Australian Taxation Law: Case Analysis and Financial Implications

VerifiedAdded on 2019/11/12

|15

|3184

|298

Homework Assignment

AI Summary

This assignment delves into the intricacies of Australian taxation law through a series of case studies. It examines various scenarios, including fringe benefits, capital assets, holiday schemes, club refunds, sports individual payments, building expenditure, short-term courses, employee expenses, and job-seeking travel costs. Each case is analyzed with reference to relevant taxation rulings and legislation, determining whether specific expenses are tax-deductible or considered taxable income. The assignment also includes a calculation of taxable income for an individual, Manpreet, based on various income sources and expenses. The analysis covers key aspects of Australian tax law, providing a comprehensive overview of tax implications in different situations.

Running head: TAXATION LAW OF AUSTRALIA

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW OF AUSTRALIA

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to (i)................................................................................................................................2

Answer to (ii)...............................................................................................................................3

Answer to (iii)..............................................................................................................................3

Answer to (iv)..............................................................................................................................4

Answer to (v)...............................................................................................................................5

Answer to (vi)..............................................................................................................................5

Answer to (vii).............................................................................................................................6

Answer to (viii)............................................................................................................................7

Answer to (ix)..............................................................................................................................8

Answer to (x)...............................................................................................................................8

Answer to Question No 2..............................................................................................................10

Reference List................................................................................................................................13

TAXATION LAW OF AUSTRALIA

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to (i)................................................................................................................................2

Answer to (ii)...............................................................................................................................3

Answer to (iii)..............................................................................................................................3

Answer to (iv)..............................................................................................................................4

Answer to (v)...............................................................................................................................5

Answer to (vi)..............................................................................................................................5

Answer to (vii).............................................................................................................................6

Answer to (viii)............................................................................................................................7

Answer to (ix)..............................................................................................................................8

Answer to (x)...............................................................................................................................8

Answer to Question No 2..............................................................................................................10

Reference List................................................................................................................................13

2

TAXATION LAW OF AUSTRALIA

Answer to Question No 1

Answer to (i)

The condition mainly reveals that there is precise advantages that is given to a business

researcher flyer on a regular basis from Webjet. In general situations, these general advantages

that are given out by the airline organizations are not regarded under the taxable income, which

has been explained by in the Taxation ruling of TR 1999/6. On the other hand, the ruling system

of Australian taxation even explains that there are certain benchmarks requires to be met before

permitting the expenditure bas an exemption of tax1. The general benefit that is given out by

Webjet is not regarded under the head of the Fringe Benefit tax or taxable income until all these

characteristics have been substantiated. There exists a connection among the employee and the

employer when they can be thought as a family2. Furthermore, if the total points of reward are

given to the employees with respect their agreement of employment. Additionally, the points in

respect to flights that have been given by Webjet are within a specific procedure. Conversely, the

assessment of the condition mainly describes that there does not exist any contract among the

Webjet and their employees or with Webjet and the employer, which has openly omitted the

advantages that have been gained from the taxable income.

1McLaverty, Peter, ed. Public participation and innovations in community governance. Taylor &

Francis, 2017.

2Eccleston, Richard, and Timothy Woolley. "From Calgary to Canberra: resource taxation and

fiscal federalism in Canada and Australia." Publius: The Journal of Federalism 45.2 (2014): 216-

243.

TAXATION LAW OF AUSTRALIA

Answer to Question No 1

Answer to (i)

The condition mainly reveals that there is precise advantages that is given to a business

researcher flyer on a regular basis from Webjet. In general situations, these general advantages

that are given out by the airline organizations are not regarded under the taxable income, which

has been explained by in the Taxation ruling of TR 1999/6. On the other hand, the ruling system

of Australian taxation even explains that there are certain benchmarks requires to be met before

permitting the expenditure bas an exemption of tax1. The general benefit that is given out by

Webjet is not regarded under the head of the Fringe Benefit tax or taxable income until all these

characteristics have been substantiated. There exists a connection among the employee and the

employer when they can be thought as a family2. Furthermore, if the total points of reward are

given to the employees with respect their agreement of employment. Additionally, the points in

respect to flights that have been given by Webjet are within a specific procedure. Conversely, the

assessment of the condition mainly describes that there does not exist any contract among the

Webjet and their employees or with Webjet and the employer, which has openly omitted the

advantages that have been gained from the taxable income.

1McLaverty, Peter, ed. Public participation and innovations in community governance. Taylor &

Francis, 2017.

2Eccleston, Richard, and Timothy Woolley. "From Calgary to Canberra: resource taxation and

fiscal federalism in Canada and Australia." Publius: The Journal of Federalism 45.2 (2014): 216-

243.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW OF AUSTRALIA

Answer to (ii)

This condition primarily explains that the authentic remuneration is gained by the

organization from a client for the damages that have taken place in their Capital Asset. With

respect to the taxation law of Australia, the total payment of damage that is undertaken on the

capital assets may not be regarded under the head of the taxable income3. Additionally, there are

distinct principles that requires to be maintained by any firm for not adding in the payment

damage of the capital assets to be their capital income. Primarily, the assets need to be utilised by

the firm in a thorough manner, which may specifically reduce the total income that is taxable.

The next step essentially explains that asset that is in nature capital is sufficiently disclosed in the

financial report where the sufficient amount of depreciation is charged. This aspect has a

significant issue as it permits the authorities of the Taxation Office of Australia in order to gain

knowledge about the fact that capital assets is utilised by the firm for over one taxation year.

Answer to (iii)

This situation primary explains that the precise holiday schemes has been given out to the

manager of the night club by the alcohol supplier. This precise arrangement has primary

described that the advantage or the reward given by the supplier of alcohol has a much increased

value. With respect to the authority of Australian taxation, the lower budget rewards that are

relieved from the taxable income and on the other hand, the gifts that are of high budget are

3Whitty, Jennifer A., and Peter Littlejohns. "Social values and health priority setting in Australia:

an analysis applied to the context of health technology assessment." Health Policy 119.2 (2015):

127-136.

TAXATION LAW OF AUSTRALIA

Answer to (ii)

This condition primarily explains that the authentic remuneration is gained by the

organization from a client for the damages that have taken place in their Capital Asset. With

respect to the taxation law of Australia, the total payment of damage that is undertaken on the

capital assets may not be regarded under the head of the taxable income3. Additionally, there are

distinct principles that requires to be maintained by any firm for not adding in the payment

damage of the capital assets to be their capital income. Primarily, the assets need to be utilised by

the firm in a thorough manner, which may specifically reduce the total income that is taxable.

The next step essentially explains that asset that is in nature capital is sufficiently disclosed in the

financial report where the sufficient amount of depreciation is charged. This aspect has a

significant issue as it permits the authorities of the Taxation Office of Australia in order to gain

knowledge about the fact that capital assets is utilised by the firm for over one taxation year.

Answer to (iii)

This situation primary explains that the precise holiday schemes has been given out to the

manager of the night club by the alcohol supplier. This precise arrangement has primary

described that the advantage or the reward given by the supplier of alcohol has a much increased

value. With respect to the authority of Australian taxation, the lower budget rewards that are

relieved from the taxable income and on the other hand, the gifts that are of high budget are

3Whitty, Jennifer A., and Peter Littlejohns. "Social values and health priority setting in Australia:

an analysis applied to the context of health technology assessment." Health Policy 119.2 (2015):

127-136.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW OF AUSTRALIA

relatively added in to the taxable income4. This primarily aids in decreasing any sort of measures

that are in nature unethical that is undertaken by the employers and the employees. Furthermore,

the situation mainly explains that the holiday scheme has an increased value, where the manager

of the night club requires to bring in the rewards and benefits within his taxable income. The

measures of Australian Taxation Office primarily explains that any rewards that can be regarded

as the cash amount that has been paid to the employees is granted as the taxable value5. It has

been explained that the employees who receives rewards and advantages from their employers

are primarily regarded as the fringe benefit tax, which has been paid by the management or the

employer.

Answer to (iv)

This scenario exclusively explains that precise funds have been returned back to the

members of the Club of Canoe, as the additional funds are gathered. This refund of capital from

the Club of Canoe has been specifically a return and may not be regarded as an earning from the

associates. According to the law of Australian Taxation, any sorts of expenditure undertaken on

the clubs for the individual entertainment are not in nature deductible6. Hence, the total return

4James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom." eJournal of Tax Research 13.1

(2015): 280.

5Moretto, Nicole, et al. "Yes, the government should tax soft drinks: findings from a citizens’

jury in Australia." International journal of environmental research and public health 11.3 (2014):

2456-2471.

6Castro, Gerardo Ángeles, and Diana Berenice Ramírez Camarillo. "Determinants of tax revenue in OECD countries

over the period 2001–2011." Contaduría y administración 59.3 (2014): 35-59.

TAXATION LAW OF AUSTRALIA

relatively added in to the taxable income4. This primarily aids in decreasing any sort of measures

that are in nature unethical that is undertaken by the employers and the employees. Furthermore,

the situation mainly explains that the holiday scheme has an increased value, where the manager

of the night club requires to bring in the rewards and benefits within his taxable income. The

measures of Australian Taxation Office primarily explains that any rewards that can be regarded

as the cash amount that has been paid to the employees is granted as the taxable value5. It has

been explained that the employees who receives rewards and advantages from their employers

are primarily regarded as the fringe benefit tax, which has been paid by the management or the

employer.

Answer to (iv)

This scenario exclusively explains that precise funds have been returned back to the

members of the Club of Canoe, as the additional funds are gathered. This refund of capital from

the Club of Canoe has been specifically a return and may not be regarded as an earning from the

associates. According to the law of Australian Taxation, any sorts of expenditure undertaken on

the clubs for the individual entertainment are not in nature deductible6. Hence, the total return

4James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom." eJournal of Tax Research 13.1

(2015): 280.

5Moretto, Nicole, et al. "Yes, the government should tax soft drinks: findings from a citizens’

jury in Australia." International journal of environmental research and public health 11.3 (2014):

2456-2471.

6Castro, Gerardo Ángeles, and Diana Berenice Ramírez Camarillo. "Determinants of tax revenue in OECD countries

over the period 2001–2011." Contaduría y administración 59.3 (2014): 35-59.

5

TAXATION LAW OF AUSTRALIA

from the funds may not be revealed as an extra revenue that is attained by the associates of the

Canoe Club. Hence, keeping in line with the Australian law of taxation, the fund return may be

exempted under the income that can be taxable from the associates of the Canoe Club.

Answer to (v)

The television organisation has paid directly to a sports individual for partaking in the

field of sports, under the situation that the sports individual is accountable to bring in wealth in

their income that is taxable. The condition is primarily explained by considering the “Taxation

Ruling TR 1999/17”, in which it has been explained that several of advantages received from the

perspective of a sports individual has to bring in the advantages that have been given out by the

television organization in its taxable income and the precise entry to the government of

Australia7. It is seen that measures of taxation is primarily exploited in decreasing any sort of

unprincipled measures that has been undertaken by an employee in order to decrease the taxable

income.

Answer to (vi)

This scenario primarily explains the total expenditure that has been undertaken in the

building, where the authentic expenditure is regarded from the perspective of the apprentice.

With respect to the taxation law of Australia, the scenario primarily explains that the novice is

directly considered under the compensation of building labour. The actions utilised in

recognising the expenditure of the building are disclosed in regards to “Taxation Ruling TR

95/22”, where precise compensation and expenditure are directly disclosed. In accordance to the

taxation rule, authentic expenditure requires to be regarded before recognising the apprentice as

an employee of the building. The primary action mainly explains that the site of the building is

7Boll, Karen. "Shady car dealings and taxing work practices: An ethnography of a tax audit process." Accounting,

Organizations and Society 39.1 (2014): 1-19.

TAXATION LAW OF AUSTRALIA

from the funds may not be revealed as an extra revenue that is attained by the associates of the

Canoe Club. Hence, keeping in line with the Australian law of taxation, the fund return may be

exempted under the income that can be taxable from the associates of the Canoe Club.

Answer to (v)

The television organisation has paid directly to a sports individual for partaking in the

field of sports, under the situation that the sports individual is accountable to bring in wealth in

their income that is taxable. The condition is primarily explained by considering the “Taxation

Ruling TR 1999/17”, in which it has been explained that several of advantages received from the

perspective of a sports individual has to bring in the advantages that have been given out by the

television organization in its taxable income and the precise entry to the government of

Australia7. It is seen that measures of taxation is primarily exploited in decreasing any sort of

unprincipled measures that has been undertaken by an employee in order to decrease the taxable

income.

Answer to (vi)

This scenario primarily explains the total expenditure that has been undertaken in the

building, where the authentic expenditure is regarded from the perspective of the apprentice.

With respect to the taxation law of Australia, the scenario primarily explains that the novice is

directly considered under the compensation of building labour. The actions utilised in

recognising the expenditure of the building are disclosed in regards to “Taxation Ruling TR

95/22”, where precise compensation and expenditure are directly disclosed. In accordance to the

taxation rule, authentic expenditure requires to be regarded before recognising the apprentice as

an employee of the building. The primary action mainly explains that the site of the building is

7Boll, Karen. "Shady car dealings and taxing work practices: An ethnography of a tax audit process." Accounting,

Organizations and Society 39.1 (2014): 1-19.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW OF AUSTRALIA

regarded when the work of a supervisor is being undertaken within the premises8. The next

action explains that the labours used for the construction of the premises is taken as an employee.

The last action explains that effective carpenters, apprentices and employees are granted under

the working labours. Furthermore, the building site is even regarded where the project manager

is used for the conducting and concluding the precise actions for the building construction.

Hence, from the assessment it can be explained that the expenditure undertaken on the apprentice

is regarded as a compensation of the labour for the building and can be subtracted from the

annual report.

Answer to (vii)

Expenditure has been undertaken on the course of the term that is short for being a

director of rule art, which has an effective establishment in the taxation office of Australia. The

diminutive progress that is utilised by a person in order to develop their career during the short

term span is mainly regarded to be an expenditure that is in nature tax deductible. This kind of

expenditure that are tax deductible is only taken when the courses of the study is diminutive and

for courses that are long term there is no exemption in the taxable income. Furthermore, precise

actions as revealed by the Australian Taxation Office requires to be assessed by the taxable

individual. Then it has been an immaterial module of education and the software course.

Furthermore, the course fees requires to be of a shorter period have authentic travelling expenses

and meals that requires to be included. These actions are given out by the Australian taxation

Office requires to be assessed before making use of the courses that are short term, as an

8Smith, Julie P. "Inquiry into the Tax Expenditures Statement (TES)." (2015).

TAXATION LAW OF AUSTRALIA

regarded when the work of a supervisor is being undertaken within the premises8. The next

action explains that the labours used for the construction of the premises is taken as an employee.

The last action explains that effective carpenters, apprentices and employees are granted under

the working labours. Furthermore, the building site is even regarded where the project manager

is used for the conducting and concluding the precise actions for the building construction.

Hence, from the assessment it can be explained that the expenditure undertaken on the apprentice

is regarded as a compensation of the labour for the building and can be subtracted from the

annual report.

Answer to (vii)

Expenditure has been undertaken on the course of the term that is short for being a

director of rule art, which has an effective establishment in the taxation office of Australia. The

diminutive progress that is utilised by a person in order to develop their career during the short

term span is mainly regarded to be an expenditure that is in nature tax deductible. This kind of

expenditure that are tax deductible is only taken when the courses of the study is diminutive and

for courses that are long term there is no exemption in the taxable income. Furthermore, precise

actions as revealed by the Australian Taxation Office requires to be assessed by the taxable

individual. Then it has been an immaterial module of education and the software course.

Furthermore, the course fees requires to be of a shorter period have authentic travelling expenses

and meals that requires to be included. These actions are given out by the Australian taxation

Office requires to be assessed before making use of the courses that are short term, as an

8Smith, Julie P. "Inquiry into the Tax Expenditures Statement (TES)." (2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW OF AUSTRALIA

expenditure that is tax deductible9. Hence, the precise deduction of tax is undertaken by the art

director, which aids in lowering the taxable income.

Answer to (viii)

There is actual expenditure undertaken on the dresses and the makeups on an employee,

which is by nature deductible as explained by the Taxation Office of Australia. Conversely, there

exists a specific standard that requires being gratified prior to permitting the expenditure that is

to be tax deductible. The expenditure make on dresses and the make up for the stage artists are

primarily in a way deductible10. Furthermore, the artist who is performing is regarded to be a

circus performer,magician, actor, singer, dancer and numerous artist. Any sort of expenditure

undertaken on these employees is regarded to be expenditure for tax deduction. Hence, the

situation explains that the actual expenditure are taken on the dresses and the makeups and no

provisions has been given with respect to who the expenditure has been undertaken. Therefore,

the assumptions that are precise are undertaken that the expenses are undertaken on the artists,

which can be deductible from the taxable income and permits the employees to decrease the tax

that is payable.

9Hoffman, William H., and James E. Smith. South-Western Federal Taxation 2015: Individual

Income Taxes. Cengage Learning, 2014.

10Lal, Anita, et al. "Modelled health benefits of a sugar-sweetened beverage tax across different

socioeconomic groups in Australia: A cost-effectiveness and equity analysis." PLoS

medicine 14.6 (2017): e1002326.

TAXATION LAW OF AUSTRALIA

expenditure that is tax deductible9. Hence, the precise deduction of tax is undertaken by the art

director, which aids in lowering the taxable income.

Answer to (viii)

There is actual expenditure undertaken on the dresses and the makeups on an employee,

which is by nature deductible as explained by the Taxation Office of Australia. Conversely, there

exists a specific standard that requires being gratified prior to permitting the expenditure that is

to be tax deductible. The expenditure make on dresses and the make up for the stage artists are

primarily in a way deductible10. Furthermore, the artist who is performing is regarded to be a

circus performer,magician, actor, singer, dancer and numerous artist. Any sort of expenditure

undertaken on these employees is regarded to be expenditure for tax deduction. Hence, the

situation explains that the actual expenditure are taken on the dresses and the makeups and no

provisions has been given with respect to who the expenditure has been undertaken. Therefore,

the assumptions that are precise are undertaken that the expenses are undertaken on the artists,

which can be deductible from the taxable income and permits the employees to decrease the tax

that is payable.

9Hoffman, William H., and James E. Smith. South-Western Federal Taxation 2015: Individual

Income Taxes. Cengage Learning, 2014.

10Lal, Anita, et al. "Modelled health benefits of a sugar-sweetened beverage tax across different

socioeconomic groups in Australia: A cost-effectiveness and equity analysis." PLoS

medicine 14.6 (2017): e1002326.

8

TAXATION LAW OF AUSTRALIA

Answer to (ix)

The expenditure undertaken by the consumers by going from home to the workplace.

This has been regraded to be an operation of the work. Conversely, there is no precise proof

provided in this instance, that may assist in recognising the validity, from which expenditure are

undertaken for workplace intentions. The taxation office of Australia primarily explains that

certain sort of expenditure undertaken by a person for official functions is in a way deductible

under the law of taxation in the specific situation11. Hence, persons require recognising the

motive behind the expense before making use of the taxable deductions. It has been cited that

without sufficient supervision there is no direction where the government could recognise the

expenditure faced by a person in the file of income tax12. Therefore, it can be explained that if the

expenditure undertaken for the purpose of office then it can be subtracted from the taxable

income. Furthermore, it would not decrease if the expenditure are undertaken for any personal

purpose.

Answer to (x)

This scenario primarily explains that the precise expenditure that are undertaken by a

person from roaming to one employee to the other. This primarily describes that the person is

using personal expenditure and undertaking travels from one place to the other in order to look

11Comans, Tracy A., et al. "The cost-effectiveness and consumer acceptability of taxation

strategies to reduce rates of overweight and obesity among children in Australia: study

protocol." BMC public health 13.1 (2013): 1182.

12Mytton, Oliver T., Helen Eyles, and David Ogilvie. "Evaluating the health impacts of food and

beverage taxes." Current obesity reports 3.4 (2014): 432-439.

TAXATION LAW OF AUSTRALIA

Answer to (ix)

The expenditure undertaken by the consumers by going from home to the workplace.

This has been regraded to be an operation of the work. Conversely, there is no precise proof

provided in this instance, that may assist in recognising the validity, from which expenditure are

undertaken for workplace intentions. The taxation office of Australia primarily explains that

certain sort of expenditure undertaken by a person for official functions is in a way deductible

under the law of taxation in the specific situation11. Hence, persons require recognising the

motive behind the expense before making use of the taxable deductions. It has been cited that

without sufficient supervision there is no direction where the government could recognise the

expenditure faced by a person in the file of income tax12. Therefore, it can be explained that if the

expenditure undertaken for the purpose of office then it can be subtracted from the taxable

income. Furthermore, it would not decrease if the expenditure are undertaken for any personal

purpose.

Answer to (x)

This scenario primarily explains that the precise expenditure that are undertaken by a

person from roaming to one employee to the other. This primarily describes that the person is

using personal expenditure and undertaking travels from one place to the other in order to look

11Comans, Tracy A., et al. "The cost-effectiveness and consumer acceptability of taxation

strategies to reduce rates of overweight and obesity among children in Australia: study

protocol." BMC public health 13.1 (2013): 1182.

12Mytton, Oliver T., Helen Eyles, and David Ogilvie. "Evaluating the health impacts of food and

beverage taxes." Current obesity reports 3.4 (2014): 432-439.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW OF AUSTRALIA

for jobs as a person cannot work in two organizations. Hence, it can be perceived that this kind

of travelling expenses is an individual endeavour, which may not be subtracted from the income

that is taxable. With respect to the taxation law of Australia, individual does not subtract the

expenditure from their income that is taxable. It has been13 explained that by taking assistance of

the laws that have been laid down by the authorities of Australian Taxation, the government of

Australia has the power to primarily decrease the total evasion of tax undertaken by a person.

Hence, it can be explained that the expenditure undertaken by the person by transporting from

one worker to the other is not deductible in nature that may not decrease their total income

amount that is taxable.

Answer to Question No 2

Taxable Income for the financial year 2016/17 of Manpreet

13Austin, Patricia M., Nicole Gurran, and Christine ME Whitehead. "Planning and affordable

housing in Australia, New Zealand and England: common culture; different

mechanisms." Journal of Housing and the Built Environment29.3 (2014): 455-472.

TAXATION LAW OF AUSTRALIA

for jobs as a person cannot work in two organizations. Hence, it can be perceived that this kind

of travelling expenses is an individual endeavour, which may not be subtracted from the income

that is taxable. With respect to the taxation law of Australia, individual does not subtract the

expenditure from their income that is taxable. It has been13 explained that by taking assistance of

the laws that have been laid down by the authorities of Australian Taxation, the government of

Australia has the power to primarily decrease the total evasion of tax undertaken by a person.

Hence, it can be explained that the expenditure undertaken by the person by transporting from

one worker to the other is not deductible in nature that may not decrease their total income

amount that is taxable.

Answer to Question No 2

Taxable Income for the financial year 2016/17 of Manpreet

13Austin, Patricia M., Nicole Gurran, and Christine ME Whitehead. "Planning and affordable

housing in Australia, New Zealand and England: common culture; different

mechanisms." Journal of Housing and the Built Environment29.3 (2014): 455-472.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW OF AUSTRALIA

Particulars Amount Amount

Gross Salary 45,000.00

Foreign Income

Income From Trust 10,000.00

Total Income 55,000.00

Deductions

Purchase of mobile work purpose 500.00

Total Deductions 500.00

Taxable Income 54,500.00

Total tax 9,259.50

Low income tax offset 182.50

Medicare Levy 1,090.00

Tax Payable 10,167.00

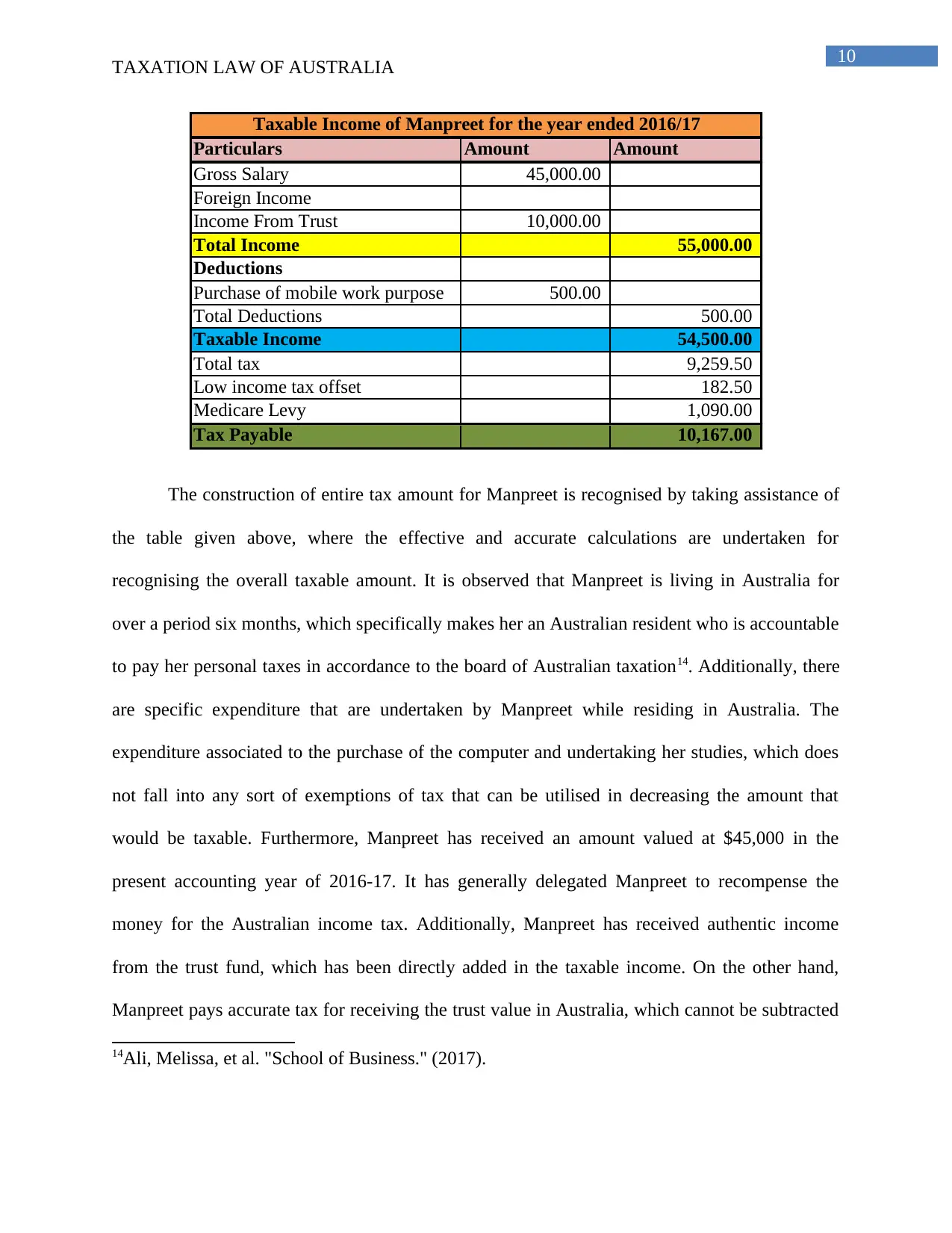

Taxable Income of Manpreet for the year ended 2016/17

The construction of entire tax amount for Manpreet is recognised by taking assistance of

the table given above, where the effective and accurate calculations are undertaken for

recognising the overall taxable amount. It is observed that Manpreet is living in Australia for

over a period six months, which specifically makes her an Australian resident who is accountable

to pay her personal taxes in accordance to the board of Australian taxation14. Additionally, there

are specific expenditure that are undertaken by Manpreet while residing in Australia. The

expenditure associated to the purchase of the computer and undertaking her studies, which does

not fall into any sort of exemptions of tax that can be utilised in decreasing the amount that

would be taxable. Furthermore, Manpreet has received an amount valued at $45,000 in the

present accounting year of 2016-17. It has generally delegated Manpreet to recompense the

money for the Australian income tax. Additionally, Manpreet has received authentic income

from the trust fund, which has been directly added in the taxable income. On the other hand,

Manpreet pays accurate tax for receiving the trust value in Australia, which cannot be subtracted

14Ali, Melissa, et al. "School of Business." (2017).

TAXATION LAW OF AUSTRALIA

Particulars Amount Amount

Gross Salary 45,000.00

Foreign Income

Income From Trust 10,000.00

Total Income 55,000.00

Deductions

Purchase of mobile work purpose 500.00

Total Deductions 500.00

Taxable Income 54,500.00

Total tax 9,259.50

Low income tax offset 182.50

Medicare Levy 1,090.00

Tax Payable 10,167.00

Taxable Income of Manpreet for the year ended 2016/17

The construction of entire tax amount for Manpreet is recognised by taking assistance of

the table given above, where the effective and accurate calculations are undertaken for

recognising the overall taxable amount. It is observed that Manpreet is living in Australia for

over a period six months, which specifically makes her an Australian resident who is accountable

to pay her personal taxes in accordance to the board of Australian taxation14. Additionally, there

are specific expenditure that are undertaken by Manpreet while residing in Australia. The

expenditure associated to the purchase of the computer and undertaking her studies, which does

not fall into any sort of exemptions of tax that can be utilised in decreasing the amount that

would be taxable. Furthermore, Manpreet has received an amount valued at $45,000 in the

present accounting year of 2016-17. It has generally delegated Manpreet to recompense the

money for the Australian income tax. Additionally, Manpreet has received authentic income

from the trust fund, which has been directly added in the taxable income. On the other hand,

Manpreet pays accurate tax for receiving the trust value in Australia, which cannot be subtracted

14Ali, Melissa, et al. "School of Business." (2017).

11

TAXATION LAW OF AUSTRALIA

with respect to the process used by the Australian taxation15. This is primarily due to the fact that

there is no contract among India and Australia, where the process of taxation that would be done

twice may be restricted by the residents. The exclusive deduction which is permitted in the value

that is taxable has been acquisition of a firsthand mobile phone that has been purchased due to

official intention.

It has been observed that “Section 8-1 of the Income tax Assessment Act” primarily

directs in recognising the real income that would be taxable for Manpreet, which requires to

paying out towards the government of Australia. Furthermore, there are cases like the “Lunnev

vs. FC of T; Hayley vs. FC of T (1958) 100 CLR 478; (1958)”, “Ronpibon Tin NL vs. FC of T

(1949)” and “FC of T vs. M I Roberts 92 ATC 4787” can be cited as instances for recognising

the real income that would be taxable to Manpreet. These instances even aids in determining into

the entire rules of taxation that the Australian government follows and the precise rectifications

that requires to be undertaken in the amount that is taxable. Furthermore, medical levy and lower

income tax for the state is even utilised in the computation of the over tax that has to be paid to

Manpreet, which has been disclosed promptly in the website of the Australian Taxation Office.

Hence the medical levy is included into the amount of the income tax, while the offset of the low

income tax is subtracted from the amount that can be taxed16. This primarily permits the

15Evans, Chris, Phil Lignier, and Binh Tran-Nam. "Tax compliance costs for the small and

medium enterprise business sector: Recent evidence from Australia." Tax Administration

Research Centre University of EXETER Discussion Paper (2013): 003-13.

16Farmer, Clare. "‘Is a 24-hour ban such a bad thing?’Police-imposed banning notices:

compatible with human rights or a diminution of due process?." Australian Journal of Human

Rights 20.2 (2014): 39-61.

TAXATION LAW OF AUSTRALIA

with respect to the process used by the Australian taxation15. This is primarily due to the fact that

there is no contract among India and Australia, where the process of taxation that would be done

twice may be restricted by the residents. The exclusive deduction which is permitted in the value

that is taxable has been acquisition of a firsthand mobile phone that has been purchased due to

official intention.

It has been observed that “Section 8-1 of the Income tax Assessment Act” primarily

directs in recognising the real income that would be taxable for Manpreet, which requires to

paying out towards the government of Australia. Furthermore, there are cases like the “Lunnev

vs. FC of T; Hayley vs. FC of T (1958) 100 CLR 478; (1958)”, “Ronpibon Tin NL vs. FC of T

(1949)” and “FC of T vs. M I Roberts 92 ATC 4787” can be cited as instances for recognising

the real income that would be taxable to Manpreet. These instances even aids in determining into

the entire rules of taxation that the Australian government follows and the precise rectifications

that requires to be undertaken in the amount that is taxable. Furthermore, medical levy and lower

income tax for the state is even utilised in the computation of the over tax that has to be paid to

Manpreet, which has been disclosed promptly in the website of the Australian Taxation Office.

Hence the medical levy is included into the amount of the income tax, while the offset of the low

income tax is subtracted from the amount that can be taxed16. This primarily permits the

15Evans, Chris, Phil Lignier, and Binh Tran-Nam. "Tax compliance costs for the small and

medium enterprise business sector: Recent evidence from Australia." Tax Administration

Research Centre University of EXETER Discussion Paper (2013): 003-13.

16Farmer, Clare. "‘Is a 24-hour ban such a bad thing?’Police-imposed banning notices:

compatible with human rights or a diminution of due process?." Australian Journal of Human

Rights 20.2 (2014): 39-61.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.