Taxation Analysis and Solutions: University Homework Assignment

VerifiedAdded on 2020/02/19

|11

|2337

|34

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation assignment, addressing various aspects of Australian taxation law. The assignment delves into several scenarios, including the tax treatment of frequent flyer rewards, reimbursements for damaged capital assets, gifts, and funds raised by clubs. It also covers the tax implications for sportsmen, construction workers, and performing artists. Furthermore, the solution explores the deductibility of expenses related to short-term courses, travel, and self-education. The assignment also includes the computation of Manpreet's assessable income, considering his employment and educational expenses. The solution references relevant taxation rulings and case law, providing a detailed analysis of each question and offering insights into the application of tax principles.

Running head: TAXATION

Taxation

Name of the student

Name of the university

Author note

Taxation

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question – i............................................................................................................2

Answer to question – ii..........................................................................................................2

Answer to question – iii.........................................................................................................3

Answer to question – iv..........................................................................................................3

Answer to question – v...........................................................................................................4

Answer to question – vi..........................................................................................................4

Answer to question – vii........................................................................................................5

Answer to question – viii.......................................................................................................5

Answer to question – ix..........................................................................................................6

Answer to question – x...........................................................................................................6

Answer to question 2..................................................................................................................7

Manpreet’s assessable income computation..........................................................................9

Reference..................................................................................................................................10

Table of Contents

Answer to question 1..................................................................................................................2

Answer to question – i............................................................................................................2

Answer to question – ii..........................................................................................................2

Answer to question – iii.........................................................................................................3

Answer to question – iv..........................................................................................................3

Answer to question – v...........................................................................................................4

Answer to question – vi..........................................................................................................4

Answer to question – vii........................................................................................................5

Answer to question – viii.......................................................................................................5

Answer to question – ix..........................................................................................................6

Answer to question – x...........................................................................................................6

Answer to question 2..................................................................................................................7

Manpreet’s assessable income computation..........................................................................9

Reference..................................................................................................................................10

2TAXATION

Answer to question 1

Answer to question – i

As per the TR 1999/6 taxation ruling if any points or rewards received by any regular

fliers from the airline organization, the amount will be included under the assessable income

of the receiver. Further, the TR 1999/6 taxation ruling deals with the points or rewards

received from the flight that is offered to the loyal customers. However, the rewards will be

dealt as fringe benefit tax if the below mentioned criteria are fulfilled –

The rewards or points offered to the employee in consideration with the specific

arrangement

The reward or point is offered to the employee owing to his job with the company or a

family relationship is there between the employee and the employer1

If the individual received the reward for offering the service as there is an entitlement

for the flight rewards, the rewards will be dealt in as the business expense of the employer. It

is evident from the given circumstances that points or rewards received by the frequent flier

of the Webjet from the large business firm in consideration for their work shall not be taxed

under regular taxable income and it shall not be included even under the fringe benefit tax.

Answer to question – ii

Where any person receives any reimbursement due to the damage of his capital asset

that he provided to the customers as part of provision of services, the amount of

1 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Answer to question 1

Answer to question – i

As per the TR 1999/6 taxation ruling if any points or rewards received by any regular

fliers from the airline organization, the amount will be included under the assessable income

of the receiver. Further, the TR 1999/6 taxation ruling deals with the points or rewards

received from the flight that is offered to the loyal customers. However, the rewards will be

dealt as fringe benefit tax if the below mentioned criteria are fulfilled –

The rewards or points offered to the employee in consideration with the specific

arrangement

The reward or point is offered to the employee owing to his job with the company or a

family relationship is there between the employee and the employer1

If the individual received the reward for offering the service as there is an entitlement

for the flight rewards, the rewards will be dealt in as the business expense of the employer. It

is evident from the given circumstances that points or rewards received by the frequent flier

of the Webjet from the large business firm in consideration for their work shall not be taxed

under regular taxable income and it shall not be included even under the fringe benefit tax.

Answer to question – ii

Where any person receives any reimbursement due to the damage of his capital asset

that he provided to the customers as part of provision of services, the amount of

1 Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

reimbursement shall not be assessed as income under the income tax of the person. However,

to be qualified to get deduction, the below mentioned conditions must be fulfilled –

The asset offered under the provision of service must be of capital nature and the asset

must be used for the purpose of business solely2

The amount of reimbursement received from the customer shall be used exclusively

for restructuring the part of the capital asset that is damaged.

The capital asset must be depreciable asset and the proof of budgeted depreciation

must be there in the books of account for the asset.

Taking into consideration the above mentioned conditions, the amount received as

reimbursement with regard to damage of the asset while it was used under the provision of

service shall not be included as income for the purpose of assessing the taxable income.

However, the above mentioned conditions must be complied with for getting the deductions.

Answer to question – iii

Any amount be it in cash or kind, received as the gift are not qualified as the

deductible income or is not included under the exempted income rather, it is included under

the assessable income as per the taxation ruling of Australian Tax Office or ATO. The small

gifts are not taken into consideration in the period while the person’s tax is assessed. On the

contrary, the bigger amounts of the gifts that are convertible into monetary form and the gifts

that are received in the form of kind, the total measurable amount with regard to the gift are

assessed as the assessable income as per the income tax ruling. In the given circumstances,

the manager of the night club was offered the holiday package to overseas by the alcohol

2 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

reimbursement shall not be assessed as income under the income tax of the person. However,

to be qualified to get deduction, the below mentioned conditions must be fulfilled –

The asset offered under the provision of service must be of capital nature and the asset

must be used for the purpose of business solely2

The amount of reimbursement received from the customer shall be used exclusively

for restructuring the part of the capital asset that is damaged.

The capital asset must be depreciable asset and the proof of budgeted depreciation

must be there in the books of account for the asset.

Taking into consideration the above mentioned conditions, the amount received as

reimbursement with regard to damage of the asset while it was used under the provision of

service shall not be included as income for the purpose of assessing the taxable income.

However, the above mentioned conditions must be complied with for getting the deductions.

Answer to question – iii

Any amount be it in cash or kind, received as the gift are not qualified as the

deductible income or is not included under the exempted income rather, it is included under

the assessable income as per the taxation ruling of Australian Tax Office or ATO. The small

gifts are not taken into consideration in the period while the person’s tax is assessed. On the

contrary, the bigger amounts of the gifts that are convertible into monetary form and the gifts

that are received in the form of kind, the total measurable amount with regard to the gift are

assessed as the assessable income as per the income tax ruling. In the given circumstances,

the manager of the night club was offered the holiday package to overseas by the alcohol

2 The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

supplier. This gift shall be included as the taxable income while calculating the assessable

income.

Answer to question – iv

In the given case, Canoe club fund-raised for buy of extra canoes and in the end the

extra monies were returned to the individual from the Canoe club. Under the ATO, the extra

cash raised which will eventually returned to the club member will not be taken into account

as assessable income while processing the assessable earning. This cash won't be assessed as

income while figuring the assessable pay under the taxable income as the additional cash

does not qualify as the option of additional reserve. Further, it will be treated as raised for the

need only3.

Answer to question – v

The benefit that is received by the sportsmen with regard to his engagement in the

sport is included while assessing his income under income tax. As per the TR 1999/17,

Taxation ruling, under the normal concept of income, if the advantage received by the

sportsman forms the part of assessable income for the purpose of tax, then the amount will be

considered as income. Under the given circumstance, the footballer received the amount from

television station as he was selected as fairest and the best player in the AFL4. Therefore, the

amount shall be assessed as taxable under the taxable ruling while the income of the player

will be calculated.

3 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

supplier. This gift shall be included as the taxable income while calculating the assessable

income.

Answer to question – iv

In the given case, Canoe club fund-raised for buy of extra canoes and in the end the

extra monies were returned to the individual from the Canoe club. Under the ATO, the extra

cash raised which will eventually returned to the club member will not be taken into account

as assessable income while processing the assessable earning. This cash won't be assessed as

income while figuring the assessable pay under the taxable income as the additional cash

does not qualify as the option of additional reserve. Further, it will be treated as raised for the

need only3.

Answer to question – v

The benefit that is received by the sportsmen with regard to his engagement in the

sport is included while assessing his income under income tax. As per the TR 1999/17,

Taxation ruling, under the normal concept of income, if the advantage received by the

sportsman forms the part of assessable income for the purpose of tax, then the amount will be

considered as income. Under the given circumstance, the footballer received the amount from

television station as he was selected as fairest and the best player in the AFL4. Therefore, the

amount shall be assessed as taxable under the taxable ruling while the income of the player

will be calculated.

3 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

5TAXATION

Answer to question – vi

TR 95/22 under the Taxation ruling deals with the allowance and reimbursement of

the employees. It is mentioned under the ruling that the activities which are qualified for

construction and building of the employees are as follows –

Labours those are engaged for the purpose of constructing the building

Trainees, apprentice and the carpenters5

Project manager or overseer engaged for the said post for any under construction

building

The engagement of the project manager in the construction site.

Expenditures made for the apprentice to construct their qualification with regard to

building is included under the taxation ruling and are regarded as construction and building of

labours and therefore, will be allowed under deduction as compensation.

Answer to question – vii

For the amount spend under the short term course to be qualified as deduction it must

be exclusively incurred for the course only6. Further, if only a part of the expenses are

incurred for the course, then the deduction will be allowed proportionately only and not for

the total amount. If any person spend monies for undertaking short course with regard to the

subject of art management in consideration of becoming art director will be qualified as

deduction, if the below mentioned conditions are satisfied –

5 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

6 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting Review 91.1 (2015):

47-68.

Answer to question – vi

TR 95/22 under the Taxation ruling deals with the allowance and reimbursement of

the employees. It is mentioned under the ruling that the activities which are qualified for

construction and building of the employees are as follows –

Labours those are engaged for the purpose of constructing the building

Trainees, apprentice and the carpenters5

Project manager or overseer engaged for the said post for any under construction

building

The engagement of the project manager in the construction site.

Expenditures made for the apprentice to construct their qualification with regard to

building is included under the taxation ruling and are regarded as construction and building of

labours and therefore, will be allowed under deduction as compensation.

Answer to question – vii

For the amount spend under the short term course to be qualified as deduction it must

be exclusively incurred for the course only6. Further, if only a part of the expenses are

incurred for the course, then the deduction will be allowed proportionately only and not for

the total amount. If any person spend monies for undertaking short course with regard to the

subject of art management in consideration of becoming art director will be qualified as

deduction, if the below mentioned conditions are satisfied –

5 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

6 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting Review 91.1 (2015):

47-68.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

Training cost incurred for the software or any module

Expenses for the meal that is recommended to be incurred7

Travelling expenses for up and down travel to the course institution

Amount paid for the course as fees under the short term course of art management.

Taking into consideration the above facts, it is presumed that the individual incurred

the expenses exclusively for the course as the detail information is not provided related to the

head of expenses and therefore will be qualified for deduction.

Answer to question – viii

Under the Australian Taxation Office ruling, the persons to be regarded as the

performing artist must satisfy one of the below mentioned criteria –

Any person performing in circus will be performing artist

Any person performing as dancer will be performing artist

Any person perform as a singer will be performing artist

Any person performing as musician will be performing artist

Any person performing as an actor will be performing artist

Various kinds of artists will be performing artist.

Under the ATO, any expenditure incurred by a performing artist in association with

the performance will be qualified as deduction, if the person is qualified as performing artist

as per the above mentioned criteria8. In the given circumstance, in absence of sufficient

7 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

8 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Training cost incurred for the software or any module

Expenses for the meal that is recommended to be incurred7

Travelling expenses for up and down travel to the course institution

Amount paid for the course as fees under the short term course of art management.

Taking into consideration the above facts, it is presumed that the individual incurred

the expenses exclusively for the course as the detail information is not provided related to the

head of expenses and therefore will be qualified for deduction.

Answer to question – viii

Under the Australian Taxation Office ruling, the persons to be regarded as the

performing artist must satisfy one of the below mentioned criteria –

Any person performing in circus will be performing artist

Any person performing as dancer will be performing artist

Any person perform as a singer will be performing artist

Any person performing as musician will be performing artist

Any person performing as an actor will be performing artist

Various kinds of artists will be performing artist.

Under the ATO, any expenditure incurred by a performing artist in association with

the performance will be qualified as deduction, if the person is qualified as performing artist

as per the above mentioned criteria8. In the given circumstance, in absence of sufficient

7 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

8 CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

information, it will be presumed that the expenses incurred were for the make-up and work

dress of the performing artist and will be therefore, allowed under deduction.

Answer to question – ix

Where the travelling expenses is proportionately official and proportionately private,

then the official part will only be qualified as deduction. The travel between office and home

is regarded as personal expenditure. However, under some particular circumstances, the

travelling to office is qualified under deduction. Where the travelling is solely carried out for

official purpose, the expenses with regard to travel will be qualified as deduction. Here in the

given case study, the expenditure with regard to travel will be presumed as incurred solely for

office purpose and thus will be qualified under deduction9.

Answer to question – x

As per the taxation ruling of Australian Tax Office, if any individual incur any travel

expense for travelling two places of work, will be qualified as the deduction. The deduction

will only be allowed if both the workplace falls under the control of same employer. In the

given circumstance, the individual travelled two workplaces that were under control of

different employers and hence will be disallowed as deduction under the taxation ruling.

Answer to question 2

Any individual can claim deduction for the self education related expenditures if she

qualifies to receive taxable scholarship that is bonded or she conduct the study for the

purpose of work. To choose the assessable situation of an individual it is essential to work out

if an individual is overseas resident or Australian inhabitant for computing the assessable

earning under taxation ruling. A foreign student admitted for a course in Australian

9 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

information, it will be presumed that the expenses incurred were for the make-up and work

dress of the performing artist and will be therefore, allowed under deduction.

Answer to question – ix

Where the travelling expenses is proportionately official and proportionately private,

then the official part will only be qualified as deduction. The travel between office and home

is regarded as personal expenditure. However, under some particular circumstances, the

travelling to office is qualified under deduction. Where the travelling is solely carried out for

official purpose, the expenses with regard to travel will be qualified as deduction. Here in the

given case study, the expenditure with regard to travel will be presumed as incurred solely for

office purpose and thus will be qualified under deduction9.

Answer to question – x

As per the taxation ruling of Australian Tax Office, if any individual incur any travel

expense for travelling two places of work, will be qualified as the deduction. The deduction

will only be allowed if both the workplace falls under the control of same employer. In the

given circumstance, the individual travelled two workplaces that were under control of

different employers and hence will be disallowed as deduction under the taxation ruling.

Answer to question 2

Any individual can claim deduction for the self education related expenditures if she

qualifies to receive taxable scholarship that is bonded or she conduct the study for the

purpose of work. To choose the assessable situation of an individual it is essential to work out

if an individual is overseas resident or Australian inhabitant for computing the assessable

earning under taxation ruling. A foreign student admitted for a course in Australian

9 Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

8TAXATION

foundation, term for which is over a half year will be represented as the Australian inhabitant

for computing the expense. It is likewise a vital factor that the course should be impressively

connected with current employment. As appreciated from the current circumstance Manpreet

will be represented as the Australian inhabitant with the true objective of assessment

gathering since he is chosen in a course that has the term of more than six months period in

Australian institution. In addition, Manpreet additionally connected with himself as part time

office assistant under an Australian firm from where he got month to month compensation

added up to $45,000. Further, Manpreet spend some costs associated with education that are

not permitted as deduction under assessable income. Moreover, the expenses with regard to

self-education amounted to $ 18,000 spend by Manpreet will likewise not qualify as

deductible costs. Further, to qualify for deduction, following conditions must be satisfied –

The study will enhance or at least will maintain the necessary knowledge and the

skills pre-requisite for the present work

The study is likely to enhance or will enhance the income of the person from the

present work10 .

One more notable fact is that to be qualified for the deduction, the course are bound to be

related to the current employment, else the expenses will not qualify for deduction even if –

It assisted the person for the opportunity of new job

It is related to the current employment in general terms

As to ITAA 1997, Section 8-1, the expenses incurred for obtaining the new mobile

phone is connected with procuring the assessable pay and in this way, Manpreet's expenses

will be reasonable deduction under the income tax ruling. Further, it is recognized from FC of

10 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

foundation, term for which is over a half year will be represented as the Australian inhabitant

for computing the expense. It is likewise a vital factor that the course should be impressively

connected with current employment. As appreciated from the current circumstance Manpreet

will be represented as the Australian inhabitant with the true objective of assessment

gathering since he is chosen in a course that has the term of more than six months period in

Australian institution. In addition, Manpreet additionally connected with himself as part time

office assistant under an Australian firm from where he got month to month compensation

added up to $45,000. Further, Manpreet spend some costs associated with education that are

not permitted as deduction under assessable income. Moreover, the expenses with regard to

self-education amounted to $ 18,000 spend by Manpreet will likewise not qualify as

deductible costs. Further, to qualify for deduction, following conditions must be satisfied –

The study will enhance or at least will maintain the necessary knowledge and the

skills pre-requisite for the present work

The study is likely to enhance or will enhance the income of the person from the

present work10 .

One more notable fact is that to be qualified for the deduction, the course are bound to be

related to the current employment, else the expenses will not qualify for deduction even if –

It assisted the person for the opportunity of new job

It is related to the current employment in general terms

As to ITAA 1997, Section 8-1, the expenses incurred for obtaining the new mobile

phone is connected with procuring the assessable pay and in this way, Manpreet's expenses

will be reasonable deduction under the income tax ruling. Further, it is recognized from FC of

10 Chartered Accountants Australia & New Zealand (2017) CAANZ https://www.charteredaccountantsanz.com/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

T versus M I Roberts 92 ATC 4787 that the use of Maddalena standards to the government

court enabled the mine director to be qualified for deductible expenses as to study under

MBA.

Simultaneously, Manpreet incurred some money towards printer and computer and

buy of another mobile phone, which was related with the prerequisite of work. According to

the general ruling, the expenses qualified for deduction under the ITAA 1997, Section 8-1, if

there is noteworthy connection among the limit of gaining and uses and it frames required

character for the relationship of work and it is not in the local or private nature. As per the

case study of Ronpibon Tin NL vs FC of T (1949), there must exist a correlation between the

taxable income and the incurred expenses for the calculation of assessable income. Therefore,

Manpreet’s expenditures for self education will be disallowed for deduction as it was not

incurred for getting new income.

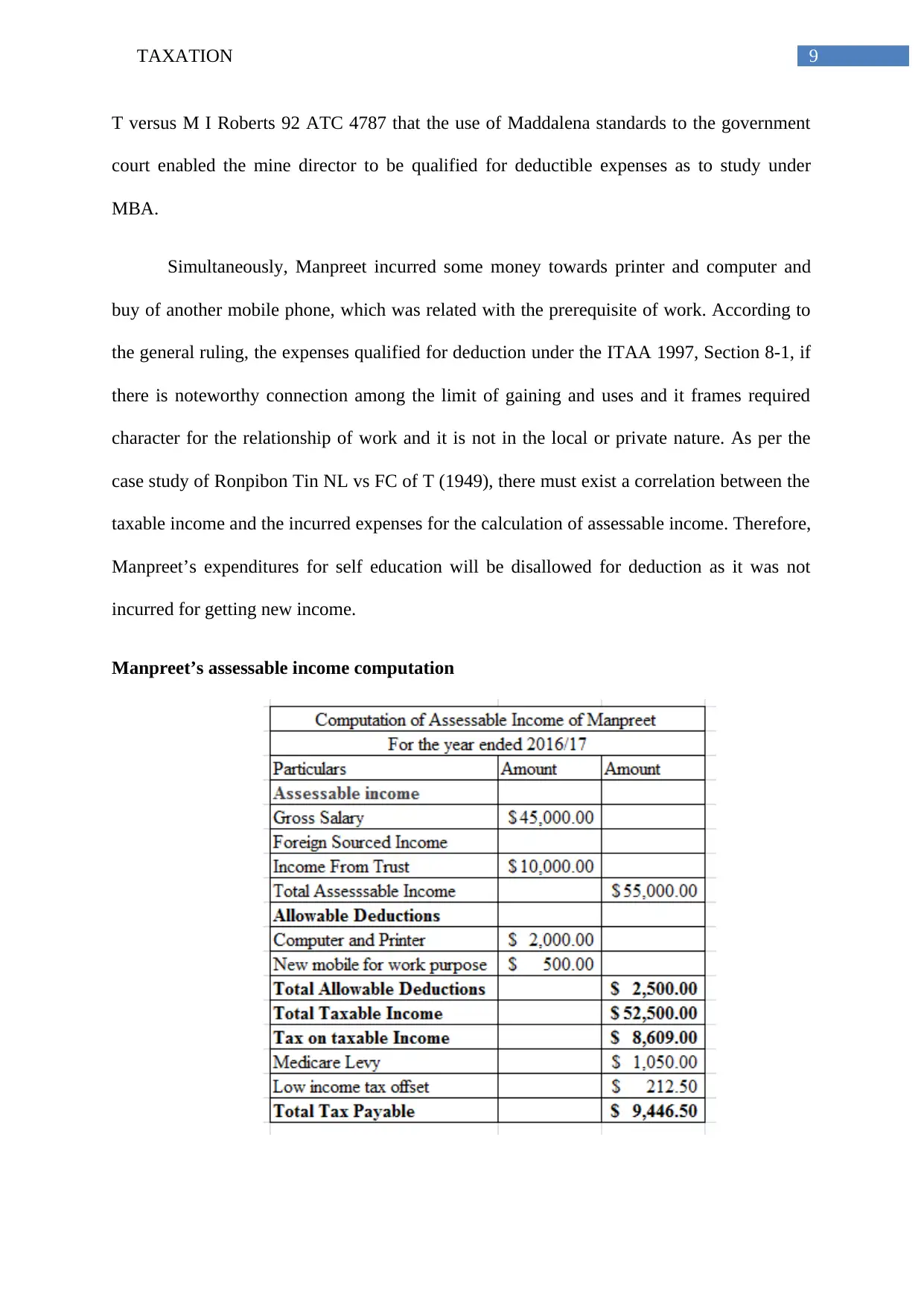

Manpreet’s assessable income computation

T versus M I Roberts 92 ATC 4787 that the use of Maddalena standards to the government

court enabled the mine director to be qualified for deductible expenses as to study under

MBA.

Simultaneously, Manpreet incurred some money towards printer and computer and

buy of another mobile phone, which was related with the prerequisite of work. According to

the general ruling, the expenses qualified for deduction under the ITAA 1997, Section 8-1, if

there is noteworthy connection among the limit of gaining and uses and it frames required

character for the relationship of work and it is not in the local or private nature. As per the

case study of Ronpibon Tin NL vs FC of T (1949), there must exist a correlation between the

taxable income and the incurred expenses for the calculation of assessable income. Therefore,

Manpreet’s expenditures for self education will be disallowed for deduction as it was not

incurred for getting new income.

Manpreet’s assessable income computation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Reference

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

Reference

Ato.Gov.Au/ (2017) Ato.gov.au https://www.ato.gov.au/

Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Chartered Accountants Australia & New Zealand (2017) CAANZ

https://www.charteredaccountantsanz.com/

CPA Australia (2017) Cpaaustralia.com.au https://www.cpaaustralia.com.au/

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Karin Simon, Sara McDonald, Accident Investigation - Databases - Library Guides At

Cquniversity (2017) Libguides.library.cqu.edu.au

http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174

Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

The Tax Institute (2017) Taxinstitute.com.au https://www.taxinstitute.com.au/

Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.