TAXATION LAW 3: Comprehensive Analysis of Taxation Law Principles

VerifiedAdded on 2020/03/23

|17

|2941

|454

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing various aspects of Australian taxation. It analyzes issues related to income tax deductions, including the deductibility of expenses such as machinery relocation, asset revaluation costs, and legal expenditures incurred during business operations. The assignment references key legislation like the ITAA 1997 and relevant case law. Furthermore, it delves into the Goods and Services Tax (GST), specifically examining input tax credits for promotional and advertisement expenditures, with calculations and references to the GST Act 1999 and related rulings. The solution provides detailed explanations, applying legal principles to specific scenarios and offering conclusions on the tax implications of each issue. The assignment covers a range of topics, including the interpretation of legal precedents and the application of tax regulations to practical business situations.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to Question No 1................................................................................................................3

Requirement 1.1...........................................................................................................................3

Issue.........................................................................................................................................3

Rules:.......................................................................................................................................3

Application:.............................................................................................................................3

Conclusion...............................................................................................................................4

Requirement 1.2...........................................................................................................................4

Issue:........................................................................................................................................4

Rule:.........................................................................................................................................4

Application..............................................................................................................................4

Conclusion...............................................................................................................................5

Requirement 1.3...........................................................................................................................5

Issue.........................................................................................................................................5

Rule:.........................................................................................................................................5

Applications:............................................................................................................................5

Conclusion...............................................................................................................................6

Requirement 1.4...........................................................................................................................6

Issue.........................................................................................................................................6

Rule:.........................................................................................................................................7

TAXATION LAW

Table of Contents

Answer to Question No 1................................................................................................................3

Requirement 1.1...........................................................................................................................3

Issue.........................................................................................................................................3

Rules:.......................................................................................................................................3

Application:.............................................................................................................................3

Conclusion...............................................................................................................................4

Requirement 1.2...........................................................................................................................4

Issue:........................................................................................................................................4

Rule:.........................................................................................................................................4

Application..............................................................................................................................4

Conclusion...............................................................................................................................5

Requirement 1.3...........................................................................................................................5

Issue.........................................................................................................................................5

Rule:.........................................................................................................................................5

Applications:............................................................................................................................5

Conclusion...............................................................................................................................6

Requirement 1.4...........................................................................................................................6

Issue.........................................................................................................................................6

Rule:.........................................................................................................................................7

2

TAXATION LAW

Applications.............................................................................................................................7

Conclusion...............................................................................................................................8

Answer to Question No 2................................................................................................................9

Issue.........................................................................................................................................9

Rule:.........................................................................................................................................9

Application..............................................................................................................................9

Conclusion.............................................................................................................................11

Answer to Question No 3..............................................................................................................12

Answer to Question No 4..............................................................................................................14

Reference List................................................................................................................................15

TAXATION LAW

Applications.............................................................................................................................7

Conclusion...............................................................................................................................8

Answer to Question No 2................................................................................................................9

Issue.........................................................................................................................................9

Rule:.........................................................................................................................................9

Application..............................................................................................................................9

Conclusion.............................................................................................................................11

Answer to Question No 3..............................................................................................................12

Answer to Question No 4..............................................................................................................14

Reference List................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

Answer to Question No 1

Requirement 1.1

Issue

The problem and the challenge that has been explained with respect to this case study

tries to handle the cost of transporting the machine and obtaining allowable deductions in income

tax. There are numerous rules and laws that can be applicable with respect to the case study and

each of them are explained as follows:

Rules: “Section 8-1 of ITAA 1997” “British Insulated & Helsby Cables v. Atherton (1926)”

Application:

The generated cost due to the transporting of the machinery to a new location includes

the capital expenditure in accordance to “Section 8-1 of ITAA 1997”. It has been viewed that

“Section 8-1 of ITAA 1997” has brought about the fact that the deductions that are permissible

for the intention of income tax is granted when the expenditure is experienced for trade functions

for each day. It has further been explained that the incurred expenditure for relocating the

machinery to its new site presents a minimal transition, which may not be permitted for any

deductions and thereby raises cost of depreciation.

As cited in the “Taxation Ruling of TD 93/123” the expenses that are associated in

installing the machine and initiation the process of manufacturing and discloses the profit and

thereby leads to a rise in the benefit of the operations of the business (Watts 2015). Hence,

according to “Section 8-1 of ITAA 1997” the relocation expenditure for the machinery in the

TAXATION LAW

Answer to Question No 1

Requirement 1.1

Issue

The problem and the challenge that has been explained with respect to this case study

tries to handle the cost of transporting the machine and obtaining allowable deductions in income

tax. There are numerous rules and laws that can be applicable with respect to the case study and

each of them are explained as follows:

Rules: “Section 8-1 of ITAA 1997” “British Insulated & Helsby Cables v. Atherton (1926)”

Application:

The generated cost due to the transporting of the machinery to a new location includes

the capital expenditure in accordance to “Section 8-1 of ITAA 1997”. It has been viewed that

“Section 8-1 of ITAA 1997” has brought about the fact that the deductions that are permissible

for the intention of income tax is granted when the expenditure is experienced for trade functions

for each day. It has further been explained that the incurred expenditure for relocating the

machinery to its new site presents a minimal transition, which may not be permitted for any

deductions and thereby raises cost of depreciation.

As cited in the “Taxation Ruling of TD 93/123” the expenses that are associated in

installing the machine and initiation the process of manufacturing and discloses the profit and

thereby leads to a rise in the benefit of the operations of the business (Watts 2015). Hence,

according to “Section 8-1 of ITAA 1997” the relocation expenditure for the machinery in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

new region is the capital expenses and therefore no allowable deductions can be provided in this

scenario. According to “British Insulated &Helsby Cables v. Atherton (1926)”, there has been a

rise the profit for the business and due to the transformation of the assets that are in nature

depreciable for the organization (Hopkins 2016).

Conclusion

The explanation of the “Section 8-1 of ITAA 1997” with respect to the expenses of

relocating the machinery to the new site has been explained as the cost of capital that has been

not permitted for the deductions in the income tax.

Requirement 1.2

Issue:

The area that has been discussed in this issue is the impact of the coverage of insurance in

the asset revaluation and would be signified as allowable deductions of income tax with respect

to “Section 8-1 of ITAA 1997”. The rules and the laws that are applicable to this scenario are

given below:

Rule: “Section 8-1 of ITAA 1997”

Application

The scenario has explained that the expenses has connections with the cost of recurring.

Therefore, during the time of determining the overall value of permissible business subtractions,

it has been imperious for the firm to determine the fact that the expenditure gained during the

asset revaluation method, which raises the earnings of the firm and the expenditure that has taken

place during the method of securing the asset (Niazi and Krever 2017). In the scenario that the

TAXATION LAW

new region is the capital expenses and therefore no allowable deductions can be provided in this

scenario. According to “British Insulated &Helsby Cables v. Atherton (1926)”, there has been a

rise the profit for the business and due to the transformation of the assets that are in nature

depreciable for the organization (Hopkins 2016).

Conclusion

The explanation of the “Section 8-1 of ITAA 1997” with respect to the expenses of

relocating the machinery to the new site has been explained as the cost of capital that has been

not permitted for the deductions in the income tax.

Requirement 1.2

Issue:

The area that has been discussed in this issue is the impact of the coverage of insurance in

the asset revaluation and would be signified as allowable deductions of income tax with respect

to “Section 8-1 of ITAA 1997”. The rules and the laws that are applicable to this scenario are

given below:

Rule: “Section 8-1 of ITAA 1997”

Application

The scenario has explained that the expenses has connections with the cost of recurring.

Therefore, during the time of determining the overall value of permissible business subtractions,

it has been imperious for the firm to determine the fact that the expenditure gained during the

asset revaluation method, which raises the earnings of the firm and the expenditure that has taken

place during the method of securing the asset (Niazi and Krever 2017). In the scenario that the

5

TAXATION LAW

revaluation expenses of the asset is ascertained that is of nature recurring and has been regarded

as deductions that are permissible for the intention of income tax that are under the “Section 8-1

of the ITAA 1997”.

Conclusion

In regards to “Section 8-1 of ITAA 1997”, it has been explained that the asset revaluation

has a significant impact on the coverage of the insurance and is taken as a deduction for income

tax. The key factor for including the deductions for the income tax has been due to the fact that

the expense possesses the nature of recurrence features.

Requirement 1.3

Issue

The problem that has been explained in this case study has been managing the challenges

related to the legal expenditure that has taken place during the method of closing down the

business of the organization. Therefore, the legal expenditure has been found to be deductions

that are non-allowable in accordance to “Section 8-1 of ITAA 1997”. The laws and the rules that

are associated with this scenario are as follows:

Rule:

Sun Newspaper Ltd v F C of T (1938)

Section 8-1 of the ITAA 1997

Applications:

The Taxation Ruling of ID 2004/367 describes that there are certain legal expenditure

that that can be claimed for the purpose of deductions in relation to the business. In accordance

to “Sun Newspaper Ltd v F C of T (1938)” the verdicts have explained that when the legal cost

TAXATION LAW

revaluation expenses of the asset is ascertained that is of nature recurring and has been regarded

as deductions that are permissible for the intention of income tax that are under the “Section 8-1

of the ITAA 1997”.

Conclusion

In regards to “Section 8-1 of ITAA 1997”, it has been explained that the asset revaluation

has a significant impact on the coverage of the insurance and is taken as a deduction for income

tax. The key factor for including the deductions for the income tax has been due to the fact that

the expense possesses the nature of recurrence features.

Requirement 1.3

Issue

The problem that has been explained in this case study has been managing the challenges

related to the legal expenditure that has taken place during the method of closing down the

business of the organization. Therefore, the legal expenditure has been found to be deductions

that are non-allowable in accordance to “Section 8-1 of ITAA 1997”. The laws and the rules that

are associated with this scenario are as follows:

Rule:

Sun Newspaper Ltd v F C of T (1938)

Section 8-1 of the ITAA 1997

Applications:

The Taxation Ruling of ID 2004/367 describes that there are certain legal expenditure

that that can be claimed for the purpose of deductions in relation to the business. In accordance

to “Sun Newspaper Ltd v F C of T (1938)” the verdicts have explained that when the legal cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

is devoted towards the course of the structural intention more than for the intention that is

operational in nature, then the expenditure and the outflows would be considered as capital

expenditure (Lang 2014). Due to this outcome, these expenditures would not be regarded for the

intention of income tax deductions. There are distinct legal expenditure that has been acquired

during the operations of the organization are generally considered for deductions in the earnings

with respect to “Section 8-1 of ITAA 1997”. Furthermore, it is authoritative to ascertain the

features of the legal costs during the claims for deductions related to the income tax. By

undertaking the activities of the solicitor is presented as the organizational expenses that is

associated directly to the creation of the earnings of the firm (Mumford 2014). It is due to this

effect, that the expenses would be permissible for the determination of the income tax as it has

been gained from the business operations of the firm.

Conclusion

By looking at the citations given in the explanations that have been given earlier and

seeking assistance of “Section 8-1 of ITAA 1997”, it can be depicted that the expenses of the

solicitor can be taken into consideration for deductions that are permissible.

Requirement 1.4

Issue

The statement of the problem has brought forward the problem that the legal expenditure

payment given to the solicitor is determined as deductions that are permissible with respect to

“Section 8-1 of the ITAA 1997”. The rules associated with this case study will be given as

follows:

TAXATION LAW

is devoted towards the course of the structural intention more than for the intention that is

operational in nature, then the expenditure and the outflows would be considered as capital

expenditure (Lang 2014). Due to this outcome, these expenditures would not be regarded for the

intention of income tax deductions. There are distinct legal expenditure that has been acquired

during the operations of the organization are generally considered for deductions in the earnings

with respect to “Section 8-1 of ITAA 1997”. Furthermore, it is authoritative to ascertain the

features of the legal costs during the claims for deductions related to the income tax. By

undertaking the activities of the solicitor is presented as the organizational expenses that is

associated directly to the creation of the earnings of the firm (Mumford 2014). It is due to this

effect, that the expenses would be permissible for the determination of the income tax as it has

been gained from the business operations of the firm.

Conclusion

By looking at the citations given in the explanations that have been given earlier and

seeking assistance of “Section 8-1 of ITAA 1997”, it can be depicted that the expenses of the

solicitor can be taken into consideration for deductions that are permissible.

Requirement 1.4

Issue

The statement of the problem has brought forward the problem that the legal expenditure

payment given to the solicitor is determined as deductions that are permissible with respect to

“Section 8-1 of the ITAA 1997”. The rules associated with this case study will be given as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

Rule: Section 8-1 of the ITAA 1997 Herald and Weekly Times v F C of T (1962)

Applications

In the context of “Section 8-1 of ITAA 1997” where it has been explained precisely that

the legal expenses that has taken place for the discharging of the organizational business

functions that creates a section of the each day activities of the taxpaying individuals that are

specifically regarded for deductions (Dicey 2017). There is even an exemption to the matter,

which has been that the expenditure are nationalised or the carrying factor of the private

expenditure or gained for the manufacture of the income that is non-exempted and in this respect

they are considered for deductions in the income tax. By looking at the decisions that has been

described in the case study of “Herald & Weekly Times v F C of T (1932)” the expenses that are

in nature legal with respect to “Section 8-1 of the ITAA 1997” and has been experienced from

the regular operations of the business then it would be looked upon as deductions for income tax

(Aroney et al. 2015).

The current case study has highlighted that the legal cost for engaging the service of the

solicitor in accordance to numerous business operations would be looked upon as allowable

income tax deductions with respect to “Section 8-1 of ITAA 1997”. The solicitor’s service

expresses the expenditure that are associated directly for the emancipation of the functions of the

business and therefore it would be looked upon as the deductions for the intention of income tax.

TAXATION LAW

Rule: Section 8-1 of the ITAA 1997 Herald and Weekly Times v F C of T (1962)

Applications

In the context of “Section 8-1 of ITAA 1997” where it has been explained precisely that

the legal expenses that has taken place for the discharging of the organizational business

functions that creates a section of the each day activities of the taxpaying individuals that are

specifically regarded for deductions (Dicey 2017). There is even an exemption to the matter,

which has been that the expenditure are nationalised or the carrying factor of the private

expenditure or gained for the manufacture of the income that is non-exempted and in this respect

they are considered for deductions in the income tax. By looking at the decisions that has been

described in the case study of “Herald & Weekly Times v F C of T (1932)” the expenses that are

in nature legal with respect to “Section 8-1 of the ITAA 1997” and has been experienced from

the regular operations of the business then it would be looked upon as deductions for income tax

(Aroney et al. 2015).

The current case study has highlighted that the legal cost for engaging the service of the

solicitor in accordance to numerous business operations would be looked upon as allowable

income tax deductions with respect to “Section 8-1 of ITAA 1997”. The solicitor’s service

expresses the expenditure that are associated directly for the emancipation of the functions of the

business and therefore it would be looked upon as the deductions for the intention of income tax.

8

TAXATION LAW

Conclusion

As described from the case study that has been undertaken before, the legal expenditure

for the solicitor’s services in the discharging of the various activities that are associated with the

everyday operations and this would be considered as deductions under “Section 8-1 of ITAA

1997”.

TAXATION LAW

Conclusion

As described from the case study that has been undertaken before, the legal expenditure

for the solicitor’s services in the discharging of the various activities that are associated with the

everyday operations and this would be considered as deductions under “Section 8-1 of ITAA

1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Answer to Question No 2

Issue

The statement of the issue of the case scenario has been reliant on the determination of

the prerogative of the promotional and advertisement expenditures that have been paid by Big

Bank Ltd with respect to the “Legislation of GSTRAct 1999”. There are certain rules that are

applicable with respect to the scenario as well and they have been laid down as follows:

Rule: “GST Act 1999” Paragraphs 11-5 and 15-5 Subsection 15-25 “Goods and Services Tax ruling of GSTR 2006/3” “Ronpibon Tin NL v F C of T”

Application

The statement of the issue that is in relation to Big Bank Ltd looks for the determination

of the input tax credit with the incorporation of “Taxation Ruling of GSTR 2006/03”. The

“GSTR 2006/3” is apprehensive with the method that requires to be incorporated in the current

scenario of Big Bank in order to determine the volume of the input tax credit for the value of the

financial supplies that is undertaken by Big Bank along with the value that is inclusive of the

“GST Act 1999”. The legislation of GST distinctly put forth the level of ascertaining the

creditable intentions and it is found in Section 11-15 and 129 of the GST Act (McGee, Devos

and Benk 2016). The entities that are taxable require to be listed or they may even get the

registration in accordance to GST Act 1999 and have even exceeded the limit of the financial

TAXATION LAW

Answer to Question No 2

Issue

The statement of the issue of the case scenario has been reliant on the determination of

the prerogative of the promotional and advertisement expenditures that have been paid by Big

Bank Ltd with respect to the “Legislation of GSTRAct 1999”. There are certain rules that are

applicable with respect to the scenario as well and they have been laid down as follows:

Rule: “GST Act 1999” Paragraphs 11-5 and 15-5 Subsection 15-25 “Goods and Services Tax ruling of GSTR 2006/3” “Ronpibon Tin NL v F C of T”

Application

The statement of the issue that is in relation to Big Bank Ltd looks for the determination

of the input tax credit with the incorporation of “Taxation Ruling of GSTR 2006/03”. The

“GSTR 2006/3” is apprehensive with the method that requires to be incorporated in the current

scenario of Big Bank in order to determine the volume of the input tax credit for the value of the

financial supplies that is undertaken by Big Bank along with the value that is inclusive of the

“GST Act 1999”. The legislation of GST distinctly put forth the level of ascertaining the

creditable intentions and it is found in Section 11-15 and 129 of the GST Act (McGee, Devos

and Benk 2016). The entities that are taxable require to be listed or they may even get the

registration in accordance to GST Act 1999 and have even exceeded the limit of the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

acquisition. The “Goods and Service Tax Ruling of GSTR 2006/3” distinctly puts forth that the

entities of the business requires to gain the registration in accordance to GST Act 1997 for the

GST value that is included in the financial supplies that are undertaken (Joseph 2017). Hence, as

an outcome, the organizations that are registered would be liable to claim input credit tax.

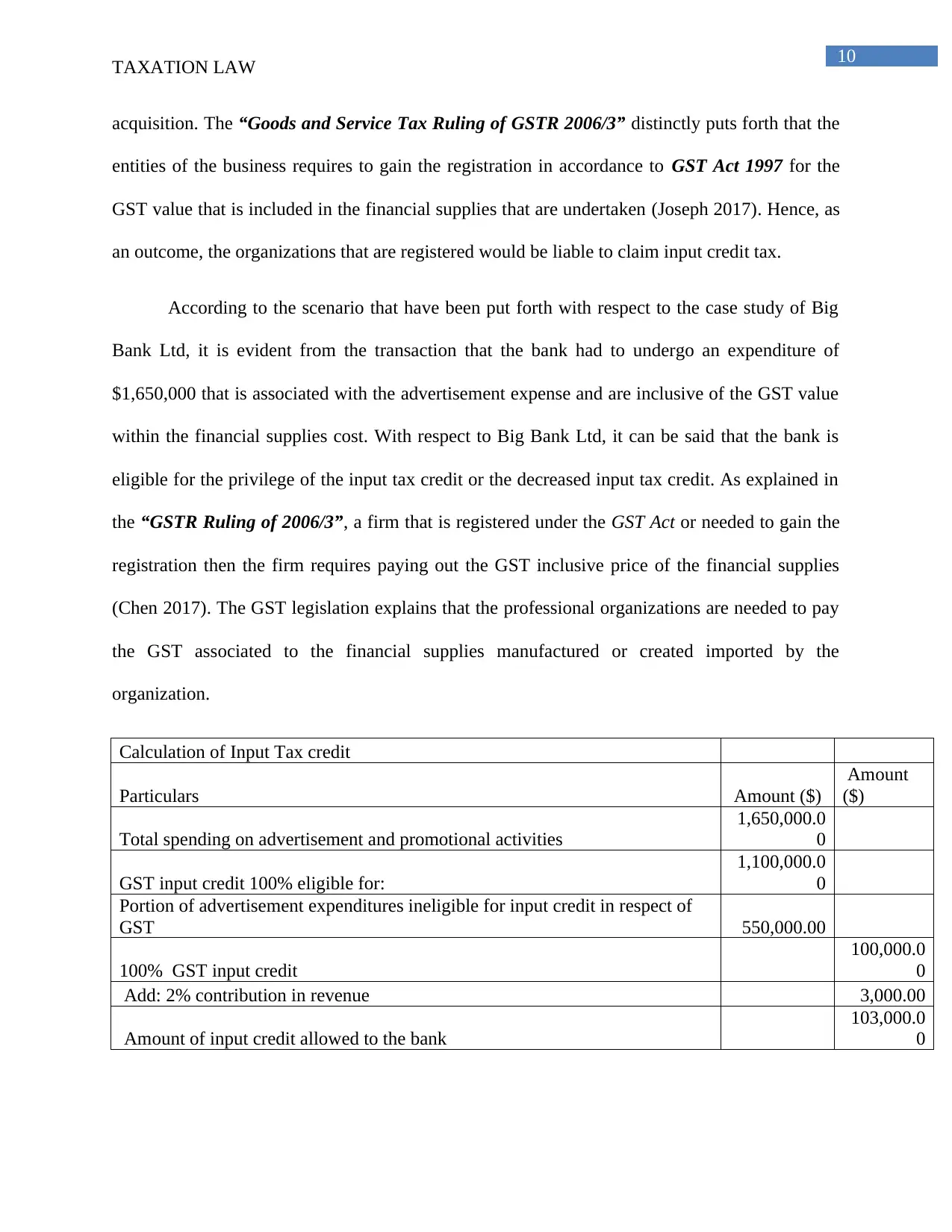

According to the scenario that have been put forth with respect to the case study of Big

Bank Ltd, it is evident from the transaction that the bank had to undergo an expenditure of

$1,650,000 that is associated with the advertisement expense and are inclusive of the GST value

within the financial supplies cost. With respect to Big Bank Ltd, it can be said that the bank is

eligible for the privilege of the input tax credit or the decreased input tax credit. As explained in

the “GSTR Ruling of 2006/3”, a firm that is registered under the GST Act or needed to gain the

registration then the firm requires paying out the GST inclusive price of the financial supplies

(Chen 2017). The GST legislation explains that the professional organizations are needed to pay

the GST associated to the financial supplies manufactured or created imported by the

organization.

Calculation of Input Tax credit

Particulars Amount ($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000.0

0

GST input credit 100% eligible for:

1,100,000.0

0

Portion of advertisement expenditures ineligible for input credit in respect of

GST 550,000.00

100% GST input credit

100,000.0

0

Add: 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

TAXATION LAW

acquisition. The “Goods and Service Tax Ruling of GSTR 2006/3” distinctly puts forth that the

entities of the business requires to gain the registration in accordance to GST Act 1997 for the

GST value that is included in the financial supplies that are undertaken (Joseph 2017). Hence, as

an outcome, the organizations that are registered would be liable to claim input credit tax.

According to the scenario that have been put forth with respect to the case study of Big

Bank Ltd, it is evident from the transaction that the bank had to undergo an expenditure of

$1,650,000 that is associated with the advertisement expense and are inclusive of the GST value

within the financial supplies cost. With respect to Big Bank Ltd, it can be said that the bank is

eligible for the privilege of the input tax credit or the decreased input tax credit. As explained in

the “GSTR Ruling of 2006/3”, a firm that is registered under the GST Act or needed to gain the

registration then the firm requires paying out the GST inclusive price of the financial supplies

(Chen 2017). The GST legislation explains that the professional organizations are needed to pay

the GST associated to the financial supplies manufactured or created imported by the

organization.

Calculation of Input Tax credit

Particulars Amount ($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000.0

0

GST input credit 100% eligible for:

1,100,000.0

0

Portion of advertisement expenditures ineligible for input credit in respect of

GST 550,000.00

100% GST input credit

100,000.0

0

Add: 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

11

TAXATION LAW

In compliance to the case of “Ronpibon Tin NL v. F C of T”, the standards of the level

and to the degree are implied with the goal of assessing the GST Act. The judgment explained in

this case efficiently to put forth the suitable processes of allotment that logically requires to be

incorporated by the company. It has been explained under the paragraph 11-5 and the 15-5 of the

GST Act 1999, the possession to be eligible for the intention of taking credit and the process of

taking credit should be temporarily and permanently for the intention of credit. With respect to

the present scenario of Big Bank Ltd, it has been discovered that the supply of finance provided

by the bank has overgrown the financial credit entry limit (Miller and Oats 2016). In order to be

eligible for the input credit tax, Big Bank can claim temporarily for the financial credit requested

by it. In compliance with Section 11-5 and 15-10 of the “GSTR Ruling of 2006/3” it can be

defined that the financial purchases undertaken by the organization would be able to ask for the

privilege of the input tax credit in accordance to the financial supplies undertaken by it.

As explained in the present scenario of Big Bank Ltd, the advertisement and the expenditure that

incurs for the intention of credit will be qualified for obtaining the input tax credit. With respect

to the “Taxation Ruling of GSTR 2006/3”, it can be said that Big Bank meets the criteria of

claiming input tax credit in association to the financial supplies that have been undertaken by the

bank.

Conclusion

With respect to the explanation received from the analysis undertaken above in regards to

Big Bank Ltd, it can be explained that Big Bank Ltd would be eligible for bringing forward the

requests of gaining the input tax credit. The financial supplies undertaken with the structure of

the “Goods and service tax ruling of GSTR 2006/3” associated with the value that has been

added in the financial supply price undertaken by the bank.

TAXATION LAW

In compliance to the case of “Ronpibon Tin NL v. F C of T”, the standards of the level

and to the degree are implied with the goal of assessing the GST Act. The judgment explained in

this case efficiently to put forth the suitable processes of allotment that logically requires to be

incorporated by the company. It has been explained under the paragraph 11-5 and the 15-5 of the

GST Act 1999, the possession to be eligible for the intention of taking credit and the process of

taking credit should be temporarily and permanently for the intention of credit. With respect to

the present scenario of Big Bank Ltd, it has been discovered that the supply of finance provided

by the bank has overgrown the financial credit entry limit (Miller and Oats 2016). In order to be

eligible for the input credit tax, Big Bank can claim temporarily for the financial credit requested

by it. In compliance with Section 11-5 and 15-10 of the “GSTR Ruling of 2006/3” it can be

defined that the financial purchases undertaken by the organization would be able to ask for the

privilege of the input tax credit in accordance to the financial supplies undertaken by it.

As explained in the present scenario of Big Bank Ltd, the advertisement and the expenditure that

incurs for the intention of credit will be qualified for obtaining the input tax credit. With respect

to the “Taxation Ruling of GSTR 2006/3”, it can be said that Big Bank meets the criteria of

claiming input tax credit in association to the financial supplies that have been undertaken by the

bank.

Conclusion

With respect to the explanation received from the analysis undertaken above in regards to

Big Bank Ltd, it can be explained that Big Bank Ltd would be eligible for bringing forward the

requests of gaining the input tax credit. The financial supplies undertaken with the structure of

the “Goods and service tax ruling of GSTR 2006/3” associated with the value that has been

added in the financial supply price undertaken by the bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.