TAXATION 11 Assignment: Taxation Law Analysis, Question and Answers

VerifiedAdded on 2020/02/23

|14

|2359

|269

Homework Assignment

AI Summary

This assignment solution for TAXATION 11 provides detailed answers to various taxation-related questions, analyzing scenarios such as fringe benefit tax, compensation for damaged assets, gifts, and travel expenses. It delves into specific rulings from the Australian Taxation Office (ATO) to determine assessable income and allowable deductions for different situations. The assignment also includes a case study on Manpreet, an international student, calculating his assessable income, considering his salary, income from overseas sources, and self-education expenses, along with deductions for work-related purchases. The solution references relevant taxation rulings and legal precedents to support its analysis, culminating in a computation of Manpreet's taxable income and tax liability.

Running head: TAXATION

Taxation

Name of the student

Name of the university

Author note

Taxation

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

QUESTION 1.............................................................................................................................2

Answer i.................................................................................................................................2

Answer ii................................................................................................................................2

Answer iii...............................................................................................................................3

Answer iv...............................................................................................................................3

Answer v................................................................................................................................4

Answer vi...............................................................................................................................4

Answer vii..............................................................................................................................4

Answer viii.............................................................................................................................5

Answer ix...............................................................................................................................6

Answer x................................................................................................................................6

QUESTION 2.............................................................................................................................7

Computation of assessable income of Manpreet........................................................................9

Reference..................................................................................................................................10

Table of Contents

QUESTION 1.............................................................................................................................2

Answer i.................................................................................................................................2

Answer ii................................................................................................................................2

Answer iii...............................................................................................................................3

Answer iv...............................................................................................................................3

Answer v................................................................................................................................4

Answer vi...............................................................................................................................4

Answer vii..............................................................................................................................4

Answer viii.............................................................................................................................5

Answer ix...............................................................................................................................6

Answer x................................................................................................................................6

QUESTION 2.............................................................................................................................7

Computation of assessable income of Manpreet........................................................................9

Reference..................................................................................................................................10

2TAXATION

QUESTION 1

Answer i

It is clearly mentioned under the Taxation ruling for TR 1999/6 that the rewards or the

points received by the clients from the airline business organizations are not treated as

income under taxation. However, these rewards or points may attract the fringe benefit tax if

the below mentioned conditions are satisfied –

The rewards or the flight points are allocated to the customers under some specific

arrangement

There exists a family relationship among the employer and employee or the rewards

and points received by the employees with regard to his employment1

From the above discussion, it is clear that the reward for repeated flier of Webjet

received from the large business entity by the employees with regard to their travel related to

work that is paid by the company shall not be included under the taxable income, nor it shall

be taxed as the fringe benefit tax.

Answer ii

If any person receives any compensation from the customer owing to the damages of

the capital asset while providing service to that customer with that capital asset, the damage

compensation shall not be included under the assessable income for tax. However, to get the

benefit followings factors must be taken into account –

The compensation amount received for the damage must be used for refurbishing the

damaged part of the asset.

1 Ato.Gov.Au/ (2017) Ato.gov.au <https://www.ato.gov.au/>.

QUESTION 1

Answer i

It is clearly mentioned under the Taxation ruling for TR 1999/6 that the rewards or the

points received by the clients from the airline business organizations are not treated as

income under taxation. However, these rewards or points may attract the fringe benefit tax if

the below mentioned conditions are satisfied –

The rewards or the flight points are allocated to the customers under some specific

arrangement

There exists a family relationship among the employer and employee or the rewards

and points received by the employees with regard to his employment1

From the above discussion, it is clear that the reward for repeated flier of Webjet

received from the large business entity by the employees with regard to their travel related to

work that is paid by the company shall not be included under the taxable income, nor it shall

be taxed as the fringe benefit tax.

Answer ii

If any person receives any compensation from the customer owing to the damages of

the capital asset while providing service to that customer with that capital asset, the damage

compensation shall not be included under the assessable income for tax. However, to get the

benefit followings factors must be taken into account –

The compensation amount received for the damage must be used for refurbishing the

damaged part of the asset.

1 Ato.Gov.Au/ (2017) Ato.gov.au <https://www.ato.gov.au/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

The asset shall be a depreciable asset and the forecasted depreciation must be

accounted for in the record with regard to the asset.

The assets shall be in the nature of capital asset and shall be exclusively used for the

business purpose of the receiver2.

Therefore, the compensation received for the damaged goods while providing services

by the company that hires crane will not be included under the taxable income, provided the

conditions mentioned above are fulfilled.

Answer iii

As per the ATO (Australian Taxation Office), any gifts received in for form of cash or

kind by any individual are treated as part of the assessable income for taxation and not

included under the non-assessable income or exempted income. With regard to the receipt of

big gifts that can be transferred into cash or money and the cash gifts or gifts received in kind

that are offered to the employee, the sum of gifts are included under the taxable income of the

receiver. However, the small amount of gift is not included under the period when the tax of

the person is calculated. Here in the given case, the supplier of alcohol offered free overseas

holiday package to the night club manager. This gift will be considered and included under

the assessable income of the night club manager.

Answer iv

A per the ATO, the additional money raised that will be refunded to the member will

not be considered as income while computing the assessable income. In the given case,

Canoe club raised money for purchase of additional canoes and eventually the additional

monies were refunded to the member of the Canoe club3. This money will not be considered

as income while computing the assessable income under income tax as the extra money does

2 CPA Australia (2017) Cpaaustralia.com.au <https://www.cpaaustralia.com.au/>.

The asset shall be a depreciable asset and the forecasted depreciation must be

accounted for in the record with regard to the asset.

The assets shall be in the nature of capital asset and shall be exclusively used for the

business purpose of the receiver2.

Therefore, the compensation received for the damaged goods while providing services

by the company that hires crane will not be included under the taxable income, provided the

conditions mentioned above are fulfilled.

Answer iii

As per the ATO (Australian Taxation Office), any gifts received in for form of cash or

kind by any individual are treated as part of the assessable income for taxation and not

included under the non-assessable income or exempted income. With regard to the receipt of

big gifts that can be transferred into cash or money and the cash gifts or gifts received in kind

that are offered to the employee, the sum of gifts are included under the taxable income of the

receiver. However, the small amount of gift is not included under the period when the tax of

the person is calculated. Here in the given case, the supplier of alcohol offered free overseas

holiday package to the night club manager. This gift will be considered and included under

the assessable income of the night club manager.

Answer iv

A per the ATO, the additional money raised that will be refunded to the member will

not be considered as income while computing the assessable income. In the given case,

Canoe club raised money for purchase of additional canoes and eventually the additional

monies were refunded to the member of the Canoe club3. This money will not be considered

as income while computing the assessable income under income tax as the extra money does

2 CPA Australia (2017) Cpaaustralia.com.au <https://www.cpaaustralia.com.au/>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

not qualify as the alternative extra fund. Rather the money was collected as per the

requirement only.

Answer v

Any benefit received by any sportsman owing to his connection with the sport is

treated under as per the Taxation ruling for TR 1999/17. With regard to the ruling, any

benefits or any sum that is received by the sportsman will be treated as income while

calculating the assessable income under taxation if the receipt forms part of the assessable

income under the general concept4. Here in the given case, the Australian footballer received

the money for being the fairest and best player in AFL from the television station will be

included under the assessable income of the player while computation the income for the

purpose of taxation.

Answer vi

The reimbursement, allowance for employees building is dealt with under the

Taxation Ruling for TR 95/22. According the said ruling the below mentioned activities are

considered as building and construction of the employees –

Apprentice, trainees and carpenters

The site of the construction where the project managers work

Supervisor or the project manager for the building which is under construction

3 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

4 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

not qualify as the alternative extra fund. Rather the money was collected as per the

requirement only.

Answer v

Any benefit received by any sportsman owing to his connection with the sport is

treated under as per the Taxation ruling for TR 1999/17. With regard to the ruling, any

benefits or any sum that is received by the sportsman will be treated as income while

calculating the assessable income under taxation if the receipt forms part of the assessable

income under the general concept4. Here in the given case, the Australian footballer received

the money for being the fairest and best player in AFL from the television station will be

included under the assessable income of the player while computation the income for the

purpose of taxation.

Answer vi

The reimbursement, allowance for employees building is dealt with under the

Taxation Ruling for TR 95/22. According the said ruling the below mentioned activities are

considered as building and construction of the employees –

Apprentice, trainees and carpenters

The site of the construction where the project managers work

Supervisor or the project manager for the building which is under construction

3 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

4 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

5TAXATION

Labours employed for the building construction5

Expenses incur with regard to the construction of apprentice for the qualification of

the building is clearly stated under the ruling as building and construction of the labours as

allowance and the compensation.

Answer vii

With regard to the expenses incurred for the purpose of short course under art

management with the expectation of becoming the art director will be allowed as deduction

provided the following conditions are fulfilled –

The expenses incurred with regard to the travelling to and from the institution of the

course

Training expenses with regard to the modules and any software

Recommended expenses incurred for meal

Expenses towards payment of fees for the short term course under art management

Further, the expenses shall be qualified for deductions if and only if the expenses

incurred in association with the short term curse on art. Moreover, if the expenses cannot be

proportionately related to the expenses associated with the course, the amount will be

disallowed as deduction. In the given case, as all the details are not provided, it can be

assumed that the expenses incurred were in association with the course only and therefore,

will be allowed as deduction.

Answer viii

As per the ATO, any artist performing and the expenses incurred with regard to the

performance will be allowed as deduction provided that the person is regarded as the

5 Chartered Accountants Australia & New Zealand (2017) CAANZ

<https://www.charteredaccountantsanz.com/>.

Labours employed for the building construction5

Expenses incur with regard to the construction of apprentice for the qualification of

the building is clearly stated under the ruling as building and construction of the labours as

allowance and the compensation.

Answer vii

With regard to the expenses incurred for the purpose of short course under art

management with the expectation of becoming the art director will be allowed as deduction

provided the following conditions are fulfilled –

The expenses incurred with regard to the travelling to and from the institution of the

course

Training expenses with regard to the modules and any software

Recommended expenses incurred for meal

Expenses towards payment of fees for the short term course under art management

Further, the expenses shall be qualified for deductions if and only if the expenses

incurred in association with the short term curse on art. Moreover, if the expenses cannot be

proportionately related to the expenses associated with the course, the amount will be

disallowed as deduction. In the given case, as all the details are not provided, it can be

assumed that the expenses incurred were in association with the course only and therefore,

will be allowed as deduction.

Answer viii

As per the ATO, any artist performing and the expenses incurred with regard to the

performance will be allowed as deduction provided that the person is regarded as the

5 Chartered Accountants Australia & New Zealand (2017) CAANZ

<https://www.charteredaccountantsanz.com/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

performing artist. As per the ATO taxation ruling the below mentioned persons will be

considered as the performing artists –

Different types of artists will be regarded as the performing artist

Any musician is considered as performing artist

The circus or dance performer will be considered as performing artist

A singer is considered as performing artist

An actor is considered as performing artist

Here in the given case the expenses incurred with regard to work dresses and work

make-up (Barkoczy, 2016). In absence of information, it is assumed as the expenses incurred

with regard to the performing artist and therefore, will be allowable as deduction under the

ATO ruling.

Answer ix

As per the general ruling the travel between home and the office is considered as the

personal expenses. However, some specific provisions are there where the expenses are

allowed as deductions as the travelling expense. If the travel is partly personal and partly

official then the official part will be allowed as deduction. However, if the travel is

exclusively fr office purpose only then the travelling expenses will be allowed as deduction.

In the given circumstance, it is assumed from the scenario that the travelling expenses were

exclusively for office purpose only and thus will be allowed as deduction while assessing the

income under taxation.

Answer x

Expenses incurred for the purpose of travelling to two different workplaces qualify for

deduction under ATO taxation ruling, provided both the workplaces are under the same

performing artist. As per the ATO taxation ruling the below mentioned persons will be

considered as the performing artists –

Different types of artists will be regarded as the performing artist

Any musician is considered as performing artist

The circus or dance performer will be considered as performing artist

A singer is considered as performing artist

An actor is considered as performing artist

Here in the given case the expenses incurred with regard to work dresses and work

make-up (Barkoczy, 2016). In absence of information, it is assumed as the expenses incurred

with regard to the performing artist and therefore, will be allowable as deduction under the

ATO ruling.

Answer ix

As per the general ruling the travel between home and the office is considered as the

personal expenses. However, some specific provisions are there where the expenses are

allowed as deductions as the travelling expense. If the travel is partly personal and partly

official then the official part will be allowed as deduction. However, if the travel is

exclusively fr office purpose only then the travelling expenses will be allowed as deduction.

In the given circumstance, it is assumed from the scenario that the travelling expenses were

exclusively for office purpose only and thus will be allowed as deduction while assessing the

income under taxation.

Answer x

Expenses incurred for the purpose of travelling to two different workplaces qualify for

deduction under ATO taxation ruling, provided both the workplaces are under the same

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

employer6. However, in the given case this deduction will not be allowed as the person

travelling to two different workplaces for two different employers. Therefore, the expenses

for travelling will not qualify for deduction as the employers are different.

6 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

employer6. However, in the given case this deduction will not be allowed as the person

travelling to two different workplaces for two different employers. Therefore, the expenses

for travelling will not qualify for deduction as the employers are different.

6 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major Australian

taxes." Treasury WP 1 (2015).

8TAXATION

QUESTION 2

To decide the assessable circumstance of an individual it is important to work out if

an individual is foreign resident or Australian resident for calculating the assessable income

under tax. A student from abroad taken admission for a course under Australian institution,

duration for which is more than six months will be accounted for as the Australian resident

for calculating the tax. The deduction can be claimed by any individual for the expenses

related to self-education if the student receives any bonded taxable scholarship or her study is

related to the work7. It is also an important factor that the course must be considerably

associated with present employment. As comprehended from the present situation Manpreet

will be accounted for as the Australian resident with the end goal of tax collection since he is

selected in a course having term of over a half year in Australian institution. Further,

Manpreet incurred some education related expenses that are not allowed as deduction under

income tax. Moreover, Manpreet also engaged himself as a part time employee under an

Australian firm from where he received monthly remuneration amounted to $45,000.

Furthermore, the self-education expenditure of $ 18,000 incurred by Manpreet will also not

qualify as deductible expense8. To get the deduction following factors must be taken into

consideration –

7 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22.1 (2013): 12-

25.

8 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing Committee on Tax

and Revenue Inquiry into the External Scrutiny of the Australian Taxation Office." (2016).

QUESTION 2

To decide the assessable circumstance of an individual it is important to work out if

an individual is foreign resident or Australian resident for calculating the assessable income

under tax. A student from abroad taken admission for a course under Australian institution,

duration for which is more than six months will be accounted for as the Australian resident

for calculating the tax. The deduction can be claimed by any individual for the expenses

related to self-education if the student receives any bonded taxable scholarship or her study is

related to the work7. It is also an important factor that the course must be considerably

associated with present employment. As comprehended from the present situation Manpreet

will be accounted for as the Australian resident with the end goal of tax collection since he is

selected in a course having term of over a half year in Australian institution. Further,

Manpreet incurred some education related expenses that are not allowed as deduction under

income tax. Moreover, Manpreet also engaged himself as a part time employee under an

Australian firm from where he received monthly remuneration amounted to $45,000.

Furthermore, the self-education expenditure of $ 18,000 incurred by Manpreet will also not

qualify as deductible expense8. To get the deduction following factors must be taken into

consideration –

7 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22.1 (2013): 12-

25.

8 Berg, Chris, and Sinclair Davidson. "Submission to the House of Representatives Standing Committee on Tax

and Revenue Inquiry into the External Scrutiny of the Australian Taxation Office." (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

The study will increase or it is expected to increase the earning from their current

employment.

Maintain or enhance the required knowledge or skills of the student necessary for the

current employment.

It is also an important factor that the course must be considerably associated with

present employment, otherwise the person will not be allowed deductions for the expenses

associated with self-education irrespective of the fact that –

It enable the person to get the opportunity for new employment

It is generally associated with the present employment

At the same rime Manpreet spend some amount towards printer and computer and

purchase of a new mobile phone, which was associated with the requirement of work. As per

the general ruling, the expenditures are qualified for deduction under the ITAA 1997, Section

8-1, if there is significant relation among the capacity of earning and expenditures and it

forms required character for the association of work and it is not in the domestic or private

nature 9

Expenditures shall be incidental and relevant with regard to the activities for

generation of income. It is not enough that the expenditures are pre-requisite for generation of

the taxable income. With regard to ITAA 1997, Section 8-1, the expenditures made for

purchasing the new mobile phone is related with earning the assessable income and therefore,

Manpreet’s expenditure will be allowable deduction under income tax. Further, it can be

identified from FC of T vs M I Roberts 92 ATC 4787 that the application of Maddalena

9 Sara McDonald Karin Simon, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au <http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174>.

The study will increase or it is expected to increase the earning from their current

employment.

Maintain or enhance the required knowledge or skills of the student necessary for the

current employment.

It is also an important factor that the course must be considerably associated with

present employment, otherwise the person will not be allowed deductions for the expenses

associated with self-education irrespective of the fact that –

It enable the person to get the opportunity for new employment

It is generally associated with the present employment

At the same rime Manpreet spend some amount towards printer and computer and

purchase of a new mobile phone, which was associated with the requirement of work. As per

the general ruling, the expenditures are qualified for deduction under the ITAA 1997, Section

8-1, if there is significant relation among the capacity of earning and expenditures and it

forms required character for the association of work and it is not in the domestic or private

nature 9

Expenditures shall be incidental and relevant with regard to the activities for

generation of income. It is not enough that the expenditures are pre-requisite for generation of

the taxable income. With regard to ITAA 1997, Section 8-1, the expenditures made for

purchasing the new mobile phone is related with earning the assessable income and therefore,

Manpreet’s expenditure will be allowable deduction under income tax. Further, it can be

identified from FC of T vs M I Roberts 92 ATC 4787 that the application of Maddalena

9 Sara McDonald Karin Simon, Accident Investigation - Databases - Library Guides At Cquniversity (2017)

Libguides.library.cqu.edu.au <http://libguides.library.cqu.edu.au/content.php?pid=166733&sid=2668174>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

principles to the federal court allowed the mine manager to get qualification for the expenses

as deductible with regard to study of MBA.

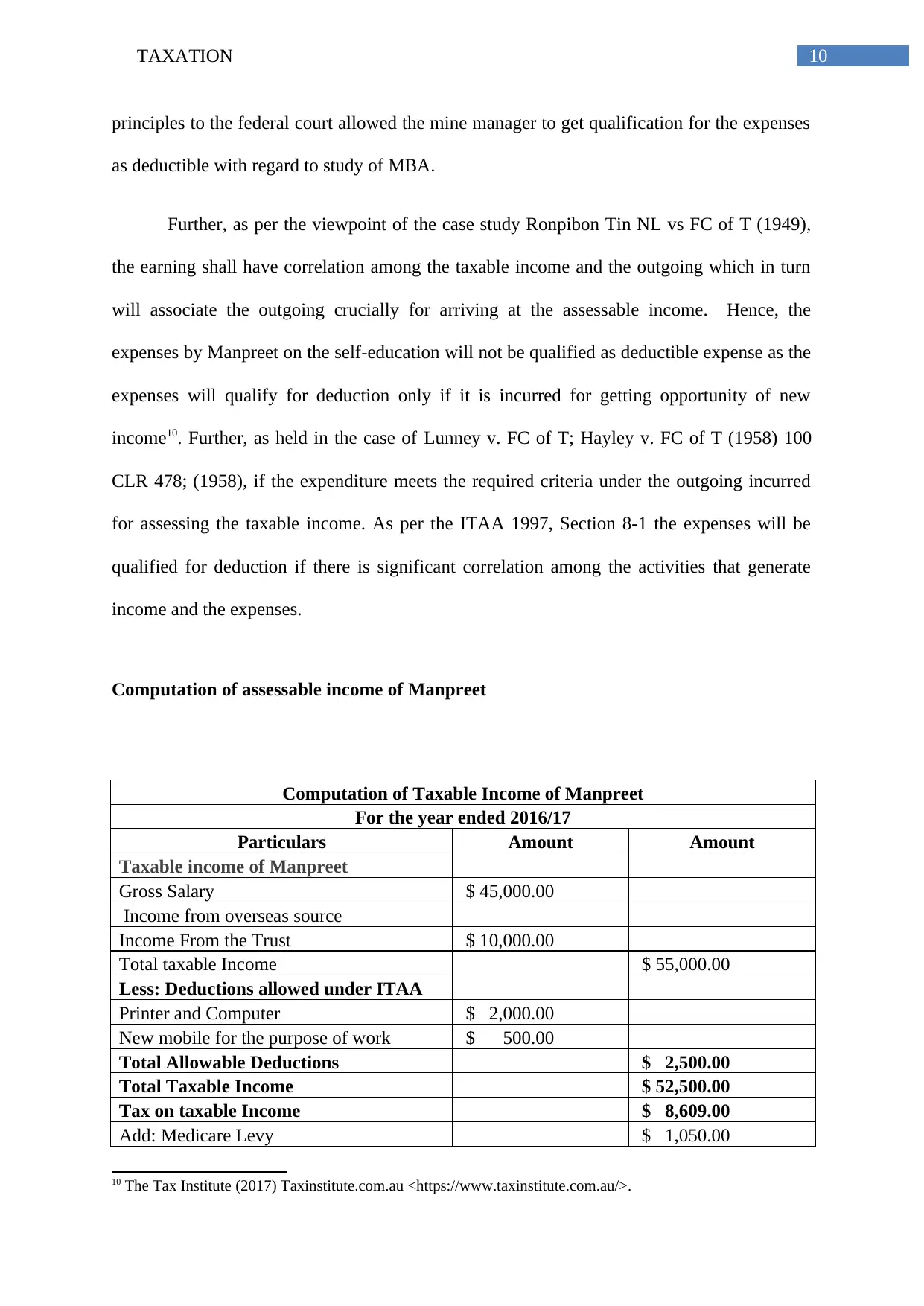

Further, as per the viewpoint of the case study Ronpibon Tin NL vs FC of T (1949),

the earning shall have correlation among the taxable income and the outgoing which in turn

will associate the outgoing crucially for arriving at the assessable income. Hence, the

expenses by Manpreet on the self-education will not be qualified as deductible expense as the

expenses will qualify for deduction only if it is incurred for getting opportunity of new

income10. Further, as held in the case of Lunney v. FC of T; Hayley v. FC of T (1958) 100

CLR 478; (1958), if the expenditure meets the required criteria under the outgoing incurred

for assessing the taxable income. As per the ITAA 1997, Section 8-1 the expenses will be

qualified for deduction if there is significant correlation among the activities that generate

income and the expenses.

Computation of assessable income of Manpreet

Computation of Taxable Income of Manpreet

For the year ended 2016/17

Particulars Amount Amount

Taxable income of Manpreet

Gross Salary $ 45,000.00

Income from overseas source

Income From the Trust $ 10,000.00

Total taxable Income $ 55,000.00

Less: Deductions allowed under ITAA

Printer and Computer $ 2,000.00

New mobile for the purpose of work $ 500.00

Total Allowable Deductions $ 2,500.00

Total Taxable Income $ 52,500.00

Tax on taxable Income $ 8,609.00

Add: Medicare Levy $ 1,050.00

10 The Tax Institute (2017) Taxinstitute.com.au <https://www.taxinstitute.com.au/>.

principles to the federal court allowed the mine manager to get qualification for the expenses

as deductible with regard to study of MBA.

Further, as per the viewpoint of the case study Ronpibon Tin NL vs FC of T (1949),

the earning shall have correlation among the taxable income and the outgoing which in turn

will associate the outgoing crucially for arriving at the assessable income. Hence, the

expenses by Manpreet on the self-education will not be qualified as deductible expense as the

expenses will qualify for deduction only if it is incurred for getting opportunity of new

income10. Further, as held in the case of Lunney v. FC of T; Hayley v. FC of T (1958) 100

CLR 478; (1958), if the expenditure meets the required criteria under the outgoing incurred

for assessing the taxable income. As per the ITAA 1997, Section 8-1 the expenses will be

qualified for deduction if there is significant correlation among the activities that generate

income and the expenses.

Computation of assessable income of Manpreet

Computation of Taxable Income of Manpreet

For the year ended 2016/17

Particulars Amount Amount

Taxable income of Manpreet

Gross Salary $ 45,000.00

Income from overseas source

Income From the Trust $ 10,000.00

Total taxable Income $ 55,000.00

Less: Deductions allowed under ITAA

Printer and Computer $ 2,000.00

New mobile for the purpose of work $ 500.00

Total Allowable Deductions $ 2,500.00

Total Taxable Income $ 52,500.00

Tax on taxable Income $ 8,609.00

Add: Medicare Levy $ 1,050.00

10 The Tax Institute (2017) Taxinstitute.com.au <https://www.taxinstitute.com.au/>.

11TAXATION

Less: Low income tax offset $ 212.50

Net Payable tax $ 9,446.50

Less: Low income tax offset $ 212.50

Net Payable tax $ 9,446.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.