iMBA Finance Autumn 2018 Project: Smiths Group Financial Analysis

VerifiedAdded on 2023/05/30

|15

|3669

|364

Report

AI Summary

This finance project report provides a comprehensive financial analysis of Smiths Group plc, comparing its performance with Hitachi Limited and assessing its industry position. The analysis includes profitability, liquidity, capital structure, asset efficiency, and shareholder ratios to evaluate the company's financial health. Furthermore, the report employs asset-based valuation, dividend valuation model, and P/E ratios to determine the intrinsic value of Smiths Group's stock, offering investment recommendations based on these valuations. The report concludes with a discussion on the limitations of ratio analysis and valuation models, ultimately suggesting that investors consider selling the stock based on P/E ratio analysis. This detailed study aims to provide valuable insights for informed decision-making regarding Smiths Group.

Finance

1

Project Report: Finance

1

Project Report: Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

2

Introduction:

In this report, the financial analysis study has been done on Smiths Group to identify

the company’s performance in the industry, Hitachi limited and industry performance have

also been assessed in the report. In the report, the overall financial performance of the

company has been evaluated through study over the financial statement along with that, the

valuation study has also been performed on the company so that the better result could be

made. A new project of the company has also been studied to recommend the top level

management that whether the project should be accepted or not.

Company brief:

Smith Group plc is British company which is operating its business at multinational

level. The company is operating its business under the engineering industry. Headquarter of

the company is in London, UK. The company has its operation under the engineering

industry. It is world’s largest manufacturer of sensors for explosive detection, chemical

agents, narcotics, biohazards and contraband (Home, 2018). The company has 5 divisions

which are John Crane Inc, Flex-tek, Smiths Medical, Smiths Detection and Smiths

Interconnect.

Financial analysis:

In order to evaluate the performance and the financial changes in Smith Group plc,

ratio analysis method has been applied on the company and it has been compared with the

ratios of Hitachi plc, one of the main competitors of Smith group plc. The ratio analysis study

of Smith group plc and the competition analysis is as follows:

Profitability analysis:

Profitability analysis is an analysis process which evaluates the profitability level of

the business in order to determine the efficiency and performance level of the business. It

evaluates the total earnings of the business on various bases to make the decision about profit

level (Gapenski, 2008). Profitability analysis measures the margin and return of the business

mainly.

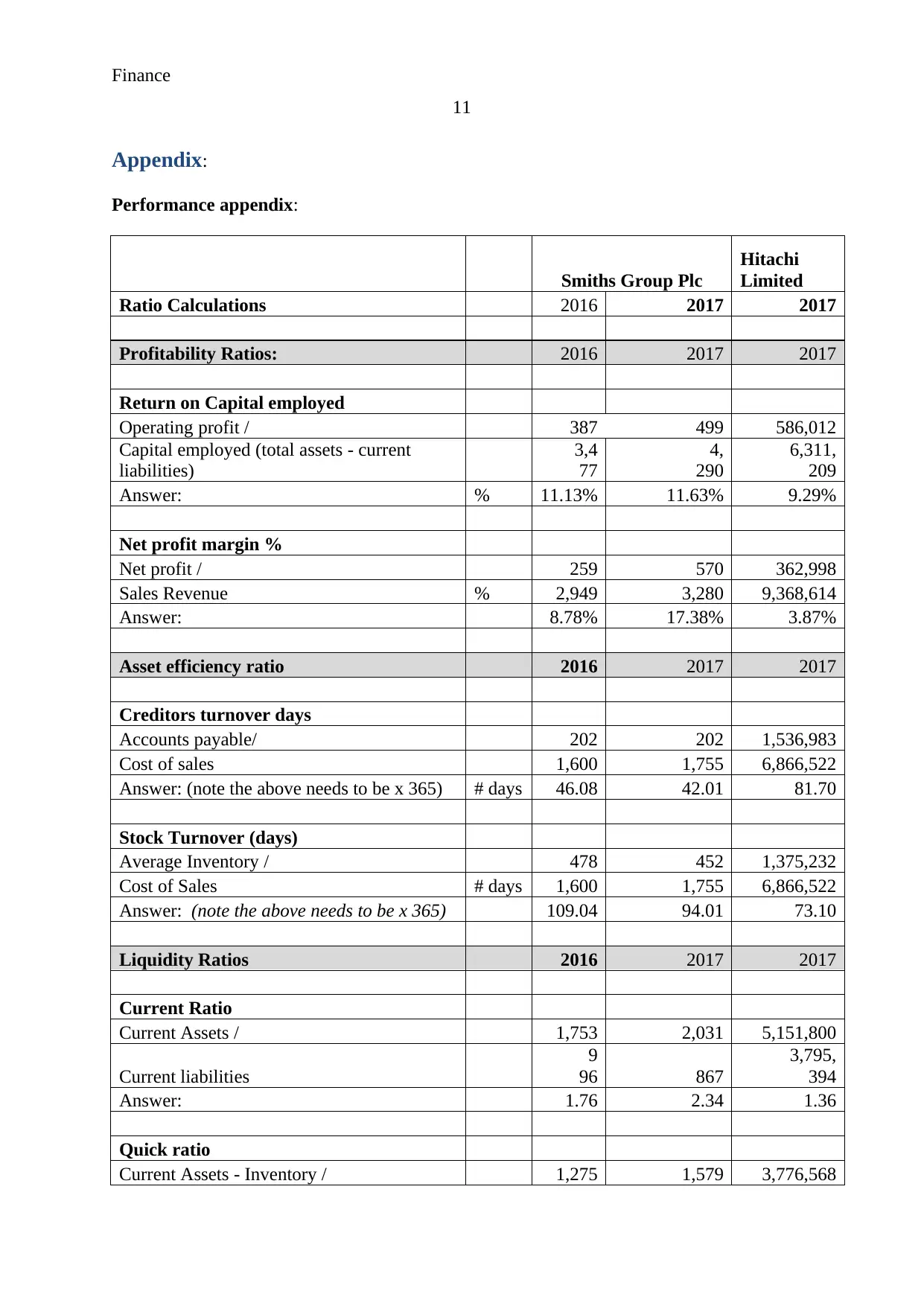

In case of Smith group plc, ROCE and profit margin ratio have been calculated.

Return on capital employed ratio brief that how much return have been generated by the

business against the total capital of the business (Barlow, 2006). The ratio analysis briefs the

2

Introduction:

In this report, the financial analysis study has been done on Smiths Group to identify

the company’s performance in the industry, Hitachi limited and industry performance have

also been assessed in the report. In the report, the overall financial performance of the

company has been evaluated through study over the financial statement along with that, the

valuation study has also been performed on the company so that the better result could be

made. A new project of the company has also been studied to recommend the top level

management that whether the project should be accepted or not.

Company brief:

Smith Group plc is British company which is operating its business at multinational

level. The company is operating its business under the engineering industry. Headquarter of

the company is in London, UK. The company has its operation under the engineering

industry. It is world’s largest manufacturer of sensors for explosive detection, chemical

agents, narcotics, biohazards and contraband (Home, 2018). The company has 5 divisions

which are John Crane Inc, Flex-tek, Smiths Medical, Smiths Detection and Smiths

Interconnect.

Financial analysis:

In order to evaluate the performance and the financial changes in Smith Group plc,

ratio analysis method has been applied on the company and it has been compared with the

ratios of Hitachi plc, one of the main competitors of Smith group plc. The ratio analysis study

of Smith group plc and the competition analysis is as follows:

Profitability analysis:

Profitability analysis is an analysis process which evaluates the profitability level of

the business in order to determine the efficiency and performance level of the business. It

evaluates the total earnings of the business on various bases to make the decision about profit

level (Gapenski, 2008). Profitability analysis measures the margin and return of the business

mainly.

In case of Smith group plc, ROCE and profit margin ratio have been calculated.

Return on capital employed ratio brief that how much return have been generated by the

business against the total capital of the business (Barlow, 2006). The ratio analysis briefs the

Finance

3

11.63% ROCE of the company which is quite higher than the ROCE of Hitachi limited i.e.

9.29%. On the other hand, net profit ratio brief the total profit earned by the company against

the sales revenue of the business. It briefs the 17.38% net profit level of the business which is

higher than 3.87% net profitability ratio of Hitachi limited (Performance appendix).

The profitability analysis expresses that Smiths group plc’s performance is quite

better and thus it is a good option in order to make an investment as higher earnings per share

could be achieved by each of the shareholders of the company.

Liquidity analysis:

Liquidity ratio analysis is an indicator to recognize whether the company has enough

current and quick assets in order to meet the short term obligation of the company. It

evaluates whether the entire short term debt obligation could be met by the company through

the available current assets or not (Higgins, 2012). It is mainly calculated to identify the

liquidity risk and working capital efficiency level of the business.

In case of Smith group plc, the current ratio and quick ratio has been calculated by the

company. Current ratio of the business indicates whether the business is capable to meet the

short term obligations. 2:1 and 1.3:1 current ratio and quick ratio are normal for the industry

(Madura, 2014). On the basis of study over Smith group plc, it has been found that the current

assets of the company are 2.34 times of current liabilities of the business which is quite

higher than the Hitachi current assets level i.e. 3.87% (Annual report, 2017). Further, the

quick assets define about the total quick assets (those assets which could be easily converted

into cash) against the current liabilities of the business. The calculations explain that the

quick ratio of the business is also higher than Hitachi limited. Quick assets of the company

are higher than 1.82 times of current liabilities of the business (Performance appendix).

Through the calculations, the liquidity risk of the business is least as the level of

current assets and quick assets of the business are higher. However, it has also been found

that in order to maintain the higher current assets, business has to bear higher expenses which

could be reduced through reducing the level of current assets a bit.

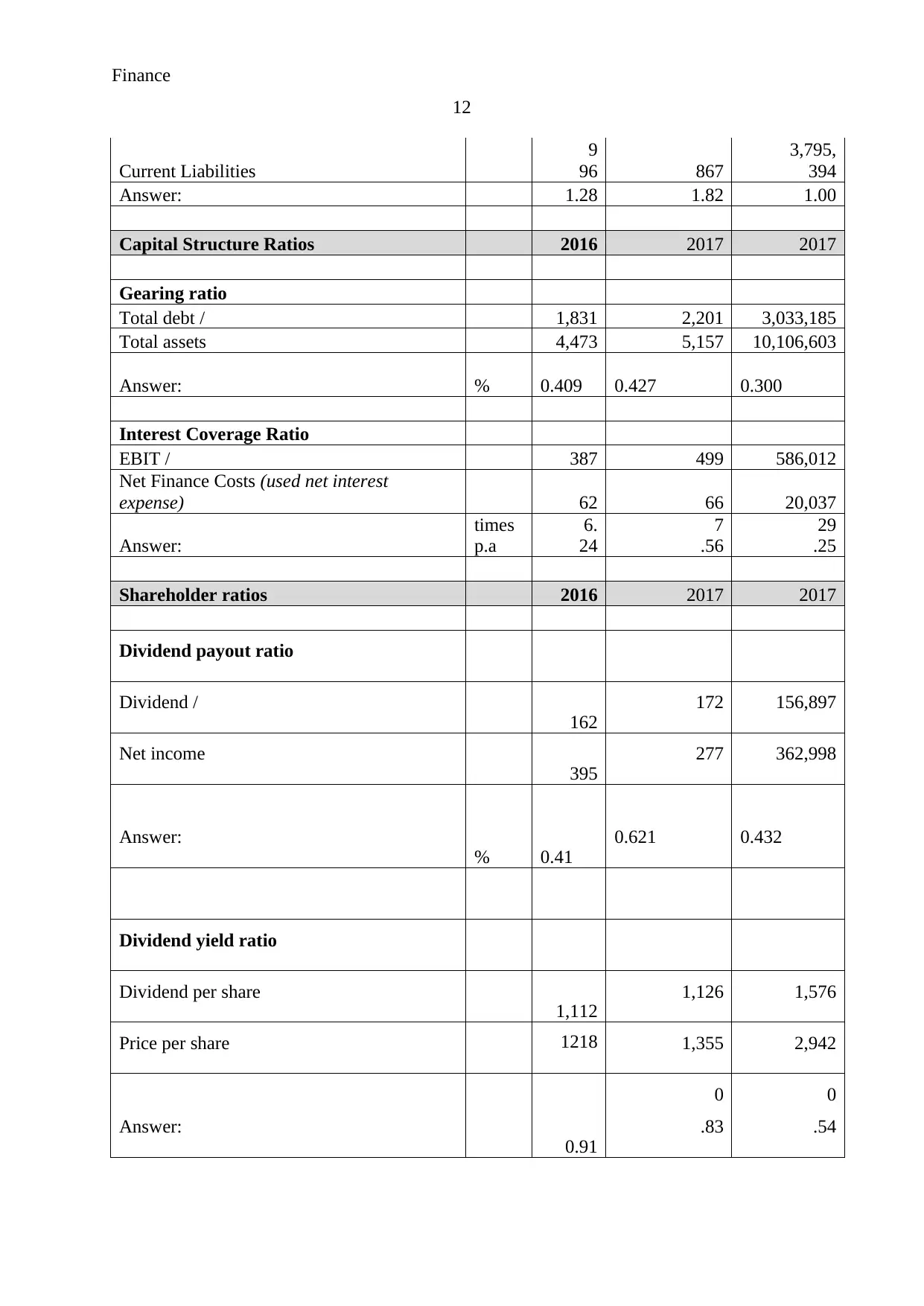

Capital structure analysis:

Capital structure ratio analysis is an indicator to recognize that how much funds have

been generated by the business and what is the proportion of different funds in the total

capital of the business. It evaluates that whether the leverage risk and capital risk of the

3

11.63% ROCE of the company which is quite higher than the ROCE of Hitachi limited i.e.

9.29%. On the other hand, net profit ratio brief the total profit earned by the company against

the sales revenue of the business. It briefs the 17.38% net profit level of the business which is

higher than 3.87% net profitability ratio of Hitachi limited (Performance appendix).

The profitability analysis expresses that Smiths group plc’s performance is quite

better and thus it is a good option in order to make an investment as higher earnings per share

could be achieved by each of the shareholders of the company.

Liquidity analysis:

Liquidity ratio analysis is an indicator to recognize whether the company has enough

current and quick assets in order to meet the short term obligation of the company. It

evaluates whether the entire short term debt obligation could be met by the company through

the available current assets or not (Higgins, 2012). It is mainly calculated to identify the

liquidity risk and working capital efficiency level of the business.

In case of Smith group plc, the current ratio and quick ratio has been calculated by the

company. Current ratio of the business indicates whether the business is capable to meet the

short term obligations. 2:1 and 1.3:1 current ratio and quick ratio are normal for the industry

(Madura, 2014). On the basis of study over Smith group plc, it has been found that the current

assets of the company are 2.34 times of current liabilities of the business which is quite

higher than the Hitachi current assets level i.e. 3.87% (Annual report, 2017). Further, the

quick assets define about the total quick assets (those assets which could be easily converted

into cash) against the current liabilities of the business. The calculations explain that the

quick ratio of the business is also higher than Hitachi limited. Quick assets of the company

are higher than 1.82 times of current liabilities of the business (Performance appendix).

Through the calculations, the liquidity risk of the business is least as the level of

current assets and quick assets of the business are higher. However, it has also been found

that in order to maintain the higher current assets, business has to bear higher expenses which

could be reduced through reducing the level of current assets a bit.

Capital structure analysis:

Capital structure ratio analysis is an indicator to recognize that how much funds have

been generated by the business and what is the proportion of different funds in the total

capital of the business. It evaluates that whether the leverage risk and capital risk of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

4

business is moderate or higher (Hillier, Grinblatt and Titman, 2011). It is mainly calculated to

identify the efficiency level and capital management level of the business.

In case of Smith group plc, the gearing ratio and interest coverage ratio have been

calculated by the company. The gearing ratio of the business indicates that how much funds

have been generated by the debt and what is the proportion of total debt against the total

resources of the business (Weaver, Weston and Weaver, 2012). In case of Smith group plc, it

has been found that the gearing ratio of the company is 42.7% of total assets of the business

which is quite higher than the Hitachi gearing level i.e. 30%. The gearing ratio of the industry

is around 40% in the industry. Further, the interest coverage ratio defines about the total

earnings before interest and tax against the total interest expenses of the business

(Performance appendix). The calculations explain that the interest coverage ratio of the

business is lower than the Hitachi limited i.e. 29.25. Interest coverage ratio of the company is

7.56 times higher than the interest expenses (Annual report, 2017). Interest coverage ratio

must be positively higher than 1.

On the basis of the calculations, capital structure level of Smith is quite better as the

financial leverage position of the company is good. The company could easily manage the

leverage and financial risk in the market and all the other factors have also been managed by

the company at better level.

Asset efficiency ratio:

Asset efficiency ratio analysis is an indicator to recognize about the total assets and

working capital management of the business. It evaluates that whether the business is able to

manage the operations and daily activities in minimum capital requirement (Ward, 2012).

In case of Smith group plc, the creditor’s turnover ratio and stock turnover ratios have

been calculated. Both the ratios define that creditor’s turnover ratio of the company is quite

lower than the Hitachi limited and stock turnover ratio of the company is quite higher than

Hitachi limited i.e. 81.70 and 73.10 (Annual report, 2017). It expresses that the working

capital requirement of the company is quite average.

On the basis of the calculations, it has been determined that the company could

improve the working capital requirement through improving the creditor’s turnover days and

reducing the stock turnover days (Performance appendix).

Shareholder ratio:

4

business is moderate or higher (Hillier, Grinblatt and Titman, 2011). It is mainly calculated to

identify the efficiency level and capital management level of the business.

In case of Smith group plc, the gearing ratio and interest coverage ratio have been

calculated by the company. The gearing ratio of the business indicates that how much funds

have been generated by the debt and what is the proportion of total debt against the total

resources of the business (Weaver, Weston and Weaver, 2012). In case of Smith group plc, it

has been found that the gearing ratio of the company is 42.7% of total assets of the business

which is quite higher than the Hitachi gearing level i.e. 30%. The gearing ratio of the industry

is around 40% in the industry. Further, the interest coverage ratio defines about the total

earnings before interest and tax against the total interest expenses of the business

(Performance appendix). The calculations explain that the interest coverage ratio of the

business is lower than the Hitachi limited i.e. 29.25. Interest coverage ratio of the company is

7.56 times higher than the interest expenses (Annual report, 2017). Interest coverage ratio

must be positively higher than 1.

On the basis of the calculations, capital structure level of Smith is quite better as the

financial leverage position of the company is good. The company could easily manage the

leverage and financial risk in the market and all the other factors have also been managed by

the company at better level.

Asset efficiency ratio:

Asset efficiency ratio analysis is an indicator to recognize about the total assets and

working capital management of the business. It evaluates that whether the business is able to

manage the operations and daily activities in minimum capital requirement (Ward, 2012).

In case of Smith group plc, the creditor’s turnover ratio and stock turnover ratios have

been calculated. Both the ratios define that creditor’s turnover ratio of the company is quite

lower than the Hitachi limited and stock turnover ratio of the company is quite higher than

Hitachi limited i.e. 81.70 and 73.10 (Annual report, 2017). It expresses that the working

capital requirement of the company is quite average.

On the basis of the calculations, it has been determined that the company could

improve the working capital requirement through improving the creditor’s turnover days and

reducing the stock turnover days (Performance appendix).

Shareholder ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

5

Shareholder ratio analysis is an indicator to recognize the market worth of the

business. It evaluates how well the market worth has been managed by the business.

In case of Smith group plc, the dividend payout ratio and dividend yield ratio have

been calculated. Both the ratios define that 0.62 and 0.83 & 0.43 and 0.54 are the dividend

payout ratio and dividend yield ratio of Smith plc and Hitachi limited. It explains that the

position of Smith plc is better in terms of paying the dividend and market position.

On the basis of the calculations, it has been determined that the company’s market

position is strong and the investment into the company would offer huge return to

stakeholders (Performance appendix).

Limitations:

The main limitations of the ratio analysis and the above comparison are as follows:

Some year-end changes might be done in the financial statement of the company in

order to improve the ratios so a stakeholder cannot totally rely on the financial

statement and ratio analysis.

Ratio analysis does not take focus on inflation. Many ratios of the business are

calculated on the basis of the historical cost which does not reflect over the actual

financial situation of the business (Lord, 2006).

Accounting ratios does not help the business to resolve the issues and the main issues

of the business can’t be resolve on the basis of the ratio analysis.

Qualitative aspect is ignored by the firm while calculating the accounting ratios so it

could not be a good reliable source to make few decisions (Krantz, 2016).

Company valuation:

Identifying the true and intrinsic worth of stock of an organization is also a good way

to recognize the investment position of the business and make decision about buy or hold the

stock of the company. Stock price of Smith plc in the market is quite different than the actual

worth of the business. In order to determine the actual worth of stock, asset based valuation,

dividend valuation model and P/E ratios have been calculated (Kaplan and Atkinson, 2015).

The calculation of each of the method has been given in the appendix and the analysis of each

of the method is as follows:

5

Shareholder ratio analysis is an indicator to recognize the market worth of the

business. It evaluates how well the market worth has been managed by the business.

In case of Smith group plc, the dividend payout ratio and dividend yield ratio have

been calculated. Both the ratios define that 0.62 and 0.83 & 0.43 and 0.54 are the dividend

payout ratio and dividend yield ratio of Smith plc and Hitachi limited. It explains that the

position of Smith plc is better in terms of paying the dividend and market position.

On the basis of the calculations, it has been determined that the company’s market

position is strong and the investment into the company would offer huge return to

stakeholders (Performance appendix).

Limitations:

The main limitations of the ratio analysis and the above comparison are as follows:

Some year-end changes might be done in the financial statement of the company in

order to improve the ratios so a stakeholder cannot totally rely on the financial

statement and ratio analysis.

Ratio analysis does not take focus on inflation. Many ratios of the business are

calculated on the basis of the historical cost which does not reflect over the actual

financial situation of the business (Lord, 2006).

Accounting ratios does not help the business to resolve the issues and the main issues

of the business can’t be resolve on the basis of the ratio analysis.

Qualitative aspect is ignored by the firm while calculating the accounting ratios so it

could not be a good reliable source to make few decisions (Krantz, 2016).

Company valuation:

Identifying the true and intrinsic worth of stock of an organization is also a good way

to recognize the investment position of the business and make decision about buy or hold the

stock of the company. Stock price of Smith plc in the market is quite different than the actual

worth of the business. In order to determine the actual worth of stock, asset based valuation,

dividend valuation model and P/E ratios have been calculated (Kaplan and Atkinson, 2015).

The calculation of each of the method has been given in the appendix and the analysis of each

of the method is as follows:

Finance

6

Asset based valuation:

Asset based valuation method focuses on the total assets and the liabilities of the

business in order to determine the fair value of the stock. Through the study over Smith plc,

the intrinsic value of the stock is $ 5.74 9 (valuation appendix) whereas the market value of

stock is $ 1417.5 (yahoo finance, 2018) which is quite higher and thus it is recommended to

the investors to sell the stock of the company so that good returns could be got. In order to

calculate the worth of the stock price, asset valuation model is not an appropriate valuation

model as it only considers the book value of the business. However, in case of merger and

amalgamation process, this model is good option.

Dividend valuation model:

Further, divided valuation model has been applied on the business. Dividend

valuation method focuses on the expected dividend, dividend growth rate, discount rate of the

business etc. in order to determine the fair value of the stock. Through the study over Smith

plc, the intrinsic value of the stock is $ 1472.08 (Valuation appendix) whereas the market

value of stock is $ 1417.5 which is lower and thus it is recommended to the investors to buy

and hold the stock of the company so that good returns could be got by the investors (Yahoo

finance, 2018).

P/E ratio:

Lastly, P/E ratio defines about the fair value of the stock of an organization on the

basis of the stock price and earnings per share of the company (Moles, Parrino and Kidwekk,

2011). It takes the concern on actual and current data of the company to measure the worth of

stock. In case of Smith group plc, it has been found that the intrinsic value of the stock is $

1157.32 (Valuation appendix) whereas the market value of stock is $ 1417.5 which is quite

higher and thus it is recommended to the investors to sell the stock of the company so that

good returns could be got by the investors.

Discussion:

To study over all the methods, it has assumed that all the valuation models (valuation

appendix) are offering the different data in order to identify the fair value of the stock. On the

basis of overall study, it has been found that P/E model is most reliable model to measure the

fair value of stock because it takes the concern on actual and current data of the company to

measure the worth of stock (Lumby and Jones, 2007). Thus, it is suggested to the investors of

6

Asset based valuation:

Asset based valuation method focuses on the total assets and the liabilities of the

business in order to determine the fair value of the stock. Through the study over Smith plc,

the intrinsic value of the stock is $ 5.74 9 (valuation appendix) whereas the market value of

stock is $ 1417.5 (yahoo finance, 2018) which is quite higher and thus it is recommended to

the investors to sell the stock of the company so that good returns could be got. In order to

calculate the worth of the stock price, asset valuation model is not an appropriate valuation

model as it only considers the book value of the business. However, in case of merger and

amalgamation process, this model is good option.

Dividend valuation model:

Further, divided valuation model has been applied on the business. Dividend

valuation method focuses on the expected dividend, dividend growth rate, discount rate of the

business etc. in order to determine the fair value of the stock. Through the study over Smith

plc, the intrinsic value of the stock is $ 1472.08 (Valuation appendix) whereas the market

value of stock is $ 1417.5 which is lower and thus it is recommended to the investors to buy

and hold the stock of the company so that good returns could be got by the investors (Yahoo

finance, 2018).

P/E ratio:

Lastly, P/E ratio defines about the fair value of the stock of an organization on the

basis of the stock price and earnings per share of the company (Moles, Parrino and Kidwekk,

2011). It takes the concern on actual and current data of the company to measure the worth of

stock. In case of Smith group plc, it has been found that the intrinsic value of the stock is $

1157.32 (Valuation appendix) whereas the market value of stock is $ 1417.5 which is quite

higher and thus it is recommended to the investors to sell the stock of the company so that

good returns could be got by the investors.

Discussion:

To study over all the methods, it has assumed that all the valuation models (valuation

appendix) are offering the different data in order to identify the fair value of the stock. On the

basis of overall study, it has been found that P/E model is most reliable model to measure the

fair value of stock because it takes the concern on actual and current data of the company to

measure the worth of stock (Lumby and Jones, 2007). Thus, it is suggested to the investors of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

7

the company to sell the stock of the company in current scenario, along with the time, the

stock price of the company could be reduced and it could lead towards huge loss to the

investors of the company.

Project appraisal:

NPV:

NPV is a project appraisal method which evaluate the total cash outflow and inflow

related to the project to identify that whether the proposal is profitable for the business or not.

On the basis of NPV calculations, it has been found that net cash flow from the project after 4

years would be £ 2,56,020 which is positive and explains that the project must be undertaken

( Project appendix).

Discounted cash flow:

In case of discounted cash flow, the market research cost has not been added as this

was the sunk cost of the business and the depreciation amount has been add back as capital

allowances into the cash flow before calculating the net worth of the cash flow of the

business. It has been added after calculating the tax amount (Horngren, 2009) (Project

appendix).

Other capital budgeting method:

IRR and discounted payback method have also been applied on the project of the

business to determine that whether the project should be undertaken or not. the IRR of the

project is 18.21% (project appendix) which is quite high than the total cost of capital and

hence, it is concluded that the project should be approached whereas the discounted payback

of the business define that the total invested amount would be got back by the business in

2.91 years which is lesser than total life time of the project (Moles, Parrino and Kidwekk,

2011).

On the basis of the above evaluation on the project with different techniques, it has

been found that the project should be accepted by the company. It would offer better return to

the company.

Conclusion and recommendation:

To conclude, the overall financial performance of Smith is bit better in the industry

(performance appendix). As well as, the project should also be accepted by the business as it

7

the company to sell the stock of the company in current scenario, along with the time, the

stock price of the company could be reduced and it could lead towards huge loss to the

investors of the company.

Project appraisal:

NPV:

NPV is a project appraisal method which evaluate the total cash outflow and inflow

related to the project to identify that whether the proposal is profitable for the business or not.

On the basis of NPV calculations, it has been found that net cash flow from the project after 4

years would be £ 2,56,020 which is positive and explains that the project must be undertaken

( Project appendix).

Discounted cash flow:

In case of discounted cash flow, the market research cost has not been added as this

was the sunk cost of the business and the depreciation amount has been add back as capital

allowances into the cash flow before calculating the net worth of the cash flow of the

business. It has been added after calculating the tax amount (Horngren, 2009) (Project

appendix).

Other capital budgeting method:

IRR and discounted payback method have also been applied on the project of the

business to determine that whether the project should be undertaken or not. the IRR of the

project is 18.21% (project appendix) which is quite high than the total cost of capital and

hence, it is concluded that the project should be approached whereas the discounted payback

of the business define that the total invested amount would be got back by the business in

2.91 years which is lesser than total life time of the project (Moles, Parrino and Kidwekk,

2011).

On the basis of the above evaluation on the project with different techniques, it has

been found that the project should be accepted by the company. It would offer better return to

the company.

Conclusion and recommendation:

To conclude, the overall financial performance of Smith is bit better in the industry

(performance appendix). As well as, the project should also be accepted by the business as it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

8

would offer great return to the business (Project appendix). However, on the basis of

valuation approaches, it is recommended to the business to make few changes in internal

activities so that the fair value of the stock could be improved (Valuation appendix).

8

would offer great return to the business (Project appendix). However, on the basis of

valuation approaches, it is recommended to the business to make few changes in internal

activities so that the fair value of the stock could be improved (Valuation appendix).

Finance

9

References:

Annual report. 2017. Hitachi limited. (online). available at:

http://www.hitachi.com/IR-e/library/integrated/ (Accessed 5/12/2018).

Annual report. 2017. Smith group plc. (online). available at:

https://www.smiths.com/-/media/files/annual-report-2017.ashx (Accessed 5/12/2018).

Barlow.J.F.,2006. Excel models for business and operations management, 2nd edition, John

Wiley and sons ltd, England

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018. Smith group plc. (online). available at: https://www.smiths.com/ (Accessed

5/12/2018).

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. London: John Wiley and Sons.

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Lumby,S and Jones,C,.2007. Corporate finance theory and practice, 7th edition, Thomson,

London

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance. European edition, John

Wiley andsons, United Kingdom

Ward, K., 2012. Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2011. Finance and accounting for nonfinancial

managers. New York: McGraw-Hill.

9

References:

Annual report. 2017. Hitachi limited. (online). available at:

http://www.hitachi.com/IR-e/library/integrated/ (Accessed 5/12/2018).

Annual report. 2017. Smith group plc. (online). available at:

https://www.smiths.com/-/media/files/annual-report-2017.ashx (Accessed 5/12/2018).

Barlow.J.F.,2006. Excel models for business and operations management, 2nd edition, John

Wiley and sons ltd, England

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018. Smith group plc. (online). available at: https://www.smiths.com/ (Accessed

5/12/2018).

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Krantz, M. 2016. Fundamental Analysis for Dummies. London: John Wiley and Sons.

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Lumby,S and Jones,C,.2007. Corporate finance theory and practice, 7th edition, Thomson,

London

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance. European edition, John

Wiley andsons, United Kingdom

Ward, K., 2012. Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2011. Finance and accounting for nonfinancial

managers. New York: McGraw-Hill.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

10

Yahoo Finance. 2018. Smith group plc. (online). available at:

https://finance.yahoo.com/quote/SMIN.L/history?

period1=1385749800&period2=1543516200&interval=div

%7Csplit&filter=div&frequency=1d (Accessed 5/12/2018).

10

Yahoo Finance. 2018. Smith group plc. (online). available at:

https://finance.yahoo.com/quote/SMIN.L/history?

period1=1385749800&period2=1543516200&interval=div

%7Csplit&filter=div&frequency=1d (Accessed 5/12/2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

11

Appendix:

Performance appendix:

Smiths Group Plc

Hitachi

Limited

Ratio Calculations 2016 2017 2017

Profitability Ratios: 2016 2017 2017

Return on Capital employed

Operating profit / 387 499 586,012

Capital employed (total assets - current

liabilities)

3,4

77

4,

290

6,311,

209

Answer: % 11.13% 11.63% 9.29%

Net profit margin %

Net profit / 259 570 362,998

Sales Revenue % 2,949 3,280 9,368,614

Answer: 8.78% 17.38% 3.87%

Asset efficiency ratio 2016 2017 2017

Creditors turnover days

Accounts payable/ 202 202 1,536,983

Cost of sales 1,600 1,755 6,866,522

Answer: (note the above needs to be x 365) # days 46.08 42.01 81.70

Stock Turnover (days)

Average Inventory / 478 452 1,375,232

Cost of Sales # days 1,600 1,755 6,866,522

Answer: (note the above needs to be x 365) 109.04 94.01 73.10

Liquidity Ratios 2016 2017 2017

Current Ratio

Current Assets / 1,753 2,031 5,151,800

Current liabilities

9

96 867

3,795,

394

Answer: 1.76 2.34 1.36

Quick ratio

Current Assets - Inventory / 1,275 1,579 3,776,568

11

Appendix:

Performance appendix:

Smiths Group Plc

Hitachi

Limited

Ratio Calculations 2016 2017 2017

Profitability Ratios: 2016 2017 2017

Return on Capital employed

Operating profit / 387 499 586,012

Capital employed (total assets - current

liabilities)

3,4

77

4,

290

6,311,

209

Answer: % 11.13% 11.63% 9.29%

Net profit margin %

Net profit / 259 570 362,998

Sales Revenue % 2,949 3,280 9,368,614

Answer: 8.78% 17.38% 3.87%

Asset efficiency ratio 2016 2017 2017

Creditors turnover days

Accounts payable/ 202 202 1,536,983

Cost of sales 1,600 1,755 6,866,522

Answer: (note the above needs to be x 365) # days 46.08 42.01 81.70

Stock Turnover (days)

Average Inventory / 478 452 1,375,232

Cost of Sales # days 1,600 1,755 6,866,522

Answer: (note the above needs to be x 365) 109.04 94.01 73.10

Liquidity Ratios 2016 2017 2017

Current Ratio

Current Assets / 1,753 2,031 5,151,800

Current liabilities

9

96 867

3,795,

394

Answer: 1.76 2.34 1.36

Quick ratio

Current Assets - Inventory / 1,275 1,579 3,776,568

Finance

12

Current Liabilities

9

96 867

3,795,

394

Answer: 1.28 1.82 1.00

Capital Structure Ratios 2016 2017 2017

Gearing ratio

Total debt / 1,831 2,201 3,033,185

Total assets 4,473 5,157 10,106,603

Answer: % 0.409 0.427 0.300

Interest Coverage Ratio

EBIT / 387 499 586,012

Net Finance Costs (used net interest

expense) 62 66 20,037

Answer:

times

p.a

6.

24

7

.56

29

.25

Shareholder ratios 2016 2017 2017

Dividend payout ratio

Dividend /

162

172 156,897

Net income

395

277 362,998

Answer:

% 0.41

0.621 0.432

Dividend yield ratio

Dividend per share

1,112

1,126 1,576

Price per share 1218 1,355 2,942

Answer:

0.91

0

.83

0

.54

12

Current Liabilities

9

96 867

3,795,

394

Answer: 1.28 1.82 1.00

Capital Structure Ratios 2016 2017 2017

Gearing ratio

Total debt / 1,831 2,201 3,033,185

Total assets 4,473 5,157 10,106,603

Answer: % 0.409 0.427 0.300

Interest Coverage Ratio

EBIT / 387 499 586,012

Net Finance Costs (used net interest

expense) 62 66 20,037

Answer:

times

p.a

6.

24

7

.56

29

.25

Shareholder ratios 2016 2017 2017

Dividend payout ratio

Dividend /

162

172 156,897

Net income

395

277 362,998

Answer:

% 0.41

0.621 0.432

Dividend yield ratio

Dividend per share

1,112

1,126 1,576

Price per share 1218 1,355 2,942

Answer:

0.91

0

.83

0

.54

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.