ACCT20073 Company Accounting Report: Investment Analysis of Soletta

VerifiedAdded on 2023/06/08

|8

|1010

|202

Report

AI Summary

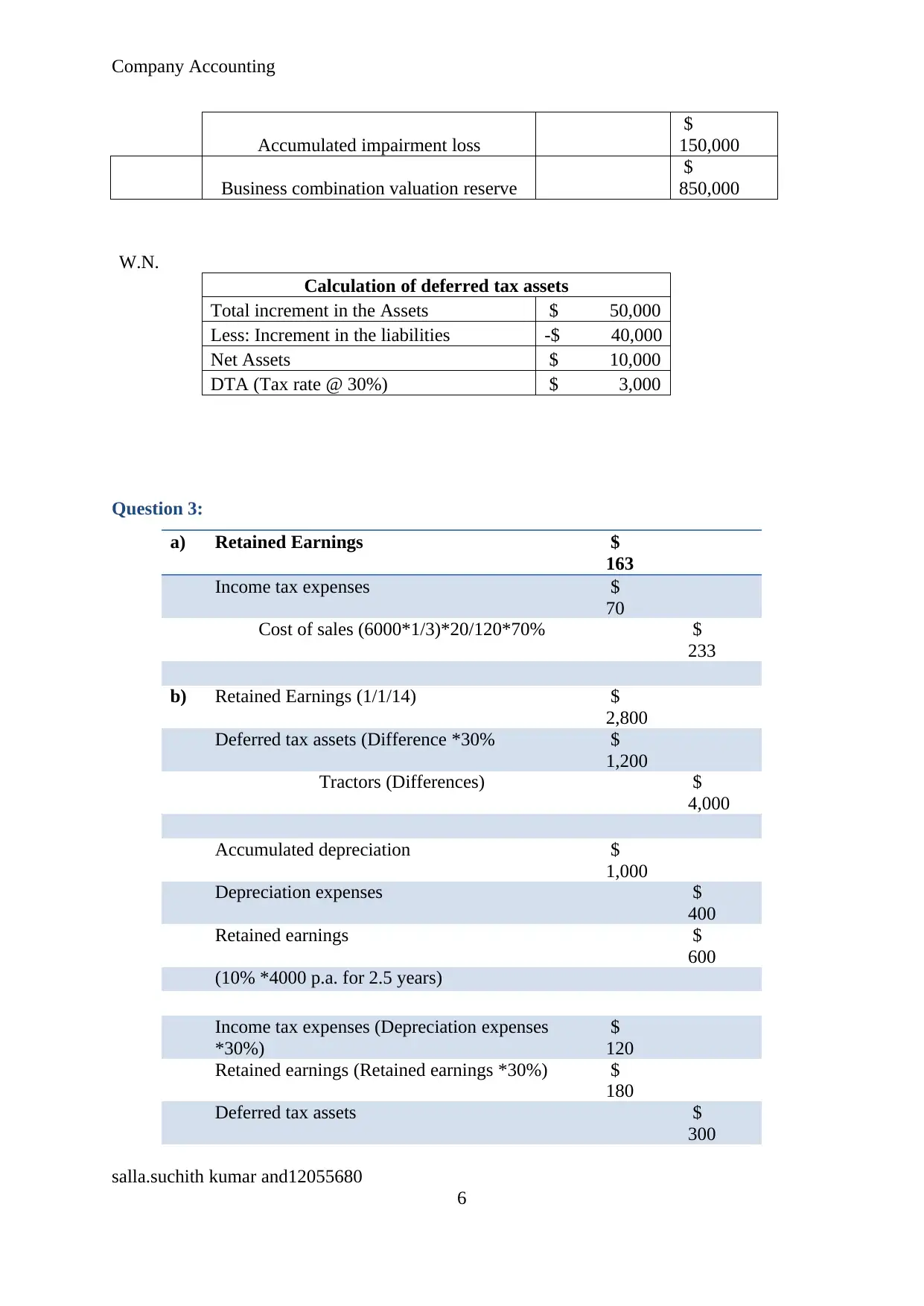

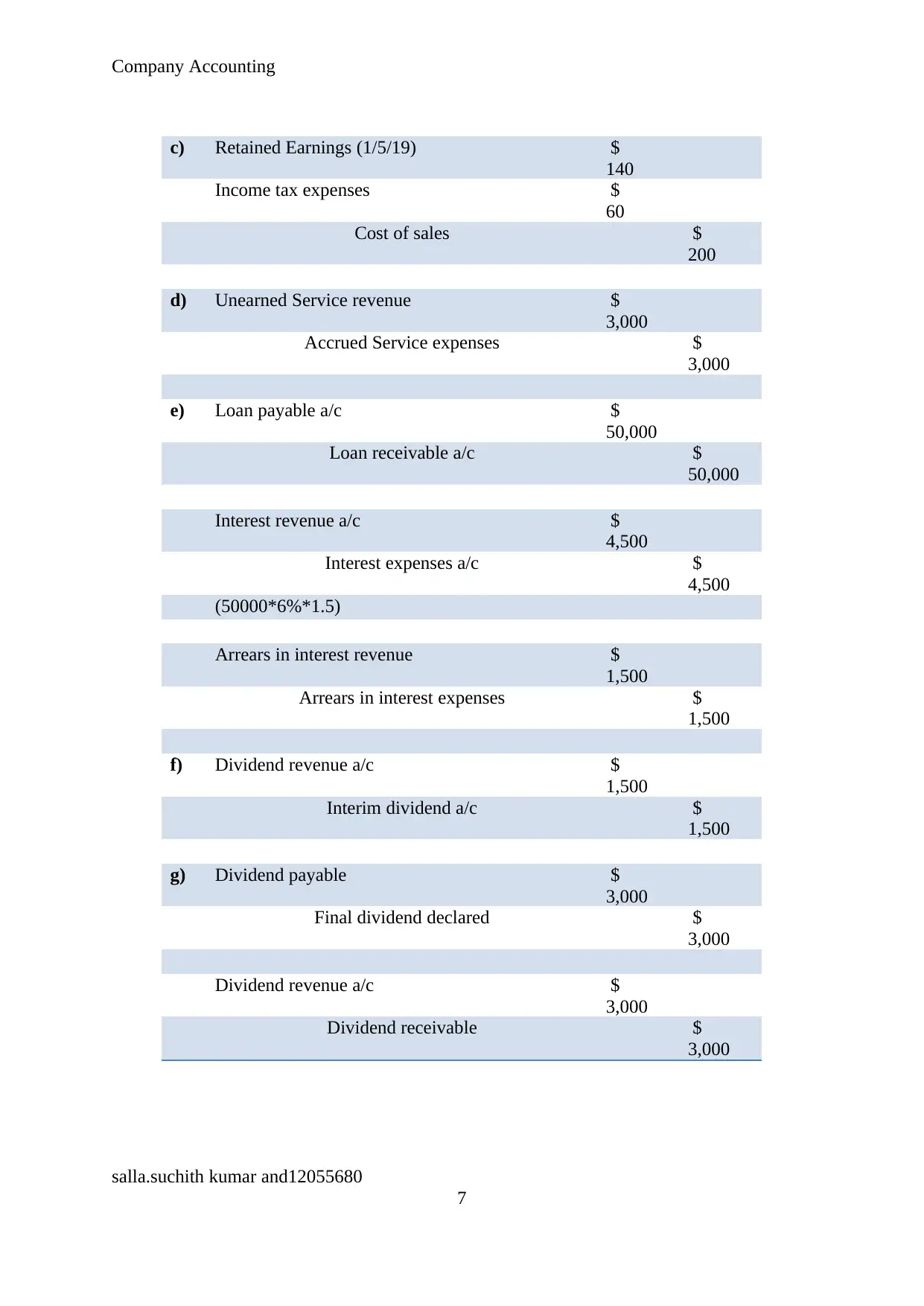

This company accounting project report analyzes Palvidia Ltd's potential investment in Soletta Ltd, covering consolidated financial statements, group company structures, and intra-group transaction adjustments. It includes an acquisition analysis with journal entries, goodwill calculation, and deferred tax asset considerations. Furthermore, the report addresses retained earnings adjustments related to income tax, cost of sales, deferred tax assets, tractors, depreciation, unearned service revenue, accrued service expenses, loan transactions, and dividend distributions. The analysis incorporates calculations and journal entries to accurately reflect the financial implications of these transactions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.