Taxation Fundamentals: Income Tax, NIC, Avoidance Analysis

VerifiedAdded on 2023/06/15

|11

|1856

|53

Homework Assignment

AI Summary

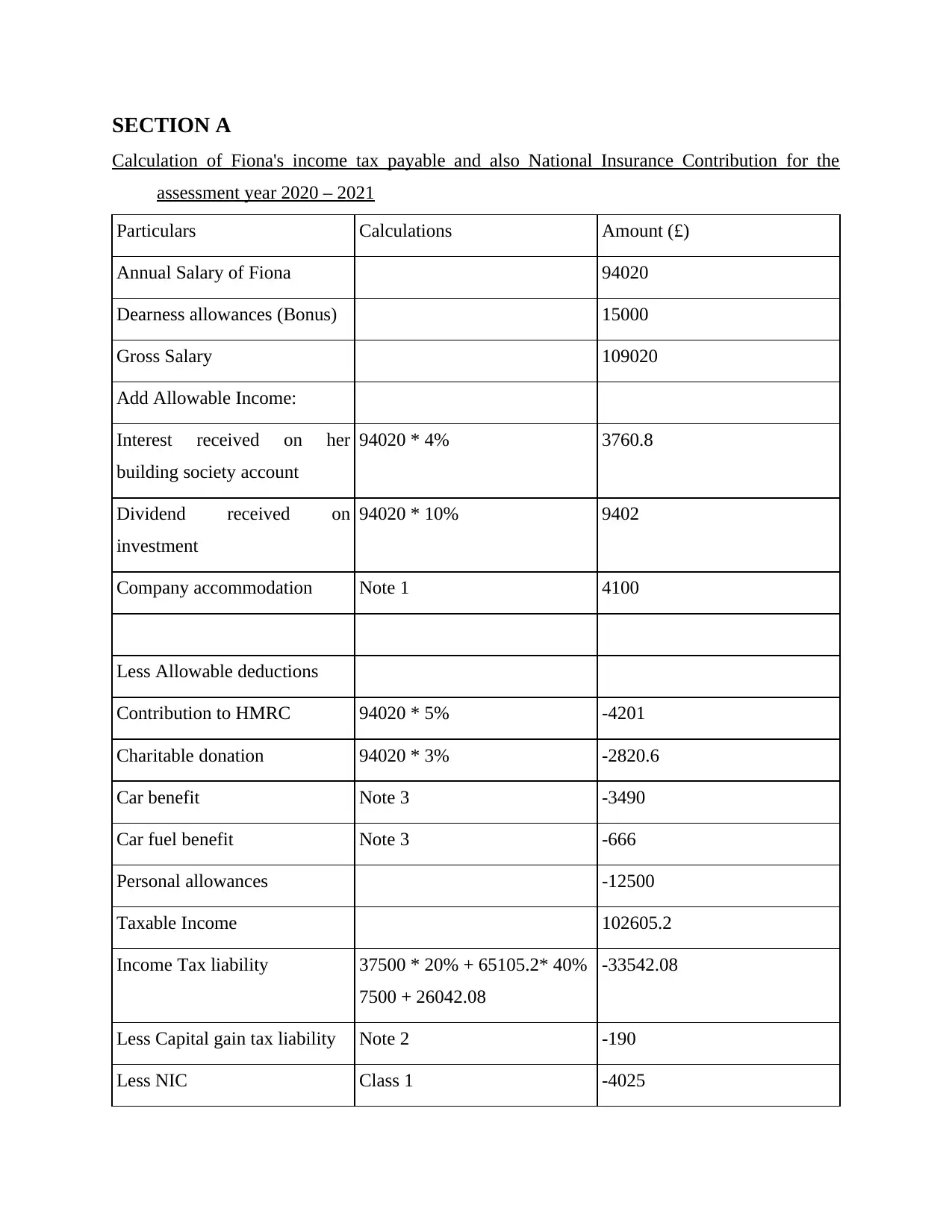

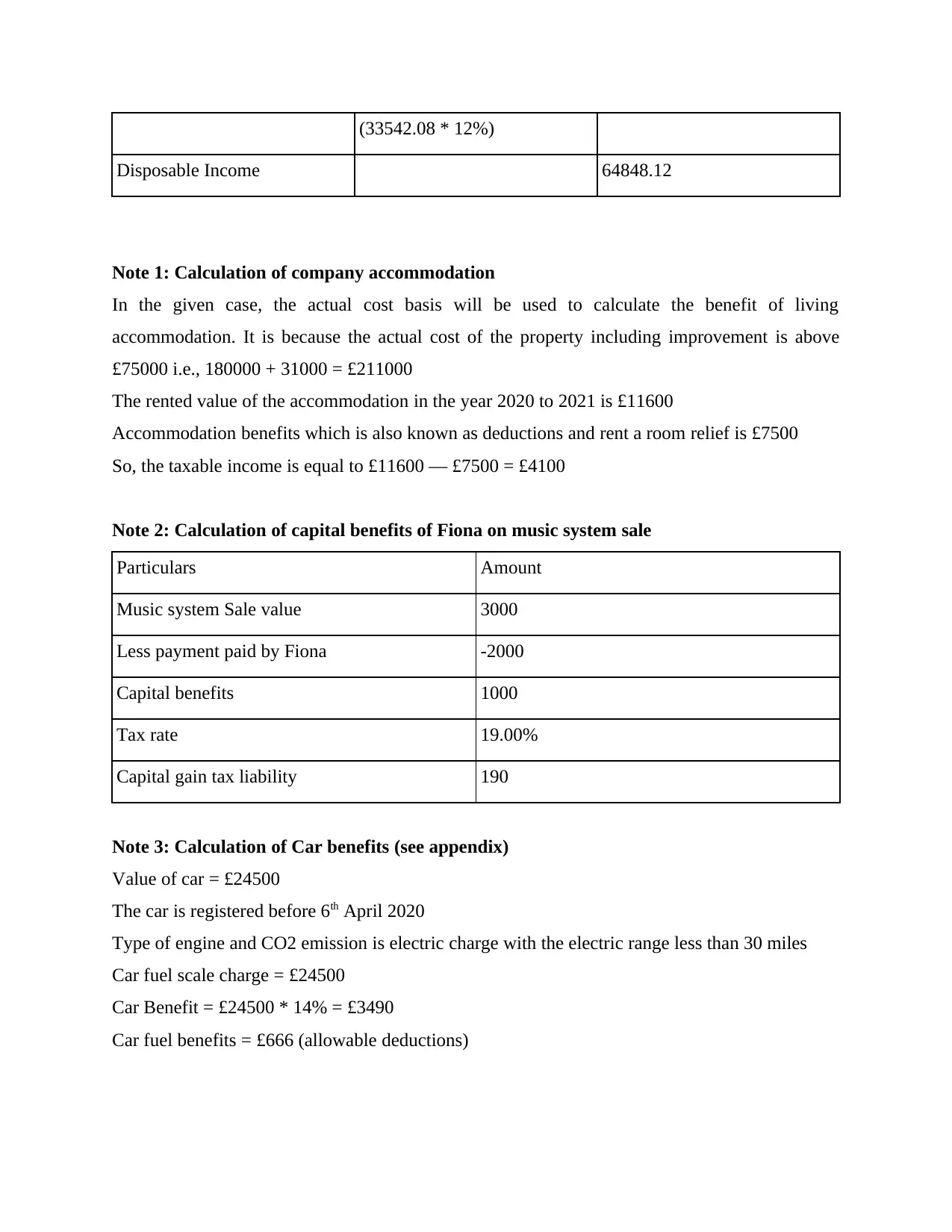

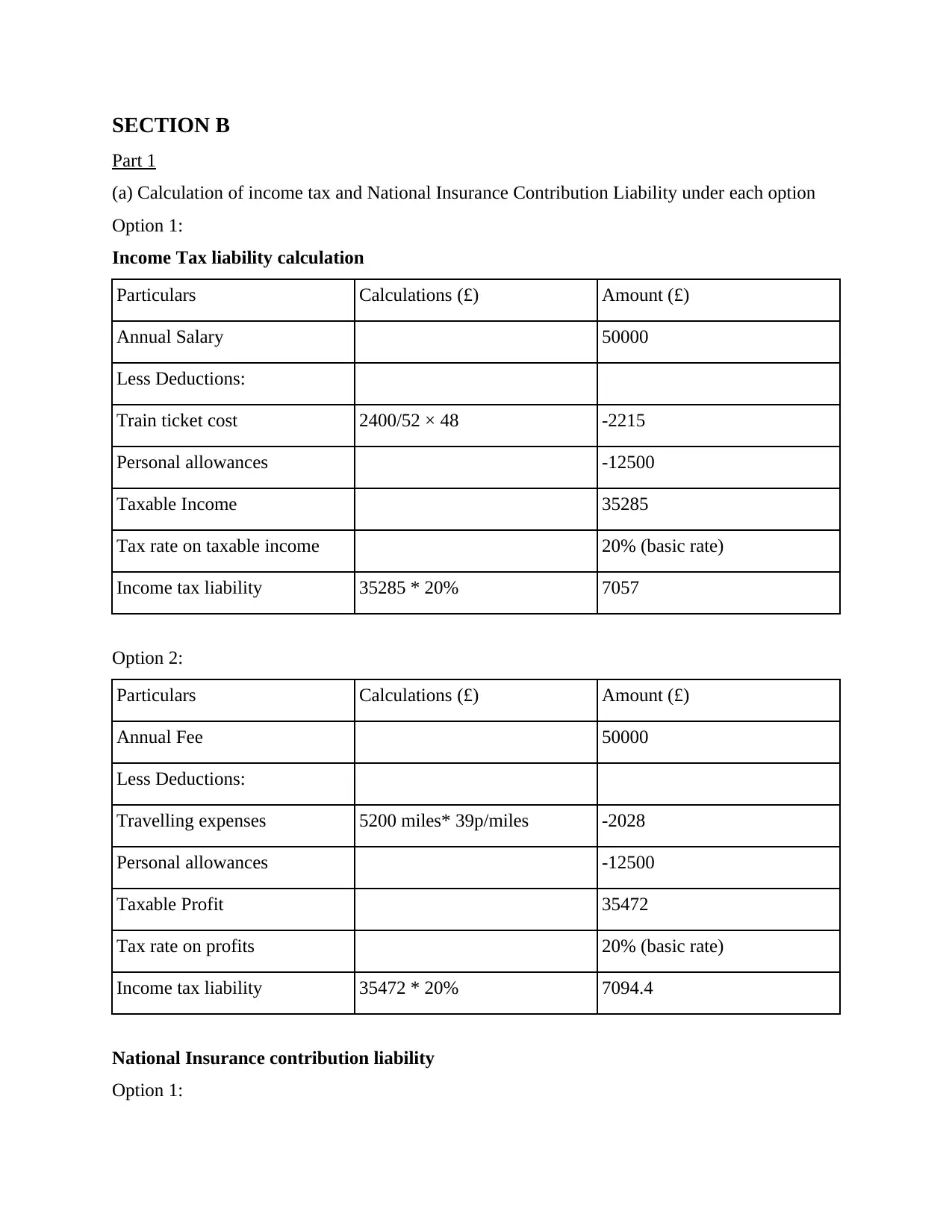

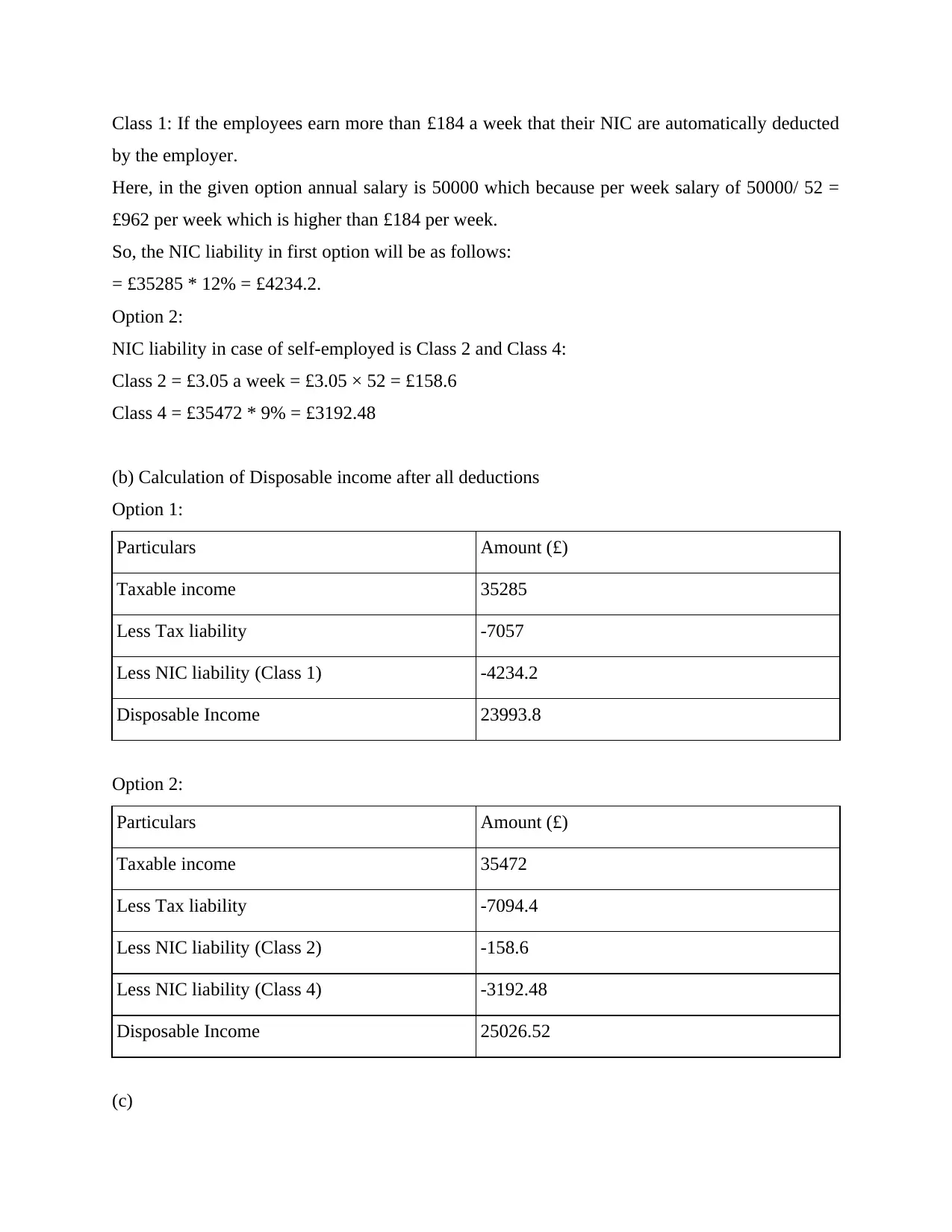

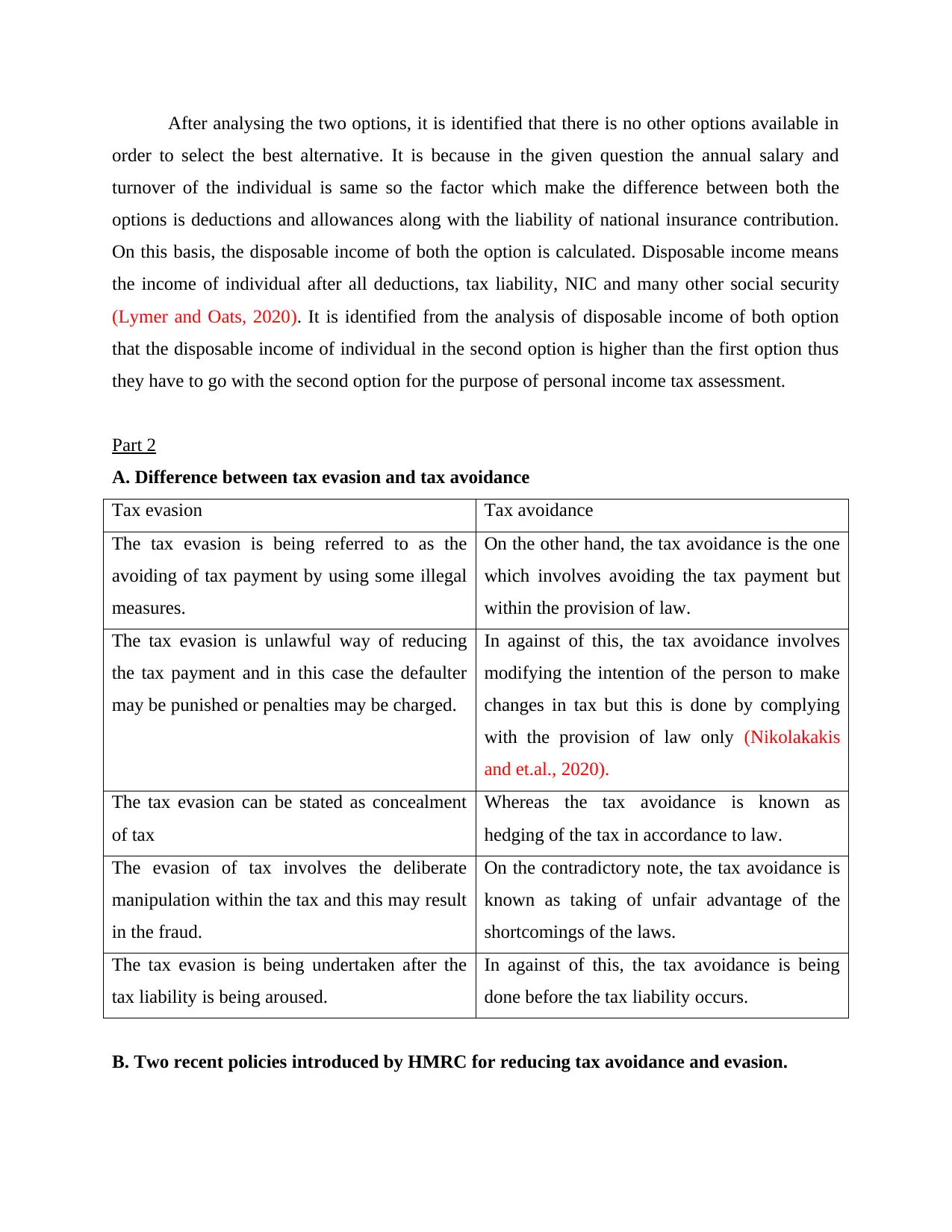

This assignment solution provides a detailed analysis of taxation fundamentals, including the calculation of Fiona's income tax payable and National Insurance Contribution for the assessment year 2020–2021. It covers various aspects such as annual salary, dearness allowances, interest received, contributions to HMRC, charitable donations, car and fuel benefits, and company accommodation. The solution also includes calculations of capital benefits, disposable income under different options, and a comparative analysis of income tax and NIC liabilities for employed and self-employed individuals. Furthermore, it discusses the differences between tax evasion and tax avoidance, recent policies introduced by HMRC to reduce tax avoidance and evasion, and an evaluation of capital gain tax versus personal income tax in property sales. The document concludes with relevant references and an appendix detailing car benefit calculations. Desklib offers a wealth of similar solved assignments and study resources to aid students in their academic pursuits.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.