WM Morrison Financial Performance Analysis and Investment Advice

VerifiedAdded on 2020/02/05

|16

|5019

|262

Report

AI Summary

This report analyzes the financial performance of WM Morrison for the years 2014 and 2015. It begins with a comparative ratio analysis, examining profitability, liquidity, solvency, and efficiency. The report then comments on Morrison's business and financial structure, comparing key financial figures between the two years. It provides investment advice to potential investors and explores alternative financial sources to meet requirements. Furthermore, the report covers cash flow budgeting for Green Limited, offering recommendations for cash flow management. Finally, it delves into investment appraisal techniques using discounted and non-discounted methods, providing recommendations based on the results. The analysis includes detailed calculations, table of contents, index of tables, and illustrations to support the findings.

Financial decision making for managers

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................................................3

A. Comparative ratio analysis of Morrison for the time period for the year 2014 and 2015..........3

B. Comment on business structure and financial structure of Morrison.........................................4

C. Compare the financial figures for the year 2014 and 2015.........................................................5

D. Advice a potential investor of Morrison to invest money in the business..................................5

E. Meeting financial requirement through possible alternatives and assessing its implications.....6

F. Advice how working capital can be managed by Morrison.........................................................7

TASK 2 ................................................................................................................................................7

A. Preparation of cash flow budget.................................................................................................7

B. Make recommendations to administrate cash flow.....................................................................8

TASK 3 ..............................................................................................................................................10

A. Using discounted and non-discounted investment appraisal techniques..................................10

B. Recommendation on the basis of results identified...................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

APPENDIX........................................................................................................................................15

Index of Tables

Table 1: Comparison of financial figures of Morrison ........................................................................5

Table 2: Cash budget of Green Limited for the period of six months ending on 31st December........8

Table 3: Calculation of cash inflow of project A................................................................................10

Table 4: Calculation of cash inflow of project B...............................................................................10

Table 5: Calculation of pay back period.............................................................................................10

Table 6: Calculation of accounting rate of return...............................................................................11

Table 7: Calculation of Net present value and internal rate of return ................................................11

Illustration Index

Illustration 1: Business structure of WM Morrison..............................................................................4

2

INTRODUCTION ...............................................................................................................................3

A. Comparative ratio analysis of Morrison for the time period for the year 2014 and 2015..........3

B. Comment on business structure and financial structure of Morrison.........................................4

C. Compare the financial figures for the year 2014 and 2015.........................................................5

D. Advice a potential investor of Morrison to invest money in the business..................................5

E. Meeting financial requirement through possible alternatives and assessing its implications.....6

F. Advice how working capital can be managed by Morrison.........................................................7

TASK 2 ................................................................................................................................................7

A. Preparation of cash flow budget.................................................................................................7

B. Make recommendations to administrate cash flow.....................................................................8

TASK 3 ..............................................................................................................................................10

A. Using discounted and non-discounted investment appraisal techniques..................................10

B. Recommendation on the basis of results identified...................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

APPENDIX........................................................................................................................................15

Index of Tables

Table 1: Comparison of financial figures of Morrison ........................................................................5

Table 2: Cash budget of Green Limited for the period of six months ending on 31st December........8

Table 3: Calculation of cash inflow of project A................................................................................10

Table 4: Calculation of cash inflow of project B...............................................................................10

Table 5: Calculation of pay back period.............................................................................................10

Table 6: Calculation of accounting rate of return...............................................................................11

Table 7: Calculation of Net present value and internal rate of return ................................................11

Illustration Index

Illustration 1: Business structure of WM Morrison..............................................................................4

2

INTRODUCTION

Managers play an important role in business as they are responsible for framing policies and

taking decisions in achieving success in the market. Finance manager in an organization have the

duty to evaluate company's financial strengths and weaknesses so that effective financial decisions

can be carried out to perform better in the future. WM Morrison is the fourth largest supermarket

chain of UK which operates in the retail industry. This assignment will conduct comparative study

of financial performance of Morrison for two financial years i.e. 2014 and 2015. It will be done by

using ratio analysis techniques like profitability, solvency, liquidity and efficiency so that each and

every aspect can be examined. Moreover, cash budget will be constructed for Green Limited and

analysed to assure surplus funds every time. In the last, investment decision will be taken for

Hanley Manufacturing Ltd by using capital budgeting techniques.

TASK 1

A. Comparative ratio analysis of Morrison for the time period for the year 2014 and 2015

Profitability:

In 2015, Morrison's GM and NM have been declined from 6.07% to 4.53% and 1.35% to

adverse 4.53%. It reflects that WM Morrison do not performed well in the year 2015 because of

fewer earnings through operations. Less turnover and ineffective control over cost are the two

reasons behind decreasing profitability in 2015 (Alnaa, Adongo and Juabin, 2016).

Liquidity:

In 2015, CR remained unchanged to 0.5 while QR shows a little bit increase by 0.02 as it has

been reached to 0.18. High proportionate decrease in current assets (CA) due to having less

inventory, trade receivables and cash position as compare to proportionate reduction in current

liabilities (CL) such as payables is the reason behind such occurrence. Idle CR and QR for retail

sector is 2:1 and 1:1. It implies that Morrison is not able to meet their short term liabilities timely

(Petruzzo and et.al., 2015).

Solvency:

Debt/equity ratio has been improved from 0.53 to 0.7 while standard ratio is 0.5:1. It shows

that there is high financial risk to invest money in Morrison. It has been increased because of using

additional debt and less equity in the capital structure. Although company achieved industrial

standard but still, it must be keep in mind that very high use of equity capital also create negative

impact (Matthew, Fada and Ukonu, 2016). It is because in this situation, investors will demand

more return on their capital. Thus, the profit of less cost of debt capital is offset by increase in the

cost of equity which is not good.

3

Managers play an important role in business as they are responsible for framing policies and

taking decisions in achieving success in the market. Finance manager in an organization have the

duty to evaluate company's financial strengths and weaknesses so that effective financial decisions

can be carried out to perform better in the future. WM Morrison is the fourth largest supermarket

chain of UK which operates in the retail industry. This assignment will conduct comparative study

of financial performance of Morrison for two financial years i.e. 2014 and 2015. It will be done by

using ratio analysis techniques like profitability, solvency, liquidity and efficiency so that each and

every aspect can be examined. Moreover, cash budget will be constructed for Green Limited and

analysed to assure surplus funds every time. In the last, investment decision will be taken for

Hanley Manufacturing Ltd by using capital budgeting techniques.

TASK 1

A. Comparative ratio analysis of Morrison for the time period for the year 2014 and 2015

Profitability:

In 2015, Morrison's GM and NM have been declined from 6.07% to 4.53% and 1.35% to

adverse 4.53%. It reflects that WM Morrison do not performed well in the year 2015 because of

fewer earnings through operations. Less turnover and ineffective control over cost are the two

reasons behind decreasing profitability in 2015 (Alnaa, Adongo and Juabin, 2016).

Liquidity:

In 2015, CR remained unchanged to 0.5 while QR shows a little bit increase by 0.02 as it has

been reached to 0.18. High proportionate decrease in current assets (CA) due to having less

inventory, trade receivables and cash position as compare to proportionate reduction in current

liabilities (CL) such as payables is the reason behind such occurrence. Idle CR and QR for retail

sector is 2:1 and 1:1. It implies that Morrison is not able to meet their short term liabilities timely

(Petruzzo and et.al., 2015).

Solvency:

Debt/equity ratio has been improved from 0.53 to 0.7 while standard ratio is 0.5:1. It shows

that there is high financial risk to invest money in Morrison. It has been increased because of using

additional debt and less equity in the capital structure. Although company achieved industrial

standard but still, it must be keep in mind that very high use of equity capital also create negative

impact (Matthew, Fada and Ukonu, 2016). It is because in this situation, investors will demand

more return on their capital. Thus, the profit of less cost of debt capital is offset by increase in the

cost of equity which is not good.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency:

ATR has been increased to 1.69 times while ITR has been reduced from 20.34 to 21.26 in

2015. It is because of having declined total asset, COGS and inventory as well. It demonstrates that

Morrison is using assets efficiently to generate more revenue while inventory is not utilized in an

effective manner (Alnaa, Adongo and Juabin, 2016).

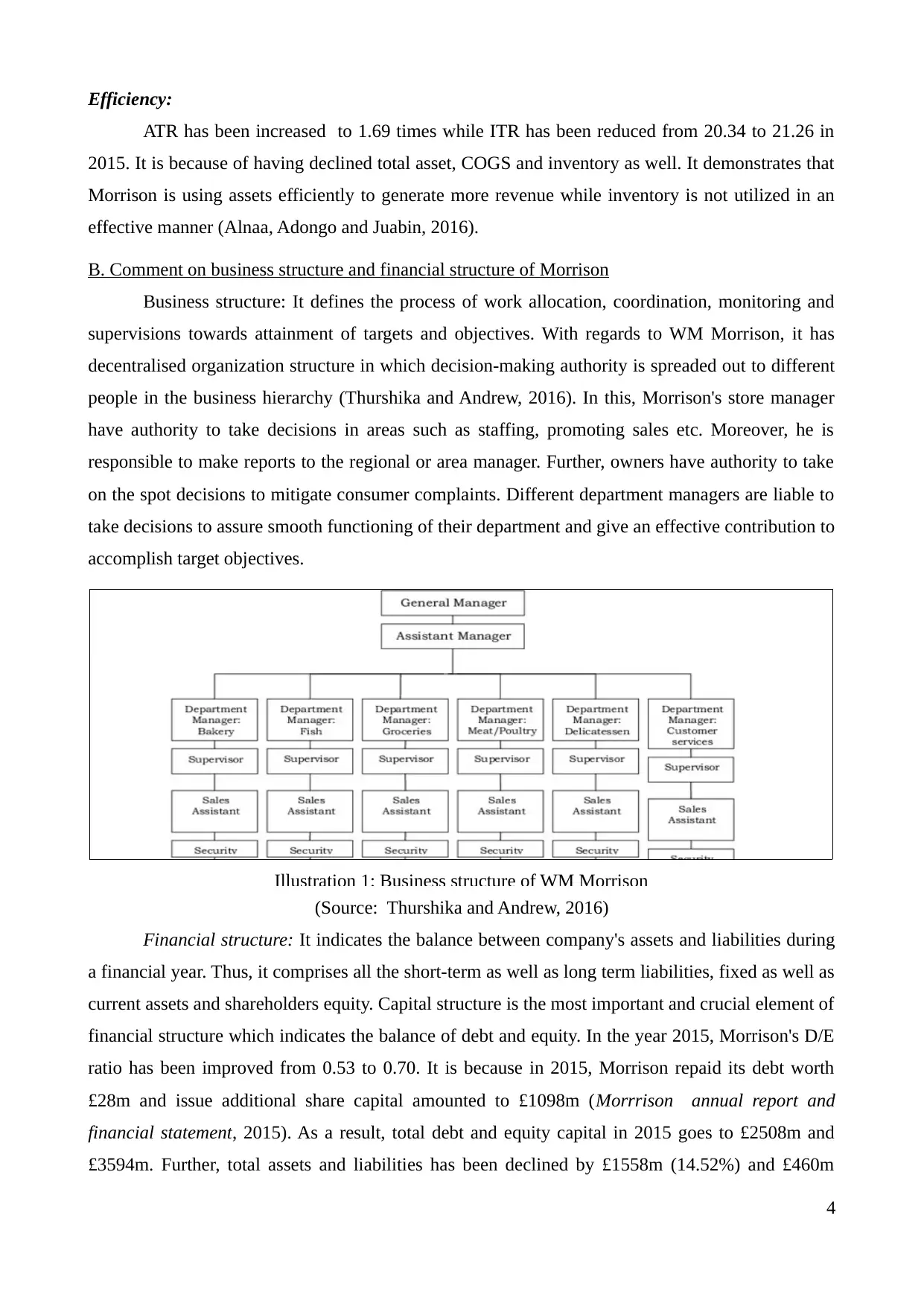

B. Comment on business structure and financial structure of Morrison

Business structure: It defines the process of work allocation, coordination, monitoring and

supervisions towards attainment of targets and objectives. With regards to WM Morrison, it has

decentralised organization structure in which decision-making authority is spreaded out to different

people in the business hierarchy (Thurshika and Andrew, 2016). In this, Morrison's store manager

have authority to take decisions in areas such as staffing, promoting sales etc. Moreover, he is

responsible to make reports to the regional or area manager. Further, owners have authority to take

on the spot decisions to mitigate consumer complaints. Different department managers are liable to

take decisions to assure smooth functioning of their department and give an effective contribution to

accomplish target objectives.

Illustration 1: Business structure of WM Morrison

(Source: Thurshika and Andrew, 2016)

Financial structure: It indicates the balance between company's assets and liabilities during

a financial year. Thus, it comprises all the short-term as well as long term liabilities, fixed as well as

current assets and shareholders equity. Capital structure is the most important and crucial element of

financial structure which indicates the balance of debt and equity. In the year 2015, Morrison's D/E

ratio has been improved from 0.53 to 0.70. It is because in 2015, Morrison repaid its debt worth

£28m and issue additional share capital amounted to £1098m (Morrrison annual report and

financial statement, 2015). As a result, total debt and equity capital in 2015 goes to £2508m and

£3594m. Further, total assets and liabilities has been declined by £1558m (14.52%) and £460m

4

ATR has been increased to 1.69 times while ITR has been reduced from 20.34 to 21.26 in

2015. It is because of having declined total asset, COGS and inventory as well. It demonstrates that

Morrison is using assets efficiently to generate more revenue while inventory is not utilized in an

effective manner (Alnaa, Adongo and Juabin, 2016).

B. Comment on business structure and financial structure of Morrison

Business structure: It defines the process of work allocation, coordination, monitoring and

supervisions towards attainment of targets and objectives. With regards to WM Morrison, it has

decentralised organization structure in which decision-making authority is spreaded out to different

people in the business hierarchy (Thurshika and Andrew, 2016). In this, Morrison's store manager

have authority to take decisions in areas such as staffing, promoting sales etc. Moreover, he is

responsible to make reports to the regional or area manager. Further, owners have authority to take

on the spot decisions to mitigate consumer complaints. Different department managers are liable to

take decisions to assure smooth functioning of their department and give an effective contribution to

accomplish target objectives.

Illustration 1: Business structure of WM Morrison

(Source: Thurshika and Andrew, 2016)

Financial structure: It indicates the balance between company's assets and liabilities during

a financial year. Thus, it comprises all the short-term as well as long term liabilities, fixed as well as

current assets and shareholders equity. Capital structure is the most important and crucial element of

financial structure which indicates the balance of debt and equity. In the year 2015, Morrison's D/E

ratio has been improved from 0.53 to 0.70. It is because in 2015, Morrison repaid its debt worth

£28m and issue additional share capital amounted to £1098m (Morrrison annual report and

financial statement, 2015). As a result, total debt and equity capital in 2015 goes to £2508m and

£3594m. Further, total assets and liabilities has been declined by £1558m (14.52%) and £460m

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

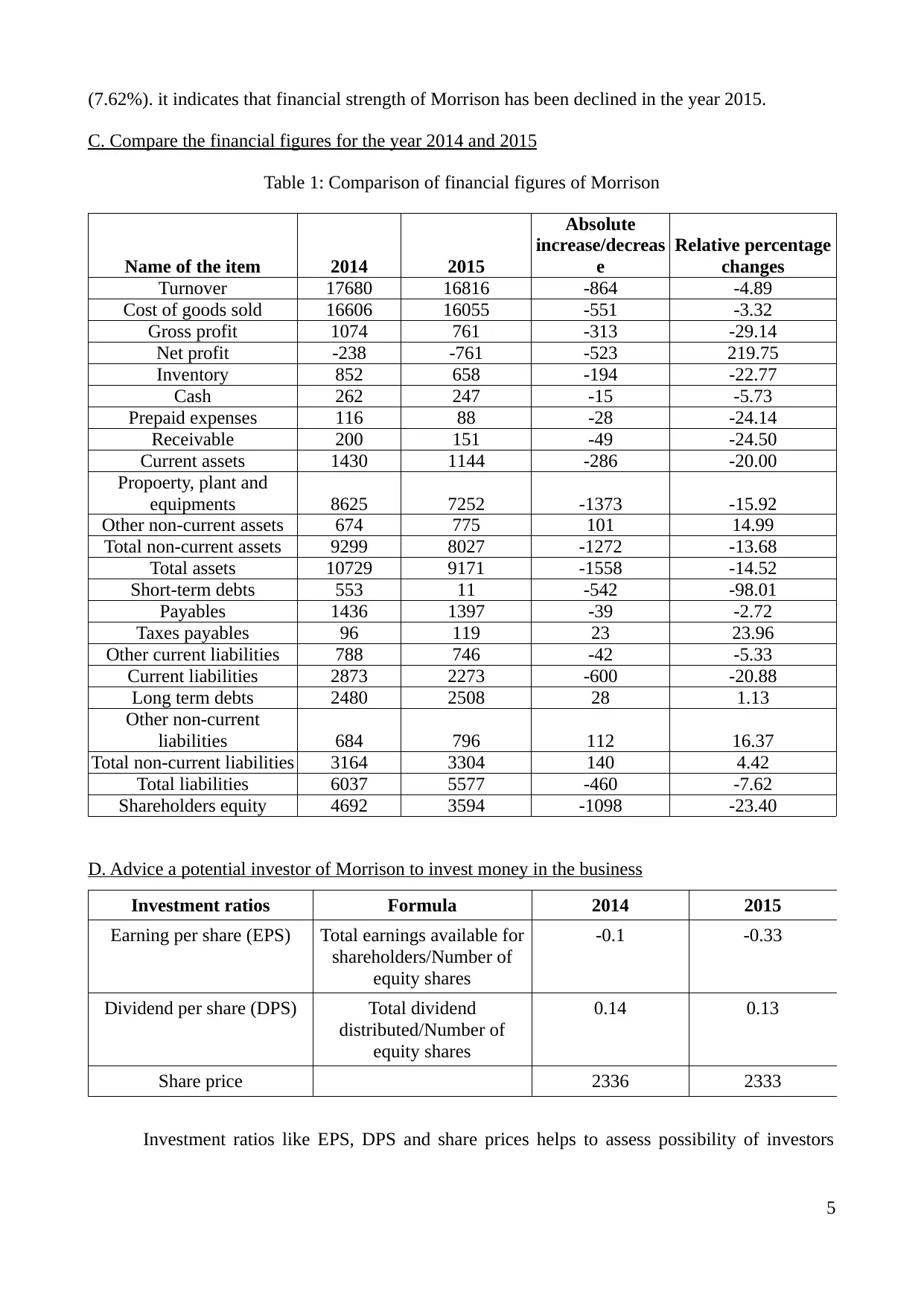

(7.62%). it indicates that financial strength of Morrison has been declined in the year 2015.

C. Compare the financial figures for the year 2014 and 2015

Table 1: Comparison of financial figures of Morrison

Name of the item 2014 2015

Absolute

increase/decreas

e

Relative percentage

changes

Turnover 17680 16816 -864 -4.89

Cost of goods sold 16606 16055 -551 -3.32

Gross profit 1074 761 -313 -29.14

Net profit -238 -761 -523 219.75

Inventory 852 658 -194 -22.77

Cash 262 247 -15 -5.73

Prepaid expenses 116 88 -28 -24.14

Receivable 200 151 -49 -24.50

Current assets 1430 1144 -286 -20.00

Propoerty, plant and

equipments 8625 7252 -1373 -15.92

Other non-current assets 674 775 101 14.99

Total non-current assets 9299 8027 -1272 -13.68

Total assets 10729 9171 -1558 -14.52

Short-term debts 553 11 -542 -98.01

Payables 1436 1397 -39 -2.72

Taxes payables 96 119 23 23.96

Other current liabilities 788 746 -42 -5.33

Current liabilities 2873 2273 -600 -20.88

Long term debts 2480 2508 28 1.13

Other non-current

liabilities 684 796 112 16.37

Total non-current liabilities 3164 3304 140 4.42

Total liabilities 6037 5577 -460 -7.62

Shareholders equity 4692 3594 -1098 -23.40

D. Advice a potential investor of Morrison to invest money in the business

Investment ratios Formula 2014 2015

Earning per share (EPS) Total earnings available for

shareholders/Number of

equity shares

-0.1 -0.33

Dividend per share (DPS) Total dividend

distributed/Number of

equity shares

0.14 0.13

Share price 2336 2333

Investment ratios like EPS, DPS and share prices helps to assess possibility of investors

5

C. Compare the financial figures for the year 2014 and 2015

Table 1: Comparison of financial figures of Morrison

Name of the item 2014 2015

Absolute

increase/decreas

e

Relative percentage

changes

Turnover 17680 16816 -864 -4.89

Cost of goods sold 16606 16055 -551 -3.32

Gross profit 1074 761 -313 -29.14

Net profit -238 -761 -523 219.75

Inventory 852 658 -194 -22.77

Cash 262 247 -15 -5.73

Prepaid expenses 116 88 -28 -24.14

Receivable 200 151 -49 -24.50

Current assets 1430 1144 -286 -20.00

Propoerty, plant and

equipments 8625 7252 -1373 -15.92

Other non-current assets 674 775 101 14.99

Total non-current assets 9299 8027 -1272 -13.68

Total assets 10729 9171 -1558 -14.52

Short-term debts 553 11 -542 -98.01

Payables 1436 1397 -39 -2.72

Taxes payables 96 119 23 23.96

Other current liabilities 788 746 -42 -5.33

Current liabilities 2873 2273 -600 -20.88

Long term debts 2480 2508 28 1.13

Other non-current

liabilities 684 796 112 16.37

Total non-current liabilities 3164 3304 140 4.42

Total liabilities 6037 5577 -460 -7.62

Shareholders equity 4692 3594 -1098 -23.40

D. Advice a potential investor of Morrison to invest money in the business

Investment ratios Formula 2014 2015

Earning per share (EPS) Total earnings available for

shareholders/Number of

equity shares

-0.1 -0.33

Dividend per share (DPS) Total dividend

distributed/Number of

equity shares

0.14 0.13

Share price 2336 2333

Investment ratios like EPS, DPS and share prices helps to assess possibility of investors

5

return that they can acquire on their invested capital. EPS indicates per share earnings that investors

received on their existing capital. WM Morrison's EPS shows an adverse return which is inclined

from -0.1 to -0.33 in 2015. It implies that investors are incurring loss on their invested funds. While,

DPS has been declined from 0.14 to 0.13 because of declined net earnings. It exhibit that equity

capitalists are not getting adequate return on their money invested (Pradhan and Das, 2016). In

addition to this, share price of WM Morrison has been reduced from 2336 to 2333 in 2015. All the

results demonstrates that company is not providing sufficient amount of return to the equity holders

and they are bearing negative return due to business loss. Henceforth, it can be advised that

potential investors should not invest capital in the Morrison because of greater risk and possibility

of negative return.

E. Meeting financial requirement through possible alternatives and assessing its implications

Additional financial requirement of £50000 can be complied through following financial

sources, described below:

Equity capital: WM Morrison can issue additional equity shares and thereby sell ownership

to the potential investors to generate funds in required quantity (Kumar and Mishra, 2016). Its good

thing is firm is not obliged to make regular dividend payment to the investors but still, equity

holders can take part in the business decisions which is its disadvantage.

Bank loan: Money can be raised through taking bank loan by fulfilling all the legal

formalities required by the bank like collateral security. Tax advantage and no dilution of

controlling power are its benefits but regular payment of fixed instalments whether Morrison have

profit or loss are the drawbacks.

Bank overdraft: It is a permission granted by bank to withdraw high amount from the firm's

account than available balance (Ibrahim and Ibrahim, 2015). Satisfying urgent financial need and

tax advantage are the advantage whereas high rate of interest payment as compare to loan are the

negative aspects.

Retained profits: Profit that remains after meeting all the business expenses are called

retained earnings. Through ploughing back of returns, Morrison can meet its long term financial

need. No financial cost is there but still, it comprises opportunity cost which means that if company

invested its earnings in alternatives than it can generate return on it (Plank, 2015).

Factoring: It provide assistance to Morrison to get earlier payments of debtors invoices

before maturity date. Through this, company can meet its urgent and medium-term financial need

which is its benefit. However, factoring company discounted invoice at some nominal charges

which is its cost.

6

received on their existing capital. WM Morrison's EPS shows an adverse return which is inclined

from -0.1 to -0.33 in 2015. It implies that investors are incurring loss on their invested funds. While,

DPS has been declined from 0.14 to 0.13 because of declined net earnings. It exhibit that equity

capitalists are not getting adequate return on their money invested (Pradhan and Das, 2016). In

addition to this, share price of WM Morrison has been reduced from 2336 to 2333 in 2015. All the

results demonstrates that company is not providing sufficient amount of return to the equity holders

and they are bearing negative return due to business loss. Henceforth, it can be advised that

potential investors should not invest capital in the Morrison because of greater risk and possibility

of negative return.

E. Meeting financial requirement through possible alternatives and assessing its implications

Additional financial requirement of £50000 can be complied through following financial

sources, described below:

Equity capital: WM Morrison can issue additional equity shares and thereby sell ownership

to the potential investors to generate funds in required quantity (Kumar and Mishra, 2016). Its good

thing is firm is not obliged to make regular dividend payment to the investors but still, equity

holders can take part in the business decisions which is its disadvantage.

Bank loan: Money can be raised through taking bank loan by fulfilling all the legal

formalities required by the bank like collateral security. Tax advantage and no dilution of

controlling power are its benefits but regular payment of fixed instalments whether Morrison have

profit or loss are the drawbacks.

Bank overdraft: It is a permission granted by bank to withdraw high amount from the firm's

account than available balance (Ibrahim and Ibrahim, 2015). Satisfying urgent financial need and

tax advantage are the advantage whereas high rate of interest payment as compare to loan are the

negative aspects.

Retained profits: Profit that remains after meeting all the business expenses are called

retained earnings. Through ploughing back of returns, Morrison can meet its long term financial

need. No financial cost is there but still, it comprises opportunity cost which means that if company

invested its earnings in alternatives than it can generate return on it (Plank, 2015).

Factoring: It provide assistance to Morrison to get earlier payments of debtors invoices

before maturity date. Through this, company can meet its urgent and medium-term financial need

which is its benefit. However, factoring company discounted invoice at some nominal charges

which is its cost.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above, bank loan and retained profits are consider more appropriate source to meet

Morrison's financial requirement.

F. Advice how working capital can be managed by Morrison

Working capital (WC): The financial need which Morrison require to run its routine

functions is called WC. Morrison will require sufficient WC to purchase goods and pay expenses

like salary, wages, rent, printing, electricity bill etc. In the present competitive age, it is essential for

the company to assure adequate funds available to face possible threats and hazard free operations.

Ways to manage working capital:

Morrison can enlarge their cash inflow by getting higher turnover from £16816m. It can be

done by delivering effective services to the customers and meet their expectations timely.

It should also control spendings so as to decline their cash disbursement in various business

activities like controlling COGS by acquiring quality material at cheaper price and recruiting

skilled employees at less wages rate (Bartram, 2013).

Regularly monitoring of business functions by the managers is also an effective way to track

expenditures and maintain it up to the maximum level of set targets. By this, Morrison can

control their indirect cost like administration, selling and distribution expenses.

Optimum utilization of all the financial sources also provide assistance to decline cost and

maximize net cash funds available (Morgan, 2012).

Improving ITR from 21.26 times enable Morrison to getting prompt payments from the

debtors which helps to increase cash inflow.

CR of 0.5 and QR of 0.18 can be improved by increasing CA like debtors, inventory and

cash and controlling CL like payables. This in turn, Morrison can increase their WC to a

desired extent (11 ways to manage working capital, n.d.).

Enlarging profitability from GM of 4.53% and getting positive net earnings are also the

ways to ensure large WC availability in the Morrison.

TASK 2

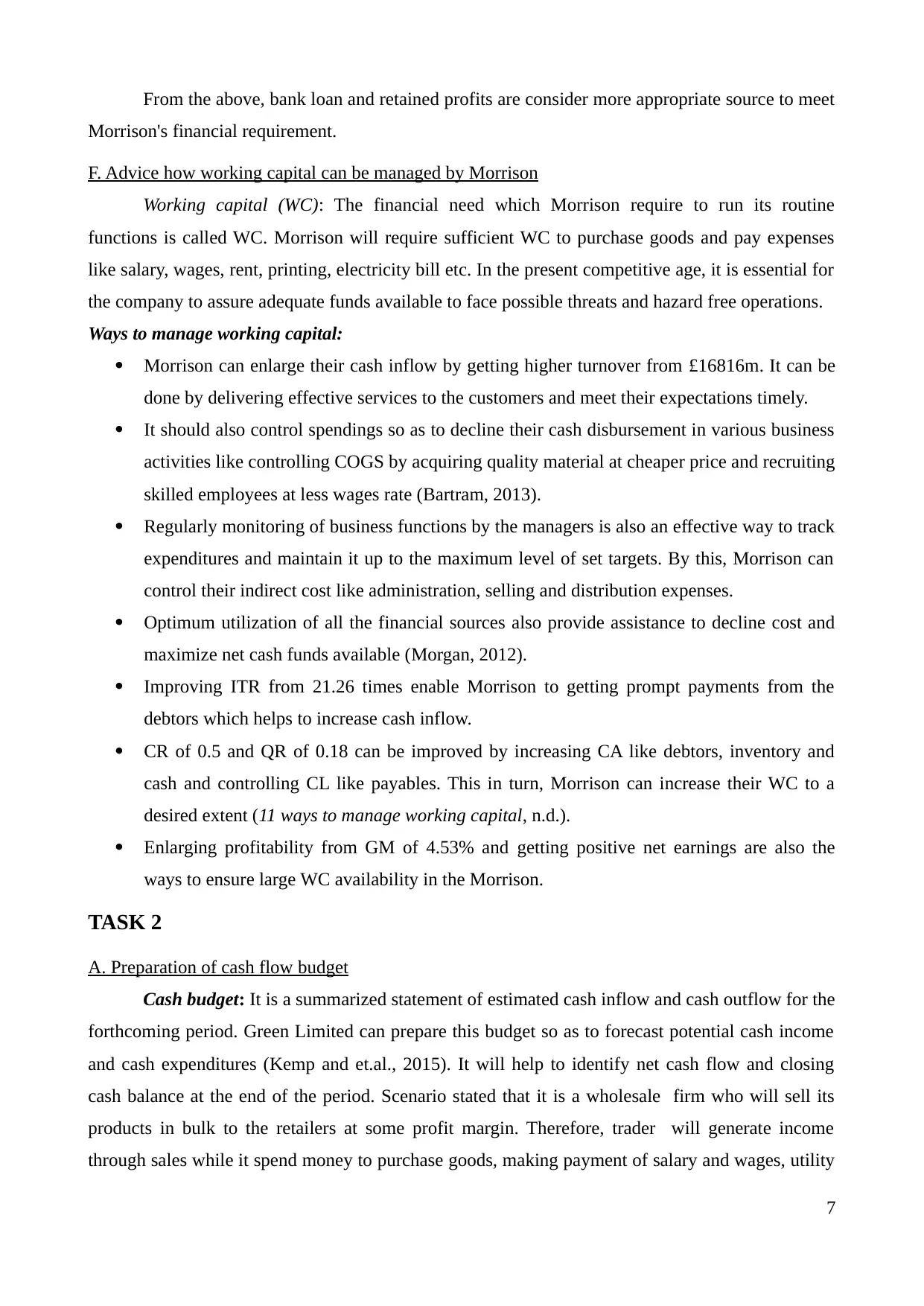

A. Preparation of cash flow budget

Cash budget: It is a summarized statement of estimated cash inflow and cash outflow for the

forthcoming period. Green Limited can prepare this budget so as to forecast potential cash income

and cash expenditures (Kemp and et.al., 2015). It will help to identify net cash flow and closing

cash balance at the end of the period. Scenario stated that it is a wholesale firm who will sell its

products in bulk to the retailers at some profit margin. Therefore, trader will generate income

through sales while it spend money to purchase goods, making payment of salary and wages, utility

7

Morrison's financial requirement.

F. Advice how working capital can be managed by Morrison

Working capital (WC): The financial need which Morrison require to run its routine

functions is called WC. Morrison will require sufficient WC to purchase goods and pay expenses

like salary, wages, rent, printing, electricity bill etc. In the present competitive age, it is essential for

the company to assure adequate funds available to face possible threats and hazard free operations.

Ways to manage working capital:

Morrison can enlarge their cash inflow by getting higher turnover from £16816m. It can be

done by delivering effective services to the customers and meet their expectations timely.

It should also control spendings so as to decline their cash disbursement in various business

activities like controlling COGS by acquiring quality material at cheaper price and recruiting

skilled employees at less wages rate (Bartram, 2013).

Regularly monitoring of business functions by the managers is also an effective way to track

expenditures and maintain it up to the maximum level of set targets. By this, Morrison can

control their indirect cost like administration, selling and distribution expenses.

Optimum utilization of all the financial sources also provide assistance to decline cost and

maximize net cash funds available (Morgan, 2012).

Improving ITR from 21.26 times enable Morrison to getting prompt payments from the

debtors which helps to increase cash inflow.

CR of 0.5 and QR of 0.18 can be improved by increasing CA like debtors, inventory and

cash and controlling CL like payables. This in turn, Morrison can increase their WC to a

desired extent (11 ways to manage working capital, n.d.).

Enlarging profitability from GM of 4.53% and getting positive net earnings are also the

ways to ensure large WC availability in the Morrison.

TASK 2

A. Preparation of cash flow budget

Cash budget: It is a summarized statement of estimated cash inflow and cash outflow for the

forthcoming period. Green Limited can prepare this budget so as to forecast potential cash income

and cash expenditures (Kemp and et.al., 2015). It will help to identify net cash flow and closing

cash balance at the end of the period. Scenario stated that it is a wholesale firm who will sell its

products in bulk to the retailers at some profit margin. Therefore, trader will generate income

through sales while it spend money to purchase goods, making payment of salary and wages, utility

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and other capital expenses. Cash budget of Green Limited is constructed below:

Table 2: Cash budget of Green Limited for the period of six months ending on 31st December

Particulars July August September October November December

Cash inflow

Sales 106000 114000 118000 124000 104000 96000

Total 106000 114000 118000 124000 104000 96000

Cash outflow

Cost of goods sold 64000 64000 66000 70000 59000 54000

Salaries and wages 20000 20000 20000 20000 20000 20000

Other overheads 4000 4000 4000 4000 4000 4000

Electricity 20000 34000

New delivery truck 25000

Bank loan 135000

Total 88000 88000 135000 94000 218000 112000

Net cash flow (NCF) 18000 26000 -17000 30000 -114000 -16000

Opening bank balance 90000 108000 134000 117000 147000 33000

Closing bank balance 108000 134000 117000 147000 33000 17000

Working note:

Green Ltd, is making sales on credit for one month means that company will generate cash

in the next month.

Cost of Goods sold also has been paid in next month from the period in which goods has

been acquired.

Green Ltd incurred capital expenses for delivery of new truck and debt payment worth

£25000 and £135000 respectively.

B. Make recommendations to administrate cash flow

Budget indicates that Green Ltd (GL) will have unfavourable NCF in September, November

and December. It demonstrates that in such period, cash inflow (CI) is comparatively lower than

cash used in the operations. In September, turnover has been inclined by only £4000 however, at the

same time, Green Ltd, incurred a heavy expenditure to buy a delivery van worth £25000. On the

other hand, in November and December firm's turnover has been declined by £20000 and £8000

respectively. While, the rate of decline in COGS is comparatively less as it has been reduced by

8

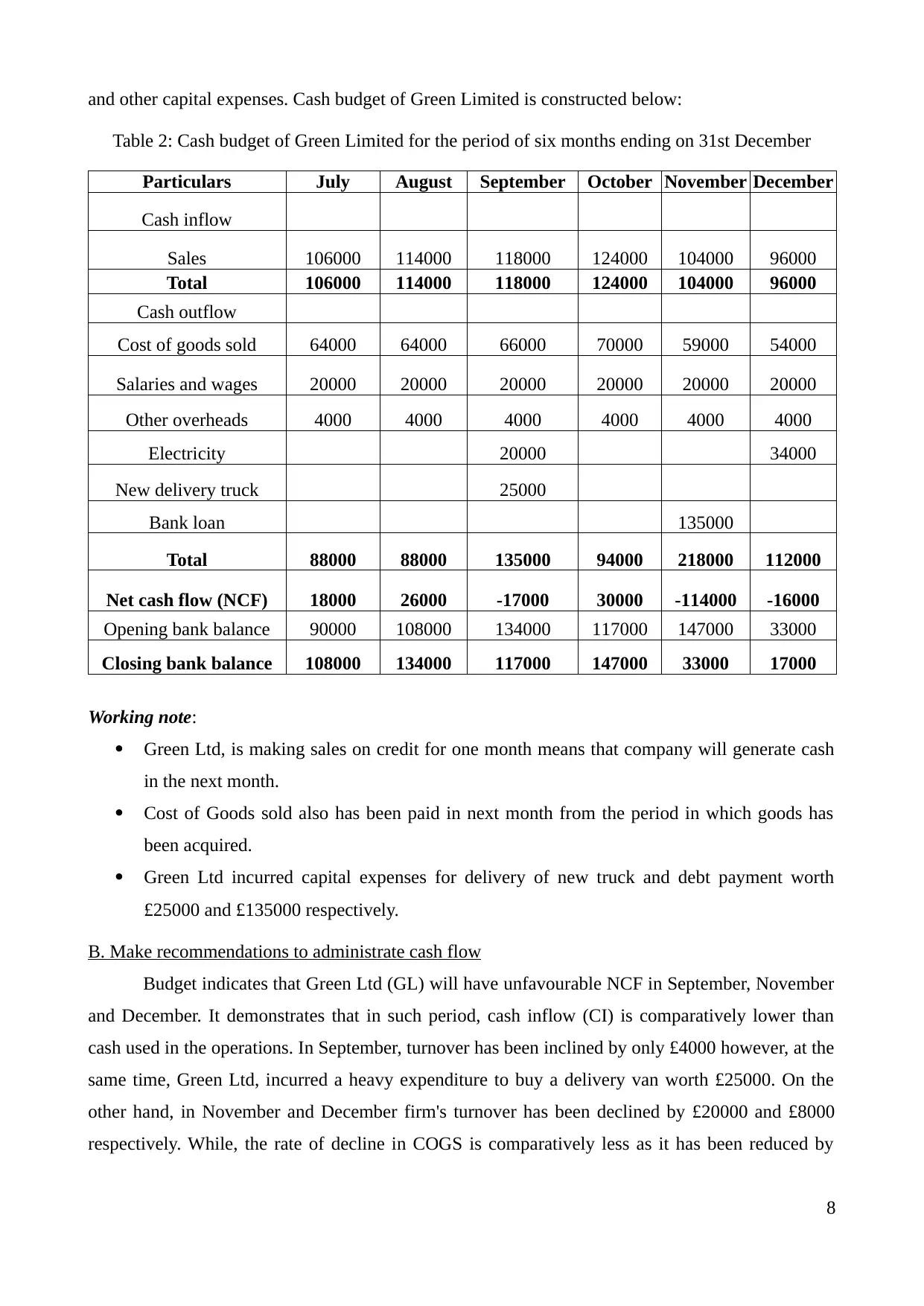

Table 2: Cash budget of Green Limited for the period of six months ending on 31st December

Particulars July August September October November December

Cash inflow

Sales 106000 114000 118000 124000 104000 96000

Total 106000 114000 118000 124000 104000 96000

Cash outflow

Cost of goods sold 64000 64000 66000 70000 59000 54000

Salaries and wages 20000 20000 20000 20000 20000 20000

Other overheads 4000 4000 4000 4000 4000 4000

Electricity 20000 34000

New delivery truck 25000

Bank loan 135000

Total 88000 88000 135000 94000 218000 112000

Net cash flow (NCF) 18000 26000 -17000 30000 -114000 -16000

Opening bank balance 90000 108000 134000 117000 147000 33000

Closing bank balance 108000 134000 117000 147000 33000 17000

Working note:

Green Ltd, is making sales on credit for one month means that company will generate cash

in the next month.

Cost of Goods sold also has been paid in next month from the period in which goods has

been acquired.

Green Ltd incurred capital expenses for delivery of new truck and debt payment worth

£25000 and £135000 respectively.

B. Make recommendations to administrate cash flow

Budget indicates that Green Ltd (GL) will have unfavourable NCF in September, November

and December. It demonstrates that in such period, cash inflow (CI) is comparatively lower than

cash used in the operations. In September, turnover has been inclined by only £4000 however, at the

same time, Green Ltd, incurred a heavy expenditure to buy a delivery van worth £25000. On the

other hand, in November and December firm's turnover has been declined by £20000 and £8000

respectively. While, the rate of decline in COGS is comparatively less as it has been reduced by

8

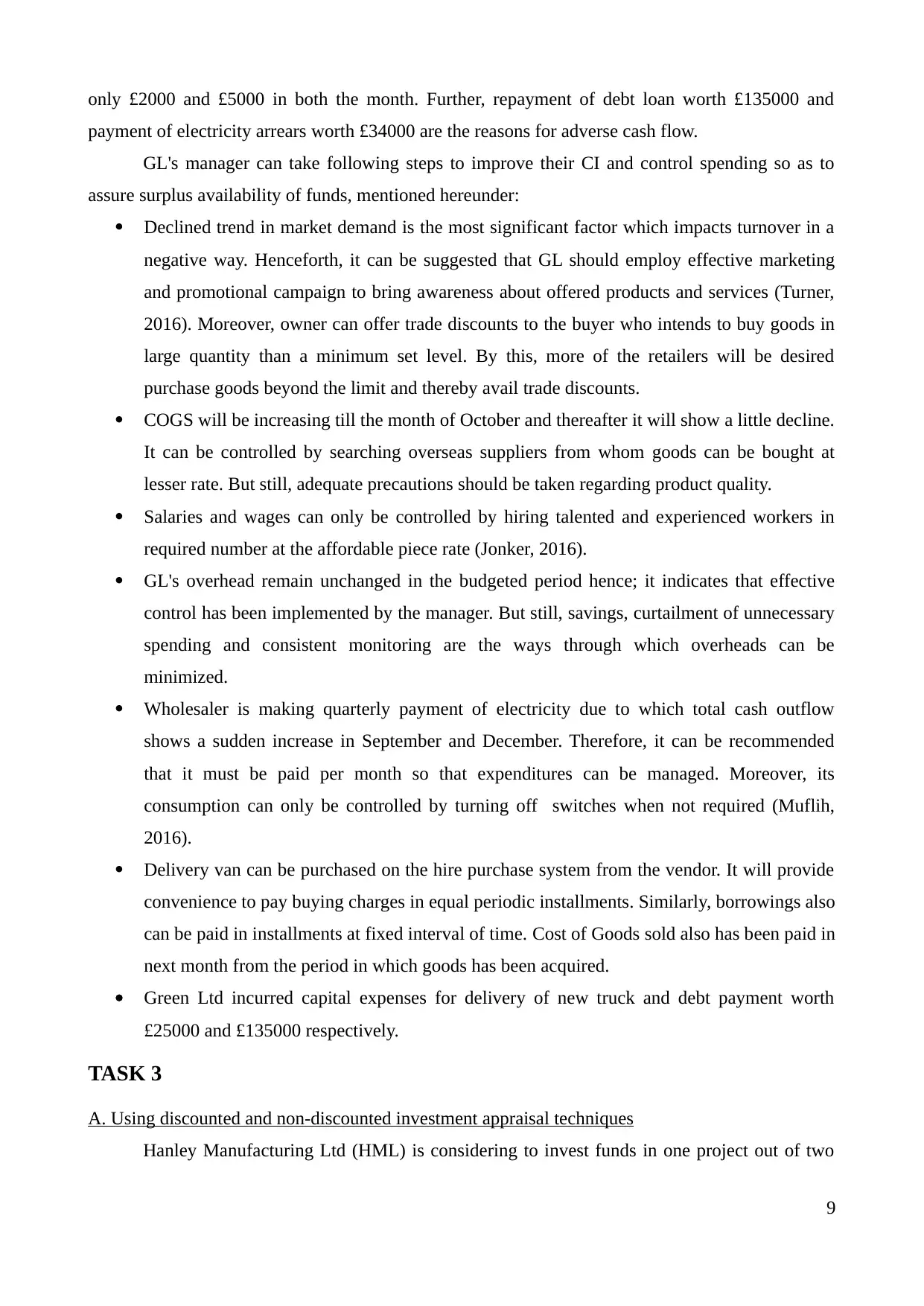

only £2000 and £5000 in both the month. Further, repayment of debt loan worth £135000 and

payment of electricity arrears worth £34000 are the reasons for adverse cash flow.

GL's manager can take following steps to improve their CI and control spending so as to

assure surplus availability of funds, mentioned hereunder:

Declined trend in market demand is the most significant factor which impacts turnover in a

negative way. Henceforth, it can be suggested that GL should employ effective marketing

and promotional campaign to bring awareness about offered products and services (Turner,

2016). Moreover, owner can offer trade discounts to the buyer who intends to buy goods in

large quantity than a minimum set level. By this, more of the retailers will be desired

purchase goods beyond the limit and thereby avail trade discounts.

COGS will be increasing till the month of October and thereafter it will show a little decline.

It can be controlled by searching overseas suppliers from whom goods can be bought at

lesser rate. But still, adequate precautions should be taken regarding product quality.

Salaries and wages can only be controlled by hiring talented and experienced workers in

required number at the affordable piece rate (Jonker, 2016).

GL's overhead remain unchanged in the budgeted period hence; it indicates that effective

control has been implemented by the manager. But still, savings, curtailment of unnecessary

spending and consistent monitoring are the ways through which overheads can be

minimized.

Wholesaler is making quarterly payment of electricity due to which total cash outflow

shows a sudden increase in September and December. Therefore, it can be recommended

that it must be paid per month so that expenditures can be managed. Moreover, its

consumption can only be controlled by turning off switches when not required (Muflih,

2016).

Delivery van can be purchased on the hire purchase system from the vendor. It will provide

convenience to pay buying charges in equal periodic installments. Similarly, borrowings also

can be paid in installments at fixed interval of time. Cost of Goods sold also has been paid in

next month from the period in which goods has been acquired.

Green Ltd incurred capital expenses for delivery of new truck and debt payment worth

£25000 and £135000 respectively.

TASK 3

A. Using discounted and non-discounted investment appraisal techniques

Hanley Manufacturing Ltd (HML) is considering to invest funds in one project out of two

9

payment of electricity arrears worth £34000 are the reasons for adverse cash flow.

GL's manager can take following steps to improve their CI and control spending so as to

assure surplus availability of funds, mentioned hereunder:

Declined trend in market demand is the most significant factor which impacts turnover in a

negative way. Henceforth, it can be suggested that GL should employ effective marketing

and promotional campaign to bring awareness about offered products and services (Turner,

2016). Moreover, owner can offer trade discounts to the buyer who intends to buy goods in

large quantity than a minimum set level. By this, more of the retailers will be desired

purchase goods beyond the limit and thereby avail trade discounts.

COGS will be increasing till the month of October and thereafter it will show a little decline.

It can be controlled by searching overseas suppliers from whom goods can be bought at

lesser rate. But still, adequate precautions should be taken regarding product quality.

Salaries and wages can only be controlled by hiring talented and experienced workers in

required number at the affordable piece rate (Jonker, 2016).

GL's overhead remain unchanged in the budgeted period hence; it indicates that effective

control has been implemented by the manager. But still, savings, curtailment of unnecessary

spending and consistent monitoring are the ways through which overheads can be

minimized.

Wholesaler is making quarterly payment of electricity due to which total cash outflow

shows a sudden increase in September and December. Therefore, it can be recommended

that it must be paid per month so that expenditures can be managed. Moreover, its

consumption can only be controlled by turning off switches when not required (Muflih,

2016).

Delivery van can be purchased on the hire purchase system from the vendor. It will provide

convenience to pay buying charges in equal periodic installments. Similarly, borrowings also

can be paid in installments at fixed interval of time. Cost of Goods sold also has been paid in

next month from the period in which goods has been acquired.

Green Ltd incurred capital expenses for delivery of new truck and debt payment worth

£25000 and £135000 respectively.

TASK 3

A. Using discounted and non-discounted investment appraisal techniques

Hanley Manufacturing Ltd (HML) is considering to invest funds in one project out of two

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

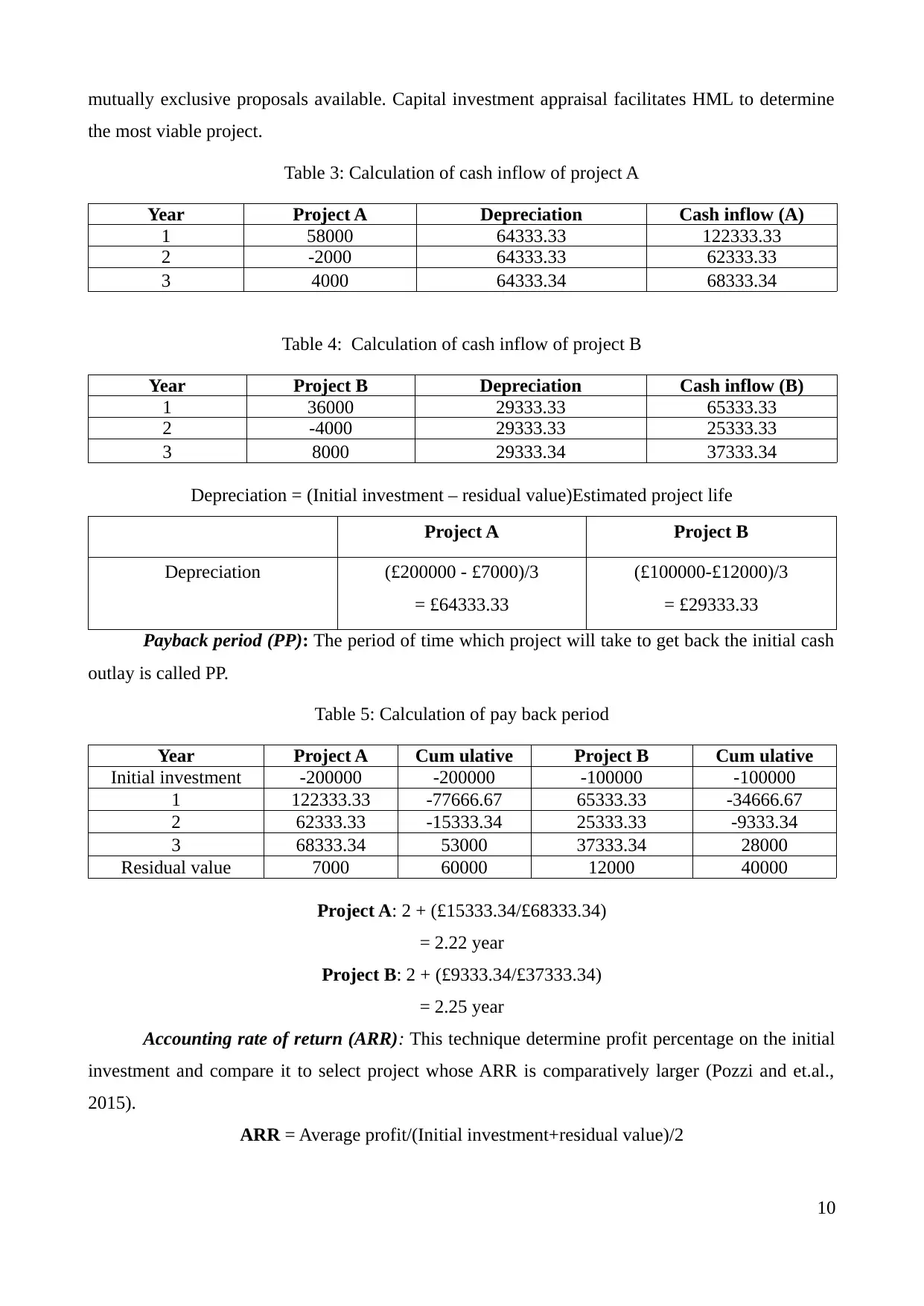

mutually exclusive proposals available. Capital investment appraisal facilitates HML to determine

the most viable project.

Table 3: Calculation of cash inflow of project A

Year Project A Depreciation Cash inflow (A)

1 58000 64333.33 122333.33

2 -2000 64333.33 62333.33

3 4000 64333.34 68333.34

Table 4: Calculation of cash inflow of project B

Year Project B Depreciation Cash inflow (B)

1 36000 29333.33 65333.33

2 -4000 29333.33 25333.33

3 8000 29333.34 37333.34

Depreciation = (Initial investment – residual value)Estimated project life

Project A Project B

Depreciation (£200000 - £7000)/3

= £64333.33

(£100000-£12000)/3

= £29333.33

Payback period (PP): The period of time which project will take to get back the initial cash

outlay is called PP.

Table 5: Calculation of pay back period

Year Project A Cum ulative Project B Cum ulative

Initial investment -200000 -200000 -100000 -100000

1 122333.33 -77666.67 65333.33 -34666.67

2 62333.33 -15333.34 25333.33 -9333.34

3 68333.34 53000 37333.34 28000

Residual value 7000 60000 12000 40000

Project A: 2 + (£15333.34/£68333.34)

= 2.22 year

Project B: 2 + (£9333.34/£37333.34)

= 2.25 year

Accounting rate of return (ARR): This technique determine profit percentage on the initial

investment and compare it to select project whose ARR is comparatively larger (Pozzi and et.al.,

2015).

ARR = Average profit/(Initial investment+residual value)/2

10

the most viable project.

Table 3: Calculation of cash inflow of project A

Year Project A Depreciation Cash inflow (A)

1 58000 64333.33 122333.33

2 -2000 64333.33 62333.33

3 4000 64333.34 68333.34

Table 4: Calculation of cash inflow of project B

Year Project B Depreciation Cash inflow (B)

1 36000 29333.33 65333.33

2 -4000 29333.33 25333.33

3 8000 29333.34 37333.34

Depreciation = (Initial investment – residual value)Estimated project life

Project A Project B

Depreciation (£200000 - £7000)/3

= £64333.33

(£100000-£12000)/3

= £29333.33

Payback period (PP): The period of time which project will take to get back the initial cash

outlay is called PP.

Table 5: Calculation of pay back period

Year Project A Cum ulative Project B Cum ulative

Initial investment -200000 -200000 -100000 -100000

1 122333.33 -77666.67 65333.33 -34666.67

2 62333.33 -15333.34 25333.33 -9333.34

3 68333.34 53000 37333.34 28000

Residual value 7000 60000 12000 40000

Project A: 2 + (£15333.34/£68333.34)

= 2.22 year

Project B: 2 + (£9333.34/£37333.34)

= 2.25 year

Accounting rate of return (ARR): This technique determine profit percentage on the initial

investment and compare it to select project whose ARR is comparatively larger (Pozzi and et.al.,

2015).

ARR = Average profit/(Initial investment+residual value)/2

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 6: Calculation of accounting rate of return

Year Project A Project B

1 58000 36000

2 -2000 -4000

3 4000 8000

Total profit 60000 40000

Average profit 20000 13333.33

Average investment 103500 56000

ARR 19.32% 23.81%

Net present value (NPV): This method evaluates net cash flow whether excess or shortfall

after meeting all the financial obligations regarding the project (Lakew and Rao, 2015).

Internal rate of return (IRR): This method evaluate project efficiency by determining the

discount rate at which project will have value of zero NPV (Pozzi and et.al., 2015).

Table 7: Calculation of Net present value and internal rate of return

Year Project A Project B

DV of £1

@10%

Present

value (A)

Present

value (B)

Initial

investment -200000 -100000 1 -200000 -100000

1 122333.33 65333.33 0.9091 111212.12 59393.94

2 62333.33 25333.33 0.8264 51515.15 20936.64

3 68333.34 37333.34 0.7513 51339.85 28049.09

Residual value 7000 12000 0.7513 5259.10 9015.60

IRR 15.81% 19.62% NPV 19326.22 17395.26

B. Recommendation on the basis of results identified

After taking into account the results, it becomes clear that project A is more viable

investment proposal. It is because according to the decisions rule of PP, shorter PP must be selected

by HML and in the case of above two projects, PP of project A is 2.22 year less than those of B to

2.25 year. It demonstrates that it will recover its initial cash outflow earlier. On the contrary, its

ARR is comparatively lower to 19.32% whereas in project B, it is 23.81%. As per this, project B is

more suitable but still, due to its limitation of considering profit rather than cash flows and avoiding

time value of money, it can't be said that it is more viable project (Götze, Northcott and Schuster,

2015).

As per discounted techniques, NPV and IRR reflects conflicting results because IRR

suggests that project B is more profitable because of higher IRR of 19.62% whilst NPV indicates

that project A is more suitable because of greater NPV of £19326.22. The reasons for such

contradicting results is both the projects have different cash flow pattern (Alkaraan, 2015). Out of

both discounted tools, NPV is consider more better technique because it determine net cash flow by

11

Year Project A Project B

1 58000 36000

2 -2000 -4000

3 4000 8000

Total profit 60000 40000

Average profit 20000 13333.33

Average investment 103500 56000

ARR 19.32% 23.81%

Net present value (NPV): This method evaluates net cash flow whether excess or shortfall

after meeting all the financial obligations regarding the project (Lakew and Rao, 2015).

Internal rate of return (IRR): This method evaluate project efficiency by determining the

discount rate at which project will have value of zero NPV (Pozzi and et.al., 2015).

Table 7: Calculation of Net present value and internal rate of return

Year Project A Project B

DV of £1

@10%

Present

value (A)

Present

value (B)

Initial

investment -200000 -100000 1 -200000 -100000

1 122333.33 65333.33 0.9091 111212.12 59393.94

2 62333.33 25333.33 0.8264 51515.15 20936.64

3 68333.34 37333.34 0.7513 51339.85 28049.09

Residual value 7000 12000 0.7513 5259.10 9015.60

IRR 15.81% 19.62% NPV 19326.22 17395.26

B. Recommendation on the basis of results identified

After taking into account the results, it becomes clear that project A is more viable

investment proposal. It is because according to the decisions rule of PP, shorter PP must be selected

by HML and in the case of above two projects, PP of project A is 2.22 year less than those of B to

2.25 year. It demonstrates that it will recover its initial cash outflow earlier. On the contrary, its

ARR is comparatively lower to 19.32% whereas in project B, it is 23.81%. As per this, project B is

more suitable but still, due to its limitation of considering profit rather than cash flows and avoiding

time value of money, it can't be said that it is more viable project (Götze, Northcott and Schuster,

2015).

As per discounted techniques, NPV and IRR reflects conflicting results because IRR

suggests that project B is more profitable because of higher IRR of 19.62% whilst NPV indicates

that project A is more suitable because of greater NPV of £19326.22. The reasons for such

contradicting results is both the projects have different cash flow pattern (Alkaraan, 2015). Out of

both discounted tools, NPV is consider more better technique because it determine net cash flow by

11

taking into account true value of money. Therefore, it is clear that project A is more viable because

there is a chance of having greater NPV worth £19326.22.

CONCLUSION

From the report, it can be concluded that WM Morrison financial performance has been

decreased in 2015. Therefore, it is essential for the manager to employ some strategic and tactical

decisions and policies to perform better in future. Middle part of the report concluded GL can assure

adequate surplus of cash funds by preparation and analysis of cash budget. Through this, it can

minimize spendings and maximise earnings to achieve business targets. While, capital budgeting

methods concluded that NPV is the most superior method henceforth, HML should select project A.

12

there is a chance of having greater NPV worth £19326.22.

CONCLUSION

From the report, it can be concluded that WM Morrison financial performance has been

decreased in 2015. Therefore, it is essential for the manager to employ some strategic and tactical

decisions and policies to perform better in future. Middle part of the report concluded GL can assure

adequate surplus of cash funds by preparation and analysis of cash budget. Through this, it can

minimize spendings and maximise earnings to achieve business targets. While, capital budgeting

methods concluded that NPV is the most superior method henceforth, HML should select project A.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.