ACCT20073 - Financial Accounting: Consolidated Financial Statements

VerifiedAdded on 2023/06/08

|11

|1276

|117

Homework Assignment

AI Summary

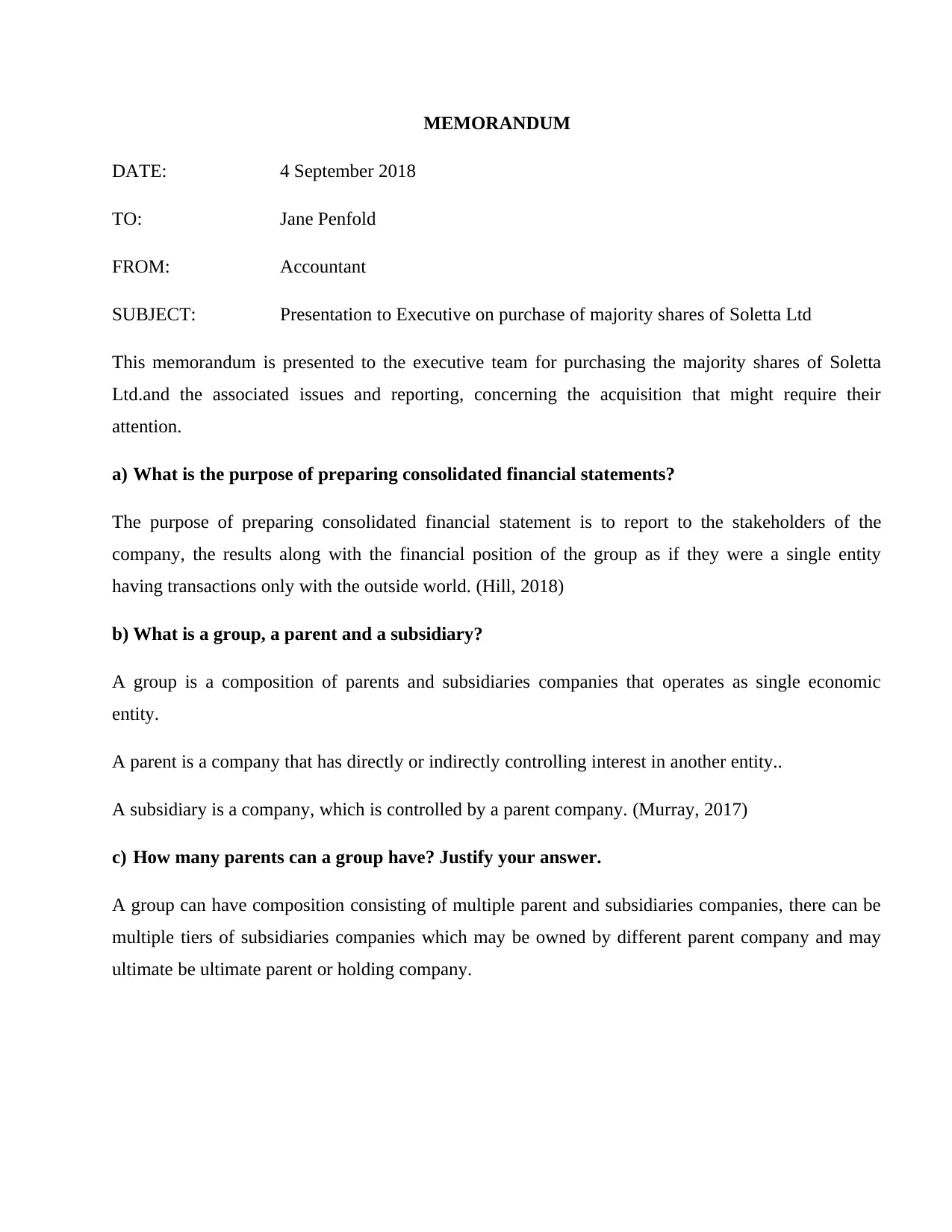

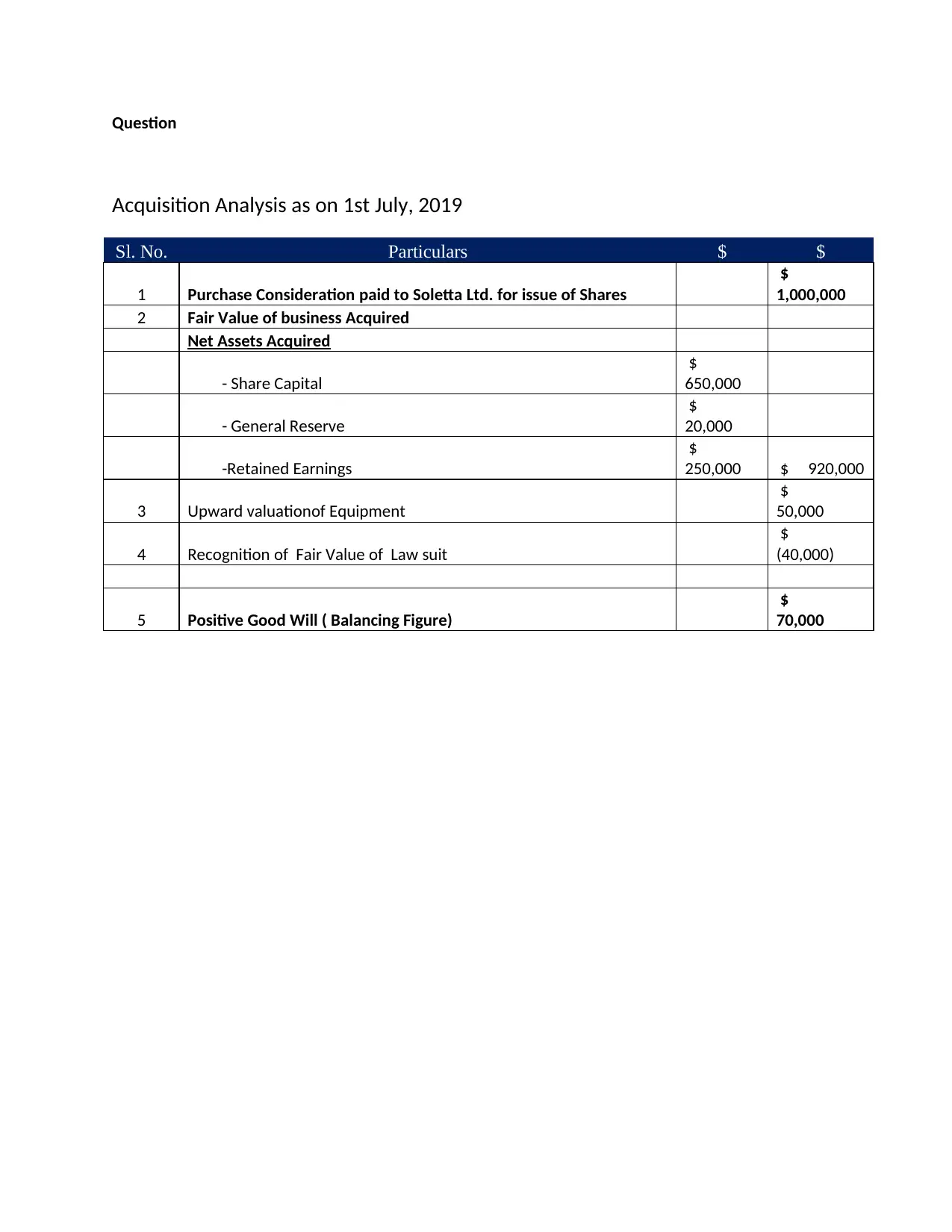

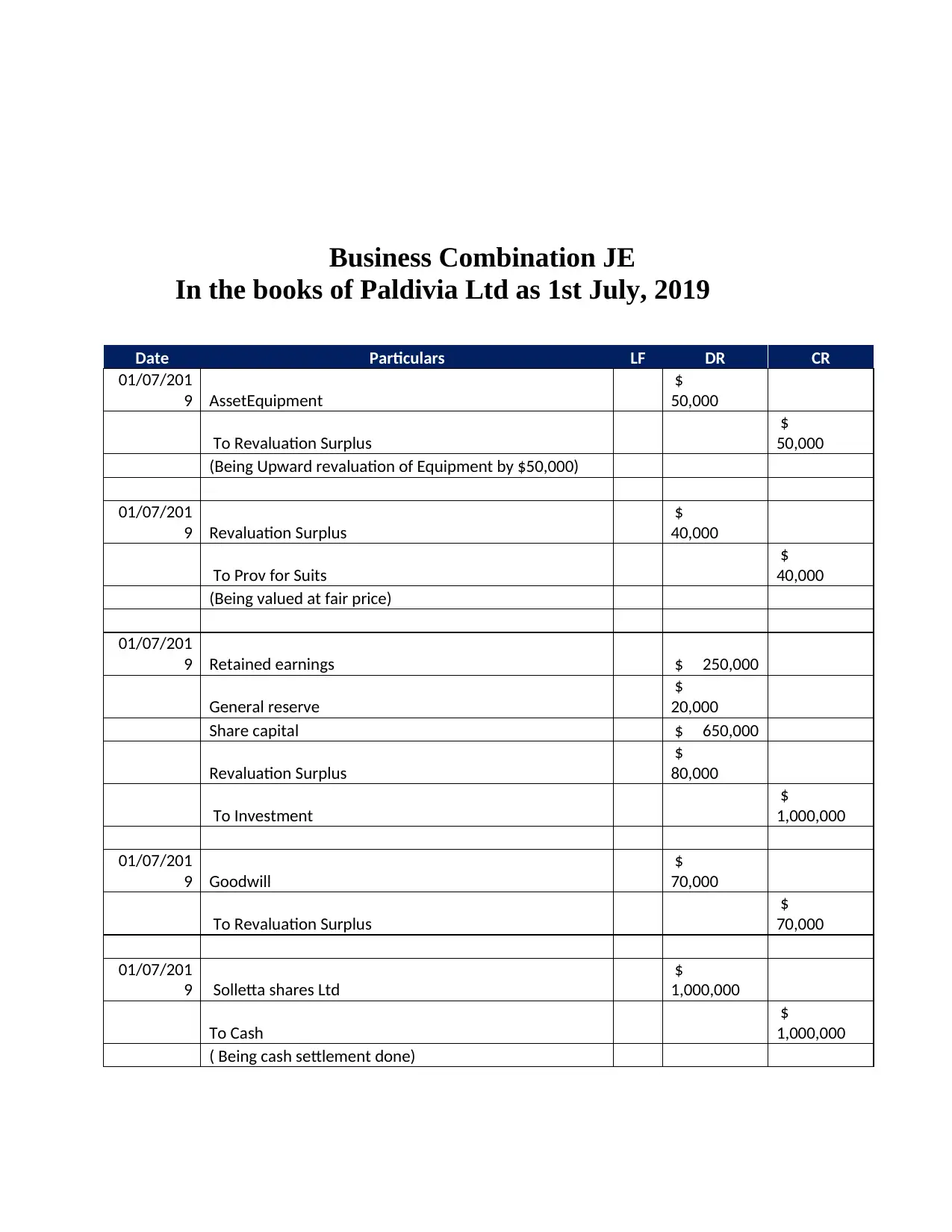

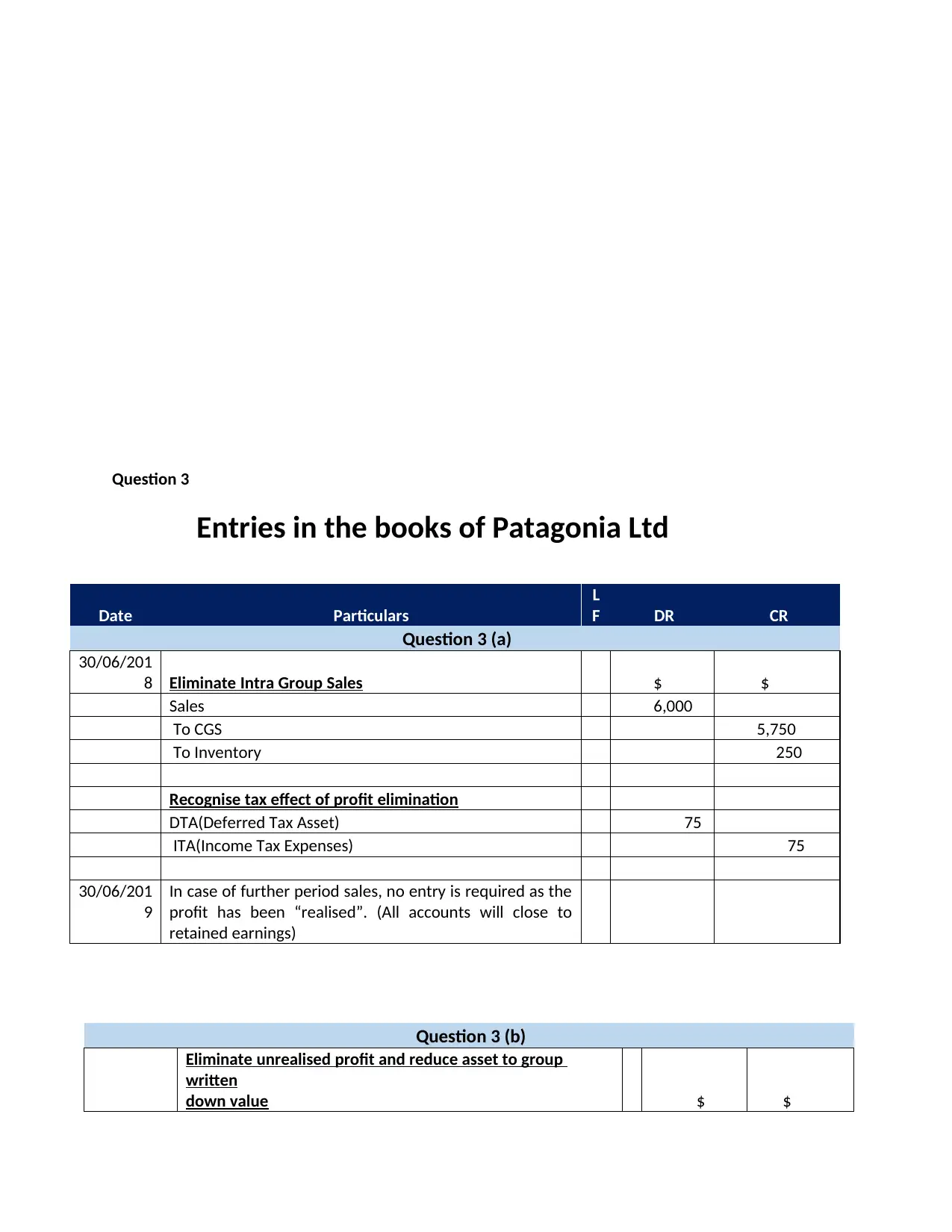

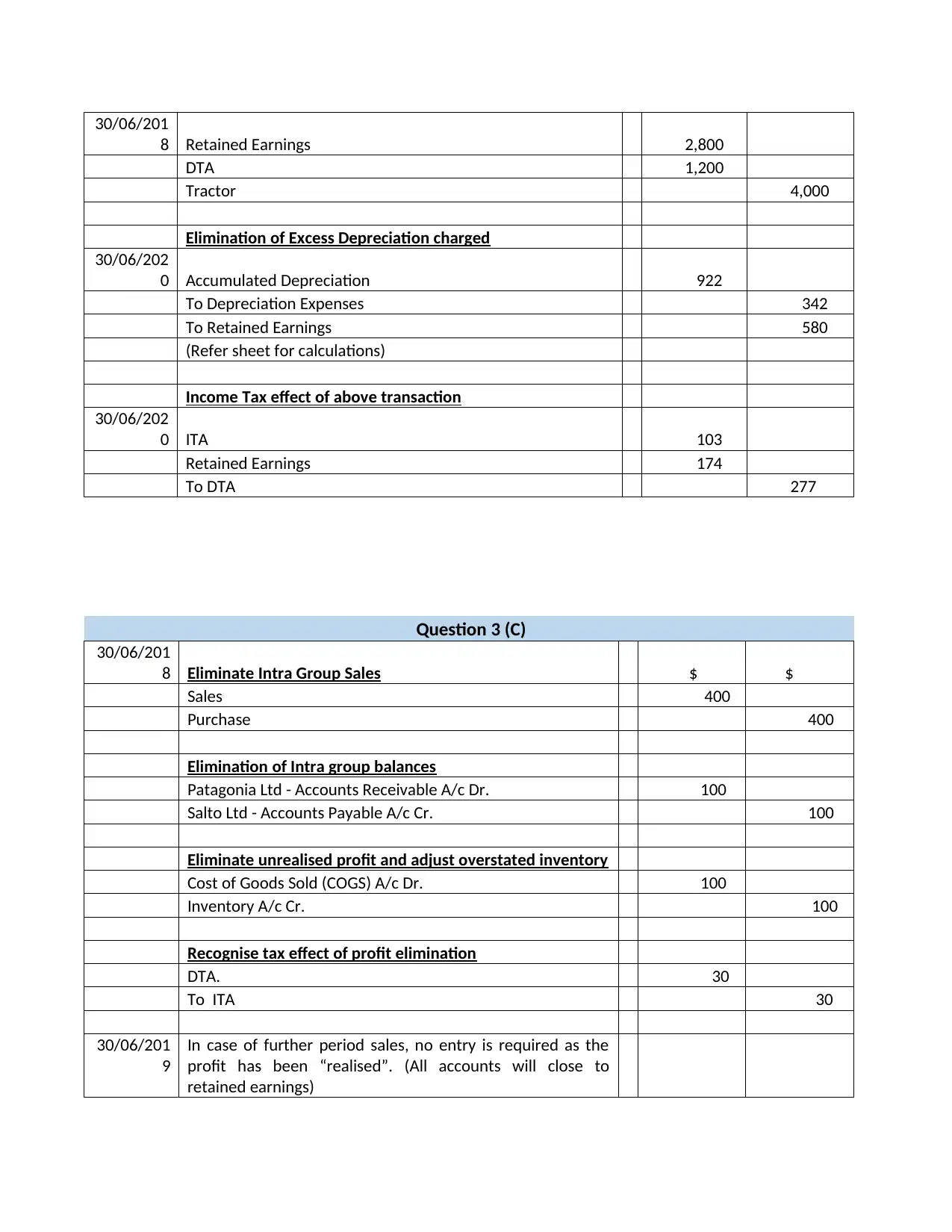

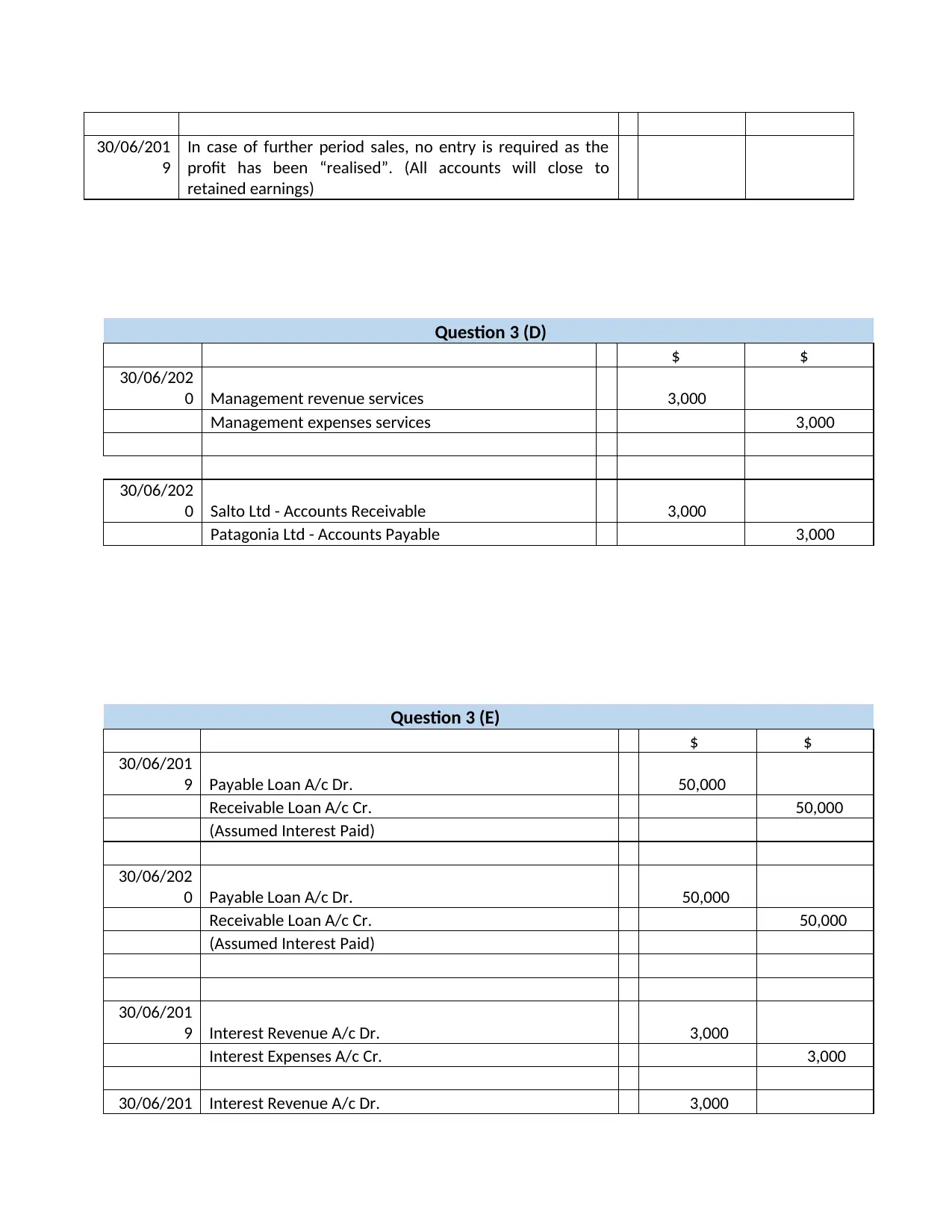

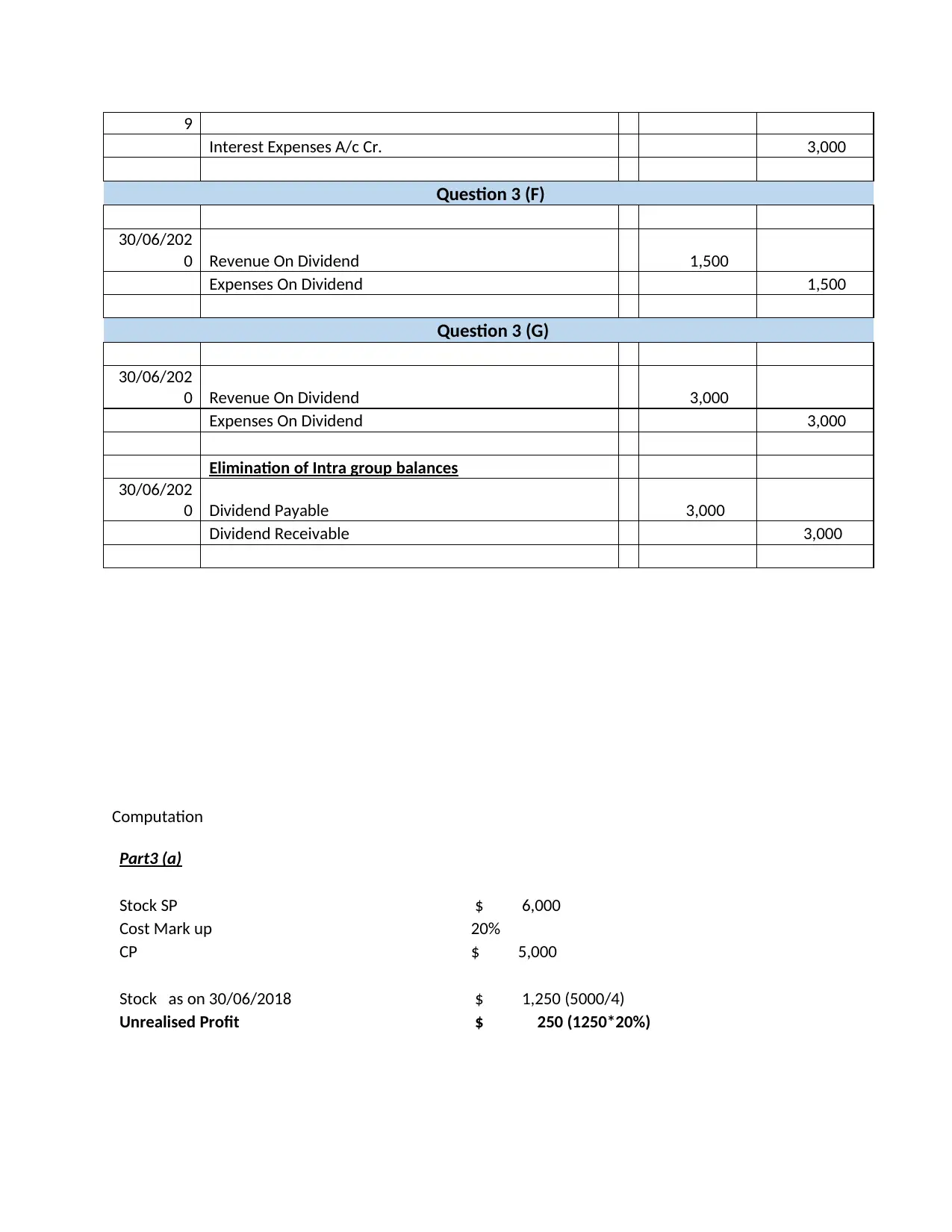

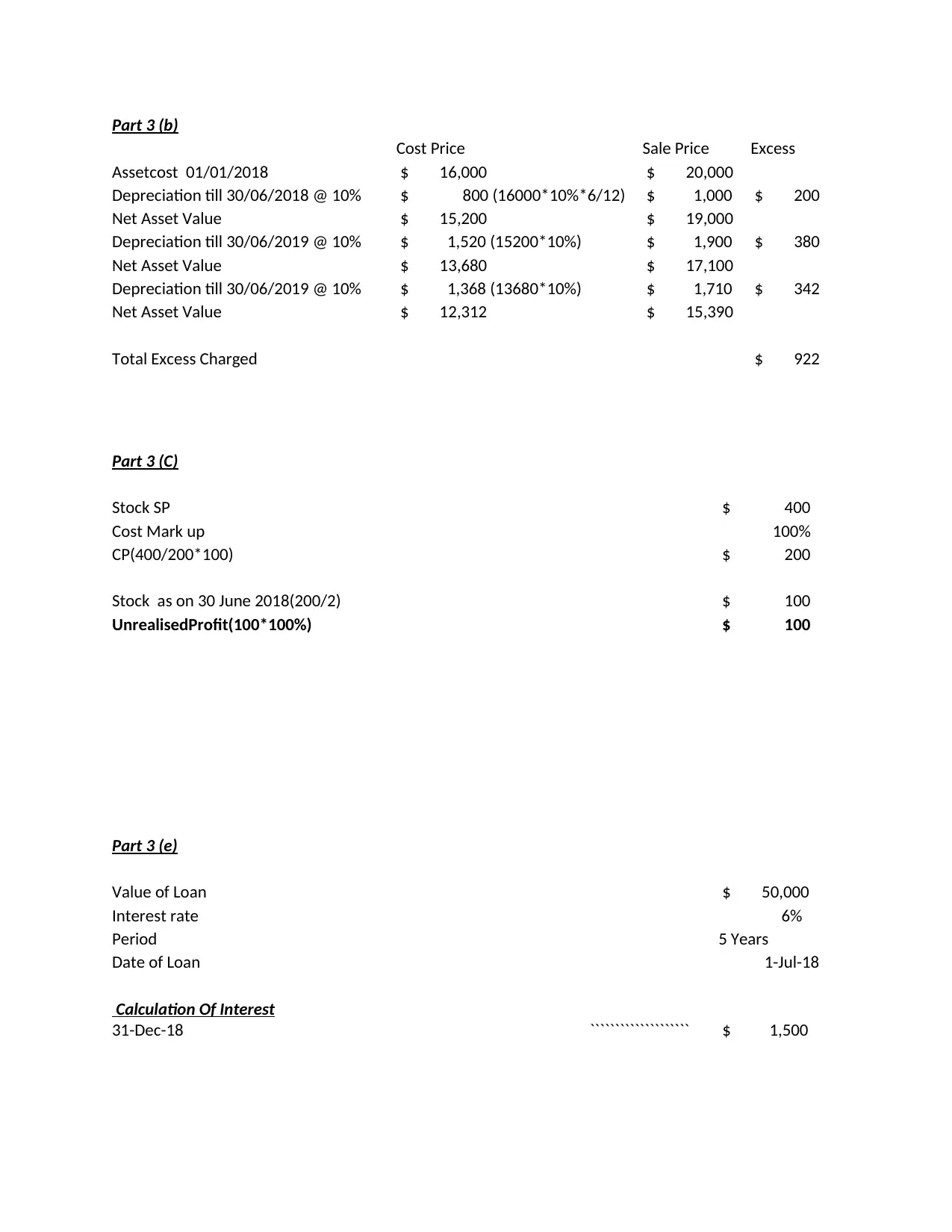

This assignment solution provides a comprehensive analysis of the consolidation of financial statements, specifically focusing on the acquisition of Soletta Ltd. It addresses the purpose of consolidated financial statements, defines key terms like group, parent, and subsidiary, and explains the necessity of adjusting for intragroup transactions. The solution includes an acquisition analysis as of July 1, 2019, detailing the purchase consideration, fair value of business acquired, net assets, upward valuation of equipment, recognition of fair value of a lawsuit, and goodwill calculation. Furthermore, it presents journal entries for the business combination and adjustments for intragroup sales, unrealized profits, excess depreciation, and other intercompany transactions, including loans and dividends. The calculations for unrealized profits on inventory and the impact of these transactions on the consolidated financial statements are thoroughly explained, with references provided for further understanding.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.