Management Accounting Analysis and Report: Nisa Ltd, UK SME

VerifiedAdded on 2020/01/23

|24

|5909

|110

Report

AI Summary

This report examines the application of management accounting principles within Nisa Ltd, a small to medium-sized enterprise (SME) in the UK retail sector. The report explores the significance of management accounting systems, including job order costing, cost accounting, inventory management, and risk management, in enhancing business operations and decision-making. It details various techniques used for management accounting reporting, such as job cost reports, inventory management reports, and performance reports, highlighting their role in financial analysis and strategic planning. Furthermore, the report delves into costing techniques for preparing income statements, specifically marginal costing, providing insights into price determination and profit analysis. The analysis underscores the importance of management accounting tools in facilitating business growth, improving efficiency, and ensuring effective resource allocation within the organization. The report emphasizes the role of management accounting in decision making and action planning for expansion of small scale firm.

Unit 5. Management

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is important for entire organization's development. It is useful

for risk management and implementing strategic plans for entity's effectiveness. In this regard,

decision making and forecasting regarding business activities are performed that is helpful for

systematic growth of enterprises. The present report is based on management accounting tools

and techniques of Nisa.

It is retail sector small medium enterprise UK that provides groceries and food items. In

accordance to this, various methods for effective accounting system including its types can be

determined. Including this, different techniques used for management accounting reporting is

presenter. Moreover, learners can learn several costing methods for preparing income statement

as well analyzing data interpretation for further decision making can be understood through this

study. Along with this, significance of management accounting tools for decision making and

action planning for expansion of small scale firm can present.

TASK 1

P1) Management accounting and its different systems

Management Accounting

General Manager

Subject: To understand significance of management accounting systems in management of

business operations for Nisa Ltd.

Management accounting: - It is considered as provision of accounting information

remains helpful for effective performance and enhancing efficiency of organization. Under

management accounting system, varieties of business activities regarding financial, production,

budgeting, action planning and solving out issues occur at workplace are determined. Therefore,

proper price determination and information related to entity's performance is obtained that is

useful for enlargement of firm and qualitative services produces by company (Otley and

Emmanuel, 2013). However, it involves variance analysis, activity based costing and different

techniques for developing effectiveness of firm. In this regard, management accountant of Nisa

recognizes financial statements and reports that leads to making decisions for further business

activities. Thus, management accounting plays crucial role in organization's systematic

1

Management accounting is important for entire organization's development. It is useful

for risk management and implementing strategic plans for entity's effectiveness. In this regard,

decision making and forecasting regarding business activities are performed that is helpful for

systematic growth of enterprises. The present report is based on management accounting tools

and techniques of Nisa.

It is retail sector small medium enterprise UK that provides groceries and food items. In

accordance to this, various methods for effective accounting system including its types can be

determined. Including this, different techniques used for management accounting reporting is

presenter. Moreover, learners can learn several costing methods for preparing income statement

as well analyzing data interpretation for further decision making can be understood through this

study. Along with this, significance of management accounting tools for decision making and

action planning for expansion of small scale firm can present.

TASK 1

P1) Management accounting and its different systems

Management Accounting

General Manager

Subject: To understand significance of management accounting systems in management of

business operations for Nisa Ltd.

Management accounting: - It is considered as provision of accounting information

remains helpful for effective performance and enhancing efficiency of organization. Under

management accounting system, varieties of business activities regarding financial, production,

budgeting, action planning and solving out issues occur at workplace are determined. Therefore,

proper price determination and information related to entity's performance is obtained that is

useful for enlargement of firm and qualitative services produces by company (Otley and

Emmanuel, 2013). However, it involves variance analysis, activity based costing and different

techniques for developing effectiveness of firm. In this regard, management accountant of Nisa

recognizes financial statements and reports that leads to making decisions for further business

activities. Thus, management accounting plays crucial role in organization's systematic

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management that aims to increase productivity and profitability with budgeting and forecasting

methods. Management accounting is helpful for entire business activities and enlargement of

small scale enterprise. Therefore, it is valuable for overall implementation of business

organization and producing qualitative services of firm.

Management accounting systems: -

Different tools and techniques are determined for effective management accounting

systems such as; analysing business performance, using costing method for adequate price

determination, inventory management and additional tools that are valuable for enlargement of

small size enterprise. Therefore, various management accounting systems and their

requirements can describe as below: -

Job order costing system: Under this management accounting system, cost incurred for

manufacturing process is analysed. It includes decisions regarding investment on

purchasing raw materials, labour costs and additional overhead (Corona, Nan and

Zhang, 2014). Therefore, decisions regarding investment are done through this process.

Cost accounting system: In this management accounting system, planning is created

regarding reducing expenses and increasing sales revenue for business operations.

However, effective price determination and management of production and distribution

of goods can be done through this process system (Bennett, Schaltegger and Zvezdov,

2013).

Inventory management system: Management accounting is also effective for

managing inventories of Nisa Ltd. However, different ideas are generated regarding

optimum utilization of resources and fund affect productivity and profitability of the

firm more efficiently (Van, 2015). Price optimization: Through identifying cost incurred on manufacturing and

production process, price can be determined as well optimized more effectively. It will

be able to increase profitability and management of entire business operations of Nisa

Ltd.

Identifying business performance: - Management accountant of Nisa evaluates

business activities including production and distribution of groceries, financial statements and

2

methods. Management accounting is helpful for entire business activities and enlargement of

small scale enterprise. Therefore, it is valuable for overall implementation of business

organization and producing qualitative services of firm.

Management accounting systems: -

Different tools and techniques are determined for effective management accounting

systems such as; analysing business performance, using costing method for adequate price

determination, inventory management and additional tools that are valuable for enlargement of

small size enterprise. Therefore, various management accounting systems and their

requirements can describe as below: -

Job order costing system: Under this management accounting system, cost incurred for

manufacturing process is analysed. It includes decisions regarding investment on

purchasing raw materials, labour costs and additional overhead (Corona, Nan and

Zhang, 2014). Therefore, decisions regarding investment are done through this process.

Cost accounting system: In this management accounting system, planning is created

regarding reducing expenses and increasing sales revenue for business operations.

However, effective price determination and management of production and distribution

of goods can be done through this process system (Bennett, Schaltegger and Zvezdov,

2013).

Inventory management system: Management accounting is also effective for

managing inventories of Nisa Ltd. However, different ideas are generated regarding

optimum utilization of resources and fund affect productivity and profitability of the

firm more efficiently (Van, 2015). Price optimization: Through identifying cost incurred on manufacturing and

production process, price can be determined as well optimized more effectively. It will

be able to increase profitability and management of entire business operations of Nisa

Ltd.

Identifying business performance: - Management accountant of Nisa evaluates

business activities including production and distribution of groceries, financial statements and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

all records that company maintained (Fullerton, Kennedy and Widener, 2013). Thus, on behalf

of these records, further decisions are made to achieve optimum utilization of resource and

gaining better quality services. In addition to this, proper financial management and costing for

goods and services are determined. However, cash flow, income statement, expenditures and

revenue of firm are recognized that is valuable for effective business performance. In

accordance to this, budget and proper strategies are prepared for implementation and systematic

management of firm.

Cost effectiveness: - Management accounting involves costing tool for determining

price of goods produced by organization. Under this system, adequate pricing is obtained for

increasing demand and productivity. In accordance to this, based on manufacturing,

expenditures incurred for work in process management accountant sets price of goods and

services provided by company. For cost effectiveness, accountant makes strategies related to

adequacy and maintaining effective productivity. In this regard, different costing methods are

used for example; marginal and absorption costing. Thus, price is determined effectively for

cost effectiveness (Van der Stede, 2015).

Inventory management: - This tool of management accounting is useful for proper

allocation of resources. This type of system, production and supplement of groceries produced

by Nisa. However, it includes places and stores to keep inventories safely such as warehouses,

stores and factories where manufacturing and production is produced. Hence, management

accountant of small scale enterprise makes decision regarding inventory management. Along

with this, business activity of last year related to inventory and its management is obtained that

than in other industries (Bui and Villiers, 2016).

Risk management: - Management accounting is essential for reducing risk occurs at

workplace. Therefore, management accountant and manager of firm identify issues and further

prepares strategies for its reduction. It is related to formulating, implementing and evaluating

strategic planning as well action plans. Moreover, different planning procedures and decision

making process is obtained for obtaining solutions to recover problems (Senftlechner and Hiebl,

2015). It is interrelated with performance and efficiency of entity remains adequate for

managing occur at workplace. Therefore, management accountant formulates financial and

other strategies for enlargement of business organization as well increasing qualitative services

3

of these records, further decisions are made to achieve optimum utilization of resource and

gaining better quality services. In addition to this, proper financial management and costing for

goods and services are determined. However, cash flow, income statement, expenditures and

revenue of firm are recognized that is valuable for effective business performance. In

accordance to this, budget and proper strategies are prepared for implementation and systematic

management of firm.

Cost effectiveness: - Management accounting involves costing tool for determining

price of goods produced by organization. Under this system, adequate pricing is obtained for

increasing demand and productivity. In accordance to this, based on manufacturing,

expenditures incurred for work in process management accountant sets price of goods and

services provided by company. For cost effectiveness, accountant makes strategies related to

adequacy and maintaining effective productivity. In this regard, different costing methods are

used for example; marginal and absorption costing. Thus, price is determined effectively for

cost effectiveness (Van der Stede, 2015).

Inventory management: - This tool of management accounting is useful for proper

allocation of resources. This type of system, production and supplement of groceries produced

by Nisa. However, it includes places and stores to keep inventories safely such as warehouses,

stores and factories where manufacturing and production is produced. Hence, management

accountant of small scale enterprise makes decision regarding inventory management. Along

with this, business activity of last year related to inventory and its management is obtained that

than in other industries (Bui and Villiers, 2016).

Risk management: - Management accounting is essential for reducing risk occurs at

workplace. Therefore, management accountant and manager of firm identify issues and further

prepares strategies for its reduction. It is related to formulating, implementing and evaluating

strategic planning as well action plans. Moreover, different planning procedures and decision

making process is obtained for obtaining solutions to recover problems (Senftlechner and Hiebl,

2015). It is interrelated with performance and efficiency of entity remains adequate for

managing occur at workplace. Therefore, management accountant formulates financial and

other strategies for enlargement of business organization as well increasing qualitative services

3

of firm.

Traditional cost accounting system- it is very helpful approach in order to determine cost of

single project. In this the direct and indirect cost is to be calculated in order to fine out exact

cost incurred for particular project. The traditional cost accounting is very important tool in

order to determine the price factor and their services.

Lean accounting system- it works in manner to have proper identification in process,

accounting, controlling and various measurement techniques. This is very flexible accounting

process. It can be understood as less complex and cost effective method.

Thus, composition of various management accounting systems is useful for Nisa for

development of small scale organization with strategic and managerial plans. In this regard,

business organization get developed entirely by focusing on overall activities and performances

of entity. Therefore, different management accounting systems are useful for enlargement and

systematic management of all activities performed by firm. It influences company's reputation

and efficiency for producing groceries and food items at high level. Hence, it is determined that

management accounting is crucial for expansion and increasing productivity of firm effectively.

P2) Techniques used for management accounting reporting

General Manager

Nisa Ltd

Management accounting is integration of overall systems for implementing business

activities (Bennett, Schaltegger and Zvezdov, 2013). Under this method, various reports and

records are maintained by accountant for decision-making and planning procedure related to

expansion and better quality services. In this process, management accountant of the enterprise

prepare and maintain following report can be described as below:

Job cost reports: In this management accounting report, accountant records all

expenditures incurred in manufacturing process for Nisa Ltd. For example; purchasing

raw materials, labor and additional overhead costs. Therefore, proper recording each

4

Traditional cost accounting system- it is very helpful approach in order to determine cost of

single project. In this the direct and indirect cost is to be calculated in order to fine out exact

cost incurred for particular project. The traditional cost accounting is very important tool in

order to determine the price factor and their services.

Lean accounting system- it works in manner to have proper identification in process,

accounting, controlling and various measurement techniques. This is very flexible accounting

process. It can be understood as less complex and cost effective method.

Thus, composition of various management accounting systems is useful for Nisa for

development of small scale organization with strategic and managerial plans. In this regard,

business organization get developed entirely by focusing on overall activities and performances

of entity. Therefore, different management accounting systems are useful for enlargement and

systematic management of all activities performed by firm. It influences company's reputation

and efficiency for producing groceries and food items at high level. Hence, it is determined that

management accounting is crucial for expansion and increasing productivity of firm effectively.

P2) Techniques used for management accounting reporting

General Manager

Nisa Ltd

Management accounting is integration of overall systems for implementing business

activities (Bennett, Schaltegger and Zvezdov, 2013). Under this method, various reports and

records are maintained by accountant for decision-making and planning procedure related to

expansion and better quality services. In this process, management accountant of the enterprise

prepare and maintain following report can be described as below:

Job cost reports: In this management accounting report, accountant records all

expenditures incurred in manufacturing process for Nisa Ltd. For example; purchasing

raw materials, labor and additional overhead costs. Therefore, proper recording each

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial transaction is prepared on which price determination is done for further

business operations (Mistry, Sharma and Low, 2014).

Inventory management report: It is one of the essential reporting managing inventory.

Similarly, it impacts on further production and distribution of goods linked with

profitability. Therefore, inventory management reporting is able to manage business

activities in the future time.

Debtors/ Accounts Receivable Aging Reports: Management accountant of Nisa Ltd

records financial transactions with debtors. Therefore, productivity and profitability of

the small scale enterprise is identified remains able to implement further transactions

(Kornberger, Pflueger and Mouritsen, 2016). It is helpful to create balance between

production and supplement for producing groceries and food items of the enterprise.

Thus, debtors receivable report is useful to manage entire business operations

effectively.

Segment/departmental report: In this report, different departments' functions' report is

prepared systematically. For instance; marketing, finance, production etc. However,

departmental report is useful for management of entire business operations effectively.

Performance reports: As management accounting is multidisciplinary approach,

performance of employees can be managed effectively (Collier, 2015). In this regard, all

employees' work performance is analyzed as well recorded on which ideas for providing

training and development programs are generated. It remains effective to increase their

working efficiencies. Thus, performance management reporting is useful for managing

entire business operations of Nisa Ltd effectively.

Operating budget report: It is prepared on the basis of analyzing actual position of

Nisa Ltd in terms of financial and non-economic position (Pettersen and Solstad, 2014).

However, it is useful for optimum utilization of resources and fund impact on further

business operations. Therefore, operating budget report is essential for management of

all business activities efficiently.

In addition to this, vital role of management accounting is essential for decision-making

and preparing strategies for effectiveness of organization systematically. Including this,

5

business operations (Mistry, Sharma and Low, 2014).

Inventory management report: It is one of the essential reporting managing inventory.

Similarly, it impacts on further production and distribution of goods linked with

profitability. Therefore, inventory management reporting is able to manage business

activities in the future time.

Debtors/ Accounts Receivable Aging Reports: Management accountant of Nisa Ltd

records financial transactions with debtors. Therefore, productivity and profitability of

the small scale enterprise is identified remains able to implement further transactions

(Kornberger, Pflueger and Mouritsen, 2016). It is helpful to create balance between

production and supplement for producing groceries and food items of the enterprise.

Thus, debtors receivable report is useful to manage entire business operations

effectively.

Segment/departmental report: In this report, different departments' functions' report is

prepared systematically. For instance; marketing, finance, production etc. However,

departmental report is useful for management of entire business operations effectively.

Performance reports: As management accounting is multidisciplinary approach,

performance of employees can be managed effectively (Collier, 2015). In this regard, all

employees' work performance is analyzed as well recorded on which ideas for providing

training and development programs are generated. It remains effective to increase their

working efficiencies. Thus, performance management reporting is useful for managing

entire business operations of Nisa Ltd effectively.

Operating budget report: It is prepared on the basis of analyzing actual position of

Nisa Ltd in terms of financial and non-economic position (Pettersen and Solstad, 2014).

However, it is useful for optimum utilization of resources and fund impact on further

business operations. Therefore, operating budget report is essential for management of

all business activities efficiently.

In addition to this, vital role of management accounting is essential for decision-making

and preparing strategies for effectiveness of organization systematically. Including this,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management accounting tool as budget is useful for management of inventories and strategies

prepared for business effectiveness. Proper decision-making is obtained by using management

accounting tools that is valuable for increasing efficiency of small scale organization and

maintaining balance of trade adequately.

TASK 2

P3) Costing techniques for preparing income statement

General Manager

Nisa Ltd

Costing is method for determining price of goods per expenses charged for manufacturing

and production system. Based on expenses such as; operating, advertising, fixed and variable

cost, management accountant of organization decides price of goods supplied by firm. It is

evaluated based on different factors for example; market demand, competition and other

determinants that are useful for costing. It leads to prepare income statement that presents

financial position of firm. There are various costing methods presented for calculating price of

products can describe as follows: -

Marginal costing method:-

Marginal costing is price determination method under which management accountant

obtains only gross profit and net profit. It does not include fixed expense and overhead for

determining net profit (Ismail, 2016). In this regard, gross profit is considered as a difference of

income to expenses. It evaluates balance of expenditure and revenue. Further, net profit is

determined for gross profit is subtracted with total variable expenditures. It helps in defining the

part of cost in this whole cost is not considered. In this the price factor change at every output

level. Fixed cost charged as per the aggregate contribution of per unit. In other words it is

treated as marginal cost derive with cost of product but fixed cost reflect as per period factor. It

is inclusive of following cost are as material cost, direct labour cost and direct expenses cost

etc.

this contribution can be understood in following manner are as-

To find out contribution- Sales price- variable cost

6

prepared for business effectiveness. Proper decision-making is obtained by using management

accounting tools that is valuable for increasing efficiency of small scale organization and

maintaining balance of trade adequately.

TASK 2

P3) Costing techniques for preparing income statement

General Manager

Nisa Ltd

Costing is method for determining price of goods per expenses charged for manufacturing

and production system. Based on expenses such as; operating, advertising, fixed and variable

cost, management accountant of organization decides price of goods supplied by firm. It is

evaluated based on different factors for example; market demand, competition and other

determinants that are useful for costing. It leads to prepare income statement that presents

financial position of firm. There are various costing methods presented for calculating price of

products can describe as follows: -

Marginal costing method:-

Marginal costing is price determination method under which management accountant

obtains only gross profit and net profit. It does not include fixed expense and overhead for

determining net profit (Ismail, 2016). In this regard, gross profit is considered as a difference of

income to expenses. It evaluates balance of expenditure and revenue. Further, net profit is

determined for gross profit is subtracted with total variable expenditures. It helps in defining the

part of cost in this whole cost is not considered. In this the price factor change at every output

level. Fixed cost charged as per the aggregate contribution of per unit. In other words it is

treated as marginal cost derive with cost of product but fixed cost reflect as per period factor. It

is inclusive of following cost are as material cost, direct labour cost and direct expenses cost

etc.

this contribution can be understood in following manner are as-

To find out contribution- Sales price- variable cost

6

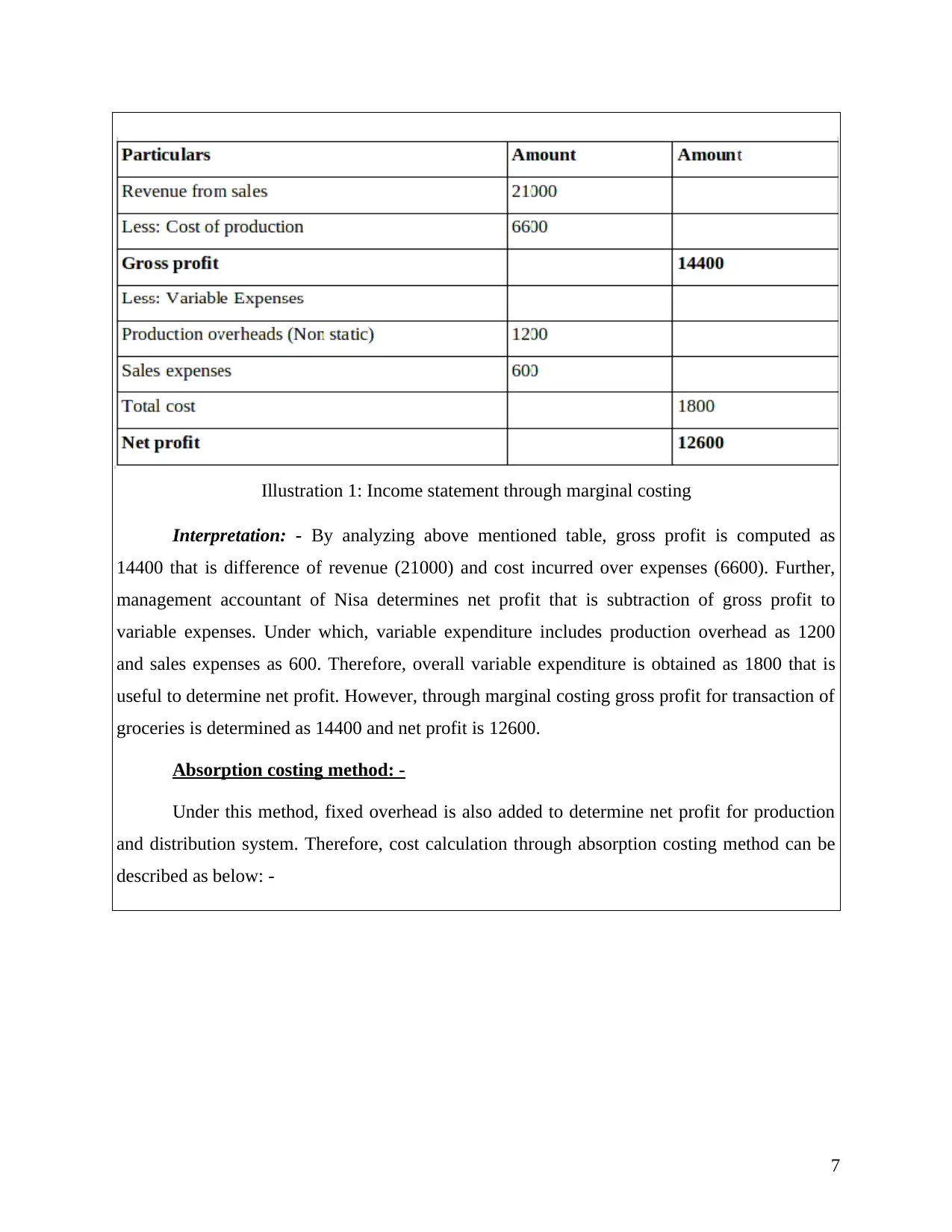

Interpretation: - By analyzing above mentioned table, gross profit is computed as

14400 that is difference of revenue (21000) and cost incurred over expenses (6600). Further,

management accountant of Nisa determines net profit that is subtraction of gross profit to

variable expenses. Under which, variable expenditure includes production overhead as 1200

and sales expenses as 600. Therefore, overall variable expenditure is obtained as 1800 that is

useful to determine net profit. However, through marginal costing gross profit for transaction of

groceries is determined as 14400 and net profit is 12600.

Absorption costing method: -

Under this method, fixed overhead is also added to determine net profit for production

and distribution system. Therefore, cost calculation through absorption costing method can be

described as below: -

7

Illustration 1: Income statement through marginal costing

14400 that is difference of revenue (21000) and cost incurred over expenses (6600). Further,

management accountant of Nisa determines net profit that is subtraction of gross profit to

variable expenses. Under which, variable expenditure includes production overhead as 1200

and sales expenses as 600. Therefore, overall variable expenditure is obtained as 1800 that is

useful to determine net profit. However, through marginal costing gross profit for transaction of

groceries is determined as 14400 and net profit is 12600.

Absorption costing method: -

Under this method, fixed overhead is also added to determine net profit for production

and distribution system. Therefore, cost calculation through absorption costing method can be

described as below: -

7

Illustration 1: Income statement through marginal costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

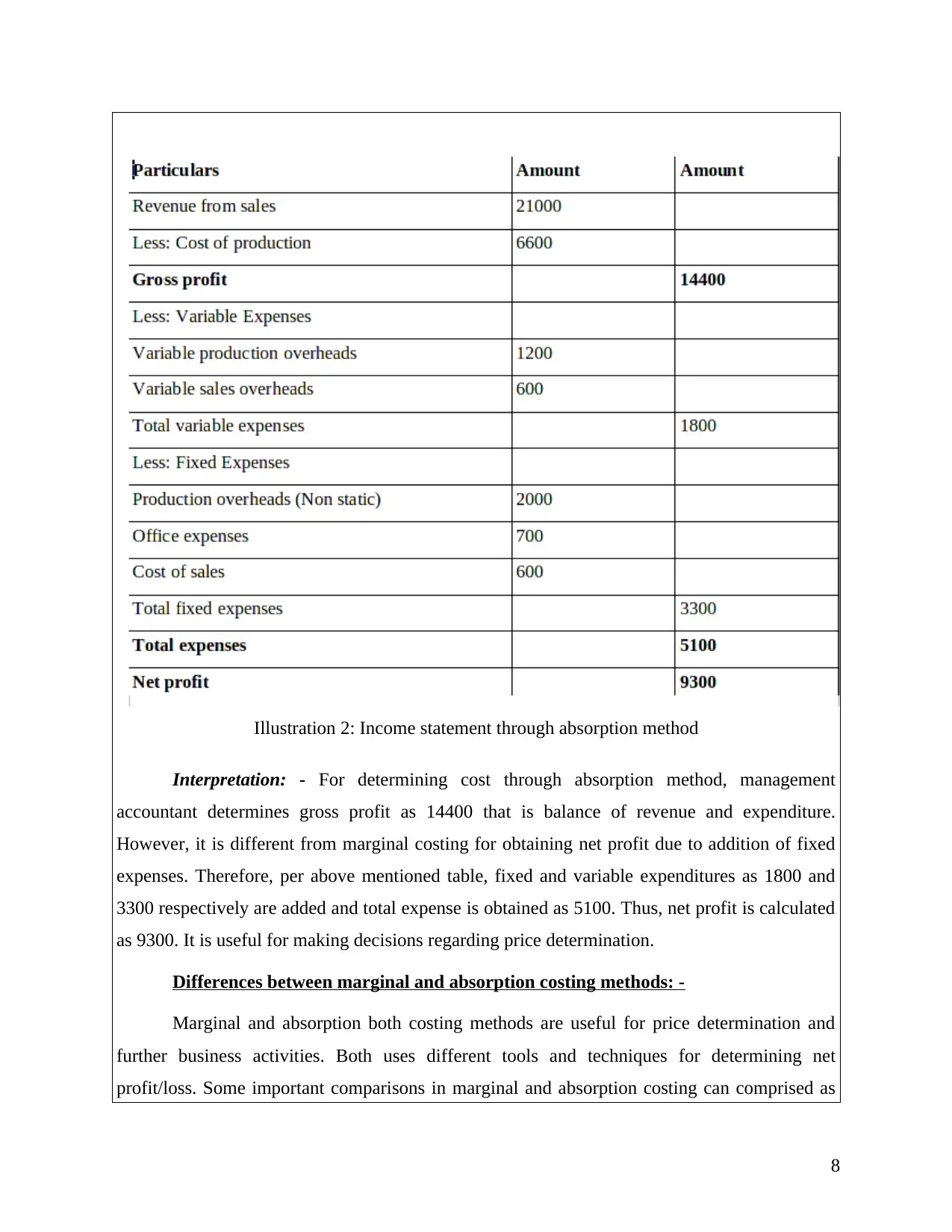

Interpretation: - For determining cost through absorption method, management

accountant determines gross profit as 14400 that is balance of revenue and expenditure.

However, it is different from marginal costing for obtaining net profit due to addition of fixed

expenses. Therefore, per above mentioned table, fixed and variable expenditures as 1800 and

3300 respectively are added and total expense is obtained as 5100. Thus, net profit is calculated

as 9300. It is useful for making decisions regarding price determination.

Differences between marginal and absorption costing methods: -

Marginal and absorption both costing methods are useful for price determination and

further business activities. Both uses different tools and techniques for determining net

profit/loss. Some important comparisons in marginal and absorption costing can comprised as

8

Illustration 2: Income statement through absorption method

accountant determines gross profit as 14400 that is balance of revenue and expenditure.

However, it is different from marginal costing for obtaining net profit due to addition of fixed

expenses. Therefore, per above mentioned table, fixed and variable expenditures as 1800 and

3300 respectively are added and total expense is obtained as 5100. Thus, net profit is calculated

as 9300. It is useful for making decisions regarding price determination.

Differences between marginal and absorption costing methods: -

Marginal and absorption both costing methods are useful for price determination and

further business activities. Both uses different tools and techniques for determining net

profit/loss. Some important comparisons in marginal and absorption costing can comprised as

8

Illustration 2: Income statement through absorption method

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

follows: -

Measurement of profit: - In marginal costing, net profit is measured by profit volume

ratio. In which, fixed overhead is not included. For computing net profit, there is only balance

of gross profit to total variable costs is obtained. While on the other side, under absorption

costing method, fixed expenditures are included for obtaining net profit (Corona, Nan and

Zhang, 2014).

Focuses on: - Marginal costing emphasis on selling and pricing of goods while

absorption costing concentrates on production of products. Therefore, different techniques are

obtained for price determination approach. For different visions, different methods are used

regarding cost efficiency.

Belief: - Both marginal and absorption costing methods have different beliefs.

Absorption costing is considered that there is need to add fixed overhead for decision making

appropriately. In comparison to absorption, marginal costing believes that only variable

expenses are appropriate for price determination and preparing income statement (Germak and

et.al., 2014). However, it is determined that both approaches are different from each other for

determining price of goods and services.

Time periodicity: - Managerial decisions are taken regarding marginal and absorption

costing. It is obtained that marginal costing is useful for fulfilling tasks in short time while

absorption costing is valuable for long term managerial decisions. In this regard, for short term

planning strategy, management accountant uses marginal costing while for long term decisions,

absorption costing is applied.

Thus, marginal and absorption costing are different for various aspects bases on several

factors. Price determination through both costing remains comprised. In accordance to this,

different techniques are used for cost effectiveness and presenting income statement of firm.

However, management accountant of Nisa uses different costing methods for obtaining various

visions. For short term goals, marginal costing is applied as well for long time period

managerial decision, absorption method is useful for effectiveness of small scale enterprise

(Zandi and Abdullah, 2015).

9

Measurement of profit: - In marginal costing, net profit is measured by profit volume

ratio. In which, fixed overhead is not included. For computing net profit, there is only balance

of gross profit to total variable costs is obtained. While on the other side, under absorption

costing method, fixed expenditures are included for obtaining net profit (Corona, Nan and

Zhang, 2014).

Focuses on: - Marginal costing emphasis on selling and pricing of goods while

absorption costing concentrates on production of products. Therefore, different techniques are

obtained for price determination approach. For different visions, different methods are used

regarding cost efficiency.

Belief: - Both marginal and absorption costing methods have different beliefs.

Absorption costing is considered that there is need to add fixed overhead for decision making

appropriately. In comparison to absorption, marginal costing believes that only variable

expenses are appropriate for price determination and preparing income statement (Germak and

et.al., 2014). However, it is determined that both approaches are different from each other for

determining price of goods and services.

Time periodicity: - Managerial decisions are taken regarding marginal and absorption

costing. It is obtained that marginal costing is useful for fulfilling tasks in short time while

absorption costing is valuable for long term managerial decisions. In this regard, for short term

planning strategy, management accountant uses marginal costing while for long term decisions,

absorption costing is applied.

Thus, marginal and absorption costing are different for various aspects bases on several

factors. Price determination through both costing remains comprised. In accordance to this,

different techniques are used for cost effectiveness and presenting income statement of firm.

However, management accountant of Nisa uses different costing methods for obtaining various

visions. For short term goals, marginal costing is applied as well for long time period

managerial decision, absorption method is useful for effectiveness of small scale enterprise

(Zandi and Abdullah, 2015).

9

Report on management accounting, its systems and costing methods:

General Manager

Nisa Ltd

Date: 1st September 2017

Subject: A report covering management accounting and its systems together with different

costing techniques and reporting enable Nisa Ltd.

In this report, we are going to discuss about management accounting and its systems'

essential requirements for forecasting and decision making regarding further business

operations. However, management accounting systems as financial, cost, performance,

inventory and risk management systems are described affect management of entire business

operations. In addition to this, management accounting reports as performance management

report, account receivable, inventory management and job order costing have been understood

remain crucial to present financial, liquidity and performance management tools for the small

scale enterprise. Including this, income statements using marginal and absorption costing

methods are described affect profit margin and management of business operations are

identified through this report. Therefore, good understanding towards management accounting

and its systems' is increased through this assignment for decision making regarding further

implementations and management of entire business operations of the small scale enterprise.

TASK 3

P4) Different planning tools and their evaluations for budgetary control

General Manager

Nisa Ltd

Budgetary control is an approach for formulating strategies regrading business activities.

It involves planning and evaluation for systematic management of organization including

services provided by company. In this regard, management accountant of Nisa identifies

financial statements including profit and loss account, balance sheet, income statement and all

10

General Manager

Nisa Ltd

Date: 1st September 2017

Subject: A report covering management accounting and its systems together with different

costing techniques and reporting enable Nisa Ltd.

In this report, we are going to discuss about management accounting and its systems'

essential requirements for forecasting and decision making regarding further business

operations. However, management accounting systems as financial, cost, performance,

inventory and risk management systems are described affect management of entire business

operations. In addition to this, management accounting reports as performance management

report, account receivable, inventory management and job order costing have been understood

remain crucial to present financial, liquidity and performance management tools for the small

scale enterprise. Including this, income statements using marginal and absorption costing

methods are described affect profit margin and management of business operations are

identified through this report. Therefore, good understanding towards management accounting

and its systems' is increased through this assignment for decision making regarding further

implementations and management of entire business operations of the small scale enterprise.

TASK 3

P4) Different planning tools and their evaluations for budgetary control

General Manager

Nisa Ltd

Budgetary control is an approach for formulating strategies regrading business activities.

It involves planning and evaluation for systematic management of organization including

services provided by company. In this regard, management accountant of Nisa identifies

financial statements including profit and loss account, balance sheet, income statement and all

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.