Taxation Assignment: Income, Deductions, and Tax Offsets Analysis

VerifiedAdded on 2020/03/28

|12

|2158

|54

Homework Assignment

AI Summary

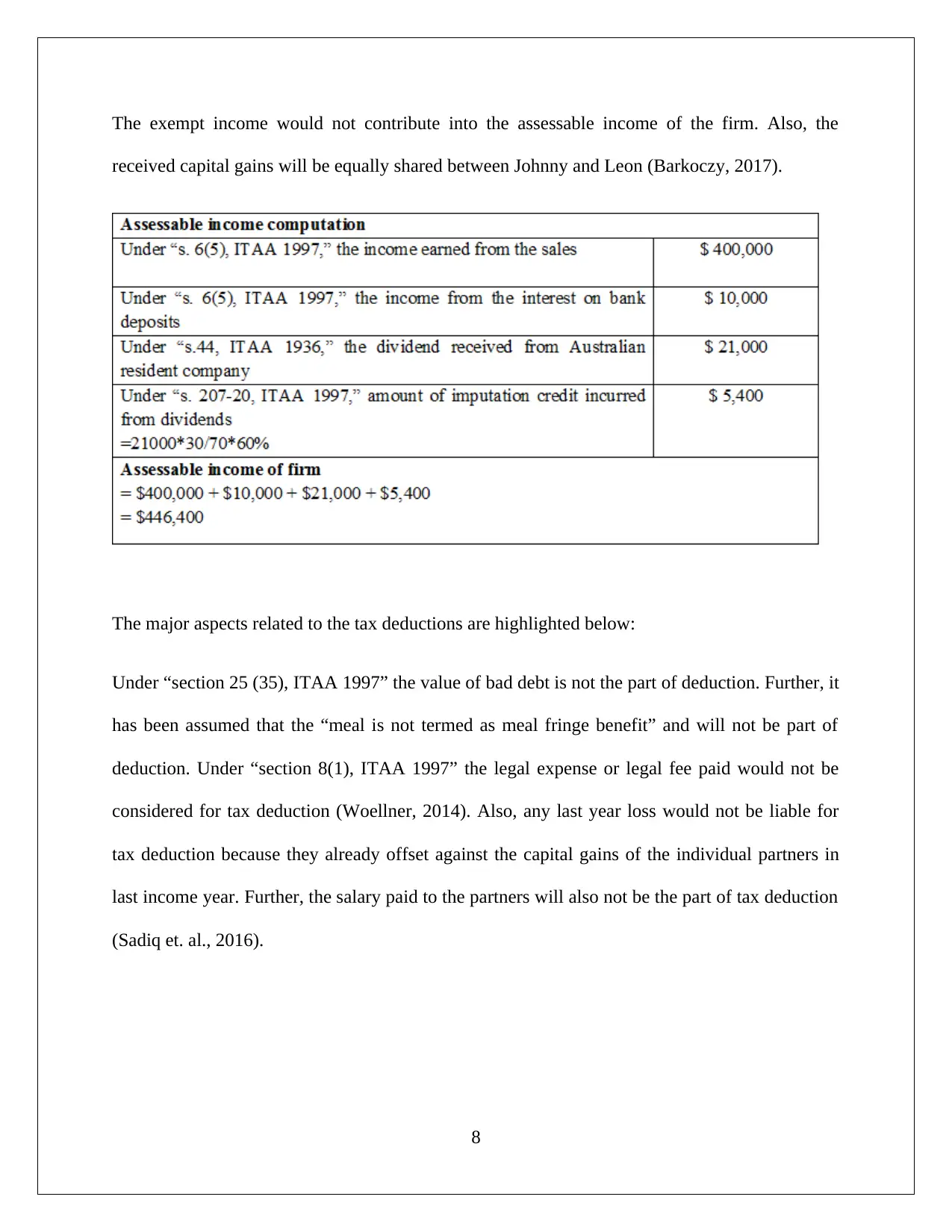

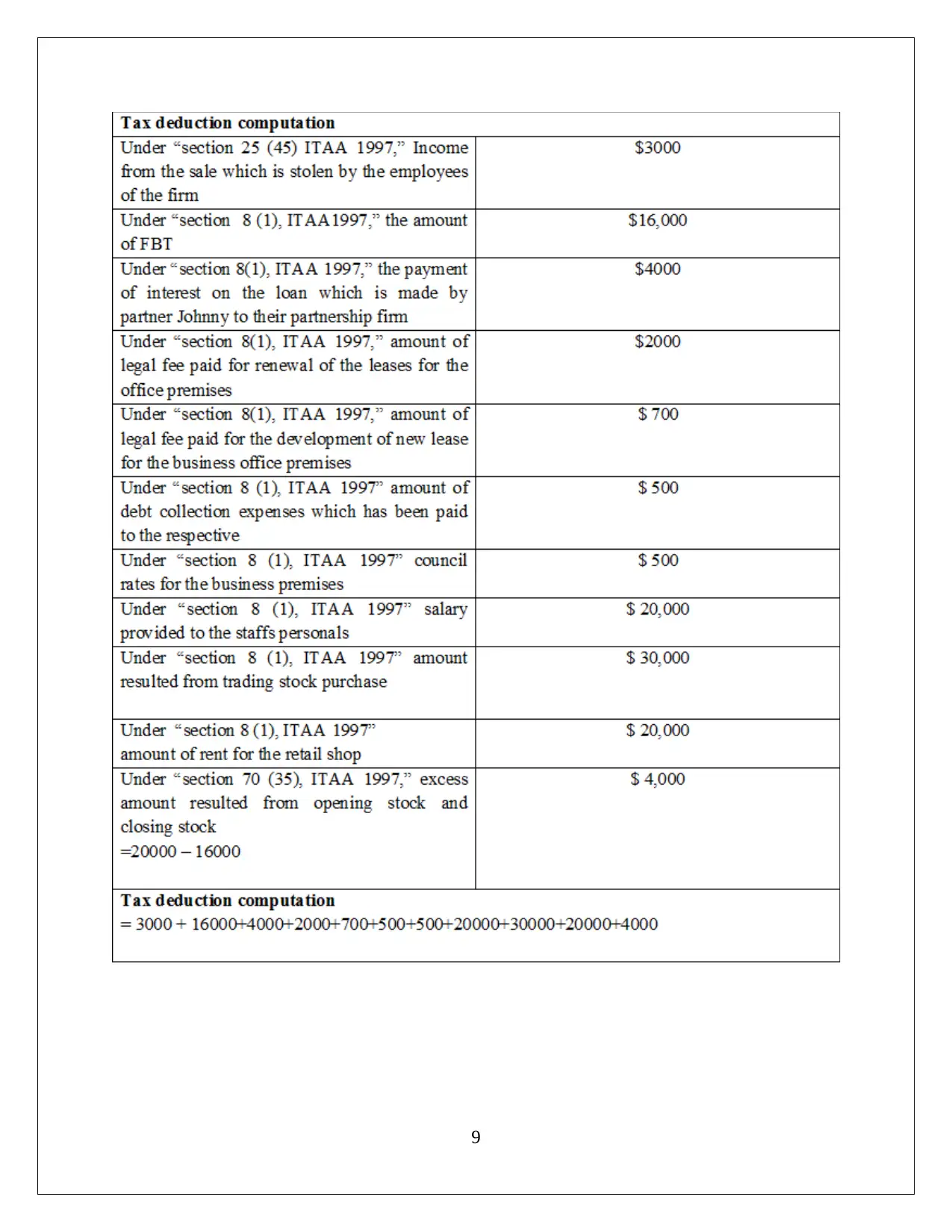

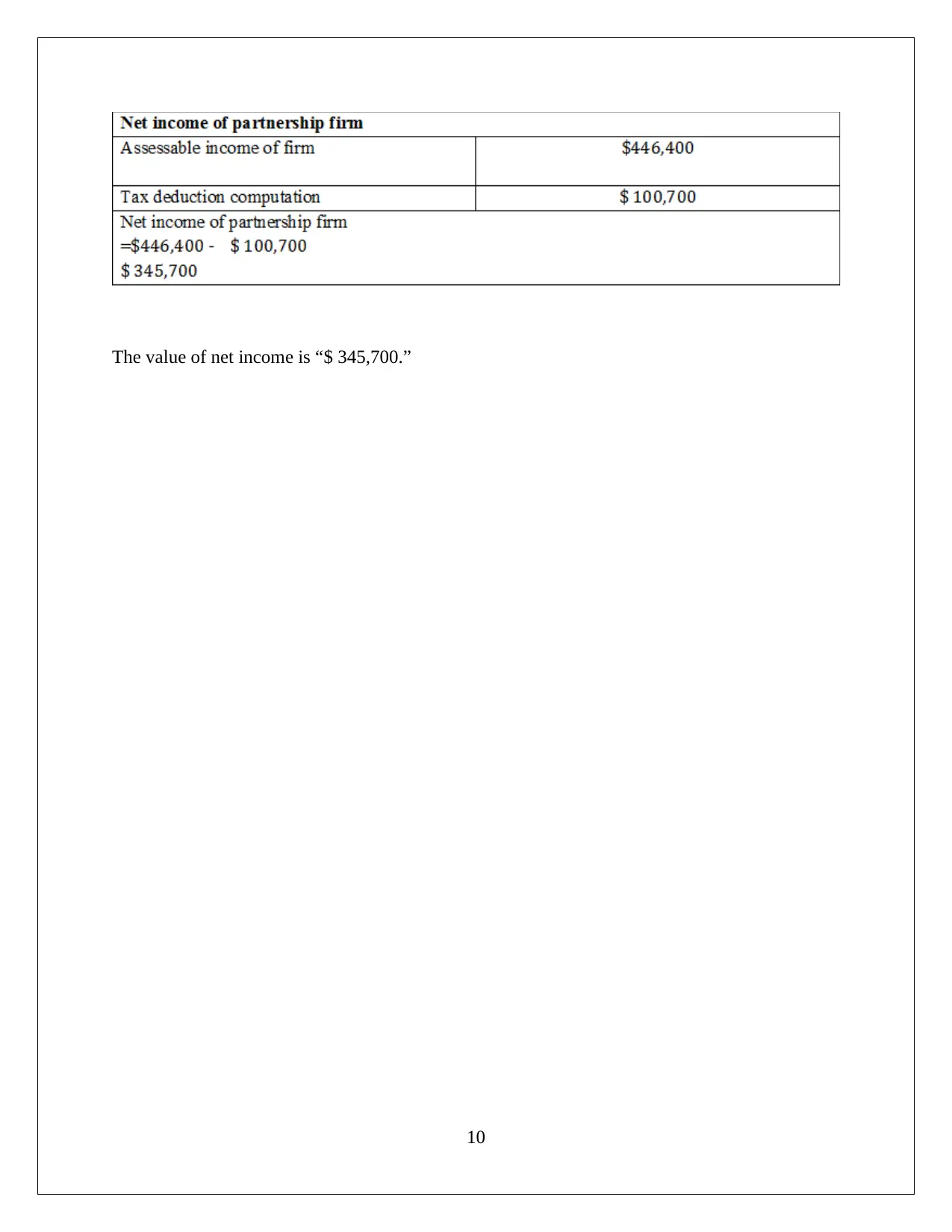

This taxation assignment analyzes several key areas of Australian tax law. Question 1 examines the deductibility of various expenses under s. 8(1) of the ITAA 1997, differentiating between capital and revenue expenses, and the impact of the underlying purpose of the expense. Question 2 focuses on GST input tax credits, particularly in the context of advertising expenditure and financial supplies, considering the Financial Acquisition Threshold (FAT). Question 3 addresses foreign tax offsets, calculating Angelo's taxable income, foreign income, and the application of foreign tax offset limits to prevent double taxation. Finally, Question 4 determines the net income of a partnership firm, identifying assessable income, non-deductible items such as bad debts and partner salaries, and the overall net income calculation.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.