Ola plc: A Financial Accountability and Strategic Analysis Report

VerifiedAdded on 2023/06/13

|14

|3238

|446

Report

AI Summary

This report provides a comprehensive financial analysis of Ola plc, Ireland's largest oil-based product manufacturer. It assesses the company's financial accountability, focusing on its cost leadership strategy and its impact on profitability and quality. The report includes an income statement, breakeven point analysis (in units and monetary value), desired sales calculations for increased profit targets, and margin of safety assessment. It also anticipates breakeven points for the upcoming year, considering projected changes in sales and costs. The analysis identifies areas for improvement, particularly in addressing quality issues and production bottlenecks, and offers recommendations for enhancing financial performance and strategic decision-making. This document is available on Desklib, a platform offering study tools and solved assignments for students.

Running Head: Managing for Financial accountability

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing for Financial accountability 2

Contents

Introduction.......................................................................................................................3

Income statement of the company....................................................................................4

Breakeven point in units...................................................................................................5

Breakeven point in monetary value..................................................................................5

Desired sales units............................................................................................................6

Desired sales in monetary value.......................................................................................7

Margin of safety................................................................................................................8

Desired sales units............................................................................................................9

Anticipates breakeven point...........................................................................................10

Recommendations...........................................................................................................11

Conclusion......................................................................................................................12

References.......................................................................................................................13

Contents

Introduction.......................................................................................................................3

Income statement of the company....................................................................................4

Breakeven point in units...................................................................................................5

Breakeven point in monetary value..................................................................................5

Desired sales units............................................................................................................6

Desired sales in monetary value.......................................................................................7

Margin of safety................................................................................................................8

Desired sales units............................................................................................................9

Anticipates breakeven point...........................................................................................10

Recommendations...........................................................................................................11

Conclusion......................................................................................................................12

References.......................................................................................................................13

Managing for Financial accountability 3

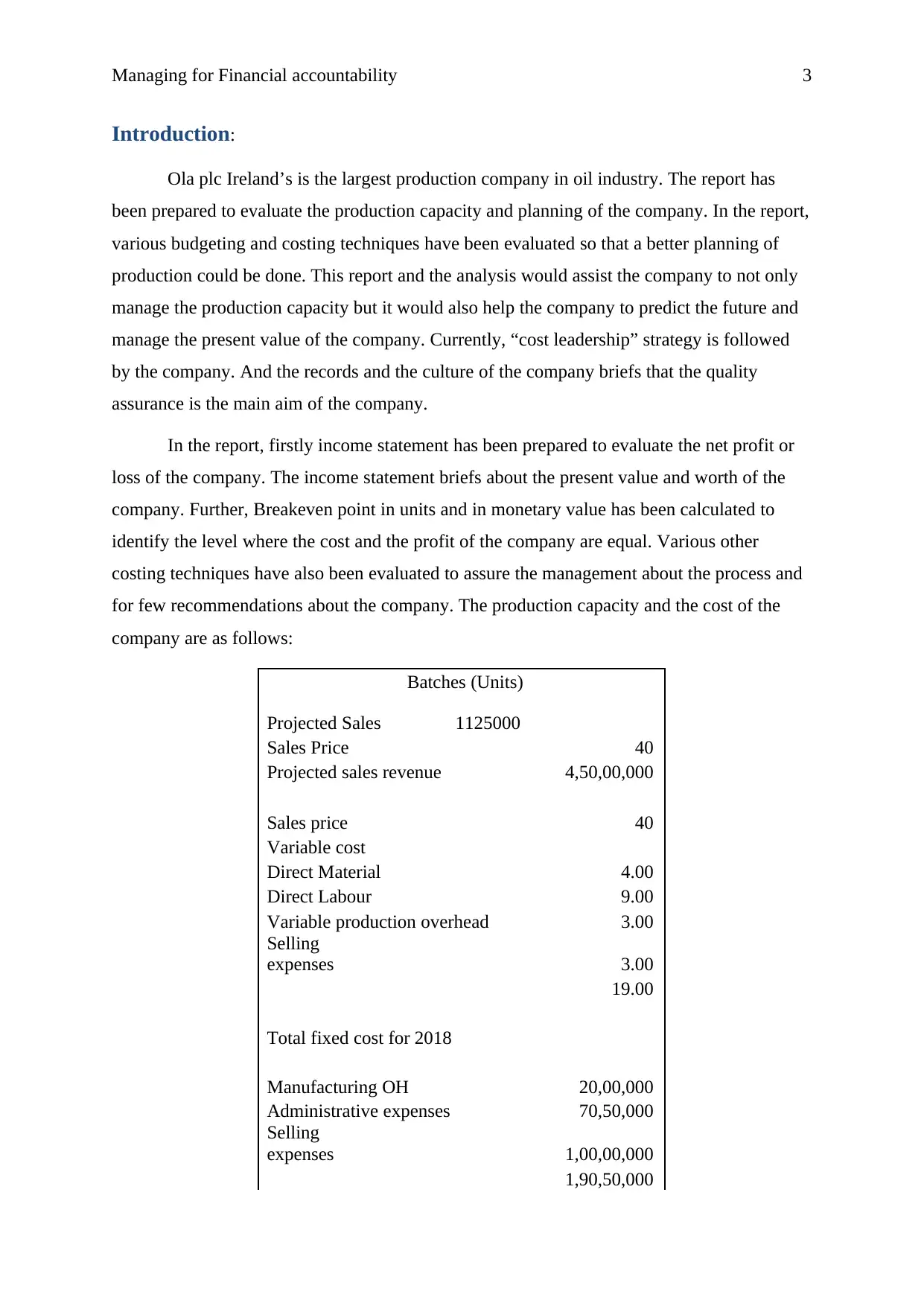

Introduction:

Ola plc Ireland’s is the largest production company in oil industry. The report has

been prepared to evaluate the production capacity and planning of the company. In the report,

various budgeting and costing techniques have been evaluated so that a better planning of

production could be done. This report and the analysis would assist the company to not only

manage the production capacity but it would also help the company to predict the future and

manage the present value of the company. Currently, “cost leadership” strategy is followed

by the company. And the records and the culture of the company briefs that the quality

assurance is the main aim of the company.

In the report, firstly income statement has been prepared to evaluate the net profit or

loss of the company. The income statement briefs about the present value and worth of the

company. Further, Breakeven point in units and in monetary value has been calculated to

identify the level where the cost and the profit of the company are equal. Various other

costing techniques have also been evaluated to assure the management about the process and

for few recommendations about the company. The production capacity and the cost of the

company are as follows:

Batches (Units)

Projected Sales 1125000

Sales Price 40

Projected sales revenue 4,50,00,000

Sales price 40

Variable cost

Direct Material 4.00

Direct Labour 9.00

Variable production overhead 3.00

Selling

expenses 3.00

19.00

Total fixed cost for 2018

Manufacturing OH 20,00,000

Administrative expenses 70,50,000

Selling

expenses 1,00,00,000

1,90,50,000

Introduction:

Ola plc Ireland’s is the largest production company in oil industry. The report has

been prepared to evaluate the production capacity and planning of the company. In the report,

various budgeting and costing techniques have been evaluated so that a better planning of

production could be done. This report and the analysis would assist the company to not only

manage the production capacity but it would also help the company to predict the future and

manage the present value of the company. Currently, “cost leadership” strategy is followed

by the company. And the records and the culture of the company briefs that the quality

assurance is the main aim of the company.

In the report, firstly income statement has been prepared to evaluate the net profit or

loss of the company. The income statement briefs about the present value and worth of the

company. Further, Breakeven point in units and in monetary value has been calculated to

identify the level where the cost and the profit of the company are equal. Various other

costing techniques have also been evaluated to assure the management about the process and

for few recommendations about the company. The production capacity and the cost of the

company are as follows:

Batches (Units)

Projected Sales 1125000

Sales Price 40

Projected sales revenue 4,50,00,000

Sales price 40

Variable cost

Direct Material 4.00

Direct Labour 9.00

Variable production overhead 3.00

Selling

expenses 3.00

19.00

Total fixed cost for 2018

Manufacturing OH 20,00,000

Administrative expenses 70,50,000

Selling

expenses 1,00,00,000

1,90,50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing for Financial accountability 4

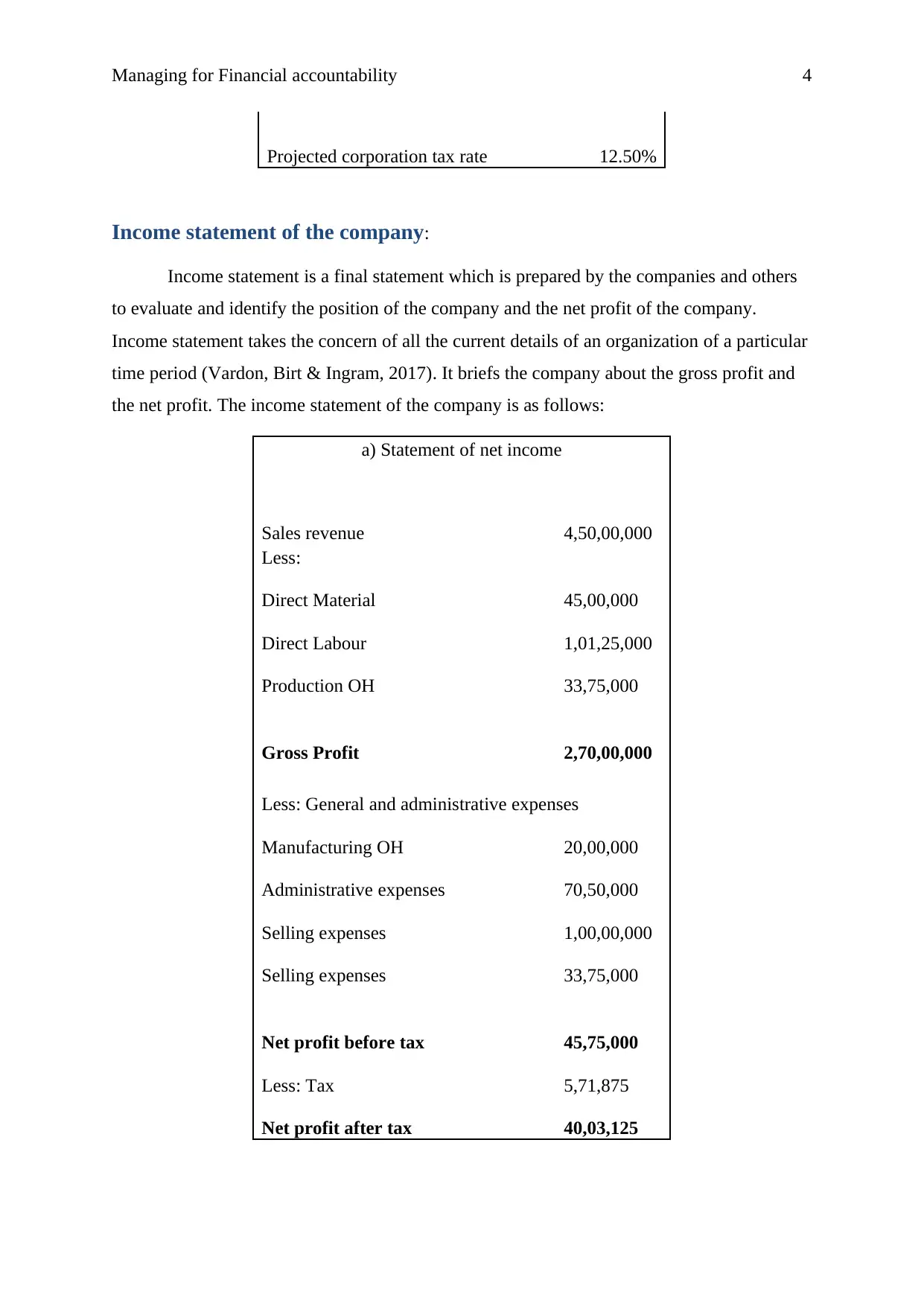

Projected corporation tax rate 12.50%

Income statement of the company:

Income statement is a final statement which is prepared by the companies and others

to evaluate and identify the position of the company and the net profit of the company.

Income statement takes the concern of all the current details of an organization of a particular

time period (Vardon, Birt & Ingram, 2017). It briefs the company about the gross profit and

the net profit. The income statement of the company is as follows:

a) Statement of net income

Sales revenue 4,50,00,000

Less:

Direct Material 45,00,000

Direct Labour 1,01,25,000

Production OH 33,75,000

Gross Profit 2,70,00,000

Less: General and administrative expenses

Manufacturing OH 20,00,000

Administrative expenses 70,50,000

Selling expenses 1,00,00,000

Selling expenses 33,75,000

Net profit before tax 45,75,000

Less: Tax 5,71,875

Net profit after tax 40,03,125

Projected corporation tax rate 12.50%

Income statement of the company:

Income statement is a final statement which is prepared by the companies and others

to evaluate and identify the position of the company and the net profit of the company.

Income statement takes the concern of all the current details of an organization of a particular

time period (Vardon, Birt & Ingram, 2017). It briefs the company about the gross profit and

the net profit. The income statement of the company is as follows:

a) Statement of net income

Sales revenue 4,50,00,000

Less:

Direct Material 45,00,000

Direct Labour 1,01,25,000

Production OH 33,75,000

Gross Profit 2,70,00,000

Less: General and administrative expenses

Manufacturing OH 20,00,000

Administrative expenses 70,50,000

Selling expenses 1,00,00,000

Selling expenses 33,75,000

Net profit before tax 45,75,000

Less: Tax 5,71,875

Net profit after tax 40,03,125

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing for Financial accountability 5

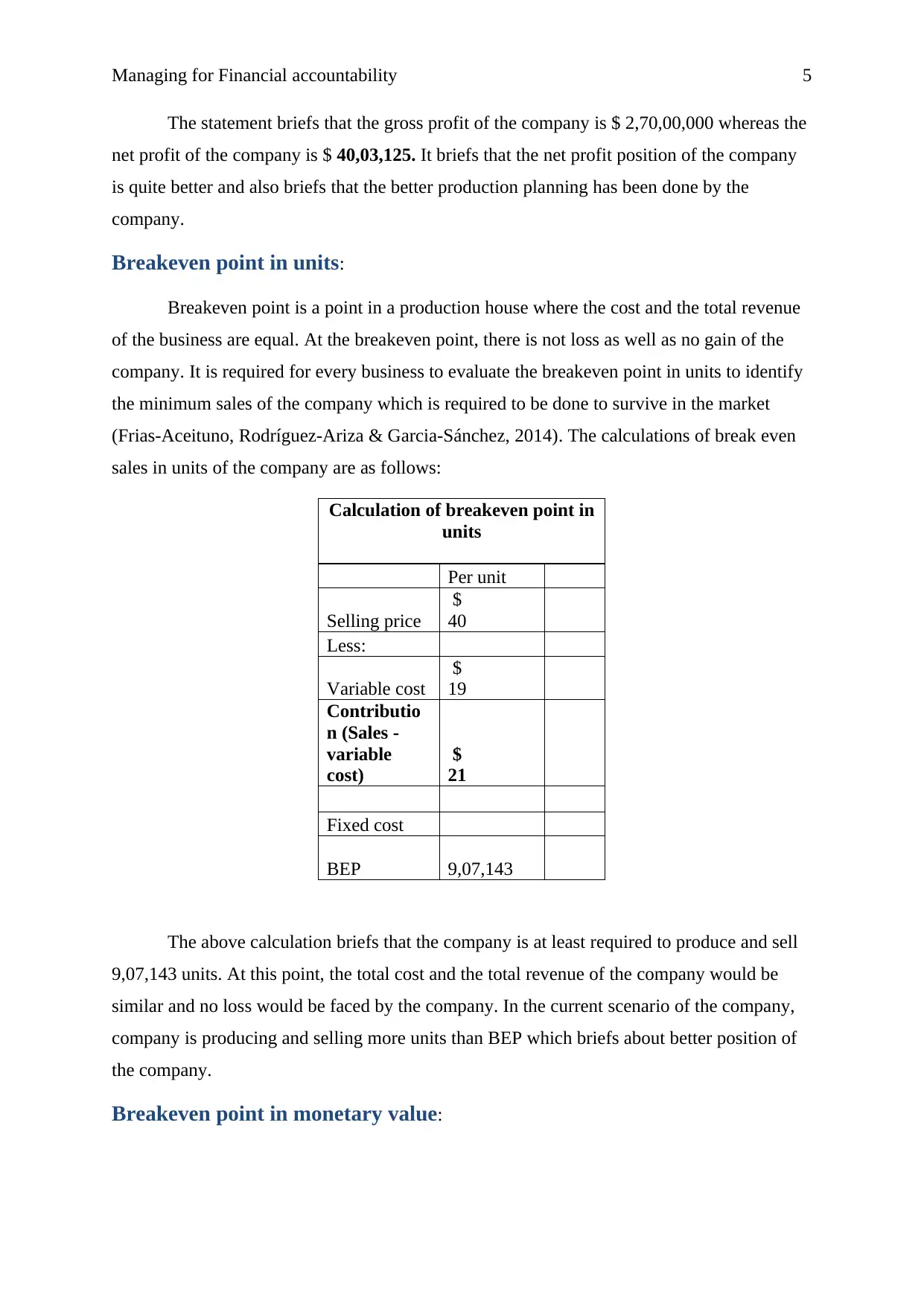

The statement briefs that the gross profit of the company is $ 2,70,00,000 whereas the

net profit of the company is $ 40,03,125. It briefs that the net profit position of the company

is quite better and also briefs that the better production planning has been done by the

company.

Breakeven point in units:

Breakeven point is a point in a production house where the cost and the total revenue

of the business are equal. At the breakeven point, there is not loss as well as no gain of the

company. It is required for every business to evaluate the breakeven point in units to identify

the minimum sales of the company which is required to be done to survive in the market

(Frias‐Aceituno, Rodríguez‐Ariza & Garcia‐Sánchez, 2014). The calculations of break even

sales in units of the company are as follows:

Calculation of breakeven point in

units

Per unit

Selling price

$

40

Less:

Variable cost

$

19

Contributio

n (Sales -

variable

cost)

$

21

Fixed cost

BEP 9,07,143

The above calculation briefs that the company is at least required to produce and sell

9,07,143 units. At this point, the total cost and the total revenue of the company would be

similar and no loss would be faced by the company. In the current scenario of the company,

company is producing and selling more units than BEP which briefs about better position of

the company.

Breakeven point in monetary value:

The statement briefs that the gross profit of the company is $ 2,70,00,000 whereas the

net profit of the company is $ 40,03,125. It briefs that the net profit position of the company

is quite better and also briefs that the better production planning has been done by the

company.

Breakeven point in units:

Breakeven point is a point in a production house where the cost and the total revenue

of the business are equal. At the breakeven point, there is not loss as well as no gain of the

company. It is required for every business to evaluate the breakeven point in units to identify

the minimum sales of the company which is required to be done to survive in the market

(Frias‐Aceituno, Rodríguez‐Ariza & Garcia‐Sánchez, 2014). The calculations of break even

sales in units of the company are as follows:

Calculation of breakeven point in

units

Per unit

Selling price

$

40

Less:

Variable cost

$

19

Contributio

n (Sales -

variable

cost)

$

21

Fixed cost

BEP 9,07,143

The above calculation briefs that the company is at least required to produce and sell

9,07,143 units. At this point, the total cost and the total revenue of the company would be

similar and no loss would be faced by the company. In the current scenario of the company,

company is producing and selling more units than BEP which briefs about better position of

the company.

Breakeven point in monetary value:

Managing for Financial accountability 6

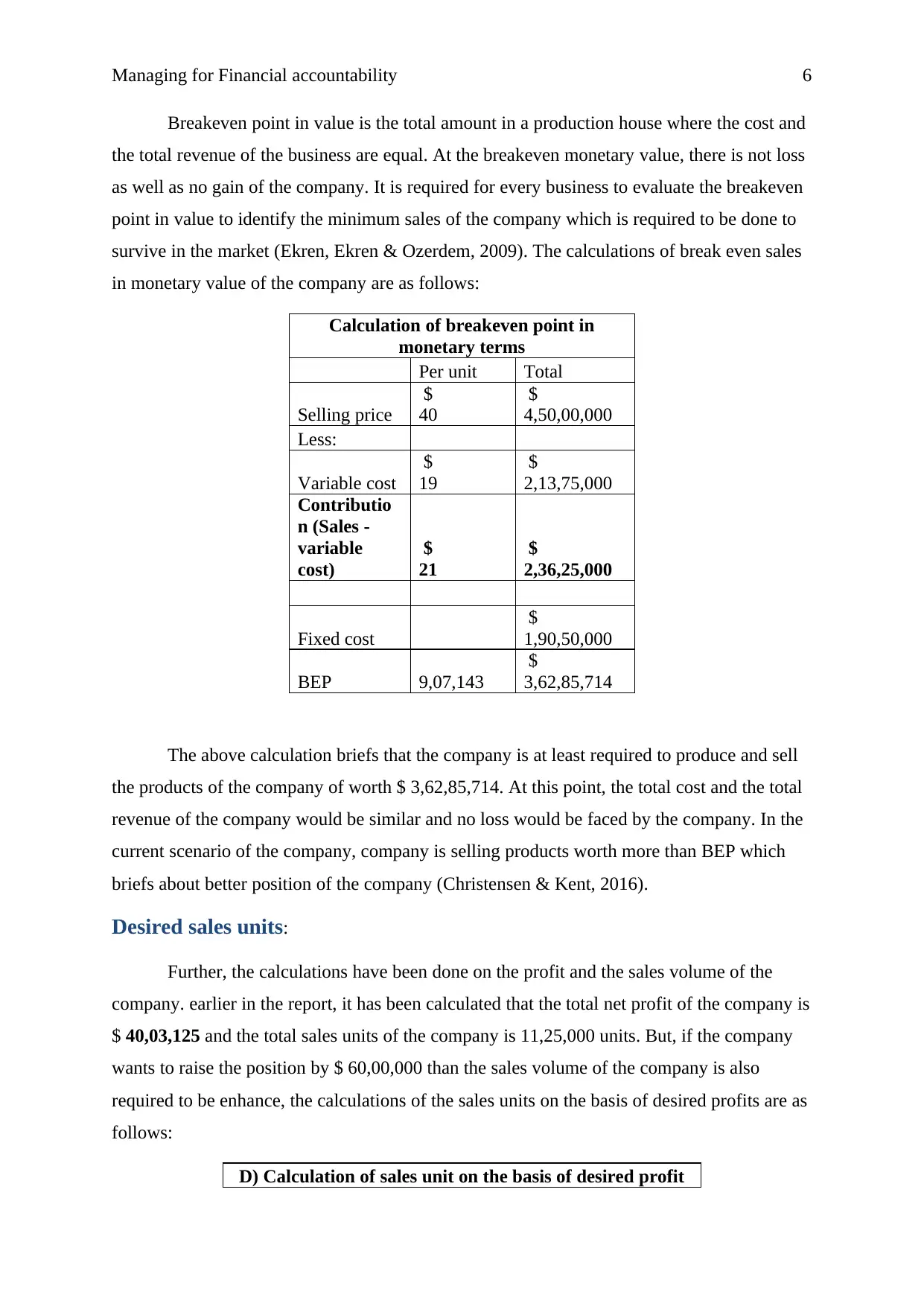

Breakeven point in value is the total amount in a production house where the cost and

the total revenue of the business are equal. At the breakeven monetary value, there is not loss

as well as no gain of the company. It is required for every business to evaluate the breakeven

point in value to identify the minimum sales of the company which is required to be done to

survive in the market (Ekren, Ekren & Ozerdem, 2009). The calculations of break even sales

in monetary value of the company are as follows:

Calculation of breakeven point in

monetary terms

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contributio

n (Sales -

variable

cost)

$

21

$

2,36,25,000

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

The above calculation briefs that the company is at least required to produce and sell

the products of the company of worth $ 3,62,85,714. At this point, the total cost and the total

revenue of the company would be similar and no loss would be faced by the company. In the

current scenario of the company, company is selling products worth more than BEP which

briefs about better position of the company (Christensen & Kent, 2016).

Desired sales units:

Further, the calculations have been done on the profit and the sales volume of the

company. earlier in the report, it has been calculated that the total net profit of the company is

$ 40,03,125 and the total sales units of the company is 11,25,000 units. But, if the company

wants to raise the position by $ 60,00,000 than the sales volume of the company is also

required to be enhance, the calculations of the sales units on the basis of desired profits are as

follows:

D) Calculation of sales unit on the basis of desired profit

Breakeven point in value is the total amount in a production house where the cost and

the total revenue of the business are equal. At the breakeven monetary value, there is not loss

as well as no gain of the company. It is required for every business to evaluate the breakeven

point in value to identify the minimum sales of the company which is required to be done to

survive in the market (Ekren, Ekren & Ozerdem, 2009). The calculations of break even sales

in monetary value of the company are as follows:

Calculation of breakeven point in

monetary terms

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contributio

n (Sales -

variable

cost)

$

21

$

2,36,25,000

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

The above calculation briefs that the company is at least required to produce and sell

the products of the company of worth $ 3,62,85,714. At this point, the total cost and the total

revenue of the company would be similar and no loss would be faced by the company. In the

current scenario of the company, company is selling products worth more than BEP which

briefs about better position of the company (Christensen & Kent, 2016).

Desired sales units:

Further, the calculations have been done on the profit and the sales volume of the

company. earlier in the report, it has been calculated that the total net profit of the company is

$ 40,03,125 and the total sales units of the company is 11,25,000 units. But, if the company

wants to raise the position by $ 60,00,000 than the sales volume of the company is also

required to be enhance, the calculations of the sales units on the basis of desired profits are as

follows:

D) Calculation of sales unit on the basis of desired profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing for Financial accountability 7

Per unit

Selling price

$

40

Less:

Variable cost

$

19

Contribution (Sales -

variable cost)

$

21

Fixed cost

BEP 9,07,143

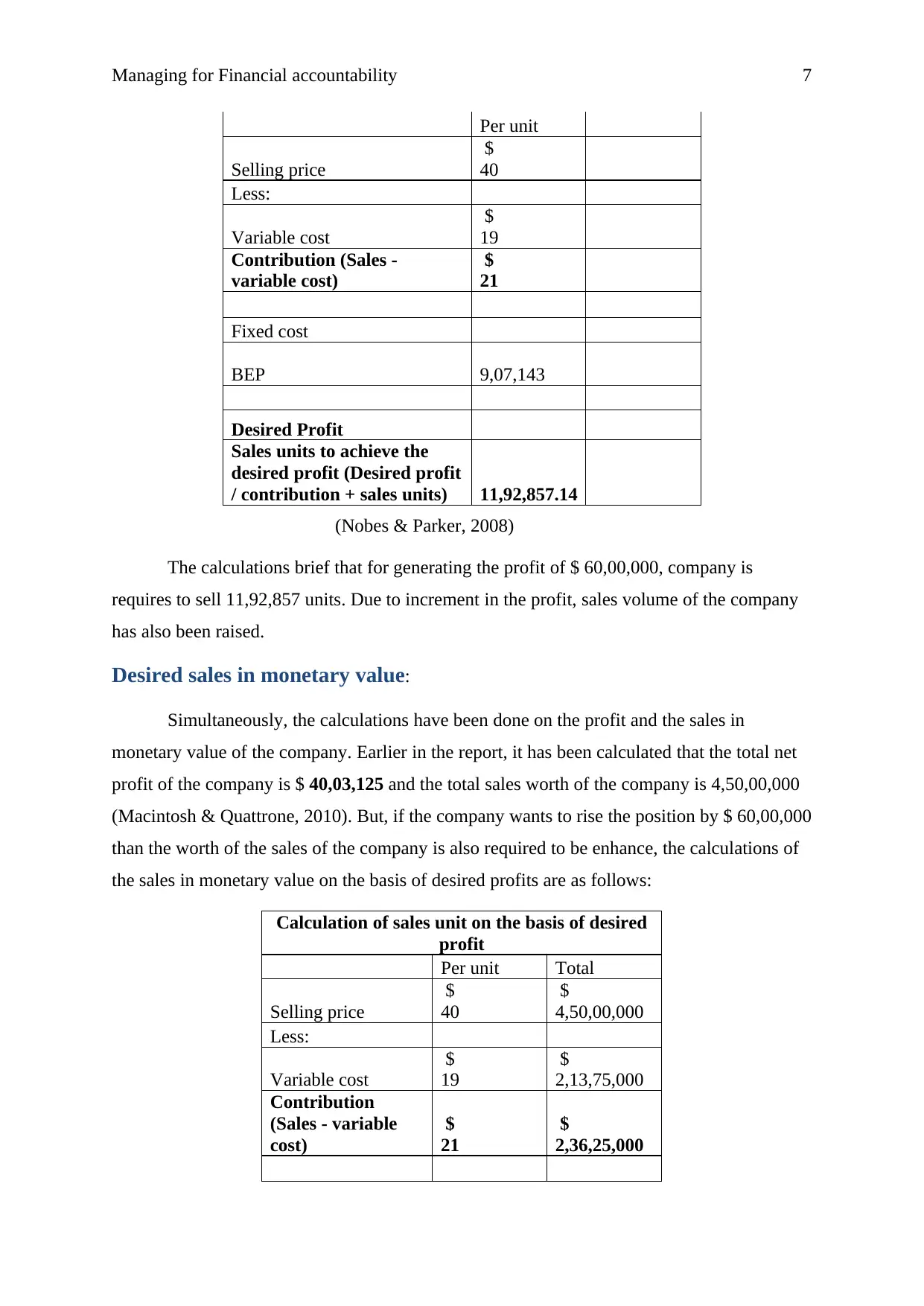

Desired Profit

Sales units to achieve the

desired profit (Desired profit

/ contribution + sales units) 11,92,857.14

(Nobes & Parker, 2008)

The calculations brief that for generating the profit of $ 60,00,000, company is

requires to sell 11,92,857 units. Due to increment in the profit, sales volume of the company

has also been raised.

Desired sales in monetary value:

Simultaneously, the calculations have been done on the profit and the sales in

monetary value of the company. Earlier in the report, it has been calculated that the total net

profit of the company is $ 40,03,125 and the total sales worth of the company is 4,50,00,000

(Macintosh & Quattrone, 2010). But, if the company wants to rise the position by $ 60,00,000

than the worth of the sales of the company is also required to be enhance, the calculations of

the sales in monetary value on the basis of desired profits are as follows:

Calculation of sales unit on the basis of desired

profit

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contribution

(Sales - variable

cost)

$

21

$

2,36,25,000

Per unit

Selling price

$

40

Less:

Variable cost

$

19

Contribution (Sales -

variable cost)

$

21

Fixed cost

BEP 9,07,143

Desired Profit

Sales units to achieve the

desired profit (Desired profit

/ contribution + sales units) 11,92,857.14

(Nobes & Parker, 2008)

The calculations brief that for generating the profit of $ 60,00,000, company is

requires to sell 11,92,857 units. Due to increment in the profit, sales volume of the company

has also been raised.

Desired sales in monetary value:

Simultaneously, the calculations have been done on the profit and the sales in

monetary value of the company. Earlier in the report, it has been calculated that the total net

profit of the company is $ 40,03,125 and the total sales worth of the company is 4,50,00,000

(Macintosh & Quattrone, 2010). But, if the company wants to rise the position by $ 60,00,000

than the worth of the sales of the company is also required to be enhance, the calculations of

the sales in monetary value on the basis of desired profits are as follows:

Calculation of sales unit on the basis of desired

profit

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contribution

(Sales - variable

cost)

$

21

$

2,36,25,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing for Financial accountability 8

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

Desired Profit

$

60,00,000

Sales units to

achieve the desired

profit (Desired

profit /

contribution +

sales units) 11,92,857.14

$

4,77,14,286

(Kieso, Weygandt & Warfield, 2010)

The calculations brief that for generating the profit of $ 60,00,000, company is

requires to enhance the sales worth by $ 4,77,14,286. Due to increment in the profit, worth of

sales of the company has also been raised.

Margin of safety:

Margin of safety is the point where the total sales are reduced by breakeven point.

This point describes about the profit level of the company. This point describes about the

profit or loss position of the organization. The formula of margin of safety is (Sales -

breakeven point) (Zimmerman & Yahya-Zadeh, 2011). The margin of safety level of the

company has been evaluated to recognize the profit position of the company as well as the

total units on which the profit is generated by the company (Ward, 2012).

Margi of safety point of the company has been calculated further on the basis of

1125,000 sales units. The calculations of margin of safety of the company are as follows:

e) Calculation of Margin point

Per unit Total

Selling price $ 40 $ 4,50,00,000

Less:

Variable cost $ 19 $ 2,13,75,000

Contribution (Sales -

variable cost)

$ 21 $ 2,36,25,000

Fixed cost $ 1,90,50,000

Breakeven point

(Fixed cost /

907142.9 36285714.3

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

Desired Profit

$

60,00,000

Sales units to

achieve the desired

profit (Desired

profit /

contribution +

sales units) 11,92,857.14

$

4,77,14,286

(Kieso, Weygandt & Warfield, 2010)

The calculations brief that for generating the profit of $ 60,00,000, company is

requires to enhance the sales worth by $ 4,77,14,286. Due to increment in the profit, worth of

sales of the company has also been raised.

Margin of safety:

Margin of safety is the point where the total sales are reduced by breakeven point.

This point describes about the profit level of the company. This point describes about the

profit or loss position of the organization. The formula of margin of safety is (Sales -

breakeven point) (Zimmerman & Yahya-Zadeh, 2011). The margin of safety level of the

company has been evaluated to recognize the profit position of the company as well as the

total units on which the profit is generated by the company (Ward, 2012).

Margi of safety point of the company has been calculated further on the basis of

1125,000 sales units. The calculations of margin of safety of the company are as follows:

e) Calculation of Margin point

Per unit Total

Selling price $ 40 $ 4,50,00,000

Less:

Variable cost $ 19 $ 2,13,75,000

Contribution (Sales -

variable cost)

$ 21 $ 2,36,25,000

Fixed cost $ 1,90,50,000

Breakeven point

(Fixed cost /

907142.9 36285714.3

Managing for Financial accountability 9

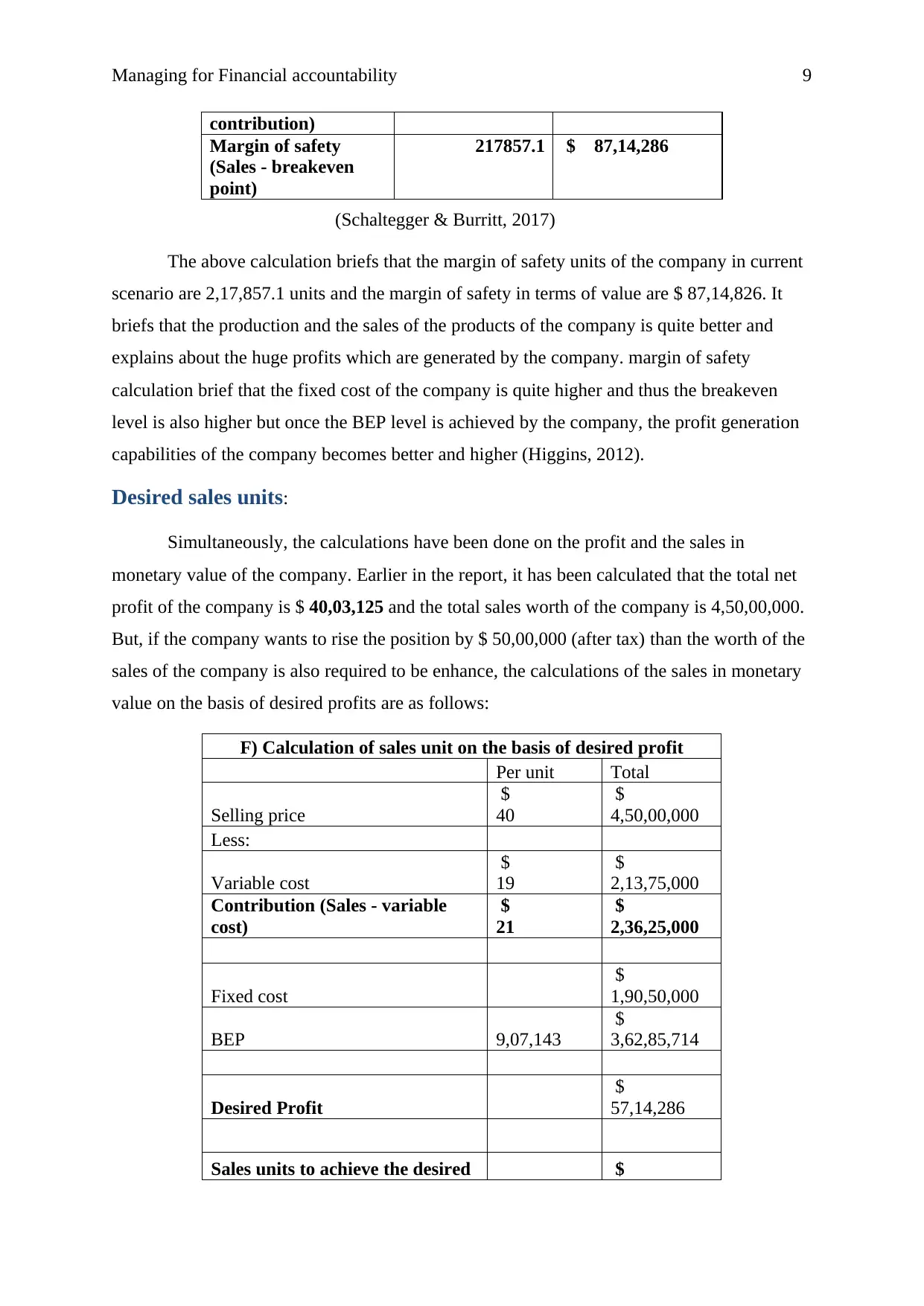

contribution)

Margin of safety

(Sales - breakeven

point)

217857.1 $ 87,14,286

(Schaltegger & Burritt, 2017)

The above calculation briefs that the margin of safety units of the company in current

scenario are 2,17,857.1 units and the margin of safety in terms of value are $ 87,14,826. It

briefs that the production and the sales of the products of the company is quite better and

explains about the huge profits which are generated by the company. margin of safety

calculation brief that the fixed cost of the company is quite higher and thus the breakeven

level is also higher but once the BEP level is achieved by the company, the profit generation

capabilities of the company becomes better and higher (Higgins, 2012).

Desired sales units:

Simultaneously, the calculations have been done on the profit and the sales in

monetary value of the company. Earlier in the report, it has been calculated that the total net

profit of the company is $ 40,03,125 and the total sales worth of the company is 4,50,00,000.

But, if the company wants to rise the position by $ 50,00,000 (after tax) than the worth of the

sales of the company is also required to be enhance, the calculations of the sales in monetary

value on the basis of desired profits are as follows:

F) Calculation of sales unit on the basis of desired profit

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contribution (Sales - variable

cost)

$

21

$

2,36,25,000

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

Desired Profit

$

57,14,286

Sales units to achieve the desired $

contribution)

Margin of safety

(Sales - breakeven

point)

217857.1 $ 87,14,286

(Schaltegger & Burritt, 2017)

The above calculation briefs that the margin of safety units of the company in current

scenario are 2,17,857.1 units and the margin of safety in terms of value are $ 87,14,826. It

briefs that the production and the sales of the products of the company is quite better and

explains about the huge profits which are generated by the company. margin of safety

calculation brief that the fixed cost of the company is quite higher and thus the breakeven

level is also higher but once the BEP level is achieved by the company, the profit generation

capabilities of the company becomes better and higher (Higgins, 2012).

Desired sales units:

Simultaneously, the calculations have been done on the profit and the sales in

monetary value of the company. Earlier in the report, it has been calculated that the total net

profit of the company is $ 40,03,125 and the total sales worth of the company is 4,50,00,000.

But, if the company wants to rise the position by $ 50,00,000 (after tax) than the worth of the

sales of the company is also required to be enhance, the calculations of the sales in monetary

value on the basis of desired profits are as follows:

F) Calculation of sales unit on the basis of desired profit

Per unit Total

Selling price

$

40

$

4,50,00,000

Less:

Variable cost

$

19

$

2,13,75,000

Contribution (Sales - variable

cost)

$

21

$

2,36,25,000

Fixed cost

$

1,90,50,000

BEP 9,07,143

$

3,62,85,714

Desired Profit

$

57,14,286

Sales units to achieve the desired $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managing for Financial accountability 10

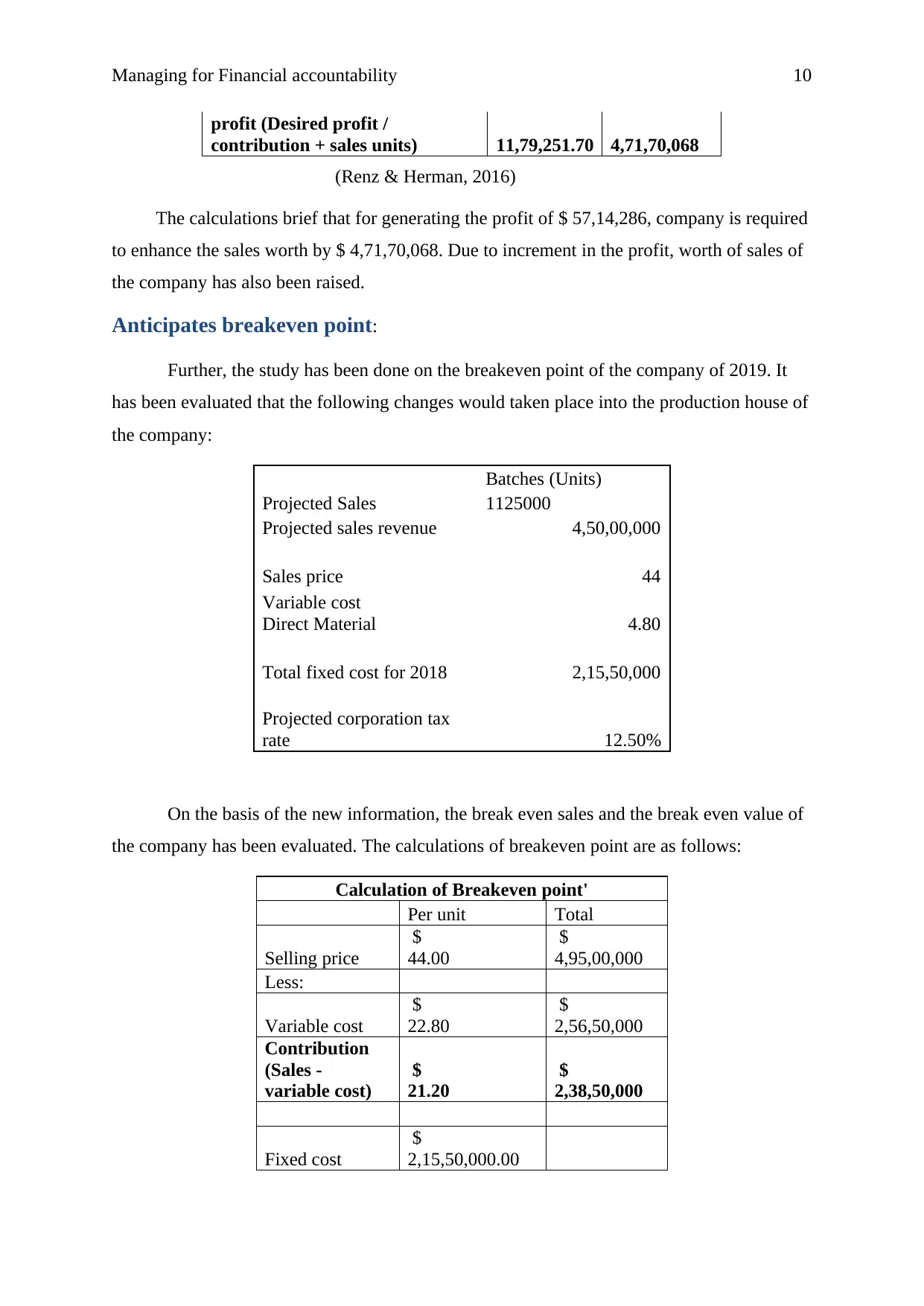

profit (Desired profit /

contribution + sales units) 11,79,251.70 4,71,70,068

(Renz & Herman, 2016)

The calculations brief that for generating the profit of $ 57,14,286, company is required

to enhance the sales worth by $ 4,71,70,068. Due to increment in the profit, worth of sales of

the company has also been raised.

Anticipates breakeven point:

Further, the study has been done on the breakeven point of the company of 2019. It

has been evaluated that the following changes would taken place into the production house of

the company:

Batches (Units)

Projected Sales 1125000

Projected sales revenue 4,50,00,000

Sales price 44

Variable cost

Direct Material 4.80

Total fixed cost for 2018 2,15,50,000

Projected corporation tax

rate 12.50%

On the basis of the new information, the break even sales and the break even value of

the company has been evaluated. The calculations of breakeven point are as follows:

Calculation of Breakeven point'

Per unit Total

Selling price

$

44.00

$

4,95,00,000

Less:

Variable cost

$

22.80

$

2,56,50,000

Contribution

(Sales -

variable cost)

$

21.20

$

2,38,50,000

Fixed cost

$

2,15,50,000.00

profit (Desired profit /

contribution + sales units) 11,79,251.70 4,71,70,068

(Renz & Herman, 2016)

The calculations brief that for generating the profit of $ 57,14,286, company is required

to enhance the sales worth by $ 4,71,70,068. Due to increment in the profit, worth of sales of

the company has also been raised.

Anticipates breakeven point:

Further, the study has been done on the breakeven point of the company of 2019. It

has been evaluated that the following changes would taken place into the production house of

the company:

Batches (Units)

Projected Sales 1125000

Projected sales revenue 4,50,00,000

Sales price 44

Variable cost

Direct Material 4.80

Total fixed cost for 2018 2,15,50,000

Projected corporation tax

rate 12.50%

On the basis of the new information, the break even sales and the break even value of

the company has been evaluated. The calculations of breakeven point are as follows:

Calculation of Breakeven point'

Per unit Total

Selling price

$

44.00

$

4,95,00,000

Less:

Variable cost

$

22.80

$

2,56,50,000

Contribution

(Sales -

variable cost)

$

21.20

$

2,38,50,000

Fixed cost

$

2,15,50,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managing for Financial accountability 11

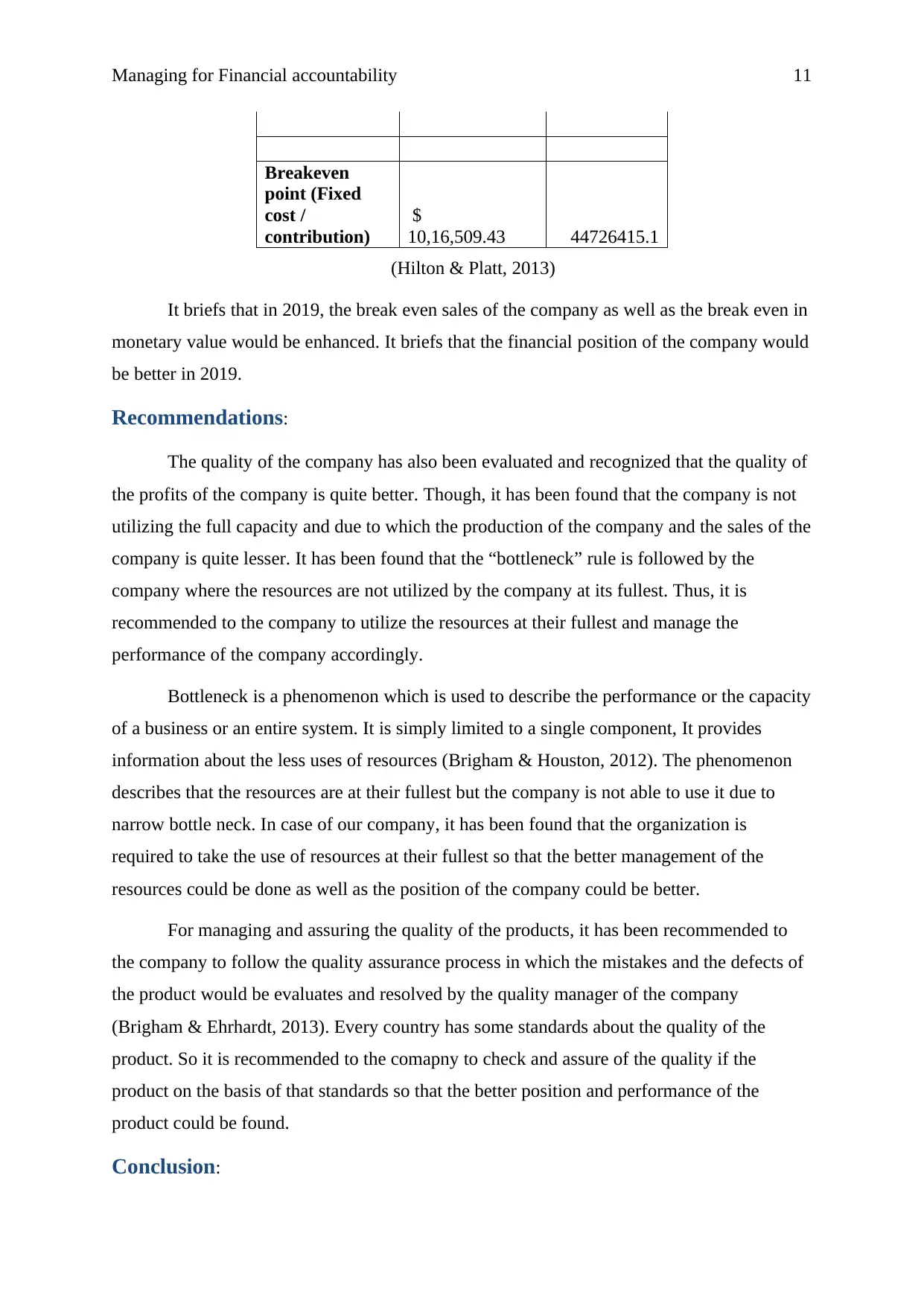

Breakeven

point (Fixed

cost /

contribution)

$

10,16,509.43 44726415.1

(Hilton & Platt, 2013)

It briefs that in 2019, the break even sales of the company as well as the break even in

monetary value would be enhanced. It briefs that the financial position of the company would

be better in 2019.

Recommendations:

The quality of the company has also been evaluated and recognized that the quality of

the profits of the company is quite better. Though, it has been found that the company is not

utilizing the full capacity and due to which the production of the company and the sales of the

company is quite lesser. It has been found that the “bottleneck” rule is followed by the

company where the resources are not utilized by the company at its fullest. Thus, it is

recommended to the company to utilize the resources at their fullest and manage the

performance of the company accordingly.

Bottleneck is a phenomenon which is used to describe the performance or the capacity

of a business or an entire system. It is simply limited to a single component, It provides

information about the less uses of resources (Brigham & Houston, 2012). The phenomenon

describes that the resources are at their fullest but the company is not able to use it due to

narrow bottle neck. In case of our company, it has been found that the organization is

required to take the use of resources at their fullest so that the better management of the

resources could be done as well as the position of the company could be better.

For managing and assuring the quality of the products, it has been recommended to

the company to follow the quality assurance process in which the mistakes and the defects of

the product would be evaluates and resolved by the quality manager of the company

(Brigham & Ehrhardt, 2013). Every country has some standards about the quality of the

product. So it is recommended to the comapny to check and assure of the quality if the

product on the basis of that standards so that the better position and performance of the

product could be found.

Conclusion:

Breakeven

point (Fixed

cost /

contribution)

$

10,16,509.43 44726415.1

(Hilton & Platt, 2013)

It briefs that in 2019, the break even sales of the company as well as the break even in

monetary value would be enhanced. It briefs that the financial position of the company would

be better in 2019.

Recommendations:

The quality of the company has also been evaluated and recognized that the quality of

the profits of the company is quite better. Though, it has been found that the company is not

utilizing the full capacity and due to which the production of the company and the sales of the

company is quite lesser. It has been found that the “bottleneck” rule is followed by the

company where the resources are not utilized by the company at its fullest. Thus, it is

recommended to the company to utilize the resources at their fullest and manage the

performance of the company accordingly.

Bottleneck is a phenomenon which is used to describe the performance or the capacity

of a business or an entire system. It is simply limited to a single component, It provides

information about the less uses of resources (Brigham & Houston, 2012). The phenomenon

describes that the resources are at their fullest but the company is not able to use it due to

narrow bottle neck. In case of our company, it has been found that the organization is

required to take the use of resources at their fullest so that the better management of the

resources could be done as well as the position of the company could be better.

For managing and assuring the quality of the products, it has been recommended to

the company to follow the quality assurance process in which the mistakes and the defects of

the product would be evaluates and resolved by the quality manager of the company

(Brigham & Ehrhardt, 2013). Every country has some standards about the quality of the

product. So it is recommended to the comapny to check and assure of the quality if the

product on the basis of that standards so that the better position and performance of the

product could be found.

Conclusion:

Managing for Financial accountability 12

To conclude, Ola plc Ireland is performing and managing its production house at a

better level. The income statement of the company briefs about the higher net profits of the

company as well as better position of the company. Further, it has been found that if the

company would utilize the resources at the fullest than the breakeven level of the company

would be lesser than the total sales of the company. It further briefs that the margin of safety

level of the company is also higher which directly briefs about the total profit from the

production process of the company. Breakeven point in units and in monetary value has been

calculated to identify the level where the cost and the profit of the company are equal.

Various other costing techniques have also been evaluated to assure the management about

the process and it has been found that the position and the level of the company s quite better.

The future prediction of the company has also been done to found the future

performance of the company and it has been analyzed that the company would perform better

in near future. The sales price of the company would be enhanced. Though, the variable cost

and fixed cost of the company also briefs about some additional cost. To conclude, the

performance of the position of the company is quite better if the company uses the entire

capacity to produce and sell the product.

To conclude, Ola plc Ireland is performing and managing its production house at a

better level. The income statement of the company briefs about the higher net profits of the

company as well as better position of the company. Further, it has been found that if the

company would utilize the resources at the fullest than the breakeven level of the company

would be lesser than the total sales of the company. It further briefs that the margin of safety

level of the company is also higher which directly briefs about the total profit from the

production process of the company. Breakeven point in units and in monetary value has been

calculated to identify the level where the cost and the profit of the company are equal.

Various other costing techniques have also been evaluated to assure the management about

the process and it has been found that the position and the level of the company s quite better.

The future prediction of the company has also been done to found the future

performance of the company and it has been analyzed that the company would perform better

in near future. The sales price of the company would be enhanced. Though, the variable cost

and fixed cost of the company also briefs about some additional cost. To conclude, the

performance of the position of the company is quite better if the company uses the entire

capacity to produce and sell the product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.