Corporate Accounting Assignment: Financial Statement Consolidation

VerifiedAdded on 2022/12/30

|11

|1664

|98

Practical Assignment

AI Summary

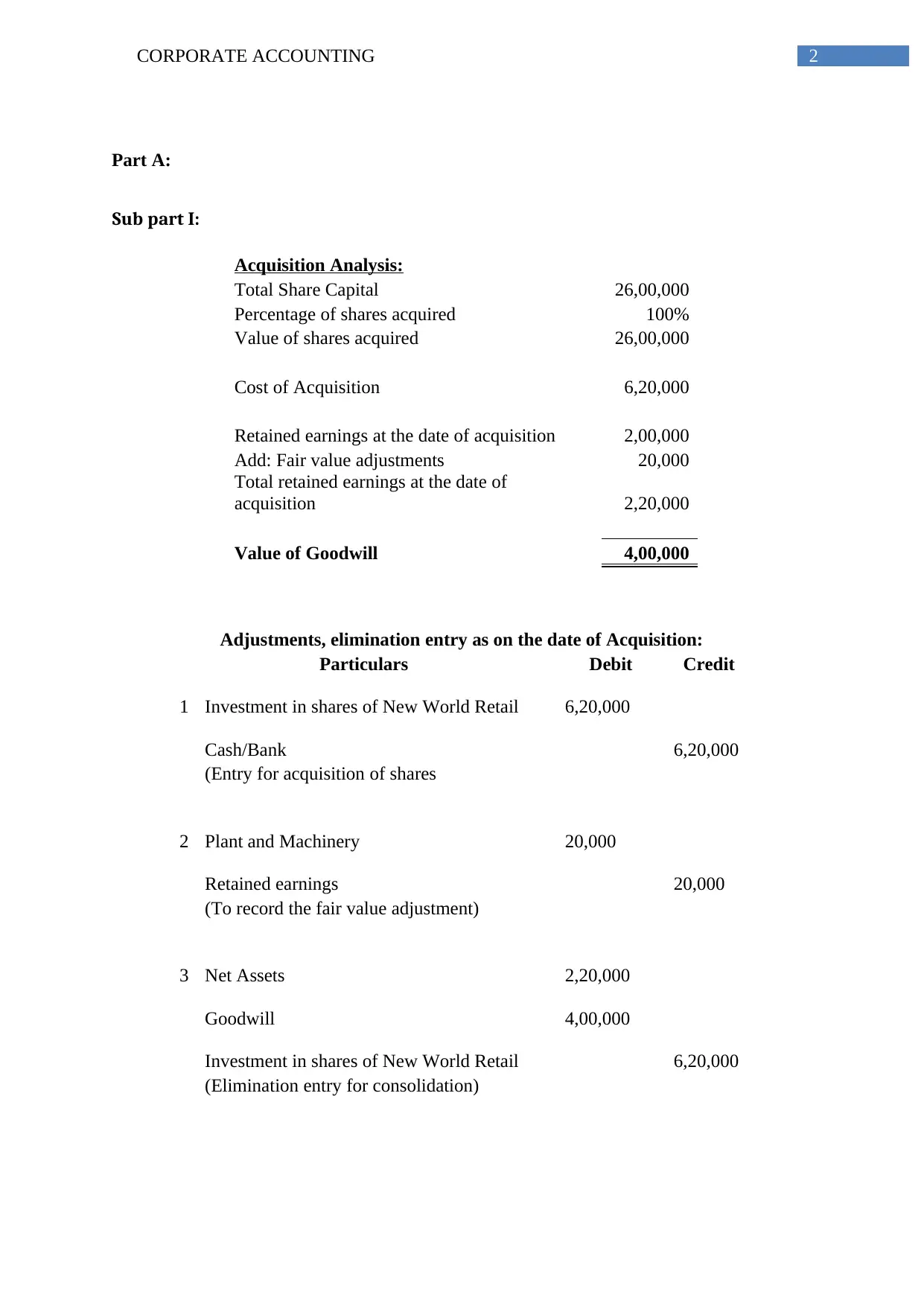

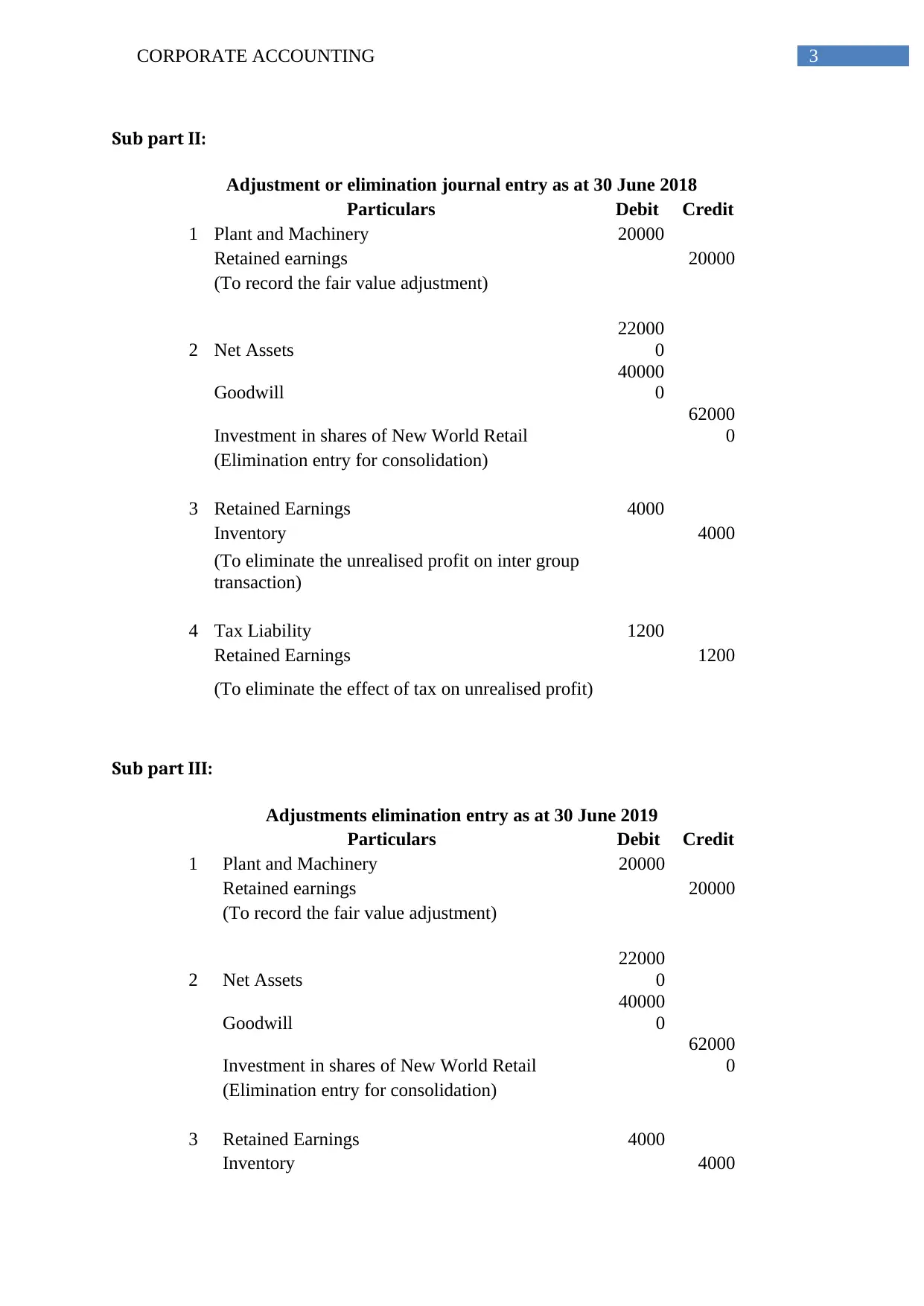

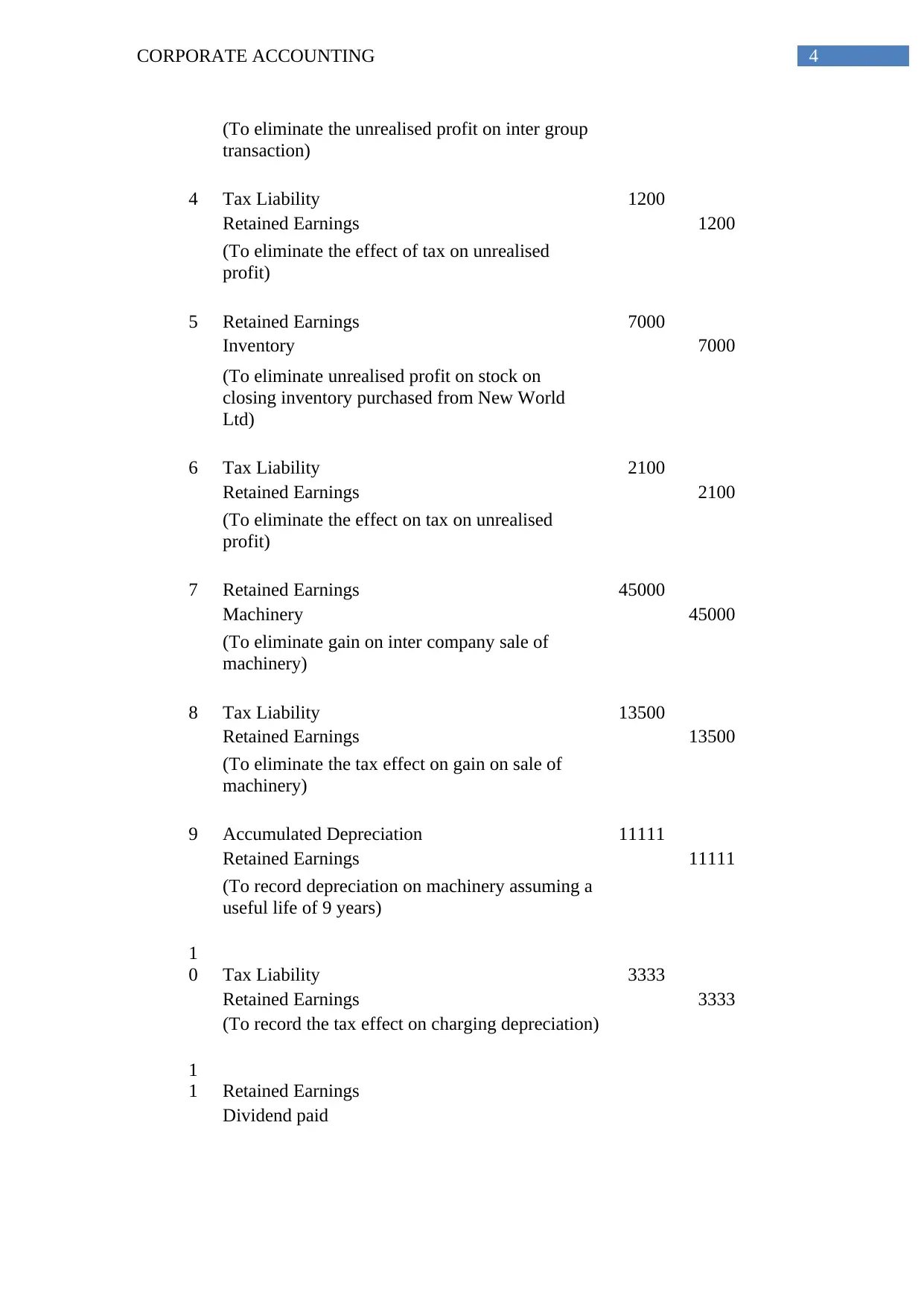

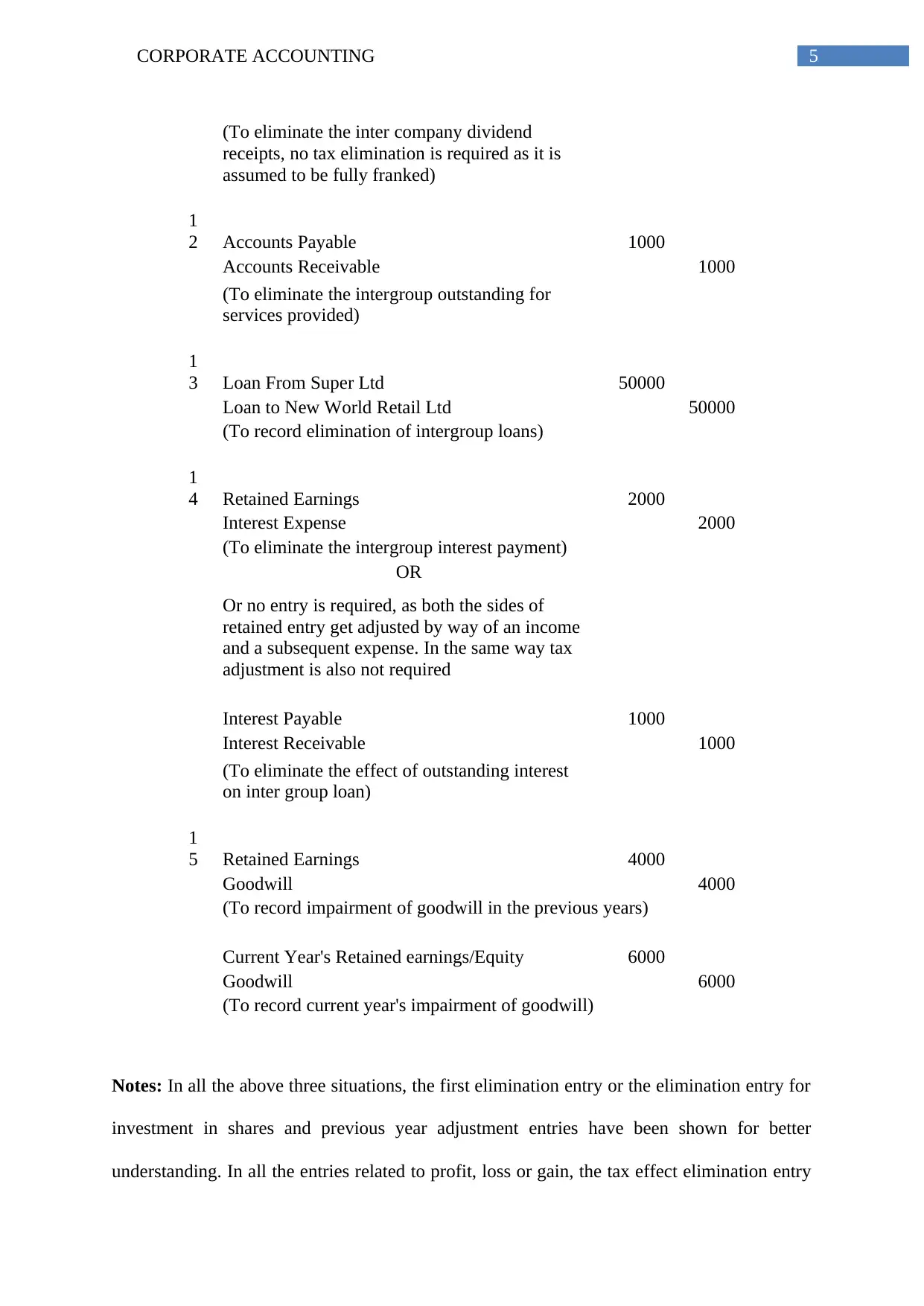

This assignment solution focuses on corporate accounting, specifically addressing the acquisition of New World Retail Ltd by Super Retail Ltd. The solution provides detailed calculations and journal entries related to the acquisition, including the determination of goodwill, fair value adjustments, and the elimination of inter-company transactions. The assignment covers consolidation adjustments for the years ended June 30, 2018, and June 30, 2019, addressing unrealized profits on inventory, inter-company sales of plant and machinery, and the elimination of intercompany loans and interest. The solution also includes an introduction discussing the challenges and complexities of international acquisitions, particularly the differences in accounting standards between countries like Australia and the United States. It emphasizes the role of IFRS in facilitating international business combinations and highlights the importance of harmonization in accounting policies.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.