Taxation Assignment 1: Income Tax and GST Calculations and Analysis

VerifiedAdded on 2019/10/31

|11

|1611

|181

Homework Assignment

AI Summary

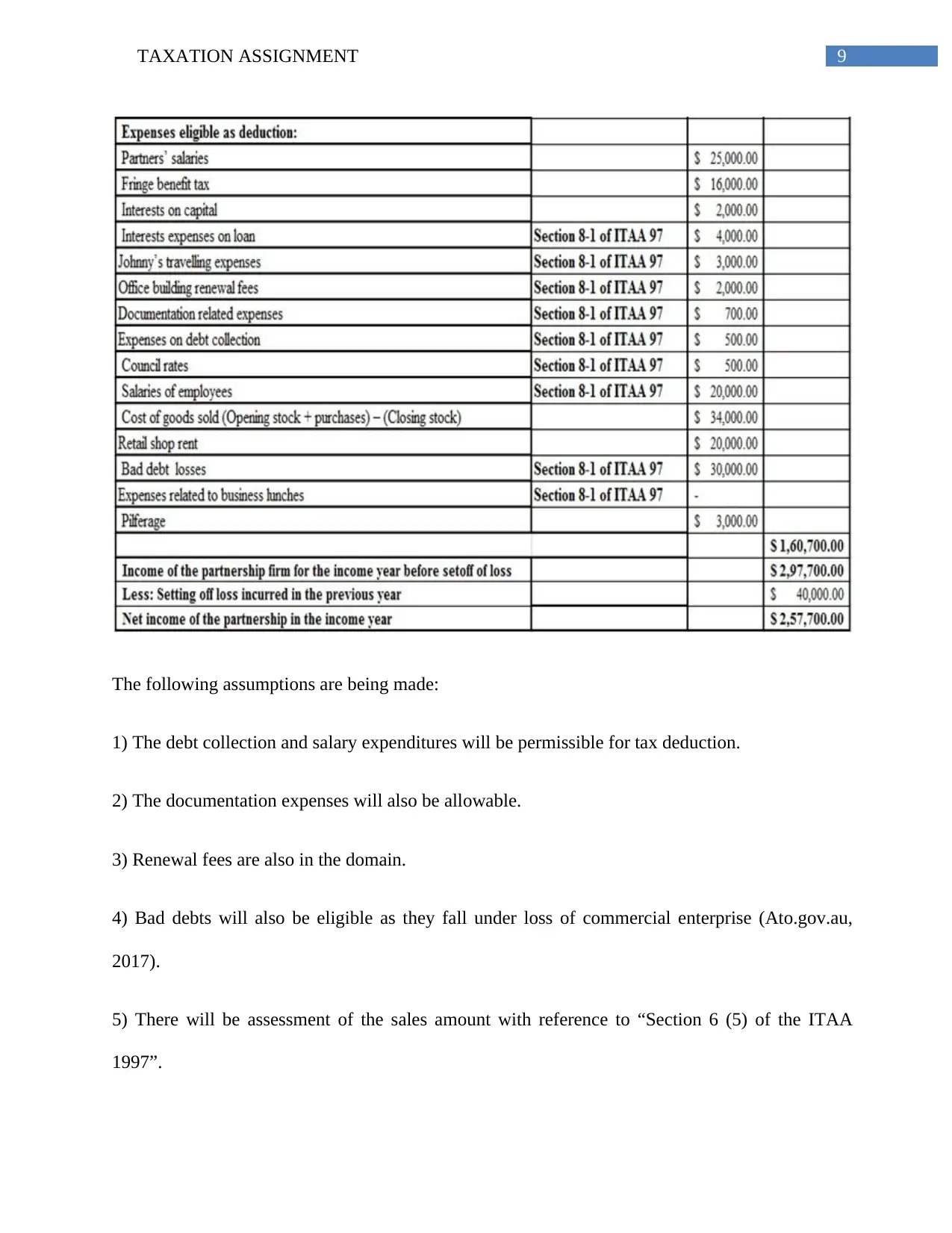

This taxation assignment solution addresses several key issues in Australian taxation law. It analyzes the deductibility of capital expenditures related to moving assets, asset revaluation expenses, and legal costs associated with business winding up and solicitor hiring. The solution references relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and case law such as British Insulated & Helsby Cables v Atherton and Sun Newspapers Ltd v F C of T to support its conclusions. Furthermore, the assignment examines the ability of a bank to claim input tax credits related to advertisement costs under the GST Act 1999, referencing GSTR 2006/3. Finally, the solution includes calculations of taxable income and net income, based on provided financial data, considering various deductions and the application of relevant tax laws and rulings. The document provides a comprehensive analysis of these taxation issues, offering insights into tax planning and compliance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.