HI3042 Taxation Law T2 2017 Individual Assignment: Tax Implications

VerifiedAdded on 2020/04/07

|11

|1489

|259

Homework Assignment

AI Summary

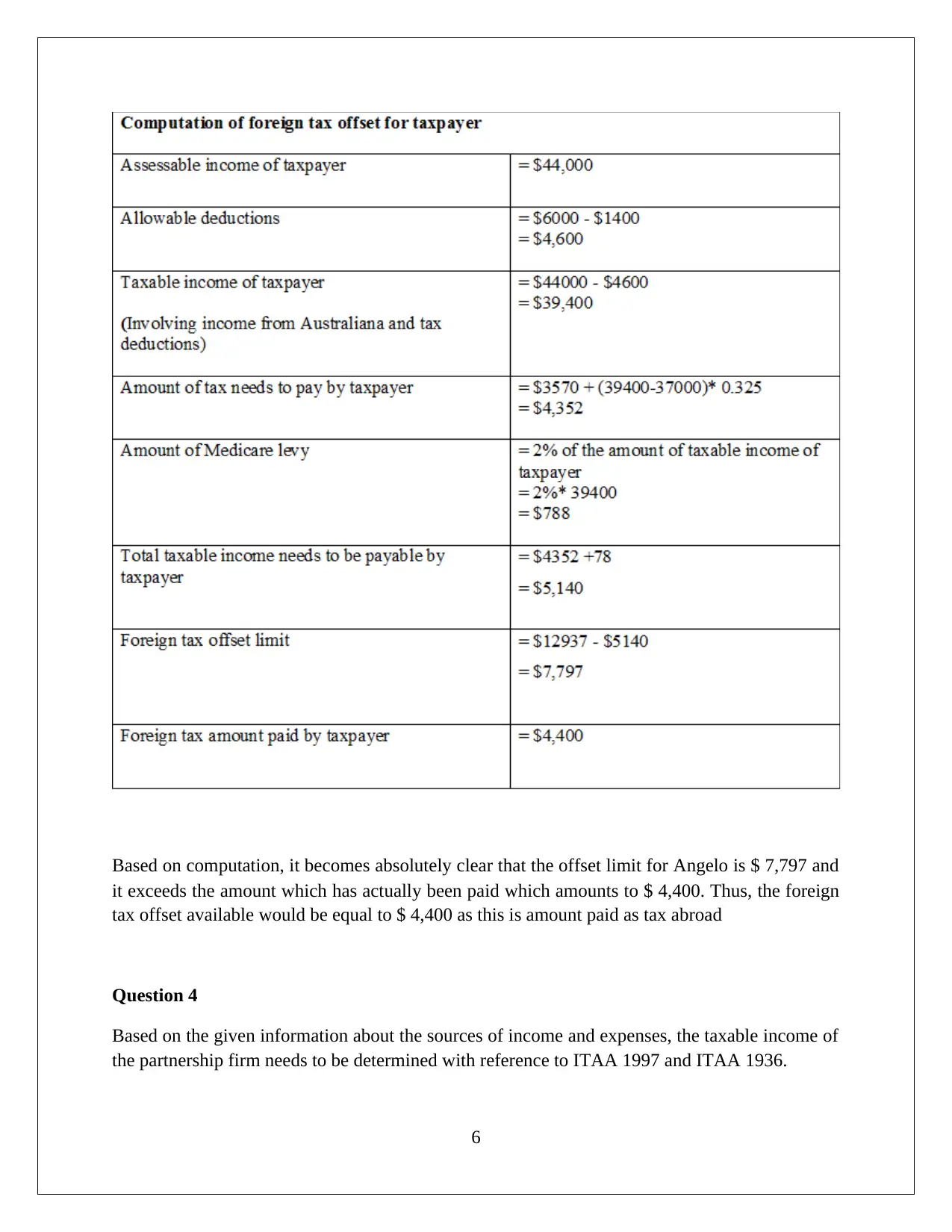

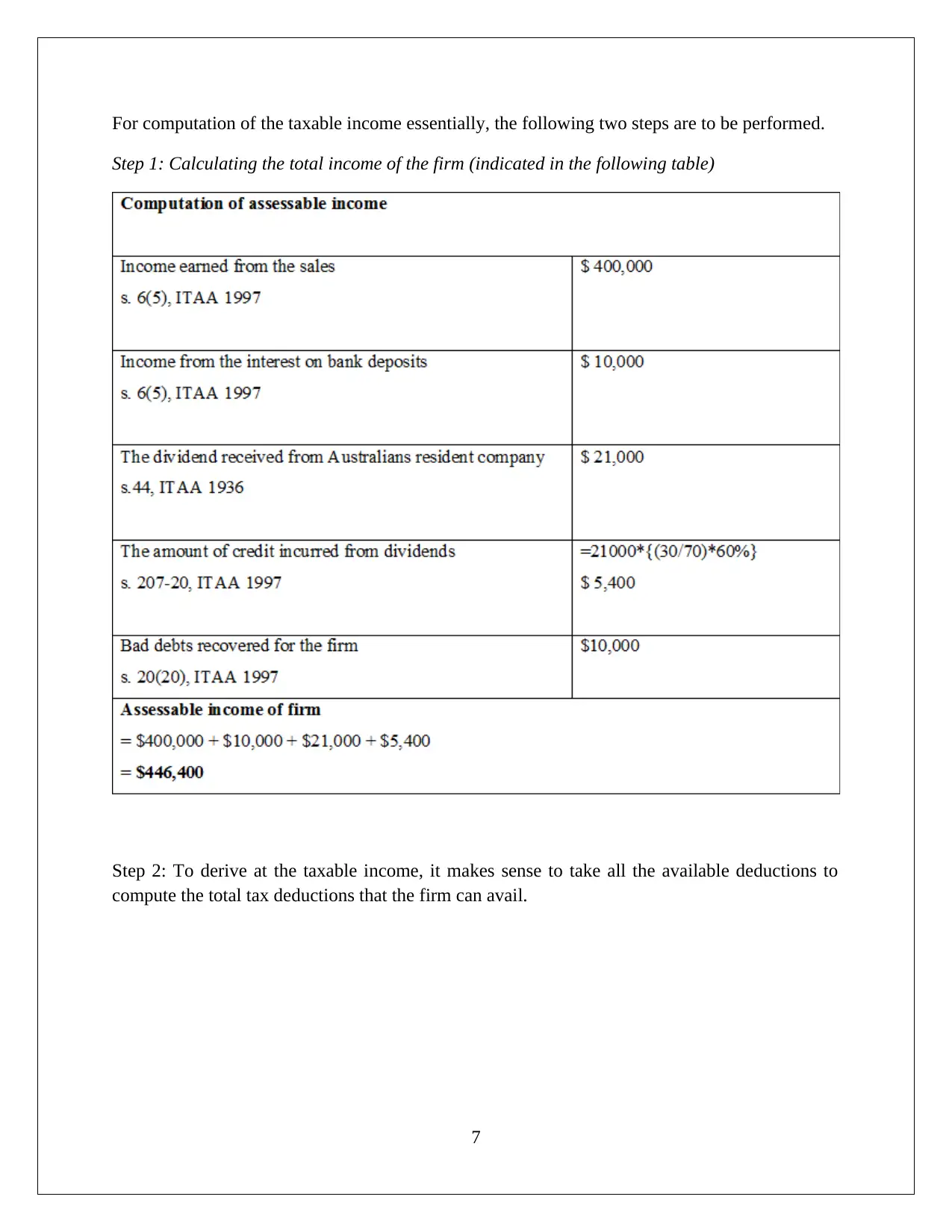

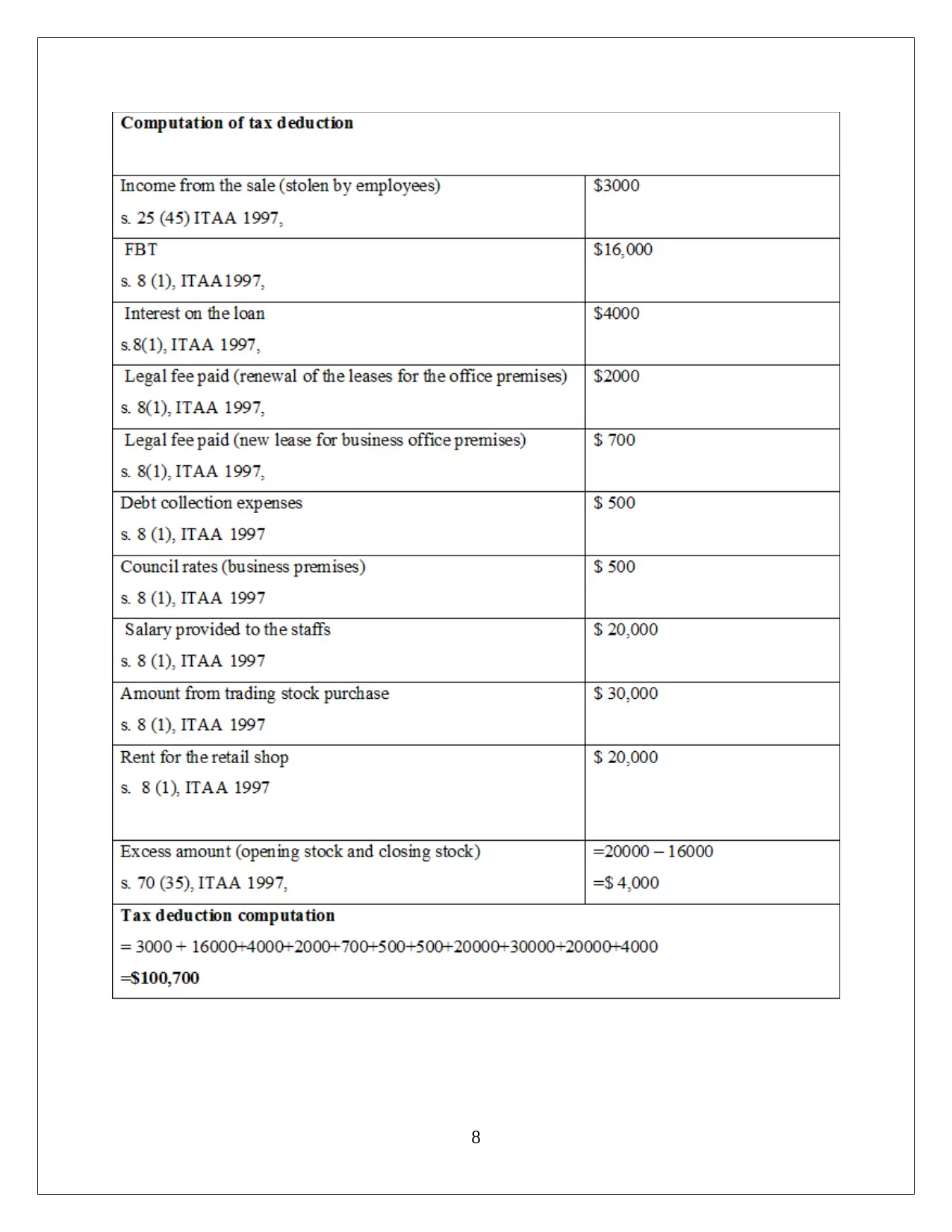

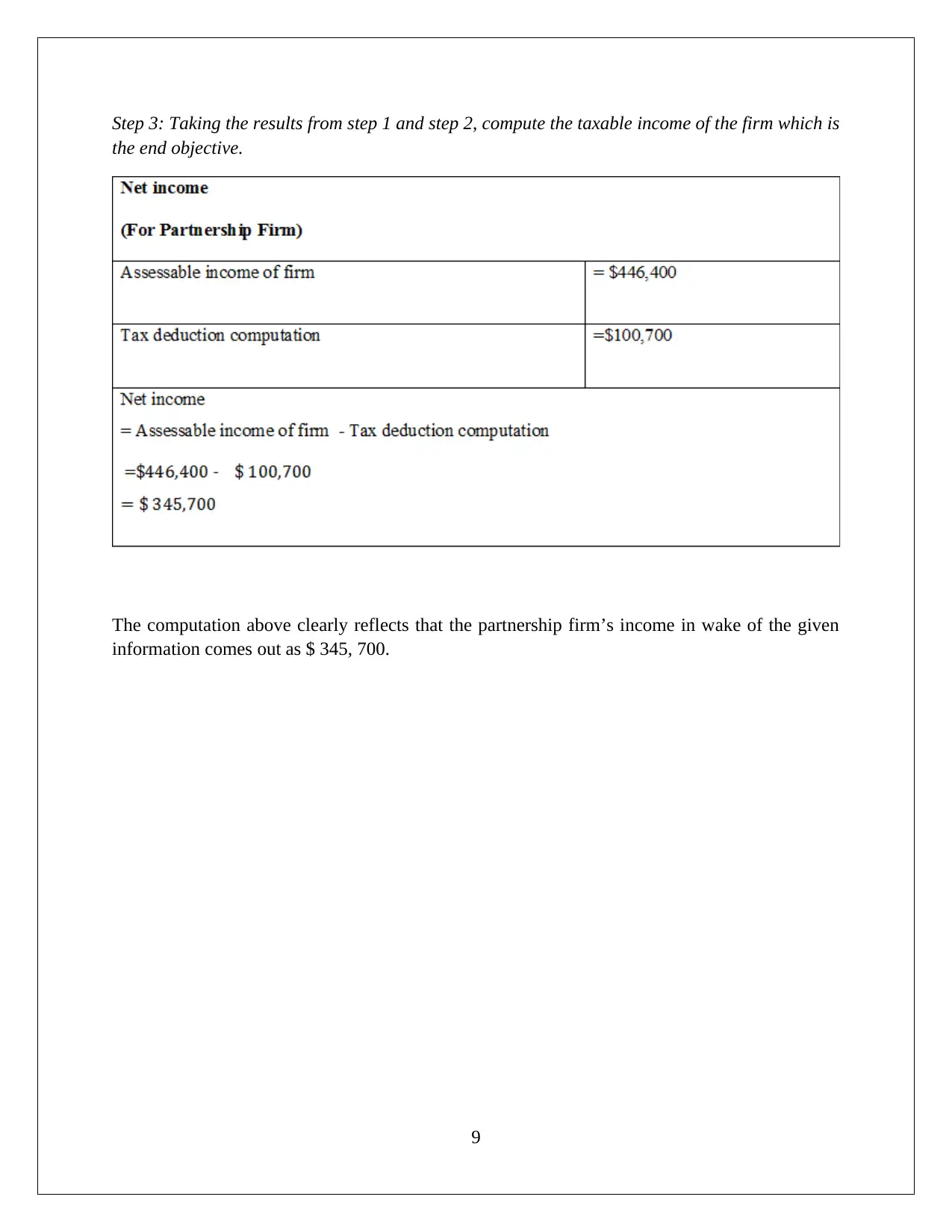

This document presents a comprehensive solution to a taxation law assignment, addressing several key issues. The first question analyzes general expense deductions under s. 8(1) ITAA 1997, differentiating between capital and revenue expenses across various scenarios. The second question focuses on input tax credits for advertising expenses, determining the creditable amount based on taxable supplies and the Financial Acquisition Threshold. The third question examines the extent of foreign tax offsets available, considering double taxation avoidance agreements. Finally, the fourth question calculates the taxable income of a partnership firm, outlining the steps involved in determining total income and deductions. The solution references relevant legal principles and case laws to support its conclusions.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.