Financial Performance Analysis of Morrison: A Comprehensive Report

VerifiedAdded on 2020/01/07

|21

|5402

|215

Report

AI Summary

This report provides a comprehensive financial analysis of Morrison, a business entity, examining various aspects of its financial performance and strategic decisions. The analysis begins with an interpretation of key financial ratios, including debtor turnover, current ratio, and debt-equity ratio, revealing insights into Morrison's liquidity, profitability, and financial health. The report then delves into the limitations of ratio analysis and compares Morrison's performance with that of Sainsbury's. Furthermore, the report explores different methodologies for product and service costing, including marginal costing, and evaluates the role and limitations of traditional budgets. It also examines activity-based management and costing, cost management methodologies for lean enterprises, and the preparation of strategic management accounting information for investment in advanced manufacturing technology. The impact of resource decisions on organizational performance, process improvement for resource allocation, and the use of benchmarks are also assessed. The report further debates the tensions between financial and strategic objectives, identifies alternative sources of finance, and explores the role of treasury management. Finally, it covers project appraisal, the calculation of the organization's cost of capital, and the evaluation of investment opportunities, including the financial appraisal of strategic proposals and the financial risk of operating in the international market.

MANAGEMENT OF

FINANCIAL

FINANCIAL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Interpretation of ratios...........................................................................................................4

1.2 Limitations of ratio analysis and its impact on same............................................................5

1.3 Comparison of Morrison and Sainsbury...............................................................................5

TASK 2............................................................................................................................................6

2.1 Evaluate the different methodologies and approaches to cost the product and services.......6

2.2 Use of marginal cost method to support short term decision making...................................6

2.3 Analysis of role and limitations of traditional budgets.........................................................7

TASK 3............................................................................................................................................7

3.1 Role of activity based management and costing method......................................................7

3.2 Use cost management methodology to support lean enterprise, business excellence and

value chain analysis.....................................................................................................................8

3.3 Preparation of strategic management accounting information to analyze investment in

advanced manufacturing technology...........................................................................................8

TASK 4............................................................................................................................................9

4.1Impact of resource decisions on organization performance and effectiveness......................9

4.2 Identify the process and activities of an organization and use these to improve resource

allocation.....................................................................................................................................9

4.3 Evaluate the use of benchmark for an organization products, process and practice to

identify opportunities to deliver value......................................................................................10

TASK 5..........................................................................................................................................11

5.1 Debate the tensions between financial and strategic objectives..........................................11

5.2 Identify and evaluate alternative source of finance.............................................................11

5.3 Role of treasury management in the financing risk and control of liquidity......................12

TASK 6..........................................................................................................................................12

6.1 Project appraisal..................................................................................................................12

6.2 Calculate organization cost of capital and explain limitation of such calculations............15

6.3 Evaluate investment opportunity and financially appraise strategic proposals...................16

TASK 7..........................................................................................................................................17

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Interpretation of ratios...........................................................................................................4

1.2 Limitations of ratio analysis and its impact on same............................................................5

1.3 Comparison of Morrison and Sainsbury...............................................................................5

TASK 2............................................................................................................................................6

2.1 Evaluate the different methodologies and approaches to cost the product and services.......6

2.2 Use of marginal cost method to support short term decision making...................................6

2.3 Analysis of role and limitations of traditional budgets.........................................................7

TASK 3............................................................................................................................................7

3.1 Role of activity based management and costing method......................................................7

3.2 Use cost management methodology to support lean enterprise, business excellence and

value chain analysis.....................................................................................................................8

3.3 Preparation of strategic management accounting information to analyze investment in

advanced manufacturing technology...........................................................................................8

TASK 4............................................................................................................................................9

4.1Impact of resource decisions on organization performance and effectiveness......................9

4.2 Identify the process and activities of an organization and use these to improve resource

allocation.....................................................................................................................................9

4.3 Evaluate the use of benchmark for an organization products, process and practice to

identify opportunities to deliver value......................................................................................10

TASK 5..........................................................................................................................................11

5.1 Debate the tensions between financial and strategic objectives..........................................11

5.2 Identify and evaluate alternative source of finance.............................................................11

5.3 Role of treasury management in the financing risk and control of liquidity......................12

TASK 6..........................................................................................................................................12

6.1 Project appraisal..................................................................................................................12

6.2 Calculate organization cost of capital and explain limitation of such calculations............15

6.3 Evaluate investment opportunity and financially appraise strategic proposals...................16

TASK 7..........................................................................................................................................17

7.1 Identify the financial risk of operating in international market..........................................17

7.2 Appraise international investment decisions.......................................................................17

7.3 Sources of finance...............................................................................................................18

TASK 8..........................................................................................................................................19

8.1 Type and sources of risk ....................................................................................................19

8.2 Use of techniques for evaluating and managing organization risk ....................................19

8.3 Prepare and utilize risk management reports......................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

ILLUSTRATION INDEX

Illustration 1: Calculation of pay back period................................................................................14

Illustration 2: Calculation of NPV.................................................................................................14

Illustration 3: Calculation of ARR.................................................................................................14

Illustration 4: Calculation of IRR..................................................................................................15

INDEX OF TABLES

Table 1: Ratios of Morrison.............................................................................................................4

7.2 Appraise international investment decisions.......................................................................17

7.3 Sources of finance...............................................................................................................18

TASK 8..........................................................................................................................................19

8.1 Type and sources of risk ....................................................................................................19

8.2 Use of techniques for evaluating and managing organization risk ....................................19

8.3 Prepare and utilize risk management reports......................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

ILLUSTRATION INDEX

Illustration 1: Calculation of pay back period................................................................................14

Illustration 2: Calculation of NPV.................................................................................................14

Illustration 3: Calculation of ARR.................................................................................................14

Illustration 4: Calculation of IRR..................................................................................................15

INDEX OF TABLES

Table 1: Ratios of Morrison.............................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Business finance is one of the most important domain whose tools and techniques are

greatly used by the managers for making tough decisions. In this report, in respect to new

product development in context of Morrison varied techniques are discussed. Along with this,

project evaluation methods are also applied practically. At end of the report, different business

risks associated with concern are discussed briefly.

TASK 1

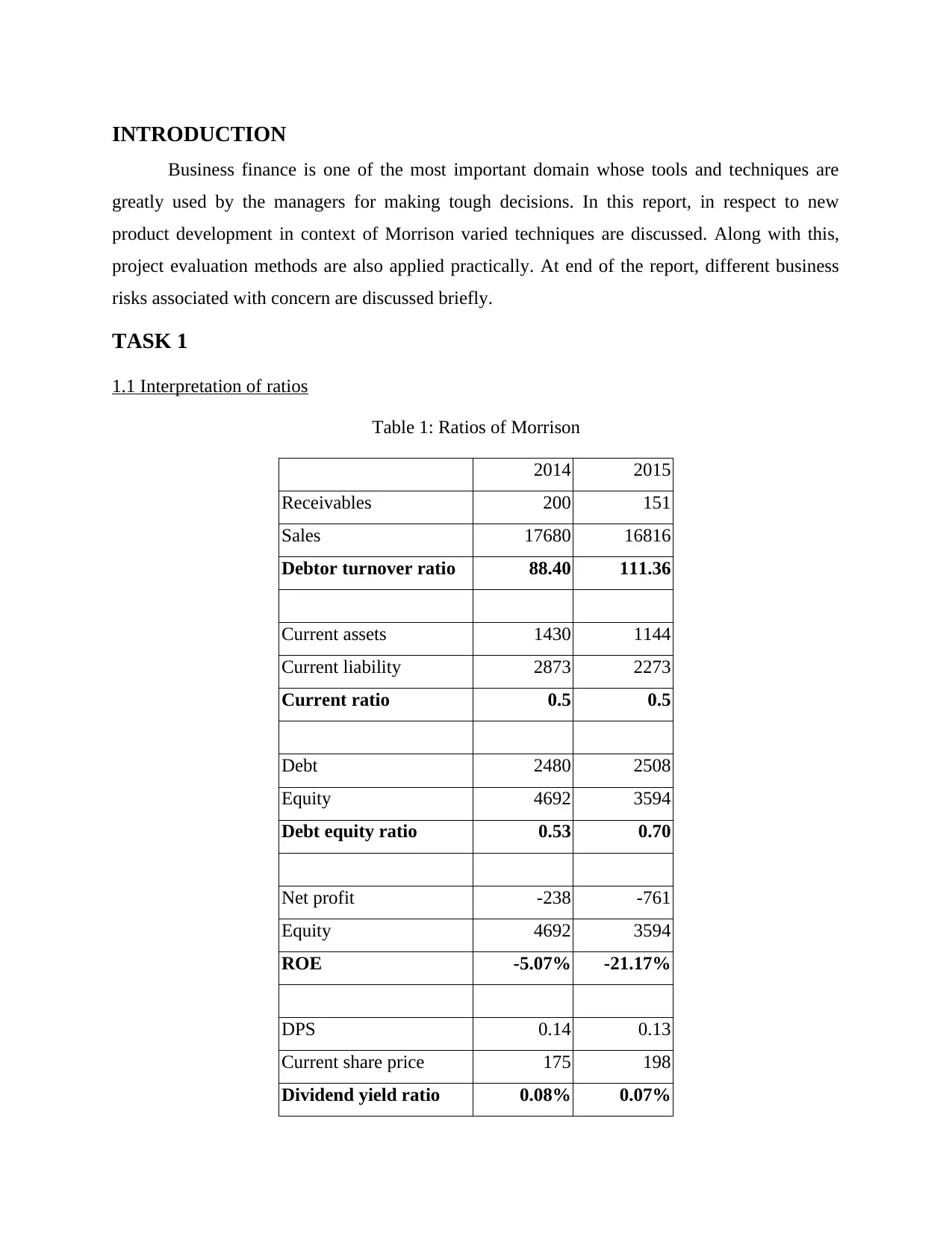

1.1 Interpretation of ratios

Table 1: Ratios of Morrison

2014 2015

Receivables 200 151

Sales 17680 16816

Debtor turnover ratio 88.40 111.36

Current assets 1430 1144

Current liability 2873 2273

Current ratio 0.5 0.5

Debt 2480 2508

Equity 4692 3594

Debt equity ratio 0.53 0.70

Net profit -238 -761

Equity 4692 3594

ROE -5.07% -21.17%

DPS 0.14 0.13

Current share price 175 198

Dividend yield ratio 0.08% 0.07%

Business finance is one of the most important domain whose tools and techniques are

greatly used by the managers for making tough decisions. In this report, in respect to new

product development in context of Morrison varied techniques are discussed. Along with this,

project evaluation methods are also applied practically. At end of the report, different business

risks associated with concern are discussed briefly.

TASK 1

1.1 Interpretation of ratios

Table 1: Ratios of Morrison

2014 2015

Receivables 200 151

Sales 17680 16816

Debtor turnover ratio 88.40 111.36

Current assets 1430 1144

Current liability 2873 2273

Current ratio 0.5 0.5

Debt 2480 2508

Equity 4692 3594

Debt equity ratio 0.53 0.70

Net profit -238 -761

Equity 4692 3594

ROE -5.07% -21.17%

DPS 0.14 0.13

Current share price 175 198

Dividend yield ratio 0.08% 0.07%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current share price 175 198

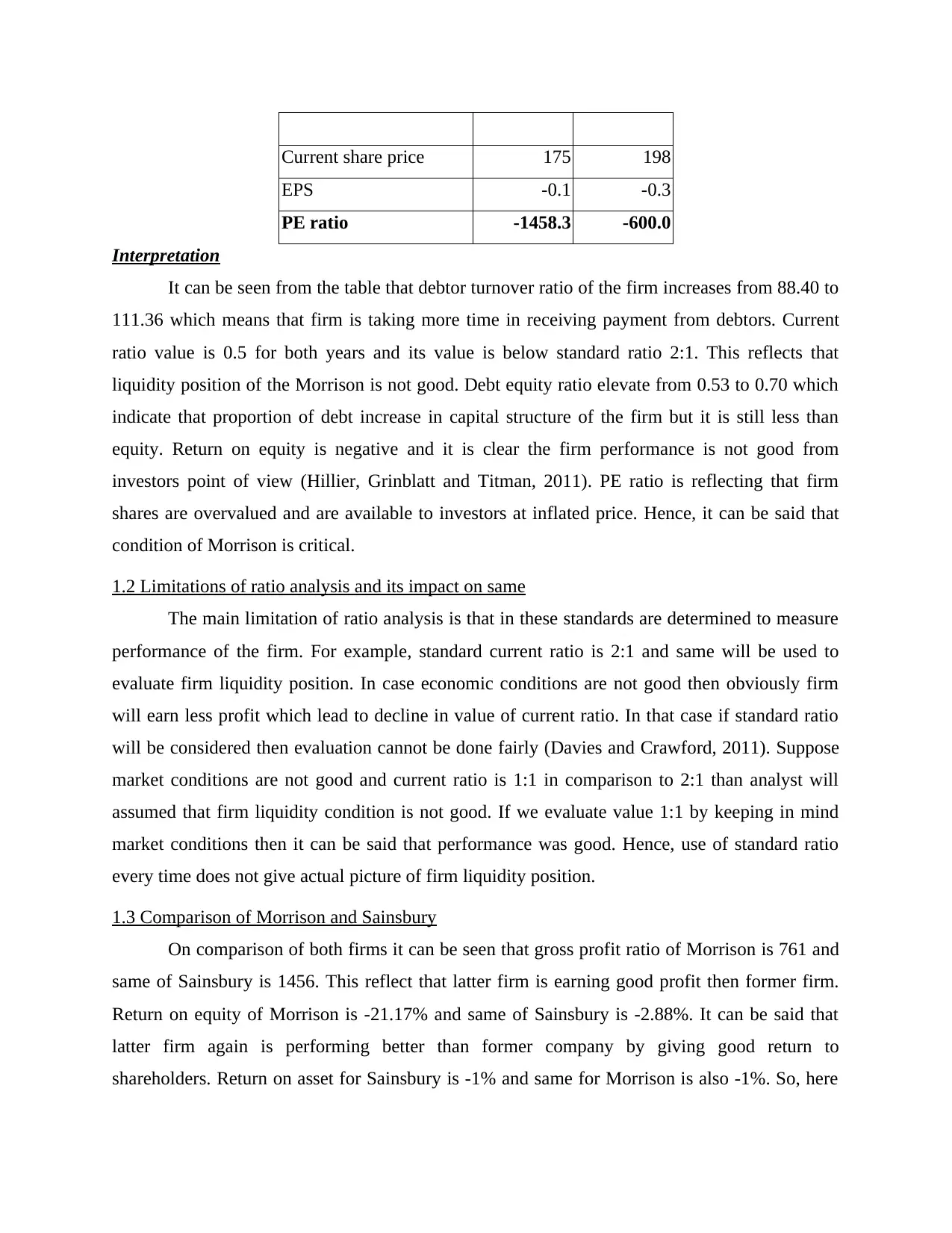

EPS -0.1 -0.3

PE ratio -1458.3 -600.0

Interpretation

It can be seen from the table that debtor turnover ratio of the firm increases from 88.40 to

111.36 which means that firm is taking more time in receiving payment from debtors. Current

ratio value is 0.5 for both years and its value is below standard ratio 2:1. This reflects that

liquidity position of the Morrison is not good. Debt equity ratio elevate from 0.53 to 0.70 which

indicate that proportion of debt increase in capital structure of the firm but it is still less than

equity. Return on equity is negative and it is clear the firm performance is not good from

investors point of view (Hillier, Grinblatt and Titman, 2011). PE ratio is reflecting that firm

shares are overvalued and are available to investors at inflated price. Hence, it can be said that

condition of Morrison is critical.

1.2 Limitations of ratio analysis and its impact on same

The main limitation of ratio analysis is that in these standards are determined to measure

performance of the firm. For example, standard current ratio is 2:1 and same will be used to

evaluate firm liquidity position. In case economic conditions are not good then obviously firm

will earn less profit which lead to decline in value of current ratio. In that case if standard ratio

will be considered then evaluation cannot be done fairly (Davies and Crawford, 2011). Suppose

market conditions are not good and current ratio is 1:1 in comparison to 2:1 than analyst will

assumed that firm liquidity condition is not good. If we evaluate value 1:1 by keeping in mind

market conditions then it can be said that performance was good. Hence, use of standard ratio

every time does not give actual picture of firm liquidity position.

1.3 Comparison of Morrison and Sainsbury

On comparison of both firms it can be seen that gross profit ratio of Morrison is 761 and

same of Sainsbury is 1456. This reflect that latter firm is earning good profit then former firm.

Return on equity of Morrison is -21.17% and same of Sainsbury is -2.88%. It can be said that

latter firm again is performing better than former company by giving good return to

shareholders. Return on asset for Sainsbury is -1% and same for Morrison is also -1%. So, here

EPS -0.1 -0.3

PE ratio -1458.3 -600.0

Interpretation

It can be seen from the table that debtor turnover ratio of the firm increases from 88.40 to

111.36 which means that firm is taking more time in receiving payment from debtors. Current

ratio value is 0.5 for both years and its value is below standard ratio 2:1. This reflects that

liquidity position of the Morrison is not good. Debt equity ratio elevate from 0.53 to 0.70 which

indicate that proportion of debt increase in capital structure of the firm but it is still less than

equity. Return on equity is negative and it is clear the firm performance is not good from

investors point of view (Hillier, Grinblatt and Titman, 2011). PE ratio is reflecting that firm

shares are overvalued and are available to investors at inflated price. Hence, it can be said that

condition of Morrison is critical.

1.2 Limitations of ratio analysis and its impact on same

The main limitation of ratio analysis is that in these standards are determined to measure

performance of the firm. For example, standard current ratio is 2:1 and same will be used to

evaluate firm liquidity position. In case economic conditions are not good then obviously firm

will earn less profit which lead to decline in value of current ratio. In that case if standard ratio

will be considered then evaluation cannot be done fairly (Davies and Crawford, 2011). Suppose

market conditions are not good and current ratio is 1:1 in comparison to 2:1 than analyst will

assumed that firm liquidity condition is not good. If we evaluate value 1:1 by keeping in mind

market conditions then it can be said that performance was good. Hence, use of standard ratio

every time does not give actual picture of firm liquidity position.

1.3 Comparison of Morrison and Sainsbury

On comparison of both firms it can be seen that gross profit ratio of Morrison is 761 and

same of Sainsbury is 1456. This reflect that latter firm is earning good profit then former firm.

Return on equity of Morrison is -21.17% and same of Sainsbury is -2.88%. It can be said that

latter firm again is performing better than former company by giving good return to

shareholders. Return on asset for Sainsbury is -1% and same for Morrison is also -1%. So, here

no comparison can be made between both firms. It is management inefficiency due to which on

every ratio performance in case of Morrison is poor relative to rival firm. Morrison needs to

introduce new products in the market which will help it in increasing its profitability. Moreover,

there is need to bring changes in the organization so that efficiency level in respect to use of asset

can be increased.

TASK 2

2.1 Evaluate the different methodologies and approaches to cost the product and services

There is different method of costing job and process costing. Process costing is used

when firm produce similar products and intends to do costing of each phase of production. By

adding cost of each stage aggregate cost is measured in process costing (Otley and Emmanuel,

2013). Contrary, to this in batch or contract costing cost of products that are different from each

other is computed separately. The main feature of absorption costing is that in this direct and

indirect cost are considered to compute per unit cost. Direct cost are allocated to the per unit of

the product. Contrary to this, indirect cost are accumulated as overhead and same are charged as

absorption rate on product which is also one of the most important feature of this method. The

third and most important feature of this method is that in this administration cost are not taken in

to consideration.

2.2 Use of marginal cost method to support short term decision making

Marginal cost method is a technique of costing under which variable expenses are

considered for costing of products. Firm sometimes add few numbers on variable expenses to

compute per unit cost. Cost volume profit analysis is a method that reflects the part of sales that

is covered variable expenses. Cost volume profit analysis is given below.

Sales 5000000

Variable expenses 2000000

Contribution 3000000

Contribution/Margin ratio 60.00%

It can be seen from the table that under marginal costing method 40% of sales is covered by

variable expenses. It can be said that 60% amount of sales is covered by profit. In order to make

higher sales in short term Morrison can make use of this technique and can determine the profit

every ratio performance in case of Morrison is poor relative to rival firm. Morrison needs to

introduce new products in the market which will help it in increasing its profitability. Moreover,

there is need to bring changes in the organization so that efficiency level in respect to use of asset

can be increased.

TASK 2

2.1 Evaluate the different methodologies and approaches to cost the product and services

There is different method of costing job and process costing. Process costing is used

when firm produce similar products and intends to do costing of each phase of production. By

adding cost of each stage aggregate cost is measured in process costing (Otley and Emmanuel,

2013). Contrary, to this in batch or contract costing cost of products that are different from each

other is computed separately. The main feature of absorption costing is that in this direct and

indirect cost are considered to compute per unit cost. Direct cost are allocated to the per unit of

the product. Contrary to this, indirect cost are accumulated as overhead and same are charged as

absorption rate on product which is also one of the most important feature of this method. The

third and most important feature of this method is that in this administration cost are not taken in

to consideration.

2.2 Use of marginal cost method to support short term decision making

Marginal cost method is a technique of costing under which variable expenses are

considered for costing of products. Firm sometimes add few numbers on variable expenses to

compute per unit cost. Cost volume profit analysis is a method that reflects the part of sales that

is covered variable expenses. Cost volume profit analysis is given below.

Sales 5000000

Variable expenses 2000000

Contribution 3000000

Contribution/Margin ratio 60.00%

It can be seen from the table that under marginal costing method 40% of sales is covered by

variable expenses. It can be said that 60% amount of sales is covered by profit. In order to make

higher sales in short term Morrison can make use of this technique and can determine the profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

percentage that can be earned on per unit sales only be considering variable expenses. There is

difference between variable and fixed cost (Herman, 2011). Former cost refers to expenses that

does not remain fixed and keeps on changing consistently. Contrary to this, fixed cost refers to

expenses that remain unchanged during lifetime of the firm. In order to take short term decision

regarding earning of profit firm can ignore consideration of fixed cost for mentioned duration.

2.3 Analysis of role and limitations of traditional budgets

There are some limitations of traditional budget like lots of time is consumed on

preparing same. There are few numbers of people that prepare a budget then also lots of time is

consumed which is its main demerit. Traditional budgets are prepared for a year and due to this

reason it is not reviewed in mentioned duration. Sometimes business conditions get changed and

it is not wise decision to follow old budget. Firm that prepared mentioned type of budget

consistently and face loss in the business (Anandarajan, Anandarajan and Srinivasan, 2012). This

is one of main demerit of traditional budget. The main benefit of traditional budget is that it is

very simple and one by looking at it can easily understand number of things. It can be said that

budget have both positive and negative points.

TASK 3

3.1 Role of activity based management and costing method

Activity based costing is the best method because in this different activities that are core

to business and affects each other are considered to compute per unit cost. By doing so costing of

products and services is done in proper way. Activity based management can be used for re-

engineering, product costing, budgeting and bench-marking (DRURY, 2013). Under mentioned

type of management each and every sort of activity can be identified and its evaluation can be

done. By doing so areas where improvements need to be done in respect to performance of

activity in relation to reducing cost of same can be identified. Budget can be prepared by using

this method because during re-engineering process deep understanding will be developed about

each activity. Hence, projection of specific one can be easily made by considering different

situations. After considering number of things cost for each activity is determined and due to this

reason values that are identified by using activity based costing can be set as benchmark in the

budget.

difference between variable and fixed cost (Herman, 2011). Former cost refers to expenses that

does not remain fixed and keeps on changing consistently. Contrary to this, fixed cost refers to

expenses that remain unchanged during lifetime of the firm. In order to take short term decision

regarding earning of profit firm can ignore consideration of fixed cost for mentioned duration.

2.3 Analysis of role and limitations of traditional budgets

There are some limitations of traditional budget like lots of time is consumed on

preparing same. There are few numbers of people that prepare a budget then also lots of time is

consumed which is its main demerit. Traditional budgets are prepared for a year and due to this

reason it is not reviewed in mentioned duration. Sometimes business conditions get changed and

it is not wise decision to follow old budget. Firm that prepared mentioned type of budget

consistently and face loss in the business (Anandarajan, Anandarajan and Srinivasan, 2012). This

is one of main demerit of traditional budget. The main benefit of traditional budget is that it is

very simple and one by looking at it can easily understand number of things. It can be said that

budget have both positive and negative points.

TASK 3

3.1 Role of activity based management and costing method

Activity based costing is the best method because in this different activities that are core

to business and affects each other are considered to compute per unit cost. By doing so costing of

products and services is done in proper way. Activity based management can be used for re-

engineering, product costing, budgeting and bench-marking (DRURY, 2013). Under mentioned

type of management each and every sort of activity can be identified and its evaluation can be

done. By doing so areas where improvements need to be done in respect to performance of

activity in relation to reducing cost of same can be identified. Budget can be prepared by using

this method because during re-engineering process deep understanding will be developed about

each activity. Hence, projection of specific one can be easily made by considering different

situations. After considering number of things cost for each activity is determined and due to this

reason values that are identified by using activity based costing can be set as benchmark in the

budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.2 Use cost management methodology to support lean enterprise, business excellence and value

chain analysis

Lean enterprise refers to the elimination of those activities that does not add value to the

product. It can be said that under lean enterprise all unproductive activities are eliminated from

production process that is related to new product development. By following lean enterprise

approach in value chain all wasteful activities can be removed and cost of production can be

reduced for new product that firm intends to develop (Bennett, Schaltegger and Zvezdov, 2011).

This lead to achievement of excellence in the business. In order to develop new product it is

necessary to conduct market research. Hence, for this some personnel will require who will

conduct field research. Thereafter, data analyst will need who will do analysis of data that is

related to the banana ripening factory that belongs to Morrison. By preparing proper strategy the

best use of resource will be made.

3.3 Preparation of strategic management accounting information to analyze investment in

advanced manufacturing technology

Tangible and intangible benefits of advanced technology

By using advanced technology banana of good quality can be made which will lead to

elevation in profitability of the firm. This will help firm in focusing more attention on new

product line (Ward, 2012). Intangible benefit of advanced technology is that it to some extent

help firm in removing loopholes from existing product line.

Balanced scorecard

Financial Internal process

Wages: 8,00,000

Employees working hours: 9 hrs

Material consumption: 100 KG per

batch

Efficient employees will be hired and

efforts will be made to retain them for

long term.

Material will be order on time so that

cost of storage remain low.

chain analysis

Lean enterprise refers to the elimination of those activities that does not add value to the

product. It can be said that under lean enterprise all unproductive activities are eliminated from

production process that is related to new product development. By following lean enterprise

approach in value chain all wasteful activities can be removed and cost of production can be

reduced for new product that firm intends to develop (Bennett, Schaltegger and Zvezdov, 2011).

This lead to achievement of excellence in the business. In order to develop new product it is

necessary to conduct market research. Hence, for this some personnel will require who will

conduct field research. Thereafter, data analyst will need who will do analysis of data that is

related to the banana ripening factory that belongs to Morrison. By preparing proper strategy the

best use of resource will be made.

3.3 Preparation of strategic management accounting information to analyze investment in

advanced manufacturing technology

Tangible and intangible benefits of advanced technology

By using advanced technology banana of good quality can be made which will lead to

elevation in profitability of the firm. This will help firm in focusing more attention on new

product line (Ward, 2012). Intangible benefit of advanced technology is that it to some extent

help firm in removing loopholes from existing product line.

Balanced scorecard

Financial Internal process

Wages: 8,00,000

Employees working hours: 9 hrs

Material consumption: 100 KG per

batch

Efficient employees will be hired and

efforts will be made to retain them for

long term.

Material will be order on time so that

cost of storage remain low.

TASK 4

4.1Impact of resource decisions on organization performance and effectiveness

In order to allocate resource among different activities Morrison can use Linear

programming model (LPP). By using same allocation of resource can be done in the best way.

This model can be developed in Excel by using Solver function. This function also develop

multiple reports that can be used to make business decisions. For allocating resource criteria can

be determined in terms of profit and cost that Morrison intends to earn and incur on its new

product that is in development phase (Van der Stede, 2011). Cost of workers can be kept at 8,

00,000 and accordingly by using LPP method allocation of same can be done in different

activities. It is possible that there is a strategic need to make payment of 8, 50,000 to workers in

order to achieve objective but firm budget of 8, 00,000. In order to manage this problem firm can

take short term loan at low interest rate. In this way, gap between strategic need and availability

can be managed.

4.2 Identify the process and activities of an organization and use these to improve resource

allocation

7 seven principles of process re-engineering are as follows.

Focus and make efforts around outcomes not tasks

Identify all activities and rank them on the basis of urgency

Integration of information processing work

Proper treatment to resources that are dispersed

Link parallel activities at place of unifying there results.

Control on process

Capturing information at once on source

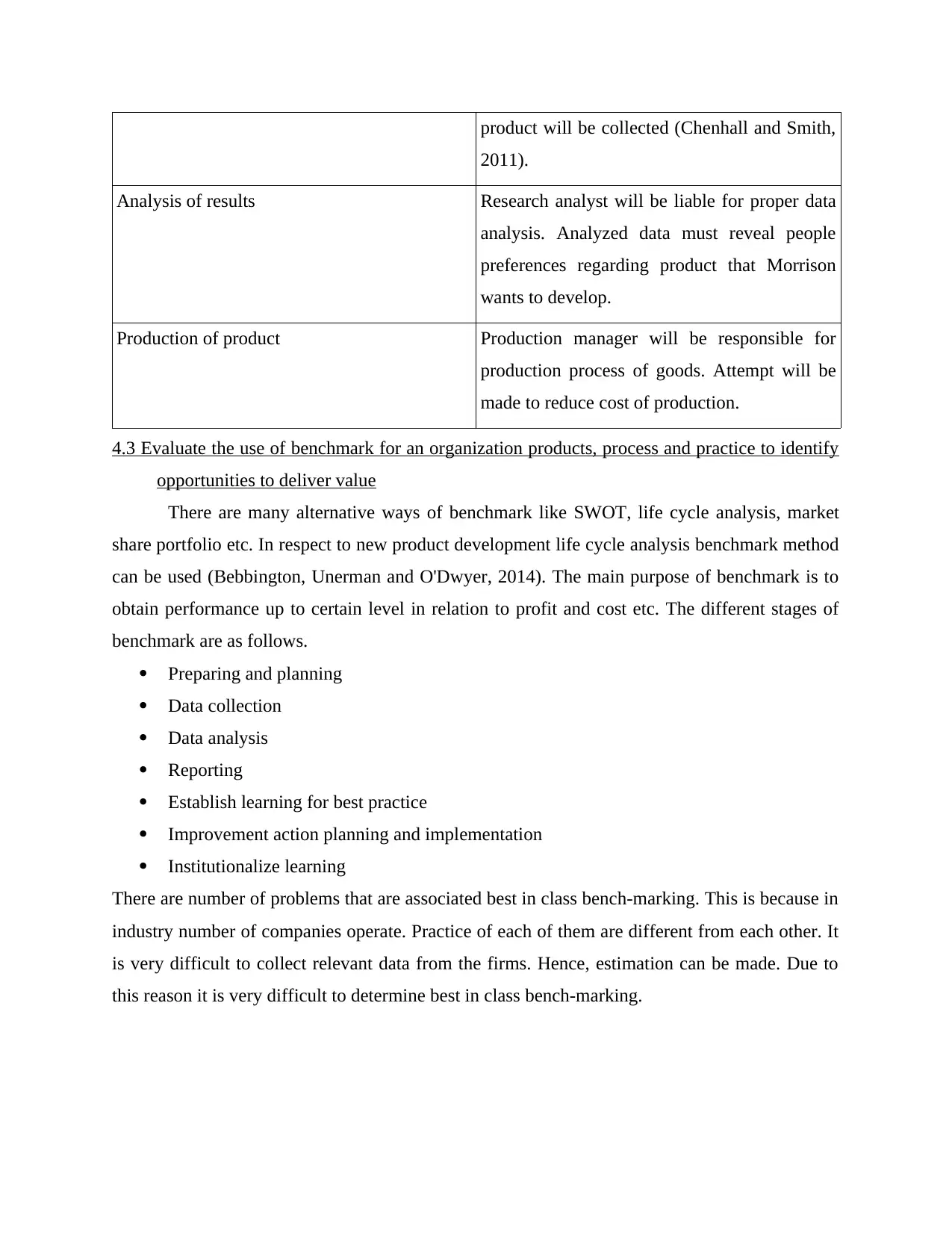

Business process mapping revealed activities that are related to defining who is responsible, to

what standard a business process should be completed etc.

Market research Marketing manager of Morrison will be

responsible for completing research on time. In

research data related to feature that people with

demographic characteristics intend to see in

4.1Impact of resource decisions on organization performance and effectiveness

In order to allocate resource among different activities Morrison can use Linear

programming model (LPP). By using same allocation of resource can be done in the best way.

This model can be developed in Excel by using Solver function. This function also develop

multiple reports that can be used to make business decisions. For allocating resource criteria can

be determined in terms of profit and cost that Morrison intends to earn and incur on its new

product that is in development phase (Van der Stede, 2011). Cost of workers can be kept at 8,

00,000 and accordingly by using LPP method allocation of same can be done in different

activities. It is possible that there is a strategic need to make payment of 8, 50,000 to workers in

order to achieve objective but firm budget of 8, 00,000. In order to manage this problem firm can

take short term loan at low interest rate. In this way, gap between strategic need and availability

can be managed.

4.2 Identify the process and activities of an organization and use these to improve resource

allocation

7 seven principles of process re-engineering are as follows.

Focus and make efforts around outcomes not tasks

Identify all activities and rank them on the basis of urgency

Integration of information processing work

Proper treatment to resources that are dispersed

Link parallel activities at place of unifying there results.

Control on process

Capturing information at once on source

Business process mapping revealed activities that are related to defining who is responsible, to

what standard a business process should be completed etc.

Market research Marketing manager of Morrison will be

responsible for completing research on time. In

research data related to feature that people with

demographic characteristics intend to see in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

product will be collected (Chenhall and Smith,

2011).

Analysis of results Research analyst will be liable for proper data

analysis. Analyzed data must reveal people

preferences regarding product that Morrison

wants to develop.

Production of product Production manager will be responsible for

production process of goods. Attempt will be

made to reduce cost of production.

4.3 Evaluate the use of benchmark for an organization products, process and practice to identify

opportunities to deliver value

There are many alternative ways of benchmark like SWOT, life cycle analysis, market

share portfolio etc. In respect to new product development life cycle analysis benchmark method

can be used (Bebbington, Unerman and O'Dwyer, 2014). The main purpose of benchmark is to

obtain performance up to certain level in relation to profit and cost etc. The different stages of

benchmark are as follows.

Preparing and planning

Data collection

Data analysis

Reporting

Establish learning for best practice

Improvement action planning and implementation

Institutionalize learning

There are number of problems that are associated best in class bench-marking. This is because in

industry number of companies operate. Practice of each of them are different from each other. It

is very difficult to collect relevant data from the firms. Hence, estimation can be made. Due to

this reason it is very difficult to determine best in class bench-marking.

2011).

Analysis of results Research analyst will be liable for proper data

analysis. Analyzed data must reveal people

preferences regarding product that Morrison

wants to develop.

Production of product Production manager will be responsible for

production process of goods. Attempt will be

made to reduce cost of production.

4.3 Evaluate the use of benchmark for an organization products, process and practice to identify

opportunities to deliver value

There are many alternative ways of benchmark like SWOT, life cycle analysis, market

share portfolio etc. In respect to new product development life cycle analysis benchmark method

can be used (Bebbington, Unerman and O'Dwyer, 2014). The main purpose of benchmark is to

obtain performance up to certain level in relation to profit and cost etc. The different stages of

benchmark are as follows.

Preparing and planning

Data collection

Data analysis

Reporting

Establish learning for best practice

Improvement action planning and implementation

Institutionalize learning

There are number of problems that are associated best in class bench-marking. This is because in

industry number of companies operate. Practice of each of them are different from each other. It

is very difficult to collect relevant data from the firms. Hence, estimation can be made. Due to

this reason it is very difficult to determine best in class bench-marking.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 5

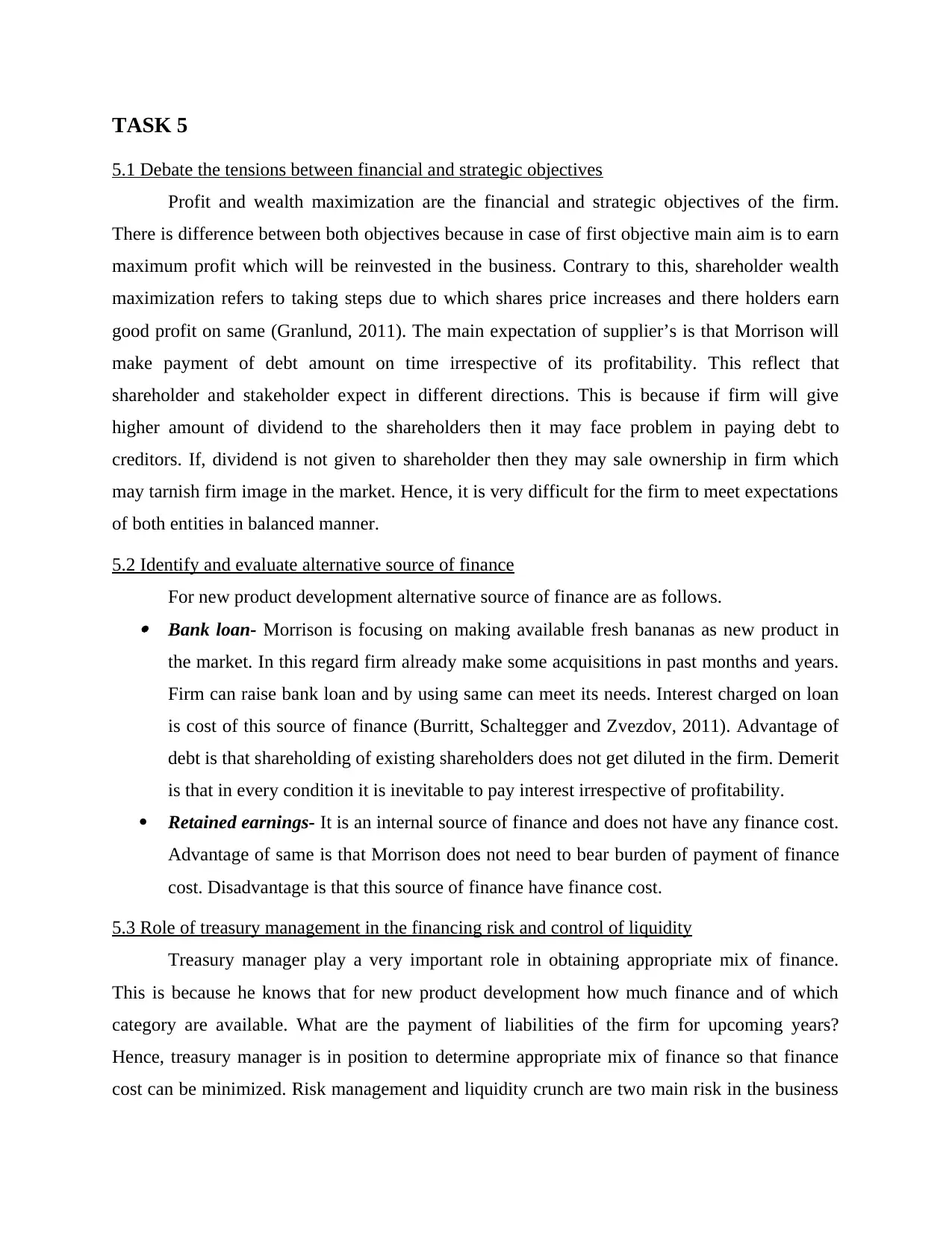

5.1 Debate the tensions between financial and strategic objectives

Profit and wealth maximization are the financial and strategic objectives of the firm.

There is difference between both objectives because in case of first objective main aim is to earn

maximum profit which will be reinvested in the business. Contrary to this, shareholder wealth

maximization refers to taking steps due to which shares price increases and there holders earn

good profit on same (Granlund, 2011). The main expectation of supplier’s is that Morrison will

make payment of debt amount on time irrespective of its profitability. This reflect that

shareholder and stakeholder expect in different directions. This is because if firm will give

higher amount of dividend to the shareholders then it may face problem in paying debt to

creditors. If, dividend is not given to shareholder then they may sale ownership in firm which

may tarnish firm image in the market. Hence, it is very difficult for the firm to meet expectations

of both entities in balanced manner.

5.2 Identify and evaluate alternative source of finance

For new product development alternative source of finance are as follows. Bank loan- Morrison is focusing on making available fresh bananas as new product in

the market. In this regard firm already make some acquisitions in past months and years.

Firm can raise bank loan and by using same can meet its needs. Interest charged on loan

is cost of this source of finance (Burritt, Schaltegger and Zvezdov, 2011). Advantage of

debt is that shareholding of existing shareholders does not get diluted in the firm. Demerit

is that in every condition it is inevitable to pay interest irrespective of profitability.

Retained earnings- It is an internal source of finance and does not have any finance cost.

Advantage of same is that Morrison does not need to bear burden of payment of finance

cost. Disadvantage is that this source of finance have finance cost.

5.3 Role of treasury management in the financing risk and control of liquidity

Treasury manager play a very important role in obtaining appropriate mix of finance.

This is because he knows that for new product development how much finance and of which

category are available. What are the payment of liabilities of the firm for upcoming years?

Hence, treasury manager is in position to determine appropriate mix of finance so that finance

cost can be minimized. Risk management and liquidity crunch are two main risk in the business

5.1 Debate the tensions between financial and strategic objectives

Profit and wealth maximization are the financial and strategic objectives of the firm.

There is difference between both objectives because in case of first objective main aim is to earn

maximum profit which will be reinvested in the business. Contrary to this, shareholder wealth

maximization refers to taking steps due to which shares price increases and there holders earn

good profit on same (Granlund, 2011). The main expectation of supplier’s is that Morrison will

make payment of debt amount on time irrespective of its profitability. This reflect that

shareholder and stakeholder expect in different directions. This is because if firm will give

higher amount of dividend to the shareholders then it may face problem in paying debt to

creditors. If, dividend is not given to shareholder then they may sale ownership in firm which

may tarnish firm image in the market. Hence, it is very difficult for the firm to meet expectations

of both entities in balanced manner.

5.2 Identify and evaluate alternative source of finance

For new product development alternative source of finance are as follows. Bank loan- Morrison is focusing on making available fresh bananas as new product in

the market. In this regard firm already make some acquisitions in past months and years.

Firm can raise bank loan and by using same can meet its needs. Interest charged on loan

is cost of this source of finance (Burritt, Schaltegger and Zvezdov, 2011). Advantage of

debt is that shareholding of existing shareholders does not get diluted in the firm. Demerit

is that in every condition it is inevitable to pay interest irrespective of profitability.

Retained earnings- It is an internal source of finance and does not have any finance cost.

Advantage of same is that Morrison does not need to bear burden of payment of finance

cost. Disadvantage is that this source of finance have finance cost.

5.3 Role of treasury management in the financing risk and control of liquidity

Treasury manager play a very important role in obtaining appropriate mix of finance.

This is because he knows that for new product development how much finance and of which

category are available. What are the payment of liabilities of the firm for upcoming years?

Hence, treasury manager is in position to determine appropriate mix of finance so that finance

cost can be minimized. Risk management and liquidity crunch are two main risk in the business

that are related to treasury management (Granlund, 2011). Relevant manager by making efforts

to receive cash as soon as possible from debtors can increase liquidity in the business. Hence, it

can be said that there is great importance of the treasury management in relation to financial risk.

TASK 6

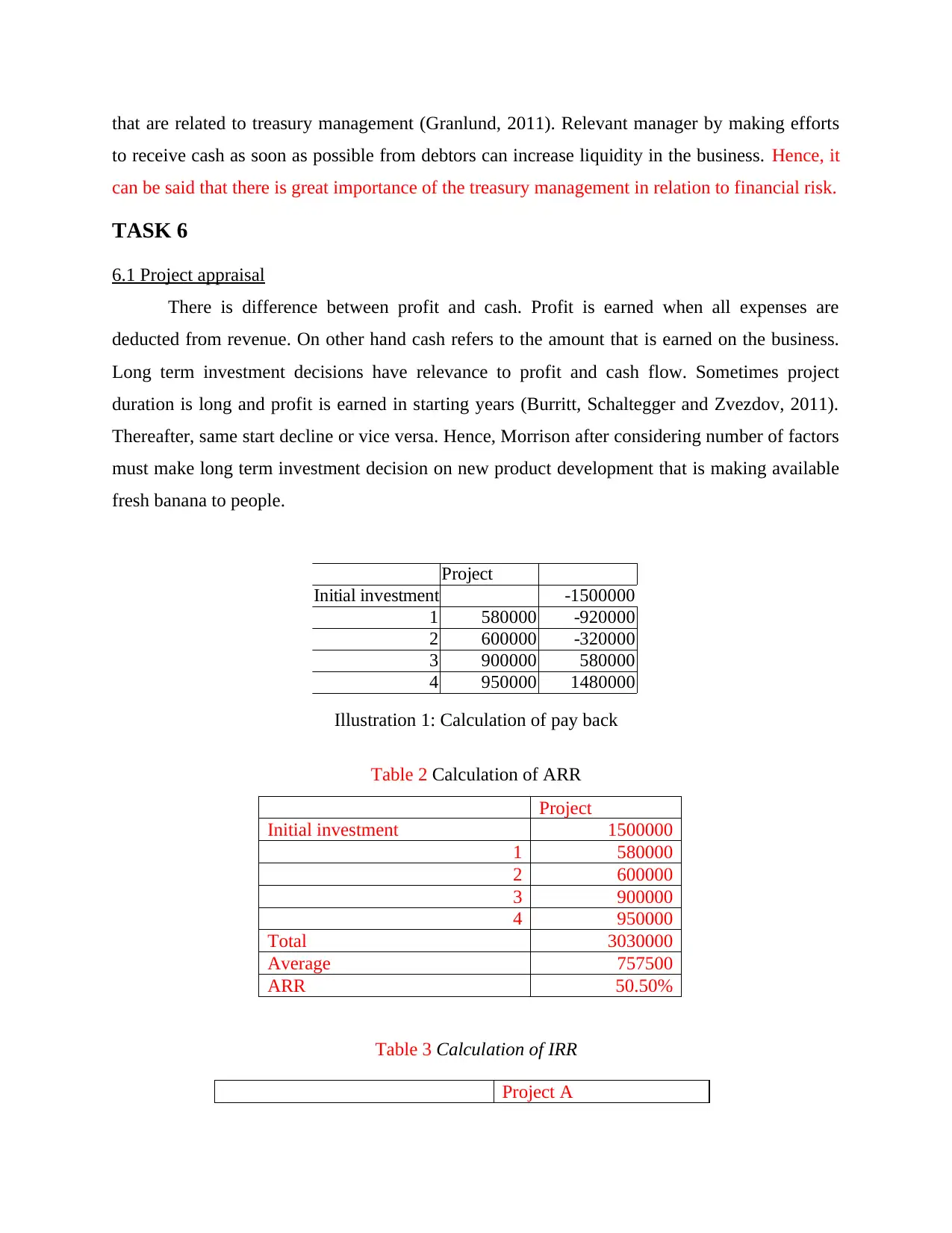

6.1 Project appraisal

There is difference between profit and cash. Profit is earned when all expenses are

deducted from revenue. On other hand cash refers to the amount that is earned on the business.

Long term investment decisions have relevance to profit and cash flow. Sometimes project

duration is long and profit is earned in starting years (Burritt, Schaltegger and Zvezdov, 2011).

Thereafter, same start decline or vice versa. Hence, Morrison after considering number of factors

must make long term investment decision on new product development that is making available

fresh banana to people.

Table 2 Calculation of ARR

Project

Initial investment 1500000

1 580000

2 600000

3 900000

4 950000

Total 3030000

Average 757500

ARR 50.50%

Table 3 Calculation of IRR

Project A

Project

Initial investment -1500000

1 580000 -920000

2 600000 -320000

3 900000 580000

4 950000 1480000

Illustration 1: Calculation of pay back

to receive cash as soon as possible from debtors can increase liquidity in the business. Hence, it

can be said that there is great importance of the treasury management in relation to financial risk.

TASK 6

6.1 Project appraisal

There is difference between profit and cash. Profit is earned when all expenses are

deducted from revenue. On other hand cash refers to the amount that is earned on the business.

Long term investment decisions have relevance to profit and cash flow. Sometimes project

duration is long and profit is earned in starting years (Burritt, Schaltegger and Zvezdov, 2011).

Thereafter, same start decline or vice versa. Hence, Morrison after considering number of factors

must make long term investment decision on new product development that is making available

fresh banana to people.

Table 2 Calculation of ARR

Project

Initial investment 1500000

1 580000

2 600000

3 900000

4 950000

Total 3030000

Average 757500

ARR 50.50%

Table 3 Calculation of IRR

Project A

Project

Initial investment -1500000

1 580000 -920000

2 600000 -320000

3 900000 580000

4 950000 1480000

Illustration 1: Calculation of pay back

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.