Financial Analysis of Sweet Menu Restaurant and Blue Island Restaurant

VerifiedAdded on 2020/01/23

|17

|5272

|54

Report

AI Summary

This report provides a comprehensive financial analysis, focusing on the Sweet Menu and Blue Island restaurants. It begins by identifying various sources of finance, both internal and external, and discusses their implications and suitability for Sweet Menu. The report then delves into the costs associated with different financing options and emphasizes the importance of financial planning for the restaurant's success. It explores the types of information needed by decision-makers, analyzes a cash budget, and evaluates investment proposals using relevant techniques. Furthermore, the report examines main financial statements and calculates various financial ratios to compare the financial positions of both restaurants, offering valuable insights into their performance and financial health.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Different types of sources of finance....................................................................................1

1.2 Implication of sources of finance..........................................................................................2

1.3 Most appropriate sources of finance for Sweet Menu restaurant.........................................3

Task 2...............................................................................................................................................4

2.1 Cost of different sources of finance......................................................................................4

2.2 Importance of financial planning to Sweet Menu restaurant...............................................5

2.3 Information needed by decision maker of Sweet Menu restaurant......................................6

2.4 Impact of sources of finance on financial statements...........................................................6

Task 3 ..............................................................................................................................................7

3.1 Analyze of Blue Island restaurant cash budget.....................................................................7

3.2 Calculation of Unit cost and its relevant decisions related to pricing...................................8

3.3 Viability of the proposal by using investment techniques....................................................8

Task 4...............................................................................................................................................9

4.1 Main financial statements....................................................................................................9

4.2 Financial statements need to be prepare by different types of organization......................10

4.3 Calculation of various ratios to find out the best company................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

INTRODUCTION ..........................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Different types of sources of finance....................................................................................1

1.2 Implication of sources of finance..........................................................................................2

1.3 Most appropriate sources of finance for Sweet Menu restaurant.........................................3

Task 2...............................................................................................................................................4

2.1 Cost of different sources of finance......................................................................................4

2.2 Importance of financial planning to Sweet Menu restaurant...............................................5

2.3 Information needed by decision maker of Sweet Menu restaurant......................................6

2.4 Impact of sources of finance on financial statements...........................................................6

Task 3 ..............................................................................................................................................7

3.1 Analyze of Blue Island restaurant cash budget.....................................................................7

3.2 Calculation of Unit cost and its relevant decisions related to pricing...................................8

3.3 Viability of the proposal by using investment techniques....................................................8

Task 4...............................................................................................................................................9

4.1 Main financial statements....................................................................................................9

4.2 Financial statements need to be prepare by different types of organization......................10

4.3 Calculation of various ratios to find out the best company................................................11

Conclusion.....................................................................................................................................13

References......................................................................................................................................13

INTRODUCTION

Finance is the branch of economics that is concerned with the allocation of resources in

each and every department and organization as well as with the management, acquisition and

investment (Barnes and Pancost, 2010). Finance deals with all the matters that are related to the

money as well as market. In simply words, it could be said that finance includes the process of

providing money for different projects.

The following report is going to depict about the various sources of finance through

which an organization can raise its funds in order to meet its various needs. In addition to this,

costs which need to be bearded by company through using various sources of finance are also

mentioned. In this report, some of the best sources of finance through which Sweet Menu

restaurant can raise its finance in order to expand its business are also discussed. In this,

importance of financial planning is also mentioned. Along with this, various types of information

needed by the decision maker of company are also interpreted.

In the following report, budget of Blue Island restaurant is analyzed in order to find out

its current market position. In addition to this, two proposals are analyzed by using various

investment techniques in order to found out the best one. In this report, different types of

financial statements are also mentioned. At last, various ratios are calculated by taking into

consideration the profit and loss account as well as balance sheet with an aim to compare the

financial position of Sweet Menu restaurant and Blue Island restaurant.

Task 1

1.1 Different types of sources of finance

There are different types of sources of finance through which company can raise its

funds. Some sources through which company can raise the availability of finance are present in

the internal environment of it while some of them are present in the external environmental.

Internal sources of finance

Sale of assets This is one of the best methods through which company can raise finance.

By selling its old or obsolescent asset, company can raise the level of its

funds. Simply, keeping the useless asset will increase the cost of company

(Bhowmik and Saha, 2013). So, this method can be used by company in

Finance is the branch of economics that is concerned with the allocation of resources in

each and every department and organization as well as with the management, acquisition and

investment (Barnes and Pancost, 2010). Finance deals with all the matters that are related to the

money as well as market. In simply words, it could be said that finance includes the process of

providing money for different projects.

The following report is going to depict about the various sources of finance through

which an organization can raise its funds in order to meet its various needs. In addition to this,

costs which need to be bearded by company through using various sources of finance are also

mentioned. In this report, some of the best sources of finance through which Sweet Menu

restaurant can raise its finance in order to expand its business are also discussed. In this,

importance of financial planning is also mentioned. Along with this, various types of information

needed by the decision maker of company are also interpreted.

In the following report, budget of Blue Island restaurant is analyzed in order to find out

its current market position. In addition to this, two proposals are analyzed by using various

investment techniques in order to found out the best one. In this report, different types of

financial statements are also mentioned. At last, various ratios are calculated by taking into

consideration the profit and loss account as well as balance sheet with an aim to compare the

financial position of Sweet Menu restaurant and Blue Island restaurant.

Task 1

1.1 Different types of sources of finance

There are different types of sources of finance through which company can raise its

funds. Some sources through which company can raise the availability of finance are present in

the internal environment of it while some of them are present in the external environmental.

Internal sources of finance

Sale of assets This is one of the best methods through which company can raise finance.

By selling its old or obsolescent asset, company can raise the level of its

funds. Simply, keeping the useless asset will increase the cost of company

(Bhowmik and Saha, 2013). So, this method can be used by company in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order to meet its both the short term and long term requirements of funds.

2

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained profit Retained profit is the part of profit which is kept by company as a reserve.

By using this method, Sweet Menu restaurant will be able to raise its finance

in order to expand its business.

Friends and

families

Sweet Menu restaurant can also raise its finance by taking funds from

friends or family members. Normally, company needs to pay less interest to

its friends and family members.

External sources of finance

Issue of shares In order to meet its long term requirement of funds, company can raise its

funds by issuing equity shares to the general public (Brigham and Daves,

2012).

Bank loan It is the method through which company can borrow funds from the bank by

paying interest to them. This method can be used by company to meet its

short-term and Long-term requirement of finance.

Hire purchase This is the method through which company can use the asset or property

without purchasing it at that particular time.

1.2 Implication of sources of finance

Sources Legal aspects dilution bankruptcy

Sale of assets At the time of selling

assets, Sweet Menu

restaurant is required

to follow the legal

procedure (Brigham

and Ehrhardt, 2013).

Once, the legal

procedure for selling

assets is completed

then, at the particular

time, ownership

changes.

If situation of

bankruptcy arises, then

creditors can sell out

the assets of company

in order to recover

their money.

Retained profit No legal procedure is

needs to be followed

by company at the

Ownership does not

change. It remains

with the company

If retained profit is

available, then in that

case, condition of

3

By using this method, Sweet Menu restaurant will be able to raise its finance

in order to expand its business.

Friends and

families

Sweet Menu restaurant can also raise its finance by taking funds from

friends or family members. Normally, company needs to pay less interest to

its friends and family members.

External sources of finance

Issue of shares In order to meet its long term requirement of funds, company can raise its

funds by issuing equity shares to the general public (Brigham and Daves,

2012).

Bank loan It is the method through which company can borrow funds from the bank by

paying interest to them. This method can be used by company to meet its

short-term and Long-term requirement of finance.

Hire purchase This is the method through which company can use the asset or property

without purchasing it at that particular time.

1.2 Implication of sources of finance

Sources Legal aspects dilution bankruptcy

Sale of assets At the time of selling

assets, Sweet Menu

restaurant is required

to follow the legal

procedure (Brigham

and Ehrhardt, 2013).

Once, the legal

procedure for selling

assets is completed

then, at the particular

time, ownership

changes.

If situation of

bankruptcy arises, then

creditors can sell out

the assets of company

in order to recover

their money.

Retained profit No legal procedure is

needs to be followed

by company at the

Ownership does not

change. It remains

with the company

If retained profit is

available, then in that

case, condition of

3

time of using retained

profit.

only. bankruptcy cannot

arise.

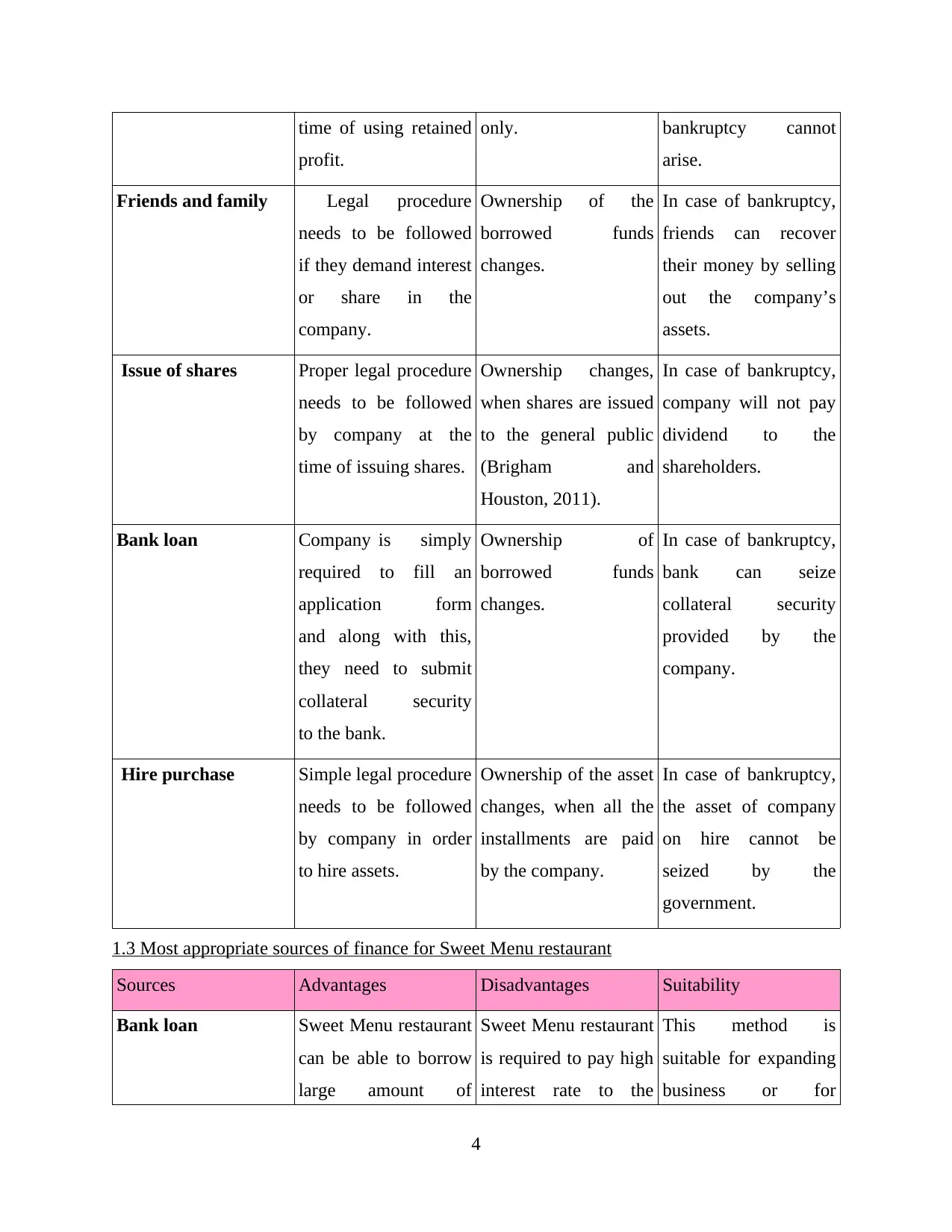

Friends and family Legal procedure

needs to be followed

if they demand interest

or share in the

company.

Ownership of the

borrowed funds

changes.

In case of bankruptcy,

friends can recover

their money by selling

out the company’s

assets.

Issue of shares Proper legal procedure

needs to be followed

by company at the

time of issuing shares.

Ownership changes,

when shares are issued

to the general public

(Brigham and

Houston, 2011).

In case of bankruptcy,

company will not pay

dividend to the

shareholders.

Bank loan Company is simply

required to fill an

application form

and along with this,

they need to submit

collateral security

to the bank.

Ownership of

borrowed funds

changes.

In case of bankruptcy,

bank can seize

collateral security

provided by the

company.

Hire purchase Simple legal procedure

needs to be followed

by company in order

to hire assets.

Ownership of the asset

changes, when all the

installments are paid

by the company.

In case of bankruptcy,

the asset of company

on hire cannot be

seized by the

government.

1.3 Most appropriate sources of finance for Sweet Menu restaurant

Sources Advantages Disadvantages Suitability

Bank loan Sweet Menu restaurant

can be able to borrow

large amount of

Sweet Menu restaurant

is required to pay high

interest rate to the

This method is

suitable for expanding

business or for

4

profit.

only. bankruptcy cannot

arise.

Friends and family Legal procedure

needs to be followed

if they demand interest

or share in the

company.

Ownership of the

borrowed funds

changes.

In case of bankruptcy,

friends can recover

their money by selling

out the company’s

assets.

Issue of shares Proper legal procedure

needs to be followed

by company at the

time of issuing shares.

Ownership changes,

when shares are issued

to the general public

(Brigham and

Houston, 2011).

In case of bankruptcy,

company will not pay

dividend to the

shareholders.

Bank loan Company is simply

required to fill an

application form

and along with this,

they need to submit

collateral security

to the bank.

Ownership of

borrowed funds

changes.

In case of bankruptcy,

bank can seize

collateral security

provided by the

company.

Hire purchase Simple legal procedure

needs to be followed

by company in order

to hire assets.

Ownership of the asset

changes, when all the

installments are paid

by the company.

In case of bankruptcy,

the asset of company

on hire cannot be

seized by the

government.

1.3 Most appropriate sources of finance for Sweet Menu restaurant

Sources Advantages Disadvantages Suitability

Bank loan Sweet Menu restaurant

can be able to borrow

large amount of

Sweet Menu restaurant

is required to pay high

interest rate to the

This method is

suitable for expanding

business or for

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

money in order to

meet its short or long

term requirement.

bank (Chandra, 2011).

Along with this, they

are also required to

submit collateral

security.

purchasing any asset.

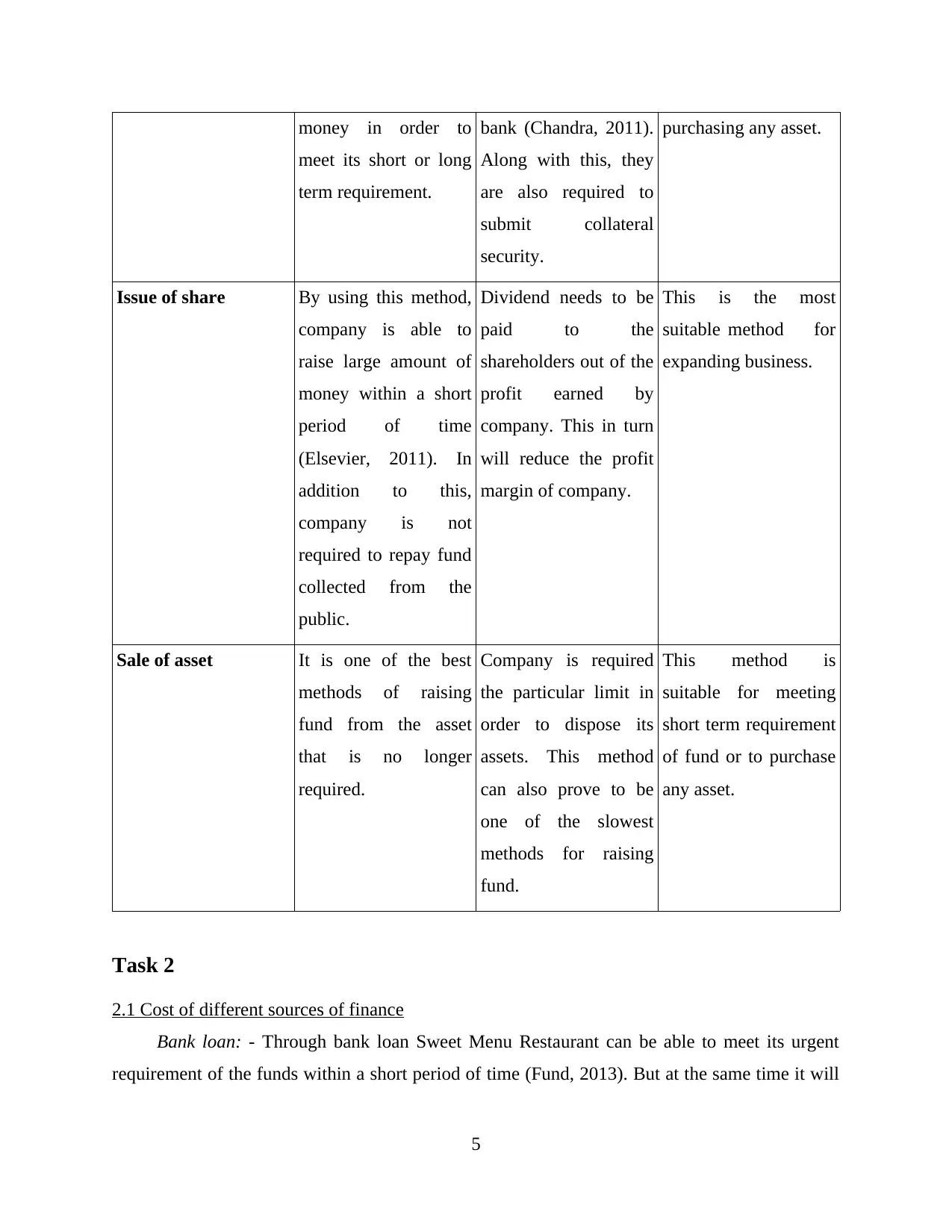

Issue of share By using this method,

company is able to

raise large amount of

money within a short

period of time

(Elsevier, 2011). In

addition to this,

company is not

required to repay fund

collected from the

public.

Dividend needs to be

paid to the

shareholders out of the

profit earned by

company. This in turn

will reduce the profit

margin of company.

This is the most

suitable method for

expanding business.

Sale of asset It is one of the best

methods of raising

fund from the asset

that is no longer

required.

Company is required

the particular limit in

order to dispose its

assets. This method

can also prove to be

one of the slowest

methods for raising

fund.

This method is

suitable for meeting

short term requirement

of fund or to purchase

any asset.

Task 2

2.1 Cost of different sources of finance

Bank loan: - Through bank loan Sweet Menu Restaurant can be able to meet its urgent

requirement of the funds within a short period of time (Fund, 2013). But at the same time it will

5

meet its short or long

term requirement.

bank (Chandra, 2011).

Along with this, they

are also required to

submit collateral

security.

purchasing any asset.

Issue of share By using this method,

company is able to

raise large amount of

money within a short

period of time

(Elsevier, 2011). In

addition to this,

company is not

required to repay fund

collected from the

public.

Dividend needs to be

paid to the

shareholders out of the

profit earned by

company. This in turn

will reduce the profit

margin of company.

This is the most

suitable method for

expanding business.

Sale of asset It is one of the best

methods of raising

fund from the asset

that is no longer

required.

Company is required

the particular limit in

order to dispose its

assets. This method

can also prove to be

one of the slowest

methods for raising

fund.

This method is

suitable for meeting

short term requirement

of fund or to purchase

any asset.

Task 2

2.1 Cost of different sources of finance

Bank loan: - Through bank loan Sweet Menu Restaurant can be able to meet its urgent

requirement of the funds within a short period of time (Fund, 2013). But at the same time it will

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase the cost of the company. Sweet Menu restaurant is required to pay high rate of interest

which in turn reduces the profit margin of the company.

Issue of shares: - By issuing shares company can be able to meet its long term

requirement of funds within the short period of time. This is one of the safest methods of raising

finance. But at the same time it increases the cost of the company. Company need to bear

various expenses at the time of issuing the shares. In addition to this company is also required

to pay dividend to the shareholders out of the profit earned.

Sale of asset: - By using this method company will be able to expand its business by

selling out the old and obsolescent assets that are of no use (Healy and Palepu, 2012). But at the

same it will increase the cost of the company. Assets of the company will reduce as compared to

its liability. Sweet Menu restaurant can also suffer loss if they are not able to sale out the assets

at its deprecated value.

2.2 Importance of financial planning to Sweet Menu restaurant

Maintain the balance between inflow and outflow of cash: - Through final planning Sweet

Menu restaurant will be able to maintain the balance between inflow and outflow of the cash that

take place within and outside the organization.

Able to properly distribute the fund in each and every department as per the requirement: -

Planning of all the financial activity in advance will assist the Sweet Menu restaurant to properly

distribute the finance in each and every department as per the requirement (Income and Sheet,

2012). This in turn will also aid the company to overcome the problem of surplus or deficit in

terms of money.

Reduce the condition of uncertainty: - Financial planning will help the company to avoid or

reduce the condition of uncertainty. The condition of uncertainty can arise due to sudden

change in business environment.

Utilization of available resources to the full extent: - Planning of all the financial activities

in advance will aid the Sweet Menu restaurant to properly allocate the resources available to the

full extent. Proper allocation will also aid the company to reduce the wastage of resources.

To manage income available with the company more effectively:- Through final planning

Sweet Menu restaurant will be able to manage the income available with them in proper and

effective manner in order to achieve the desired target (Kaplan and Atkinson, 2015).

6

which in turn reduces the profit margin of the company.

Issue of shares: - By issuing shares company can be able to meet its long term

requirement of funds within the short period of time. This is one of the safest methods of raising

finance. But at the same time it increases the cost of the company. Company need to bear

various expenses at the time of issuing the shares. In addition to this company is also required

to pay dividend to the shareholders out of the profit earned.

Sale of asset: - By using this method company will be able to expand its business by

selling out the old and obsolescent assets that are of no use (Healy and Palepu, 2012). But at the

same it will increase the cost of the company. Assets of the company will reduce as compared to

its liability. Sweet Menu restaurant can also suffer loss if they are not able to sale out the assets

at its deprecated value.

2.2 Importance of financial planning to Sweet Menu restaurant

Maintain the balance between inflow and outflow of cash: - Through final planning Sweet

Menu restaurant will be able to maintain the balance between inflow and outflow of the cash that

take place within and outside the organization.

Able to properly distribute the fund in each and every department as per the requirement: -

Planning of all the financial activity in advance will assist the Sweet Menu restaurant to properly

distribute the finance in each and every department as per the requirement (Income and Sheet,

2012). This in turn will also aid the company to overcome the problem of surplus or deficit in

terms of money.

Reduce the condition of uncertainty: - Financial planning will help the company to avoid or

reduce the condition of uncertainty. The condition of uncertainty can arise due to sudden

change in business environment.

Utilization of available resources to the full extent: - Planning of all the financial activities

in advance will aid the Sweet Menu restaurant to properly allocate the resources available to the

full extent. Proper allocation will also aid the company to reduce the wastage of resources.

To manage income available with the company more effectively:- Through final planning

Sweet Menu restaurant will be able to manage the income available with them in proper and

effective manner in order to achieve the desired target (Kaplan and Atkinson, 2015).

6

Avoid the condition of shocks and surprises: - Planning of all the final activities in advance

will assist the company to avoid the condition of shocks and surprises that can occur due to

sudden change in internal and external environmental condition.

2.3 Information needed by decision maker of Sweet Menu restaurant

There are many types of information which are needed by decision maker of the

company. Thus, in order to collect all the required information stakeholders/decision maker

prefers financial statements and audit report of the company.

Investors: - Investors are the one who invest their personal saving into the company.

They want that company should generate more profitability. This in turn will aid them to gain

more return on investment. These investors want the financial statements of the company in

order to find out the profit earned by the company at the end of every financial year (McKinney,

2015).

Employees: - They are the one who works for the betterment of the company. These

employees simply want to see the income statement in order to find out whether the company is

in a position to pay them salary. In addition to this they want see that company is paying them

fair salary or not.

Manager: - Managers are the one who prepare various strategies in order to achieve the

desire objectives (Sabău, 2013). They want financial statement and audit report of the company

to form the various strategies with an aim to beat the competitor and to achieve the desired

objective.

Government: - Government is the one which works for the welfare of the society. They

prefer to see the financial statements and audit report of the company in order to conclude

whether the company financial position is good or not (Shahrokhi, 2008). In addition to this they

also prefer these statements in order to calculate the amount of tax need to be paid by the

company.

Customer: - Customers are the one who want value for their money. They do not require

any type of financial statements. They simply want high quality product at an affordable price.

2.4 Impact of sources of finance on financial statements

Sale of assets: - Entry of sale of assets will be made on the asset side of the balance sheet.

It will be deducted from the fixed assets. Amount of cash will increase due to sale of the assets.

7

will assist the company to avoid the condition of shocks and surprises that can occur due to

sudden change in internal and external environmental condition.

2.3 Information needed by decision maker of Sweet Menu restaurant

There are many types of information which are needed by decision maker of the

company. Thus, in order to collect all the required information stakeholders/decision maker

prefers financial statements and audit report of the company.

Investors: - Investors are the one who invest their personal saving into the company.

They want that company should generate more profitability. This in turn will aid them to gain

more return on investment. These investors want the financial statements of the company in

order to find out the profit earned by the company at the end of every financial year (McKinney,

2015).

Employees: - They are the one who works for the betterment of the company. These

employees simply want to see the income statement in order to find out whether the company is

in a position to pay them salary. In addition to this they want see that company is paying them

fair salary or not.

Manager: - Managers are the one who prepare various strategies in order to achieve the

desire objectives (Sabău, 2013). They want financial statement and audit report of the company

to form the various strategies with an aim to beat the competitor and to achieve the desired

objective.

Government: - Government is the one which works for the welfare of the society. They

prefer to see the financial statements and audit report of the company in order to conclude

whether the company financial position is good or not (Shahrokhi, 2008). In addition to this they

also prefer these statements in order to calculate the amount of tax need to be paid by the

company.

Customer: - Customers are the one who want value for their money. They do not require

any type of financial statements. They simply want high quality product at an affordable price.

2.4 Impact of sources of finance on financial statements

Sale of assets: - Entry of sale of assets will be made on the asset side of the balance sheet.

It will be deducted from the fixed assets. Amount of cash will increase due to sale of the assets.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

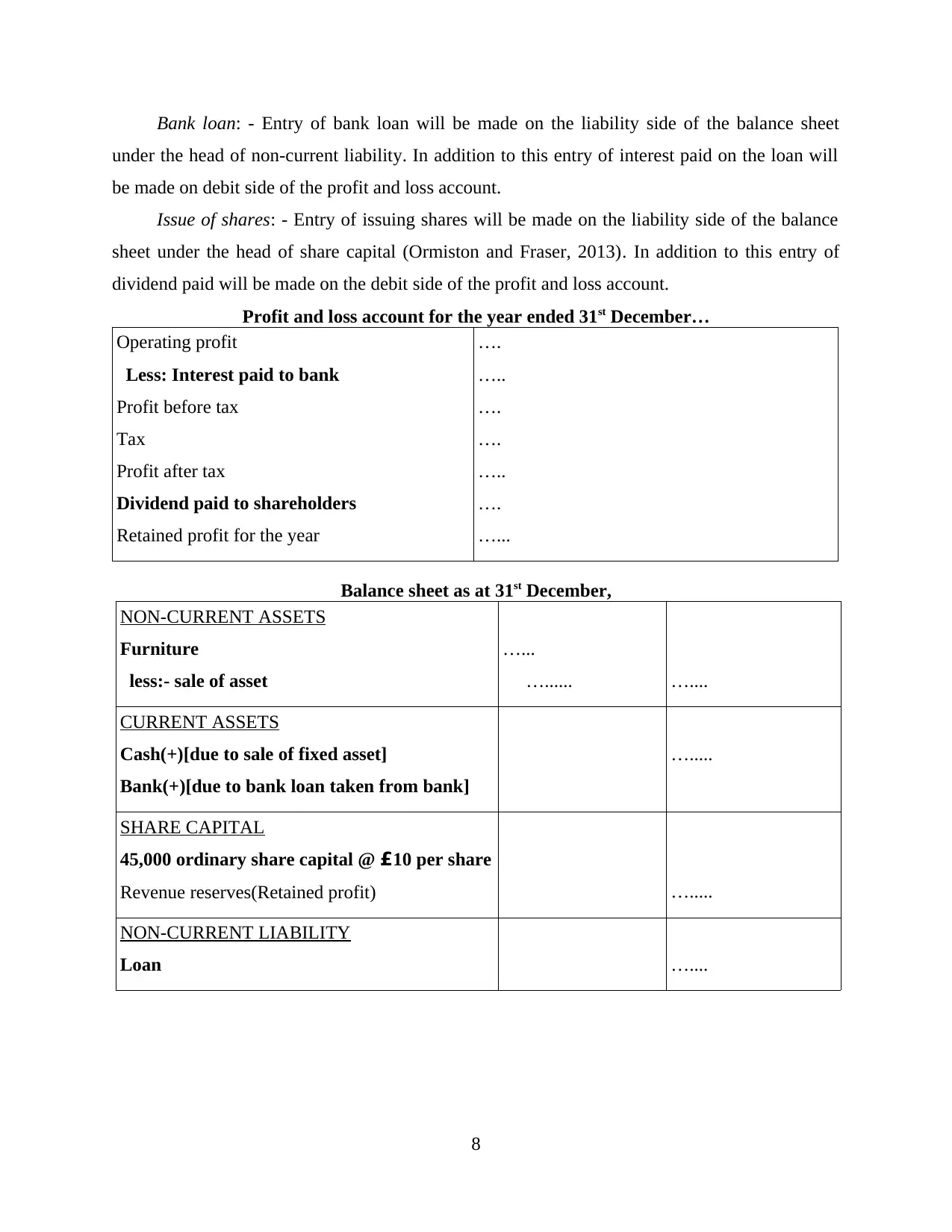

Bank loan: - Entry of bank loan will be made on the liability side of the balance sheet

under the head of non-current liability. In addition to this entry of interest paid on the loan will

be made on debit side of the profit and loss account.

Issue of shares: - Entry of issuing shares will be made on the liability side of the balance

sheet under the head of share capital (Ormiston and Fraser, 2013). In addition to this entry of

dividend paid will be made on the debit side of the profit and loss account.

Profit and loss account for the year ended 31st December…

Operating profit

Less: Interest paid to bank

Profit before tax

Tax

Profit after tax

Dividend paid to shareholders

Retained profit for the year

….

…..

….

….

…..

….

…...

Balance sheet as at 31st December,

NON-CURRENT ASSETS

Furniture

less:- sale of asset

…...

…...... …....

CURRENT ASSETS

Cash(+)[due to sale of fixed asset]

Bank(+)[due to bank loan taken from bank]

….....

SHARE CAPITAL

45,000 ordinary share capital @ £10 per share

Revenue reserves(Retained profit) ….....

NON-CURRENT LIABILITY

Loan …....

8

under the head of non-current liability. In addition to this entry of interest paid on the loan will

be made on debit side of the profit and loss account.

Issue of shares: - Entry of issuing shares will be made on the liability side of the balance

sheet under the head of share capital (Ormiston and Fraser, 2013). In addition to this entry of

dividend paid will be made on the debit side of the profit and loss account.

Profit and loss account for the year ended 31st December…

Operating profit

Less: Interest paid to bank

Profit before tax

Tax

Profit after tax

Dividend paid to shareholders

Retained profit for the year

….

…..

….

….

…..

….

…...

Balance sheet as at 31st December,

NON-CURRENT ASSETS

Furniture

less:- sale of asset

…...

…...... …....

CURRENT ASSETS

Cash(+)[due to sale of fixed asset]

Bank(+)[due to bank loan taken from bank]

….....

SHARE CAPITAL

45,000 ordinary share capital @ £10 per share

Revenue reserves(Retained profit) ….....

NON-CURRENT LIABILITY

Loan …....

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

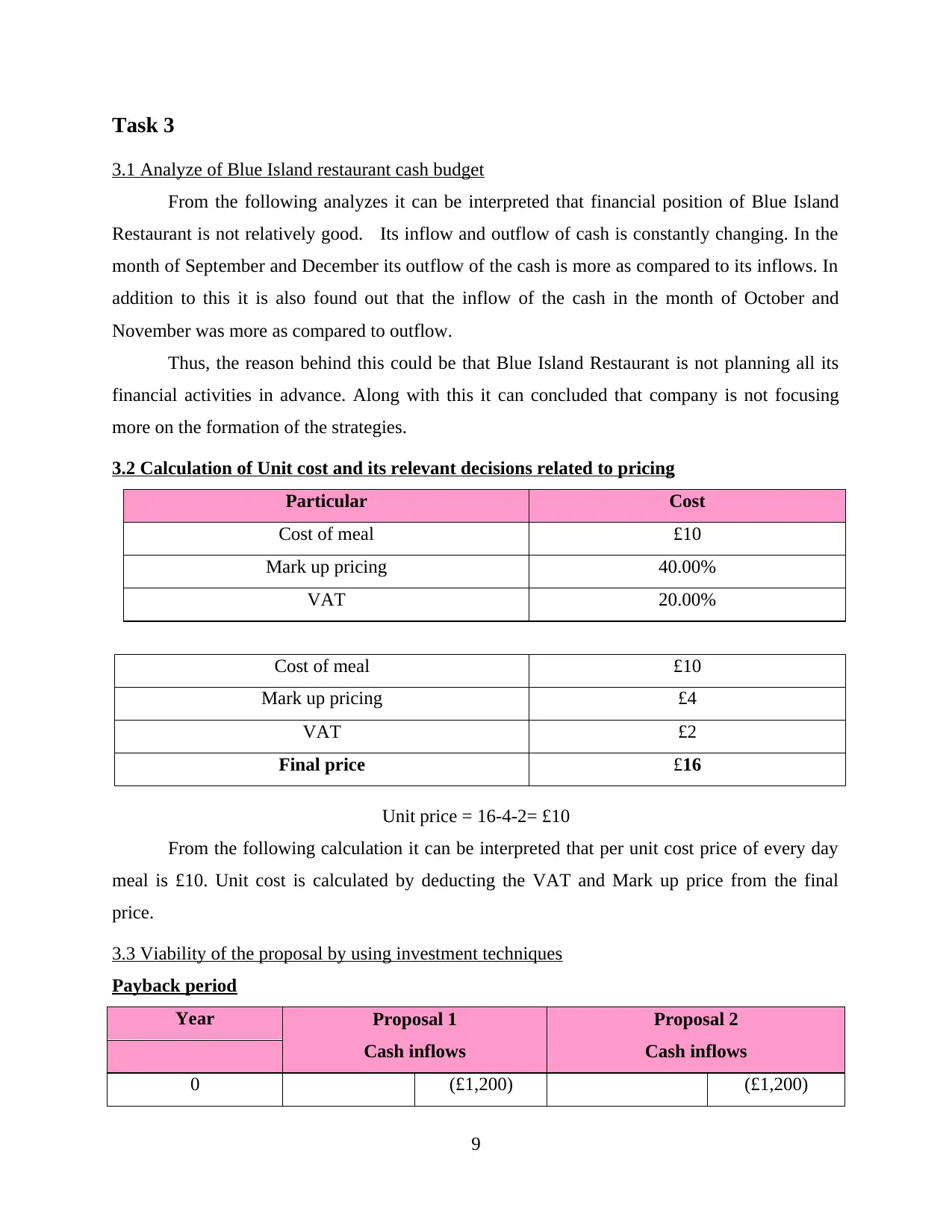

3.1 Analyze of Blue Island restaurant cash budget

From the following analyzes it can be interpreted that financial position of Blue Island

Restaurant is not relatively good. Its inflow and outflow of cash is constantly changing. In the

month of September and December its outflow of the cash is more as compared to its inflows. In

addition to this it is also found out that the inflow of the cash in the month of October and

November was more as compared to outflow.

Thus, the reason behind this could be that Blue Island Restaurant is not planning all its

financial activities in advance. Along with this it can concluded that company is not focusing

more on the formation of the strategies.

3.2 Calculation of Unit cost and its relevant decisions related to pricing

Particular Cost

Cost of meal £10

Mark up pricing 40.00%

VAT 20.00%

Cost of meal £10

Mark up pricing £4

VAT £2

Final price £16

Unit price = 16-4-2= £10

From the following calculation it can be interpreted that per unit cost price of every day

meal is £10. Unit cost is calculated by deducting the VAT and Mark up price from the final

price.

3.3 Viability of the proposal by using investment techniques

Payback period

Year Proposal 1

Cash inflows

Proposal 2

Cash inflows

0 (£1,200) (£1,200)

9

3.1 Analyze of Blue Island restaurant cash budget

From the following analyzes it can be interpreted that financial position of Blue Island

Restaurant is not relatively good. Its inflow and outflow of cash is constantly changing. In the

month of September and December its outflow of the cash is more as compared to its inflows. In

addition to this it is also found out that the inflow of the cash in the month of October and

November was more as compared to outflow.

Thus, the reason behind this could be that Blue Island Restaurant is not planning all its

financial activities in advance. Along with this it can concluded that company is not focusing

more on the formation of the strategies.

3.2 Calculation of Unit cost and its relevant decisions related to pricing

Particular Cost

Cost of meal £10

Mark up pricing 40.00%

VAT 20.00%

Cost of meal £10

Mark up pricing £4

VAT £2

Final price £16

Unit price = 16-4-2= £10

From the following calculation it can be interpreted that per unit cost price of every day

meal is £10. Unit cost is calculated by deducting the VAT and Mark up price from the final

price.

3.3 Viability of the proposal by using investment techniques

Payback period

Year Proposal 1

Cash inflows

Proposal 2

Cash inflows

0 (£1,200) (£1,200)

9

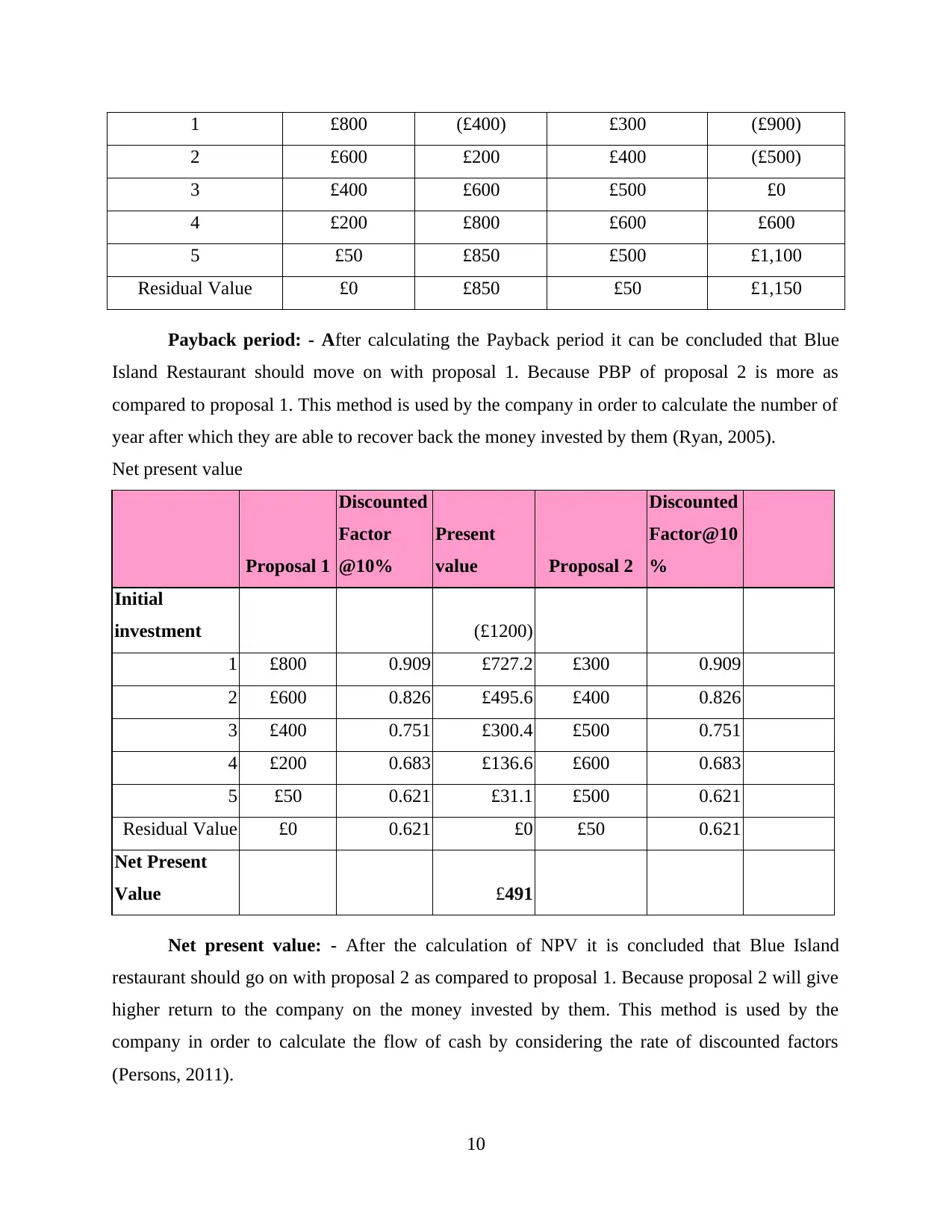

1 £800 (£400) £300 (£900)

2 £600 £200 £400 (£500)

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual Value £0 £850 £50 £1,150

Payback period: - After calculating the Payback period it can be concluded that Blue

Island Restaurant should move on with proposal 1. Because PBP of proposal 2 is more as

compared to proposal 1. This method is used by the company in order to calculate the number of

year after which they are able to recover back the money invested by them (Ryan, 2005).

Net present value

Proposal 1

Discounted

Factor

@10%

Present

value Proposal 2

Discounted

Factor@10

%

Initial

investment (£1200)

1 £800 0.909 £727.2 £300 0.909

2 £600 0.826 £495.6 £400 0.826

3 £400 0.751 £300.4 £500 0.751

4 £200 0.683 £136.6 £600 0.683

5 £50 0.621 £31.1 £500 0.621

Residual Value £0 0.621 £0 £50 0.621

Net Present

Value £491

Net present value: - After the calculation of NPV it is concluded that Blue Island

restaurant should go on with proposal 2 as compared to proposal 1. Because proposal 2 will give

higher return to the company on the money invested by them. This method is used by the

company in order to calculate the flow of cash by considering the rate of discounted factors

(Persons, 2011).

10

2 £600 £200 £400 (£500)

3 £400 £600 £500 £0

4 £200 £800 £600 £600

5 £50 £850 £500 £1,100

Residual Value £0 £850 £50 £1,150

Payback period: - After calculating the Payback period it can be concluded that Blue

Island Restaurant should move on with proposal 1. Because PBP of proposal 2 is more as

compared to proposal 1. This method is used by the company in order to calculate the number of

year after which they are able to recover back the money invested by them (Ryan, 2005).

Net present value

Proposal 1

Discounted

Factor

@10%

Present

value Proposal 2

Discounted

Factor@10

%

Initial

investment (£1200)

1 £800 0.909 £727.2 £300 0.909

2 £600 0.826 £495.6 £400 0.826

3 £400 0.751 £300.4 £500 0.751

4 £200 0.683 £136.6 £600 0.683

5 £50 0.621 £31.1 £500 0.621

Residual Value £0 0.621 £0 £50 0.621

Net Present

Value £491

Net present value: - After the calculation of NPV it is concluded that Blue Island

restaurant should go on with proposal 2 as compared to proposal 1. Because proposal 2 will give

higher return to the company on the money invested by them. This method is used by the

company in order to calculate the flow of cash by considering the rate of discounted factors

(Persons, 2011).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.