Bank Failures in Australia: Causes, Government Role and Prevention

VerifiedAdded on 2023/06/11

|11

|1142

|127

Report

AI Summary

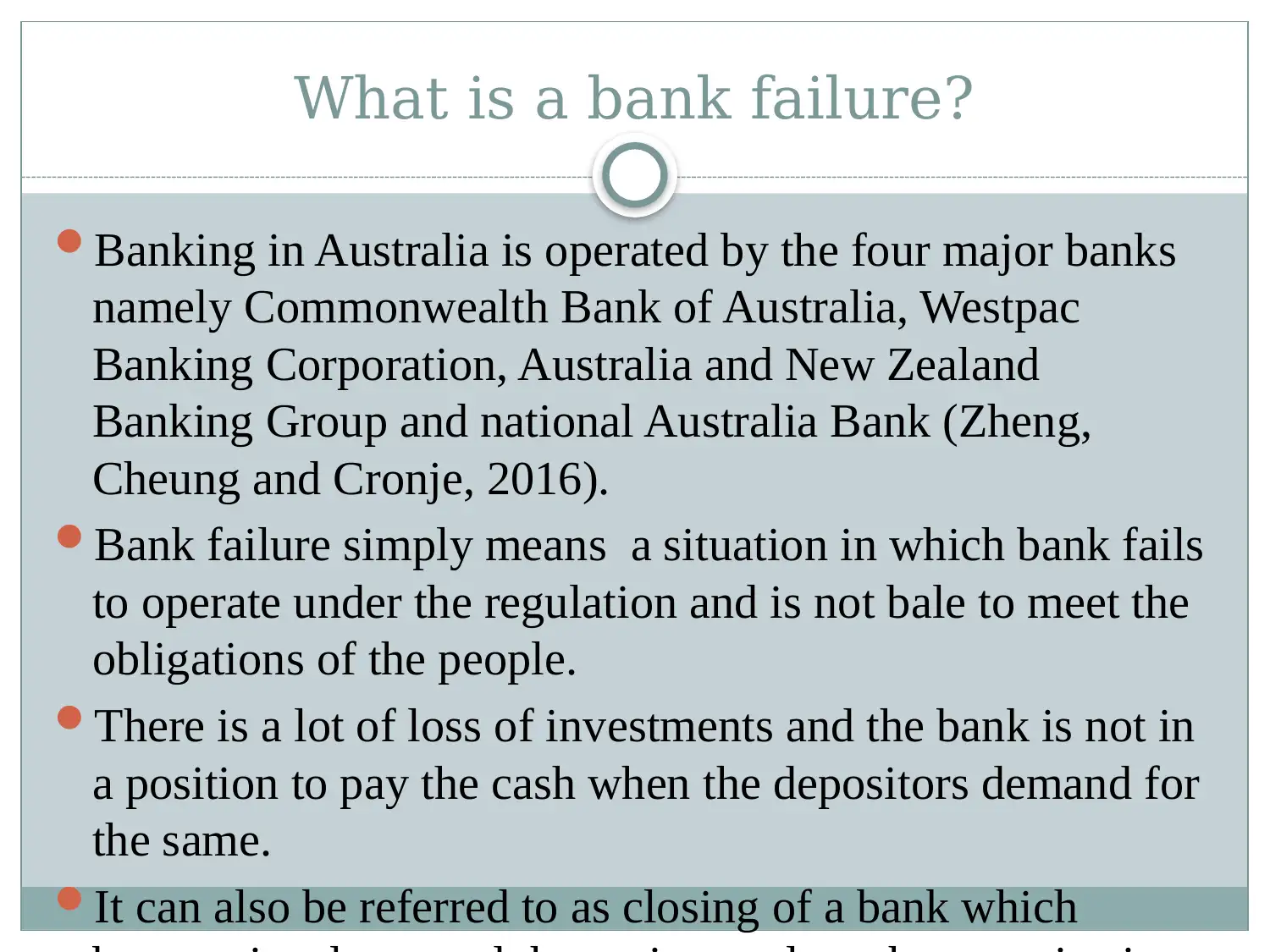

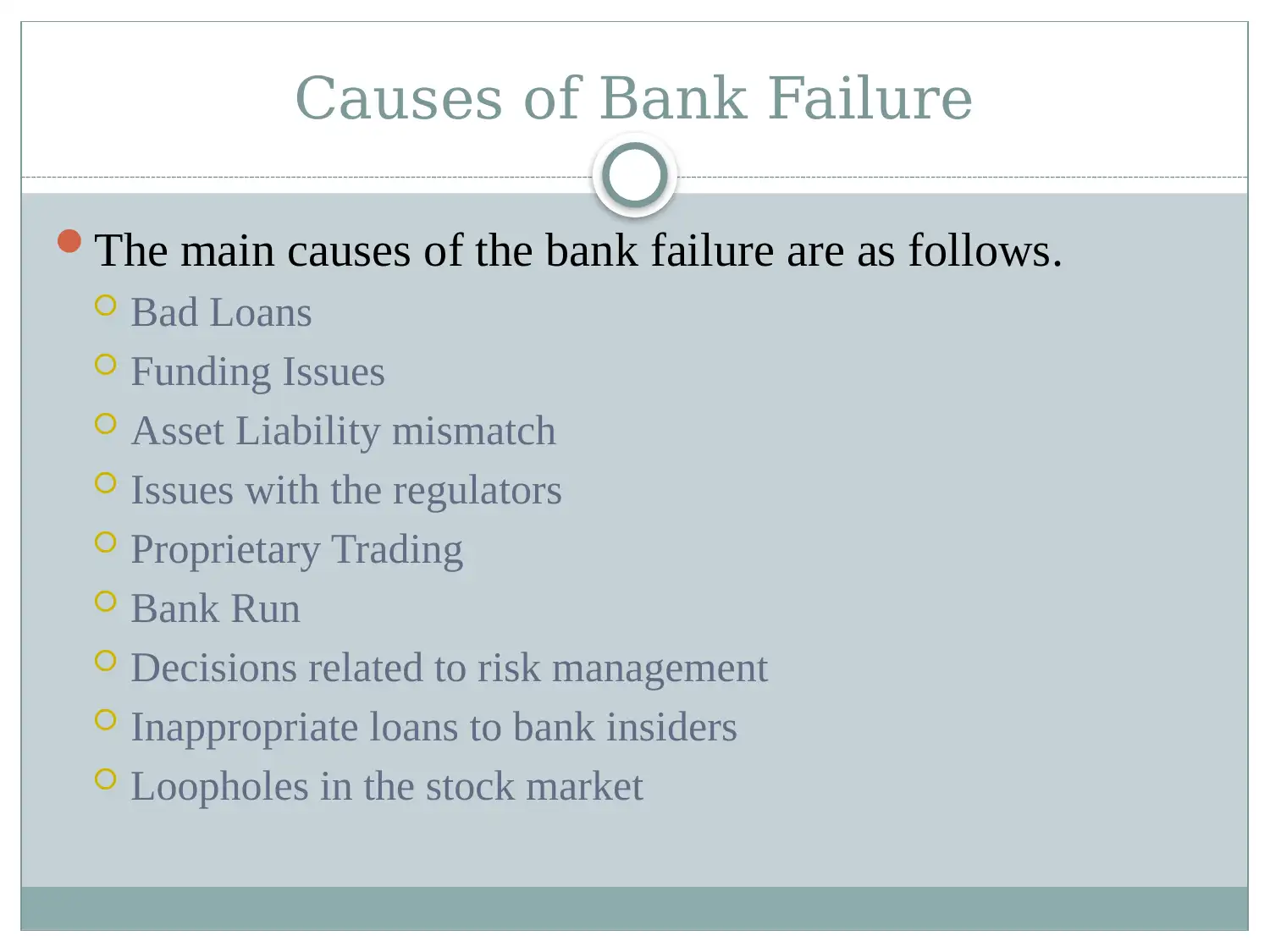

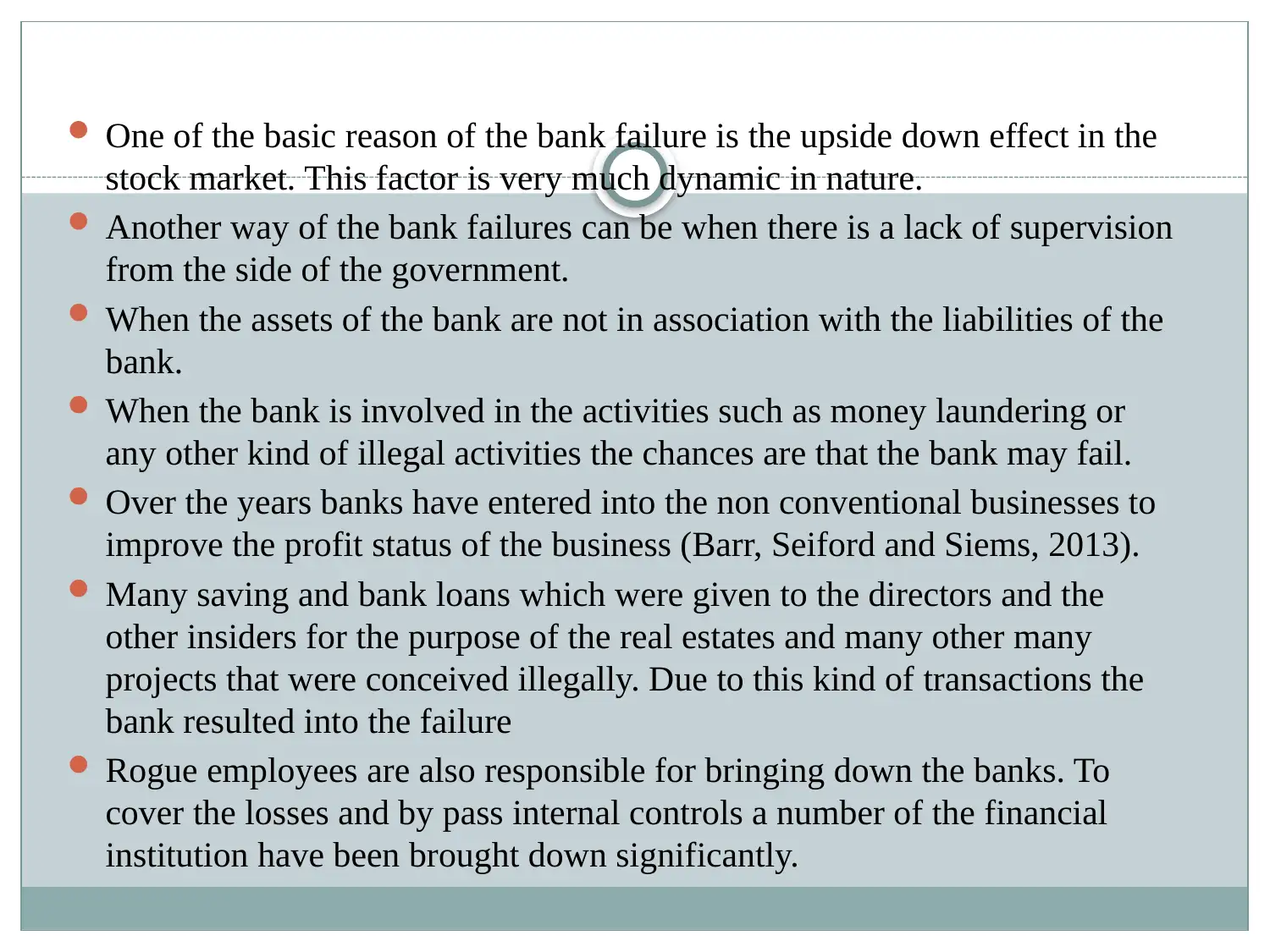

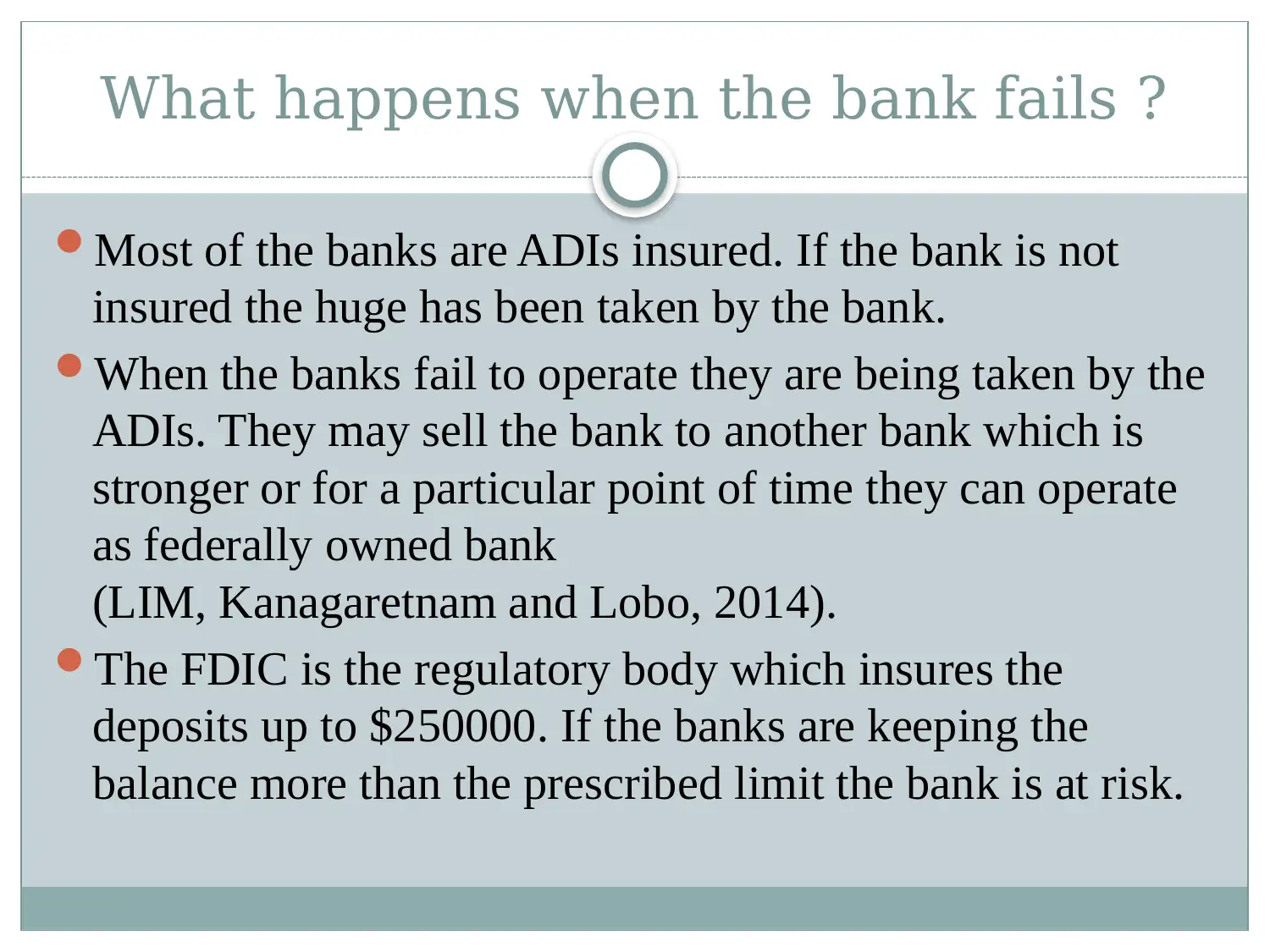

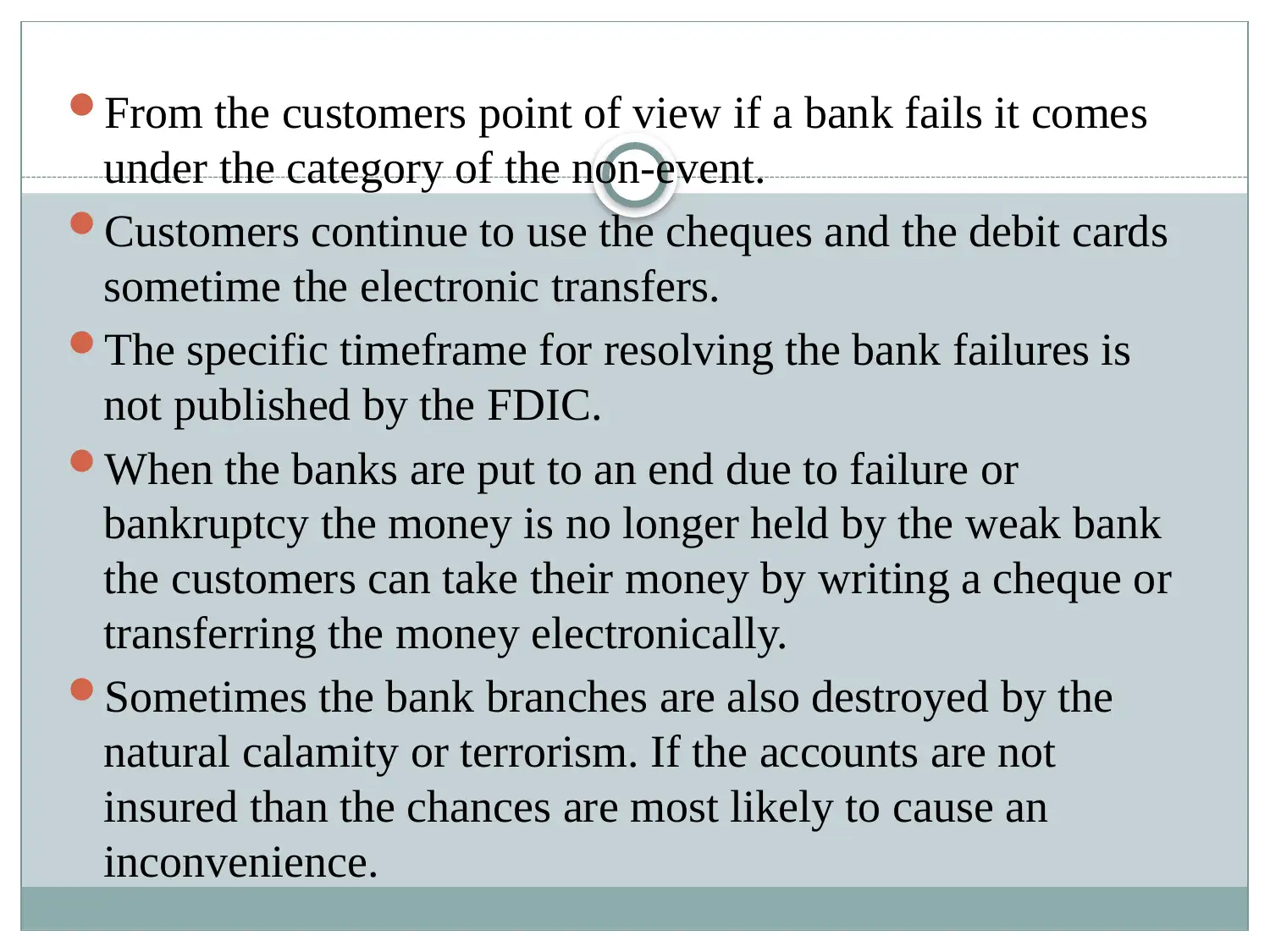

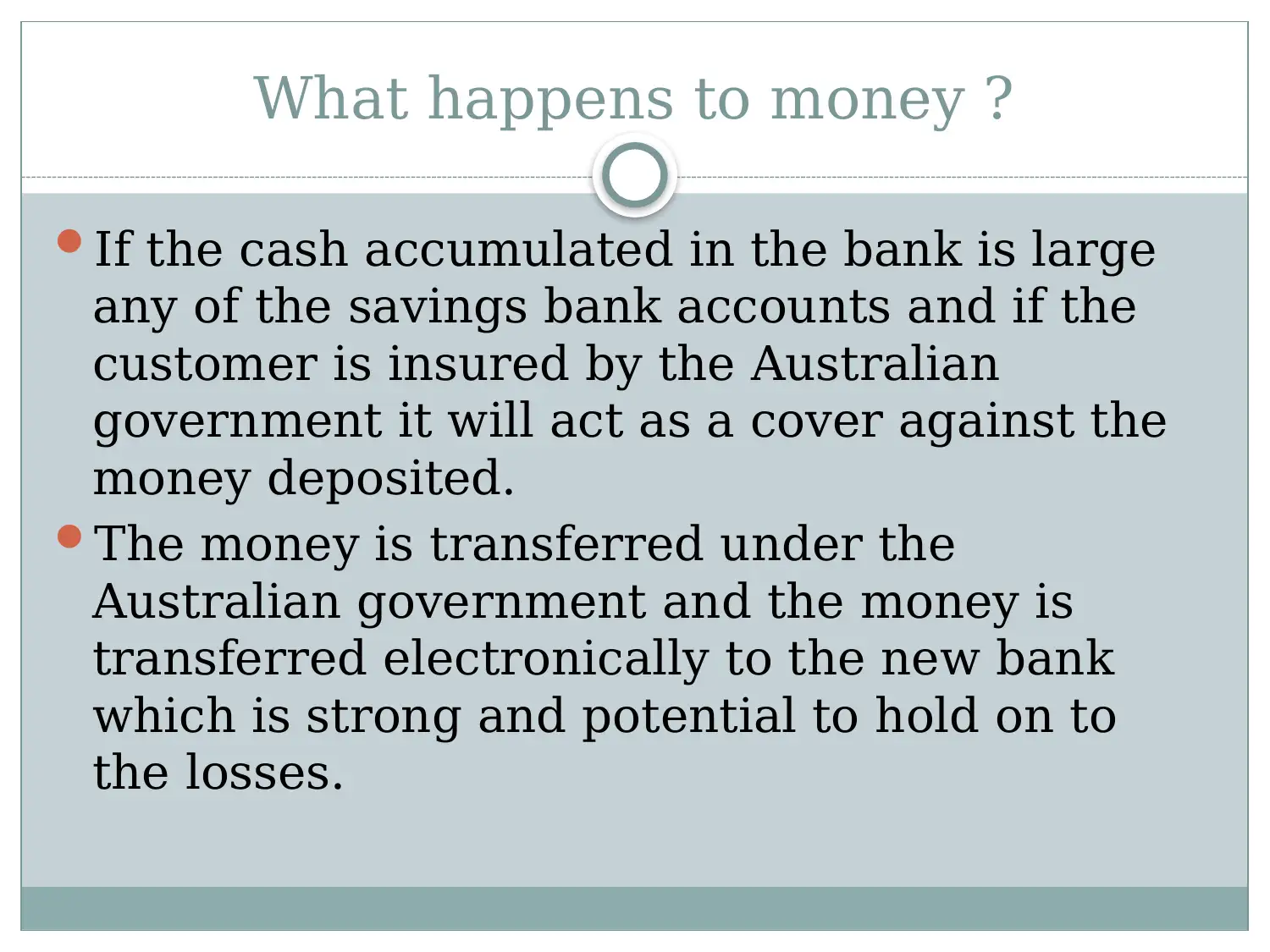

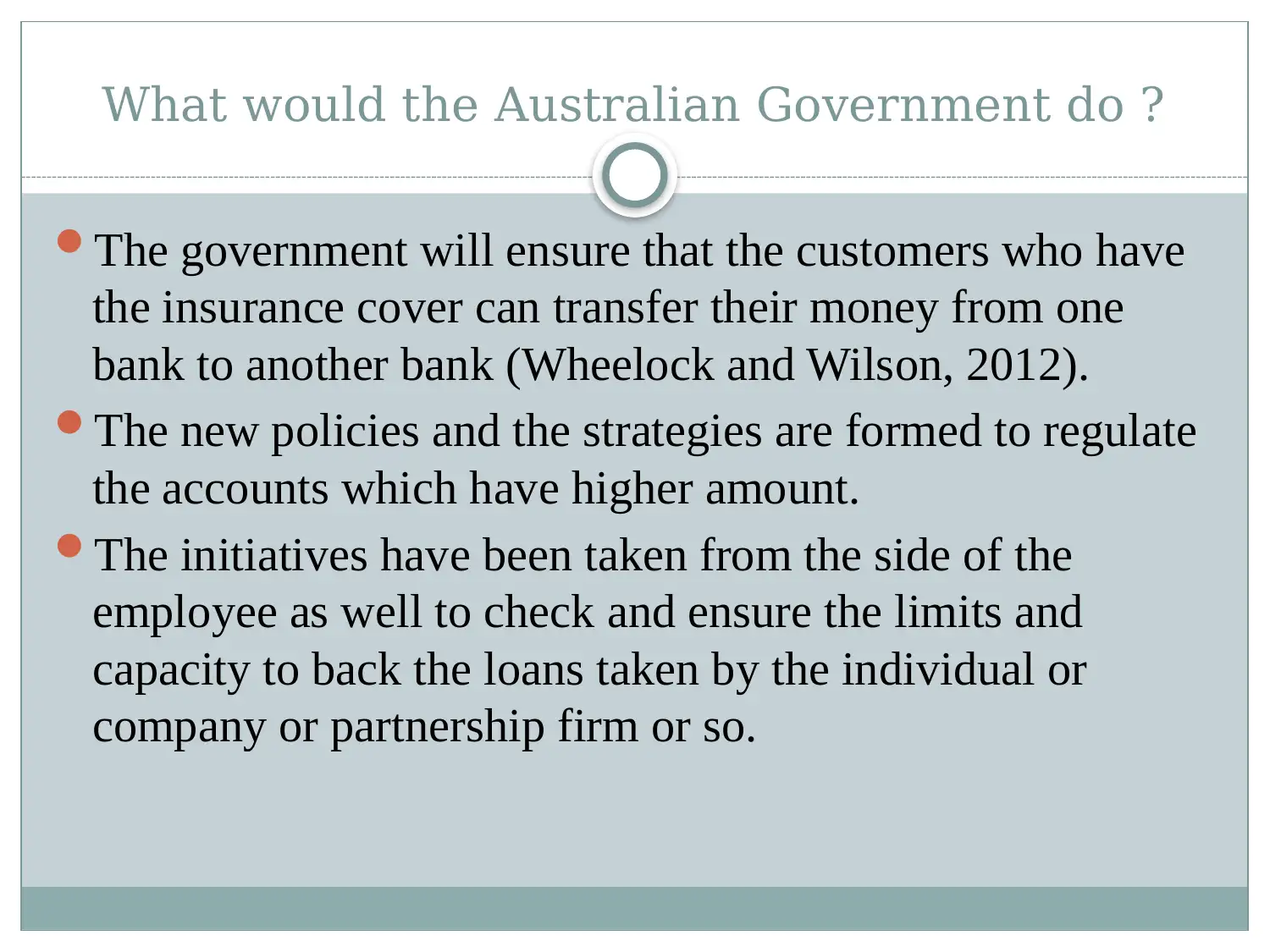

This report provides a comprehensive analysis of bank failures in Australia, focusing on the causes, impacts, and prevention strategies. It identifies key factors contributing to bank failures, including bad loans, funding issues, asset-liability mismatches, regulatory issues, and risky trading activities. The report also discusses the role of the Australian government in protecting depositors and preventing future failures through deposit insurance and regulatory oversight. Furthermore, it examines the actions taken when a bank fails, such as acquisition by another bank or federal ownership, and how customers are protected through the Australian Depositor Protection Scheme. The report concludes by suggesting measures to prevent bank failures, such as dynamic capital management, effective regulatory control, and daily monitoring of account transactions. Desklib provides access to this and many other solved assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.