Audit Planning and Financial Analysis: Morris Ltd Case Study

VerifiedAdded on 2022/08/24

|16

|1770

|14

Case Study

AI Summary

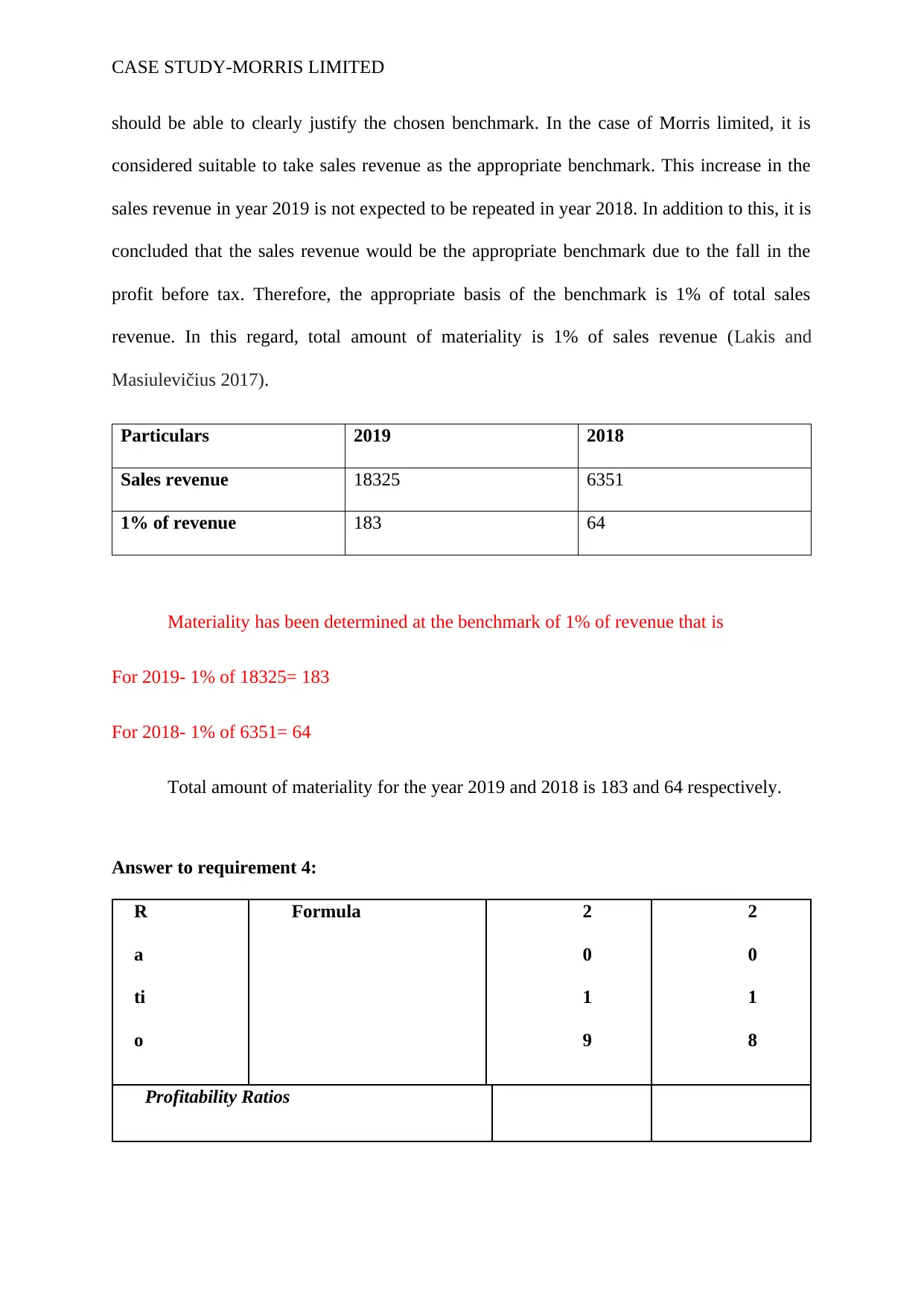

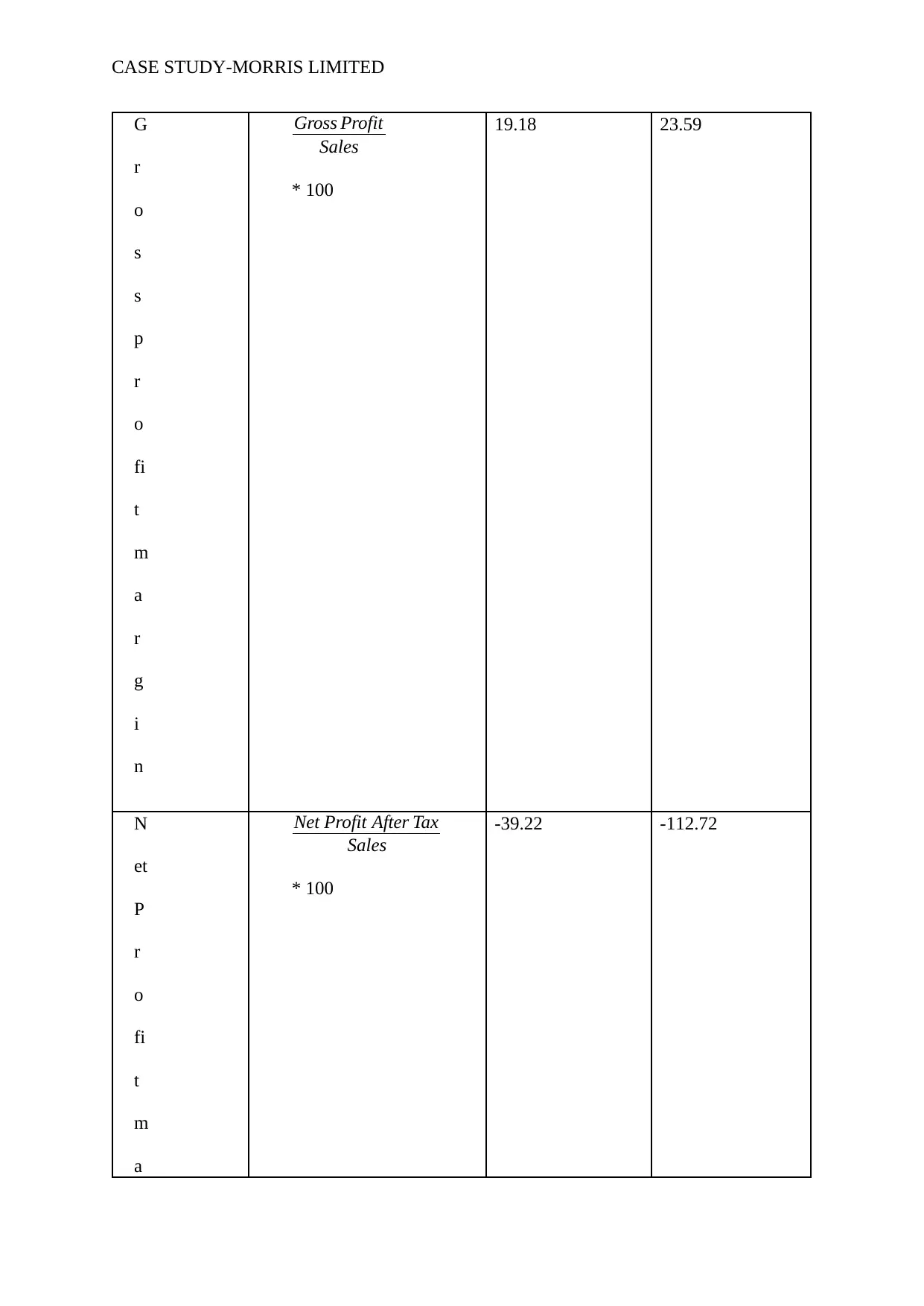

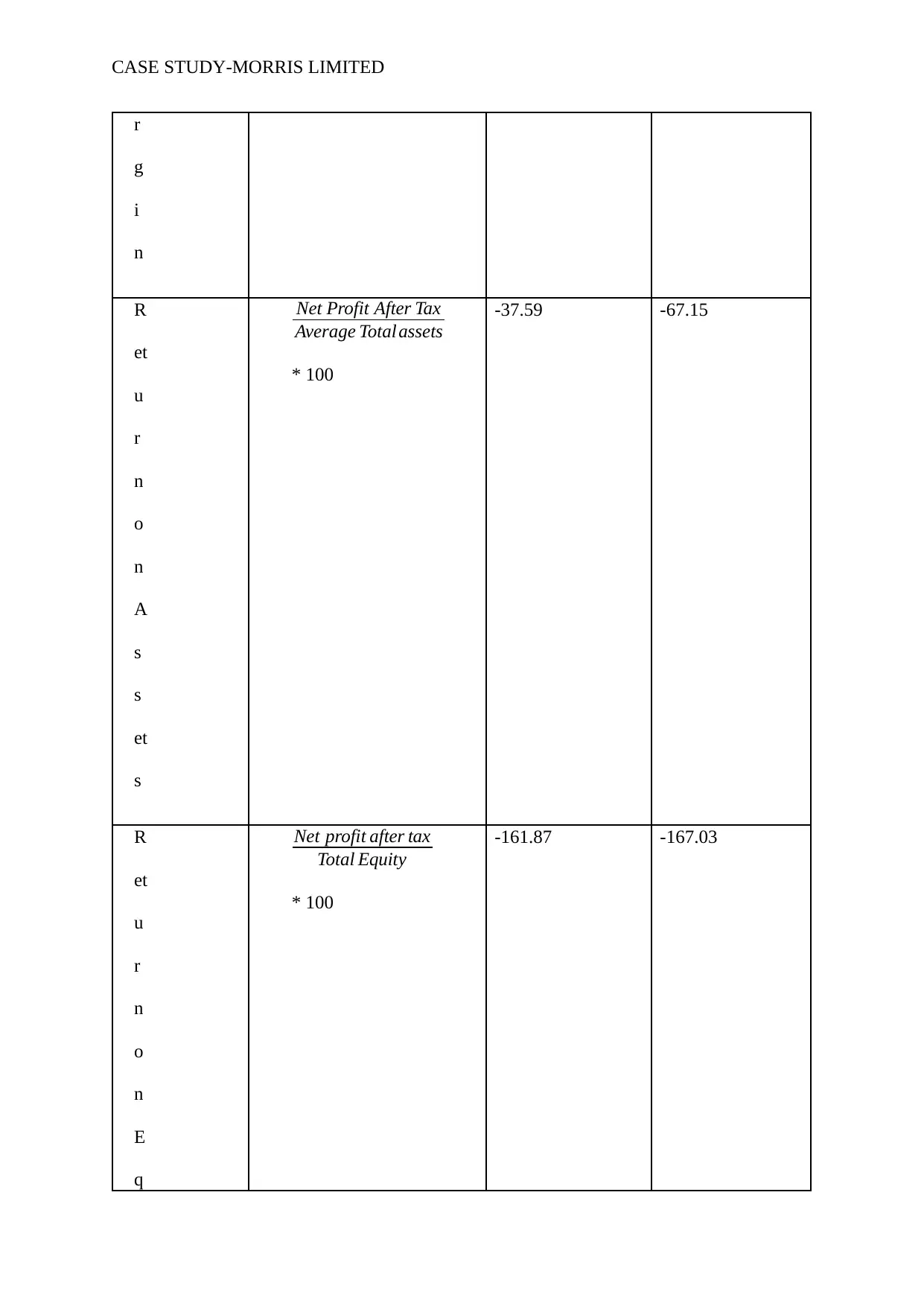

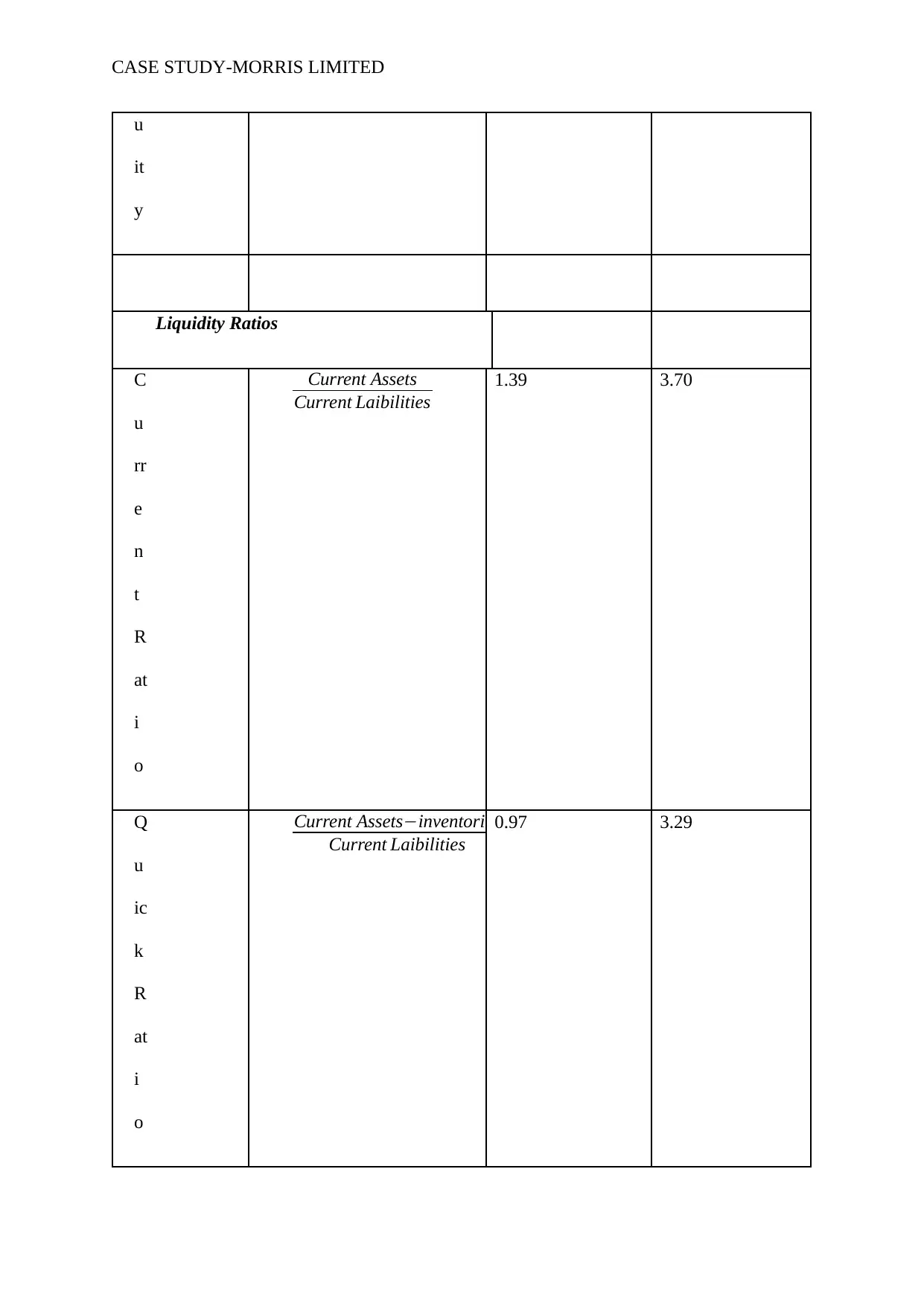

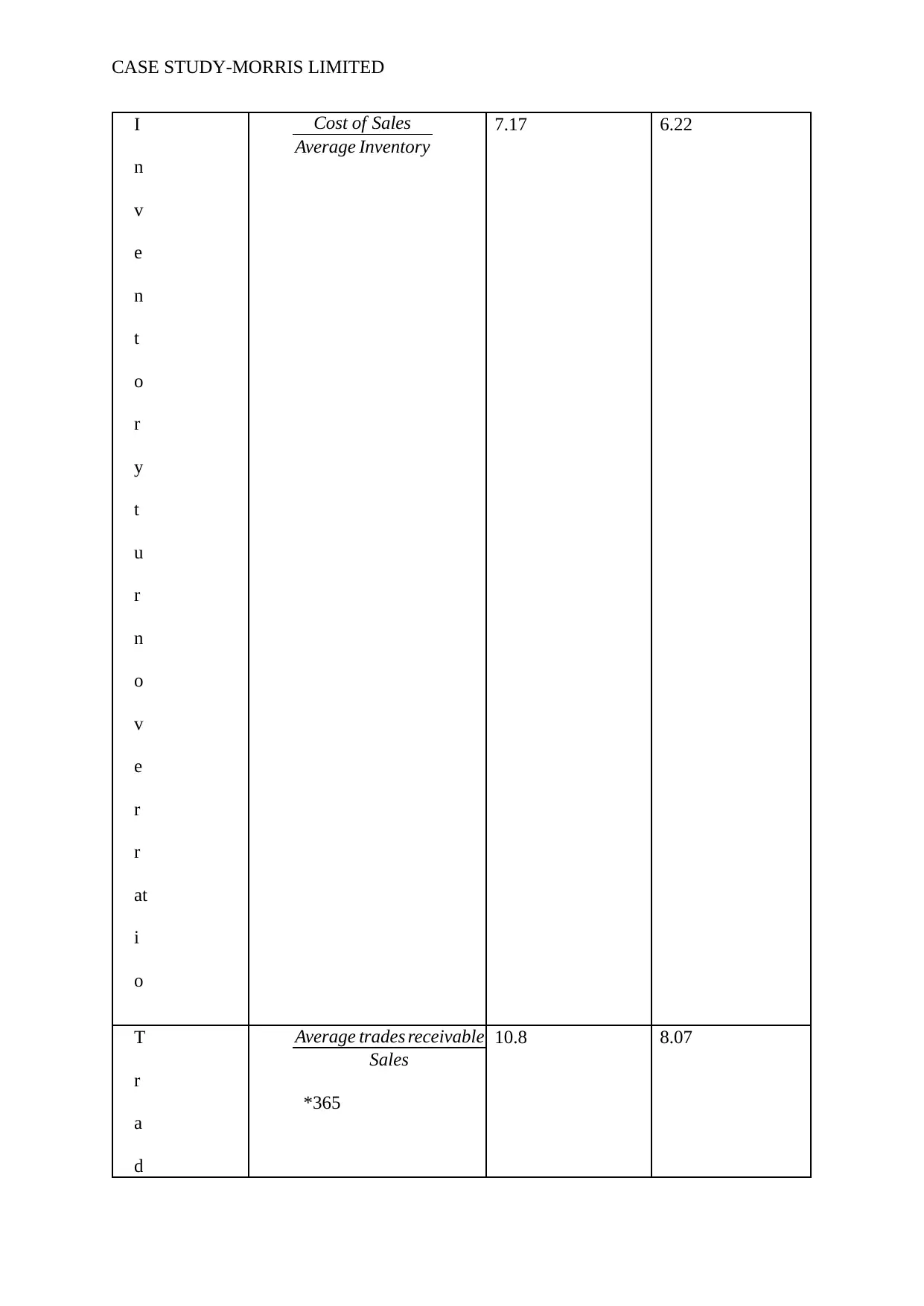

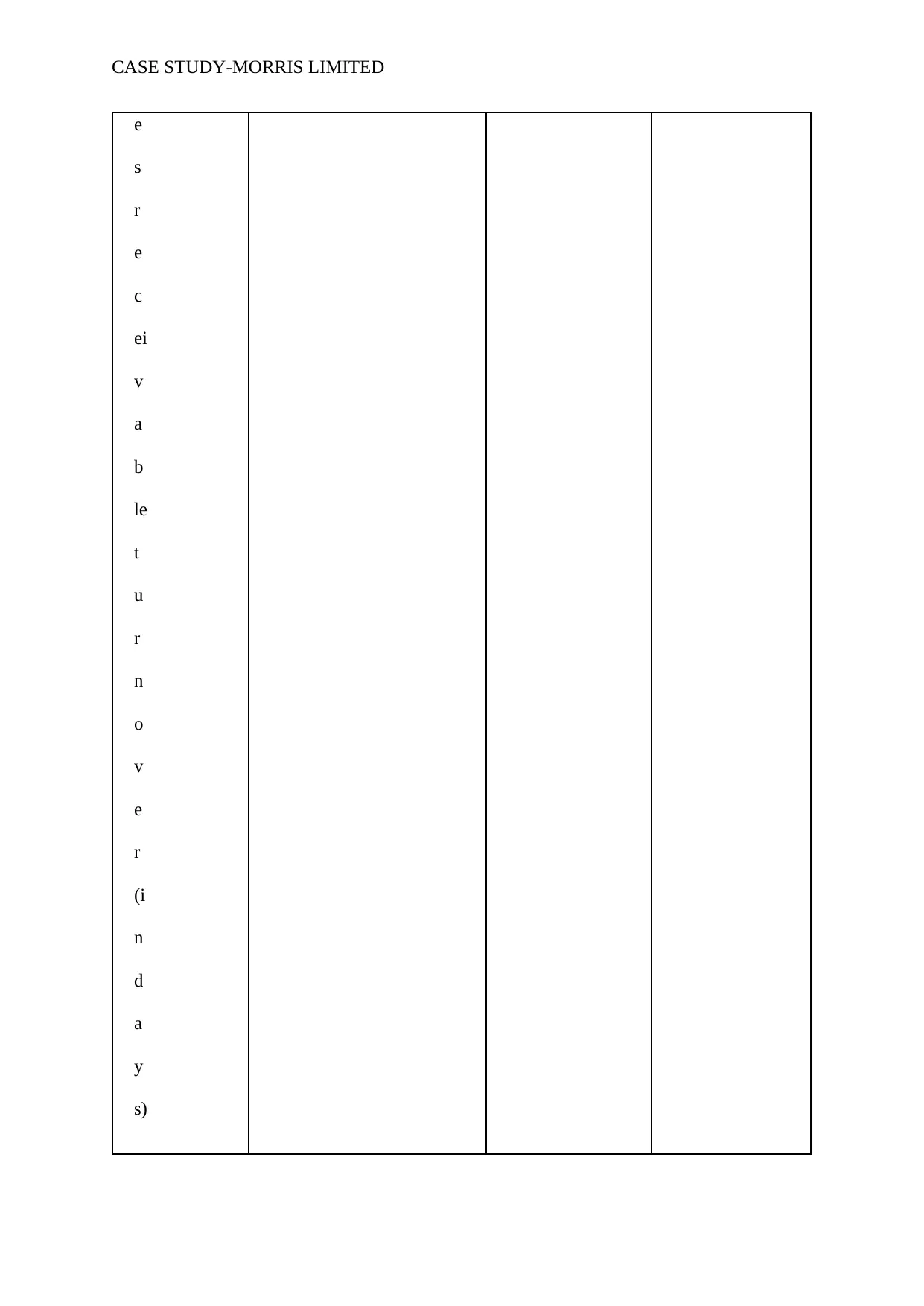

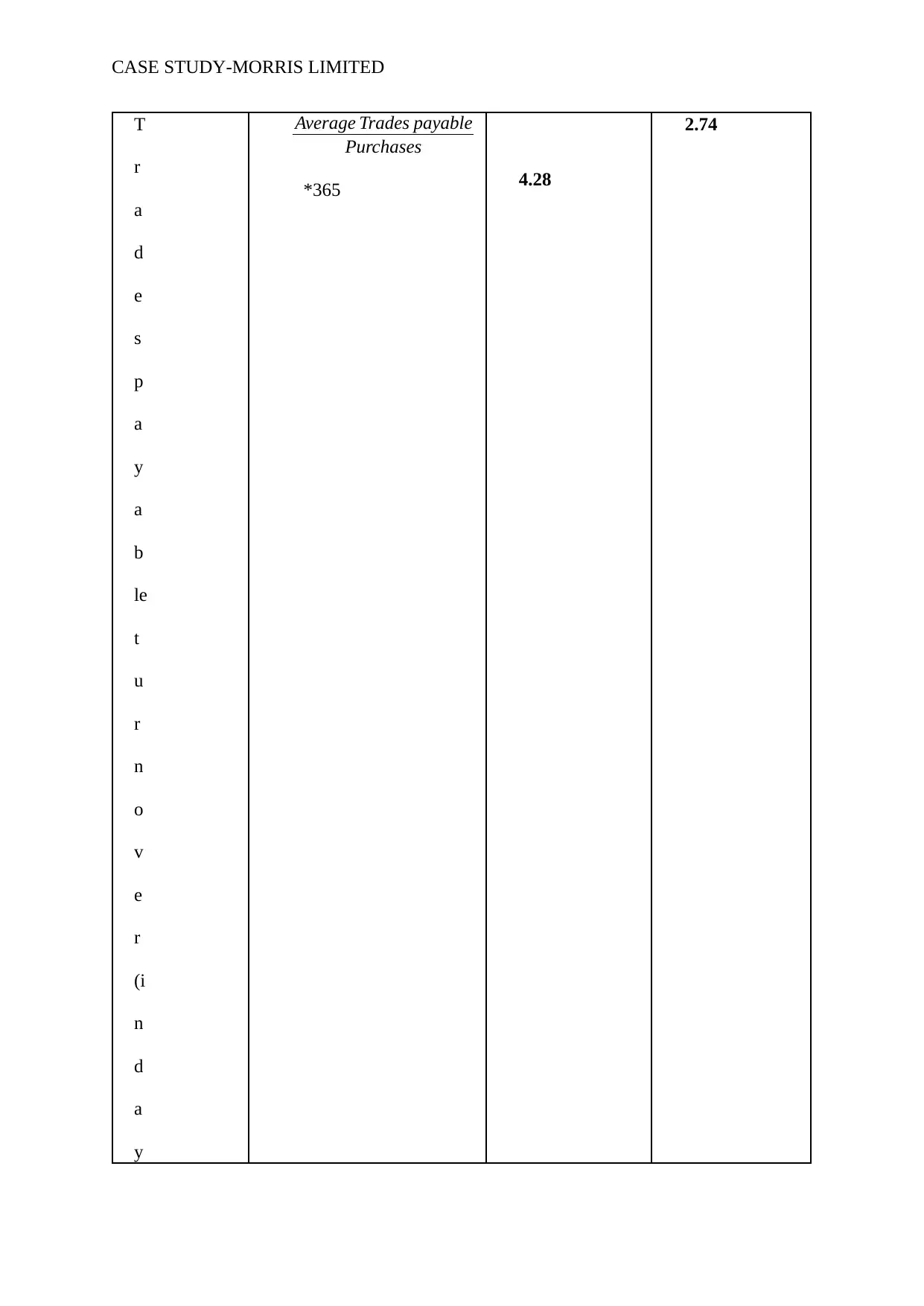

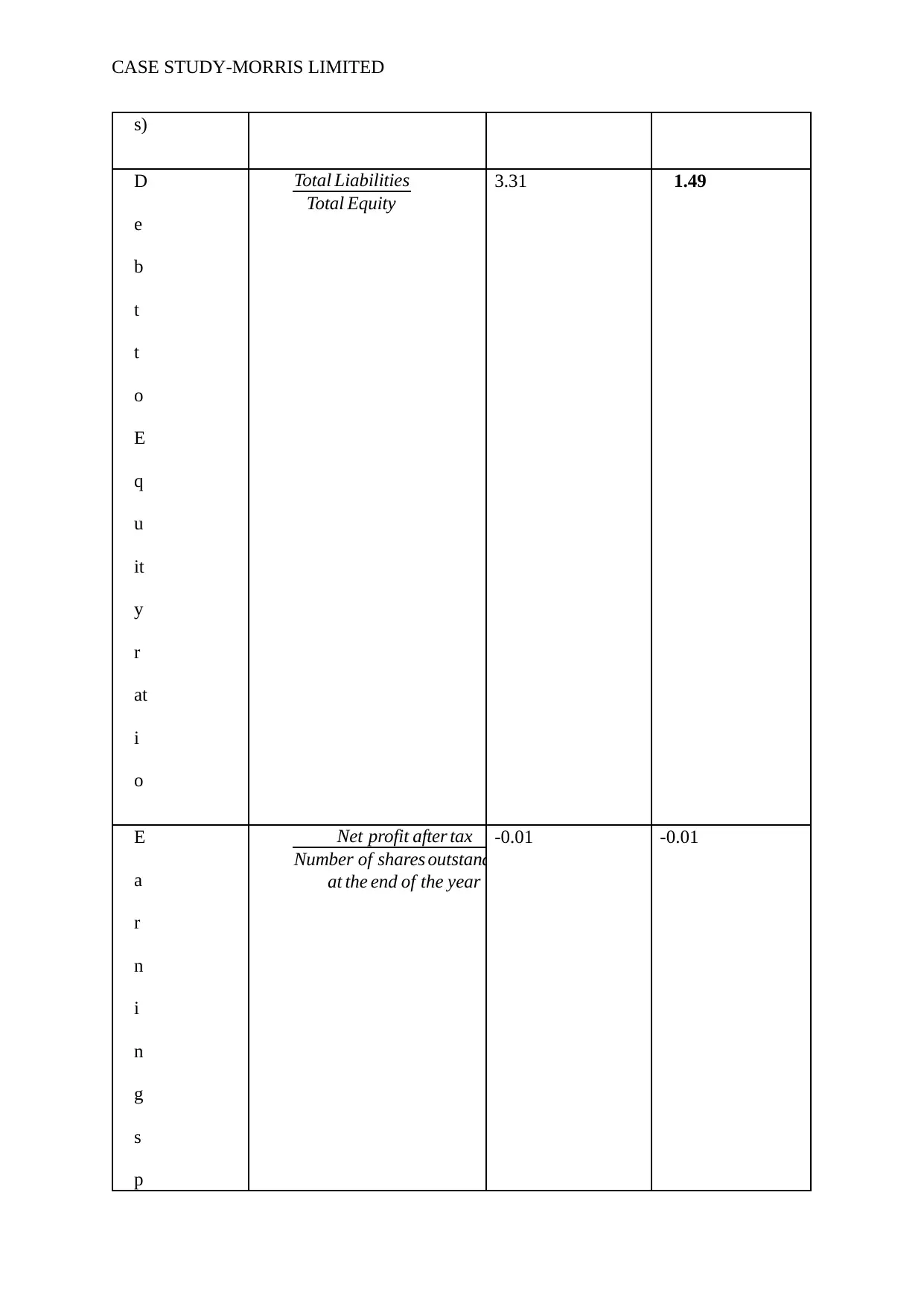

This case study focuses on the financial analysis and audit planning for Morris Ltd, a company recently listed on the Australian Securities Exchange. The assignment requires an analysis of the company's financial statements, including the application of analytical procedures to identify and assess material misstatement risks. It emphasizes the importance of professional skepticism throughout the audit process and the determination of materiality. The case study includes ratio analysis, comparing key financial figures from 2018 and 2019 to evaluate profitability, liquidity, and solvency. The student analyzes the financial ratios, identifying trends and potential risks such as declining gross profit margins, negative net profit margins, and changes in liquidity ratios. The analysis concludes with an assessment of potential material misstatements in the financial statements, specifically highlighting risks related to total liabilities, cost of sales, and inventory valuation.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.