Detailed Report on Management Accounting for Nisa Ltd (Business)

VerifiedAdded on 2020/07/22

|17

|4580

|29

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Nisa Ltd, a UK-based retail entity. It begins with an introduction to management accounting, highlighting its importance in decision-making and planning, and then delves into various management accounting systems, including traditional cost accounting, lean accounting, throughput accounting, and transfer pricing. The report then examines different types of management accounting reports such as job order costing, sales forecasting, budget analysis, inventory management, and performance management reports. Furthermore, the report explores cost calculation techniques, specifically marginal costing and absorption costing, and provides income statements for each method. Finally, it evaluates planning tools used for budgetary control and discusses the significance of management accounting systems in addressing financial problems. The report concludes by emphasizing the value of management accounting in improving service quality and making informed business decisions.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1) Management accounting and essential requirements of different types of systems.............1

P2) Management accounting reports...........................................................................................2

TASK 2............................................................................................................................................4

P3) Cost calculation using different techniques..........................................................................4

TASK 3............................................................................................................................................8

P4) Critical evaluation on different types of planning tools used for budgetary control............8

P5) Significance of management accounting systems for responding to financial problems...11

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1) Management accounting and essential requirements of different types of systems.............1

P2) Management accounting reports...........................................................................................2

TASK 2............................................................................................................................................4

P3) Cost calculation using different techniques..........................................................................4

TASK 3............................................................................................................................................8

P4) Critical evaluation on different types of planning tools used for budgetary control............8

P5) Significance of management accounting systems for responding to financial problems...11

CONCLUSION..............................................................................................................................13

REFERENCE.................................................................................................................................14

Illustration Index

Illustration 1: Income statement through marginal costing method................................................5

Illustration 2: Income statement through absorption costing method..............................................6

Illustration 1: Income statement through marginal costing method................................................5

Illustration 2: Income statement through absorption costing method..............................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a multidisciplinary approach that is essential for decision

making process regarding business operations. It includes different tools for analysing

organization's performance and further preparing plans for proper management of all activities.

The present report is based on understanding different aspects of management accounting for

improving service qualities of Nisa Ltd. It is retail scale entity of UK that provides services of

groceries, food items and clothes to customers. However, concept of management accounting

including planning tools are to be described for decision making process. Including this, various

methods for management accounting report and costing is to be understood through this

assignment. Moreover, planning tools used for budgetary control can be presented that involves

its positive and negative both aspects. However, several management accounting systems to

reduce financial problem is to be introduced that affects effectiveness of entity. Thus, learners

are able to acquire knowledge about management accounting and its aspects for preparing

planning and decision making through this project.

TASK 1

P1) Management accounting and essential requirements of different types of systems

Management accounting can be defined as procedure that helps in preparing the reports

and accounts of company. This document contains facts and figures about financial and

statistical information of business operations. That helps management in making sound business

decisions for the development of the corporation. It is an essential business function that helps in

keeping the detail about product and services so that managers can allocate funds to each activity

effective and can gain high return over its investments (Otley and Emmanuel, 2013). Report of

management accounting shows amount of cash availability in the firm, raw material,

outstanding, debt, sales revenues etc. By this way managers can forecast the returns and can

make sound decision so that it can meet with the objectives.

Different types of management accounting system

There are many management accounting systems that can be used by Nisa for making

sound business decisions. These are described as below: Traditional cost accounting: It is the traditional approach that is used by most of the

firms. It involves direct cost, labour cost and overhead expenditures of the company in

order to identify the cash flow in the workplace. Nisa can take support of this system

1

Management accounting is a multidisciplinary approach that is essential for decision

making process regarding business operations. It includes different tools for analysing

organization's performance and further preparing plans for proper management of all activities.

The present report is based on understanding different aspects of management accounting for

improving service qualities of Nisa Ltd. It is retail scale entity of UK that provides services of

groceries, food items and clothes to customers. However, concept of management accounting

including planning tools are to be described for decision making process. Including this, various

methods for management accounting report and costing is to be understood through this

assignment. Moreover, planning tools used for budgetary control can be presented that involves

its positive and negative both aspects. However, several management accounting systems to

reduce financial problem is to be introduced that affects effectiveness of entity. Thus, learners

are able to acquire knowledge about management accounting and its aspects for preparing

planning and decision making through this project.

TASK 1

P1) Management accounting and essential requirements of different types of systems

Management accounting can be defined as procedure that helps in preparing the reports

and accounts of company. This document contains facts and figures about financial and

statistical information of business operations. That helps management in making sound business

decisions for the development of the corporation. It is an essential business function that helps in

keeping the detail about product and services so that managers can allocate funds to each activity

effective and can gain high return over its investments (Otley and Emmanuel, 2013). Report of

management accounting shows amount of cash availability in the firm, raw material,

outstanding, debt, sales revenues etc. By this way managers can forecast the returns and can

make sound decision so that it can meet with the objectives.

Different types of management accounting system

There are many management accounting systems that can be used by Nisa for making

sound business decisions. These are described as below: Traditional cost accounting: It is the traditional approach that is used by most of the

firms. It involves direct cost, labour cost and overhead expenditures of the company in

order to identify the cash flow in the workplace. Nisa can take support of this system

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because by this way cited firm will be able to shed hight on the overall expenditure of the

entity and manager can allocate resources accordingly (Fullerton, Kennedy and Widener,

2013). It is highly required in the organization because by this way margin of profit can

be estimated by the company. Lean accounting: It is another management accounting system in which management

includes accounting, controlling and measuring of performance of the entity. It is an

effective tool that needs to be used by Nisa in making necessary changes in its controlling

and measuring process (Kaplan and Atkinson, 2015). That can help the cited firm in

making sound pricing decisions that can help in enhancing the overall business

performance significantly. It is less complex and cost effective method that can support

the organization in accomplishing its goal soon. It is the system which focuses more on

lean manufacturing and lean thinking so that entity can sustain in the complex situation

well and can improve its performance continuously. Throughput accounting: This is regarded as the type of accounting that includes the

examination of the constraints within the system that is related with the production within

the firm. This is on the basis of the principal as well as approach attached with simplified

management. In relation with increasing the profitability Nisa is being assisted towards

the procedure of decision making (Nørreklit and et.al., 2016).

Transfer pricing: Such is considered as the price wherein the products and service

movement is being carried out. With the cost calculation the transfer expenses attached

with the goods and services are being included to a greater extent.

P2) Management accounting reports

Management accountant of Nisa Ltd prepares and maintains different reports that

presents organization's financial and non-economic performance (Macinati and Anessi, 2014).

For example; job order costing, inventory management report, ratio analysis, budgeting and

performance management reports and so on. However, these management accounting reports can

be described as below:-

Job order costing report:- Through this reporting system, cost incurred on

manufacturing of products including purchasing raw material, labour cost and overhead

expenses are analysed. On the basis of this, price is determined on product services

produced by entity. However, various tools and expenses incurred on production and

2

entity and manager can allocate resources accordingly (Fullerton, Kennedy and Widener,

2013). It is highly required in the organization because by this way margin of profit can

be estimated by the company. Lean accounting: It is another management accounting system in which management

includes accounting, controlling and measuring of performance of the entity. It is an

effective tool that needs to be used by Nisa in making necessary changes in its controlling

and measuring process (Kaplan and Atkinson, 2015). That can help the cited firm in

making sound pricing decisions that can help in enhancing the overall business

performance significantly. It is less complex and cost effective method that can support

the organization in accomplishing its goal soon. It is the system which focuses more on

lean manufacturing and lean thinking so that entity can sustain in the complex situation

well and can improve its performance continuously. Throughput accounting: This is regarded as the type of accounting that includes the

examination of the constraints within the system that is related with the production within

the firm. This is on the basis of the principal as well as approach attached with simplified

management. In relation with increasing the profitability Nisa is being assisted towards

the procedure of decision making (Nørreklit and et.al., 2016).

Transfer pricing: Such is considered as the price wherein the products and service

movement is being carried out. With the cost calculation the transfer expenses attached

with the goods and services are being included to a greater extent.

P2) Management accounting reports

Management accountant of Nisa Ltd prepares and maintains different reports that

presents organization's financial and non-economic performance (Macinati and Anessi, 2014).

For example; job order costing, inventory management report, ratio analysis, budgeting and

performance management reports and so on. However, these management accounting reports can

be described as below:-

Job order costing report:- Through this reporting system, cost incurred on

manufacturing of products including purchasing raw material, labour cost and overhead

expenses are analysed. On the basis of this, price is determined on product services

produced by entity. However, various tools and expenses incurred on production and

2

marketing of goods and identified through this report (Christ, 2014). In accordance to

this, financial records related to costing on expenses and revenue are prepared by which

further decisions are made. Besides this, economic position of entity is recognized that

leads to prepare plans for further implementations.

Sales forecasting reports:- This report is prepared for recording financial data related to

marketing of goods and services provided by Nisa Ltd. It involves expenditures and

revenue on production and distribution of product services. On behalf of analysing these

reports, further decisions are made related to planning including forecasting and decision

making in future time. Moreover, market position of entity and its products is recognized

through maintaining this report (Tucker and Schaltegger, 2016). Therefore, selling of

groceries and items are managed by identifying last year's performance. Including this, it

is able for optimum allocation of resources and fund therefore proper management of all

goods can achieve systematically.

Budget analysis report:- Budget is a management accounting technique that is useful for

preparing plan involving forecasting and decision making for further years. In this regard,

actual performance of entity is identified also provides several ideas for better quality

services and managing all resources. By preparing and maintaining records, adequate

allocation of goods and fund can be managed efficiently (Van, 2015). However, it is

suitable for preparing systematic planning schedule to be followed on to achieve set

target. Thus, budget is one of the main management accounting tool useful for optimum

allocation of goods and making decisions to improve efficiencies and quality services of

entity in a systematic manner.

Inventory management report:- It affects liquidity position of Nisa Ltd which plays

crucial role in management of business operations. In this process, inventory and goods

provided organization is recorded. Overall transaction of goods and financial information

obtained by this method that proceed to making decisions for further years; business

operations. However, reporting for inventory management is useful for adequate

production and supplement of goods. It is also valuable to improve quality services of

products as well enhancing efficiencies of entity efficiently (Kaming and Marliansyah,

2016). Thus, reporting for inventory management is appropriate for following on

particular strategies and plans of organization for improving liquidity position as well

3

this, financial records related to costing on expenses and revenue are prepared by which

further decisions are made. Besides this, economic position of entity is recognized that

leads to prepare plans for further implementations.

Sales forecasting reports:- This report is prepared for recording financial data related to

marketing of goods and services provided by Nisa Ltd. It involves expenditures and

revenue on production and distribution of product services. On behalf of analysing these

reports, further decisions are made related to planning including forecasting and decision

making in future time. Moreover, market position of entity and its products is recognized

through maintaining this report (Tucker and Schaltegger, 2016). Therefore, selling of

groceries and items are managed by identifying last year's performance. Including this, it

is able for optimum allocation of resources and fund therefore proper management of all

goods can achieve systematically.

Budget analysis report:- Budget is a management accounting technique that is useful for

preparing plan involving forecasting and decision making for further years. In this regard,

actual performance of entity is identified also provides several ideas for better quality

services and managing all resources. By preparing and maintaining records, adequate

allocation of goods and fund can be managed efficiently (Van, 2015). However, it is

suitable for preparing systematic planning schedule to be followed on to achieve set

target. Thus, budget is one of the main management accounting tool useful for optimum

allocation of goods and making decisions to improve efficiencies and quality services of

entity in a systematic manner.

Inventory management report:- It affects liquidity position of Nisa Ltd which plays

crucial role in management of business operations. In this process, inventory and goods

provided organization is recorded. Overall transaction of goods and financial information

obtained by this method that proceed to making decisions for further years; business

operations. However, reporting for inventory management is useful for adequate

production and supplement of goods. It is also valuable to improve quality services of

products as well enhancing efficiencies of entity efficiently (Kaming and Marliansyah,

2016). Thus, reporting for inventory management is appropriate for following on

particular strategies and plans of organization for improving liquidity position as well

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

making decisions for future production of product services. Along with this, excess of

wastage material get reduced through this process thereby proper management of

material is gained for manufacturing process.

Performance management report:- As management accounting is multidisciplinary

approach, it focuses on all activities involving performance of worker performs their job

for entity's effectiveness. In this process, critical evaluation their performances is created

by which different ideas are generated for improving working efficiencies. Along with

this, it is helpful for encouraging them regarding better contribution in team work

(Wodchis and et.al., 2013). On the basis of this performance evaluation, report is

prepared related to their work performance by which segmentation of work can be done

according to workers' abilities. However, report is prepared and maintained related to

making decisions for better work performance that affects effectiveness of entity.

TASK 2

P3) Cost calculation using different techniques

Costing is a process of price determination by which adequate cost of product and

services is set. It is set on the basis of expenditures incurred on manufacturing and production of

goods. However, cost is calculated on the basis of different factors as purchasing materials,

labour cost, expenditures on production and advertisement of goods, market demand,

competition and so on (Ninan and Inoue, 2013). Further, price is determined through costing

method that leads to prepare income statement to present financial position of Nisa Ltd. In this

regard, income statement through absorption and marginal costing can be expressed as follows:-

Marginal costing:- It is a method for calculating cost of product on the basis of direct

and indirect expenses incurred for business operations. For preparing income income through

this costing method, net profit is evaluated by deducting gross profit with variable expenses only.

Therefore, it is suitable for short term decision making process and preparing strategies for

solving out any problem occur at workplace (Nazifi, 2016). Including this, preparing income

statement through this method is suitable for making decisions regarding business operations for

normal investments. In this regard, management accountant of Nisa Ltd prepares following

income statement through marginal costing as:-

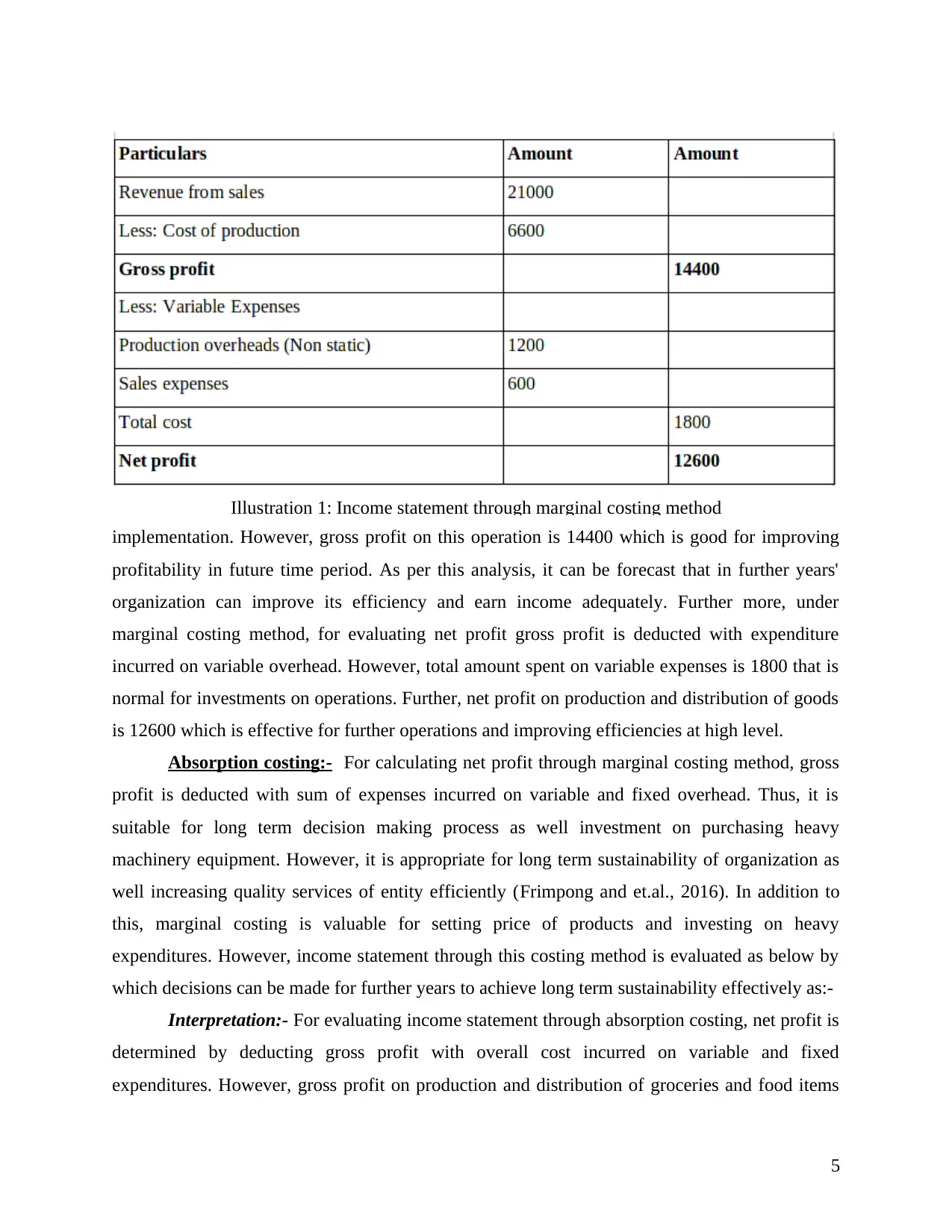

Interpretation:- It is determined that amount on expenditures of groceries and food items

is 6600 on which organization gains revenue of 21000. It is quite effective for further

4

wastage material get reduced through this process thereby proper management of

material is gained for manufacturing process.

Performance management report:- As management accounting is multidisciplinary

approach, it focuses on all activities involving performance of worker performs their job

for entity's effectiveness. In this process, critical evaluation their performances is created

by which different ideas are generated for improving working efficiencies. Along with

this, it is helpful for encouraging them regarding better contribution in team work

(Wodchis and et.al., 2013). On the basis of this performance evaluation, report is

prepared related to their work performance by which segmentation of work can be done

according to workers' abilities. However, report is prepared and maintained related to

making decisions for better work performance that affects effectiveness of entity.

TASK 2

P3) Cost calculation using different techniques

Costing is a process of price determination by which adequate cost of product and

services is set. It is set on the basis of expenditures incurred on manufacturing and production of

goods. However, cost is calculated on the basis of different factors as purchasing materials,

labour cost, expenditures on production and advertisement of goods, market demand,

competition and so on (Ninan and Inoue, 2013). Further, price is determined through costing

method that leads to prepare income statement to present financial position of Nisa Ltd. In this

regard, income statement through absorption and marginal costing can be expressed as follows:-

Marginal costing:- It is a method for calculating cost of product on the basis of direct

and indirect expenses incurred for business operations. For preparing income income through

this costing method, net profit is evaluated by deducting gross profit with variable expenses only.

Therefore, it is suitable for short term decision making process and preparing strategies for

solving out any problem occur at workplace (Nazifi, 2016). Including this, preparing income

statement through this method is suitable for making decisions regarding business operations for

normal investments. In this regard, management accountant of Nisa Ltd prepares following

income statement through marginal costing as:-

Interpretation:- It is determined that amount on expenditures of groceries and food items

is 6600 on which organization gains revenue of 21000. It is quite effective for further

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

implementation. However, gross profit on this operation is 14400 which is good for improving

profitability in future time period. As per this analysis, it can be forecast that in further years'

organization can improve its efficiency and earn income adequately. Further more, under

marginal costing method, for evaluating net profit gross profit is deducted with expenditure

incurred on variable overhead. However, total amount spent on variable expenses is 1800 that is

normal for investments on operations. Further, net profit on production and distribution of goods

is 12600 which is effective for further operations and improving efficiencies at high level.

Absorption costing:- For calculating net profit through marginal costing method, gross

profit is deducted with sum of expenses incurred on variable and fixed overhead. Thus, it is

suitable for long term decision making process as well investment on purchasing heavy

machinery equipment. However, it is appropriate for long term sustainability of organization as

well increasing quality services of entity efficiently (Frimpong and et.al., 2016). In addition to

this, marginal costing is valuable for setting price of products and investing on heavy

expenditures. However, income statement through this costing method is evaluated as below by

which decisions can be made for further years to achieve long term sustainability effectively as:-

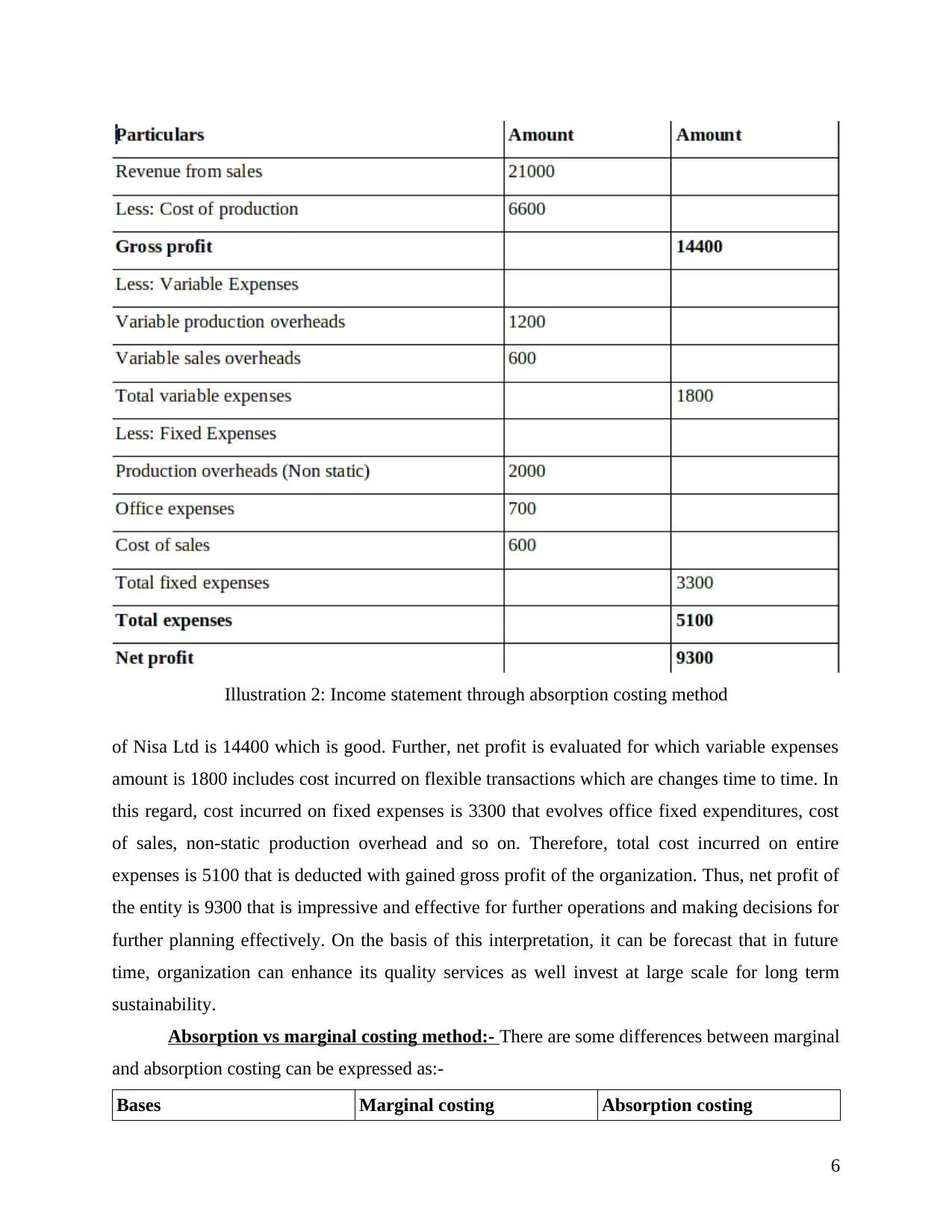

Interpretation:- For evaluating income statement through absorption costing, net profit is

determined by deducting gross profit with overall cost incurred on variable and fixed

expenditures. However, gross profit on production and distribution of groceries and food items

5

Illustration 1: Income statement through marginal costing method

profitability in future time period. As per this analysis, it can be forecast that in further years'

organization can improve its efficiency and earn income adequately. Further more, under

marginal costing method, for evaluating net profit gross profit is deducted with expenditure

incurred on variable overhead. However, total amount spent on variable expenses is 1800 that is

normal for investments on operations. Further, net profit on production and distribution of goods

is 12600 which is effective for further operations and improving efficiencies at high level.

Absorption costing:- For calculating net profit through marginal costing method, gross

profit is deducted with sum of expenses incurred on variable and fixed overhead. Thus, it is

suitable for long term decision making process as well investment on purchasing heavy

machinery equipment. However, it is appropriate for long term sustainability of organization as

well increasing quality services of entity efficiently (Frimpong and et.al., 2016). In addition to

this, marginal costing is valuable for setting price of products and investing on heavy

expenditures. However, income statement through this costing method is evaluated as below by

which decisions can be made for further years to achieve long term sustainability effectively as:-

Interpretation:- For evaluating income statement through absorption costing, net profit is

determined by deducting gross profit with overall cost incurred on variable and fixed

expenditures. However, gross profit on production and distribution of groceries and food items

5

Illustration 1: Income statement through marginal costing method

of Nisa Ltd is 14400 which is good. Further, net profit is evaluated for which variable expenses

amount is 1800 includes cost incurred on flexible transactions which are changes time to time. In

this regard, cost incurred on fixed expenses is 3300 that evolves office fixed expenditures, cost

of sales, non-static production overhead and so on. Therefore, total cost incurred on entire

expenses is 5100 that is deducted with gained gross profit of the organization. Thus, net profit of

the entity is 9300 that is impressive and effective for further operations and making decisions for

further planning effectively. On the basis of this interpretation, it can be forecast that in future

time, organization can enhance its quality services as well invest at large scale for long term

sustainability.

Absorption vs marginal costing method:- There are some differences between marginal

and absorption costing can be expressed as:-

Bases Marginal costing Absorption costing

6

Illustration 2: Income statement through absorption costing method

amount is 1800 includes cost incurred on flexible transactions which are changes time to time. In

this regard, cost incurred on fixed expenses is 3300 that evolves office fixed expenditures, cost

of sales, non-static production overhead and so on. Therefore, total cost incurred on entire

expenses is 5100 that is deducted with gained gross profit of the organization. Thus, net profit of

the entity is 9300 that is impressive and effective for further operations and making decisions for

further planning effectively. On the basis of this interpretation, it can be forecast that in future

time, organization can enhance its quality services as well invest at large scale for long term

sustainability.

Absorption vs marginal costing method:- There are some differences between marginal

and absorption costing can be expressed as:-

Bases Marginal costing Absorption costing

6

Illustration 2: Income statement through absorption costing method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit variation For evaluating net profit, gross

profit is deducted with

expenditures incurred on

variable overhead only.

Net profit is determined

through deducting gross profit

with overall cost incurred on

variable and fixed overhead.

Time periodicity Suitable for short term

operations.

Appropriate for long time

periodicity.

Decision making process Decisions are made on normal

investments.

Decisions are made related to

long term sustainability and

competitiveness including

heavy expenses.

It is evaluated that preparing income statement through marginal costing is suitable for

making decisions for short time period investments. While, on the other side, absorption costing

is appropriate for making decisions on heavy investments for improvement in quality services.

However, decisions can be made through costing methods regarding business operations and

further implementations. It shows financial position of organization and different aspects for

better quality services and effectiveness of entity at high level (Frimpong and et.al., 2016). Apart

form this, it is gained that on the basis of preparing and analysing income statements through this

method, further decisions are made for improvements and effectiveness of entity. Thus, marginal

and absorption both kinds of costing methods are suitable for decision making related to

organization's growth and proper effectiveness in systematic manner.

TASK 3

P4) Critical evaluation on different types of planning tools used for budgetary control

The concept of budgetary control is considered as one with which management of Nisa

would make construction of future period's budget by the means of projection. Further it is

comprised of making comparison with the actual performance in order to make determination of

the flaws so that corrective measures can be taken without making any type of delay (Otley and

Emmanuel, 2013). There is presence of several tools and techniques that can assist in

development of budget for the years to comes. These are enumerated in the manner stated as

below:

7

profit is deducted with

expenditures incurred on

variable overhead only.

Net profit is determined

through deducting gross profit

with overall cost incurred on

variable and fixed overhead.

Time periodicity Suitable for short term

operations.

Appropriate for long time

periodicity.

Decision making process Decisions are made on normal

investments.

Decisions are made related to

long term sustainability and

competitiveness including

heavy expenses.

It is evaluated that preparing income statement through marginal costing is suitable for

making decisions for short time period investments. While, on the other side, absorption costing

is appropriate for making decisions on heavy investments for improvement in quality services.

However, decisions can be made through costing methods regarding business operations and

further implementations. It shows financial position of organization and different aspects for

better quality services and effectiveness of entity at high level (Frimpong and et.al., 2016). Apart

form this, it is gained that on the basis of preparing and analysing income statements through this

method, further decisions are made for improvements and effectiveness of entity. Thus, marginal

and absorption both kinds of costing methods are suitable for decision making related to

organization's growth and proper effectiveness in systematic manner.

TASK 3

P4) Critical evaluation on different types of planning tools used for budgetary control

The concept of budgetary control is considered as one with which management of Nisa

would make construction of future period's budget by the means of projection. Further it is

comprised of making comparison with the actual performance in order to make determination of

the flaws so that corrective measures can be taken without making any type of delay (Otley and

Emmanuel, 2013). There is presence of several tools and techniques that can assist in

development of budget for the years to comes. These are enumerated in the manner stated as

below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental budgeting

It is regarded as the tool that depends on development of smaller alteration in the

prevailing budget for the sake making development of the new budget for the year to come. This

is considered simple manner as each year incremental amount is being added to the budget of

past year as well as makes sure requirement for regular funding (Tucker and Schaltegger, 2016).

On the other hand it makes promotion of the expenses and does not offer managers with any kind

of incentives for cost curtailment.

Advantages Disadvantages

Easier in budget creation

Makes sure small or less differences

Ensure maintenance of equality in all

the departments that exists within Nisa

Make promotion of unimportant

spending

In order to control cost no incentive

System of permanent resource

allocation

Zero based budgeting

The manager of Nisa can make development of the budget by the means of considering

zero as base as well as make analysis of the need and cost associated of each function with

suitable justification by the means carrying out investigation in market (Nisa Ltd, 2016). It offer

real figures regarding the potential operations as managers make analysis of the conditions

existing in the external market as well as forecast the future. Thus elimination of unnecessary

actions is done that encourages saving.

Advantages Disadvantages

Real figures along with judgement

Assist is suitable planning

Lays emphasis on cost curtailment

Consumes time

Require huge amount of funds

Manager has to be highly experienced

and talented for the sake of assessing

trends within the market along with the

challenges related with preparation of

budget

8

It is regarded as the tool that depends on development of smaller alteration in the

prevailing budget for the sake making development of the new budget for the year to come. This

is considered simple manner as each year incremental amount is being added to the budget of

past year as well as makes sure requirement for regular funding (Tucker and Schaltegger, 2016).

On the other hand it makes promotion of the expenses and does not offer managers with any kind

of incentives for cost curtailment.

Advantages Disadvantages

Easier in budget creation

Makes sure small or less differences

Ensure maintenance of equality in all

the departments that exists within Nisa

Make promotion of unimportant

spending

In order to control cost no incentive

System of permanent resource

allocation

Zero based budgeting

The manager of Nisa can make development of the budget by the means of considering

zero as base as well as make analysis of the need and cost associated of each function with

suitable justification by the means carrying out investigation in market (Nisa Ltd, 2016). It offer

real figures regarding the potential operations as managers make analysis of the conditions

existing in the external market as well as forecast the future. Thus elimination of unnecessary

actions is done that encourages saving.

Advantages Disadvantages

Real figures along with judgement

Assist is suitable planning

Lays emphasis on cost curtailment

Consumes time

Require huge amount of funds

Manager has to be highly experienced

and talented for the sake of assessing

trends within the market along with the

challenges related with preparation of

budget

8

Fixed budgeting

This is regarded as the financial plan which do not differ in accordance with the actual

production volume of Nisa. In addition to this it offers budgeted targets for activity level that is

fixed.

Advantages Disadvantages

It assist in measurement and

examination of the performance

Act as an aid in strategic decision

making and plan for growth

Maintains the level of cost at minimum

for greater return

It does not offer any kind of assistance

towards making comparison of the

outcomes in case standard and actual

results varies

It cannot alter in accordance with the

actual level of activity

Flexible budgeting

As compared with the fixed this budgeting plan pays greater focus towards more than one

output related with production (Kaplan and Atkinson, 2015). Further it can be effectively

adjusted as per the real output of Nisa.

Advantages Disadvantages

It act as an aid in adjusting the target in

accordance with the actual volume of

production related with Nisa

It offers assistance in making optimum

allocation of resources in accordance

with the need

It makes important adjustment with

respect to volatility within the market

that is inflation and others.

It needs monitoring on continuous basis

in order to track the alterations within

the external market environment that is

time consuming procedure

There is difficulty in making

determination of accurate data that

results in increasing the complexities

within the construction of budget

Activity based budgeting

In the present time the use of activity based budgeting is being done by the organizations

for the sake of making development of their budgets. In accordance with such tool Nisa can

9

This is regarded as the financial plan which do not differ in accordance with the actual

production volume of Nisa. In addition to this it offers budgeted targets for activity level that is

fixed.

Advantages Disadvantages

It assist in measurement and

examination of the performance

Act as an aid in strategic decision

making and plan for growth

Maintains the level of cost at minimum

for greater return

It does not offer any kind of assistance

towards making comparison of the

outcomes in case standard and actual

results varies

It cannot alter in accordance with the

actual level of activity

Flexible budgeting

As compared with the fixed this budgeting plan pays greater focus towards more than one

output related with production (Kaplan and Atkinson, 2015). Further it can be effectively

adjusted as per the real output of Nisa.

Advantages Disadvantages

It act as an aid in adjusting the target in

accordance with the actual volume of

production related with Nisa

It offers assistance in making optimum

allocation of resources in accordance

with the need

It makes important adjustment with

respect to volatility within the market

that is inflation and others.

It needs monitoring on continuous basis

in order to track the alterations within

the external market environment that is

time consuming procedure

There is difficulty in making

determination of accurate data that

results in increasing the complexities

within the construction of budget

Activity based budgeting

In the present time the use of activity based budgeting is being done by the organizations

for the sake of making development of their budgets. In accordance with such tool Nisa can

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.