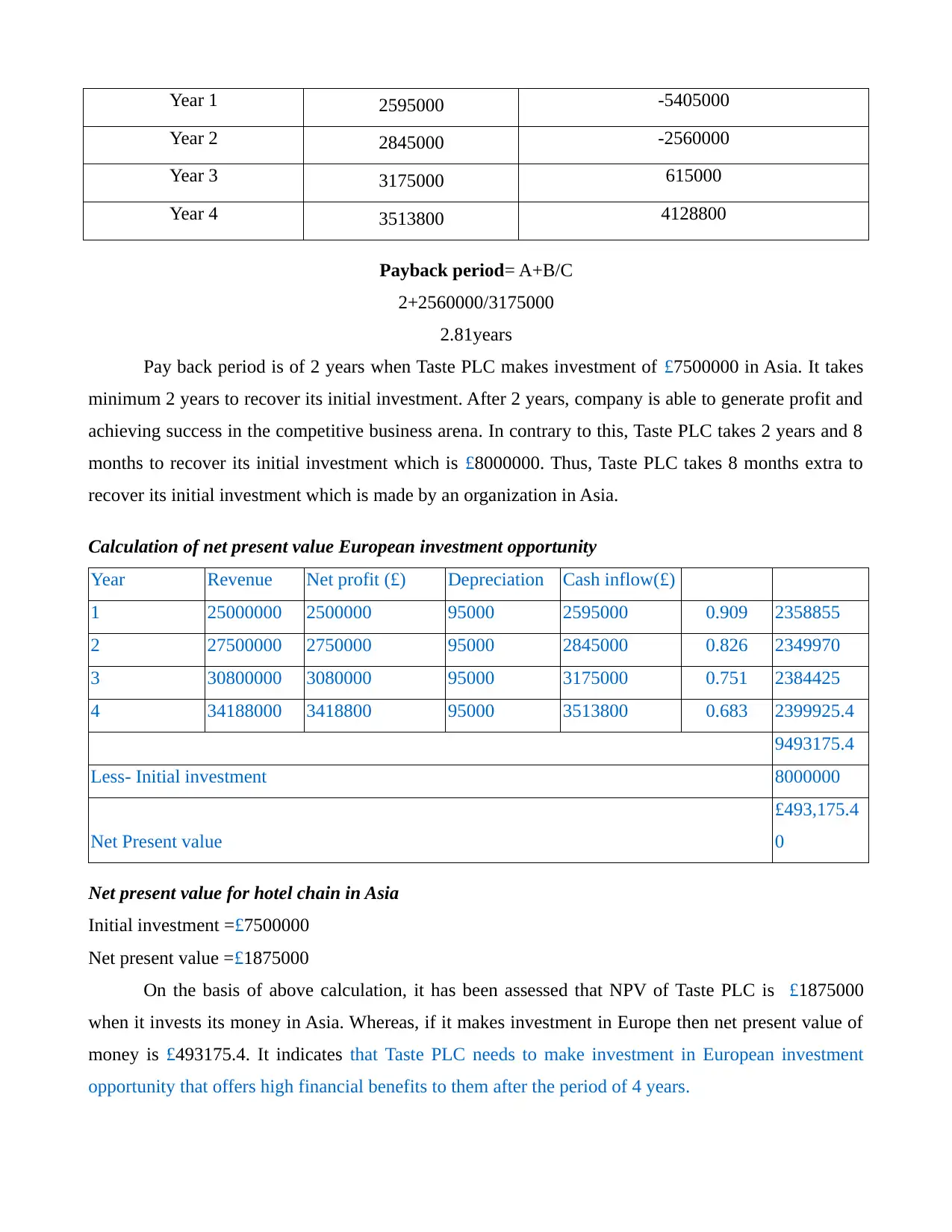

Given:

Payback period for hotel chain in Asia

Initial investment = £7500000

Payback period = 2 years

Calculation of payback period for European investment opportunity

Project A Cumulative frequency

Initial Investment £-8000000

they generate from making investment in Taste PLC. Investment decisions of shareholders are highly

dependent upon the growth and development aspects of corporation. By dividing profit after tax to the

number of shares, investor can assess the return which they get from an organization.

Profit before interest and tax = £720000

Number of shares = 3000

Earnings per share = Profit before interest and tax/number of shares

EPS = 720000/3000

EPS = £240 each

4. INVESTMENT APPRIASAL

4.1 Benefits of net present value method of investment appraisal

NPV can be defined as an investment appraisal technique through which organization is able to

assess the inflow and outflow of cash through the discounting factors. This method considers time

value of money concept which provides deeper insight to Taste PLC about the investment which proves

to be more profitable for the firm. Besides this, it also facilitates the comparison between two potential

investments. Through this, organization is able to select the investment which gives higher return to an

organization (Guerrero, Maas and Hogland, 2013). It is one of the important investment appraisal

methods which help in assessing the return which organization gets over the period of time. If it is

positive then, firm should select the investment; otherwise, it should reject it.

4.3 Calculation of the payback period and net present value for European investment opportunity

Investment appraisal techniques can be defined as a tool through which organization is able to

assess the suitability of investment (Maditinos and et.al, 2011). It provides assistance to an organization

in making appropriate investment decisions which makes contribution in the achievement of

organizational goals and objectives.

Given:

Payback period for hotel chain in Asia

Initial investment = £7500000

Payback period = 2 years

Calculation of payback period for European investment opportunity

Project A Cumulative frequency

Initial Investment £-8000000

Year 1 2595000 -5405000

Year 2 2845000 -2560000

Year 3 3175000 615000

Year 4 3513800 4128800

Payback period= A+B/C

2+2560000/3175000

2.81years

Pay back period is of 2 years when Taste PLC makes investment of £7500000 in Asia. It takes

minimum 2 years to recover its initial investment. After 2 years, company is able to generate profit and

achieving success in the competitive business arena. In contrary to this, Taste PLC takes 2 years and 8

months to recover its initial investment which is £8000000. Thus, Taste PLC takes 8 months extra to

recover its initial investment which is made by an organization in Asia.

Calculation of net present value European investment opportunity

Year Revenue Net profit (£) Depreciation Cash inflow(£)

1 25000000 2500000 95000 2595000 0.909 2358855

2 27500000 2750000 95000 2845000 0.826 2349970

3 30800000 3080000 95000 3175000 0.751 2384425

4 34188000 3418800 95000 3513800 0.683 2399925.4

9493175.4

Less- Initial investment 8000000

Net Present value

£493,175.4

0

Net present value for hotel chain in Asia

Initial investment =£7500000

Net present value =£1875000

On the basis of above calculation, it has been assessed that NPV of Taste PLC is £1875000

when it invests its money in Asia. Whereas, if it makes investment in Europe then net present value of

money is £493175.4. It indicates that Taste PLC needs to make investment in European investment

opportunity that offers high financial benefits to them after the period of 4 years.

Year 2 2845000 -2560000

Year 3 3175000 615000

Year 4 3513800 4128800

Payback period= A+B/C

2+2560000/3175000

2.81years

Pay back period is of 2 years when Taste PLC makes investment of £7500000 in Asia. It takes

minimum 2 years to recover its initial investment. After 2 years, company is able to generate profit and

achieving success in the competitive business arena. In contrary to this, Taste PLC takes 2 years and 8

months to recover its initial investment which is £8000000. Thus, Taste PLC takes 8 months extra to

recover its initial investment which is made by an organization in Asia.

Calculation of net present value European investment opportunity

Year Revenue Net profit (£) Depreciation Cash inflow(£)

1 25000000 2500000 95000 2595000 0.909 2358855

2 27500000 2750000 95000 2845000 0.826 2349970

3 30800000 3080000 95000 3175000 0.751 2384425

4 34188000 3418800 95000 3513800 0.683 2399925.4

9493175.4

Less- Initial investment 8000000

Net Present value

£493,175.4

0

Net present value for hotel chain in Asia

Initial investment =£7500000

Net present value =£1875000

On the basis of above calculation, it has been assessed that NPV of Taste PLC is £1875000

when it invests its money in Asia. Whereas, if it makes investment in Europe then net present value of

money is £493175.4. It indicates that Taste PLC needs to make investment in European investment

opportunity that offers high financial benefits to them after the period of 4 years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.