Comprehensive Management Accounting Assignment: Budgeting and Strategy

VerifiedAdded on 2023/01/23

|14

|2265

|75

Homework Assignment

AI Summary

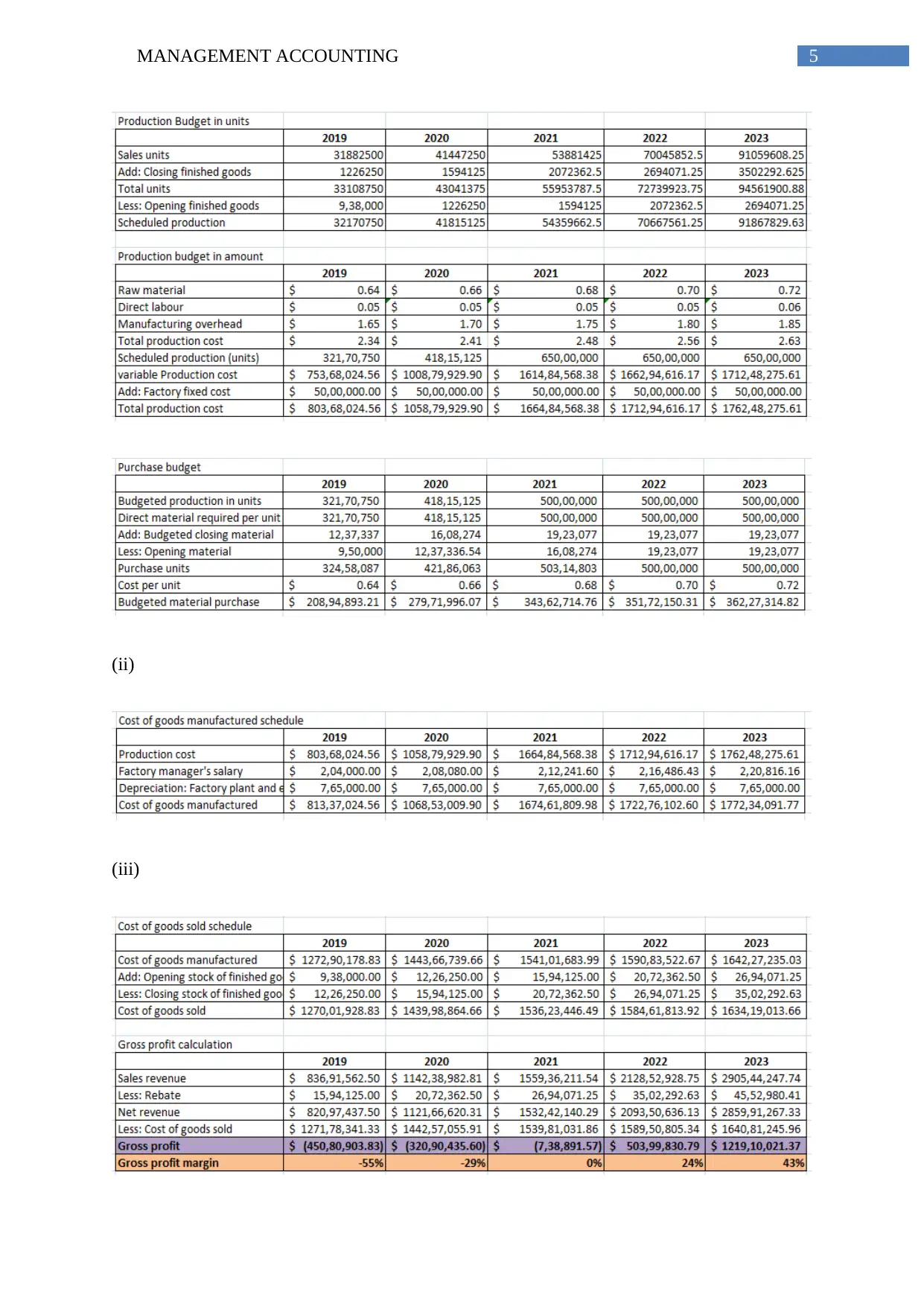

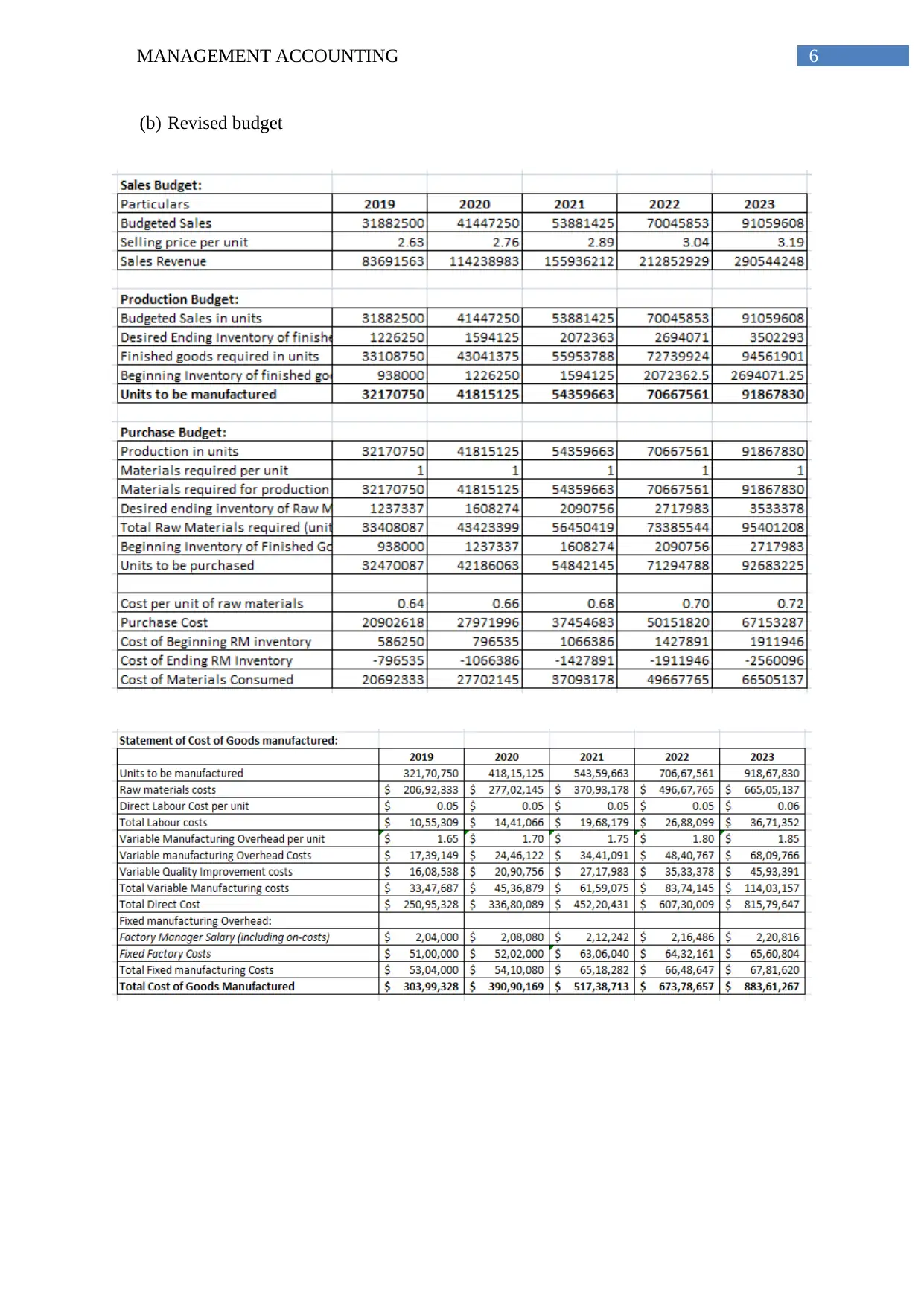

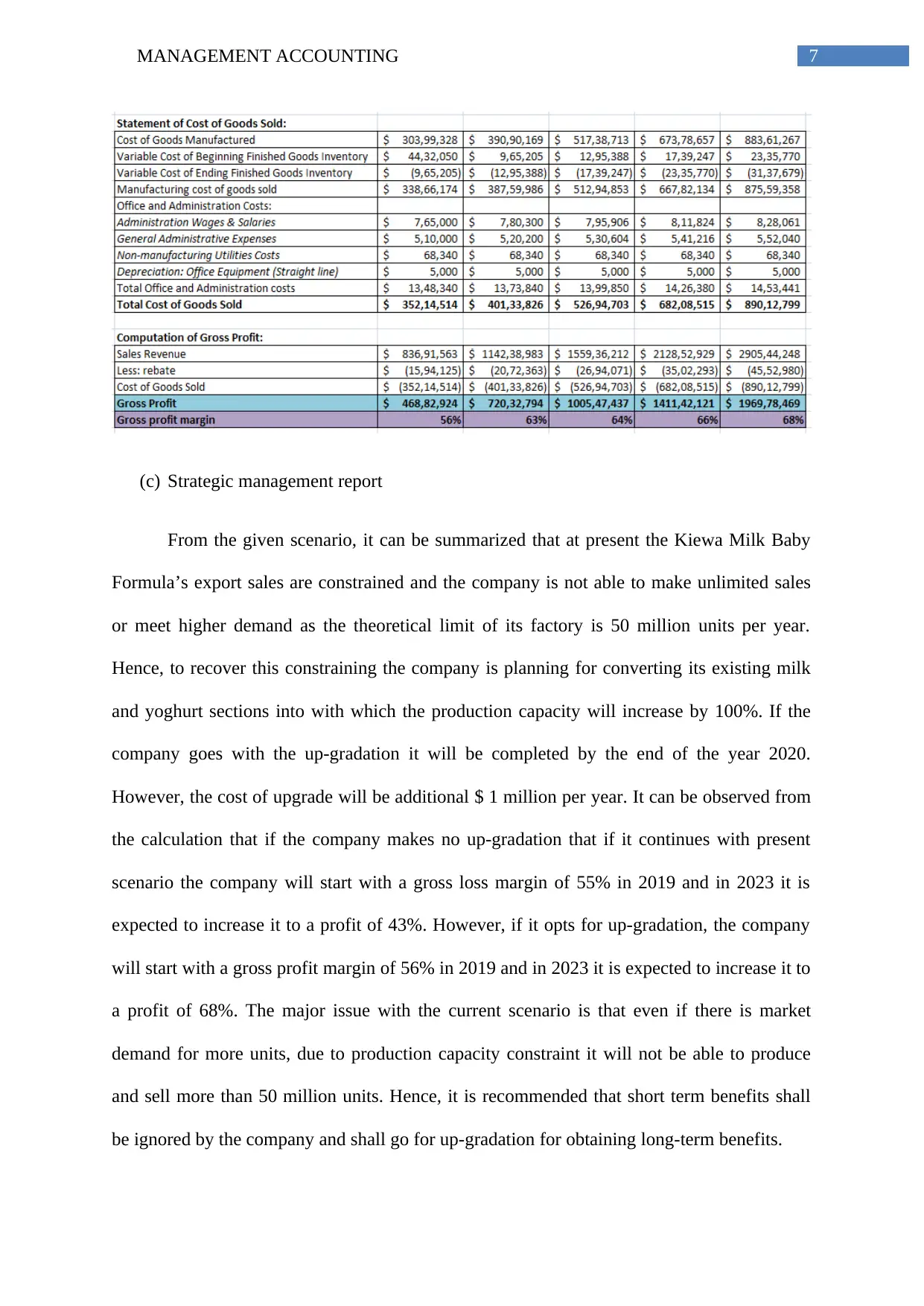

This assignment solution covers various aspects of management accounting, including manufacturing cost flows, cost behavior analysis, and the creation of a comprehensive manufacturing budget. It delves into production capacity constraints, relevant ranges, and the impact of different factors on production. Furthermore, the assignment addresses strategic and international issues, particularly in the context of the dairy industry, exploring global demand, trade agreements, and cultural considerations like Guanxi and power distance in China. The solution also includes a comparative analysis of a product, offers recommendations for a strategic management committee, and examines the cost and profit structure of a company, providing insightful recommendations based on the analysis. The assignment emphasizes the application of technical, analytical, and communication skills in addressing management accounting problems.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.