Comprehensive Risk Assessment: Comparative Analysis of Bank Ratios

VerifiedAdded on 2023/06/03

|23

|5344

|196

Report

AI Summary

This report provides a comparative risk assessment of four major Australian banks—National Australia Bank (NAB), ANZ, Commonwealth Bank, and Westpac—focusing on strategic risk, interest rate risk, market risk, credit risk, and liquidity risk. The assessment utilizes financial ratios calculated from publicly available data to identify potential 'red flags' requiring management attention. The analysis covers capital ratios, operational ratios, liquidity ratios, and asset ratios over a 12-year period. Key findings include ANZ's high Tier 1 ratio indicating strong loss absorption capacity, NAB's consistent equity to total assets ratio, and a comparative evaluation of net interest margins and return on equity. The report concludes with recommendations to the Board based on these analyses, offering insights into the banks' financial stability and risk management strategies.

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

0

INSTITUTIONAL ASSETS AND LIABILITIES

0

INSTITUTIONAL ASSETS AND LIABILITIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

Table of Contents

Introduction................................................................................................................................2

Strategic risk...............................................................................................................................2

Capital Ratios.........................................................................................................................2

Interest rate risk..........................................................................................................................3

Operational Ratios..................................................................................................................4

Market Risk................................................................................................................................6

Liquidity ratios.......................................................................................................................6

Credit risk...................................................................................................................................7

Asset ratios.............................................................................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Strategic risk...............................................................................................................................2

Capital Ratios.........................................................................................................................2

Interest rate risk..........................................................................................................................3

Operational Ratios..................................................................................................................4

Market Risk................................................................................................................................6

Liquidity ratios.......................................................................................................................6

Credit risk...................................................................................................................................7

Asset ratios.............................................................................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

Introduction

Risk assessment is the term which is used by the company to determine the overall

process and the methods. The process is undertaken to identify the hazards and the risky

factors that the company is going to affect the organisation. Analyse and evaluate the risk

associated with the risk analysis and the risk evaluation. The report below is the analysis of

the ratios of the 4 banks which are National Australian Bank and the same is compared with

the ANZ bank, Commonwealth bank and the Westpac bank (Cohen & Scatigna, 2016).

Strategic risk

The strategic risk has been defined as the central risk of the business. The key aim of

the strategic risk management is to strengthen the earnings of the banks through the resilience

and the same has been protected with the assistance of the undue earnings volatility to gauge

the overall risk targets. For the purpose of determining the strategic risk of any bank the

leverage ratios and the CET 1 ratios are calculated (Behn, Haselmann & Vig, 2016).

Capital Ratios

Capital Adequacy ratio is also known as the Capital to Risk Weighted Asset ratio in

relation to the bank’s capital and the risk. The capital ratios are divided among the three

major categories such as the Tier 1 ratios, the equity to total assets ratio and the capital funds

by liabilities. This ratio basically determines the capital structure of the banks and from the

table below it can be analysed that the NAB’s Tier 1 ratio is has been 12.41 which are the

third highest in terms of the other comparing banks. The tier 1 ratio of the NAB increased

from 6.67 in the year 2007 to 12.41 in the year 2017 and the ANZ bank increased from 7.30

and just reached double the amount at 14.10 being the highest performer in terms of the tier 1

ratio. The CBA and the Westpac are again on the same motion at 12.3 and the 12.66

Introduction

Risk assessment is the term which is used by the company to determine the overall

process and the methods. The process is undertaken to identify the hazards and the risky

factors that the company is going to affect the organisation. Analyse and evaluate the risk

associated with the risk analysis and the risk evaluation. The report below is the analysis of

the ratios of the 4 banks which are National Australian Bank and the same is compared with

the ANZ bank, Commonwealth bank and the Westpac bank (Cohen & Scatigna, 2016).

Strategic risk

The strategic risk has been defined as the central risk of the business. The key aim of

the strategic risk management is to strengthen the earnings of the banks through the resilience

and the same has been protected with the assistance of the undue earnings volatility to gauge

the overall risk targets. For the purpose of determining the strategic risk of any bank the

leverage ratios and the CET 1 ratios are calculated (Behn, Haselmann & Vig, 2016).

Capital Ratios

Capital Adequacy ratio is also known as the Capital to Risk Weighted Asset ratio in

relation to the bank’s capital and the risk. The capital ratios are divided among the three

major categories such as the Tier 1 ratios, the equity to total assets ratio and the capital funds

by liabilities. This ratio basically determines the capital structure of the banks and from the

table below it can be analysed that the NAB’s Tier 1 ratio is has been 12.41 which are the

third highest in terms of the other comparing banks. The tier 1 ratio of the NAB increased

from 6.67 in the year 2007 to 12.41 in the year 2017 and the ANZ bank increased from 7.30

and just reached double the amount at 14.10 being the highest performer in terms of the tier 1

ratio. The CBA and the Westpac are again on the same motion at 12.3 and the 12.66

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

respectively. The tier 1 ratio determines the ability of the company to absorb the losses

therefore higher the ratio, higher the company is able to absorb it. From the above results it

can be analysed that ANZ bank is highly capable and after that the Westpac bank in

comparison to the NBA bank for the financial year 2017 as well as the past 4 years (Estrella,

Park & Peristiani, 2012).

The equity to total assets of the company is the measure of the equity and the total

assets held by the banks for the period of the 12 years. This basically determines the ratio

which determines that how much assets are in the range of the shareholders having the

residual claim. The figures are taken from the balance sheet. Except the ANZ bank the NBA,

CBA and the Westpac bank have increased the ratio from the 4.86% to 6.39% in the year

2017, 5.34% to 6.91% and 5.37% to 7.20% respectively. The increase in the ratio is basically

by the fluctuations in the earnings of the banks and therefore the balance of the shareholders

equity has also been changed over the years. The higher the ratio the more the number of the

assets is in the hands of the shareholder. From the results as given in the table it can be

concluded that the thought the highest ratio is of the ANZ bank yet this bank is prone to the

maximum amount of the fluctuations. In terms of the consistency the NBA bank has been

increasing consistently and so is the Westpac bank, henceforth, the NBA bank is performing

better (Shrieves & Dahl, 2012).

Particula

rs

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Capital

Ratios

NBA

respectively. The tier 1 ratio determines the ability of the company to absorb the losses

therefore higher the ratio, higher the company is able to absorb it. From the above results it

can be analysed that ANZ bank is highly capable and after that the Westpac bank in

comparison to the NBA bank for the financial year 2017 as well as the past 4 years (Estrella,

Park & Peristiani, 2012).

The equity to total assets of the company is the measure of the equity and the total

assets held by the banks for the period of the 12 years. This basically determines the ratio

which determines that how much assets are in the range of the shareholders having the

residual claim. The figures are taken from the balance sheet. Except the ANZ bank the NBA,

CBA and the Westpac bank have increased the ratio from the 4.86% to 6.39% in the year

2017, 5.34% to 6.91% and 5.37% to 7.20% respectively. The increase in the ratio is basically

by the fluctuations in the earnings of the banks and therefore the balance of the shareholders

equity has also been changed over the years. The higher the ratio the more the number of the

assets is in the hands of the shareholder. From the results as given in the table it can be

concluded that the thought the highest ratio is of the ANZ bank yet this bank is prone to the

maximum amount of the fluctuations. In terms of the consistency the NBA bank has been

increasing consistently and so is the Westpac bank, henceforth, the NBA bank is performing

better (Shrieves & Dahl, 2012).

Particula

rs

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Capital

Ratios

NBA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

Tier 1

ratios

12.4

1

12.1

9

12.4

4

10.8

1

10.3

5

10.2

7 9.7 8.91 8.96 7.35 6.67 7.35

Equity/

Total

Assets

6.39

%

6.48

%

5.71

%

5.20

%

5.46

%

5.40

%

5.26

%

5.30

%

5.39

%

4.64

%

4.86

%

5.36

%

Capital

funds/Liabi

lities 1.08 1.08 1.07 1.06 1.06 1.06 1.06 1.06 1.07 1.06 1.06 1.07

ANZ

Tier 1

ratios

14.1

0

13.2

0

12.7

0

11.1

0

10.8

0

10.8

0

10.0

2 9.68 9.03 8.13 7.90 7.34

Equity/

Total

Assets

8.11

%

7.72

%

8.24

%

8.91

%

9.26

%

8.99

%

8.91

%

8.97

%

8.56

%

7.98

%

8.07

% 9%

Capital

funds/Liabi

lities 1.09 1.09 1.09 1.10 1.11 1.10 1.10 1.10 1.09 1.09 1.09 1.09

CBA

Tier 1

ratios 12.3 12.1 12.3 11.2 11.1 10.3

10.0

1

10.0

1 9.15 8.07 8.17 7.14

Equity/

Total

Assets

6.91

%

6.47

%

6.44

%

5.90

%

6.05

%

5.85

%

5.58

%

5.37

%

5.36

%

4.92

%

5.17

%

5.34

%

Capital 109 108 108 107 107 107 107 107 107 106 107 107

Tier 1

ratios

12.4

1

12.1

9

12.4

4

10.8

1

10.3

5

10.2

7 9.7 8.91 8.96 7.35 6.67 7.35

Equity/

Total

Assets

6.39

%

6.48

%

5.71

%

5.20

%

5.46

%

5.40

%

5.26

%

5.30

%

5.39

%

4.64

%

4.86

%

5.36

%

Capital

funds/Liabi

lities 1.08 1.08 1.07 1.06 1.06 1.06 1.06 1.06 1.07 1.06 1.06 1.07

ANZ

Tier 1

ratios

14.1

0

13.2

0

12.7

0

11.1

0

10.8

0

10.8

0

10.0

2 9.68 9.03 8.13 7.90 7.34

Equity/

Total

Assets

8.11

%

7.72

%

8.24

%

8.91

%

9.26

%

8.99

%

8.91

%

8.97

%

8.56

%

7.98

%

8.07

% 9%

Capital

funds/Liabi

lities 1.09 1.09 1.09 1.10 1.11 1.10 1.10 1.10 1.09 1.09 1.09 1.09

CBA

Tier 1

ratios 12.3 12.1 12.3 11.2 11.1 10.3

10.0

1

10.0

1 9.15 8.07 8.17 7.14

Equity/

Total

Assets

6.91

%

6.47

%

6.44

%

5.90

%

6.05

%

5.85

%

5.58

%

5.37

%

5.36

%

4.92

%

5.17

%

5.34

%

Capital 109 108 108 107 107 107 107 107 107 106 107 107

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

funds/Liabi

lities % % % % % % % % % % % %

WESTP

AC

Tier 1

ratios

12.6

6

11.1

7

11.4

0

10.6

0

10.7

0

10.3

0 9.70 9.10 8.10 7.80 6.50 6.90

Equity/

Total

Assets

7.20

%

6.93

%

6.55

%

6.30

%

6.67

%

6.57

%

6.25

%

6.49

%

6.20

%

4.43

%

4.72

%

5.37

%

Capital

funds/Liabi

lities 1.09 1.08 1.08 1.07 1.08 1.08 1.07 1.07 1.07 1.05 1.05 1.06

Interest rate risk

Interest Rate risk exposure arises when the change in the interest rates has the

potential to affect the numerical value of the assets and the liabilities, the operational ratios

are calculated. The following table determine the data of the National Bank of Australia for

the period of 12 years. The operational ratios basically are divided into the four categories

which are Net interest margin, return on assets, return on equity and cost to income ratio

(Drechsler, Savov & Schnabl, 2018).

NB

A 2017

201

6 2015 2014 2013

201

2 2011 2010

200

9 2008 2007 2006

funds/Liabi

lities % % % % % % % % % % % %

WESTP

AC

Tier 1

ratios

12.6

6

11.1

7

11.4

0

10.6

0

10.7

0

10.3

0 9.70 9.10 8.10 7.80 6.50 6.90

Equity/

Total

Assets

7.20

%

6.93

%

6.55

%

6.30

%

6.67

%

6.57

%

6.25

%

6.49

%

6.20

%

4.43

%

4.72

%

5.37

%

Capital

funds/Liabi

lities 1.09 1.08 1.08 1.07 1.08 1.08 1.07 1.07 1.07 1.05 1.05 1.06

Interest rate risk

Interest Rate risk exposure arises when the change in the interest rates has the

potential to affect the numerical value of the assets and the liabilities, the operational ratios

are calculated. The following table determine the data of the National Bank of Australia for

the period of 12 years. The operational ratios basically are divided into the four categories

which are Net interest margin, return on assets, return on equity and cost to income ratio

(Drechsler, Savov & Schnabl, 2018).

NB

A 2017

201

6 2015 2014 2013

201

2 2011 2010

200

9 2008 2007 2006

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

Net

interes

t

Margi

n

0.6

%

0.6

%

0.6

%

0.6

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

1.3

%

return

on

assets

0.7

%

0.0

%

0.7

%

0.6

%

0.7

%

0.5

%

0.7

%

0.6

%

0.4

%

0.5

%

1.0

%

1.1

%

Return

on

Equity

10.5

%

0.7

%

11.7

%

11.5

%

12.1

%

9.9

%

13.2

%

11.6

%

7.3

%

10.2

%

20.0

%

19.8

%

Cost

to

incom

e ratio 2.69

41.1

7 2.49 3.21 3.34

5.2

2 4.07 4.16

7.3

5 9.10 3.81 3.28

Operational Ratios

The net interest margin ratio is the measure of the difference between the interest

income generated either by the banks or the financial institutions and the amount of the

interest paid out to the lenders in relation to their interest earning asset. The net interest

margin helps in improving the assets of the banks and the structure and assessing the stability

and the efficiency of their operations. Besides this the interest margin of the ANZ Company

was 1.4% in the year 2006 and the 0.7% in the year 2017. The ratio was consistent for the

period of the 7 years as can be observed form the table. Analysing the situation of the

Westpac bank and the Commonwealth Bank of Australia, the net margins were almost similar

Net

interes

t

Margi

n

0.6

%

0.6

%

0.6

%

0.6

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

1.3

%

return

on

assets

0.7

%

0.0

%

0.7

%

0.6

%

0.7

%

0.5

%

0.7

%

0.6

%

0.4

%

0.5

%

1.0

%

1.1

%

Return

on

Equity

10.5

%

0.7

%

11.7

%

11.5

%

12.1

%

9.9

%

13.2

%

11.6

%

7.3

%

10.2

%

20.0

%

19.8

%

Cost

to

incom

e ratio 2.69

41.1

7 2.49 3.21 3.34

5.2

2 4.07 4.16

7.3

5 9.10 3.81 3.28

Operational Ratios

The net interest margin ratio is the measure of the difference between the interest

income generated either by the banks or the financial institutions and the amount of the

interest paid out to the lenders in relation to their interest earning asset. The net interest

margin helps in improving the assets of the banks and the structure and assessing the stability

and the efficiency of their operations. Besides this the interest margin of the ANZ Company

was 1.4% in the year 2006 and the 0.7% in the year 2017. The ratio was consistent for the

period of the 7 years as can be observed form the table. Analysing the situation of the

Westpac bank and the Commonwealth Bank of Australia, the net margins were almost similar

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

at 0.6% in comparison to each other. Therefore it can be interpreted that in terms of the Net

interest margin the NBA is performing better than among all the three banks (Hevert, 2014).

The return on assets of the National Bank of Australia was highest in the year 2006

at 1.3% and thereafter the ratio decreased to the range of the 0.5% to 0.7%. The return on

assets basically determines the ability of the company to use the assets and generate the

revenue for the company. The higher the return on assets the more efficient the company is

working. The ANZ bank on the other hand has improved its performance as it can be

reflected from the hike in the ratio of the 1.1% to 1.2% from the year 2006 to 2015.

Thereafter the bank reached back to square 1, on the same ratio on which it was in the year

2006. The CBA bank and the Westpac bank are on the same platform in terms of the return

on the assets and over the period of the 12 years the ratio remained in the range of the 0.9%

to 1.1% (Liang, et al 2016).

The return on equity is the ratio which determines the amount of equity that has

been invested in the organisation and the return on the equity received by the shareholder. In

case of the National Bank of Australia the return on equity was highest in the year 2007 at

19.97% and thereafter it decreased to 13.18% in the year 2011 and further it almost touched

the figure of 10.50% in the year 2017. The return on equity has been decreasing as can be

seen from the table and the major reason is that the bank has sold the shares and converted

into the liquid form. The return on equity of the ANZ bank has increased from 13% to 14.1%

over the period of the 12 years and is performing better than NBA. In case of the CBA and

the Westpac Bank the return on equity of the Westpac Bnak is better than the NBA; however

the ANZ bank is the most consistent. The CBA on the other hand has lost the position which

it was having in the year 2013 at 18.1% and thereafter it decreased and reached to 13.9% in

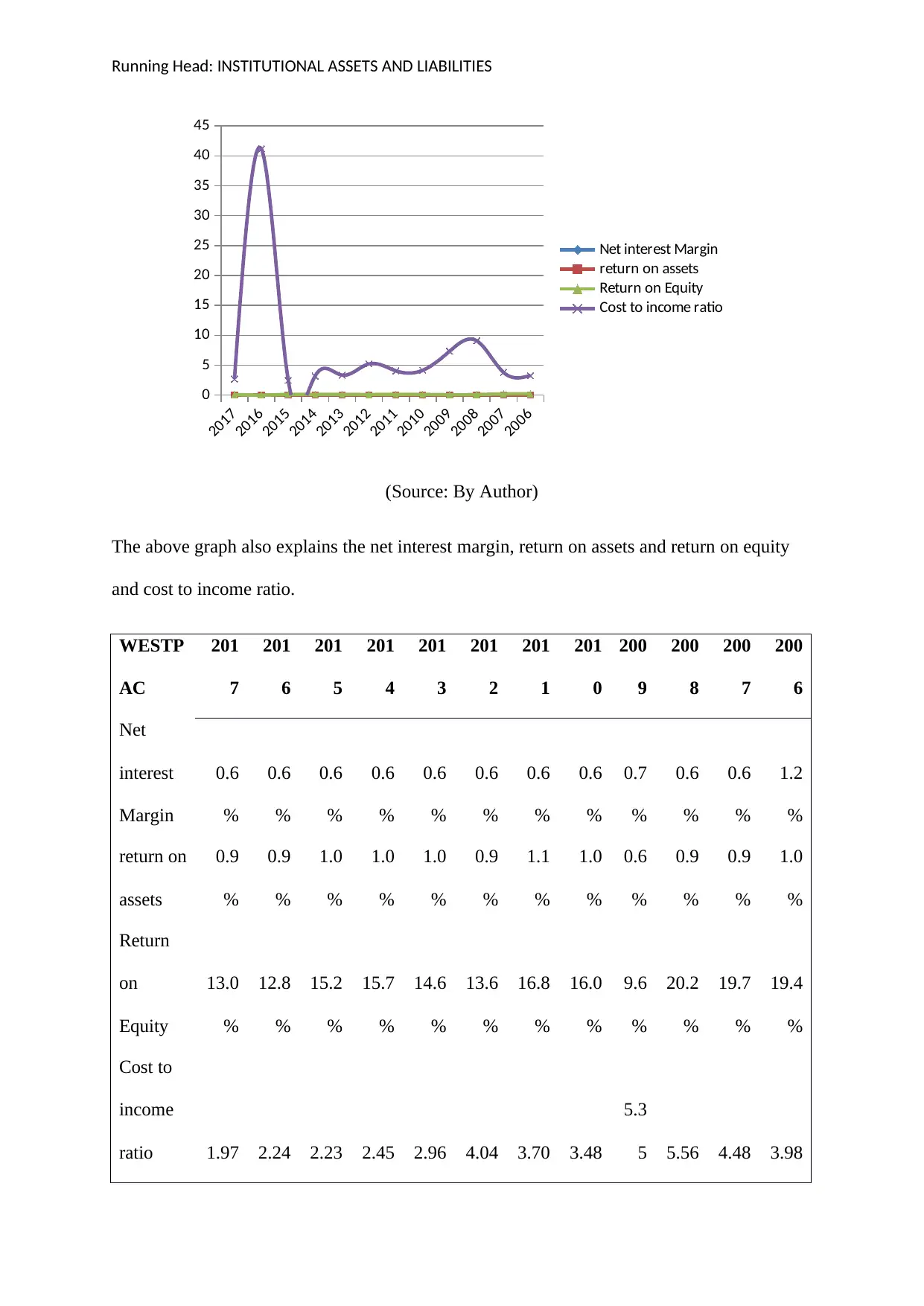

the year 2017 (Moreira, 2016). The same is explained by the graph also.

at 0.6% in comparison to each other. Therefore it can be interpreted that in terms of the Net

interest margin the NBA is performing better than among all the three banks (Hevert, 2014).

The return on assets of the National Bank of Australia was highest in the year 2006

at 1.3% and thereafter the ratio decreased to the range of the 0.5% to 0.7%. The return on

assets basically determines the ability of the company to use the assets and generate the

revenue for the company. The higher the return on assets the more efficient the company is

working. The ANZ bank on the other hand has improved its performance as it can be

reflected from the hike in the ratio of the 1.1% to 1.2% from the year 2006 to 2015.

Thereafter the bank reached back to square 1, on the same ratio on which it was in the year

2006. The CBA bank and the Westpac bank are on the same platform in terms of the return

on the assets and over the period of the 12 years the ratio remained in the range of the 0.9%

to 1.1% (Liang, et al 2016).

The return on equity is the ratio which determines the amount of equity that has

been invested in the organisation and the return on the equity received by the shareholder. In

case of the National Bank of Australia the return on equity was highest in the year 2007 at

19.97% and thereafter it decreased to 13.18% in the year 2011 and further it almost touched

the figure of 10.50% in the year 2017. The return on equity has been decreasing as can be

seen from the table and the major reason is that the bank has sold the shares and converted

into the liquid form. The return on equity of the ANZ bank has increased from 13% to 14.1%

over the period of the 12 years and is performing better than NBA. In case of the CBA and

the Westpac Bank the return on equity of the Westpac Bnak is better than the NBA; however

the ANZ bank is the most consistent. The CBA on the other hand has lost the position which

it was having in the year 2013 at 18.1% and thereafter it decreased and reached to 13.9% in

the year 2017 (Moreira, 2016). The same is explained by the graph also.

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

NBA

ANZ

CBA

WESTPAC

(Source: by Author)

AN

Z 2017 2016 2015 2014 2013 2012 2011

201

0

200

9 2008 2007 2006

Net

interes

t

Margi

n

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.8

%

0.7

%

0.7

%

0.7

%

0.6

%

0.7

%

1.4

%

return

on

assets

1.1

%

1.0

%

1.2

%

1.3

%

1.1

%

1.1

%

0.9

%

0.7

%

0.3

%

0.9

%

1.1

%

1.1

%

Retur

n on

Equity

14.1

%

12.4

%

14.7

%

14.9

%

12.3

%

12.1

%

10.2

%

7.9

%

3.0

%

11.9

%

13.4

%

13.0

%

Cost 1.79 2.23 2.27 2.06 2.44 2.52 3.29 4.1 16.4 6.51 5.19 4.74

2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

2.00%

NBA

ANZ

CBA

WESTPAC

(Source: by Author)

AN

Z 2017 2016 2015 2014 2013 2012 2011

201

0

200

9 2008 2007 2006

Net

interes

t

Margi

n

0.7

%

0.7

%

0.7

%

0.7

%

0.7

%

0.8

%

0.7

%

0.7

%

0.7

%

0.6

%

0.7

%

1.4

%

return

on

assets

1.1

%

1.0

%

1.2

%

1.3

%

1.1

%

1.1

%

0.9

%

0.7

%

0.3

%

0.9

%

1.1

%

1.1

%

Retur

n on

Equity

14.1

%

12.4

%

14.7

%

14.9

%

12.3

%

12.1

%

10.2

%

7.9

%

3.0

%

11.9

%

13.4

%

13.0

%

Cost 1.79 2.23 2.27 2.06 2.44 2.52 3.29 4.1 16.4 6.51 5.19 4.74

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

to

incom

e ratio 8 2

CB

A

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Net

interes

t

Margi

n

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

return

on

assets

1.0

%

1.0

%

1.0

%

1.0

%

1.1

%

1.0

%

1.0

%

1.0

%

0.9

%

0.8

%

1.0

%

1.0

%

Retur

n on

Equity

13.9

%

15.8

%

15.4

%

17.6

%

18.1

%

17.3

%

17.7

%

17.9

%

16.4

%

15.6

%

19.1

%

19.1

%

Cost

to

incom

e ratio 1.73 1.58 1.83 2.02 2.14 2.73 3.54 3.88 3.57 4.46 4.42 3.74

to

incom

e ratio 8 2

CB

A

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Net

interes

t

Margi

n

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

return

on

assets

1.0

%

1.0

%

1.0

%

1.0

%

1.1

%

1.0

%

1.0

%

1.0

%

0.9

%

0.8

%

1.0

%

1.0

%

Retur

n on

Equity

13.9

%

15.8

%

15.4

%

17.6

%

18.1

%

17.3

%

17.7

%

17.9

%

16.4

%

15.6

%

19.1

%

19.1

%

Cost

to

incom

e ratio 1.73 1.58 1.83 2.02 2.14 2.73 3.54 3.88 3.57 4.46 4.42 3.74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

0

5

10

15

20

25

30

35

40

45

Net interest Margin

return on assets

Return on Equity

Cost to income ratio

(Source: By Author)

The above graph also explains the net interest margin, return on assets and return on equity

and cost to income ratio.

WESTP

AC

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Net

interest

Margin

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.7

%

0.6

%

0.6

%

1.2

%

return on

assets

0.9

%

0.9

%

1.0

%

1.0

%

1.0

%

0.9

%

1.1

%

1.0

%

0.6

%

0.9

%

0.9

%

1.0

%

Return

on

Equity

13.0

%

12.8

%

15.2

%

15.7

%

14.6

%

13.6

%

16.8

%

16.0

%

9.6

%

20.2

%

19.7

%

19.4

%

Cost to

income

ratio 1.97 2.24 2.23 2.45 2.96 4.04 3.70 3.48

5.3

5 5.56 4.48 3.98

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

0

5

10

15

20

25

30

35

40

45

Net interest Margin

return on assets

Return on Equity

Cost to income ratio

(Source: By Author)

The above graph also explains the net interest margin, return on assets and return on equity

and cost to income ratio.

WESTP

AC

201

7

201

6

201

5

201

4

201

3

201

2

201

1

201

0

200

9

200

8

200

7

200

6

Net

interest

Margin

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.6

%

0.7

%

0.6

%

0.6

%

1.2

%

return on

assets

0.9

%

0.9

%

1.0

%

1.0

%

1.0

%

0.9

%

1.1

%

1.0

%

0.6

%

0.9

%

0.9

%

1.0

%

Return

on

Equity

13.0

%

12.8

%

15.2

%

15.7

%

14.6

%

13.6

%

16.8

%

16.0

%

9.6

%

20.2

%

19.7

%

19.4

%

Cost to

income

ratio 1.97 2.24 2.23 2.45 2.96 4.04 3.70 3.48

5.3

5 5.56 4.48 3.98

Running Head: INSTITUTIONAL ASSETS AND LIABILITIES

Liquidity Risk

Market risk is the risk of the losses and it determines the position of the bank in terms

of the market risk arising due to the fluctuations. The risk is further segregated into the

Equity risk, net loans risk and for the purpose of the ascertainment of this risk the liquidity

ratios are calculated.

Market Risk

Market Risk refers to the losses in the books of the banks due to the changes in the equity

prices the rate of interest and the commodity prices and other indicators having the current

value in the public market. The interest rate of the banks is 3.6% of the NAB, 2.30% of the

CBA, 4.85% of the ANZ and lastly in case of the Westpac the rate of interest came to 2.51%.

In terms of the equity prices the price of the Westpac is at $27.49 the NAB is $27.21 and that

of the CBA and the ANZ is $69.9 and 27.72 (Drechsler, Savov & Schnabl, 2018). The

highest range is of the CBA in terms of the equity price and in terms of the interest rate again

the CBA is having the highest bracket. Therefore it can be interpreted for the above

information that CBA is good in terms of the interest rate yet if the investor wishes to

purchase the stock is costly than the other three banks.

Liquidity ratios

The liquidity ratios of the bank generally determine the ability of the banks the short

term loans are made or not. The short term financial obligation is of greater concern to the

creditors. Therefore it is an important ratio in terms of the banks financial position. In case of

the banks the liquidity ratios are categorised into the interbank ratio, net loans to total asset

ratio (Heider, Hoerova & Holthausen, 2015).

Liquidity Risk

Market risk is the risk of the losses and it determines the position of the bank in terms

of the market risk arising due to the fluctuations. The risk is further segregated into the

Equity risk, net loans risk and for the purpose of the ascertainment of this risk the liquidity

ratios are calculated.

Market Risk

Market Risk refers to the losses in the books of the banks due to the changes in the equity

prices the rate of interest and the commodity prices and other indicators having the current

value in the public market. The interest rate of the banks is 3.6% of the NAB, 2.30% of the

CBA, 4.85% of the ANZ and lastly in case of the Westpac the rate of interest came to 2.51%.

In terms of the equity prices the price of the Westpac is at $27.49 the NAB is $27.21 and that

of the CBA and the ANZ is $69.9 and 27.72 (Drechsler, Savov & Schnabl, 2018). The

highest range is of the CBA in terms of the equity price and in terms of the interest rate again

the CBA is having the highest bracket. Therefore it can be interpreted for the above

information that CBA is good in terms of the interest rate yet if the investor wishes to

purchase the stock is costly than the other three banks.

Liquidity ratios

The liquidity ratios of the bank generally determine the ability of the banks the short

term loans are made or not. The short term financial obligation is of greater concern to the

creditors. Therefore it is an important ratio in terms of the banks financial position. In case of

the banks the liquidity ratios are categorised into the interbank ratio, net loans to total asset

ratio (Heider, Hoerova & Holthausen, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.