Corporate Accounting & Reporting: Movement of Reserves and Impairment

VerifiedAdded on 2023/06/07

|6

|1488

|405

Report

AI Summary

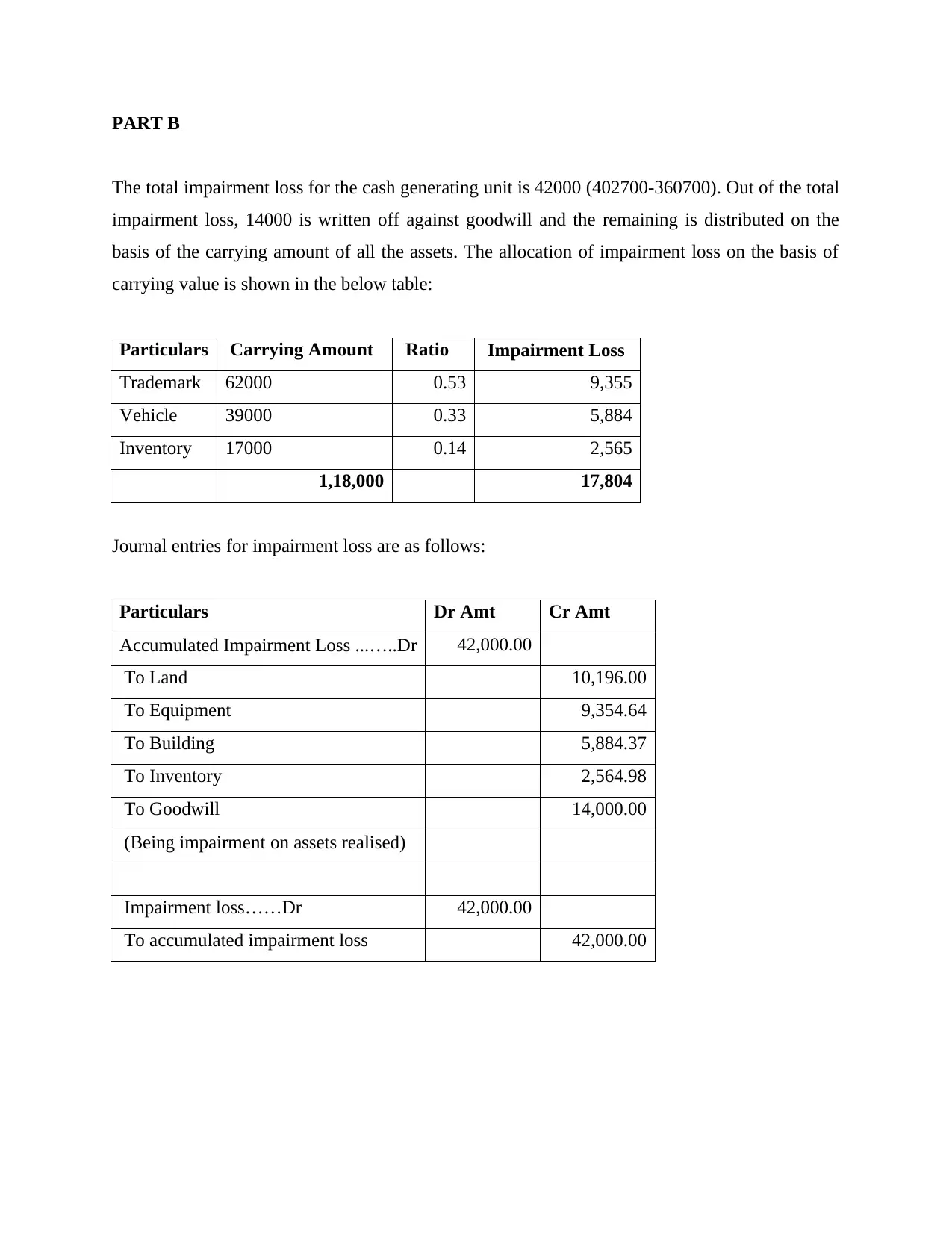

This report provides a comprehensive analysis of corporate accounting and reporting, focusing on reserves and impairment. It begins by defining reserves as profits set aside for specific purposes, managed by the board of directors, and discusses their accounting treatment, including debiting retained earnings and crediting reserve accounts. The report elaborates on open reserves (capital and revenue reserves) and secret reserves, detailing their creation and usage, and also touches on other reserves like foreign currency transaction reserves. Furthermore, it explains the movement of reserves, including dividend payments and transfers between reserves, as reflected in the Statement of Changes in Equity. The report also addresses the accounting treatment of dividends, distinguishing between cash and scrip dividends. In the second part, the report presents a practical example of impairment loss allocation across different assets of a cash-generating unit, along with corresponding journal entries. This student-contributed assignment is available on Desklib, a platform offering AI-based study tools and a wealth of academic resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.