Financial Decisions and Resources for Sweet Menu Restaurant Expansion

VerifiedAdded on 2020/01/28

|19

|6191

|73

Report

AI Summary

This report provides a comprehensive financial analysis for Sweet Menu Restaurant, focusing on its expansion plans. It identifies and evaluates both internal (retained earnings, personal savings) and external (issuing shares, borrowed funds, lease, venture capital) financial sources, assessing their implications and suitability. The report recommends a combination of retained earnings and loan capital as the most appropriate funding sources for the restaurant's expansion, considering factors such as cost, control, and market position. It also delves into the cost of finance, the importance of financial planning, information needs of different decision-makers, and the impact of finance sources on financial statements. Furthermore, the report examines budgeting, unit cost calculations, pricing decisions, and investment appraisal techniques to assess project viability. Finally, it addresses the production and interpretation of financial statements using ratio analysis.

MANAGING

FINANCIAL

RESOURCES AND

DECISIONS

FINANCIAL

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

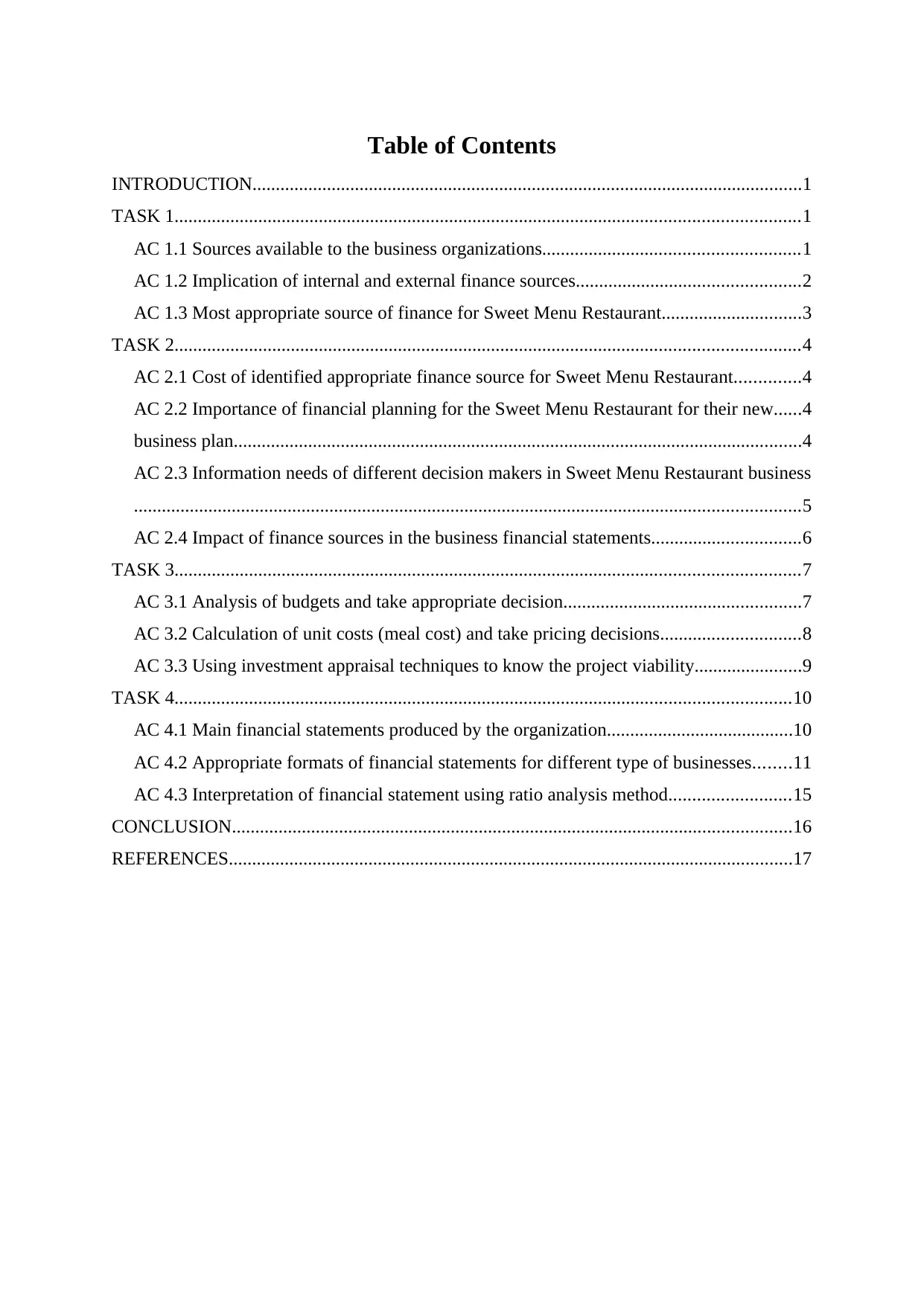

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Sources available to the business organizations.......................................................1

AC 1.2 Implication of internal and external finance sources................................................2

AC 1.3 Most appropriate source of finance for Sweet Menu Restaurant..............................3

TASK 2......................................................................................................................................4

AC 2.1 Cost of identified appropriate finance source for Sweet Menu Restaurant..............4

AC 2.2 Importance of financial planning for the Sweet Menu Restaurant for their new......4

business plan..........................................................................................................................4

AC 2.3 Information needs of different decision makers in Sweet Menu Restaurant business

...............................................................................................................................................5

AC 2.4 Impact of finance sources in the business financial statements................................6

TASK 3......................................................................................................................................7

AC 3.1 Analysis of budgets and take appropriate decision...................................................7

AC 3.2 Calculation of unit costs (meal cost) and take pricing decisions..............................8

AC 3.3 Using investment appraisal techniques to know the project viability.......................9

TASK 4....................................................................................................................................10

AC 4.1 Main financial statements produced by the organization........................................10

AC 4.2 Appropriate formats of financial statements for different type of businesses........11

AC 4.3 Interpretation of financial statement using ratio analysis method..........................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Sources available to the business organizations.......................................................1

AC 1.2 Implication of internal and external finance sources................................................2

AC 1.3 Most appropriate source of finance for Sweet Menu Restaurant..............................3

TASK 2......................................................................................................................................4

AC 2.1 Cost of identified appropriate finance source for Sweet Menu Restaurant..............4

AC 2.2 Importance of financial planning for the Sweet Menu Restaurant for their new......4

business plan..........................................................................................................................4

AC 2.3 Information needs of different decision makers in Sweet Menu Restaurant business

...............................................................................................................................................5

AC 2.4 Impact of finance sources in the business financial statements................................6

TASK 3......................................................................................................................................7

AC 3.1 Analysis of budgets and take appropriate decision...................................................7

AC 3.2 Calculation of unit costs (meal cost) and take pricing decisions..............................8

AC 3.3 Using investment appraisal techniques to know the project viability.......................9

TASK 4....................................................................................................................................10

AC 4.1 Main financial statements produced by the organization........................................10

AC 4.2 Appropriate formats of financial statements for different type of businesses........11

AC 4.3 Interpretation of financial statement using ratio analysis method..........................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

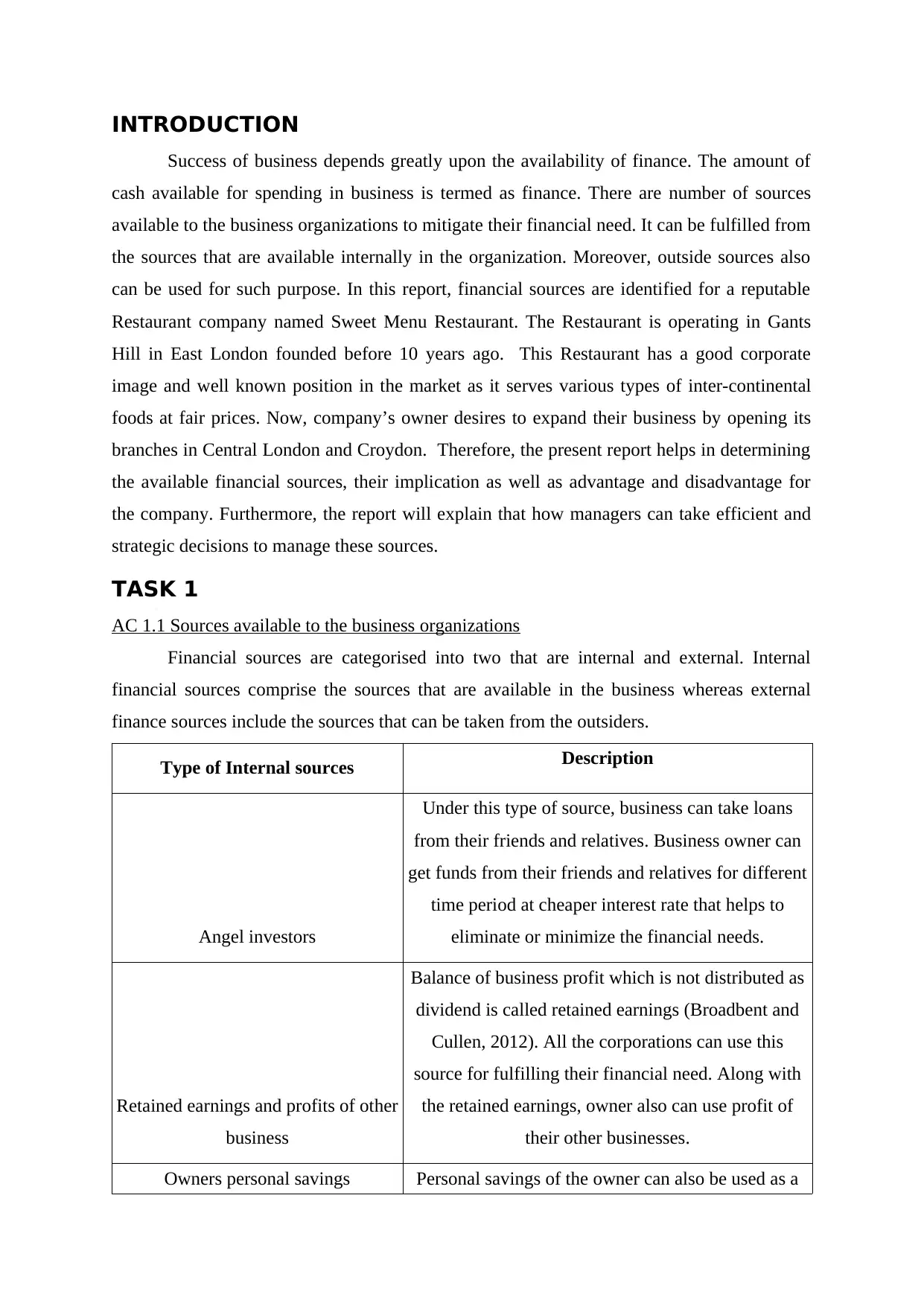

INTRODUCTION

Success of business depends greatly upon the availability of finance. The amount of

cash available for spending in business is termed as finance. There are number of sources

available to the business organizations to mitigate their financial need. It can be fulfilled from

the sources that are available internally in the organization. Moreover, outside sources also

can be used for such purpose. In this report, financial sources are identified for a reputable

Restaurant company named Sweet Menu Restaurant. The Restaurant is operating in Gants

Hill in East London founded before 10 years ago. This Restaurant has a good corporate

image and well known position in the market as it serves various types of inter-continental

foods at fair prices. Now, company’s owner desires to expand their business by opening its

branches in Central London and Croydon. Therefore, the present report helps in determining

the available financial sources, their implication as well as advantage and disadvantage for

the company. Furthermore, the report will explain that how managers can take efficient and

strategic decisions to manage these sources.

TASK 1

AC 1.1 Sources available to the business organizations

Financial sources are categorised into two that are internal and external. Internal

financial sources comprise the sources that are available in the business whereas external

finance sources include the sources that can be taken from the outsiders.

Type of Internal sources Description

Angel investors

Under this type of source, business can take loans

from their friends and relatives. Business owner can

get funds from their friends and relatives for different

time period at cheaper interest rate that helps to

eliminate or minimize the financial needs.

Retained earnings and profits of other

business

Balance of business profit which is not distributed as

dividend is called retained earnings (Broadbent and

Cullen, 2012). All the corporations can use this

source for fulfilling their financial need. Along with

the retained earnings, owner also can use profit of

their other businesses.

Owners personal savings Personal savings of the owner can also be used as a

Success of business depends greatly upon the availability of finance. The amount of

cash available for spending in business is termed as finance. There are number of sources

available to the business organizations to mitigate their financial need. It can be fulfilled from

the sources that are available internally in the organization. Moreover, outside sources also

can be used for such purpose. In this report, financial sources are identified for a reputable

Restaurant company named Sweet Menu Restaurant. The Restaurant is operating in Gants

Hill in East London founded before 10 years ago. This Restaurant has a good corporate

image and well known position in the market as it serves various types of inter-continental

foods at fair prices. Now, company’s owner desires to expand their business by opening its

branches in Central London and Croydon. Therefore, the present report helps in determining

the available financial sources, their implication as well as advantage and disadvantage for

the company. Furthermore, the report will explain that how managers can take efficient and

strategic decisions to manage these sources.

TASK 1

AC 1.1 Sources available to the business organizations

Financial sources are categorised into two that are internal and external. Internal

financial sources comprise the sources that are available in the business whereas external

finance sources include the sources that can be taken from the outsiders.

Type of Internal sources Description

Angel investors

Under this type of source, business can take loans

from their friends and relatives. Business owner can

get funds from their friends and relatives for different

time period at cheaper interest rate that helps to

eliminate or minimize the financial needs.

Retained earnings and profits of other

business

Balance of business profit which is not distributed as

dividend is called retained earnings (Broadbent and

Cullen, 2012). All the corporations can use this

source for fulfilling their financial need. Along with

the retained earnings, owner also can use profit of

their other businesses.

Owners personal savings Personal savings of the owner can also be used as a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial source for the expansion of business. It is

mostly used in case of newly business organization

when outside sources are available in very less

amount.

External sources Description

Issuing shares

There are two types of shares that are

ordinary and preference share capital.

Business can issue these shares in the market

in order to get funds easily.

Borrowed funds

Bank loan is the most common source of

borrowed funds (Thomas, 2001). Bank gives

loans to the corporate sectors for a specified

time period at an implied interest rate.

Lease

Under the lease financing, business can attain

rights for using assets without having

ownership (Brayley and McLean, 2001). It is

a contract between the asset’s owner and user

that provides rights for the use of assets at a

rental charges.

Venture capital

Venture capital can be acquired in the highly

potential growth earning businesses. Venture

capitalists are much interested to invest in

such businesses that can provide higher

returns to them and fulfil long term business

requirements.

AC 1.2 Implication of internal and external finance sources

Internal sources Implications External sources implications

Angel Investors: Borrowing loans from Issuing shares: On the amount of equity

mostly used in case of newly business organization

when outside sources are available in very less

amount.

External sources Description

Issuing shares

There are two types of shares that are

ordinary and preference share capital.

Business can issue these shares in the market

in order to get funds easily.

Borrowed funds

Bank loan is the most common source of

borrowed funds (Thomas, 2001). Bank gives

loans to the corporate sectors for a specified

time period at an implied interest rate.

Lease

Under the lease financing, business can attain

rights for using assets without having

ownership (Brayley and McLean, 2001). It is

a contract between the asset’s owner and user

that provides rights for the use of assets at a

rental charges.

Venture capital

Venture capital can be acquired in the highly

potential growth earning businesses. Venture

capitalists are much interested to invest in

such businesses that can provide higher

returns to them and fulfil long term business

requirements.

AC 1.2 Implication of internal and external finance sources

Internal sources Implications External sources implications

Angel Investors: Borrowing loans from Issuing shares: On the amount of equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

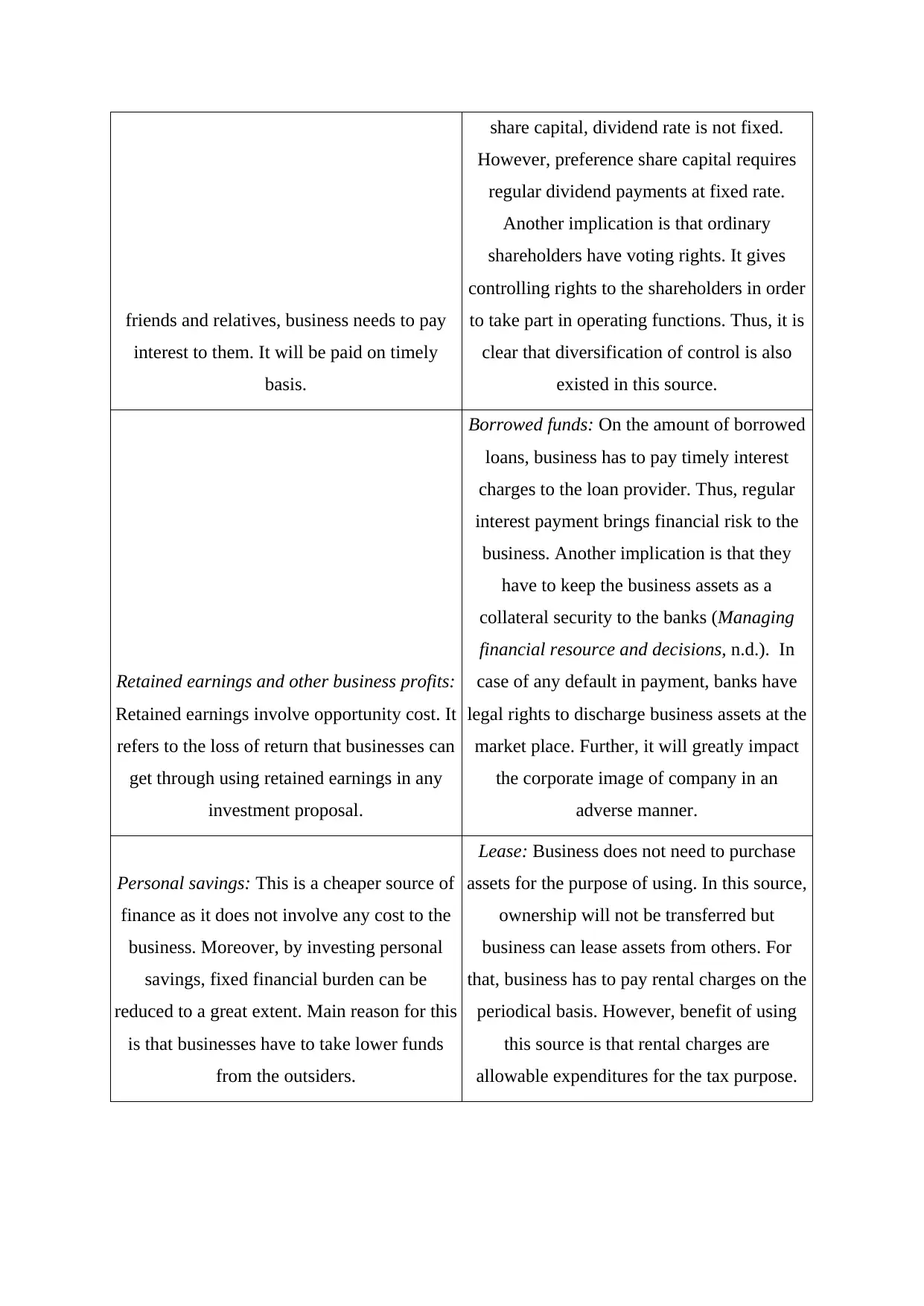

friends and relatives, business needs to pay

interest to them. It will be paid on timely

basis.

share capital, dividend rate is not fixed.

However, preference share capital requires

regular dividend payments at fixed rate.

Another implication is that ordinary

shareholders have voting rights. It gives

controlling rights to the shareholders in order

to take part in operating functions. Thus, it is

clear that diversification of control is also

existed in this source.

Retained earnings and other business profits:

Retained earnings involve opportunity cost. It

refers to the loss of return that businesses can

get through using retained earnings in any

investment proposal.

Borrowed funds: On the amount of borrowed

loans, business has to pay timely interest

charges to the loan provider. Thus, regular

interest payment brings financial risk to the

business. Another implication is that they

have to keep the business assets as a

collateral security to the banks (Managing

financial resource and decisions, n.d.). In

case of any default in payment, banks have

legal rights to discharge business assets at the

market place. Further, it will greatly impact

the corporate image of company in an

adverse manner.

Personal savings: This is a cheaper source of

finance as it does not involve any cost to the

business. Moreover, by investing personal

savings, fixed financial burden can be

reduced to a great extent. Main reason for this

is that businesses have to take lower funds

from the outsiders.

Lease: Business does not need to purchase

assets for the purpose of using. In this source,

ownership will not be transferred but

business can lease assets from others. For

that, business has to pay rental charges on the

periodical basis. However, benefit of using

this source is that rental charges are

allowable expenditures for the tax purpose.

interest to them. It will be paid on timely

basis.

share capital, dividend rate is not fixed.

However, preference share capital requires

regular dividend payments at fixed rate.

Another implication is that ordinary

shareholders have voting rights. It gives

controlling rights to the shareholders in order

to take part in operating functions. Thus, it is

clear that diversification of control is also

existed in this source.

Retained earnings and other business profits:

Retained earnings involve opportunity cost. It

refers to the loss of return that businesses can

get through using retained earnings in any

investment proposal.

Borrowed funds: On the amount of borrowed

loans, business has to pay timely interest

charges to the loan provider. Thus, regular

interest payment brings financial risk to the

business. Another implication is that they

have to keep the business assets as a

collateral security to the banks (Managing

financial resource and decisions, n.d.). In

case of any default in payment, banks have

legal rights to discharge business assets at the

market place. Further, it will greatly impact

the corporate image of company in an

adverse manner.

Personal savings: This is a cheaper source of

finance as it does not involve any cost to the

business. Moreover, by investing personal

savings, fixed financial burden can be

reduced to a great extent. Main reason for this

is that businesses have to take lower funds

from the outsiders.

Lease: Business does not need to purchase

assets for the purpose of using. In this source,

ownership will not be transferred but

business can lease assets from others. For

that, business has to pay rental charges on the

periodical basis. However, benefit of using

this source is that rental charges are

allowable expenditures for the tax purpose.

AC 1.3 Most appropriate source of finance for Sweet Menu Restaurant

The given scenario stated that Sweet Menu Restaurant needs finance amounted to

300000£ and 500000£ for the business expansion. On the basis of above identified

implications, it can be said that under the internal sources, retained earnings and profits from

other businesses will be the best among them. The reason for such decision is that it does not

involve higher cost to the company. Further, these are the regular finance sources and

eliminate the immediate finance requirements also. However, if company receives funds from

the angel investors, then business will need to pay interest to them. On contrary, through

ploughing back of profits, firm can generate funds without any cost.

Moreover, Restaurant has a good market position and well known in the market. Loan

capital will be the most appropriate finance source under the external sources. The reason for

such decision is that banks and other financial institutions provide loans on the basis of their

credit worthiness. Therefore, loans will be available easily to the Sweet Menu Restaurant.

Moreover, it fulfils the short term, medium term and long term finance requirements of

business. In addition to it, business has good reputation in the market thus, company is able to

bear fixed financial burden. Other benefits will be that control diversification can be

eliminated through using this finance source. Thus, it has become clear that both types of

sources are appropriate for Sweet Menu Restaurant for their expansion plans.

TASK 2

AC 2.1 Cost of identified appropriate finance source for Sweet Menu Restaurant

The cost of retained earnings and other business profits for Sweet Menu Restaurant

business is opportunity cost. It concerns with the loss of possible returns that the business can

receive by investing the profits in other businesses or in other available alternative investment

proposal. Moreover, higher rate of ploughing back of profits may create negative impacts to

the shareholders.

Furthermore, the amount of borrowed funds imposes cost of regular payment of

interest. The interest rate may be fixed or volatile also called fluctuating. Fixed rate imposed

fixed amount of financial burden to the company (Managing financial resource and

decisions, n.d.). However, in case of fluctuates interest rates, the financial liability cannot be

assessed in a correct manner. Another, the need of giving business assets as a collateral

security will be included in the cost. Further, in case of having business loss it will affects the

business operations in a negative direction. In addition to it, at the time of maturity, Sweet

Menu Restaurant has to repay the loan amount.

The given scenario stated that Sweet Menu Restaurant needs finance amounted to

300000£ and 500000£ for the business expansion. On the basis of above identified

implications, it can be said that under the internal sources, retained earnings and profits from

other businesses will be the best among them. The reason for such decision is that it does not

involve higher cost to the company. Further, these are the regular finance sources and

eliminate the immediate finance requirements also. However, if company receives funds from

the angel investors, then business will need to pay interest to them. On contrary, through

ploughing back of profits, firm can generate funds without any cost.

Moreover, Restaurant has a good market position and well known in the market. Loan

capital will be the most appropriate finance source under the external sources. The reason for

such decision is that banks and other financial institutions provide loans on the basis of their

credit worthiness. Therefore, loans will be available easily to the Sweet Menu Restaurant.

Moreover, it fulfils the short term, medium term and long term finance requirements of

business. In addition to it, business has good reputation in the market thus, company is able to

bear fixed financial burden. Other benefits will be that control diversification can be

eliminated through using this finance source. Thus, it has become clear that both types of

sources are appropriate for Sweet Menu Restaurant for their expansion plans.

TASK 2

AC 2.1 Cost of identified appropriate finance source for Sweet Menu Restaurant

The cost of retained earnings and other business profits for Sweet Menu Restaurant

business is opportunity cost. It concerns with the loss of possible returns that the business can

receive by investing the profits in other businesses or in other available alternative investment

proposal. Moreover, higher rate of ploughing back of profits may create negative impacts to

the shareholders.

Furthermore, the amount of borrowed funds imposes cost of regular payment of

interest. The interest rate may be fixed or volatile also called fluctuating. Fixed rate imposed

fixed amount of financial burden to the company (Managing financial resource and

decisions, n.d.). However, in case of fluctuates interest rates, the financial liability cannot be

assessed in a correct manner. Another, the need of giving business assets as a collateral

security will be included in the cost. Further, in case of having business loss it will affects the

business operations in a negative direction. In addition to it, at the time of maturity, Sweet

Menu Restaurant has to repay the loan amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC 2.2 Importance of financial planning for the Sweet Menu Restaurant for their new

Business plan

Financial planning plays a vital a significant role in the organization success. It

mainly concerns with the process of setting business goals, targets and objectives and making

plans for go ahead (Dunn and Liang, 2015). Financial manager is greatly responsible for

making financial plans for the business. According to the scenario, Sweet Menu Restaurant

business is making plans for expanding their business operations. Therefore, the need of

making strategic financial plans will be arise for the business. It helps to acquire sufficient

amount of funds and manage it in a proper way so as to achieve financial goals.

Initially, the business financial planner has to determine the current available finance

sources that can be used for opening branches in Central London and Croydon. He has to

make strategic business plans to met their financial need at lower the cost factor. After that,

the financial manager has to forecast the future incomes and expenditures that can be occur

from the operational activities (Snider, 2015). It will be estimate for all the projects,

departments and the business divisions. The managers also identify the cash need and make

plans for raising the cash funds in business. Finance managers can prepare budget for that

purpose that combines all the probable incomes and expenditures for the future period. It

aims at running business operations successfully through controlling business cost and

maximize its incomes. This in turn, company will be able to generate higher the profits.

Furthermore, financial policy helps to manage the business funds in an effective and efficient

manner. Overall, the financial planning helps to achieve the predetermined financial targets

of business.

AC 2.3 Information needs of different decision makers in Sweet Menu Restaurant business

Different users need distinct information to take better decisions. In Context to Sweet

Menu Restaurant business, the information need of different decision makers are explained

below:

Decision makers Information need

Business managers In the present era, running business successfully is the

responsibility of all level of managers. It includes higher

level managers, middle level and lower level managers.

Higher level managers includes directors, CEO and CFO

take strategic business decisions for business development,

Business plan

Financial planning plays a vital a significant role in the organization success. It

mainly concerns with the process of setting business goals, targets and objectives and making

plans for go ahead (Dunn and Liang, 2015). Financial manager is greatly responsible for

making financial plans for the business. According to the scenario, Sweet Menu Restaurant

business is making plans for expanding their business operations. Therefore, the need of

making strategic financial plans will be arise for the business. It helps to acquire sufficient

amount of funds and manage it in a proper way so as to achieve financial goals.

Initially, the business financial planner has to determine the current available finance

sources that can be used for opening branches in Central London and Croydon. He has to

make strategic business plans to met their financial need at lower the cost factor. After that,

the financial manager has to forecast the future incomes and expenditures that can be occur

from the operational activities (Snider, 2015). It will be estimate for all the projects,

departments and the business divisions. The managers also identify the cash need and make

plans for raising the cash funds in business. Finance managers can prepare budget for that

purpose that combines all the probable incomes and expenditures for the future period. It

aims at running business operations successfully through controlling business cost and

maximize its incomes. This in turn, company will be able to generate higher the profits.

Furthermore, financial policy helps to manage the business funds in an effective and efficient

manner. Overall, the financial planning helps to achieve the predetermined financial targets

of business.

AC 2.3 Information needs of different decision makers in Sweet Menu Restaurant business

Different users need distinct information to take better decisions. In Context to Sweet

Menu Restaurant business, the information need of different decision makers are explained

below:

Decision makers Information need

Business managers In the present era, running business successfully is the

responsibility of all level of managers. It includes higher

level managers, middle level and lower level managers.

Higher level managers includes directors, CEO and CFO

take strategic business decisions for business development,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expansion, acquisition and introducing new product in the

market. Thus, both the financial as well as non financial

information are required by the mangers. Therefore, they

require information regarding all the incomes and

expenditures from the financial statements. Middle level

managers include regional managers, division managers and

store managers take medium term decisions. They take

decisions about strategic business unit, motivation,

performance improvement and enforcement of business

policies. The managers analyse and evaluate the business

expenses with the objectives of making effective control

(Slack, Chambers and Johnston, 2010). Further, budgeting

is also an important tool that used by managers to manage

the cash sources and its applications to ensure adequate cash

availability. Through managing the funds appropriately,

financial position and operational performance can be

improved in a great manner. Lower level managers includes

team leaders and supervisors take short term business

decisions such as day to day planning, production, ordering

goods and mitigate customer queries helps to improve

business performance

Creditors

They provide credit to the Sweet Menu Restaurant business,

therefore they analyse the business creditworthiness. They

analyse the financial statements and cash flow statements to

identify the liquid availability and cash earning capacity

(Zager and Zager, 2006.). Further, they analyse the

profitability statement to know the Restaurant business

profits.

Government Government have the objectives to increase their incomes

sources. Tax is the most important source of government

incomes that is calculated on earned business profits.

Therefore, government need information regarding business

market. Thus, both the financial as well as non financial

information are required by the mangers. Therefore, they

require information regarding all the incomes and

expenditures from the financial statements. Middle level

managers include regional managers, division managers and

store managers take medium term decisions. They take

decisions about strategic business unit, motivation,

performance improvement and enforcement of business

policies. The managers analyse and evaluate the business

expenses with the objectives of making effective control

(Slack, Chambers and Johnston, 2010). Further, budgeting

is also an important tool that used by managers to manage

the cash sources and its applications to ensure adequate cash

availability. Through managing the funds appropriately,

financial position and operational performance can be

improved in a great manner. Lower level managers includes

team leaders and supervisors take short term business

decisions such as day to day planning, production, ordering

goods and mitigate customer queries helps to improve

business performance

Creditors

They provide credit to the Sweet Menu Restaurant business,

therefore they analyse the business creditworthiness. They

analyse the financial statements and cash flow statements to

identify the liquid availability and cash earning capacity

(Zager and Zager, 2006.). Further, they analyse the

profitability statement to know the Restaurant business

profits.

Government Government have the objectives to increase their incomes

sources. Tax is the most important source of government

incomes that is calculated on earned business profits.

Therefore, government need information regarding business

profits to identify the tax obligations and in case of any

default, they impose penalties and other lawsuits.

Shareholders

Shareholders are the connect stakeholders of the business.

They influence business operation greatly need information

about share prices, earning per share, dividend incomes,

business performance in terms of business profits, ethical

awareness and fulfilling corporate social responsibility.

AC 2.4 Impact of finance sources in the business financial statements

All the business transactions show in the business financial statements. It includes

financial and operating transactions. Therefore, the type of financial sources that have been

used by Sweet Menu Restaurant business will impact the financial position statements.

However, the cost of financial statements impacts the profitability statement.

As stated earlier, most appropriate finance source for Sweet menu Restaurant are

retained earnings and borrowed funds. The cost of retained earnings that is opportunity cost

will not show in the profit and loss account. However, the amount of retained earnings used

will be shows in the statement of changes in retained earnings.

On contrary, cost of borrowed funds that is interest will be show in expenditure sides

of profit and loss account. Further, it will be deducted from the cash in the company's current

assets head. According to the given scenario, the cost will be show in profit and loss account

as interest charges however, under the current assets group; it will be subtracted from cash

and banks (Managing financial resource and decisions, n.d.). Another, the taken amount of

borrowed funds will be show in balance sheet. In context to Sweet Menu Restaurant business,

the amount will be show in liability side as long term loan under the noncurrent liabilities

head. Further, the amount will raise the business cash hence; it will be show in assets side

under the current assets group through increasing the cash and bank balance.

TASK 3

AC 3.1 Analysis of budgets and take appropriate decision

The present scenario stated the cash and inventory budget of Blue Island Restaurant

for the upcoming four months. The company is a great competitor of Sweet Menu Restaurant

default, they impose penalties and other lawsuits.

Shareholders

Shareholders are the connect stakeholders of the business.

They influence business operation greatly need information

about share prices, earning per share, dividend incomes,

business performance in terms of business profits, ethical

awareness and fulfilling corporate social responsibility.

AC 2.4 Impact of finance sources in the business financial statements

All the business transactions show in the business financial statements. It includes

financial and operating transactions. Therefore, the type of financial sources that have been

used by Sweet Menu Restaurant business will impact the financial position statements.

However, the cost of financial statements impacts the profitability statement.

As stated earlier, most appropriate finance source for Sweet menu Restaurant are

retained earnings and borrowed funds. The cost of retained earnings that is opportunity cost

will not show in the profit and loss account. However, the amount of retained earnings used

will be shows in the statement of changes in retained earnings.

On contrary, cost of borrowed funds that is interest will be show in expenditure sides

of profit and loss account. Further, it will be deducted from the cash in the company's current

assets head. According to the given scenario, the cost will be show in profit and loss account

as interest charges however, under the current assets group; it will be subtracted from cash

and banks (Managing financial resource and decisions, n.d.). Another, the taken amount of

borrowed funds will be show in balance sheet. In context to Sweet Menu Restaurant business,

the amount will be show in liability side as long term loan under the noncurrent liabilities

head. Further, the amount will raise the business cash hence; it will be show in assets side

under the current assets group through increasing the cash and bank balance.

TASK 3

AC 3.1 Analysis of budgets and take appropriate decision

The present scenario stated the cash and inventory budget of Blue Island Restaurant

for the upcoming four months. The company is a great competitor of Sweet Menu Restaurant

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

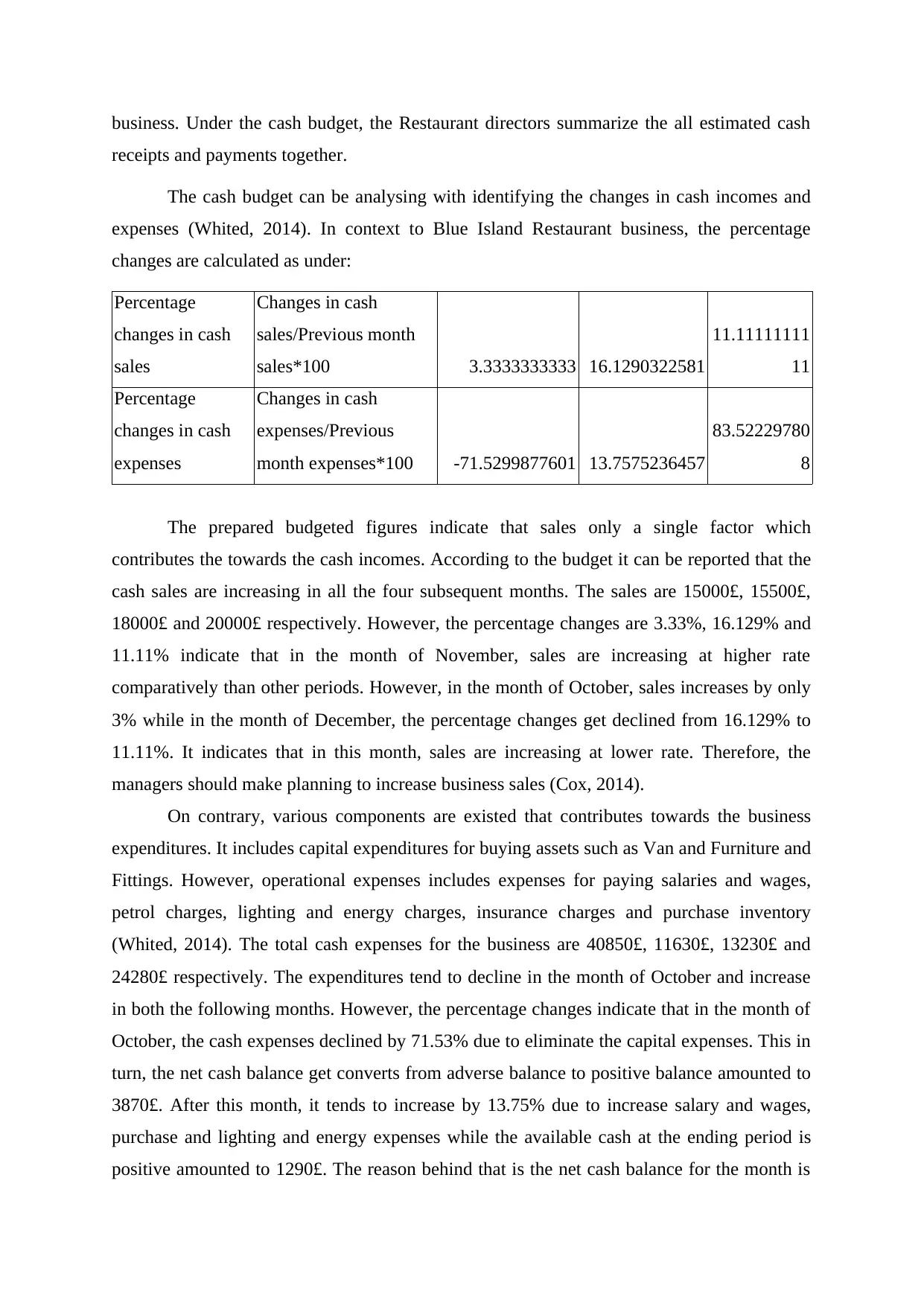

business. Under the cash budget, the Restaurant directors summarize the all estimated cash

receipts and payments together.

The cash budget can be analysing with identifying the changes in cash incomes and

expenses (Whited, 2014). In context to Blue Island Restaurant business, the percentage

changes are calculated as under:

Percentage

changes in cash

sales

Changes in cash

sales/Previous month

sales*100 3.3333333333 16.1290322581

11.11111111

11

Percentage

changes in cash

expenses

Changes in cash

expenses/Previous

month expenses*100 -71.5299877601 13.7575236457

83.52229780

8

The prepared budgeted figures indicate that sales only a single factor which

contributes the towards the cash incomes. According to the budget it can be reported that the

cash sales are increasing in all the four subsequent months. The sales are 15000£, 15500£,

18000£ and 20000£ respectively. However, the percentage changes are 3.33%, 16.129% and

11.11% indicate that in the month of November, sales are increasing at higher rate

comparatively than other periods. However, in the month of October, sales increases by only

3% while in the month of December, the percentage changes get declined from 16.129% to

11.11%. It indicates that in this month, sales are increasing at lower rate. Therefore, the

managers should make planning to increase business sales (Cox, 2014).

On contrary, various components are existed that contributes towards the business

expenditures. It includes capital expenditures for buying assets such as Van and Furniture and

Fittings. However, operational expenses includes expenses for paying salaries and wages,

petrol charges, lighting and energy charges, insurance charges and purchase inventory

(Whited, 2014). The total cash expenses for the business are 40850£, 11630£, 13230£ and

24280£ respectively. The expenditures tend to decline in the month of October and increase

in both the following months. However, the percentage changes indicate that in the month of

October, the cash expenses declined by 71.53% due to eliminate the capital expenses. This in

turn, the net cash balance get converts from adverse balance to positive balance amounted to

3870£. After this month, it tends to increase by 13.75% due to increase salary and wages,

purchase and lighting and energy expenses while the available cash at the ending period is

positive amounted to 1290£. The reason behind that is the net cash balance for the month is

receipts and payments together.

The cash budget can be analysing with identifying the changes in cash incomes and

expenses (Whited, 2014). In context to Blue Island Restaurant business, the percentage

changes are calculated as under:

Percentage

changes in cash

sales

Changes in cash

sales/Previous month

sales*100 3.3333333333 16.1290322581

11.11111111

11

Percentage

changes in cash

expenses

Changes in cash

expenses/Previous

month expenses*100 -71.5299877601 13.7575236457

83.52229780

8

The prepared budgeted figures indicate that sales only a single factor which

contributes the towards the cash incomes. According to the budget it can be reported that the

cash sales are increasing in all the four subsequent months. The sales are 15000£, 15500£,

18000£ and 20000£ respectively. However, the percentage changes are 3.33%, 16.129% and

11.11% indicate that in the month of November, sales are increasing at higher rate

comparatively than other periods. However, in the month of October, sales increases by only

3% while in the month of December, the percentage changes get declined from 16.129% to

11.11%. It indicates that in this month, sales are increasing at lower rate. Therefore, the

managers should make planning to increase business sales (Cox, 2014).

On contrary, various components are existed that contributes towards the business

expenditures. It includes capital expenditures for buying assets such as Van and Furniture and

Fittings. However, operational expenses includes expenses for paying salaries and wages,

petrol charges, lighting and energy charges, insurance charges and purchase inventory

(Whited, 2014). The total cash expenses for the business are 40850£, 11630£, 13230£ and

24280£ respectively. The expenditures tend to decline in the month of October and increase

in both the following months. However, the percentage changes indicate that in the month of

October, the cash expenses declined by 71.53% due to eliminate the capital expenses. This in

turn, the net cash balance get converts from adverse balance to positive balance amounted to

3870£. After this month, it tends to increase by 13.75% due to increase salary and wages,

purchase and lighting and energy expenses while the available cash at the ending period is

positive amounted to 1290£. The reason behind that is the net cash balance for the month is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

comparatively higher than cash availability at the ending month of October. Once again,

expenditures increases by 83.52% due to acquiring the fixed assets amounted to 10000£.

Another reason for such increases is increasing the operating expenses of salary and wages,

lighting and energy and purchasing inventory. This in turn, resulted in negative cash balance

and adverse cash availability at the month ending. On the basis of above identification, it can

be reported that the months in which capital expenditures will be occur lead to highly

increase in the cash expenses results in adverse availability of cash. Through implementing

an effective control tool, expenditures can be minimised (Amoako and et. al., 2013). Apart

from it, inventory budget indicate that Restaurant is paying 60% of purchase obligations in

same month and 40% in the next month.

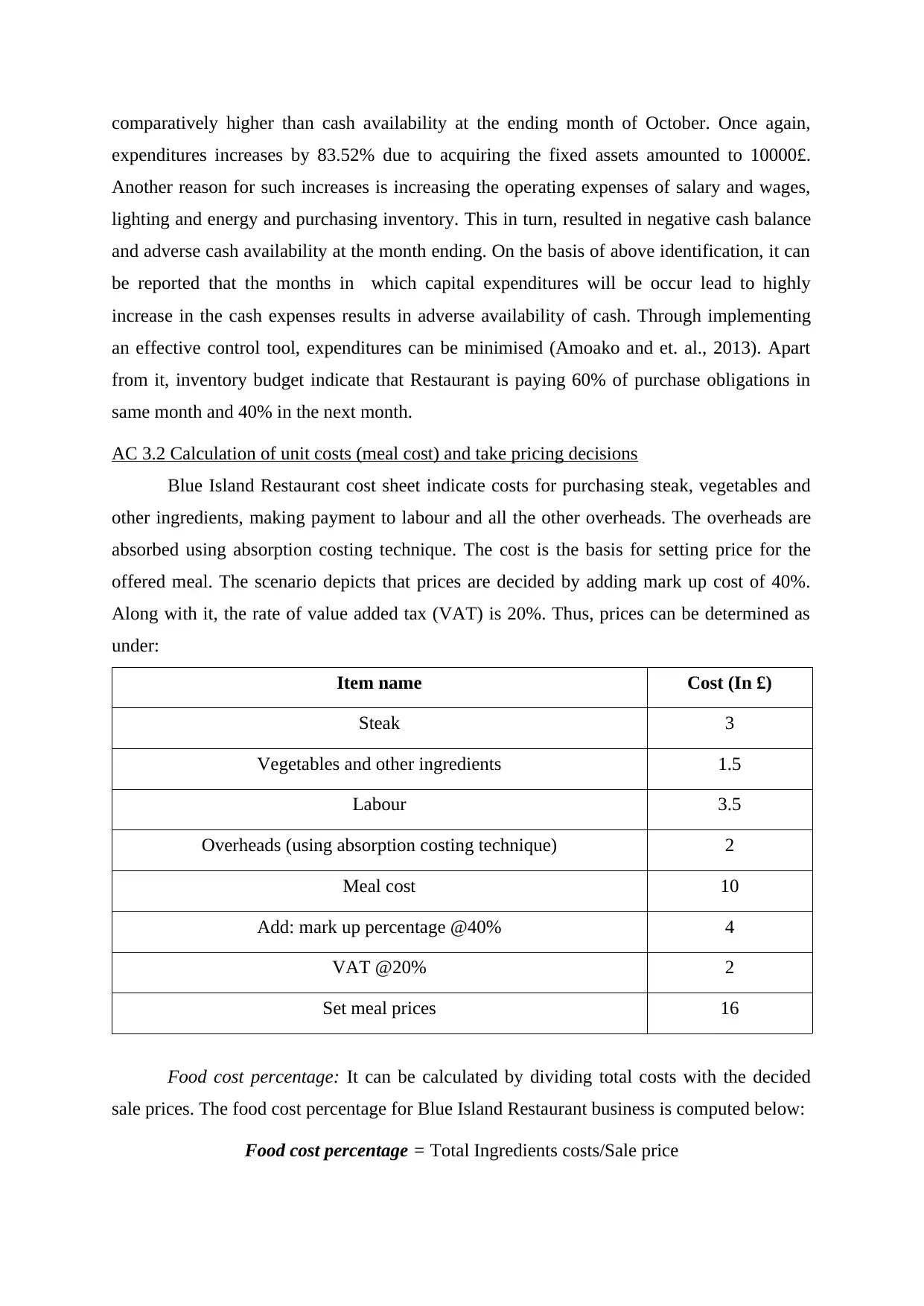

AC 3.2 Calculation of unit costs (meal cost) and take pricing decisions

Blue Island Restaurant cost sheet indicate costs for purchasing steak, vegetables and

other ingredients, making payment to labour and all the other overheads. The overheads are

absorbed using absorption costing technique. The cost is the basis for setting price for the

offered meal. The scenario depicts that prices are decided by adding mark up cost of 40%.

Along with it, the rate of value added tax (VAT) is 20%. Thus, prices can be determined as

under:

Item name Cost (In £)

Steak 3

Vegetables and other ingredients 1.5

Labour 3.5

Overheads (using absorption costing technique) 2

Meal cost 10

Add: mark up percentage @40% 4

VAT @20% 2

Set meal prices 16

Food cost percentage: It can be calculated by dividing total costs with the decided

sale prices. The food cost percentage for Blue Island Restaurant business is computed below:

Food cost percentage = Total Ingredients costs/Sale price

expenditures increases by 83.52% due to acquiring the fixed assets amounted to 10000£.

Another reason for such increases is increasing the operating expenses of salary and wages,

lighting and energy and purchasing inventory. This in turn, resulted in negative cash balance

and adverse cash availability at the month ending. On the basis of above identification, it can

be reported that the months in which capital expenditures will be occur lead to highly

increase in the cash expenses results in adverse availability of cash. Through implementing

an effective control tool, expenditures can be minimised (Amoako and et. al., 2013). Apart

from it, inventory budget indicate that Restaurant is paying 60% of purchase obligations in

same month and 40% in the next month.

AC 3.2 Calculation of unit costs (meal cost) and take pricing decisions

Blue Island Restaurant cost sheet indicate costs for purchasing steak, vegetables and

other ingredients, making payment to labour and all the other overheads. The overheads are

absorbed using absorption costing technique. The cost is the basis for setting price for the

offered meal. The scenario depicts that prices are decided by adding mark up cost of 40%.

Along with it, the rate of value added tax (VAT) is 20%. Thus, prices can be determined as

under:

Item name Cost (In £)

Steak 3

Vegetables and other ingredients 1.5

Labour 3.5

Overheads (using absorption costing technique) 2

Meal cost 10

Add: mark up percentage @40% 4

VAT @20% 2

Set meal prices 16

Food cost percentage: It can be calculated by dividing total costs with the decided

sale prices. The food cost percentage for Blue Island Restaurant business is computed below:

Food cost percentage = Total Ingredients costs/Sale price

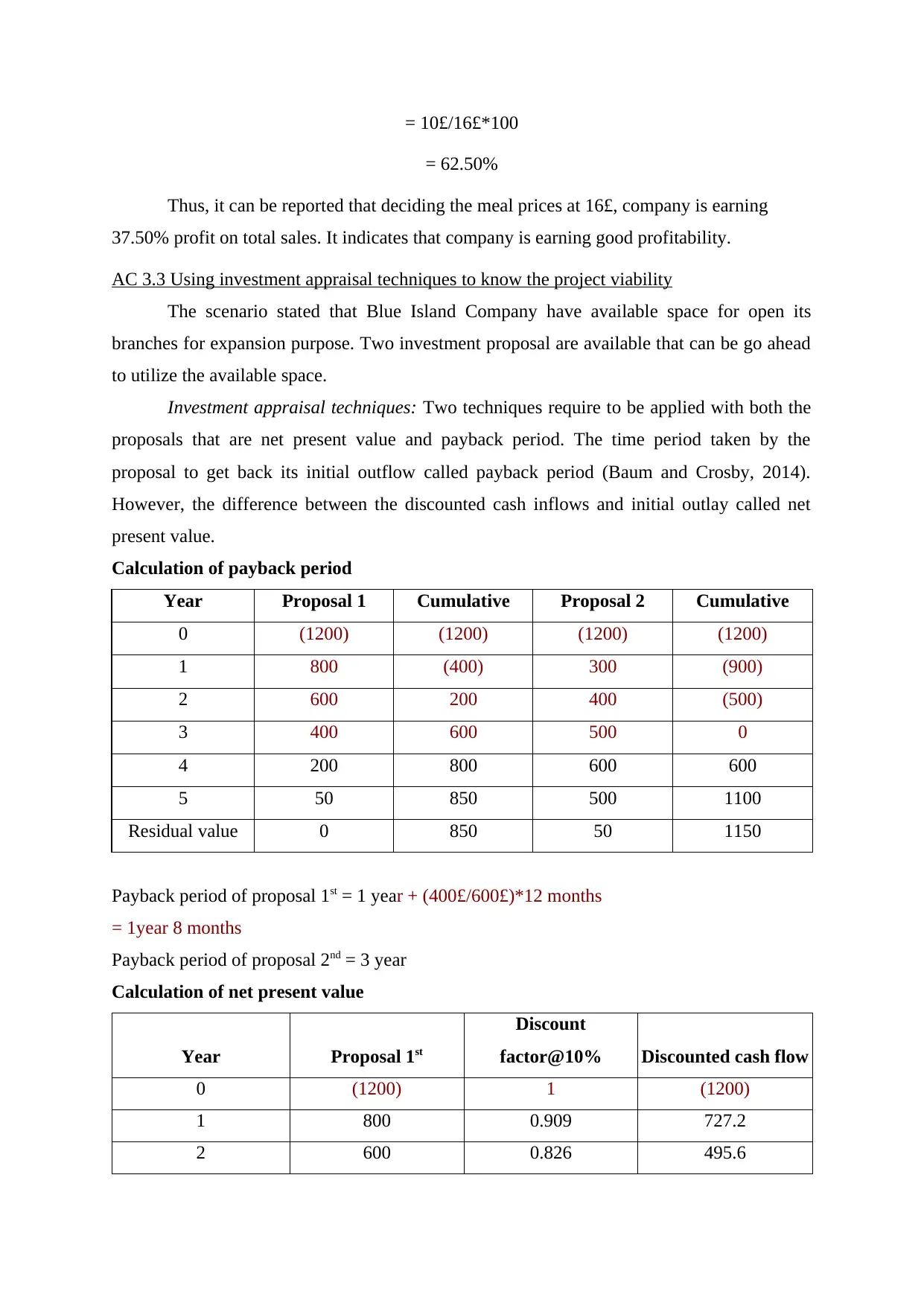

= 10£/16£*100

= 62.50%

Thus, it can be reported that deciding the meal prices at 16£, company is earning

37.50% profit on total sales. It indicates that company is earning good profitability.

AC 3.3 Using investment appraisal techniques to know the project viability

The scenario stated that Blue Island Company have available space for open its

branches for expansion purpose. Two investment proposal are available that can be go ahead

to utilize the available space.

Investment appraisal techniques: Two techniques require to be applied with both the

proposals that are net present value and payback period. The time period taken by the

proposal to get back its initial outflow called payback period (Baum and Crosby, 2014).

However, the difference between the discounted cash inflows and initial outlay called net

present value.

Calculation of payback period

Year Proposal 1 Cumulative Proposal 2 Cumulative

0 (1200) (1200) (1200) (1200)

1 800 (400) 300 (900)

2 600 200 400 (500)

3 400 600 500 0

4 200 800 600 600

5 50 850 500 1100

Residual value 0 850 50 1150

Payback period of proposal 1st = 1 year + (400£/600£)*12 months

= 1year 8 months

Payback period of proposal 2nd = 3 year

Calculation of net present value

Year Proposal 1st

Discount

factor@10% Discounted cash flow

0 (1200) 1 (1200)

1 800 0.909 727.2

2 600 0.826 495.6

= 62.50%

Thus, it can be reported that deciding the meal prices at 16£, company is earning

37.50% profit on total sales. It indicates that company is earning good profitability.

AC 3.3 Using investment appraisal techniques to know the project viability

The scenario stated that Blue Island Company have available space for open its

branches for expansion purpose. Two investment proposal are available that can be go ahead

to utilize the available space.

Investment appraisal techniques: Two techniques require to be applied with both the

proposals that are net present value and payback period. The time period taken by the

proposal to get back its initial outflow called payback period (Baum and Crosby, 2014).

However, the difference between the discounted cash inflows and initial outlay called net

present value.

Calculation of payback period

Year Proposal 1 Cumulative Proposal 2 Cumulative

0 (1200) (1200) (1200) (1200)

1 800 (400) 300 (900)

2 600 200 400 (500)

3 400 600 500 0

4 200 800 600 600

5 50 850 500 1100

Residual value 0 850 50 1150

Payback period of proposal 1st = 1 year + (400£/600£)*12 months

= 1year 8 months

Payback period of proposal 2nd = 3 year

Calculation of net present value

Year Proposal 1st

Discount

factor@10% Discounted cash flow

0 (1200) 1 (1200)

1 800 0.909 727.2

2 600 0.826 495.6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.